It’s time to dive deep into the world of AI, specifically Palantir Technologies (PLTR). A once shadowy figure in the realm of data mining and artificial intelligence, Palantir emerged from the shadows after its 2020 IPO.

The company, which had been cutting its teeth on intelligence agency contracts, suddenly found itself in the investor spotlight.

However, it wasn’t all smooth sailing. The stock, once a darling of the market, faced a rough patch in 2021 and 2022, plummeting by a staggering 84%.

But let's fast-forward to 2023.

Palantir is making a comeback, thanks to the surging interest in generative AI. The company's market cap stands at $42 billion, and while it might seem like a leap to imagine it hitting the $1 trillion mark, it's never too early to speculate on long-term performance.

Let’s revisit the company’s roots for a moment.

Founded in 2003, in the wake of the 9/11 attacks, Palantir's raison d'être was to create algorithms that could comb through vast amounts of data to detect potential security threats.

They crafted algorithms that were nothing short of digital sleuths. These clever bits of code were unleashed into the labyrinth of U.S. intelligence, defense, and law enforcement databases.

Their mission? To ferret out the subtle, seemingly harmless details – think a lone plane ticket, a string of rented properties, frequent calls to the Middle East, or hefty withdrawals from an overseas bank.

Isolated, these bits are innocuous. But stitch them together, and you've got the makings of a potential terrorist plot. It’s like finding a needle in a haystack, except Palantir built a magnet.

Now, in the present day, Palantir’s algorithms have evolved. They’re being retooled for the commercial world, helping businesses forecast customer behavior, optimize resource management, and enhance data-driven decision-making.

The arrival of generative AI platforms, like ChatGPT, has transformed the AI landscape. These systems, capable of summarizing data, generating original content, and boosting business productivity, have opened new doors.

Palantir, with its rich history in AI, was quick to adapt, developing tools to meet these burgeoning business needs.

Considering the AI market potential, which ranges from a jaw-dropping $14 trillion by 2030 to more conservative, yet still impressive, estimates of $6 to $7 trillion, Palantir is positioned to make significant strides. Its expertise could be the key to unlocking a share of this lucrative market.

Palantir’s recent performance has been solid, with a 17% year-over-year revenue growth in the third quarter, amounting to $558 million. Its commercial revenue outpaced government sales, and the company recorded its fourth consecutive quarter of GAAP profits.

With a projected full-year revenue of $2.2 billion and a total addressable market now estimated at a whopping $800 billion (thanks to generative AI), Palantir's future looks promising.

Capturing just 7% of this market annually could skyrocket Palantir's revenue to $56 billion over the next decade. This growth, coupled with an operating margin of 25%, could translate into approximately $14 billion in operating profits.

As enticing as these numbers are, achieving a trillion-dollar valuation isn’t a walk in the park.

Palantir’s journey to this milestone will require sustained innovation, market adaptation, and perhaps a bit of luck. The company's two-decade expertise gives it a significant advantage over its neophyte rivals, but the path is fraught with challenges.

Management’s recent shareholder letter expressed an unprecedented demand for their AI platform, a testament to the company's growing influence in this domain.

The convergence of opportunity and expertise could very well propel Palantir to that elusive trillion-dollar valuation over the next decade.

So, what does the future hold for Palantir?

Palantir Technologies, riding the AI wave, is positioned similarly to how Amazon Web Services revolutionized computing. With AI and big data becoming increasingly pivotal, Palantir stands to benefit significantly from these trends.

Will Palantir join the ranks of the trillion-dollar giants?

While the road is long and uncertain, the potential is undeniably there. For forward-looking investors, Palantir isn’t just a company to watch; it’s a gateway to the ever-evolving and exciting world of AI and big data.

Buying the dip could be a strategic move for those willing to invest in a future shaped by AI innovations.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/12/Screenshot-2023-12-11-155416.jpg739739Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2023-12-11 16:00:232023-12-11 16:00:23CLAIMING A CROWN IN THE AI KINGDOM

In prior years, big social media companies were the class of the tech industry.

It’s not so much like that today but they still have highly profitable models and a lot of juice left in the tank.

I do believe big social media companies will still do well in 2024 because they have proved themselves through the test of time.

However, now that media has fragmented, smaller social media stocks that are tailored to a certain niche are due to overperform in 2024.

This is happening at a time when cord-cutting is accelerating and the lowering of interest rates next year could serve as a catalyst to higher share prices for the likes of Snap and Pinterest.

Then there is the wider trend of potential beneficiaries from a recovery in the digital advertising market.

As marketing clients look to redeploy their dollars following post-pandemic cutbacks, stocks such as Snap and Pinterest could be next in line for a payday.

For Pinterest, I have been highly bullish on them ever since Elliot Management scooped them up and revamped management.

Snap is in the sweet spot catering to a growing demographic who are seeing their earning power rise as they come of age.

Still, the industry faces risks given an uncertain economic backdrop.

I anticipate higher ad sales of online retail platforms that will jump 20% versus last year. Moreover, online ad growth should accelerate meaningfully in 2024.

I believe the media will obtain about $17 billion in political ads next year when many U.S. campaigns will be in full swing.

It’s hard not to see social media stocks winning out in a presidential election year in one of the most polarizing contests in recent memory.

More and more consumers spend most of their days online and most of those funds likely will be spent on digital platforms where these consumers station eyeballs.

And worldwide, ad spending is expected to jump 8.2% next year, a sharp acceleration from the 4.4% gain anticipated this year.

Marketers spend money on platforms in direct proportion to the number of users that they attract.

Digital platforms, which include search, social, commerce, retail media, and digital video platforms, will account for about 64% of all advertising in 2023.

Digital platform-focused companies are expected to collectively grow 11%, led in large part by retail media, which will account for about $42 billion in advertising revenue in 2023, up 20% over 2022.

Traditional television, both national and local, will experience declines over the year.

The setup is boding nicely for these smaller social media stocks and that is not to say stocks like Meta and Google will perform poorly.

Realistically, the Nasdaq can’t move higher without the Magnificent 7, but based on pure percentage gains, I do believe Snap and Pinterest have a good chance to beat out the heavyweights next year.

There is a high likelihood that tech will lead this next bull market because they are the largest winner from the lowering of interest rates.

Not only will tech IPOs be back in vogue, but the prototypical tech zombie firms that burn cash will pop up again showing that investors reserve large amounts of capital for potential tech growth companies.

Part of the capital allocation will be to Snap and Pins which are solid companies with a great brand image.

I believe 2024 will be a year where investors pile into these 2 stocks much like how investors piled into Uber in 2023.

(A WEAK U.S. DOLLAR CREATES RIPPLE EFFECTS ACROSS THE WORLD)

December 11, 2023

Hello everyone,

Economic Calendar for the week ahead.

Monday December 11, 2023

Australia Consumer Confidence change

Previous:2.6%

Time: 6.30 pm ET

Tuesday, December 12, 2023

US Core Inflation Rate

Previous: 4.0%

Time: 8:30 am ET

Wednesday, December 13, 2023

US Interest Rate Decision

Previous: 5.5%

Time: 2:00 pm ET

Thursday December 14, 2023

ECB Interest Rate Decision

Previous: 4.5%

Time 8:15 am ET

Friday December 15, 2023

EA Manufacturing PMI

Previous: 44.2

Time: 4:00 am ET

A weak U.S. dollar has ramifications for investors across the world.

The dollar index measures the US dollar’s value against a basket of six key currencies: the euro, the Japanese yen, the pound sterling, the Canadian dollar, the Swedish krona, and the Swiss franc.

The dollar normally rises when the US Federal Reserve raises interest rates (which it has been doing over the past 18 months) as overseas investors flock to US bonds because of the higher yields that they offer.Now the greenback is overvalued.The US dollar could still rise for the next few months, but by this time next year, it will be lower than where it is now.

As the US dollar is the world’s reserve currency, it is important for a lot of financial products.

So, if it weakens, how does it affect these products?

Commodities

Assets that are denominated in US dollars should do well if the dollar weakens. In other words, if the denominator gets smaller, the price goes higher. A weak US dollar makes dollar-denominated assets cheaper to buy with other currencies.

This should make commodities attractive:all the main raw materials are priced in US dollars, except for cocoa, which is priced in sterling.You could play this through a broad commodity exchange-traded fund (ETF) such as the Wisdom-Tree Enhanced Commodity ETF.

Within commodities, gold is likely to be the biggest winner – it hit a record high of over $2,100 last week, at which point it had climbed 16% in the space of two months.

Gold is benefiting from several different trends:US dollar weakness, central banks buying bullion, expectations that real interest rates will fall, and geopolitical turmoil.If an investor expects the US dollar to weaken then gold is a good asset in which to take a position.

Consider the iShares Physical Gold exchange-traded commodity (ETC) or the Invesco Physical Gold ETC.

Emerging Markets

Historically, when the dollar has been strong, the stock markets of emerging countries have performed worse than developed markets.These periods occurred between 1995 and 2000, and 2012 and 2015.

By contrast, emerging market equities performed well between 2003 and 2007, 2009 and 2012, and 2017 and 2018 – periods when the dollar was weak.

The reason is that many developing nations borrow in US dollars, so weakness in their currency relative to the dollar means it’s more expensive to afford the interest on that debt and to repay their loans.

The opposite is also true; if the dollar is weak relative to their currency, it is cheaper for them to borrow and service their debts.

You could consider a cheap index-tracking fund to take advantage of this, such as the iShares Core MSCI EM IMI ETF or the Fidelity Index Emerging Markets fund.

How does a weak dollar influence the movement of stocks?

When the dollar is weakening it tends to mean that global economic growth and, consequently, risk appetite are strong.This can be positive for equities.

A weaker dollar means that it’s cheaper for non-US companies with US supply chains to import goods.It also means that US exporters’ goods and services are cheaper for overseas customers to buy.

But a weaker dollar can also have a negative impact on companies that sell a lot of goods and services to Americans because those US earnings become worth less when converted back to their base currency.

If you own shares in an ETF that tracks the performance of America’s S&P 500, a weak dollar relative to the pound, for example, will affect your returns.

In the long term, these peaks and troughs tend to even out.In the past five years, the Vanguard S&P500 ETF is up 81.5% in US dollar terms and has gained 83.3% in sterling terms.

With almost all economic data now universally slowing, Fed Governor Jay Powell is limbering up to take his victory lap. That’s put inflation in full retreat and well on its way to our central bank’s 2% target by summer. Interest rate cuts are just a matter of time.

That sets up a fabulous year in 2024. While this year was mostly a hard slog, next year should be a piece of cake. I can’t wait until it starts!

That puts my 4,800 target for the end of 2023 well within range. People told me I was crazy when I made such an outlandish forecast last January 1, yet here we are.

Investors missed the mark by a mile this year because they thought the Fed's extreme moves in interest rates would trigger a recession.

It didn’t.

Those who bet on falling inflation this year were big winners. That gave the Fed permission to cancel any further rate rises. Economists were too bearish and the technical picture flipped from bearish to bullish in a heartbeat on October 26.

The kinds of moves you are seeing in the stock market, with banks and industrials turning upward, signal that we are not in a bear market, but the start of a new long-term bull one.

Stocks are looking for at least 15% gains in 2024 with earnings consistently surprising to the upside. Domestics will catch fire in the second half. Inflation will fall further than expected, well into the 2% handle, thanks to hyperaccelerating technology crushing prices.

The Fed has won the war on inflation so there is room for 10-year US Treasury bond yields to hit 3.0% next year, taking mortgage interest rates under 5.0%. That will be a shot of adrenaline for the residential real estate market.

A (SPY) target of 5,500 by the end of 2024 is entirely within reason.

It turns out that when ten-year bond yields are between 4.00% and 5.00%, stocks sport a price-earnings multiple of 20X. That allows S&P 500 earnings to hit $2.65 per share in 2025, up from today’s $2.20.

Financials (JPM), industrials (CAT), energy (XOM), and small caps (IWM) will take over market leadership sometime in 2024. The best market risk reward is here. Financials now trading in the dumps have huge multiple expansion potential.

The $240 billion in cash that left equities in 2023 will have to fight their way back in. That’s why we haven’t seen any substantial pullbacks in share prices since October. Once investors got the cash weightings they were happy with, they could never get back into stocks.

Hedge fund equity weightings are at five-year lows. Small caps have very heavy weightings in regional banks, while large banks have great capital spending plays.

Big techs, the meteoric performers of 2023, will likely take a rest sometime in Q1.

Europe and China took the big hits this year, but we didn’t. If they turn around, it will supercharge our economy….and the stock market.

Which brings me to the subject of bank stocks. Banks have had an atrocious 2023, when their shares were either flat or down big, underperforming the S&P 500 by a massive 30%. However, they are looking pretty darn attractive for 2024.

Banks now offer pretty cheap balance sheets relative to next year’s profit outlook, with many still trading at big discounts to book value. A recovering economy means new capital spending jumps, which is great for big banks. Exposure to high-risk office loans which get so much print from the financial media account for less than 5% of their loan books.

Small banks will put the March crisis behind them by recapitalizing or merging. It turns out that only a handful of banks were badly managed (no downside hedge on (TLT) holdings while they were crashing from $166 to $82!!). The survivors will build market share at higher margins.

Economic recovery also means default rates on loans ebb.

Goldman Sachs (GS) is my top pick, after being taken to the woodshed for a very expensive unwind of their poorly thought-out consumer business this year. Key Corp (KEY) is also looking good on a possible 70% earnings growth.

If you are looking for a pure small bank play, you can buy Webster Financial (WBS) based in Stamford, CT, Columbia Banking (COLB) of Tacoma, WA, or Pinnacle Financial (PNFP) from Nashville, TN.

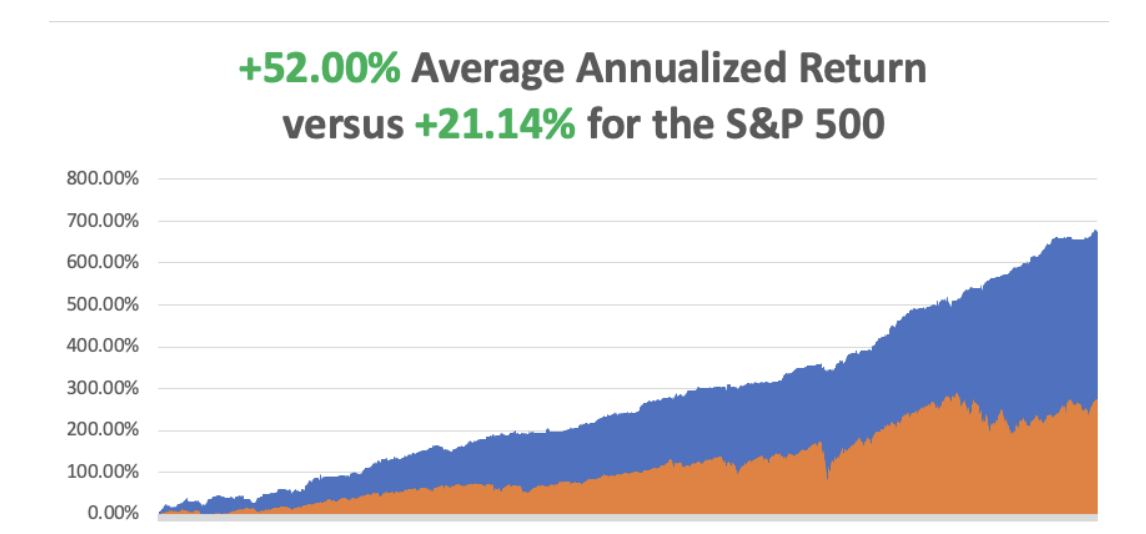

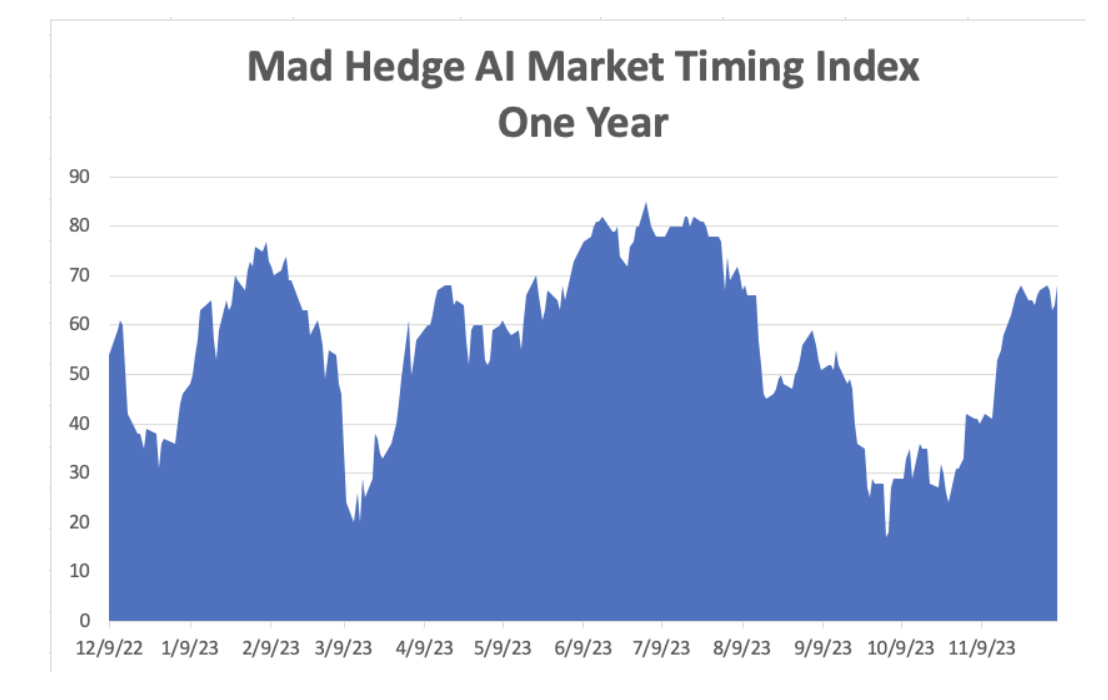

So far in December, we are down -2.85%. We’ve had a heck of a run and the market was bound to bite back sometime. My 2023 year-to-date performance is still at an eye-popping +78.86%.The S&P 500 (SPY) is up +21.05%so far in 2023. My trailing one-year return reached +75.38% versus +24.75% for the S&P 500.

That brings my 15-year total return to +676.05%. My average annualized return has exploded to +52.00%,another new high.

I am 40% invested with 60% in cash, with longs in (NLY), (BRK/B), (GOOGL), and (CAT). Last week, I got stopped out of a long in (XOM), thanks to the oil price dive, and a short in (TLT).

Some 63 of my 70 trades this year have been profitable this year.

Nonfarm Payroll Comes in Soft, in November at 199,000. The headline Unemployment Rate fell to 3.7%, near a 50-year low. Healthcare was the biggest growth industry, adding 77,000. Other big gainers included government (49,000), manufacturing (28,000), and leisure and hospitality (40,000). Average hourly earnings, a key inflation indicator, increased by 0.4% for the month and 4% from a year ago, close to expectations. It was a Goldilocks number for the Fed.

Refi Demand Rockets, as interest rates plunge to four-month lows. The rate for the popular 30-year mortgage fell back toward 7% after hitting 8% earlier this fall. Applications to refinance a home loan index increased 14% from the previous week and were 10% higher than the same week a year ago.

Exploding Sales of EVs Are Ringing the Bell for Oil, leading forecasters to speed up their projections for when global oil use will peak, as public subsidies and improved technology help consumers overcome the sometimes eye-popping sticker prices for battery-powered cars.

Panic Buying Drives Treasury Yields to 4.10%, down nearly a full percentage point in little more than a month on weakening economic data. It’s hard to believe that we drop below 4.10% but anything is possible in this market.

Uber Entered S&P 500, on December 18, taking the stock up 10% on the news. A company needs to fulfill certain criteria to be included in the S&P 500. Firstly, its market capitalization should be at least $14.5 billion. As of Dec 1, 2023, the market capitalization of UBER was $118.02 billion. Additionally, U.S. firms that meet profitability, liquidity, and share-float standards are the ones that can qualify for the S&P 500.

Pending Home Sales Collapse, dropping to the lowest level since the National Association of Realtors began tracking them in 2001. Sales were down 8.5% from October of last year. Tight supply and still-strong demand have kept pressure on home prices, which not only continue to hit new highs but appear to be accelerating in their gains. ales of homes priced above $750,000 have been increasing simply because there is more supply on the high end of the market.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, December 11, at 8:30 AM EST, the Consumer Inflation Expectations are out, one of the Fed’s favorite inflation reads.

On Tuesday, December 12 at 8:30 AM,the Consumer Price Index will be released. The Federal Reserve Open Market Committee starts a two-day meeting.

On Wednesday, December 13 at 2:00 PM, the Federal Reserve will release its interest rate decision. No change is expected. At 2:30, the Producer Price Index is out.

On Thursday, December 14 at 8:30 AM, the Weekly Jobless Claims are announced. We also get Retail Sales.

On Friday, December 15 at 2:30 PM, the October New York Empire StateManufacturing Index is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, it was with a heavy heart that I boarded a plane for Los Angeles to attend a funeral for Bob, the former scoutmaster of Boy Scout Troop 108.

The event brought a convocation of ex-scouts from up and down the West Coast and said much about our age.

Bob, 85, called me two weeks ago to tell me his CAT scan had just revealed advanced metastatic lung cancer. I said, “Congratulations Bob, you just made your life span.”

It was our last conversation.

He spent only a week in bed and then was gone. As a samurai warrior might have said, it was a good death. Some thought it was the smoking he quit 20 years ago.

Others speculated that it was his close work with uranium during WWII. I chalked it up to a half-century of breathing the air in Los Angeles.

Bob originally hailed from Bloomfield, New Jersey. After WWII, every East Coast college was jammed with returning vets on the GI bill. So he enrolled in a small, well-regarded engineering school in New Mexico in a remote place called Alamogordo.

His first job after graduation was testing V2 rockets newly captured from the Germans at the White Sands Missile Test Range. He graduated to design ignition systems for atomic bombs. A boom in defense spending during the fifties swept him up to the Greater Los Angeles area.

Scouts I last saw at age 13 or 14 are now 60, while the surviving dads were well into their 80s. Everyone was in great shape, those endless miles lugging heavy packs over High Sierra passes yielding lifetime benefits.

Hybrid cars lined both sides of the street. A tag-along guest called out for a cigarette and a hush came over a crowd numbering over 100.

Some things stuck. It was a real cycle of life weekend. While the elders spoke about blood pressure and golf handicaps, the next generation of scouts played in the backyard or picked lemons off a ripening tree.

Bob was the guy who taught me how to ski, cast rainbow trout in mountain lakes, transmit Morse code, and survive in the wilderness. He used to scrawl schematic diagrams for simple radios and binary computers on a piece of paper, usually built around a single tube or transistor.

I would run off to Radio Shack to buy WWII surplus parts for pennies on the pound and spend long nights attempting to decode impossibly fast Navy ship-to-ship transmissions. He was also the man who pinned an Eagle Scout badge on my uniform in front of beaming parents when I turned 15.

While in the neighborhood, I thought I would drive by the house in which I grew up, once a modest 1,800 square-foot ranch-style home to a happy family of nine. I was horrified to find that it had been torn down, and the majestic maple tree that I planted 40 years ago had been removed.

In its place was a giant, 6,000-square-foot marble and granite monstrosity under construction for a wealthy family from China.

Profits from the enormous China-America trade have been pouring into my hometown from the Middle Kingdom for the last decade, and mine was one of the last houses to go.

When I was class president of the high school here, there were 3,000 white kids and one Chinese. Today, those numbers are reversed. Such is the price of globalization.

I guess you really can’t go home again.

At the family's request, I assisted in liquidating his investment portfolio. Bob had been an avid reader of the Diary of a Mad Hedge Fund Trader since its inception and attended my Los Angeles lunches.

It seems he listened well. There was Apple (AAPL) in all its glory at a cost of $21. I laughed to myself. The master had become the student and the student had become the master.

Like I said, it was a real circle of life weekend.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

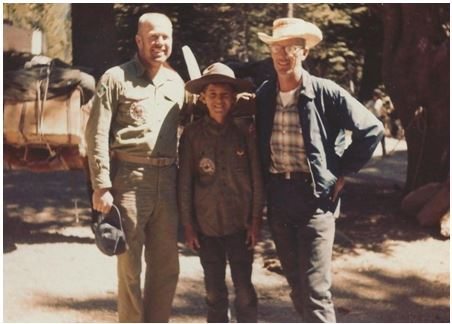

Scoutmaster Bob

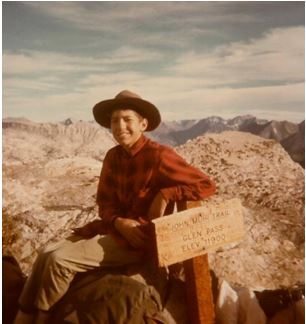

1965 Scout John Thomas

The Mad Hedge Fund Trader at Age 11 in 1963

https://www.madhedgefundtrader.com/wp-content/uploads/2023/12/old-sick-man.png492410april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-12-11 09:02:242023-12-11 11:36:38The Market Outlook for the Week Ahead, or Powell’s Victory Lap

“It’s going to be a shock when we wake up one morning and learn that China got to the moon while we were suing each other,” saidElon Musk, founder of PayPal, Space X, Tesla, Solar City, The Boring Company, Neuralink, and owner of “X”, the former Twitter.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/12/moon-wolf.png382468april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-12-11 09:00:432023-12-11 11:36:08December 11, 2023 - Quote of the Day

Remember when Apple (AAPL) swaggered into the trillion-dollar club in 2018, strutting out as the first company to hit that mind-boggling market cap?

Back then, it seemed like a peak had been reached in Silicon Valley, a modern “Valley of the Kings” where tech titans rule the economic world.

In the ever-evolving realm of Silicon Valley, financial titans don’t just join the trillion-dollar club; they redefine it. We've now got six behemoths, each commanding their empires past the trillion-dollar mark.

Apple leads this charge with a whopping $2.97 trillion market cap, trailed by Microsoft (MSFT) at $2.78 trillion, Alphabet (GOOGL) at $1.66 trillion, and Amazon (AMZN) at $1.51 trillion.

Fast forward to now, and this valley is witnessing a new sovereign rising to power - Nvidia (NVDA).

This semiconductor giant, not one to shy away from a growth spurt, recently posted numbers that'll make your head spin. Their revenue nearly tripled last quarter, riding high on a wave of demand for chips powering artificial intelligence (AI) applications.

With a stock split in July 2021 - a 4-for-1 move, their fifth since hitting the public markets in 1999, Nvidia’s growth trajectory seems set for the stars, especially with AI being the industry's hot ticket item.

As for their stock, it’s ablaze, having skyrocketed 211% year to date.

A deep dive into their figures reveals a 206% surge in third-quarter revenue to $18.12 billion.

This growth is thanks largely to their data center business and those fancy AI chips like the h100 and a100.

Evidently, Nvidia is doing more than riding the AI wave – they are at the forefront, driving its momentum.

The generative AI market is projected to hit a cool $1.3 trillion by 2032. And Nvidia, supplying the chips that make the magic happen, is sitting in a sweet spot for sustained growth.

Nvidia's price-to-sales (P/S) ratio is a lofty 26, shadowing the S&P 500's average of 2.5.

But before you balk at that figure, consider this: it doesn't quite capture Nvidia's rapid growth and hefty net income margin, which was over 50% in the third quarter of 2023.

Plus, their forward price-to-earnings ratio is a more palatable 24, suggesting that investing in Nvidia might just be the shrewdest move for those looking at the long game in AI.

Looking back, it’s clear that 2021 has been a banner year for Nvidia's GPUs, the go-to for AI projects from language model training to inference.

However, Nvidia's not running a solo race here.

Microsoft recently unveiled its Azure Maia AI Accelerator chip, while Amazon just announced its next-gen Trainium AI chip. And don’t forget the likes of Advanced Micro Devices (AMD), Intel (INTC), and Google, all busy in their labs.

Attempting to dethrone Nvidia? It's proving to be a formidable challenge.

The robustness of technology underpinning Nvidia's platforms proves their dominance in the field, with the company holding an 86% share of the market. Why? Three big reasons.

First, they've got the most mature AI tech in the game. They’ve spent over a decade refining their CUDA software programming ecosystem.

Second, Nvidia is cloud-agnostic, allowing customers to hop from one cloud to another, unlike Amazon or Google's chips.

Finally, developers stick with Nvidia for its stability, market share, industry-specific tools, and reputation for backward compatibility.

So, who's the king of the hill in our modern-day “Valley of the Kings,” (aka Silicon Valley)?

It’s still a battleground where the mightiest of tech titans clash, and right now, Nvidia is the one wearing the crown, and wearing it with a certain flair, I might add.

But, as the tech world spins on, with AI carving out the future, remember this – in the Valley of the Kings, it's Nvidia's throne, and they're not giving it up without a fight. In this land of tech titans, they're the ones calling the shots... at least for now.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2023-12-08 17:04:192023-12-08 17:04:19SILICON VALLEY OF THE KINGS

Big developments happening in the tech sector abroad and investors should take notice.

The CEO of technology giant Nvidia Jensen Huang said he believes that Malaysia will become a potential hub for artificial intelligence “manufacturing.”

This is big news for South Asia and this is the first stage of Silicon Valley looking to harness the power of South Asia to progress its narrative and developmental footprint.

It’s essential they find some low-cost countries to partner with because it’s not always sensible to manufacture in the United States because of cost restrictions.

Take AI, the need for large-scale servers is intense, and opting for a better cost-efficient place is a good strategy.

Huang mentioned that Malaysian conglomerate YTL Corp. could play an important role in setting up AI data centers.

Malaysia “is a very important hub for SEA’s computing infrastructure. It requires access to land, facilities, power, which is extraordinarily important,” he said. “I think YTL could play a great role in that.”

Malaysia’s expertise in packaging, assembly, and other aspects of manufacturing makes it well-suited for the manufacturing of artificial intelligence.

Nvidia is working with 80 AI startups in the country.

In Malaysia, the data center infrastructure layer of computing, which is one of the most important parts of the AI and the cloud, is very successful.

Southeast Asia will likely be a hub for AI computing because countries need their own AI data centers to refine and transform data into valuable information. Old data processing centers were designed to hold data files and run applications. AI requires the use of each place's culture, language, values, literature, and common sense.

The prospects of Southeast Asia are highly positive as it attempts to turn into an important technology hub. It’s already experienced in packaging, assembly, and battery manufacturing. It has rounded out to perform well throughout the entire technological supply chain.

The smart move here is to decouple from China as geopolitics threaten to spin out of control.

Also, consider that Chinese demographics are one of the grimmest in the world.

China simply isn’t producing young workers anymore and wages have skyrocketed.

It doesn’t make sense to build factories there anymore.

India will have a big role to play in the advancement of Silicon Valley production in the next generation.

Apple will shift a quarter of its iPhone production to India in the next two to three years.

The decision will translate into more than 50 million iPhones a year being built in India.

The iPhone production in India lagged seriously behind China but that changed with the iPhone 14, which began manufacturing in the same month as in China.

In 2023, Apple built more iPhone 15 units in India than any other model and it marked the first time it managed to release a model made in India on launch day.

Foxconn is currently building a plant in Karnataka state that should open for business in April 2024.

As Silicon Valley marches on, they will have an interest in partnering in other parts of the world to fine-tune their business models.

Expect a heavy dose of South Asia for the next generation because that is where the low-hanging fruit is.

India will come into its own in the next few years, and Malaysia certainly is a good value player.

The most important takeaway is the accretive effect they will have on American technology companies.

In the short term, I believe NVDA is a better stock player than Apple, although Apple is a great long-term investment.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-12-08 14:02:472023-12-08 16:21:24South Asia Partners

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.