Stock markets are only in the business of discounting what happens next. I spend so much time anticipating the coming moves in shares that I can't even remember what I had for breakfast.

This is why technical analysis is such a bust as an investment strategy, except on an intraday basis only, as it is entirely founded on historical data. It is 100% backward looking.

So, I'll take you through the same thought experiments that convinced me to adopt a much more aggressive stance toward the markets after spending two months hiding in the weeds.

What happens after stocks hit new highs? They hit new lows, as they did on April 1, when the Dow Average plunged to 23,600.

What happens after markets hit new lows? They hit new highs again, supported by the strongest earning reports in history, which begin on Friday, April 13.

What happens after the inflation scare we received in the January Nonfarm Payroll Report with the surprise pop in average hourly earnings?

Inflation non-events, which unfolded with average hourly wages that came in subdued with the February and March Nonfarm Payroll Reports.

What follows a trade war? Trade peace, which is yet to come, but will arrive eventually nevertheless.

All of this points to stock markets that are in the process of putting in the lows for 2018. That means it is time to start ramping up your risk, as I did with three rapid Trade Alerts yesterday.

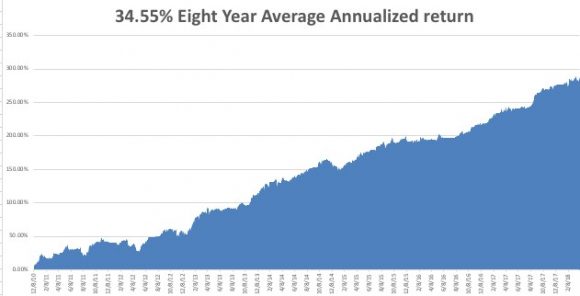

What does this look like on the charts? Alphabet (GOOGL) is a perfect example, which is in the process of putting in a very convincing triple bottom around the $1,000 level, right around the 200-day moving average.

What if I'm wrong?

After all the trade war continues to inflame by the day, the algorithms are still running amok, and the president still has a Twitter account.

What did it today? The Congressional Budget Office forecast of $1 trillion deficits running indefinitely? Or the FBI raids on the offices of the president's personal lawyer?

Then markets will edge down to the next support levels, about 4% lower than the most recently visited bottom, or about 22,600 in the Dow Average.

So, it would seem that the really smart thing to do here is to build options positions that can take that 4% hit, and STILL expire at their maximum profit points.

And this is exactly what I have been doing for the past two weeks: piling on long positions in the best technology stocks, and adding to short positions in bonds.

For fans of LEAPS, long dated out-of-the-money option call spreads one year or more out, this is the best time this year to get involved.

I'll give you an example.

BUY one June 21, 2019 $1,000 call at $145.00

SELL one June 21, 2019 $1,050 call at $120.00

NET COST = $25.00

In the event that (GOOGL) closes over $1,050 on June 21, 2019, or up 3% from today's closing level, the profit on this position would amount to $25.00 from an initial cost of $25.00, or a 100% gain in 14 months.

The only catch is that if the recession comes sooner than expected, the value of this position falls to zero in 14 months.

If you go deeper out-of-the-money with your strike prices, the potential profit rises by a multiple.

You can generate this kind of astronomical return with any of the FANGs assuming no real movement of the stock in a year.

It looks pretty good to me.

You heard it here first.

Winter Is Ending