Yesterday, I listed my Five Surprises of 2019 which will play out during the first half of the year prompting stocks to take another run at the highs, and then fail.

What if I’m wrong? I’ve always been a glass half full kind of guy. What if instead, we get the opposite of my five surprises? This is what they would look like. And better yet, this is how financial markets would perform.

*The government shutdown goes on indefinitely throwing the US economy into recession.

*The Chinese trade war escalates, deepening the recession both here and in the Middle Kingdom.

*The House moves to impeach the president, ignoring domestic issues, driven by the younger winners of the last election.

*A hard Brexit goes through completely cutting Britain off from Europe.

*The Mueller investigation concludes that Trump is a Russian agent and is guilty of 20 felonies including capital treason.

*All of the above are HUGELY risk negative and will trigger a MONSTER STOCK SELLOFF.

It’s really difficult to quantify how badly markets will behave given that this scenario amounts to five black swans landing simultaneously. However, we do have a recent benchmark with which to make comparisons, the 2008-2009 stock market crash and great recession. I’ll list off the damage report by asset class. I also include the exchange-traded fund you need to hedge yourself against Armageddon in each asset class.

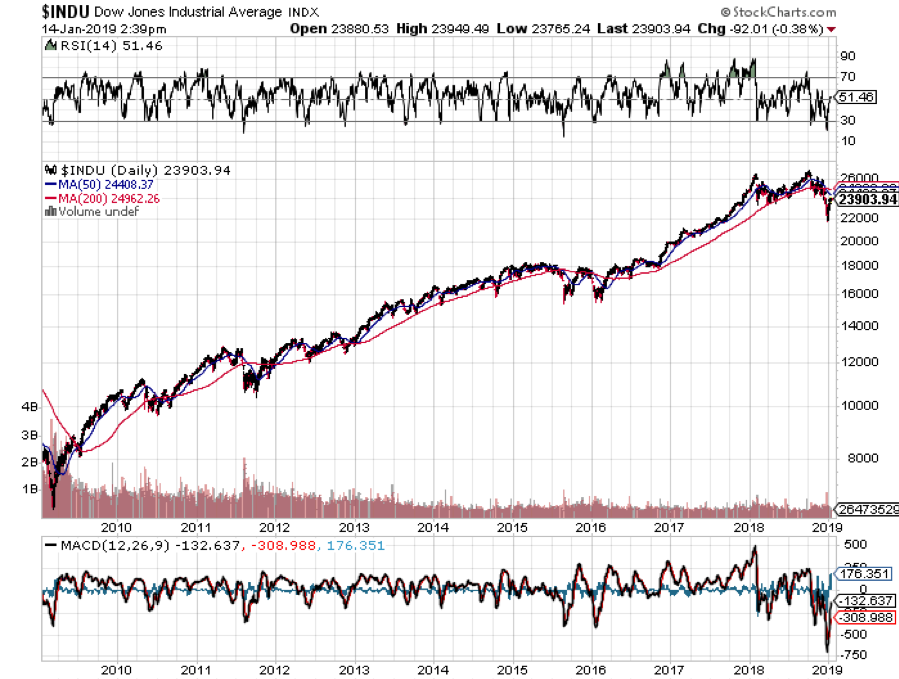

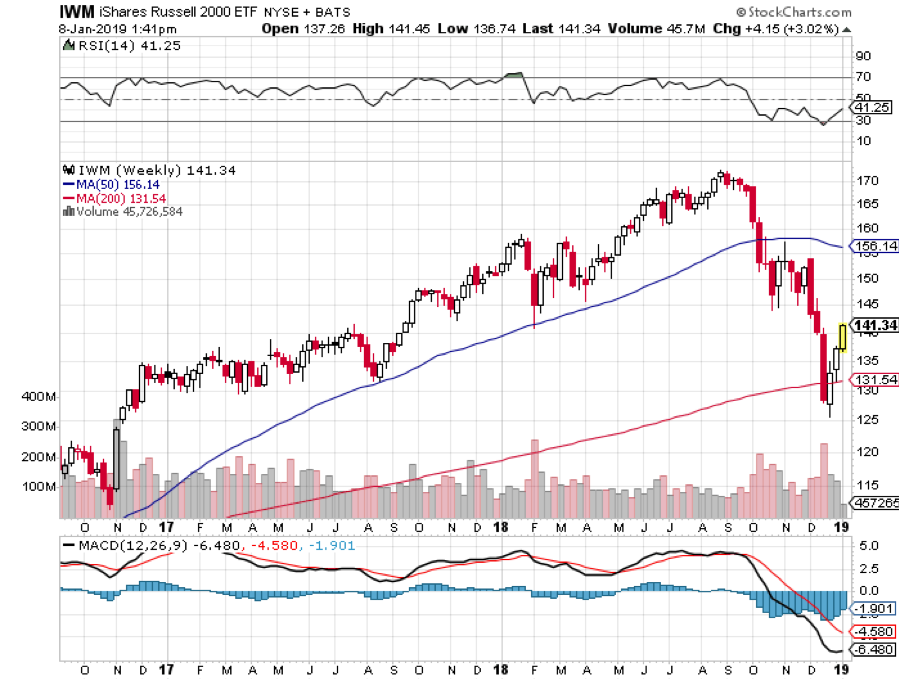

*Stocks – Depending on how fast the above rolls out, you will see a stock market (SPY) collapse of Biblical proportions. You’ll easily unwind the Trump rally that started at a Dow Average of 18,000, down 25% from the current level, and off a gut-churning 9,000 points or 33% from the September top. The next support below is the 2015 low at 15,500, down 11,500 points, or 43% from the top. By comparison, during the 2008-2009 crash, we fell 52%. Everything falls and there is no safe place to hide. Buy the ProShares UltraShort S&P 500 bear ETF (SDS).

*Bonds – With the ten-year US Treasury yield peaking at 3.25% last summer, a buying panic would spill into the bond market. Inflation is nonexistent, we are running at only a 2.2% YOY rate now, so widespread deflation would rapidly swallow up the entire economy. In that case, all interest rates go to zero very quickly. The Fed cuts rates as fast as it can. Eventually, the ten-year yield drops to -0.40%, the bottom seen in Japanese and German debt three years ago. Buy the 2X short bond ETF (TBT) which will rocket to from $35 to $200.

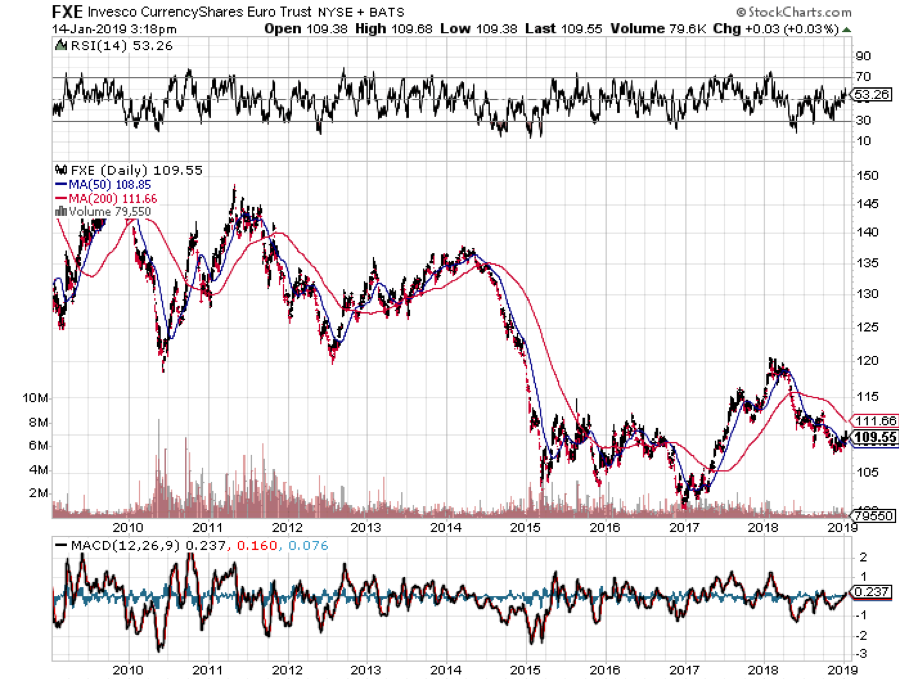

*Foreign Exchange – With US interest rates going to zero, the US Dollar (UUP) gets the stuffing knocked out of it. The Euro soars from $1.10 to $1.60 last seen in 2010, and the Japanese yen (FXY) revisits Y80. Strong currencies then crush the economies of our largest trading partners. Their governments take their interest rates back to negative numbers to cool their own currencies. Cash becomes trash….globally.

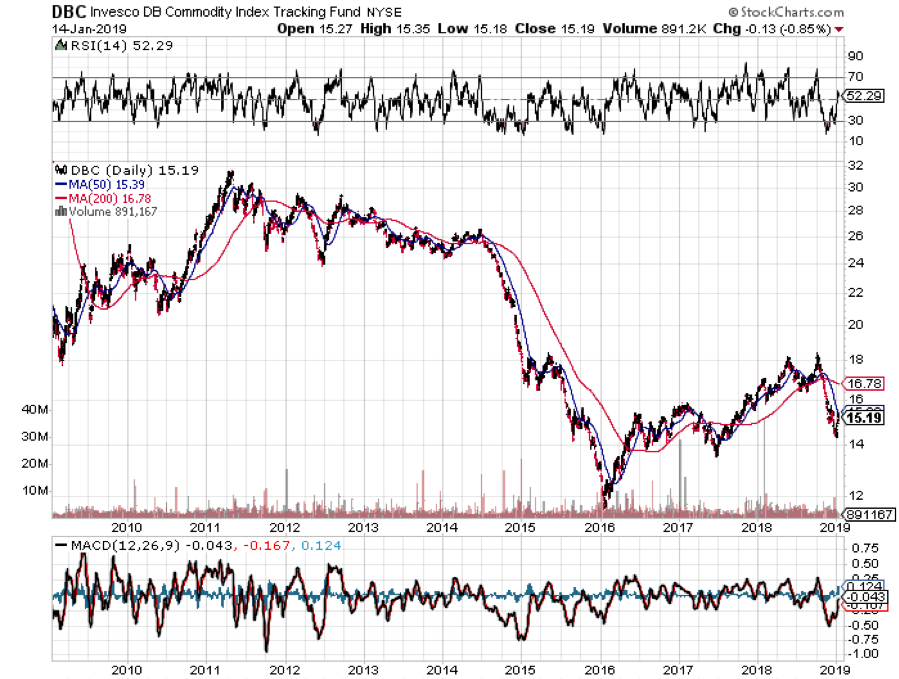

*Commodities

Here’s the really ugly part about commodities. They are only just starting to crawl OUT of a seven-year bear market. To hit them with another price collapse now would devastate the industry. Producer bankruptcies would be widespread. The ags would get especially hard hit as they have already been pummeled by the trade war with China. Midwestern regional banks would get wiped out. Buy the DB Commodity Short ETN (DDP).

*Energy

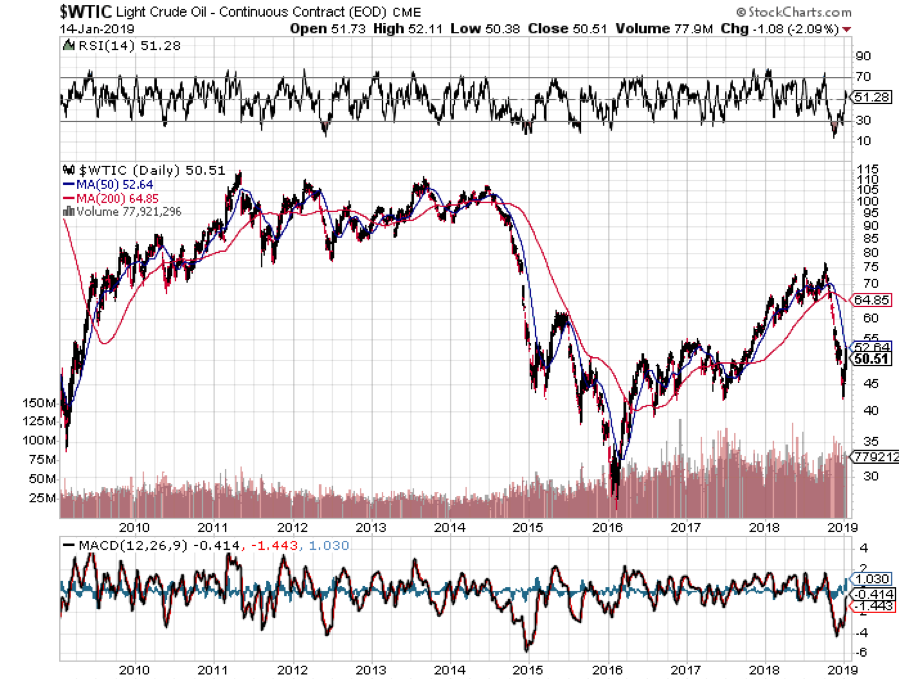

The price of oil (USO) is also just crawling back from a correction for the ages, down from $77 to $42 a barrel in only three months. Hit the sector with a recession now in the face of global overproduction and the 2009 low of $25 becomes a chip shot, and possibly much lower. Those who chased for yield with energy master limited partnerships will get flushed. Several smaller exploration and production companies will get destroyed. And gasoline drops to $1 a gallon. The Middle East collapses into a geopolitical nightmare and much of Texas files chapter 11. Buy the ProShares UltraShort Bloomberg Crude Oil ETF (SCO).

*Precious metals

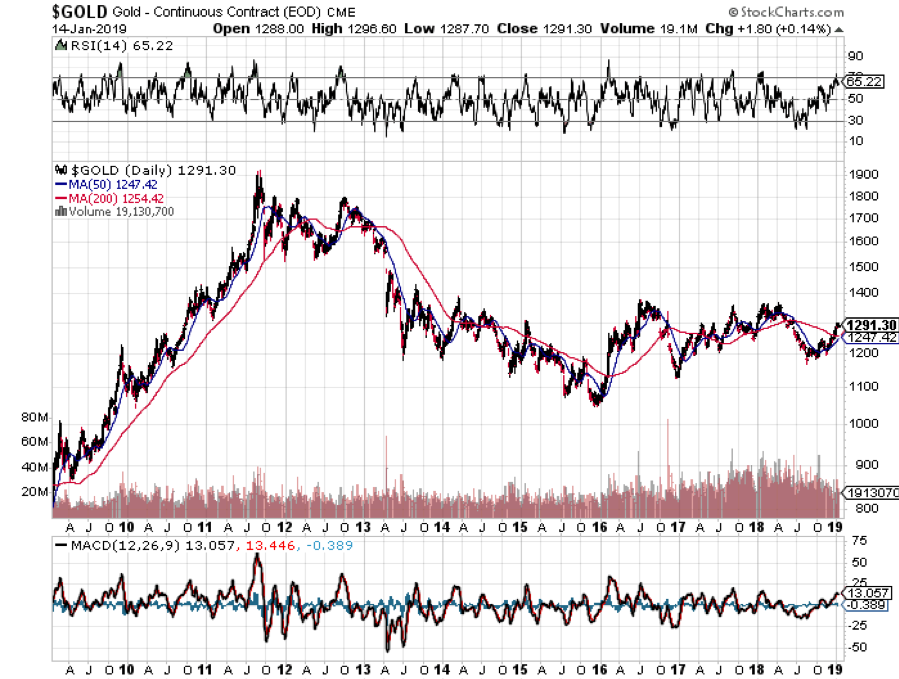

Gold (GLD) initially rallies on the flight to safety bid that we have seen since September. However, if things get really bad, EVERYTHING gets sold, even the barbarous relic, as margin clerks are in the driver’s seat. You sell what you can, not what you want to, as liquidity becomes paramount. This is what took the yellow metal down to $900 an ounce in 2009. Buy the DB Gold Short ETN (DGZ).

*Real Estate

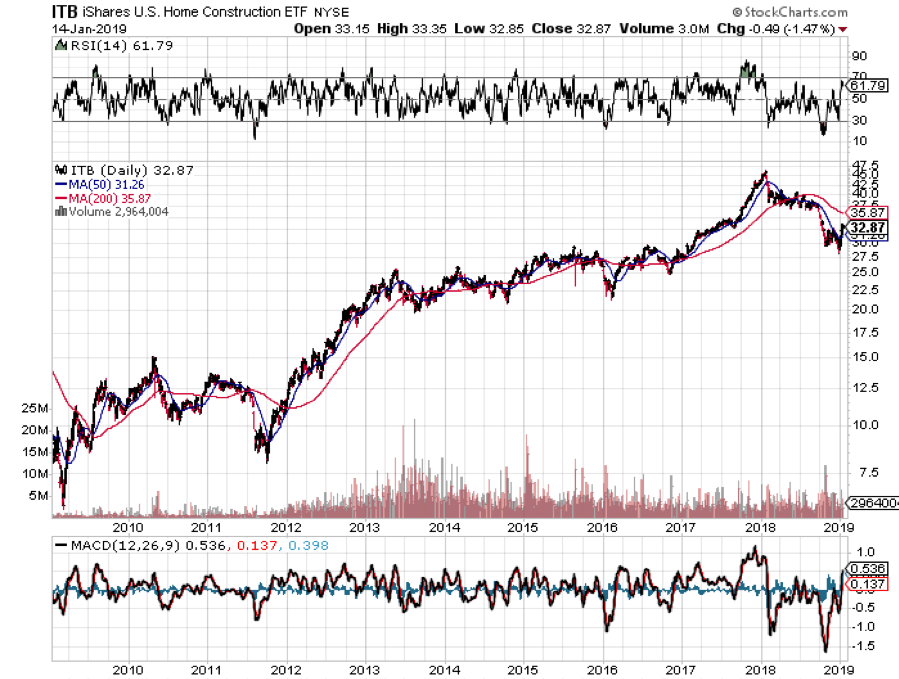

Believe it or not, real estate doesn’t do all that bad in a worst-case scenario. It is perhaps the safest asset class around if a new crisis financial unfolds. For a start, interest rates at zero would provide a huge cushion. The Dodd-Frank financial regulation bill successfully prevented lenders returning to even a fraction of the leverage they used in the run-up to the last recession. We are about to enter a major demographic tailwind in housing as the Millennial generation become the predominant home buyers. I’ve never seen a housing slump in the face of a structural shortage. And homebuilder stocks (ITB) have already been discounting the next recession for the past year. A lot is already baked in the price.

Conclusion

Of course, it is highly unlikely that any of the above happens. Think of it all as what Albert Einstein called a “thought experiment.” But it is better to do the thinking now so you can do the trading later. There may not be time to do otherwise.

Be Careful, They Bite!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/03/John-Thoms-Black-Swans-e1413901799656.jpg337400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-15 08:06:042019-07-09 04:42:36Here’s the Worst-Case Scenario

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could get to navigate it.

I am not Houdini, so I go downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google search obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 10x.

After making the rounds with strategists, portfolio managers, and hedge fund traders in the run-up to this trip, I can confirm that 2018 was one of the most brutal to trade for careers lasting 30, 40, or 50 years. This was the year that EVERYTHING went down, the first time that has happened since 1972. Comparisons with 1929, 1987, and 2008 were frequently made.

While my own 23.56% return for last year is the most modest in a decade, it beats the pants off of the Dow Average plunge of 8% and 99.9% of the other managers out there. That is a mere shadow of the spectacular 57.91% profit I took in during 2017. This keeps my ten-year average annualized return at 34.20%.

Our entire fourth-quarter loss came from a single trade, a far too early bet that the Volatility Index would fall from the high of the year at $30.

For a decade, all you had to do was throw a dart at the stock page of the Wall Street Journal and you made money, as long as it didn’t end on retail. No more.

For the first time in years, the passive index funds lost out to the better active managers. The Golden Age of the active manager is over. Most hedge funds did horribly, leveraged long technology stocks and oil and short bonds. None of it worked.

If you think I spend too much time absorbing conspiracy theories from the Internet, let me give you a list of the challenges I see financial markets facing in the coming year:

The Nine Key Variables for 2019

1) Will the Fed raise rates one, two, or three times, or not at all?

2) Will there be a recession this year or will we have to wait for 2020?

3) Is the tax bill fully priced into the economy or is there more stimulus to come?

4) Will the Middle East drag us into a new war?

5) Will technology stocks regain market leadership or will it be replaced by other sectors?

6) Will gold and other commodities finally make a long-awaited comeback?

7) Will rising interest rates (positive) or deficits (negative) drive the US dollar this year?

8) Will oil prices recover in 2019?

9) Will bitcoin ever recover?

Here are your answers to the above: 1) Two, 2) 2020, 3) Yes, 4) No, 5) Both, 6) Yes, 7) Yes, 8) Yes, 9) No.

There you go! That’s all the research you have to do for the coming year. Everything else is a piece of cake. You can go back to your vacation.

The Twelve Highlights of 2018

1) Stocks will finish lower in 2019. However, we aren’t going to collapse from here. We will take one more rush at the all-time highs that will take us up 10% to 15% from current levels, and then fail. That will set up the perfect “head and shoulders” top on the long-term charts that will finally bring to an end this ten-year bull market. This is when you want to sell everything. The May 10, 2019 end to the bull market forecast I made a year ago is looking pretty good.

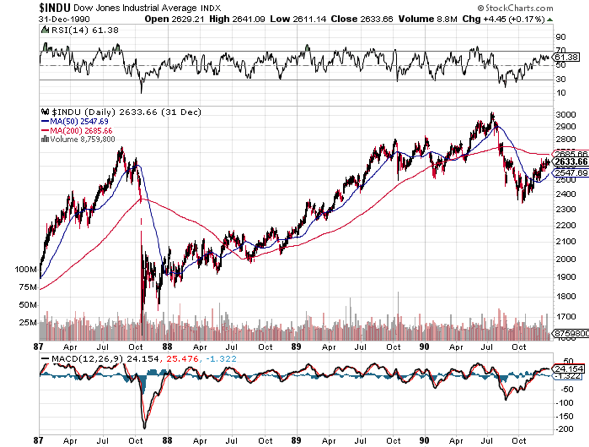

I think there is a lot to learn from the 1987 example when stocks crashed 20% in a single day, and 42% from their 1987 high, and then rallied for 28 more months until the next S&L crisis-induced recession in 1991.

Investors have just been put through a meat grinder. From here on, its all about trying to get out at a better price, except for the longest-term investors.

2) Stocks will rally from here because they are STILL receiving the greatest amount of stimulus in history. Energy prices have dropped by half, taxes are low, inflation is non-existent, and interest rates are still well below long term averages.

Corporate earnings will grow at a 6% rate, not the 26% we saw in 2018. But growing they are. At current prices, the stock market is assuming that companies will generate big losses in 2019, which they won’t. Just try to find a parking space at a shopping mall anywhere and you’ll see what I mean.

3) Technology stocks will lead any recovery. Love them or hate them, big tech accounts for 25% of stock market capitalization but 50% of US profits. That is where the money is. However, in 2019 they will be joined by biotech and health care companies as market leaders.

4) The next big rally in the market will be triggered by the end of the trade war with China. Don’t expect the US to get much out of the deal. It turns out that the Chinese can handle a 20% plunge in the stock market much better than we can.

5) The Treasury bond market will finally get the next leg down in its new 10-year bear market, but don’t expect Armageddon. The ten-year Treasury yield should hit at least 3.50%, and possibly 4.0%.

6) With slowing, US interest rate rises, the US dollar will have the wind knocked out of it. It’s already begun. The Euro and the Japanese yen will both gain about 10% against the greenback.

7) Political instability is a new unknown factor in making market predictions which most of us have not had to deal with since the Watergate crisis in 1974. It’s hard to imagine the upcoming Mueller Report not generating a large market impact, and presidential tweets are already giving us Dow 1,000-point range days. These are all out of the blue and totally unpredictable.

8) Oil at $42.50 a barrel has also fully discounted a full-on recession. So, if the economic slowdown doesn’t show, we can make it back up to $64 quickly, a 50% gain.

9) Gold continues its slow-motion bull market, gaining another 10% since the August low. It barely delivered in 2018 as a bear market hedge. But once inflation starts to pick up a head of steam, so should the price of the barbarous relic.

10) Commodities had a horrific year, pulled under by the trade war, rising rates, and strong dollar. Reverse all that and they should do better.

11) Residential real estate has been in a bear market since March. You’ll find out for sure if you try to sell your home. Rising interest rates and a slowing economy are not what housing bull markets are made of. However, prices will drop only slightly, like 10%, as there is still a structural shortage of housing in the US.

12) The new tax bill came and went with barely an impact on the economy. At best we got two-quarters of above-average growth and slightly higher capital spending before it returned to a 2%-2.5% mean. Unfortunately, it will cost us $4 trillion in new government debt to achieve this. It was probably the worst value for money spent in American history.

Dow Average 1987-90

The Thumbnail Portfolio

Equities - Go Long. The tenth year of the bull market takes the S&P 500 up 13% from $2,500 to $2,800 during the first half, and then down by more than that in the second half. This sets up the perfect “head and shoulders” top to the entire decade-long move that I have been talking about since the summer.

Technology, Pharmaceuticals, Healthcare, and Biotech will lead on the up moves and now is a great entry point for all of these. Buy low, sell high. Everyone talks about it but few ever actually execute like this.

Bonds - Sell Short. Down for the entire year big time. Sell short every five-point rally in the ten-year Treasury bond. Did I mention that bonds have just had a ten-point rally? That’s why I am doubled up on the short side.

Foreign Currencies - Buy. The US dollar has just ended its five-year bull trend. Any pause in the Fed’s rate rising schedule will send the buck on a swan dive, and it’s looking like we may be about to get a six-month break.

Commodities - Go Long. Global synchronized recovery continues the new bull market.

Precious Metals - Buy. Emerging market central bank demand, accelerating inflation, and a pause in interest rate rises will keep the yellow slowly rising.

Real Estate – Stand Aside. Prices are falling but not enough to make it worth selling your home and buying one back later. A multi-decade demographic tailwind is just starting, and it is just a matter of time before prices come roaring back.

1) The Economy-Slowing

A major $1.5 trillion fiscal stimulus was a terrible idea in the ninth year of an economic recovery with employment at a decade high. Nevertheless, that’s what we got.

The certainty going forward is that the gains provided by lower taxes will be entirely offset by higher interest rates, higher labor costs, and rising commodity and oil prices.

Since most of the benefits accrued to the top 1% of income earners, the proceeds of these breaks entirely ended up share buybacks and the bond market. This is why interest rates are still so incredibly low, even though the Fed has been tightening for 4 ½ years (remember the 2014 taper tantrum?) and raising rates for three years.

And every corporate management views these cuts as temporary so don’t expect any major capital investment or hiring binges based on them.

The trade wars have shifted the global economy from a synchronized recovery to a US only recovery, to a globally-showing one. It turns out that damaging the economies of your biggest economies is bad for your own business. They are also a major weight on US growth. CEOs would rather wait to see how things play out before making ANY long-term decisions.

As a result, I expect real US economic growth will retreat from the 3.0% level of 2018 to a much more modest 1.5%-2.0% range in 2019.

The government shutdown, now in its third week (and second year), will also start to impact 2019 growth estimates. For every two weeks of closure, you can subtract 0.1% in annual growth.

Twenty weeks would cut a full 1%. And if you only have 2% growth to start with that means you don’t have much to throw away until you end up in a full-on recession.

Hyper-accelerating and cross-fertilizing technology will remain a long term and underestimated positive. But you have to live here next to Silicon Valley to realize that.

S&P 500 earnings will grow from the current $170 to $180 at a price earnings multiple at the current 14X, a gain of 6%. Unfortunately, these will start to fade in the second half from the weight of rising interest rates, inflation, and political certainty. Loss of confidence will be a big influence in valuing shares in 2019.

Whatever happened to the $2.5 trillion in offshore funds held by American companies expected to be repatriated back to the US? That was supposed to be a huge market stimulus last year. It’s still sitting out there. It turns out companies still won’t bring the money home even with a lowly 10% tax rate. They’d rather keep it abroad to finance growth there or borrow against it in the US.

Here is the one big impact of the tax bill that everyone is still missing. The 57% of the home-owning population are about to find out how much their loss of local tax deductions and mortgage deductions is going to cost them when they file their 2018 returns in April. They happen to be the country’s biggest spenders. That’s another immeasurable negative for the economy.

Take money out of the pockets of the spenders and give it to the savers and you can’t have anything but a weakening on the economy.

All in all, it will be one of the worst years of the decade for the economy. Maybe that’s what the nightmarish fourth quarter crash was trying to tell us.

The final move of a decade long bull market is upon us.

Corporate earnings are at record levels and are climbing at 6% a year. Cash on the balance sheet is at an all-time high as are profit margins. Interest rates are still near historic lows.

Yet, there is not a whiff of inflation anywhere except in now fading home costs and paper asset prices. Almost all other asset classes offer pitiful alternatives.

The golden age of passive index investing is over. This year, portfolio managers are going to have to earn their crust of bread through perfect market timing, sector selection, and individual name-picking. Good luck with that. But then, that’s why you read this newsletter.

I expect an inverse “V”, or Greek lambda type of year. Stocks will rally first, driven by delayed rate rises, a China war settlement, and the end of the government shut down. That will give the Fed the confidence to start raising rates again by mid-year because inflation is finally starting to show. This will deliver another gut-punching market selloff in the second half giving us a negative stock market return for the second year in a row. That hasn’t happened since the Dotcom Bust of 2001-2002.

How much money will I make this year? A lot more than last year’s middling 23.56% because now we have some reliable short selling opportunities for the first time in a decade. Short positions performed dreadfully when global liquidity is expanding. They do much better when it is shrinking, as it is now.

Amtrak needs to fill every seat in the dining car to get everyone fed, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam vet Phantom jet pilot who now refused to fly because he was treated so badly at airports. A young couple desperate fleeing Omaha could only afford seats as far as Salt Lake City, sitting up all night. I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites returning home by train because their religion forbade automobiles or airplanes.

This year is simply a numbers game for the bond market. The budget deficit should come in at a record $1.2 trillion. The Fed will take out another $600 billion through quantitative tightening. Some $1.8 trillion will be far too much for the bond market to soak up, meaning prices can only fall.

Except that this year is different for the following reasons.

1) The US government is now at war with the world’s largest bond buyer, the Chinese government.

2) A declining US dollar will frighten off foreign buyers to a large degree.

3) The tax cuts have come and gone with no real net benefit to the average American. Probably half of the country saw an actual tax increase from this tax cut, especially me.

All are HUGELY bond negative.

It all adds up to a massive crowding out of individual and corporate borrowers by the federal government, which will be forced to bid up for funds. You are already seeing this in exploding credit spreads. This will be a global problem. There are going to be a heck of a lot of government bonds out there for sale.

That 2.54% yield for the ten-year Treasury bond you saw on your screen in early January? You will laugh at that figure in a year as it hits 3.50% to 4.0%.

Bond investors today get an unbelievably bad deal. If they hang on to the longer maturities, they will get back only 90 cents worth of purchasing power at maturity for every dollar they invest a decade down the road at best.

The only short-term positive for bonds was Fed governor Jay Powell’s statement last week that our central bank will be sensitive to the level of the stock market when considering rate rises. That translates into the reality that rates won’t go up AT ALL as long as markets are in crash mode.

It all means that we are now only two and a half years into a bear market that could last for ten or twenty years.

The IShares 20+ Year Treasury Bond ETF (TLT) trading today at $123 could drop below $100. The 2X ProShares 20+ Short Treasury Bond Fund (TBT) now at $31 is headed for $50 or more.

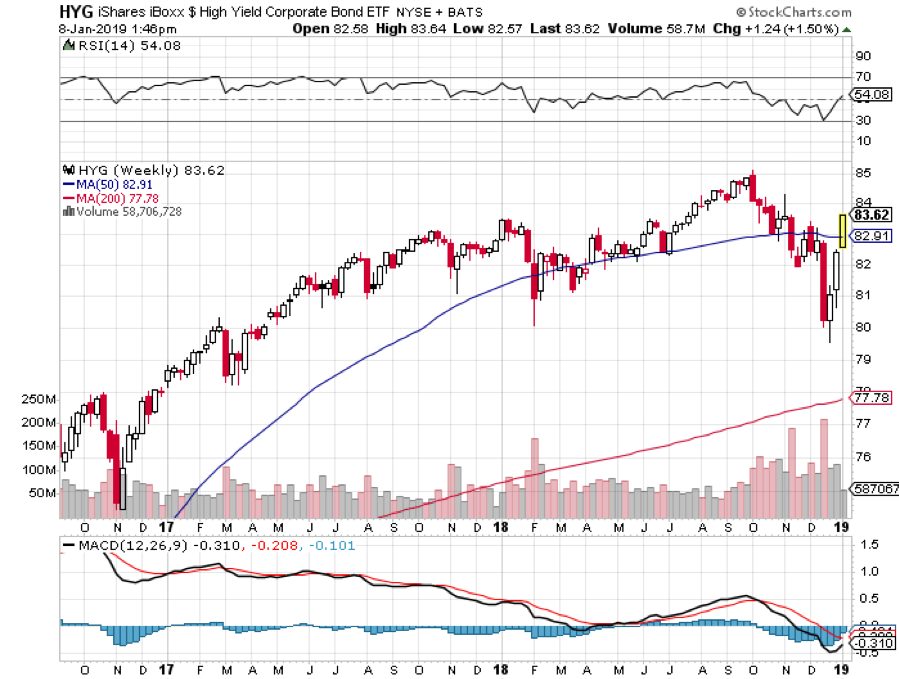

Junk Bonds (HYG) are already reading the writing on the wall taking a shellacking during the Q4 stock market meltdown. This lackluster return ALWAYS presages an inverted yield curve by a year where short term interest rates are higher than long term ones. This in turn reliably predicts a full-scale recession by 2020 at the latest.

I have pounded away at you for years that interest rate differentials are far and away the biggest decider of the direction in currencies.

This year will prove that concept once again.

With overnight rates now at 2.50% and ten-year Treasury bonds at 2.54%, the US now has the highest interest rates of any major industrialized economy.

However, pause interest rate rises for six months or a year and the dollar loses its mojo very quickly.

Compounding the problem is that a weak dollar begets selling from foreign investors. They are in a mood to do so anyway, as they see rising political instability in the US a burgeoning threat to the value of the greenback.

So the dollar will turn weak against all major currencies, especially the Japanese yen (FXY), and the Australian (FXA) and Canadian (FXC) dollars.

A global synchronized economic slowdown can mean only one thing and that is sustainably lower commodity prices.

Industrial commodities, like copper, iron ore, performed abysmally in 2018, dope slapped by the twin evils of a strong dollar and the China trade war.

We aren’t returning to the heady days of the last commodity bubble top anytime soon. Investors are already front running that move now.

However, once this sector gets the whiff of a weak dollar or higher inflation, it will take off like a scalded chimp.

Now that their infrastructure is largely built out, the Middle Kingdom will change drivers of its economy. This is world-changing.

The shift will be from foreign exports to domestic consumption. This will be a multi-decade process, and they have $3.1 trillion in foreign exchange reserves to finance it.

It will still demand prodigious amounts of imported commodities but not as much as in the past.

This trend ran head-on into a decade-long expansion of capacity by the commodities industry, delivering the five-year bear market that we are only just crawling out of.

The derivative equity plays here, Freeport McMoRan (FCX) and Companhia Vale do Rio Doce (VALE) have all been some of the best-performing assets of 2017.

If you expect a trade war-induced global economic slowdown, the last thing in the world you want to own is an energy investment.

And so it was in Q4 when the price of oil got hammered doing a swan dive from $68 to $42 a barrel, an incredible 38% hickey.

All eyes will be focused on OPEC production looking for new evidence of quota cheating which is slated to expire at the end of 2018. Their latest production cut looked great on paper but proved awful in practice. Welcome to the Middle East.

The only saving grace is that with crude at these subterranean levels, new investment in fracking production has virtually ceased. No matter, US pipelines are operating at full capacity anyway.

OPEC production versus American frackers will create the constant tension in the marketplace for all of 2019.

My argument in favor of commodities and emerging markets applies to Texas tea as well. A weaker US dollar, trade war end, interest rate halt are all big positives for any oil investment. The cure for low oil prices is low prices.

That makes energy Master Limited Partnerships, now yielding 6-10%, especially interesting in this low yield world. Since no one in the industry knows which issuers are going bankrupt, you have to take a basket approach and buy all of them.

The Alerian MLP ETF (AMLP) does this for you in an ETF format. Our train has moved over to a siding to permit a freight train to pass, as it has priority on the Amtrak system.

Three Burlington Northern engines are heaving to pull over 100 black, spanking brand new tank cars, each carrying 30,000 gallons of oil from the fracking fields in North Dakota.

There is another tank car train right behind it. No wonder Warren Buffett tap dances to work every day as he owns the railroad.

We are also seeing relentless improvements on the energy conservation front with more electric vehicles, high mileage conventional cars, and newly efficient building.

Anyone of these inputs is miniscule on its own. But add them all together and you have a game changer.

As is always the case, the cure for low prices is low prices. But we may never see $100/barrel crude again. In fact, the coming peak in oil prices may be the last one we ever see. The word is that leasing companies will stop offering five-year leases in five years because cars with internal combustion engines will become worthless in ten.

Add to your long-term portfolio (DIG), ExxonMobile (XOM), Cheniere Energy (LNG), the energy sector ETF (XLE), Conoco Phillips (COP), and Occidental Petroleum (OXY). But date these stocks, don’t marry them.

Skip natural gas (UNG) price plays and only go after volume plays because the discovery of a new 100-year supply from “fracking” and horizontal drilling in shale formations is going to overhang this subsector for a very long time, like the rest of our lives.

It is a basic law of economics that cheaper prices bring greater demand and growing volumes which have to be transported. Any increase in fracking creates more supply of natural gas.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly that it blew a train over on to its side.

In the snow-filled canyons, we sight a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to them, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Gold (GLD) lost money in 2018, off 2.4%. More volatile silver (SLV) shed 12%.

This was expected, as non-yielding assets like precious metals do terribly during times of rising interest rates.

In 2019, gold will finally be coming out of a long dark age. As long as the world was clamoring for paper assets like stocks, gold was just another shiny rock. After all, who needs an insurance policy if you are going to live forever?

But the long-term bull case is still there. Gold is not dead; it is just resting.

If you forgot to buy gold at $35, $300, or $800, another entry point here up for those who, so far, have missed the gravy train.

To a certain extent, the belief that high-interest rates are bad for gold is a myth. Wealth creation is a far bigger driver. To see what I mean, take a look at a gold chart for the 1970s when interest rates were rising sharply.

Remember, this is the asset class that takes the escalator up and the elevator down, and sometimes the window.

If the institutional world devotes just 5% of their assets to a weighting in gold, and an emerging market central bank bidding war for gold reserves continues, it has to fly to at least $2,300, the inflation-adjusted all-time high, or more.

This is why emerging market central banks step in as large buyers every time we probe lower prices. China and India emerged as major buyers of gold in the final quarters of 2018.

They were joined by Russia which was looking for non-dollar investments to dodge US economic and banking sanctions.

That means it’s just a matter of time before gold breaks out to a new multiyear high above $1,300 an ounce. ETF players can look at the 1X (GLD) or the 2X leveraged gold (DGP).

I would also be using the next bout of weakness to pick up the high beta, more volatile precious metal, silver (SLV) which I think could rise from the present $14 and hit $50 once more, and eventually $100.

The turbocharger for gold will hit sometime in 2019 with the return of inflation. Hello stagflation, it’s been a long time.

Would You Believe This is a Purple State?

8) Real Estate (ITB), (LEN),

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving bands of Indians, itinerant fur traders, the Pony Express, my own immigrant forebears in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

There is no doubt a long-term bull market in real estate is taking a major break. If you didn’t sell your house by March last year you’re screwed and stuck for the duration.

And you’re doubly screwed if you’re trying to sell your home now during the government shutdown. With the IRS closed, tax return transcripts are unobtainable making any loan approval impossible. And no one at Fannie Mae or Freddie Mac, the ultimate buyers of 70% of US home loans, has answered their phone this year.

The good news is that we will not see a 2008 repeat when home values cratered by 50%-70%. There is just not enough leverage in the system to do any real damage. That has gone elsewhere, like in exchange-traded funds. You can thank Dodd/Frank for that which imposed capital rules so strict that it is almost impossible for banks to commit suicide.

And no matter how dire conditions may appear now, you are not going to see serious damage in a market where there is a generational structural shortage of supply.

We are probably seven years into a 17-year run at the next peak in 2028. What we are suffering now is a brief two-year pause to catch our breath. Those bidding wars were getting tiresome anyway.

There are only three numbers you need to know in the housing market for the next 20 years: there are 80 million baby boomers, 65 million Generation Xers who follow them, and 86 million in the generation after that, the Millennials.

The boomers have been unloading dwellings to the Gen Xers since prices peaked in 2007. But there is not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis.

If they have prospered, banks won’t lend to them. Brokers used to say that their market was all about “location, location, location.” Now it is “financing, financing, financing.” Imminent deregulation is about to deep-six that problem.

There is a happy ending to this story.

Millennials now aged 23-38 are already starting to kick in as the dominant buyers in the market. They are just starting to transition from 30% to 70% of all new buyers in this market.

The Great Millennial Migration to the suburbs has just begun.

As a result, the price of single-family homes should rocket tenfold during the 2020s as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a coming labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of the gross income, compared to only 18% for owners, and less when multiple deductions and tax subsidies are taken into account.

Remember too that, by then, the US will not have built any new houses in large numbers in 12 years.

We are still operating at only a half of the peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

That makes a home purchase now particularly attractive for the long term, to live in, and not to speculate with. And now that it is temporarily a buyer’s market, it is a good time to step in for investment purposes.

You will boast to your grandchildren how little you paid for your house as my grandparents once did to me ($3,000 for a four-bedroom brownstone in Brooklyn in 1922), or I do to my kids ($180,000 for an Upper East Side high rise in 1983).

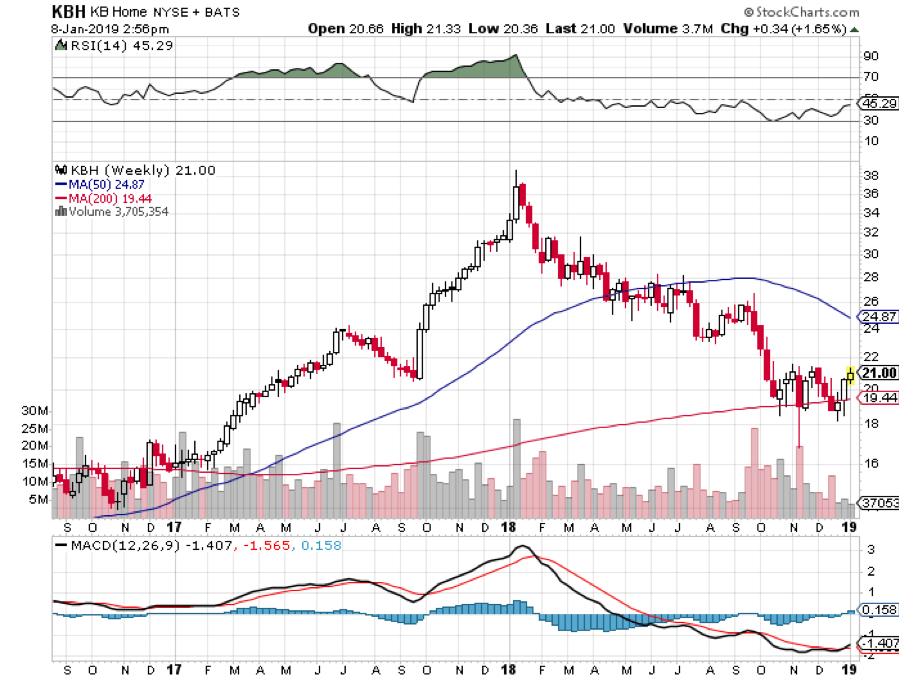

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) may finally be a buy on the dip.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now.

If you borrow at a 4% 5/1 ARM rate, and the long-term inflation rate is 3%, then over time you will get your house nearly for free.

How hard is that to figure out?

Crossing the Bridge to Home Sweet Home

9) Postscript

We have pulled into the station at Truckee in the midst of a howling blizzard.

My loyal staff has made the ten-mile treck from my beachfront estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed the Pacific mothball fleet moored near the Benicia Bridge. The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my water bottle.

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro and iPhone X, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above.

Good trading in 2019!

John Thomas

The Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-09 01:05:052019-01-08 21:01:382019 Annual Asset Class Review: A Global Vision

Not a day goes by when someone doesn’t ask me about what to do about Apple (AAPL).

After all, it is the world largest company. It is the planet’s most widely owned stock. Almost everyone uses their products in some form or another.

So, the widespread interest is totally understandable.

Apple is a company with which I have a very long relationship. During the early 1980s, I was ordered by Morgan Stanley to take Steve Jobs around to the big New York Institutional Investors to pitch a secondary share offer for the sole reason that I was one of three people who worked for the firm who was then from California.

They thought one West Coast hippy would easily get along with another. Boy, were they wrong. It was the worst day of my life. Steve was not a guy who palled around with anyone.

Today, some 200 Apple employees subscribe to the Diary of a Mad Hedge Fund Trader looking to diversify their substantial holdings. Many own Apple stock with an adjusted cost basis of under $5. Suffice it to say, they all drive really nice Priuses.

So I get a lot of information about the firm far above and beyond the normal effluent of the media and stock analysts. That’s why Apple has become a favorite target of my Trade Alerts over the years.

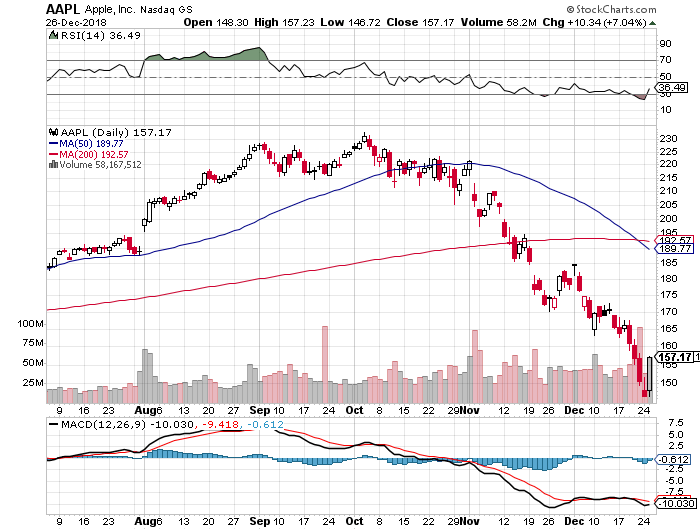

And here is the take: You didn’t want to touch the stock during the last quarter of 2018.

And here’s why. Apple is all about the iPhone which accounts for 75% of its total earnings. The TV, the watch, the car, iPods, the iMac, and Apple pay are all a waste of time and consume far more coverage than they are collectively worth.

The good news is that iPhone sales are subject to a fairly reliable cycle. Apple launches a major new iPhone every other fall. The share price peaks shortly after that. The odd years see minor upgrades, not generational changes.

Just like you see a big pullback in the tide before a tsunami hits, iPhone sales are flattening out. This is because consumers start delaying purchases in expectation of the introduction of the iPhone 7 in September 2016 with far more power, gadgets, and gizmos.

Channel checks, however dubious these may be, are already confirming the slowdown of orders for iPhone-related semiconductors from suppliers you would expect from such a downturn.

So during those in-between years, the stock performance is disappointing. 2018 certainly followed this script with Apple down a horrific 30.13% at the lows. Maybe it’s a coincidence, but that last generation in Apple shares in 2015 brought a decline of, you guessed it, exactly 29.33%.

The coming quarter could bring the opposite.

After March, things will start to get interesting especially post the Q1 earnings report in April. That’s when investors will start to discount the rollout of the next iPhone seven months later.

The last time this happened, in 2018, Apple stock rocketed by $86, or 55.33%. This time, I expect a minimum rally to the old $233 high, a gain of $71, or 43.82%.

After all, I am such a conservative guy with my predictions.

Even at that price, it will still be one of the cheapest stocks in the market on a valuation basis which currently trades at a 14X earnings multiple. The value players will have no choice to join in, if they’re not already there.

But Apple is a much bigger company this time around, and well-established cycles tend to bring in diminishing returns. It’s like watching the declining peaks of a bouncing rubber ball.

The bull case for Apple isn’t dead, it is just resting.

The China business will continue to grow nicely once we get through the current trade war. Their new lease program promises to deliver a faster upgrade cycle that will allow higher premium prices for their products. That will bring larger profits.

Just thought you’d like to know.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-27 01:08:082018-12-26 18:31:24How to Play Apple in 2019

As you are all well aware, I have long been a history buff. I am particularly fond of studying the history of my own avocation, trading, in the hope that the past errors of others will provide insights into the future.

History doesn’t repeat itself, but it certainly rhymes.

So after decades of research on the topic, I thought I would provide you with a list of the eight worst trades in history. Some of these are subjective, some are judgment calls, but all are educational. And I do personally know many of the individuals involved.

Here they are for your edification, in no particular order. You will notice a constantly recurring theme of hubris.

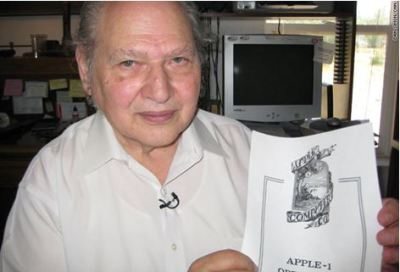

1) Ron Wayne’s sales of 10% of Apple (AAPL) for $800 in 1976

Say you owned 10% of Apple (AAPL) and you sold it for $800 in 1976. What would that stake be worth today? Try $70 billion. That is the harsh reality that Ron Wayne, 76, faces every morning when he wakes up, one of the three original founders of the consumer electronics giant.

Ron first met Steve Jobs when he was a spritely 21-year-old marketing guy at Atari, the inventor of the hugely successful “Pong” video arcade game.

Ron dumped his shares when he became convinced that Steve Jobs’ reckless spending was going to drive the nascent startup into the ground and he wanted to protect his own assets in a future bankruptcy.

Co-founders Jobs and Steve Wozniak each kept their original 45% ownership. Today Jobs’ widow, Laurene Powel Jobs, has a 0.5% ownership in Apple worth $4 billion, while the value of Woz’s share remains undisclosed.

Today, Ron is living off of a meager monthly Social Security check in remote Pahrump, Nevada, about as far out in the middle of nowhere as you can get where he can occasionally be seen playing the penny slots.

2) AOL's 2001 Takeover of Time Warner

Seeking to gain dominance in the brave new online world, Gerald Levin pushed old-line cable TV and magazine conglomerate, Time Warner, to pay $164 billion to buy upstart America Online in 2001. AOL CEO, Steve Case, became chairman of the new entity. Blinded by greed, Levin was lured by the prospect of 130 million big spending new customers.

It was not to be.

The wheels fell off almost immediately. The promised synergies never materialized. The Dotcom Crash vaporized AOL’s business the second the ink was dry. Then came a big recession and the Second Gulf War. By 2002, the value of the firm’s shares cratered from $226 billion to $20 billion.

The shareholders got wiped out, including “Mouth of the South” Ted Turner. That year, the firm announced a $99 billion loss as the goodwill from the merger was written off, the largest such loss in corporate history. Time Warner finally spun off AOL in 2009, ending the agony.

Steve Case walked away with billions, and is now an active venture capitalist. Gerald Levin left a pauper, and is occasionally seen as a forlorn guest on talk shows. The deal is widely perceived to be the worst corporate merger in history.

Buy High, Sell Low?

3) Bank of America's Purchase of Countrywide Savings in 2008

Bank of America’s CEO Ken Lewis thought he was getting the deal of the century picking up aggressive subprime lender, Countrywide Savings, for a bargain $4.1 billion, a “rare opportunity.”

As a result, Countrywide CEO Angelo Mozilo pocketed several hundred million dollars. Then the financial system collapsed, and suddenly we learned about liar loans, zero money down, and robo signing of loan documents.

Bank of America’s shares plunged by 95%, wiping out $500 billion in market capitalization. The deal saddled (BAC) with liability for Countrywide’s many sins, ultimately, paying out $40 billion in endless fines and settlements to aggrieved regulators and shareholders.

Ken Lewis was quickly put out to pasture, cashing in on an $83 million golden parachute, and is now working on his golf swing. Mozilo had to pay a number of out of court settlements, but was able to retain a substantial fortune, and is still walking around free.

The nicely tanned Mozilo is also working on his golf swing.

4) The 1973 Sale of All Star Wars Licensing and Merchandising Rights by 20th Century Fox for Free

In 1973, my former neighbor George Lucas approached 20th Century Fox Studios with the idea for the blockbuster film, Star Wars. It was going to be his next film after American Graffiti which had been a big hit earlier that year.

While Lucas was set for a large raise for his directing services – from $150,000 for American Graffiti to potentially $500,000 for Star Wars– he had a different twist ending in mind. Instead of asking for the full $500,000 directing fee, he offered a discount: $350,000 off in return for the unlimited rights to merchandising and any sequels.

Fox executives agreed, figuring that the rights were worthless, and fearing that the timing might not be right for a science fiction film.

In hindsight, their decision seems ridiculously short-sighted.

Since 1977, the Star Wars franchise has generated about $27 billion in revenue, leaving George Lucas with a net worth of over $3 billion by 2012. In 2012, Disney paid Lucas an additional $4 billion to buy the rights to the franchise

The initial budget for Star Wars was a pittance at $8 million, a big sum for an unproven film. So, saving $150,000 on production costs was no small matter, and Fox thought it was hedging its bets.

George once told me that he had a problem with depressed actors on the set while filming. Harrison Ford and Carrie Fisher thought the plot was stupid and the costumes silly.

Today, it is George Lucas that is laughing all the way to the bank.

$150,000 for What?

5) Lehman Brothers Entry Into the Bond Derivatives Market in the 2000s

I hated the 2000s because it was clear that men with lesser intelligence were using other people’s money to hyper leverage their own personal net worth. The money wasn’t the point. The quantities of cash involved were so humongous they could never be spent. It was all about winning points in a game with the CEOs of the other big Wall Street institutions.

CEO Richard Fuld could have come out of central casting as a stereotypical bad guy. He even once offered me a job which I wisely turned down. Fuld took his firm’s leverage ratio up to 100 times in an extended reach for obscene profits. This meant that a 1% drop in the underlying securities would entirely wipe out its capital.

That’s exactly what happened, and 10,000 employees lost their jobs, sent packing with their cardboard boxes with no notice. It was a classic case of a company piling on more risk to compensate for the lack of experience and intelligence. This only ends one way.

Morgan Stanley (MS) and Goldman Sachs (GS) drew the line at 40 times leverage and are still around today but just by the skin of their teeth, thanks to the TARP.

Fuld has spent much of the last five years ducking in and out of depositions in protracted litigation. Lehman issued public bonds only months before the final debacle, and how he has stayed out of jail has amazed me. Today he works as an independent consultant. On what I have no idea.

Out of Central Casting

6) The Manhasset Indians' Sale of Manhattan to the Dutch in 1626

Only a single original period document mentions anything about the purchase of Manhattan. This letter states that the island was bought from the Indians for 60 Dutch guilders worth of trade goods which would consist of axes, iron kettles, beads, and wool clothing.

No record exists of exactly what the mix was. Indians were notoriously shrewd traders and would not have been fooled by worthless trinkets.

The original letter outlining the deal is today kept at a museum in the Netherlands. It was written by a merchant, Pieter Schagen, to the directors of the West India Company (owners of New Netherlands) and is dated 5 November 1626.

He mentions that the settlers “have bought the island of Manhattes from the savages for a value of 60 guilders.” That’s it. It doesn’t say who purchased the island or from whom they purchased it, although it was probably the local Lenape tribe.

Historians often point out that North American Indians had a concept of land ownership different from that of the Europeans. The Indians regarded land, like air and water, as something you could use but not own or sell. It has been suggested that the Indians may have thought they were sharing, not selling.

It is anyone’s guess what Manhattan is worth today. Just my old two-bedroom 34th-floor apartment at 400 East 56th Street is now worth $2 million. Better think in the trillions.

7) Napoleon's 1803 Sale of the Louisiana Purchase to the United States

Invading Europe is not cheap, as Napoleon found out, and he needed some quick cash to continue his conquests. What could be more convenient than unloading France’s American colonies to the newly founded United States for a tidy $7 million? A British naval blockade had made them all but inaccessible anyway.

What is amazing is that president Thomas Jefferson agreed to the deal without the authority to do so, lacking permission from Congress, and with no money. What lies beyond the Mississippi River then was unknown.

Many Americans hoped for a waterway across the continent while others thought dinosaurs might still roam there. Jefferson just took a flyer on it. It was up to the intrepid explorers, Lewis and Clark, to find out what we bought.

Sound familiar? Without his bold action, the middle 15 states of the country would still be speaking French, smoking Gitanes, and getting paid in Euros.

After Waterloo in 1815, the British tried to reverse the deal and claim the American Midwest for themselves. It took Andrew Jackson’s (see the $20 bill) surprise win at the Battle of New Orleans to solidify the US claim.

The value of the Louisiana Purchase today is incalculable. But half of a country that creates $17 trillion in GDP per year and is still growing would be worth quite a lot.

Great General, Lousy Trader

8) The John Thomas Family Sale of Nantucket Island in 1740

Yes, my own ancestors are to be included among the worst traders in history. My great X 12 grandfather, a pioneering venture capitalist investor of the day from England, managed to buy the island of Nantucket off the coast of Massachusetts from the Indians for three ax heads and a sheep in the mid-1600s. Barren, windswept, and distant, it was considered worthless.

Two generations later, my great X 10 grandfather decided to cut his risk and sell the land to local residents just ahead of the Revolutionary War. Some 17 of my ancestors fought in that war including the original John Thomas who served on George Washington’s staff at the harsh winter encampment at Valley Forge during 1777-78. Maybe that’s why I have an obsession about not wasting food?

By the early 19th century, a major whaling industry developed on Nantucket fueling the lamps of the world with smoke-free fuel. By then, our family name was “Coffin,” which is still abundantly found on the headstones of the island’s cemeteries.

One Coffin even saw his ship, the Essex, rammed by a whale and sunk in the Pacific in 1821 (read about it in The Heart of the Sea by Nathaniel Philbrick, to be released as a movie in 2015). He was eaten by fellow crewmembers after spending 99 days adrift in an open lifeboat. Maybe that’s why I have an obsession about not wasting food?

In the 1840s, a young itinerant writer named Herman Melville visited Nantucket and heard the Essex story. He turned it into a massive novel about a mysterious rogue white whale, Moby Dick, which has been torturing English literature students ever since. Our family name, Coffin, is mentioned seven times in the book.

Nantucket is probably worth many tens of billions of dollars today as a playground for the rich and famous. Just a decent beachfront cottage there rents for $50,000 a week in the summer.

The Ron Howard film The Heart of the Sea came out a few years ago, and it is breathtaking. Just be happy you never worked on a 19th-century sailing ship.

Yes, it’s all true and documented.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/Moby-Dick.jpg389387DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2018-12-27 01:07:372018-12-26 18:32:31The Eight Worst Trades in History

I am ever on the lookout for disruptive technologies that lead to great investment opportunities. Sitting here next door to Silicon Valley, that is not hard to do.

So I watched my TV with utter amazement the other day when I saw a 3-D printer create an entire car from scratch. It took ten hours to build the body, and the rest of the day to bolt on the electric motors, axels, wheels, and the rest of the parts.

Beyond the drive train, the vehicle has only 50 parts. This compares to the 5,000 or 6,000 parts needed for a conventional car. There’s a gigantic labor and cost saving right there.

I have to admit that I came late to the 3-D printing scene. When hobbyists started making colorful figurines on their printers a few years ago, I thought it no more than a niche of a few passionate geeks who are in such abundance here.

That was a good thing because the initial batch of stock market plays all went meteoric, then crashed and burned.

Such is often the case with cutting-edge technologies. You often don’t generate real profits until you get the second or third generation.

That’s the way the personal computer started which went mainstream with incredible speed in the early 1980s (to get the flavor of the day, watch the hit AMC series “Halt and Catch Fire”).

Then my biotech friends told me they were printing human organs substituting ink with cells. After that, I discovered that Elon Musk was using 3-D printers to build rocket engine parts at his Space X venture in Los Angeles.

Suddenly, I started to take the technology seriously.

Arizona-based Local Motors plans to take a great leap forward with the launch of a 3D printed car next year (click herefor their website).

Dubbed the “Strati” (layers in Italian), the vehicle is made of reinforced carbon fiber thermoplastic, or ABS. It has one fifth the weight of steel with ten times the strength. You can pick up the car with two hands.

The company planned to build two versions of its vehicle during the first quarter of 2016. One would be a low-speed battery car or so-called neighborhood electric vehicle priced between $18,000 and $30,000. Faster, higher-priced versions would come later.

While the entry costs to the auto industry are legendarily high, in the billions of dollars, Local Motors’ upfront expenses are miniscule by comparison. The 49 foot long printer needed to print the body costs only $50,000.

Oak Ridge National Labs in Tennessee is a partner in the project which helped develop the monster printer. Nuclear weapons historians will recall them as the first refiner of U-235 during WWII.

It is the first effort to fundamentally change the way cars are put together since Henry Ford modernized the auto assembly line 100 years ago.

Local Motors is an internet creation all the way. It obtained its original funding through crowdsourcing, and held an international contest to find a design. An Italian won, hence the name.

It’s hard to see the Strati threatening the Tesla (TSLA), or any conventional car manufacturer any time soon. The current car is not yet street legal, and only does 40 miles per hour.

There is no great trading or investment play here yet. It is still early days. Give it a year or two.

However, it could be a hint of great things to come. I’ll take mine in black.

For the YouTube video of and interview with the Strati engineer, click here.

Ah, But is the Girl Printed As Well?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/12/Strati-Car-e1449756259694.jpg299400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-21 01:07:552018-12-20 18:39:52Print Your Own Car

That seems to be the judgment of the markets today in the wake of the Fed’s decision to raise interest rates by 25 basis points. The overnight range for Fed funds is now 2.25%-2.50%.

The Dow Average soared by 350 points going into the decision. Then it plunged by 900 points to 23,200, a new low for 2018. It was one of the largest range days in market history.

Traders chose to focus only on the bad news and completely ignore the good. That makes this a totally “glass half empty” market.

Never mind Chairman Jerome Powell’s statement that the Fed was cutting back its 2019 forecast from three interest rate hikes to only two. Stocks should have rallied 1,000 points on just that! And they still might!

Powell also redefined the meaning of the word “neutral”, taking it down from 3.0% to 2.8%. That means only one more quarter-point hike would take us to the low end of neutral, and that might be it. That should have been worth another 1,000 points, and we still might get that as well.

The Fed affirmed that the economy is still generally strong and that unemployment is at historic lows. Nothing to worry about here.

You can see where I’m going with this.

Down 3,800 points from the October high, stocks are now approaching stupidly cheap prices and valuations. Call it insanely cheap. What we are seeing here is the coiling up of a spring that will lead to an explosive upside move.

That may happen with the quadruple witching options expiration on Friday, the last real trading day of the year. It may wait until January 2, the first trading day of 2019. But coming it is.

And let me throw a theory at you which a hedge fund friend bounced off of me yesterday while I was on one of my legendary night hikes.

What if we really have been in a bear market since January 31 and we are now approaching the end of it? That would give us a typical one-year long bear market from which we are about to blast out to the upside.

When does this new bull market begin? When the last week hands intent on avoiding another 2008 repeat bails on their holdings. In other words, it could happen any day now.

Interesting food for thought.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-20 01:07:332018-12-19 19:06:46The Glass Half Empty Market

Blue chip growth stocks? Diamonds? Residential real estate? Gold?

No, I am talking about grand pianos manufactured by Steinway & Sons of Queens, New York.

Did you say pianos?

Yup, the kind with which you sit down and play “As Time Goes By.” (Casablanca).

During the 19th century, there were over 1,200 US piano makers manufacturing a product which can include more than 12,000 parts. It was the technological Boeing 474 of its day.

Today, there are only five American piano makers, and just one, Steinway, is considered investment grade.

That’s because when Carnegie Hall, London’s Royal Albert Hall, or Beijing’s Concert Hall National Grand Theater is in the market for a new concert grand piano, they only consider Steinways.

You can start with an entry level 5’1” Steinway Model M baby grand piano, or ostentatiously splurge with an opera house filling nine-foot-long concert grand Model D.

I received the bad news from my kids’ piano teacher a few months ago. After six years of lessons, they had outgrown their piano, a modest entry level 1966 Wurlitzer spinet.

I approached the matter as I do everything, with exhaustive, no stone unturned research. What I learned was fascinating.

Given the available space in my home and the kids’ commitment to the enterprise, I decided that a seven-foot Steinway Model B would do.

My first visit was to the local Steinway dealer. For a mere $100,000, and $110,000 with tax I could buy a brand new 6’11” Model B.

For an extra $15,000 I could buy a model B with the Spirio technology that enabled the piano to play itself to incredible symphony standard.

Financing was available at a hefty 10%, compared to only 2% for my Tesla. Banks are not allowed to accept pianos as collateral.

Steinway also sells used pianos, but will only go back 15 years, getting me down to the $70,000 range. I thought I’d look around more.

So I plunged into my favorite source of incredible, once-in-a-lifetime deals, eBay (EBAY).

The offerings were vast.

They included everything from a $13,500 1897 Model B in desperate need of a complete $30,000 rebuild to a 2013 Model B in showroom condition for $87,500.

Obviously, I had my work cut out for me especially since I am not a musician myself. Coming from a family of seven kids, there was never enough money for music lessons.

Thus, I have been a lifetime consumer of music rather than a producer.

It turns out that, like Rolls Royce’s (that other great unknown inflation hedge), no one ever throws a Steinway away. A fully restored 130-year-old model can almost cost as much as a new one.

And there is your inflation play.

The list price for a Steinway Model B in 1900 was $1,050. Some 117 years later, it is up 100-fold, giving you a compound annual growth rate of 3.97% a year.

This compares to 5.18% for ten-year US Treasury bonds, and 9.71% for the S&P 500 over the same time period. But then you can’t play a stock certificate, let alone make your kids practice on it.

A Steinway is, in fact, the perfect instrument with which to make these long-term inflation calculations.

Vintage cars, diamonds, and homes are all unique, have varying quality, and are all susceptible to overvaluation and hype from aggressive salesmen and dealers. Even gold coins can have huge differences in valued based on grade and rarity.

Save for a few patents issued in the 1930s covering keyboard and soundboard manufacturing, Steinways are built almost identically to the way they were made 117 years ago. Tour their factory and you find workshops filled with primitive 100-year-old iron and wooden tools.

Every other manufactured product has seen massive productivity and technology improvements over a century that have caused real prices to completely collapse.

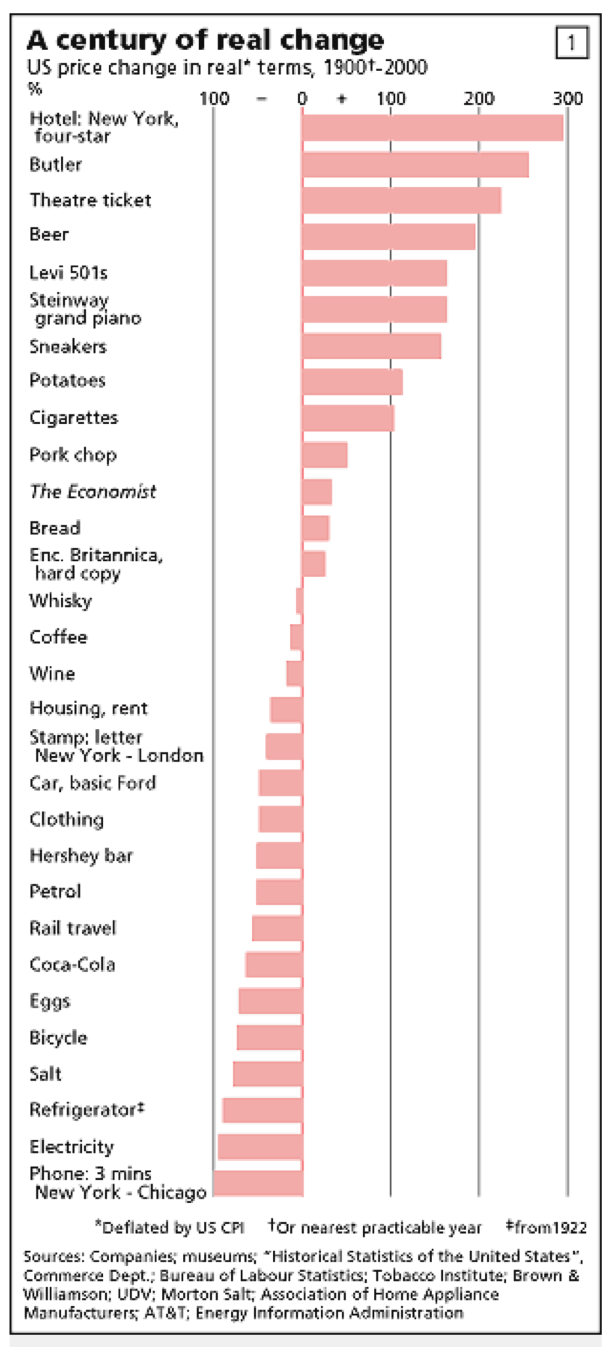

Take computers, for instance, which have suffered an average annual price decline of 30% since 1950. The cost of telephone calls has fallen by almost 100% in real terms since 1900 (see table below which I lifted from my former employers at The Economist)

That is the source of the rise in our standard of living.

It gets better. The prices of Steinways are rising fairly dramatically in real terms relative to almost everything else, thanks to a host of geopolitical reasons.

It turns out that the Chinese are taking over the global market.

While 200,000 pianos a year are sold in the US, the figure is over 1 million in China.

Many Chinese parents hope their children will achieve the international prominence of 35-year-old Lang Lang who commands millions of dollars a year in global performance and licensing fees. Many aspiring parents drive their kids to practice eight hours a day.

As a result, the Chinese have been buying up all the used premium pianos in the world including Steinways in the US, Bechsteins and Bosendorfers in Germany, Faziolis in Italy, and Yamahas and Kawais in Japan.

Whenever Chinese buy a luxury apartment in San Francisco, the first thing they do is outfit it with a Steinway grand piano even if they don’t play. It is the ultimate status symbol not only because of the price they pay but the space it takes up.

As a result, Steinways not only sell at a large premium to other pianos but are dear relative to ALL manufactured products over the expanse of time.

Researching the history of Steinway, you find a storied company that has undergone the sad but familiar travails of American manufacturing over the last century.

In short, it’s a miracle that this company still exists.

The first pianos were sold by a German immigrant from Hamburg in 1856. By 1972, a lengthy strike and competition from Japanese imports forced the original Steinway family to sell out to CBS after five generations.

Then there was a brief but disastrous experiment with Teflon parts in the 1970s. Suddenly Steinways didn’t sound like Steinways.

A private equity deal followed in 1985. From 1996 to 2013 it traded on the New York Stocks exchange under its own ticker symbol (LVB) (for Ludwig von Beethoven).

Steinway was then bought by my friend and newsletter client, hedge fund legend John Paulsen for $500 million. It produced its 600,000th piano in 2015.

If you want to watch a film about old-fashioned American manufacturing, vanishing skills, the pride of craftsmanship and working with your hands, watch the highly entertaining documentary movie “Note by Note: The making of Steinway L1037.”

It has won several awards.

It is wonderful to watch with the kids in that it shows what work was like in the old United States I remember, and can be streamed online for $4.99 by clicking here. https://www.amazon.com/Note-Harry-Connick-Jr/dp/B002ZS0R5I/ref=tmm_aiv_swatch_0?_encoding=UTF8&qid=&sr=

As for my own Steinway search, it had a very happy ending.

eBay enabled me to find a local Craigslist listing in Jackson, Mississippi for a 1951 Model B that was originally purchased by the University of Mississippi Music Department. It had been played by every noted pianist touring the South for a half century.

Some 20 years ago, a local doctor then purchased it right off the stage at a university surplus equipment sale.

This year the doctor retired, sold his mansion but had no room for a grand piano in his rapidly downsizing lifestyle.

He listed the piano for a low-ball price of $18,000, the cost of his 1997 ground up restoration. After I had a professional musician visit the house to check the condition and tone, I was the only bidder.

I figure if the kids ever get sick of practicing, I can always flip it to the Chinese for double. That’s me, always the trader.

I am totally comfortable buying big-ticket items off of eBay as I have been trading there for 20 years. I have bought five cars there for assorted family members.

If you aren’t comfortable with eBay, there is always Bruno.

Dallas, Texas-based Maestro Bruno Santo is a Julliard graduate, former Steinway dealer, and the most knowledgeable individual I ran into during my far-ranging research. He is also quite the salesman.

He runs a high-volume, low-margin business model which I admire and can probably get you a very nice Steinway in the mid $30,000s.

To learn more about the interesting and beautiful world of Steinway pianos, please visit the company’s website at http://www.steinway.com

Getting an 800-pound finely tuned musical instrument from Jackson, Mississippi to San Francisco, California is a whole new story on its own.

What I learned about the national trucking industry was amazing, and boy, did I get a deal!

Watch for my future research piece on “What I learned Moving My Steinway Grand Piano.”

As for the old Wurlitzer, it is now happily ensconced in my Lake Tahoe beachfront estate. Neighbor Michael Milliken has already completed the quality of the play.

The Winning Bid

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-19 01:06:122018-12-18 18:34:57The Great Inflation Hedge You’ve Never Heard Of

It was 38 years ago today that Apple (AAPL) went public and has generated a 43,000% return since its $22 IPO price. If you bought one share of Apple way back then for $22 it would be worth a breathtaking $95,000 today.

I waited until the next crash and then bought it at $4, and it sits in one of my “no touch” ultra-long-term retirement portfolios today.

Suddenly, the torture I endured taking Steve Jobs around to visit the New York institutional investors during the early 1980s was worth it.

The great rule of thumb I have learned after 50 years of investment is that if you hold a stock long enough, the dividend will exceed your original capital cost, giving you a 100% a year annual cash flow.

Three months ago, Apple was the Teflon stock of the entire market, the company that could do no wrong, the only “safe” stock that traded. Any selling met a wave of buying from Oracle of Omaha Warren Buffet and Apple itself, limiting corrections to a feeble 4%.

What a difference three months make!

Now the shares have become a market pariah, targeted by algorithms and hedge funds alike, and beaten like the proverbial red-headed stepchild. As a result, the shares have plunged an eye-popping 29.61%, vaporizing $311 billion in market capitalization.

Which begs one to ask the question, “What’s the matter with Apple?” How can things go from so right to so wrong?

Just like success has many fathers, failure is an orphan.

The harsh truth is that Apple became too much of a good thing to too many people. Expectations had become excessive and it had become too widely owned by traders with weak hands. In other words, people like me.

I had been cautious of Apple for a while because if its massive China exposure. You don’t want to own a company that relies entirely on Middle Kingdom production during a running trade war. Apple sold an incredible 216 million iPhones in 2017, and all of them are made at the Foxconn factories in southern China.

Apple has become the whipping boy for both sides in the trade conflict. The company has always run the risk of its Foxconn workers arriving at work late someday, or not showing up at all at the prodding of Beijing. Recently, Trump said iPhones imported from China could be subject to the current 10%, soon to be 25% tariff.

The final nail in the coffin came on Monday morning when we learned of a lower Chinese court’s ruling against Apple in a lawsuit from QUALCOMM (QCOM). Never mind that the suit was years old and applied only to the company’s older phones. With the shares in free fall, that is just what investors DIDN’T want to hear.

However, Apple is not dead, it is just resting. Or, call it ripening.

Not only could Apple recover strongly from these abysmal levels, IT COULD DOUBLE IN VALUE.

The core of my argument (no pun intended) is that Apple is in the process of fundamentally evolving its business model. It is rapidly morphing from a one-time sale only hardware company to a recurring subscription services company. And that is where the big money is in the future.

Microsoft (MSFT) is already doing it, so are Amazon (AMZN) and Netflix (NFLX). In fact, everyone is doing it, even the Diary of a Mad Hedge Fund Trader.

In fact, Apple's services revenue could balloon to $100 billion in five years, compared to its estimated total sales this year of $265 billion.

This accomplishes several important things. It moves the company out of a 30% gross margin business to a 70% gross margin. It converts Apple from a highly cyclical to stable earnings growth. Stable earnings growth companies are awarded much higher share price multiples.

Look no further than my next-door neighbor, Clorox (CLX), which trades at a much loftier 23X multiple and Coca-Cola (KO) which can be found at generous 19X multiple. Earnings visibility is worth its weight in gold. This could make Apple’s current 14X multiple a thing of the past.

Of course, we are not going to see a straight line move from one dominant business to another, and the road along the road could be bumpy. We could easily see one more meltdown which takes us to the subterranean $160 handle.

But $10 of downside risk versus $170 of upside? I’ll take that all day long. I bet you will too!

Time for a Nibble?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-13 06:10:042018-12-13 06:08:30What’s the Matter With Apple?

The Mad Hedge Fund Trader is seeing its biggest one-day gains since the inception of our Trade Alert Service 11 years ago. By the time you read this, we will have picked up an astounding 11% profit for the entire portfolio in 24 hours.

However, this being Halloween, I don’t want to sound like I’m whistling by the graveyard. But what I am about to say will scare the daylights out of you.

I hate to say I told you so but my prediction a year ago that the bull market would end on May 10, 2019 at 4:00 PM is starting to look pretty good.

If I am right, the charts for the S&P 500 (SPY) are setting up a classic head and shoulders top. The left shoulder was created by the January 2018 rally to $282.

We just saw the head created at the beginning of October at $293. All that remains is to build the right shoulder back up to $282 by the spring. What will then follow is the crying.

This is not a matter of throwing a dart at a calendar or reciting a chant taught to me by a long-dead Yaqui Indian. It is a simple matter of math. Here’s how it goes:

*The Fed Raises funds rate 25 basis points per quarter for the next four quarters to 3.25%

*The Yields Curve Inverts, taking short rates higher than long rates now at 3.15%

*Bond yield spread trades increase massively going into the inversion as traders ramp up the size to make up for shrinking spreads.

*When the spread turns negative, they dump everything, creating an interest rate spike to 4% or 5%.

*Inverted yield curves last an average of 14 months or until February 2020 in this cycle when a recession begins.

*Stock markets peak on average seven months before recessions, and you arrive at Friday, May 10, 2019 at 4:00 PM EST as the date for the demise of the bull market. At that point, it will be ten years and two months old, the longest such move in history.

A lot of people asked why I sent out so few trade alerts during the summer and going into the fall.

In fact, the list of negatives has reached laughable proportions:

*Longest bull market in history

*In the face of rising interest rates

*In the face of rising oil prices

*Rising inflation

*Nothing else to buy

*Only bull market in the world

*Valuations approaching two-decade highs

*Overwhelmingly concentration in big cap tech

*Double top in the market on an Equal Weight S&P 500 chart

*Record retail inflows into ETFs

*Recession has already started in the auto industry

*Recession has already started in the housing industry

*Rotation to value defensive stocks underway

*Massive unicorn IPOs planned in 2019- $215 billion

*Slowing GDP Growth 4.2% to 3.5%

*Large amount of economic growth sucked forward from 2019 as businesses accelerate Chinese imports to beat the tariffs

*The same is going on in China to buy our exports

Should you throw up your hands, dump all your stocks, and hide out in cash?

Absolute not! In fact, the last six months of a bull market are often the most profitable. Many tech stocks like Micron Technology (MU) and Advanced Micro Devices (AMD) have dropped by half in recent months. That means they have to double to get back to their old highs.

Other big quality stocks such as Amazon (AMZN) and Netflix (NFLX) have plunged by 30% and only have to appreciate by 43% to hit highs. It is, in fact, the best entry point for large-cap tech stocks since 2015 with valuations at a three-year low.

If I am wrong, the trade war with China plunges us into recession and ends the bull market sooner. Almost all the “worry” items on the list above are getting worse by the day.

Save That Date!