The shares of FANGs are all about to double in value in the Silicon Valley if commercial real estate is any indication of the future growth rates.

The group is gobbling up office space at such a prodigious rate that only a vast expansion of their business would justify these massive long-term commitments.

Commercial real estate commitments are one of the most valuable leading indicators of stock performance out there. They show what the companies themselves think are their future prospects.

Apparently, the stock market agrees with me. Technology is virtually the only group of shares moving to new all-time highs in these otherwise dismal trading conditions.

Just this month Facebook (FB) signed a lease for the entire brand new 43-story Park Tower in downtown San Francisco, and that's just to house its Instagram business.

Google (GOOGL) is leasing 39% of the office space in Mountain View, CA. It is currently in negotiations with the nearby city of San Jose to build a skyscraper occupying an entire city block that will house 10,000 tech workers. It also is building another 1 million square feet near an old prewar dirigible landing strip in Moffett Park.

Apple (AAPL) is hogging some 69% of the office space in Cupertino, CA. It is just now moving into its new massive spaceship-inspired headquarters, where 10,000 workers will slave away. The world's largest company is currently on the hunt for a second headquarters location.

Netflix is slowly gobbling up Los Gatos, CA. It was recently joined by the set top device company Roku (ROKU), which is growing by leaps and bounds.

Fruit canning was the original industry of Silicon Valley at the turn of the 20th century, taking advantage of the surrounding peach, plum, and apricot groves. When I was a kid after WWII, defense firms such as Lockheed (LMT) took over, creating thousands of high-paying engineering jobs.

It didn't hurt that Stanford University was spitting distance away, and the University of California was just on the other side of the bay. These two schools supplied the manpower to fuel the hypergrowth ahead.

To say the growth has caused local headaches would be an understatement in the extreme. The San Francisco Bay Area now sports the world's most expensive residential housing. The median San Francisco home price has skyrocketed to $1,334,000 and requires an annual income of $334,000 to support it.

Small businesses such as dry cleaners, nail salons, restaurants, and barber shops have been driven out by soaring rents. It's not uncommon now to go out to dinner only to find a "closed" sign on your favorite nightspot. Your personal assistant now has to travel miles just to get your suits pressed.

As for traffic, forget about it. Rush hour has ceased to exist. Freeways are now jammed a nonstop 12 hours a day in the worst neighborhoods.

Success has its price, and this was never truer than in Silicon Valley.

The New Apple HQ

Where Instagram Now Lives

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/APPLE-HQ-story-2-image-6-e1527804149789.jpg326580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-06-01 01:07:092018-06-01 01:07:09Why Your FANG Stocks are About to Double in Value

AT&T (T), Verizon (VZ), and the other telecom heavies are in the process of investing $30 billion to make sure that fifth-generation wireless, or 5G, will roll out on time in 2020.

What 5G will do is improve the functionality of IoT (Internet of Things) by 10 times at one-tenth the cost, bringing a 100X increase of functionality over price.

The last time I saw a leap that great was when Intel (INTC) brought out its groundbreaking 8008 8-bit microprocessor chip in 1972. I remember it like it was yesterday.

The news that gravitational waves were discovered, as well as wrinkles in the space-time continuum, was big news in my family. 5G will be of that order.

Of course, we knew it was coming. It was just a matter of when.

I have 11- and 13-year-old girls (I can't help it if the plumbing still works!). Whenever we drive somewhere, we carry out what Einstein called "thought experiments."

They will come up with scientific questions, and I then direct them into finding their own answers through a series of prodding and hopeful questions.

It is much like how the children of royalty were tutored during the Middle Ages.

So they asked, "When will we get driverless cars?" which they had heard about on TV.

I answered in about two years, but that I had friends who run Tesla (TSLA) who already have them now.

And you know the interesting thing they discovered? After two years of beta testing, the cars are starting to develop their own personalities.

Each car has highly advanced learning software. When the mapping software requires one to take a difficult sharp left turn, the vehicle may miss it the first time.

It will then make the next legal U-turn, and then nail that turn every time in the future.

The cars are all programmed to drive like little old ladies. It will never speed, break the law, and always lets other cars cut in front. Over time, some are becoming cautious, while others are getting more aggressive depending on each individual's driving experience.

In other words, experience is turning them into "people."

I asked my daughters, "What would the world be like if everyone had driverless cars?" which will occur in about 30 years, or during their middle age.

They pondered for a moment. Then my older daughter shouted out, "There won't be car accidents anymore!" "Right!" I answered.

"But what will that mean?" I asked.

They puzzled over this.

A few seconds passed. Then it came. "The people who fix cars won't have anything to do!"

"You got it," I replied.

In fact, about 1 million people in the car repair industry will lose their jobs. A small group of vintage car fanatics will survive, much like horse and buggy hobbyists do today.

I pointed out that this is already happening because electric cars don't require any maintenance. You just rotate the tires every 6,000 miles (because electric batteries are so heavy).

I moved on. "Who else will lose their jobs when cars become self-driving?" They hit a brick wall. Then I asked "What else breaks when cars have accidents?"

A few seconds later it came. "People!"

"For sure," I shot back.

Actually, about 35,000 people die in car accidents every year in the United States, and another 500,000 are injured.

This means the demand for doctors, hospitals, and ambulances will go down. Say goodbye to another 1 million jobs.

"So, what else will self-driving cars do?" I was relentless.

My older girl was first: "If cars are driven by computers, it means they can drive closer together." I said, "That was true, but what was the consequence of that?"

The mountain scenery whizzed by. Then they got it.

"There won't be traffic jams anymore."

"Yes!" I blurted out. If a car can drive 70 miles per hour, but only needs to remain one car length behind the one in front of it, that effectively increases the capacity of freeways seven times.

We will never need to build another freeway again. Another 1 million jobs go down the drain.

"What else will self-driving cars do?" I carried on.

They hit a dead end. So, I gave a hint. "What do you see in cities?" After going through buildings, parks, roads, lots of cars, and bridges, I finally got the answer I wanted: "Parking lots."

I then posed the conundrum, "What's the connection between self-driving cars and parking lots?"

Now they were getting into the spirit of the thing. "They won't need them." I replied, "Absolutely."

Self-driving cars won't need to park. They'll just be able to drop you off and drive around the block until you are ready to go home.

This will be economical because after three decades of battery and solar improvements, energy will effectively be free, like air is today.

Oh, and at least 100,000 parking attendants might as well start joining the unemployment lines now.

It gets better.

Entrepreneurs now are developing apps for cars so they never need to park.

In an iteration of the sharing economy, and in a club or membership type format, your car will just drive person to person, selling rides, until you are ready to go home.

Think of it as Uber, without the drivers, that pays you.

Today, parking lots occupy about 15% of the land area of large cities. Self-driving cars will free up a lot of that space for other uses, such as housing and parks.

Then I asked the really big question. "What do all of these changes have in common?"

My 11-year-old picked up on this immediately. "A lot of people are going to lose their jobs!"

"For sure," I bubbled. Notice that every new technology improvement creates a lot of job losses. I went on.

"The trick for you girls is to always stay ahead of the technology curve so your job doesn't get lost, too." This is why I have been sending them to Java development school since they were 8 and 9.

They looked daunted.

And this is what 11- and 13-year-olds were able to figure out. Granted, they were MY kids.

Imagine what Google (GOOGL), Apple (AAPL), and Tesla are doing with this idea. It has become a hot bottom "next big thing." Silicon Valley is now rife with rumors of breakthrough developments and the poaching of staff.

The U.S. military and the Defense Advanced Research Projects Agency (DARPA) are involved in self-driving vehicles in a big way as well, holding regular contests with big prize money and the prospect of mammoth government contracts.

More and more generals and admirals are telling me that the wars of the future will be fought with software.

The bottom line is that things are happening much faster than we imagined possible only a few years ago.

Then my oldest daughter piped up.

"Dad, can I get my driver's license before all the cars are self-driving?" I said, "Sure. What kind of car do you want?"

"A red one."

My first car was a red 1957 Volkswagen Beetle.

On our next trip we will cover gravitational waves, Einstein's Theory of Relativity, and the significance of the clock tower in Bern, Switzerland.

By the way, these girls will be graduating from college in 2026 and 2027 and will be looking for jobs.

"Homo sapiens, the first truly free species, is about to decommission the natural selection, the force that made us," said E.O. Wilson, a Harvard University biology professor.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/John-and-car-image.jpg312553MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-25 01:05:362018-05-25 01:05:36Where 5G Connectivity Will Take Us

The Amazon (AMZN) and Netflix (NFLX) model is not the only technology business model out there.

Micron (MU) has amply proved that.

Bulls were dancing in the streets when Micron announced a blockbuster share buyback of $10 billion starting in September.

This is all from a company that lost $276 million in 2016.

The buyback is an overwhelmingly bullish premonition for the chip sector that should be the lynchpin to any serious portfolio.

The news keeps getting better.

Micron struck a deal with Intel to produce chips used in flash drives and cameras. Every additional contract is a feather in its cap.

The share repurchase adds up to about 16% of its market value and meshes nicely with its choreographed road map to return 50% of free cash flow to shareholders.

Tech's weighting in the S&P has increased 3X in the past 10 years.

To put tech's strength into perspective, I will roll off a few numbers for you.

The whole American technology sector is worth $7.3 trillion, and emerging markets and European stocks are worth $5 trillion each.

Tech is not going away anytime soon and will command a higher percentage of the S&P moving forward and a higher multiple.

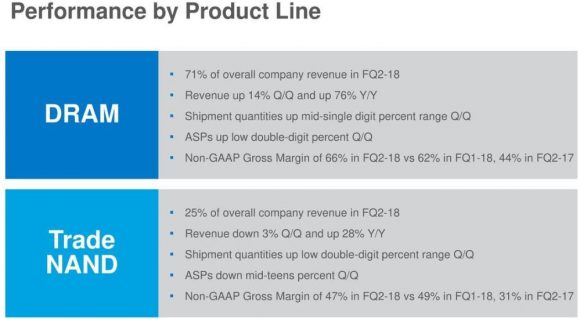

The $5 billion in profit Micron earned in 2017 was just the start and sequential earnings beats are part of their secret sauce and a big reason why this name has been one of the cornerstones of the Mad Hedge Technology Letter portfolio since its inception as well as the first recommendation at $41 on February 1.

Did I mention the stock is dirt cheap at a forward PE multiple of just 6 and that is after a 35% rise in the share price so far this year?

What's more, putting ZTE back into business is a de-facto green light for chip companies to continue sales to Chinese tech companies.

China consumed 38% of semiconductor chips in 2017 and is building 19 new semiconductor fabrication plants (FAB) in an attempt to become self-sufficient.

This is part of its 2025 plan to jack up chip production from less than 20% of global share in 2015 to 70% in 2025.

This is unlikely to happen.

If it was up to them, China would dump cheap chips to every corner of the globe, but the problem is the lack of innovation.

This is hugely bullish for Micron, which extracts half of its revenue from China. It is on cruise control as long as China's nascent chip industry trails miles behind them.

At Micron's investor day, CFO David Zinsner elaborated that the mammoth buyback was because the stock price is "attractive" now and further appreciation is imminent.

Apparently, management was in two camps on the capital allocation program.

The two choices were offering shareholders a dividend or buying back shares.

Management chose share repurchases but continued to say dividends will be "phased in."

This is a company that is not short on cash.

The free cash flow generation capabilities will result in a meaningful dividend sooner than later for Micron, which is executing at optimal levels while its end markets are extrapolating by the day.

As it stands today, Micron is in the midst of taking its 2017 total revenue of about $20 billion and turning it into a $30 billion business by the end of 2018.

The overall chips market is as healthy as ever and data from IDC shows total revenues should grow 7.7% in 2018 after a torrid 2017, which saw a 24% bump in revenues.

The road map for 2019 is murkier with signs of a slowdown because of the nature of semi-conductor production cycles. However, these marginal prognostications have proved to be red herrings time and time again.

Each red herring has offered a glorious buying opportunity and there will be more to come.

Consolidation has been rampant in the chip industry and shows no signs of abating.

Almost two-thirds of total chip revenue comes from the largest 10 chip companies.

This trend has been inching up from 2015 when the top 10 comprised 53% in 2016 and 56% in 2017.

If your gut can't tell you what to buy, go with the bigger chip company with a diversified revenue stream.

The smaller players simply do not have the cash to splurge on cutting-edge R&D to keep up with the jump in innovation.

The leading innovator in the tech space is Nvidia, which has traded back up to the $250 resistance level and has fierce support at $200.

Nvidia is head and shoulders the most innovative chip company in the world.

The innovation is occurring amid a big push into autonomous vehicle technology.

Some of the new generation products from Nvidia have been worked on diligently for the past 10 years, and billions and billions of dollars have been thrown at it.

Chips used for this technology are forecasted to grow 9.6% per year from 2017-2022.

Another death knell for the legacy computer industry sees chips for computers declining 4% during 2017-2022, which is why investors need to avoid legacy companies like the plague, such as IBM and Oracle because the secular declines will result in nasty headlines down the road.

Half way into 2018, and there is still a dire shortage of DRAM chips.

Micron's DRAM segments make up 71% of its total revenue, and the 76% YOY increase in sales underscores the relentless fascination for DRAM chips.

Another superstar, Advanced Micro Devices (AMD), has been drinking the innovation Kool-Aid with Nvidia (NVDA).

Reviews of its next-generation Epyc and Ryzen technology have been positive; the Epyc processors have been found to outperform Intel's chips.

The enhanced products on offer at AMD are some of the reasons revenue is growing 40% per year.

AMD and Nvidia have happily cornered the GPU market and are led by two game-changing CEOs.

It is smart for investors to focus on the highest quality chip names with the best innovation because this setup is most conducive to winning the most lucrative chip contracts.

Smaller players are more reliant on just a few contracts. Therefore, the threat of losing half of revenue on one announcement exposes smaller chip companies to brutal sell-offs.

The smaller chip companies that supply chips to Apple (AAPL) accept this as a time-honored tradition.

Avoid these companies whose share prices suffer most from poor analyst downgrades of the end product.

Cirrus Logic (CRUS), Skyworks Solutions (SWKS), and Qorvo Inc. (QRVO) are small cap chip companies entirely reliant on Apple come hell or high water.

Let the next guy buy them.

Stick with the tried and tested likes of Nvidia, AMD, and Micron because John Thomas told you so.

"Bitcoin will do to banks what email did to the postal industry." - said Swedish IT entrepreneur and founder of the Swedish Pirate Party Rick Falkvinge.

Beyond cutting-edge technology, there's nothing that China WANTS OR NEEDS to buy from the U.S. China's largest imports are in energy and foodstuffs, both globally traded commodities.

China is playing the long game because it can.

Earlier this year, China altered its constitution to remove term limits and any obstacle that would hinder Chairman Xi to serve indefinitely.

If it's two, four, eight or 10 years, no problem, China will wait it out.

As it stands, China is enjoying the status quo, which is a robust economic trajectory of 6.7% economic growth YOY and at that rate will leapfrog America as the biggest economy in the world by 2030.

China does not need handouts.

It already has its mooncake and is eating it.

The Chinese are also betting that Donald Trump fades away with the passage of time, possibly soon, and that a vastly different administration will enter the fray with an entirely different strategy.

The indefinite "hold" pattern is a polite way to say we surrender.

ZTE Corporation is a Chinese telecommunications equipment manufacturer and low-end smartphone maker based in Shenzhen, China.

This seemingly innocuous company is ground zero for the U.S. vs China trade practice dispute.

The U.S. Department of Commerce banned American tech companies from selling components to ZTE for seven years, crippling its supply chain after violating sanctions against Iran and North Korea.

ZTE uses about 30% of American components to produce its smorgasbord of telecom equipment and down-market cell phones.

What most people do not know is that ZTE is the fourth most prevalent smartphone in America, only behind Apple, Samsung, and LG, commanding a 12.2% market share, and its phones require an array of American made silicon parts.

In 2017, the company shipped more than 20 million phones to the United States.

The ruling effectively put ZTE out of business because the lack of components shelved production.

Low-end smartphones account for almost one-third of total revenue.

ZTE could very well have survived with a direct hit to its consumer phone business, but the decision to ban components made the telecom equipment division inoperable.

This segment accounts for a heavy 58.2% of revenue. Therefore, disrupting ZTE's supply chain would effectively take down more than 91% of its business for a company that employs 75,000 employees in over 160 countries.

Upon news of ZTE's imminent demise, the administration made a U-turn on its initial decision stating "too many jobs in China lost."

The reversal made America look bad.

It shows that America is being dictated to and not the other way around.

When did it become the responsibility of the American administration to fill Chinese jobs for a company that is a threat to national security?

The Chinese refused to continue talks with the visiting delegation until the ZTE situation was addressed.

Treasury Secretary Steve Mnuchin and company were able to "continue" the talks then were politely shown the door.

Bending the rules for ZTE should have never been a prerequisite for talks, stressing the lack of firepower in the administration's holster.

However, stranding the delegation in Chinese hotel rooms for days waiting in limbo, without offering an audience, would have caused even more humiliation and anguish for the administration.

China is not interested in buying much from America, but one thing it needs -- and needs in droves -- are chips.

Long term, this ZTE ban is great for China.

I believe China will use this episode to rile up the nationalistic rhetoric and make it a point to wean itself from American chips.

However, for the time being, American chips are the most valuable import America can offer China, and that won't change for the foreseeable future.

The numbers back me up.

Micron (MU) earns more than $10 billion in revenue from China, which makes up over 51% of its total revenue.

Qualcomm (QCOM), mainly through its lucrative licensing division, makes more than $14.5 billion from its Chinese revenue, which comprises over 65% of revenue.

Texas Instruments (TXN) earns more than 44% of revenue from China, and almost a quarter of Intel's (INTC) revenue is derived from its China operations.

The biggest name embedded in China is Apple (AAPL), which earned almost $45 billion in sales last year. Its China revenue is three times larger than any other American company.

In less than a decade, China has caught up.

China now has adequate local smartphone substitutes through Huawei, Oppo, Vivo, and Xiaomi phones.

Skyworks Solutions (SWKS), a chip company reliant on iPhone contracts, is most levered toward the Chinese market capturing almost 83% of revenue from China.

You would think these chips would be the first on the chopping block in a trade war. However, you are wrong.

China needs all the chips it can get because there is no alternative.

Stopping the inflow of chips is another way of stopping China from doing business and developing technology.

The Chinese economy has been led by the powerful BATs of Baidu (BIDU), Tencent, and Alibaba (BABA) occupying the same prominent role the American FANGs hold in the American economy.

They are not interested in digging their own grave.

To execute the 2025 plan to become the world leaders in advanced technology, they need chips that power all modern electronic devices.

The most likely scenario is that China maintains development using American chips for the time being and slowly pivots to the Korean chip sector, which is vulnerable to Chinese political pressure.

Remember that South Koreans have two of the three biggest chip companies in the world in Samsung and SK Hynix. China has used economic coercion to get what it wants from Korea in the past or to prove a point.

Korean multinational companies, shortly after the Terminal High Altitude Area Defense (THAAD) installation on the Korean peninsula, were penalized by the Chinese government shutting down mainland Korean stores, temporarily banning Chinese tourism in South Korea, and blocking K-pop stars from performing in the lucrative Chinese market.

The Chinese communist government can turn the screws when it wants and how it wants.

Therefore, the next battleground for tech could migrate to South Korean chip companies as China is on a mission to suck up as much high-grade tech ingenuity as possible while it can.

China has some easy targets to whack down if the administration forces it into a corner with a knife to its throat.

Non-tech companies are ripe for massacre because they do not produce chips.

Companies such as Procter & Gamble, Starbucks, McDonald's, and Nike could be replaced by a Chinese imitation in a jiffy.

Apple is the 800-pound gorilla in the room.

An attack on Apple would hyper-accelerate tension between two leaders to the highest it's ever been and would be the straw that breaks the camel's back.

Technology has transformed the world.

Technology also has been adopted by nations as a critical component to national security.

Nothing has changed fundamentally, and nothing will.

China will become the biggest economy in the world by 2030.

China will kick the proverbial can down the road because it can. It never has to cooperate with America again.

Contrary to expectations, American chip companies are untouchable, and investors won't see Micron suddenly losing half its revenue over this trade war.

Until China can produce higher quality chips, it will lap up as much of Uncle Sam's chips until it can force transfer the chip technology from the Koreans.

American chip companies can breathe a sigh of relief.

"If we go to work at 8 a.m. and go home at 5 p.m., this is not a high-tech company and Alibaba will never be successful. If we have that kind of 8-to-5 spirit, then we should just go and do something else." - said Alibaba founder and executive chairman Jack Ma.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-23 01:05:202018-05-23 01:05:20Why the Big Deal Over ZTE?

Capitol Hill unleashed a healthy dose of criticism on Facebook (FB) CEO Mark Zuckerberg and he has mobilized the forces to avoid a repeat shellacking.

Zuckerberg's response has been to reshuffle his cabinet at the Menlo Park, CA, headquarters, and a few tell-tale signs offer a unique glimpse into Facebook's future.

Basically, something needed to change at Facebook.

The company single-handedly took the blame for the entire sector and was not the only company with a liberal stance on personal data.

Zuckerberg would like to eschew public humiliation and avoid being a sitting duck.

The episode in Washington highlights the need for Facebook to decouple itself from ad revenue, which makes up the lion's share of revenue at the firm and find other levers to pull.

Down the road, Facebook's ad business could get crimped by regulators, and a lack of fallback options haunts Facebook investors in their sleep.

Consequently, a whole slew of high-level management rotation is underway at Facebook.

It is the biggest shake-up in the history of Facebook.

The road map starts with one of Zuckerberg's best friends and protege Chris Cox who will manage the new "family of apps" segment.

This collection of projects he will preside over include WhatsApp, Messenger, Instagram, and the Facebook Core App.

The step up in responsibility is warranted for Chris Cox who was credited with creating the Facebook news feed after joining the company in 2005 after ditching his Stanford graduate degree program at the time.

The executive reshuffle coincided with WhatsApp co-founder Jan Koum, one of Silicon Valley's biggest advocates for data privacy, who quit his post as a show of disapproval to Facebook's business model.

Mark Zuckerberg wants to aggressively monetize the WhatsApp messenger service that was acquired for $19 billion in 2014.

Zuckerberg's blueprint involves using the WhatsApp phone numbers as a vehicle to monetize through offering different products.

Facebook would then collect the data from its 1 billion usership and WhatsApp would become Facebook's new advertisement clearing house.

WhatsApp's leadership vehemently refused this U-turn and Koum decided he would rather leave then see his baby ruined.

Facebook consistently refrained in the past from passing WhatsApp to the data mining scientists and was able to prevent full-scale implementations of advertisements onto its platform.

Currently, there are no ads on WhatsApp's interface, and users could be in store for a massive transformation in look and feel.

Facebook investors have been clamoring for Zuckerberg to start the process of making WhatsApp into a material revenue stream.

Time is of the essence as the big data police creep in from the shadows.

Putting Zuckerberg's top guy on the job embarks Facebook down a new path of hyper accelerated profit-making.

Well, that is the goal.

Compounding Facebook's pivot to other businesses is commissioning a new blockchain tech team.

Blockchain technology, the technology that helped unearth bitcoin, has seen a recent slew of endorsements from financial heavy hitters such as Goldman Sachs (GS), which acknowledged the formation of a new business brokering in bitcoin futures.

A year ago, no reputable organization would touch blockchain with a 10-foot pole.

The utilization of blockchain technology would allow trackability and provide more security.

That would help Facebook to understand the provenance of unique problems allowing staff to nip problems in the bud before they snowball.

Blockchain tech fits nicely within the constraints of the model and would enhance the existing Facebook product.

Let's not forget that Facebook has a mountain of cash to fix any problem that crops up.

It is not one of these early stage seed companies burning through heaps of cash waiting for "scalability" down the road.

Facebook is here and now, and it has the money to show for it.

The pillars of blockchain revolve around cryptography. Blockchain would effectively allow individuals to possess more power over their identity decentralizing the stranglehold from Menlo Park.

Thus, Facebook must invest deeply into blockchain to counter the fear that this technology can marginalize the core business.

This epitomizes the tendency for large-cap tech to become preemptive.

None of the powerful FANGs want to miss the next big shift in technology, and the cash hoard allows them to have skin in the game in each revolutionary trend.

The tide has changed at Facebook from the early years where growing the user base was paramount.

Now that user base has matured into a 2.2 billion marketplace.

Facebook's strategy has shifted to extracting more revenue per user and management closely follows this metric.

Mike Schroepfer, the CTO of Facebook, was tabbed as the man leading the charge for Artificial Intelligence (A.I.), Augmented Reality (A.R.), and Virtual Reality (V.R.) technology.

Facebook was able to poach Jerome Pesenti from IBM (IBM), where he was a critical cog in the development of IBM's Watson, to run the Facebook A.I. team. A.I. is routinely implemented into Facebook's core products to enhance performance.

Promoting Chris Cox as the next in line and giving him control over all the powerful products effectively pushes ad tech down the pecking order.

Javier Olivan is the new man at Facebook tasked for managing ads, analytics, and integrity, growth and product management.

Moving forward, the ad division will be laced with a certain level of security to avoid a repeat of Cambridge Analytica.

Zuckerberg must know that there are other Cambridge Analytica's hidden somewhere in the system; another incident would knock down the stock 5% to 10%.

Facebook could look vastly different in a few years if some of these profit drivers prove successful. It only needs one to work.

Disrupt or be disrupted.

At this point, the big tech companies are considering anywhere or anyone to capture accelerated growth. The FANGs are spilling over to other companies' turf.

Crossover is everywhere and this is just the beginning.

Expect Amazon's (AMZN) ad division to grow from the already $2 billion per quarter, gradually challenging the duopoly of Facebook and Alphabet in the digital ad revenue industry.

It is yet to be seen if the new revamp of management will produce better results.

This move could backfire as the management carousel excluded any fresh blood from taking part.

Effectively, Zuckerberg rotated his best friends into different parts of the business without demoting anyone.

Solidifying his close-knit circle of trust is no doubt a defensive reaction to being hounded the past few months, leaving his existing circle as the few people on which he can still count.

Facebook's stock remains healthy and the brouhaha stoked by the data leak gave investors a timely entry point.

I pounded on the table calling the bluff, begging readers to get into Facebook.

The long-term Facebook story is intact but the stock is overbought short-term.

Investors should not sleep on Facebook as it is a profit machine printing money like Apple (AAPL) and the executive revamp is a bullish development for Facebook.

My bet is that Chris Cox goes for the low hanging fruit monetizing WhatsApp, inciting the next leg up in Facebook shares later in the year.

"Simply put: We don't build services to make money; we make money to build better services." - said Facebook CEO Mark Zuckerberg

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Zuckerberg-on-the-Hill-image-2-e1526417830446.jpg343580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-16 01:05:032018-05-16 01:05:03What's Up at Facebook?

Featured Trade:

(THURSDAY, JUNE 14, 2018, NEW YORK, NY, GLOBAL STRATEGY LUNCHEON),

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, OR TAKING ANOTHER BITE AT THE APPLE),

(AAPL),

(FAREWELL TO DAVID ROCKEFELLER)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.