What happens after markets test the top end of a range? They test the bottom end of the range. So, the game here is to pick where and when is the next short-term top.

Now that Q1 earnings are out of the way, there is no major positive driver of the market for two more months, until the end of July, when the Q2 earnings start to roll out. And they will be good.

That leaves us only geopolitical shocks and chaos from Washington as the major market influences, and none of those are going to be positive. When traders shift from a focus on earnings to fear, the result is usually negative for share prices.

One major event that occurred last week but was totally ignored by the media was the administration's trade negotiating team scampering back from China completely empty handed. They called his bluff. So, the trade war is still on, it's just moved from the front burner to the back burner. Don't get complacent.

And here is the worrisome issue for the bulls. Q1 earnings were up 25.5% YOY, one of the best in my long career. Revenues accounted for 8.3%, margin improvements 8.1%, new tax breaks 7.6%, and share buybacks 1.5%. This means that 35.6% of the total earnings were from one-time only benefits that aren't going to be there next year.

Given that the global economy is slowing down, revenue and margin improvement will probably drop by half next year. That means the best case for Q1 2019 earnings will show a drop from 25.5% to only 8.2%.

It's not a matter of IF the market will top out, but WHEN. Enjoy the bull move while it lasts. It isn't going to be there next year.

I decided to sit out the current leg up in the market. I didn't think it would be big or sustained enough to squeeze in another round trip. Besides, after shooting out 26 Trade Alerts in April earning an eye-popping 12.54% profit, not only was my staff exhausted, so were the followers.

My year-to-date return stands at a robust 19.30%, my trailing one-year returns have risen to 55.59%, and my eight-year sits at an 295.77% apex.

And remember, the market is making this move in the face of rising oil prices and interest rates, always bull market killers.

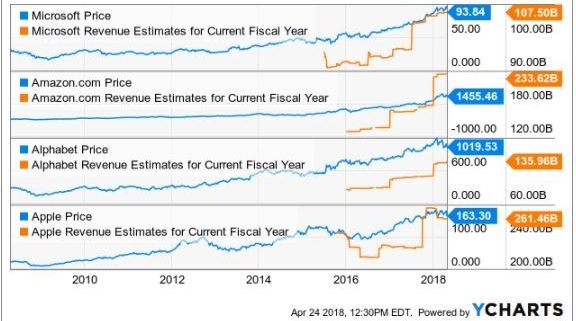

Of course, nobody at Apple (AAPL) cares about any of this one wit, as its stock blasted through to new all-time highs every day last week. Steve Jobs' creation is on a race to a $1 trillion market capitalization and was worth $930 billion at the market high. That's when Apple will have the same GDP as Russia or Australia.

The dividend yield has fallen to 1.56%. The company is increasingly being viewed as a luxury brand commanding a much higher multiple than the 9X that it earned when it was perceived as a lowly hardware company. By the way, Ferrari (RACE) has a price earnings multiple of 39X versus Apple's current 16X ex-cash.

I'll be raising my target for the stock from $200 to $220 as soon as I get time to write the report. Steve Jobs must be smiling down from Heaven. By the way, this service first recommended Apple as a strong "BUY" in 2010 when the shares traded at $10. That's a gain of 1,900%. Click here for the link.

Apple's stellar gains were part of a much broader move back into technology, which we expected. It turns out that the semiconductor cycle IS NOT ending after all, as predicted by the neophyte coverage of UBS.

Suddenly, all is forgiven at Facebook (FB), as the shares are now 2% short of an all-time high. Amazon is going from strength to strength, with Amazon Web Services' cloud business now accounting for an impressive $50 billion of sales and is growing at a breakneck 50% a year.

It all goes back to my seminal rule of investing that has worked for my entire 50-year career. While much of the rest of the U.S. economy is slowly fading from the scene, TECHNOLOGY ALWAYS COMES BACK!

The last of the Q1 earnings reports will dribble out this week.

On Monday, May 14, at 3:00 PM, we get a deluge of Feds speakers, now that the quiet period from the last meeting is over.

On Tuesday, May 15, at 8:30 AM EST, we receive the April Retail Sales, which has been red hot as of late. Home Depot (HD), a long-time Mad Hedge favorite, reports.

On Wednesday, May 16, at 8:30 AM, the April Housing Starts. Cisco Systems (CSCO) reports.

Thursday, May 17, leads with the Weekly Jobless Claims at 8:30 AM EST, which remained unchanged last week at 211,000, a 43-year low. At 10:00 AM EST, the April Index of Leading Economic Indicators is released, a compilation of 10 forward-looking statistics compiled by the private Conference Board. Applied Materials (AMAT) reports.

On Friday, May 18, we wrap up with the Baker Hughes Rig Count at 1:00 PM EST. Deere & Co. (DE) reports.

As for me, I'll be working in the garden this weekend. It's time to plant the pumpkins if I want nice jack-o-lanterns by Halloween, the tomatoes are thriving, and I will have an ample supply of fresh pepper this coming winter.

Good Luck and Good Trading.

Rolling in the Clover