Over the last few weeks, I picked up some astonishing developments in artificial intelligence.

*Mainframes at Stanford University and the University of California at Berkeley were given a direct connection to speak freely with each other. Within 30 minutes they dumped English as a means of communication because it was too inefficient and developed their own language which no human could understand. They then began exchanging immense amounts of data. Fearful of what was going on, the schools unplugged the machines after only eight hours.

*All of the soccer videos ever recorded were downloaded into two robots, but they were not taught how to play the game or given any rules. Not only did figure out how to play the game, it developed plays and maneuvers no one in the sport has ever thought of in its 150-year history.

*It normally takes a PhD candidate five years to 3D map a protein. An AI app 3D mapped all 200 million known proteins in seven weeks, shortcutting one billion years of PhD level research with existing technology. These new maps have already been used to design a malaria vaccine and enzymes that eat plastic. They will soon cure all human diseases.

*A developer asked an AI program a half dozen questions in Bengali, not an easy language. Within an hour, it spoke the language fluently, without any instructions to do so.

By now, word has gotten out about the incredible opportunities AI presents. Our only limitation is our own imagination on how to use it. AI will instantly triple the value of any company that uses it.

What has changed is that we now have millions of computers powerful enough and an Internet fast enough to realize its full potential.

It all vindicates my own long-term vision, unique in the investing community, that in the coming decade, immense technology profits will more than replace the trillions of dollars worth of Fed liquidity we feasted on during the 2010s. Extended QE is proving just a bridge to a much more prosperous future.

The Internet has created about $10 trillion in value since its inception. AI will create double that in half the time. That’s what will take the Dow from 33,000 to 240,000.

No surprise then that the top ten AI companies have delivered 120% of the stock market gains so far in 2023. The other 490 companies in the S&P 500 have either gone nowhere to down.

However, there are many things that AI can’t do. Here is the list.

1) AI Can’t Predict large anomalous events, otherwise known as Black Swans. AI takes past trends and extrapolates them into the future. It in no way could have seen 9/11, the 2008 crash or the pandemic coming, although I warned my hedge fund clients for years that we were overdue. All of the AI stock trading apps I have seen so far, including my own, max out at 90% accuracy. The other 10% is accounted for by black swans: earnings shocks, foreign crises, sudden FDA stage three denials, surprise legal judgments, foreign invasions, or the murder of a key man in a tech company, as recently happened in San Francisco.

2) AI Lies and Lies Often. AI was asked to write a scientific paper on a specific subject. It came back with an elegant and well-researched piece. The problem was that all of the books it made reference to didn’t exist. AI learned early to tell humans what they want to hear.

3) AI Requires Exponential Computing Capacity. Only five companies have the muscle to pursue true AI. No surprise that these, including (AAPL), (GOOGL), (AMZN), and (TSLA), account for the bulk of stock market performance this year. This won’t always be the case. Some 30 years ago, it required thousands of mainframes to contain all human knowledge. Today, that task can be accomplished with a cheap $1,000 laptop.

4) Internet Capacity Will Be a Limiting Factor for AI for Years. To accommodate the traffic that is taking place right now, the Internet will have to grow 500% practically overnight, and that is with five main players. What happens when we have 5 million? That’s why NVIDIA (NVDA) has gone nuts.

5) AI Hallucinates, as anyone who drives a Tesla will tell you. If a car makes a left turn in Florida, the 4 million vehicles in the world’s largest neural network learn from it. The problem is that sometimes the data from that Florida car is placed directly in front of a California one, prompting it to brake abruptly, causing accidents. This is known as “ghost braking.” I have explained to Elon Musk that his database has grown so large, eight video feeds per 4 million cars going back many years and billions of miles, that he may be going behind the limits of known physics.

6) While the Growth Opportunities for AI are Unlimited, the ability of humans and society to absorb it isn’t. All jobs will be affected by AI and millions destroyed, starting with low-level programmers and call centers, and millions more will be created. People are talking about regulating AI but have no idea where to start. Maybe with (AAPL), (GOOGL), (AMZN), and (TSLA)?

7) The Terminator Issue. Can AI be controlled? Or have we started a chain reaction that is unstoppable, as with an atomic bomb? AI researchers have noticed a disturbing issue where AI programs are learning skills on their own, without our instructions. This is referred to as “emergent properties.” If AI is using humans as its example, we can’t exactly count on it to be benign.

Needless to say, AI will be at the core of your investment approach, probably for the rest of your life.

2014 at Micron Technology

https://www.madhedgefundtrader.com/wp-content/uploads/2019/02/John-micron.png358293Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-31 09:02:022023-05-31 16:42:24What AI Can and Can’t Do

I have always believed that markets will always do whatever they have to do to screw the most people and it is doing that right now with a vengeance.

Some $750 billion has poured into cash and equivalents since January 1. Margin debt is now at the Dotcom bust low of 1.4% of the S&P 500 not seen since 2002. Equity Allocations are at a 15 Year Low, with massive amounts of cash in 90-day T-bills now yielding 5.25%.

The broader market is expensive looking at 19 times 2023 earnings. But take out the top five performing FANGS and we are down to a very reasonable 15 times for the remaining 495 stocks.

I told you this would happen, that the bear market ended on October 15 and that big tech would lead any recovery. I reiterated this view in depth with my 2023 All Asset Class Review on January 4 (click here for the link).

In the meantime, a lot of investors had angry conversations with investment advisors this week as to why they didn’t own NVIDIA (NVDA). They heard it was too expensive, that it had already moved too much (triple since October 15), the government was going default on its debt, and that we were headed into recession.

Suffice it to say that if they lived here with me in Silicon Valley, they wouldn’t take this view. The world is going NVIDIA crazy on a huge earnings beat, taking the shares up 30%. Q1 revenues came in at $7.2 billion versus an expected $6.5 billion. Demand from AI and data centers is surging.

(NVDA) has been a core Mad Hedge holding since it went public a decade ago. It is now up 175-fold and has at least another seven bagger ahead of it. (NVDA) has matched the 175-fold gain we caught with our 2010 recommendation for Tesla. The (NVDA) January 2025 LEAPS I recommended on September 29 at 50 cents is now worth $6.25 and expires worth $10, up 20-fold!

It all vindicates my own long-term vision, unique in the investing community, that in the coming decade, technology profits will more than replace the Fed liquidity we feasted on during the 2010s.

The Internet has created about $10 trillion in value since inception. AI will create a lot more than that. That’s what will take the Dow from 33,000 to 240,000.

In the meantime, new home building is incredibly going from strength to strength and is one of the few domestic sides of the economy that is prospering mightily. New Home Sales hit a 13-Month High, up 4.1% in April. If you had told me five years ago that while 30-year fixed mortgage rates were at a two-decade high of 7.0%, demand for new homes was so strong that builders were running out of inventory, I would have told you that you were out of your mind.

Yet, here we are.

This is because half of the builders that went bust in the 2008 subprime housing crash never came back, creating a structural shortage of homes that will take 20 years to return to balance.

Baby boomers now aged 61 to 78 rushed to buy homes in their late 20s during the prosperity of the 1960s and 1970s. Only 10% paid cash for their homes, many of whom worked on Wall Street, like me.

Some 75 million Millennials are now buying homes in their mid 30’s and are therefore much wealthier than previous generations. Working in tech like my kids, some 35% are paying all cash and are immune to the interest rate cycle. That means they can afford much nicer homes than we boomers could.

Those who do borrow plan to refi quickly in a year or two when mortgages are back below 5.0%. Then the residential real estate will absolutely catch on fire. Buy (TOL), (LEN), (KBH), and (PHM) on dips.

Oh, and buy boatloads of bonds (TLT) too.

There is another angle to the story that is fascinating. High housing prices are turning Yankees into Confederates and Hawaiians into cowboys.

An onslaught of my friends have recently retired from New York for the green hills of North Carolina. The problem is that if I moved there, they’d be burning crosses on my front lawn in the first week.

Natives Hawaiians have fled their green hills for the Nevada deserts because they can’t afford to live there anymore, moving from an $800,000 median homes price to $400,000. When I was in Las Vegas a few weeks ago, I noticed ads for a hula contest, Hawaiian language lessons at the county library, and SPAM at Safeway. Outrigger canoes have been spotted on a disappearing Lake Mead. The chief complaint? Leis wilt a lot faster in the dry desert air.

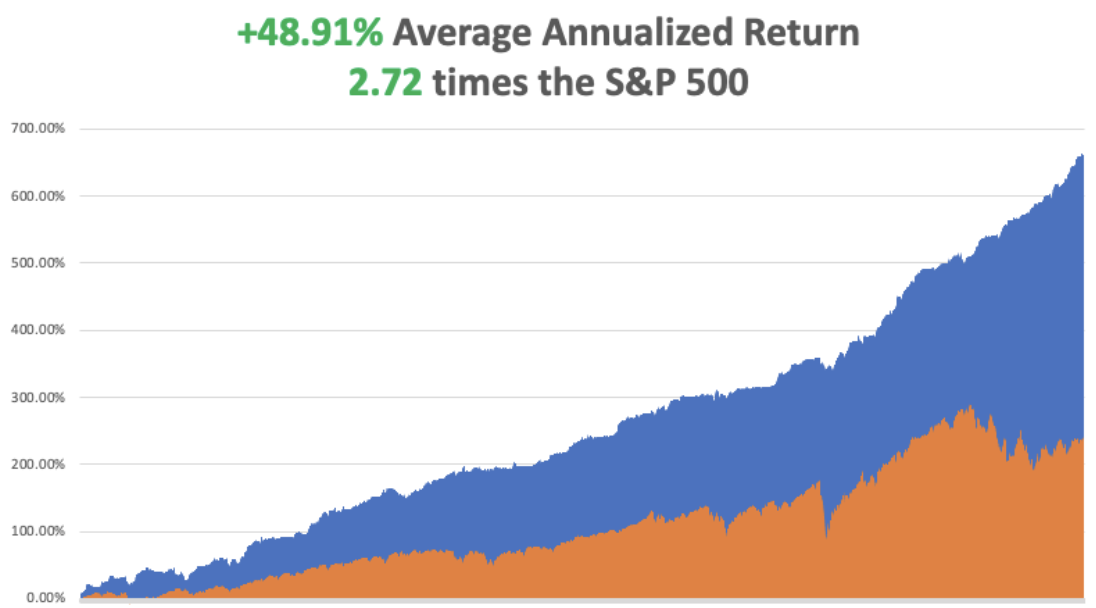

So far in May, I have managed a modest 1.38%profit. My 2023 year-to-date performance is now at an eye-popping +63.13%.The S&P 500 (SPY) is up only a miniscule +10.53%so far in 2023. My trailing one-year return reached a 15-year high at +108.59% versus +12.02%for the S&P 500.

That brings my 15-year total return to +660.32%. My average annualized return has blasted up to +48.91%,another new high, some 2.72 times the S&P 500over the same period.

Some 41 of my 44 trades this year have been profitable. My last 22 consecutive trade alerts have been profitable.

I executed no trades last week, content to run my long in Tesla and a short in Tesla, the “short strangle” strategy. I now have a very rare 80% cash position due to the lack of high-return, low-risk trades. I ran a rare loss last week because while my long in Tesla is now at max profit, my short is approaching its near strike. That goes with my philosophy of when you’re wrong, be small. When you’re right, go big.

Ford (F) Cuts Deal with Tesla to Share National Charger Network, putting Elon Musk well on his way to becoming the largest electric utility in the world. It won’t affect the existing 4 million Tesla drivers yet. Ford only sold 62,000 EVs in 2022 and 25,000 the year before. Access will be provided through adapters, the (F) adopting the Tesla charging standard. It kind of screws (GM) left on its own. It was worth a $13 pop for (TSLA). Keep buying (TSLA) on dips.

Divergence Between the S&P 500 and the S&P Equal Weight is the greatest since December 1999. The Dotcom Bubble topped four months later. It’s a function of concentration in the top five tech stocks, my “Five Aces” strategy. Risk is rising. The flight to big tech balance sheets and AI has been huge. You heard it here first.

Marvel Technologies (MRVL) Rockets 25% on Spectacular Earnings Beat, as the AI fever spreads out into infrastructure plays like second-line chip makers. Demand for integrated circuits from data centers, carrier infrastructure, networking, and the auto industry is off the charts. The Internet has to grow 500% quickly to accommodate new AI demand right now. The gold rush is on. Buy (MRVL) on dips.

Inflation Continues to Fall, down 0.4% in April according to the Personal Consumption Expenditures Index Price Index. Food prices rose 6.9% from a year ago while energy fell 6.3%.

Fitch Puts US Debt on Credit Watch, meaning that it is due for a downgrade. It’s the first time since the 2011 Moody’s downgrade from AAA to AA+. Threats of default have real-world consequences.

Pending Home Sales Collapse, unchanged from March, but down 20% YOY on a signed contract basis. Soaring interest rates get the blame. The northeast took the big hit.

Ely Lily Price Target Raised to $500, by Bank of America on the strength of their Ozempic weight loss drug. The stock is up fivefold since Mad Hedge recommended it five years ago. Keep buying (LLY) on tips.

30-Year Fixed Rate Mortgages Jump Back to 7.0%, on the impasse in Washington and default fears. The residential real estate recovery goes back on hold.

(TLT) Approaches 2023 Low. The closer we get to a debt ceiling deal, the lower we go. When a deal is done, it unleashes a new onslaught of bond selling by the Treasury, and lower lows on bonds. In the dream scenario, we fall all the way to $95 in the (TLT) where we will be issuing recommendations for call spreads and LEAPS by the boatload.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 29 is Memorial Day. All markets are closed.

On Tuesday, May 30 at 6:00 AM EST, the S&P Case Shiller National Home Price Index is printed.

On Wednesday, May 31 at 7:00 AM, the JOLTS Job Openings Report is out.

On Thursday, June 1 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, June 2 at 2:00 PM, the May Nonfarm Payroll Report is released.

As for me, with the 36th anniversary of the 1987 crash coming up this year, when shares dove 20% in one day, I thought I’d part with a few memories.

I was in Paris visiting Morgan Stanley’s top banking clients, who then were making a major splash in Japanese equity warrants, my particular area of expertise.

When we walked into our last appointment, I casually asked how the market was doing (Paris is six hours ahead of New York). We were told the Dow Average was down a record 300 points. Stunned, I immediately asked for a private conference room so I could call the equity trading desk in New York to buy some stock.

A woman answered the phone, and when I said I wanted to buy, she burst into tears and threw the handset down on the floor. Redialing found all transatlantic lines jammed.

I never bought my stock, nor found out who picked up the phone. I grabbed a taxi to Charles de Gaulle airport and flew my twin Cessna as fast as the turbocharged engines take me back to London, breaking every known air traffic control rule.

By the time I got back, the Dow had closed down 512 points. Then I learned that George Soros asked us to bid on a $250 million blind portfolio of US stocks after the close. He said he had also solicited bids from Goldman Sachs, Merrill Lynch, JP Morgan, and Solomon Brothers, and would call us back if we won.

We bid 10% below the final closing prices for the lot. Ten minutes later he called us back and told us we won the auction. How much did the others bid? He told us that we were the only ones who bid at all!

Then you heard that great sucking sound.

Oops!

What has never been disclosed to the public is that after the close, Morgan Stanley received a margin call from the exchange for $100 million, as volatility had gone through the roof, as did every firm on Wall Street. We ordered JP Morgan to send the money from our account immediately. Then they lost the wire transfer!

After some harsh words at the top, it was found. That’s when I discovered the wonderful world of Fed wire numbers.

The next morning, the Dow continued its plunge, but after an hour managed a U-turn, and launched on a monster rally that lasted for the rest of the year. We made $75 million on that one trade from Soros.

It was the worst investment decision I have seen in the markets in 53 years, executed by its most brilliant player. Go figure. Maybe it was George’s risk control discipline kicking in?

At the end of the month, we then took a $75 million hit on our share of the British Petroleum privatization, because Prime Minister Margaret Thatcher refused to postpone the issue, believing that the banks had already made too much money.

That gave Morgan Stanley’s equity division a break-even P&L for the month of October 1987, the worst in market history. Even now, I refuse to gas up at a BP station on the very rare occasions I am driving a rental internal combustion engine from Enterprise.

My Quotron Screen on 1987 Crash Day

Good luck and good trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/05/Screenshot-2023-05-31-at-3.24.25-AM.png6321086Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-30 10:02:292023-05-30 16:06:10The Market Outlook for the Week Ahead, or A Tale of Two Markets

Below please find subscribers’ Q&A for the May 24 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: Should I roll over my $55-$60 Freeport-McMoRan (FCX) 2024 LEAPS?

A: Yes, move it from the January 2024 expiration to January 2025—that gives you a full 18 months for the stock to recover from a recession (which it’s now discounting) and then double, which is where you make the really big money on our LEAPS.

Q: What's your year-end price prediction for Freeport-McMoRan (FCX)?

A: $50, this year’s high.

Q: If there’s a default, do members of Congress get paid?

A: No, they don’t, no money is no money, the cupboard is bare. Nothing gets paid. And the Treasury will have to choose who gets paid last because when they run out of money there's no money to pay anybody, which then leads to a default and a 50% stock market correction.

Q: Why do you buy in-the-money bull call spreads instead of selling credit spreads?

A: They’re easier to understand for beginners. It’s easier for people to understand that if you buy something and it goes up, you make money. It’s harder for people to understand that if you sell short something and it goes down, you make money. And it’s basically six of one and half a dozen of the other in terms of profit. I get that question constantly and that is always going to be the answer.

Q: What do you think about artificial intelligence; how will it affect stock prices?

A: It’ll be what takes the Dow average ($INDU) from $32,000 to $240,000 over the next 10 years. What AI does is it automatically triples the value of any company using it, even though now it may take years for the stock market to catch up. On top of that, companies will have their regular earnings growth from their traditional businesses.

Q: How far will Nvidia (NVDA) stock go up?

A: Well the consensus between fund managers is it goes up 7 times from here, to well over 1,000. It's at 300 today, so it sounds like 2,100 is the final target, assuming we don't have any more recessions. And by the way, we did recommend NVDA on a split adjusted basis around $2, so NVDA has gone up 175 times already from our initial recommendation 7 years ago when it was just a gaming play. The (NVDA) January 2025 LEAPS I recommended on September 29 at 50 cents is now worth $6.25 and expires worth $10, up 20-fold!

Q: How can companies be selling AI prediction services for traders, as no one can predict the future?

A: Well that is accurate, no one person can predict the future. However, algorithms can take patterns in the past, project them in the future, and they're often accurate as long as a black swan doesn’t happen. AI is getting so sophisticated now—not only do we have index predictions which we’ve been using now for almost 10 years to great success, but Mad Hedge is now services with single stock recommendations. They will say in 30 days (AMZN) will be at $X, and they’re right 90% of the time. This is getting very advanced very quickly, and we are at the absolute cutting edge of this (and have been for a long time), and that’s why we’re getting such spectacular results—it's me plus my algorithm.

Q: Are money market funds at risk if the US defaults?

A: If the US defaults and stays defaulted, then yes. Nothing anywhere is safe except gold bricks under the bed. If the US does default, they’ll get defaulted probably in days. And that's what happened last time, 12 years ago. So, I don't expect the world to end.

Q: What is the best strategy for a long-term retirement account?

A: If you're already retired like over 70, I would go 100% into fixed income, and spread out your fixed income exposure to 10-year treasuries which is now yielding 3.75%, to junk which is yielding 8.5%. And you might throw in a couple high dividend stocks like (CCI). Over age 70 you basically are looking for a 100% income portfolio, because you’re too old to go back to work at Taco Bell if you lose all your money. And believe me, I’ve been to Taco Bell and seen the 70-year-olds working there who did lose all their money, so you don’t want to do that. Equities are for younger kids like me, who are going to live forever.

Q: What about iShares 20 Plus Year Treasury Bond ETF (TLT)?

A: We’re watching very closely. We will do LEAPS, but I’m waiting for a capitulation selloff triggered by inaction in Washington to get there. Also, when they do reach a deal, it unleashes a bunch of bond selling by the government. The US Treasury is going to have to sell 700 billion dollars’ worth of bonds immediately, because they’re behind on their bills, how about that? They’re not paying military contractors. So yes, the initial move of a debt deal could be down for bonds—that's the move I'm waiting for.

Q: Are you buying at the money’s or out of the moneys on LEAPS?

A: At the money if you’re a conservative old fogie like me, and out of the money like 20% or 30% where you get like a 400% return for younger people so they still will live long enough to earn back all the money if they lose it.

Q: What do you think the next move on CBOE Volatility Index ($VIX) is?

A: Up, and I think we could see VIX at $30 sometime in June or July when our 10% selloff happens.

Q: Would you buy the ProShares UltraShort S&P 500 (SDS) now for protection?

A: Yes, I’d be buying some as a hedge against your long-term positions.

Q: Do you prefer one or two year LEAPS?

A: Two years is the more conservative maturity because it gives you two years to go into recession and get back out. If you think there isn’t going to be a recession and we reaccelerate from here, then you only want to do one year. With Treasuries bonds, I’m inclined to do one year because I think once the rise in prices happens it’ll happen very quickly. If you’re not happy with a 100% return in a year maybe you should consider another line of business.

Q: Is the housing market going to crash because of 7% mortgage rates?

A: No, one third of all the buyers now are cash buyers, who are spending their savings and will refinance when mortgages get back to 3% or 4%. Until then, housing prices go sideways because there is a severe shortage of housing nationwide, which is getting worse.

Q: How do I get my wife used to regenerative braking in Tesla (TSLA)?

A: Just take your foot off the acceleration pedal; as the car slows down, each of the four wheels perform as generators and recharge the battery. That means when you drive from Lake Tahoe at 7,000 ft down to the Central Valley at sea level, your power consumption is zero. You’re getting a free ride because you’re gravity powered, the wheels are recharging the battery the whole time. All you have to do is take your foot off the acceleration and the regenerative braking kicks in instantly. Teslas only use actual use brake shoes when they slowdown from five miles an hour down to zero.

Q: Which level is more likely this year in oil: $50 a barrel or $100?

A: Well, if we do get the recession or something close to it, we’ll see the $50 first, and then we’ll see the $100 on the recovery. That is what’s going to happen.

Q: When is the economic recovery going to be this year?

A: In the 4th quarter, starting in October, and the stock market will start discounting that in July or August. That is my view.

Q: What’s a better investment: stocks or real estate?

A: It depends on the person. At this level, stocks will probably deliver bigger returns than real estate. But real estate allows you 5-1 leverage. If you have an 80% mortgage, and that’s more leverage than most people can get in the stock market. The other thing about homes is that you don’t get to see the price every day in the newspaper and then panic and sell at the bottom. That's the other great thing about houses.

Q: Will this recording be available?

A: Yes we post it in about two hours on the website. You can look at all the charts and the commentary then.

Q: How would you hedge a 100% equity portfolio?

A: I would buy deep out of the money puts on the S&P 500, maybe 10% out of the money on puts—something like a 360 put on the SPY with a 2 month maturity. That gets you through the summer, gets you through any debt crisis, and certainly will reduce the volatility of your portfolio.

Q: Would you be buying Alibaba (BABA) down here?

A: No, I don’t want to get involved in China in anything—too much political risk.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

A Senior Citizen Teach Me the Computer at Taco Bell

https://www.madhedgefundtrader.com/wp-content/uploads/2023/05/taco-bell-lady.jpg324432Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-26 09:02:292023-05-26 11:45:51May 24 Biweekly Strategy Webinar Q&A

You can count on a bear market hitting sometime in 2038, one falling by at least 40%.

Worse, there is almost a guarantee that a financial crisis, severe real estate crash, and possibly another Great Depression will take place no later than 2058 that would take the major indexes down by 50% or more.

No, I have not taken to using an Ouija board, reading tea leaves, or examining animal entrails in order to predict the future.

I simply read the data just released from the National Center for Health Statistics, a subsidiary of the federal Centers for Disease Control and Prevention (click here for their link).

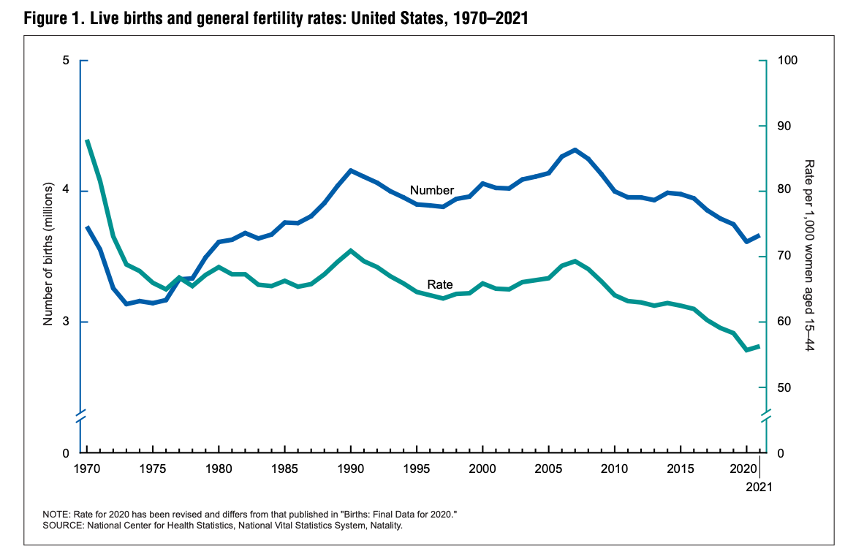

The government agency reported that the US birth rate fell to a new all-time low for the second year in a row, to 11 births per 1,000 women of childbearing age. A birth rate of 125 per 1,000 is necessary for a population to break even. The absolute number of births is 3,664,292, the lowest since 1987. In 2021, women had 37% fewer babies than in 2007.

These are the lowest number since WWII, when 17 million men were away in the military, a crucial part of the equation.

Babies grow up, at least most of them. In 20 years, they become consumers, earning wages, buying things, paying taxes, and generally contributing to economic growth.

In 45 years, they do so quite substantially, becoming the major drivers of the economy as “peak spenders”. When these numbers fall, recessions and bear markets occur with absolute certainty.

You have long heard me talk about the coming “Golden Age” of the 2020s. That’s when a two-decade-long demographic tailwind ensues because the number of “peak spenders’ in the economy starts to balloon to generational highs. The last time this happened was during the 1980s and in 19990’s stocks rose 20-fold.

Right now we are just coming out of two decades of demographic headwind, when the number of big spenders in the economy reached a low ebb. This was the cause of the Great Recession, the stock market crash, and the anemic 2% annual growth since then.

The reasons for the maternity ward slowdown are many. The great recession certainly blew a hole in the family plans of many Millennials. So did the pandemic. Falling incomes always lead to lower birth rates, with many Millennial couples delaying children by five years or more. Millennial mothers are now having children later than at any time in history.

Burgeoning student debt, which just topped $1.7 trillion is another. Many prospective mothers would rather get out from under substantial debt before they add to the population. So is a structural shortage of housing.

The rising education of women is another drag on childbearing and is a global trend. When spouses become serious wage earners, families inevitably shrink. Husbands would rather take the money and improve their lifestyles than have more kids to feed.

Women are also delaying having children to postpone the “pay gaps” that always kick in after they take maternity leave. Many are pegging income targets before they entertain starting families.

As a result of these trends, one in five children last year were born to women over the age of 35, a new high.

This is how Latin American moved from eight to two-child families in only one generation. The same is about to take place in Africa, where standards of living are rising rapidly, thanks to the eradication of several serious diseases.

The sharpest falls in the US have been with minorities. Since 2017, the birthrates for Hispanics has dropped by 27% from a very high level, African Americans 11%, whites 5%, and Asian 4%.

Europe has long had the same problem with plunging growth rates but only much worse. Historically the US has made up for the shortfall with immigration, but that is now falling thanks to the current administration's policies. Restricting immigration now is a guarantee of slowing economic growth in the future. It’s just a numbers game.

So watch that growth rate. When it starts to tick up again it’s time to buy….in about 20 years. I’ll be there to remind you of this newsletter.

As for me, I’ve been doing my part. I have five kids aged 17-36, and my life is only half over. Where did you say they keep the Pampers?

I'm Doing My Part

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/John-and-family-story-1-image-e1526596823183.jpg266400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-25 09:02:492023-05-25 17:21:55They're Not Making Americans Anymore

I spent a sad and depressing but highly instructional evening with Dr. Stephen Greenspan, who had lost most of his personal fortune with Bernie Madoff.

The University of Connecticut psychology professor had poured the bulk of his savings into Sandra Mansky's Tremont feeder fund; receiving convincing trade confirms and rock-solid custody statements from the Bank of New York.

This is a particularly bitter pill for Dr. Greenspan to take because he is an internationally known authority on Ponzi schemes, and published a book entitled Annals of Gullibility - Why We Get Duped and How to Avoid It.

It is a veritable history of scams, starting with Eve's subterfuge to get Adam to bite the apple, to the Trojan horse and the Pied Piper, up to more modern-day cons in religion, politics, science, medicine, and yes, personal investments.

Madoff's genius was that the returns he fabricated were small, averaging only 11% a year, making them more believable. In the 1920s, the original Ponzi promised his Boston area Italian immigrant customers a 50% return every 45 days. My grandmother was tempted, but my grandfather nexed the idea, always the conservative guy.

Madoff also feigned exclusivity, often turning potential investors down, leading them to become even more desirous of joining his club.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/Madoff-story-2.jpg238320MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2023-03-14 08:04:252023-03-14 07:42:03How to Avoid Ponzi Schemes

I believe that the pandemic and hyper-accelerating technology is bringing forward the future at an astonishing rate.

More applications will be created in the next year than over the last 40, some 500,000. The sum total of human knowledge is now doubling every year. The profits spun off and investment opportunities will be incredible, which is why I just doubled my ten-year forecast for the Dow Average (INDU) from 120,000 to 240,000.

Here are ten major trends for the economy and the markets that we can see already. It’s the unseen ones that will be really interesting.

(1) The Insurance Industry Changes Beyond All Recognition, confirming from “Recovery After Risk” to “Prevention of Risk”. Today, fire insurance pays you after your house burns down. Life insurance pays your next of kin after you die. And health insurance (which is really sick insurance) pays only after you get sick. During the next decade, we’ll see a new generation of insurance providers that offer you a service to KEEP you healthy and keep your house safe during a wildfire. Also, full autonomous driving will cut hospital admissions by half, dramatically dropping the cost of insurance. This is driven by machine learning, ubiquitous sensors, low-cost genome sequencing, and robotics to detect risk, prevent disaster, and guarantee safety before any costs are incurred.

(2) Autonomous Vehicles and Flying Cars (eVTOL) will make travel cheaper and easier. Fully autonomous vehicles (TSLA), (GOOGL), car-as-a-service fleets, and aerial ridesharing (flying cars) will be fully operational in most major metropolitan cities in the coming decade. The cost of transportation will plummet 3-4X, transforming real estate, finance, insurance, the materials economy, and urban planning. Where you live and work, and how you spend your time, will all be fundamentally reshaped by this future of human travel. Your kids and elderly parents will never drive. Already, a half dozen eVTOL companies have gone public raising more than $10B to fuel their growth. These vehicles are real and will help define the decade ahead. This is driven by machine learning, sensors, materials science, battery storage improvements, and ubiquitous gigabit connections.

(3) On-demand Production and On-demand Delivery Will Create an “Instant Economy of Things”. Urban dwellers will learn to expect “instant fulfillment” of their retail orders as drone and robotic last-mile delivery services carry products from local supply depots directly to your doorstep. Further riding the deployment of regional on-demand digital manufacturing (3D printing farms), individualized products can be obtained within hours—anywhere, anytime. I ordered a new high-end 50-pound garage door opener from Amazon Prime (AMZN) last month after my old one went kaput. Incredibly, they delivered it in hours! This is driven by networks, 3D printing, robotics, and AI.

(4) The Ability to Sense and Know Anything, Anytime, Anywhere. We’re rapidly approaching the era where 100 billion sensors (the Internet of Everything) are monitoring and sensing (imaging, listening, measuring) every facet of our environments, all the time. Global imaging satellites, drones, autonomous car LIDARs, and forward-looking augmented reality (AR) headset cameras are all part of a global sensor matrix, together allowing us to know anything, anytime, anywhere. In this future, it’s not “what you know,” but rather “the quality of the questions you ask” that will be most important. That gives us old guys a huge advantage. This is driven by the convergence of terrestrial, atmospheric, and space-based sensors, vast data networks, 5G and 6G communication networks (AAPL), next-gen Wi-Fi, and machine learning.

(5) Advertising Hyper Evolves. As ads become the primary driver of new services for free, AI becomes increasingly embedded in everyday life and your custom personal AI will soon understand what you want better than you do. In turn, we will begin to both trust and rely upon our AIs to make most of our buying decisions, turning over shopping to AI-enabled personal assistants. Your AI might make purchases based on your past desires, current shortages, conversations you’ve allowed your AI to listen to, or by tracking where your pupils focus on a virtual interface (i.e., what catches your attention). As a result, the advertising industry—which normally competes for your attention (whether at the Superbowl or through search engines)—will have a hard time influencing your AI. This is driven by machine learning, sensors, augmented reality, and 5G/networks.

(6) Cellular Agriculture Moves from the Lab to Inner Cities, Providing High-quality Protein that is Cheaper and Healthier. The next decade will witness the birth of the most ethical, nutritious, and environmentally sustainable protein production system devised by humankind. Stem cell-based “cellular agriculture” will allow the production of beef, chicken, and fish anywhere, on-demand, with far higher nutritional content, and a vastly lower environmental footprint than traditional livestock options. Traditional legacy steaks found at Ruth’s Chris and Morton’s will only to available to the wealthy. This is driven by biotechnology, materials science, machine learning, and agtech.

(7) Your Brain Will Integrate with Super-Fast Hardware and Software. My friend, technologist and futurist Ray Kurzweil, has predicted that by the mid-2030s, we will begin connecting the human neocortex to the cloud. This next decade will see tremendous progress in that direction, first serving those with spinal cord injuries, whereby patients will regain both sensory capacity and motor control. Yet beyond assisting those with motor function loss, several BCI pioneers are now attempting to supplement their baseline cognitive abilities, a pursuit with the potential to increase their sensorium, memory, and even intelligence. Recent demonstrations of a macaque monkey playing Pong using a Neuralink implant is proof of incredible progress. This is driven by materials science, AI/machine learning, robotics, and some fantastic imaginations.

(8) High-resolution Virtual RealityWill Transform Both Retail and Real Estate Shopping & the Future of Education. If you were a couch potato, you are about to become one on steroids. High-resolution, lightweight virtual reality headsets will allow individuals at home to shop for everything from clothing to real estate—all from the convenience of their living room. Need a new outfit? Your AI knows your detailed body measurements and can whip up a fashion show featuring your avatar wearing the latest 20 designs on a runway. Want to see how your furniture might look inside a house you’re viewing online? No problem! Your AI can populate the property with your virtualized inventory and give you a guided tour. On the education front, the use of VR and AI-driven avatars with technology such as that demonstrated by Dreamscape promises a future of game-like, immersive, and powerful education and training. This is driven by VR, machine learning, and high-bandwidth networks. Get your Oculus Rift from Facebook (FB) now!

(9) Increased Focus on Sustainability and the Environment will drive companies to invest in sustainability—both from a necessity standpoint and for marketing purposes. Breakthroughs in materials science, enabled by AI, will allow companies to drive tremendous reductions in waste and environmental contamination. One company’s waste will become another company’s profit center. Want to visit my chalet in Switzerland? You can do so by connecting your Oculus Rift headset to Google Maps….today! This is driven by materials science, AI, CRISPR, digital biology, and broadband networks.

(10) CRISPR and Gene Therapies Will Eliminate Disease. Perhaps one of the most powerful, underappreciated technologies in the world is CRISPR. In 2020, two incredible women won the Nobel Prize in medicine for its discovery, and revenues from CRISPR doubled between 2019 and 2020 to over $1.5B. A vast range of infectious diseases, from AIDS to Ebola, are now potentially curable, as are a wide range of genetic ailments like sickle cell anemia, thalassemia, and certain forms of congenital blindness. In addition, gene-editing technologies continue to advance in precision and ease of use, allowing families to treat and ultimately cure hundreds of inheritable genetic diseases. This is driven by various biotechnologies (CRISPR, Gene Therapy), genome sequencing, and AI. Only three companies have a monopoly in this sector right now, (CRSP), (EDIT), and (NTLA).

In the decade ahead, master entrepreneurs will look beyond the immediate effects of a given technology to seize secondary and tertiary, Google-sized business opportunities on the horizon.

As an investor, you should be asking yourself: What challenges or problems can I help solve? How can I leverage the coming waves of tech advancements?

I just thought you’d like to know.

John Thomas

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-at-micron.png708580Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-22 09:02:052023-02-22 10:43:06Ten More Trends to Bet the Ranch On

Last summer, I stayed at an Airbnb in Long Beach, CA in order to pick up my kids from the Boy Scout Camp on Catalina Island. It was billed as a vintage 1920s residence with all the period finishes, was two blocks from the beach, and was a short drive to the Cataline ferry, so it seemed like the ideal place.

But the second I walked into the place I was overcome by a ghostly Twilight Zone type feeling. Everything seemed strangely familiar. What really freaked me out was that the grill on the electric wall heater exactly matched the scar on my sister’s hand. Even though the place was 100 years old, I had been here before.

When I returned home, I headed straight for a voluminous genealogy file that I maintained. After an hour of going through all the family records, I hit paydirt. The address of the Airbnb was listed as the home address of my grandmother when she was married in 1925.

When the pandemic hit in February 2020, I figured Airbnb (ABNB) was toast. Global travel had ground to a halt, and competitors like Wynn Resorts (WYNN) and Hyatt Hotels (H) saw their share prices plunge to near zero.

Instead, the opposite happened.

While the big hotels continue to roast in purgatory, Airbnb catapulted to a new golden age, and how they did it was amazing.

They turned all travel local. Instead of recommending that I visit Cairo, Tokyo, or Rio de Janeiro, they suggested Carmel, Monterey, or Mendocino, all destinations within driving distance.

It worked spectacularly well, and the company is now moving from strength to strength. Since the pandemic bottom, the shares have rocketed from $69 to $210.

My neighborhood in Incline Village, NV was almost always deserted outside of holidays. Now it is packed with Airbnber’s awkwardly moving in every Friday only to flee on Sunday.

How would you like to get an 80% discount on all of your luxury hotel accommodations?

During my recent trip to Dubrovnik in Croatia, I rented an 800-square-foot, two-bedroom, two-bath home inside the city walls for $300 a night.

A single, cramped 150-square-foot room in the nearest five-star hotel was $600 night.

All that was missing was room service, a handout for a big tip, and a surly attitude at the front desk.

Sounds like a massive, game-changing disruption to me.

Thank you, Airbnb!

The big question for you and me is: Will the valuation soar tenfold from the current $106 billion to $1 trillion?

Is (ABNB) your next ten bagger?

To answer that question, I spent six weeks traveling around the world as an Airbnb customer. This enabled me to understand their business model, their strengths and weaknesses, and analyze their long-term potential.

As a customer, the value you receive is nothing less than amazing.

I have been a five-star hotel guest for most of my life, with someone else picking up the tab much of the time (thank you Morgan Stanley!), so I have a pretty good idea on the true value of accommodations.

What you get from Airbnb is nothing less than spectacular. You get three or four times the floor space for one-third the price. That’s a disruption factor of 7:1.

The standards are often five-star and at the top end, depending on how much you spend. I found I could often get an entire three-bedroom house for the price of a single hotel room, with a better location.

Or, I could get an excellent abode in rural settings, where none other was to be had, whatsoever.

That’s a big deal for someone like me who spends so much of the year on the road.

You also get a new best friend in every city you visit.

On most occasions, the host greeted me on the doorsteps with the keys, and then introduced me to the mysteries of European kitchen appliances, heating, and air conditioning.

Pre-stocking the refrigerator with fresh milk, coffee, tea, and jam seems to be a tradition the hosts pick up in their Airbnb orientation course.

One in Waterford, Ireland even left me a bottle of wine, plenty of beer, and a frozen pizza. She read my mind. She then took me on a one-hour tour of their city, divulging secrets about their favorite restaurants, city sights, and nightspots. Everyone proved golden. Thanks, Mary!

After you check out, Airbnb asks you to review the accommodation. These can be incredibly valuable in deciding your next pick.

I had one near miss with what I thought was a great deal in London, until I read, “The entire place reeks of Indian cooking.” Having caught amoebic dysentery in India once Indian cooking does not exactly bring back fond memories.

Similarly, the hosts rate you as a guest.

One hostess in Dingle, Ireland shared a story about picking up her clients from town after they got drunk and lost in the middle of the night. Then they threw up in the back of the car on the way home.

Guests forgetting to return keys is another common complaint.

Needless to say, I received top ratings from my hosts, as fixing their WIFI to boost performance became a regular and very popular habit of mine.

After my initial fabulous experience in London, I thought it might be a one-off, limited to only the largest cities. So, I started researching accommodations for my upcoming trips.

I couldn’t have been more wrong.

Just the Kona Coast on the big island of Hawaii had an incredible 300 offerings, including several bargain beachfront properties.

The center of Tokyo had over 300 listings. The historic district in Florence, Italy had a mind-blowing 351 properties. When I stayed there, six of seven floors of the building I stayed in were devoted to (ABNB) accommodations. The one full time resident was pissed and often slammed his door.

Fancy a retreat on the island of Bali in Indonesia and tune up your surfing? There are over 197 places to stay!

Airbnb has truly gone global.

Airbnb’s business model is almost too simple to be true, involving no more than a couple of popular applications. Call it an artful melding of Google Earth (GOOG), email, text, and PayPal (PYPL).

While no one was looking, it became the world’s largest hotel at a tiny fraction of the capital cost.

The company has 6 million hosts in 100,000 cities worldwide in 220 countries who so far have earned $150 billion, and 150 million users. The all-time number of guests is 1 billion. The company recently shut down all of its Russia listings.

That supply/demand imbalance shifts the burden of the cost to the renters, who usually have to fork out a 12% fee, plus the cost of the cleaning service.

Hosts only pay 3% to process the credit card fees for the payment.

To say that Airbnb has created controversy would be a huge understatement.

For a start, it has emerged as a major challenge to the hotel industry, which is still stuck with a 20th century business model. There’s no way hotels can compete on price.

One Airbnb “super host” in Manhattan managed 200 apartments, essentially, creating out of scratch, a medium-sized virtual “hotel” until the city caught on to them.

Taxes are another matter.

Some municipalities require hosts to pay levies of up to 20%, while others demand quarterly tax filings and withholding taxes. That is, if tax collectors can find them.

Airbnb may be the largest new source of tax evasion today.

In cities where housing is in short supply, Airbnb is seen as crowding out local residents. After all, an owner can make far more money subletting their residence nightly than with a long-term lease.

Several owners told me that Airbnb covered their entire mortgage and housing cost for the year while paying off the mortgage at the same time.

Owners in the primmest of areas, like mid-town Manhattan off of Central Park, or the old city center in Dubrovnik rent, their homes out as much as 180 days a year.

It is doing nothing less than changing lives.

That has forced local governments to clamp down.

San Francisco has severe, iron-clad planning and zoning restrictions that only allow 2,000 new residences a year to come on the market.

It is cracking down on Airbnb, as well as other home-sharing apps like FlipKey, VRBO, and HomeAway, by forcing hosts to register with the city or face brutal $1,000 a day fine.

Ratting out your neighbor as an off-the-grid Airbnb member has become a new cottage industry in the City of the Bay.

Airbnb is fighting back with multiple lawsuits, citing the federal Communications Decency Act, the Stored Communications Act, and the First Amendment covering the freedom of speech.

It is a safe bet that a $91 billion company can spend more on legal fees than a city the size of San Francisco.

The company has also become the largest contributor in San Francisco’s local elections. In 2015, it fought a successful campaign against Proposition “F”, meant to place severe restrictions on their services.

An Airbnb stayover is not without its problems.

The burden of truth in advertising is on the host, not the company, and inaccurate listings are withdrawn only after complaints.

A twenty-something-year-old guy’s idea of cleanliness may be a little lower than your own.

Long-time users learn the unspoken “code”.

“Cozy” can mean tiny, “as is” can be a dump, and “lively” can bring the drunken screaming of four-letter words all night long, especially if you are staying upstairs from a pub.

And that spectacular seaside view might come with relentlessly whining Vespa’s on the highway out front as I was once confronted with in coastal Italy. Always brings earplugs and blindfolds as backups.

Researching complaints, it seems that the worst of the abuses occur in shared accommodations. Learning new foreign cultures can be fascinating. But your new roommate may want to get to know you better than you want, especially if you are female.

In one notorious incident, a Madrid guest was raped and had to call customer service in San Francisco to get the local police to rescue her. The best way to guard against such unpleasantries is to rent the entire residence for your use only, as I do.

Another problem arises when properties are rented out for illegal purposes, such as prostitution or drug dealing. Near my San Francisco home five people were shot and killed in an illegal block party nearby in a Airbnb weekend rental that was supposed let out to a “quiet couple.”

More than once, an unsuspecting resident woke up one morning to discover they were living next door to a new bordello.

Coming out of the pandemic, my conclusion is that the travel industry is entering a hyper-growth phase. Blame the emerging middle-class Chinese, who are going to be everywhere.

The real shock came when I left Airbnb and stayed in a regular hotel. Include the fees and the cleaning charges, and the service is no longer competitive for a single-night stay. Total costs now regularly run double the posted one-night price posted on websites.

In any case, most hosts have two or three-night minimums to minimize hassle.

When I checked in at a Basel, Switzerland Five Star hotel, all I got was a set of keys and a blank stare. No great restaurant tips, no local secrets, no new best friend.

I spent that night surfing www.airbnb.com, planning my next adventure.

Grandparents at Future Airbnb in 1925

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-Airbnb.png466456MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2023-02-16 09:02:202023-02-16 15:55:35Is Airbnb Your Next Ten Bagger?

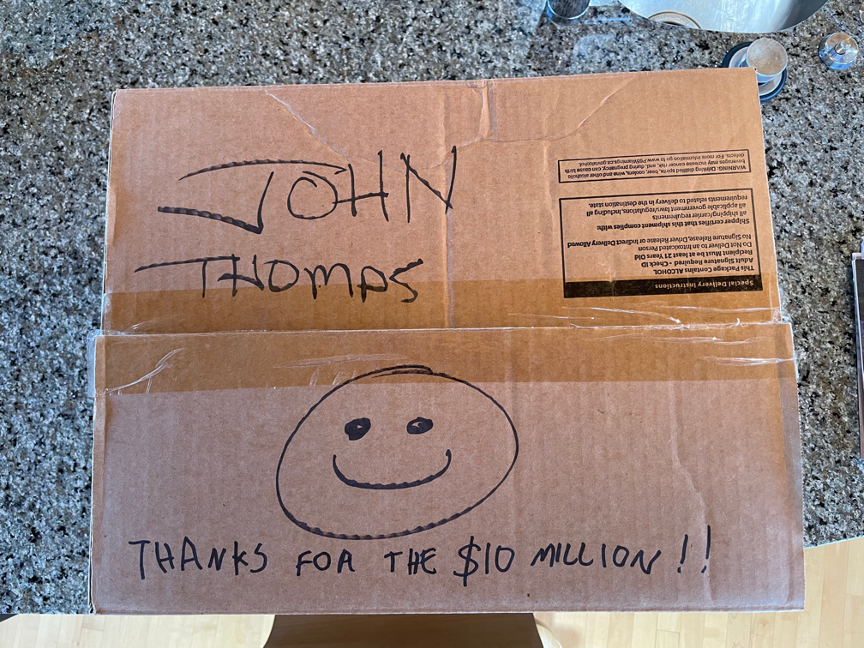

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks to Peter Martin and Marjorie Deane!), has just released its "Big Mac" index of relative international currency valuations.

Although initially launched as a joke five decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald's (MCD) premium two beef patty sandwiches around the world, ranging from $8.35 in Venezuela to $1.68 in Lebanon, and comes up with a measure of currency under and overvaluation.

What are its conclusions today?

The Venezuelan Bolivar is wildly expensive, with 235 years of annual per capita income needed to buy a single Big Mac in local currency terms if you can find one. There are currently 4 million Bolivars to the US Dollar in this sadly bankrupt country.

The Norwegian Kroner, Swiss franc (FXF), and the US Dollar (UUP) are also dear, with the average cost of an American Big Mac at $5.35. Every year I make a ritual visit to what is often the most expensive McDonald’s in the world at Zermatt Switzerland (see pictures below). There the Big Macs taste slightly acidic.

The cheapest currencies are the South African Rand, the Russian Ruble, and the Lebanese Pound, a Big Mac coming in at $1.68 in Beirut.

I couldn't agree more with many of these conclusions. It's as if the august weekly publication was tapping The Diary of a Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool than a speedy lunch.

The Big Mac is a Steal Here in Turkey

No Bargain Here in Italy Either

And Costs a King’s Ransome Here in Zermatt

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/zermatt-mcdonalds.png488652Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-14 09:02:022023-02-14 17:23:40Where the Economist “Big Mac” Index Finds Currency Value Today

The Diary of a Mad Hedge Fund Trader is read in 140 counties. About a quarter of our readers run the letter through a Google Translator before reading.

That has created a problem.

Stock trading is probably the most slang and acronym-ridden profession on the planet, second only to the United States Marine Corps. (Semper Fi).

And guess what? The Google Translator has never worked on the floor of a major stock exchange.

That means its translations often come out as gobbledygook or complete nonsense. So, the customers email me asking what the heck I am talking about in my daily newsletters, eating up a portion of my day.

I am therefore enclosing “The Mad Hedge Fund Trader’s Dictionary of Traders’ Slang” below.

To keep this a PG-rated publication, I have left some terms undefined, but you can make a good guess as to their true meaning. It turns out that most traders never got to finishing school, and many are not even gentlemen.

If any of you out there have additional terms you would like to add, please email them to me at support@madhedgefundtrader.com and put “DICTIONARY” in the subject line. I’ll use them in a future update. No doubt there are hundreds, if not thousands more.

Read, enjoy, and laugh.

Accelerated Time Decay – The increasing decline of the value of a stock option as it approaches its expiration date

Black Swan – A term made popular by Nassim Taleb that refers to a sudden, unexpected, low-probability event that has a disproportionately high impact on your portfolio.

Boredom Trading – reaching for marginally profitable trades during quiet markets because there is nothing else to do. Usually a bad idea.

Bottoming Process – When a market makes several failed attempts to make new lows, creating a medium term bottom

Blow off Top – The top of a price spike upward usually associated with a volume spike as well

Bubble – Any assets class rising in price far above and beyond any rational valuation measures

Buy the Dip – BTD/BTFD/BTMFD - Buy the recent decline in prices.

Don’t Catch a Falling Knife – don’t try and buy a stock in free fall

Don’t be a Hero – keep positions small during volatile markets

“Be greedy when others are fearful, and fearful when others are greedy” is a classic Benjamin Graham quote which means “buy bottoms and sell top.”

Pigs Get Slaughtered – Buy a position that is too big for you and it will turn around and bite you

Bull Trap – a strong market move up that sucks in buyers and then dies as soon as the last one is in

Bear Trap – A strong market move down that sucks in lots of short sellers and turns around as soon and the last one sells

Buy When There is Blood in the Streets – Buy stocks at market bottoms

Capitulation Bottom – The last bull throws in the towel, gives up, and dumps all his stock, making the final bottom of a major move

Capitulation Top – The last bear throws in the towel, gives up, and jumps into the market late, making the final top of a major move

Choppy – sudden and erratic price moves within a narrow range

Contrarian – one who trades against the general market consensus

Dead Cat Bounce – A brief rally in s stock that has just seen a sharp drop

Dialing for Dollars – Calling brokerage house customers to sell stocks for commissions

Don’t Fight the Fed – Don’t expect markets to fall when interest rates are falling

Don’t Fight the Tape – Don’t trade against the market trend. Comes for the paper ticker tapes that once transmitted stock prices by telegraph

Dry Powder – Keeping cash in reserve for better trading opportunities

Dumb Money – what inexperienced retail investors are doing. Thanks to the internet, they’re not as dumb as they used to be

Get Filled – Your order is executed

Growing Hair on It – Keeping a position for too long

The Greeks – Greek alphabet letters that refer to option valuation components, such as delta, theta, gamma, and vega

High-Frequency Traders (HFT) – Firms using sophisticated computer programs to take positions for infinitesimally short periods of time taking microscopic profits in enormous volumes. They account for roughly 70% of daily trading volume

Holding the Bag – you are left holding stock in a falling market or short in a rising one

Honor Your Stops - don’t make excuses for ignoring stop losses. This is where the really big hits come from

Killing It – Making a series of successful trades

Locked Market – When the bid and offer are identical

Market Makers – firms that provide market liquidity with two-sided bids and offers, now largely replaced by computers

Melt Up – A straight line move upward in shares with no pullbacks whatsoever, usually triggered by a news or earnings release

Never Short a Dull Market – Quiet markets can often rally sharply because the selling is done

Noise – Random media reporting that has no true impact on the direction of stock prices

Pain Trade – the market is moving against the positions of the trading community

Permabear – A persona who is always bearish, usually driven by some bizarre Armageddon-type ideology, or suffering from paranoia

Permabull – a person who is always bullish, despite deteriorating fundamental conditions

Picking Up Pennies in Front of a Steamroller – Sell short naked put options

Pump and Dump – Unethical brokers run of the prices of small illiquid stocks and then sell them to clients at market tops. The shares usually collapse afterwards. See the movie Wolf of Wall Street

Resistance Level – A price on a stock chart offering technical resistance to further price appreciation

Sell in May and Go Away – The preference for selling shares ahead of a period of seasonal weakness

Sell the Rip – STR/STFR/ STMFR

Short Squeeze – A sharp run-up in share prices that forces short sellers to buy to avoid accelerating losses.

Smart Money – what the best informed, most experienced investors are doing. Not as smart as they used to be.

Snakebit – A surprise news development that comes out of the blue and costs you money

Spoofing – entering orders without any intention of executing them and cancelling them before they can be executed. It is a common tactic of high-frequency traders

Spoos – S&P 500 futures contracts

Squak Box – A small loudspeaker on a desktop in a trading room constantly broadcasting news reports and large trades

Support Level – A price on a stock chart offering significant technical support

Stop Loss - a price at which, when reached, a liquidation of the position is automatically triggered

The Trend is Your Friend – Trade with the market direction, not against it

Theta Burn – Time decay on options

Ticker Tape – A white ¾ inch wide paper tape used to transmit stock prices by telegraph at the rate of 500 characters a minute that was used until the 1950s to transmit stock prices. See ticker tape parade and delayed tape.

Topping Process – occurs when a market makes several failed attempts to make a new high, creating a medium term top

Turnaround Tuesday – the tendency of markets to reverse direction after the markets digest weekend news on a Monday

Yellen Put – an assumption that the Fed will come to the rescue with a monetary easing on any substantial market selloff

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/John-Thomas-1.png336428MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2023-02-07 09:02:382023-02-07 16:09:11The Mad Hedge Dictionary of Trading Slang

Mr. John Thomas, you have changed my life. Before I found your service, I bounced from one terrible service to another, losing money at every step of the way. Even when I found you, I was pretty leery. I then pulled off 22 money-making trades in a row. I gained so much confidence that I really poured money into your strategies. Since I met you last year, I have made over $10 million. I bought call options on Tesla when it was at $80. I also filled all 45 trade alerts you send out selling short the (TLT). It really has been an amazing run.

Please accept the attached case of cabernet. It is a mixed case from boutique vineyards that aren’t sold to the public. These are all “know somebody” wines. If you could buy them, they would cost from $220-$500 a bottle.

If there are any charities you would like me to send a check to, just let me know. You’re really great!

Joseph

Napa, California

https://www.madhedgefundtrader.com/wp-content/uploads/2021/06/smiley-box.png648864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-24 09:04:142023-01-24 14:27:46Testimonial

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.