(The Mad June traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE MALLARD MARKET and ME AND 23 AND ME),

(AAPL), (GOOGL), (AMZN), (TSLA), (MSFT), (META), (AVGO), (LRCX), (SMCI), (NVR), (BKNG), (LLY), (NFLX), (VIX), (COPX), (T), (NVDA), (LEN), (KBH)

There’s nothing like the comfort and self-satisfaction of having a 100% cash position in a falling market. While everyone else is bleeding red ink, I am happily plotting my next trades.

Of course, the rest of the market isn’t really bleeding red ink, just giving up windfall profits. Still, it’s better to trade from a position of strength than weakness. It makes identifying the next winners easier.

Think of this as the “Mallard Market”. On the surface, it seems calm and peaceful, while underwater, it is paddling along like crazy. The damage has been unmistakable. Dell, the faux AI stock (DELL) crashed by 28%, Salesforce (CRM) got creamed for 34%, and ServiceNow (NOW) got taken to the woodshed for 22%.

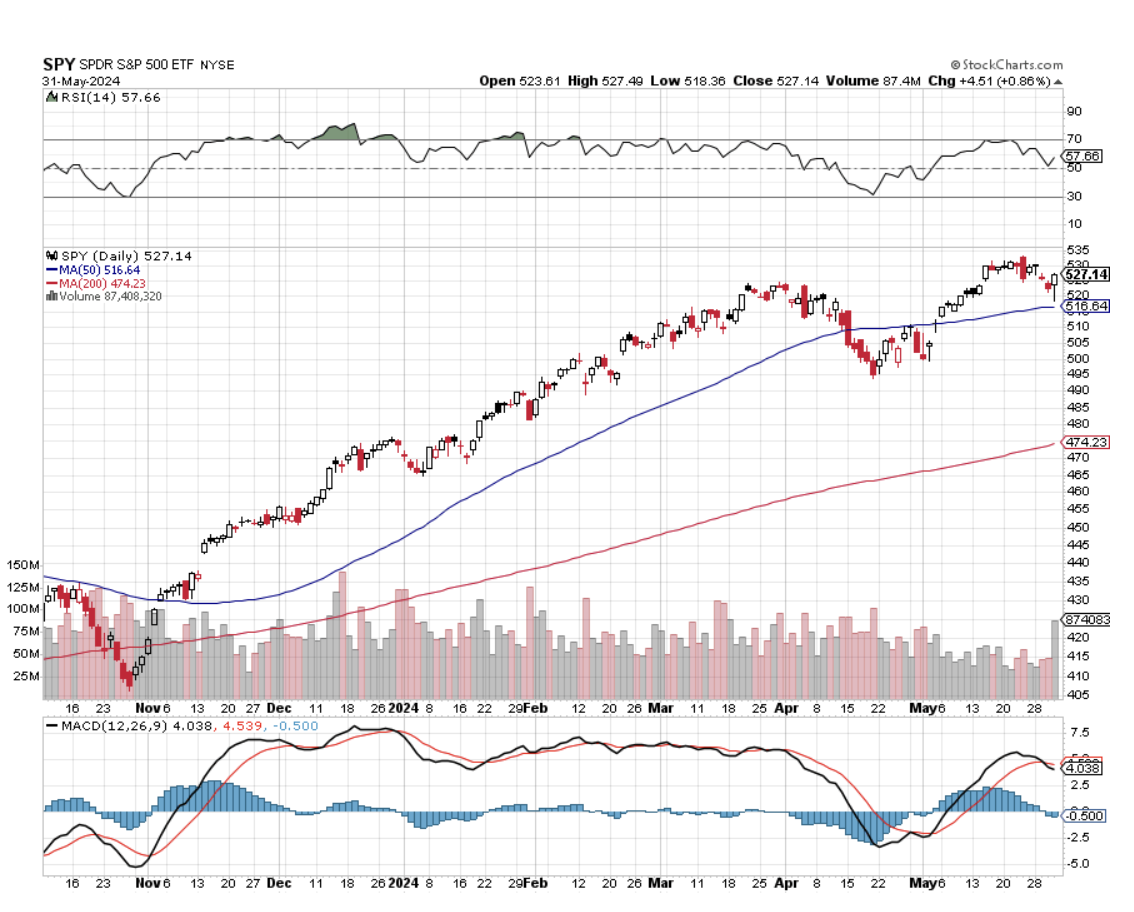

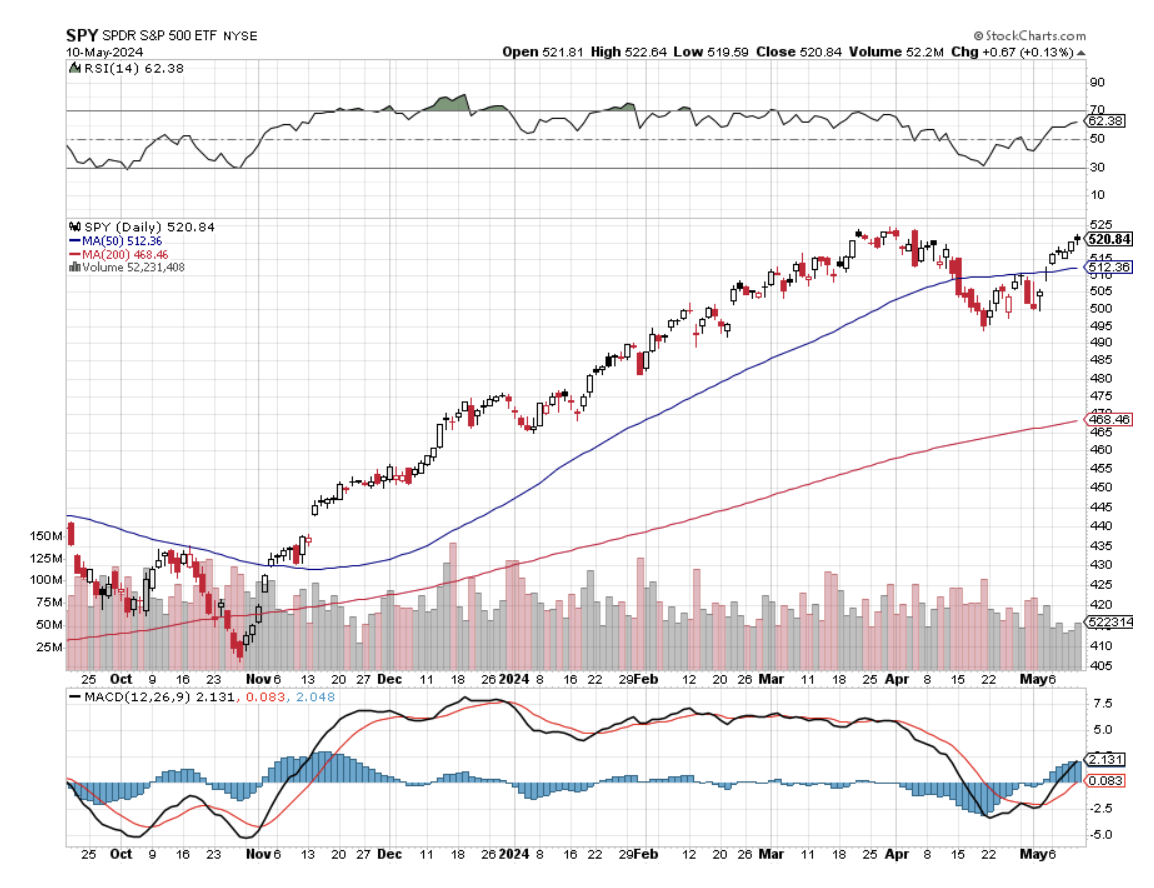

It all belies a market that is incredibly nervous and fast on the trigger. The tolerance for any bad news is zero. Yet there has been no market crash as I expected. The 5,300 level for the (SPX) seems to possess a gravitational field, powered by $250 earnings per share and a multiple of 51X.

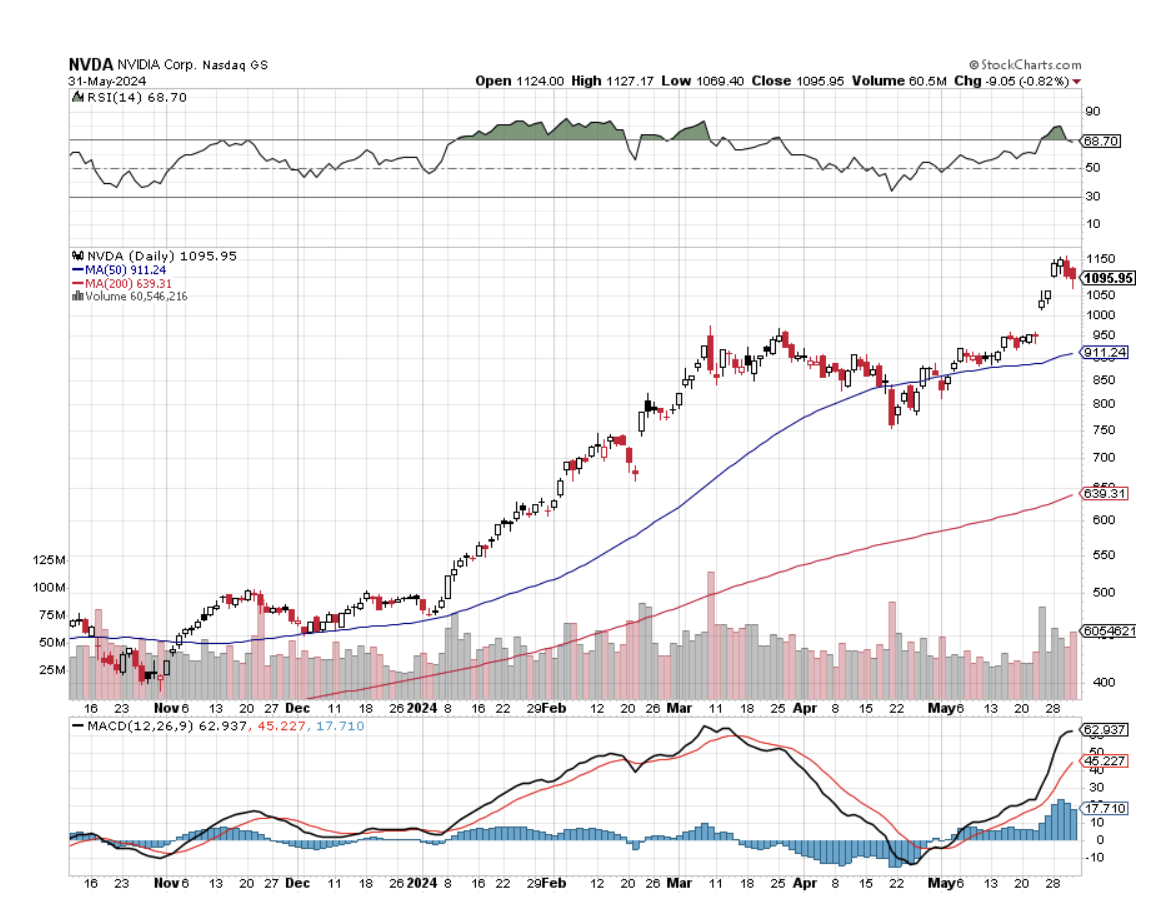

It was NVIDIA that put the writing on the wall by announcing a 10:1 split that has opened the floodgates for similar prosperous and high-priced companies.

There are now 36 stocks with share prices of $500 or more ripe for splits with $7 trillion in market cap, or 16% of the total market. While splits don’t change the value of a company, perceptions are everything, as they prove shareholder-friendly policies. While individual investors are confused by an onslaught of contradictory research recommendations, splits are a great “tell” on what to buy next.

Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), and Tesla (TSLA) have already carried out splits, some multiple times, to great success. Of the Magnificent Seven, only Microsoft (MSFT) and Meta (META) have yet to split.

In the tech area Broadcom (AVGO), Lam Research (LRCX), Super Micro Computer (SMCI), and Service Now (NOW) have yet to split. In the non-tech area, there are NVR Inc. (NVR), Booking Holdings (BKNG), Eli Lilly (LLY), and Netflix (NFLX). Many of these are well-known Mad Hedge recommended stocks.

History has shown that stocks rise 25% one year after a split compared to 12% for the market as a whole. A stock’s addition to the Dow Average or the S&P 500 (SPY) provides a boost. If both occur, stocks will absolutely explode. Stock splits are also much more attractive than buybacks at these high prices.

So, I’ll be trolling the market for split-happy candidates.

You should too.

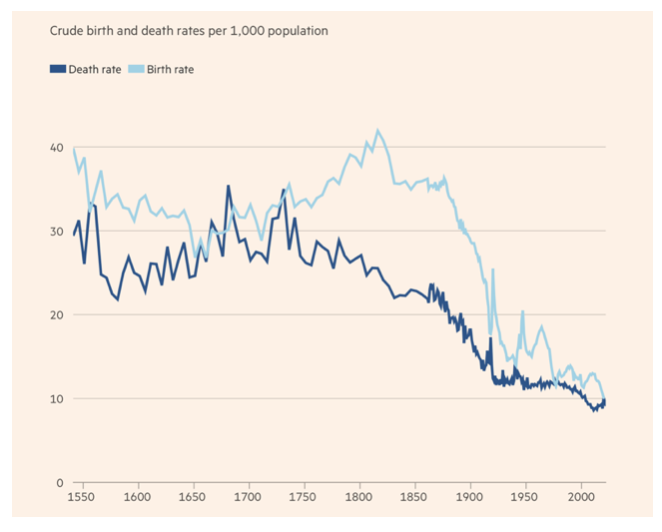

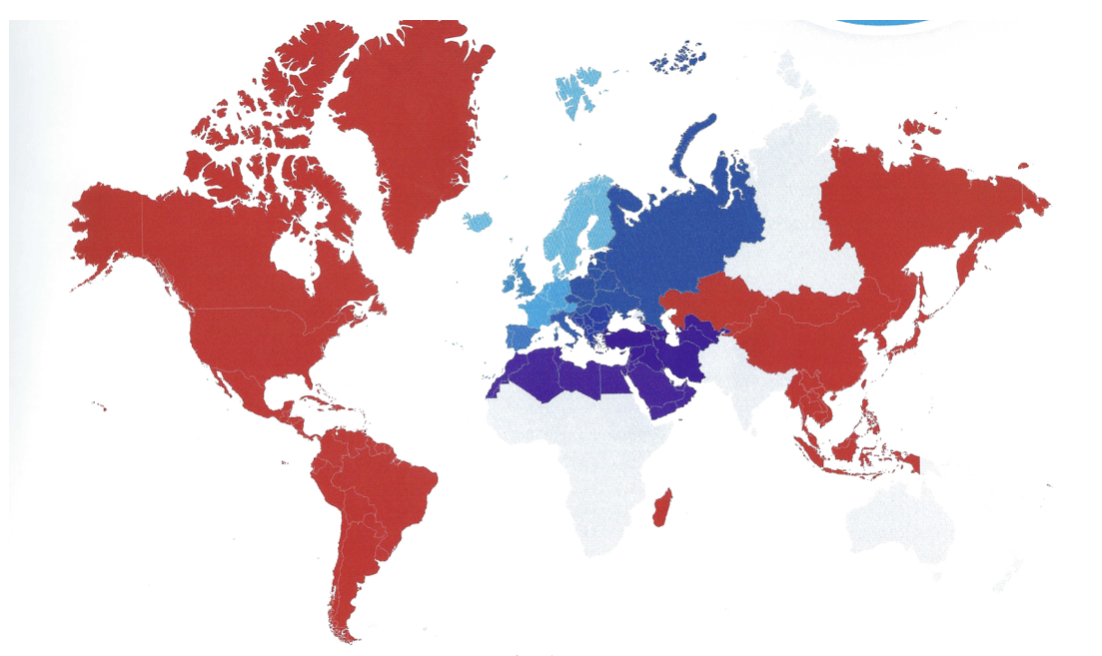

Since it may be some time before we capitulate and take a worthwhile run at new highs, I thought I’d update you on the global demographic outlook, which is always a long-term driver of economies and markets.

People are now living longer than ever before. But postponing death is only a part of the demographic story. The other is the decline in births. The combination of the two is creating huge changes in the global economy.

The notion of a “demographic transition” is almost a century old. Human societies used to have roughly stable populations, with high mortality matched by high fertility. Families had eight kids and 3-5 usually died in childhood, barely maintaining population growth.

In England and Wales in the 18th and 19th centuries, death rates suddenly plummeted. But fertility did not. The result was a population explosion. As the benefits of economic growth and advances in medicine and public health spread, most of the world has followed a similar transition, but far faster. As a result, human numbers rose fourfold over the last hundred years, from 2 billion to 8 billion.

In time, fertility followed mortality on a downward path across most of the world. As a result, fertility rates in more than half of all countries and territories in 2021 fell below the replacement level. For the world as a whole, the fertility rate was 2.3 in 2021, barely above the replacement of 2.1, down from 4.7 in 1960.

For high-income countries, the fertility rate was a mere 1.6, down from 3.0 in 1960. In general, poor countries still have higher fertility rates than richer ones, but they have been falling there, too.

What explains this collapse in fertility rates? An important part of the answer is the wonderful surprise that more children survived than expected. So, people started to practice various forms of birth control.

But the desire to have many children also shrank sharply. When husbands realized that smaller families meant high standards of living for themselves, family sizes dropped sharply. Even in ultra-conservative Iran, the fertility rate has collapsed from 6.6 in 1980 to only 1.7 in 2021.

A big reason for this shift was that, for their parents, children have moved from being a valuable productive asset in the 19th century to an expensive luxury today. That was back when 50% of our population worked on farms. Today it’s only 2%.

In the meantime, female participation in the economy rose dramatically in the 20th century, including in highly skilled careers. That raised the “opportunity cost” of producing children, especially for mothers. So, they have children later, or even not at all.

Where public childcare is more generous women are encouraged to combine careers with having children. The absence of such help helps explain the exceptionally low fertility rates in much of East Asia and Southern Europe, where parental support is limited.

This global shift towards very low fertility, with the exception (so far) of sub-Saharan Africa, is among the most important events driving the global economy. One implication is that the population of Africa is forecast to be larger than that of all today’s high-income countries, plus China by 2060, thanks to the elimination of many diseases there.

Why is all this important?

Because rising populations create larger markets, more profits for corporations, and rising share prices. Shrinking populations have the opposite effect, as China is learning about its distress now. One reason the US is growing faster than the rest of the world is that a continuous stream of new immigrants since its foundation has created endless numbers of new workers and customers. Dow 240,000 here we come!

Just thought you’d like to know.

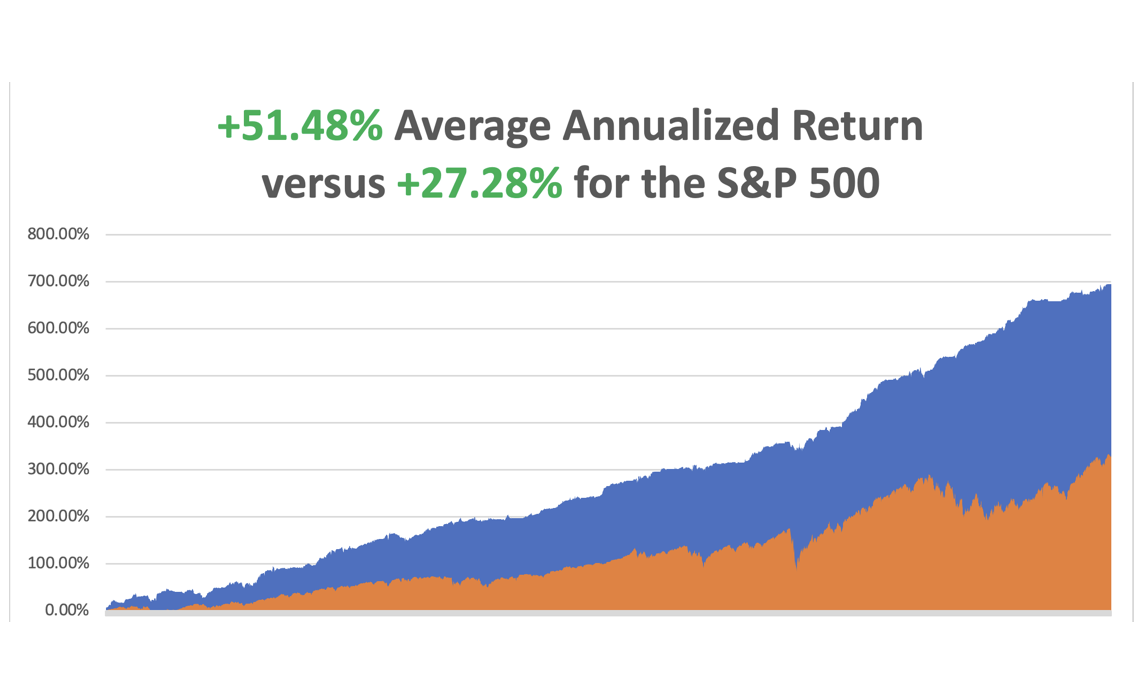

So far in May, we are up +3.74%. My 2024 year-to-date performance is at +18.35%.The S&P 500 (SPY) is up +10.48%so far in 2024. My trailing one-year return reached +35.74%. That brings my 16-year total return to +694.78%.My average annualized return has recovered to +51.48%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I bailed on my last position early in the week, covering a short in Apple for a profit.

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Fed’s Favorite Inflation Gauge Cools by 0.2% in April, with the PCE, or the Personal Consumer Inflation Expectations Price Index. This one strips out the volatile food and energy components. It gives more credibility to a September rate cut and gave bonds a good day. NVIDIA Shares Continues to Go Ballistic, creating another $800 billion in market capitalization in three trading days. That is the most in history. That took NASDAQ to a new all-time high at 17,000. At $2.8 trillion (NVDA) could become the largest publicly traded company in the world in another day. Today’s tailwind came from an Elon Musk comment that his new xAI start-up would buy the company's high-end H100 graphics cards. Buy (NVDA) on the next 20% dip.

Pending Home Sales Dive, down 7.7% in April, the worst since the Covid market three years ago. The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market. But the anticipated rate cuts later this year should lead to better conditions, with improved affordability and more supply. Buy (LEN) and (KBH) on dips.

Money Supply Rises for the First Time in More than a Year. Remember money supply? As measured by M2, it sums up the currency, coins, and savings deposits held by banks, balances in retail money-market funds, and more. Data for April released on Tuesday afternoon showed an increase of 0.6% from a year ago. The Fed balance sheet has shrunk by $1.5 trillion in two years, the fastest decline in history, slowing the economy.

AT&T’s (T) Copper is Worth More Than the Company, and with plans to convert half its copper network to fiber by 2025 could free up billions of tons of the red metal to sell on the market. Copper prices have doubled over the past two years, and they could double again by next year. Worldwide there are 7 trillion tons of copper wire in place. Fiber is cheaper and exponentially more efficient than copper, which is facing huge demands from AI, EVs, and the electrification of the grid. Buy copper (COPX) on dips.

Markets are Underpricing Low Volatility (VIX), not a good thing at all-time highs. Volatility across equity and currency markets is low. The Volatility Index (VIX) at $12.46 compares with an average over five years of $21.5 and over the longer term of $19.9. Markets are heavily discounting good news and a disinflationary environment. It is not only stocks. There is also low volatility across currency markets. The DB index of foreign exchange volatility is at $6.3 versus an average of $7.6 over five years and $9.3 over the longer term. This will end in tears.

S&P Case Shiller Jumps to New All-Time High, with its National Home Price Index. The index rose by 1.29%, the fastest growth since April 2023. All 20 major metro cities were up last month and gained 6.5% YOY. Four cities are currently at all-time highs: San Diego, Los Angeles, Washington, D.C., and New York. Prices in San Diego saw the biggest gain, up 11.4% from February of 2023. Both Chicago and Detroit reported 8.9% annual increases. Portland, Oregon, saw the smallest gain in the index of just 2.2%. Unaffordability is the big story in the market right now. The sunbelt is seeing the most weakness, thanks to a post-pandemic construction boom.

Space X’s Starlink Tops 3 million Subscribers, and is rapidly moving towards a global WiFi network. I set up a dozen of these in Ukraine last October and even the Russians couldn’t hack them. It sets a global 200 Mb standard usable in most countries, even the remote Galapagos Islands in the Pacific. It’s only a VC investment now but could become Elon Musk’s next trillion-dollar company.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 3, the ISM Manufacturing PMI is released.

On Tuesday, June 4 at 7:00 AM, the JOLTS Job Openings Report will be published.

On Wednesday, June 5 at 7:00 AM, the ISM Services PMI is published.

On Thursday, June 6 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Challenger Job Cuts Report.

On Friday, June 7 at 8:30 AM, the Nonfarm Payroll and headline Unemployment Rate are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when Anne Wojcicki founded 23andMe in 2007, I was not surprised. As a DNA sequencing pioneer at UCLA, I had been expecting it for 35 years. It just came 70 years sooner than I expected.

For a mere $99 back then they could analyze your DNA, learn your family history, and be apprised of your genetic medical risks. But there were also risks. Some early customers learned that their father wasn’t their real father, learned of unknown brothers and sisters, that they had over 100 brothers and sisters (gotta love that Berkeley water polo team!), and other dark family secrets.

So, when someone finally gave me a kit as a birthday present, I proceeded with some foreboding. My mother spent 40 years tracing our family back 1,000 years all the way back to the 1086 English Domesday Book (click here)

I thought it would be interesting to learn how much was actually fact and how much fiction. Suffice it to say that while many questions were answered, alarming new ones were raised.

It turns out that I am descended from a man who lived in Africa 275,000 years ago. I have 311 genes that came from a Neanderthal. I am descended from a woman who lived in the Caucuses 30,000 years ago, which became the foundation of the European race.

I am 13.7% French and German, 13.4% British and Irish, and 1.4% North African (the Moors occupied Sicily for 200 years). Oh, and I am 50% less likely to be a vegetarian (I grew up on a cattle ranch).

I am related to King Louis XVI of France, who was beheaded during the French Revolution, thus explaining my love of Bordeaux wines, women wearing vintage Channel dresses, and pate foie gras.

Although both my grandparents were Italian, making me 50% Italian, I learned there is no such thing as pure Italian. I come out only 40.7% Italian. That’s because a DNA test captures not only my Italian roots, plus everyone who has invaded Italy over the past 250,000 years, which is pretty much everyone.

The real question arose over my native American roots. I am one-sixteenth Cherokee Indian according to family lore, so my DNA reading should have come in at 6.25%. Instead, it showed only 3.25% and that launched a prolonged and determined search.

I discovered that my French ancestors in Carondelet, MO, now a suburb of Saint Louis, learned of rich farmland and easy pickings of gold in California and joined a wagon train headed there in 1866. The train was massacred in Kansas. The adults were all killed, and the young children were adopted into the tribe, including my great X 5 Grandfather Alf Carlat and his brother, then aged four and five.

When the Indian Wars ended in the 1880s, all captives were returned. Alf was taken in by a missionary and sent to an eastern seminary to become a minister. He then returned to the Cherokees to convert them to Christianity.By then, Alf was in his late twenties so he married a Cherokee woman, baptized her, and gave her the name of Minto, as was the practice of the day.

After a great effort, my mother found a picture of Alf & Minto Carlat taken shortly after. You can see that Alf is wearing a tie pin with the letter “C” for his last name Carlat. We puzzled over the picture for decades. Was Minto French or Cherokee? You can decide for yourself.

Then 23andMe delivered the answer. Aha! She was both French and Cherokee, descended from a mountain man who roamed the western wilderness in the 1840s. That is what diluted my own Cherokee DNA from 6.50% to 3.25%. And thus, the mystery was solved.

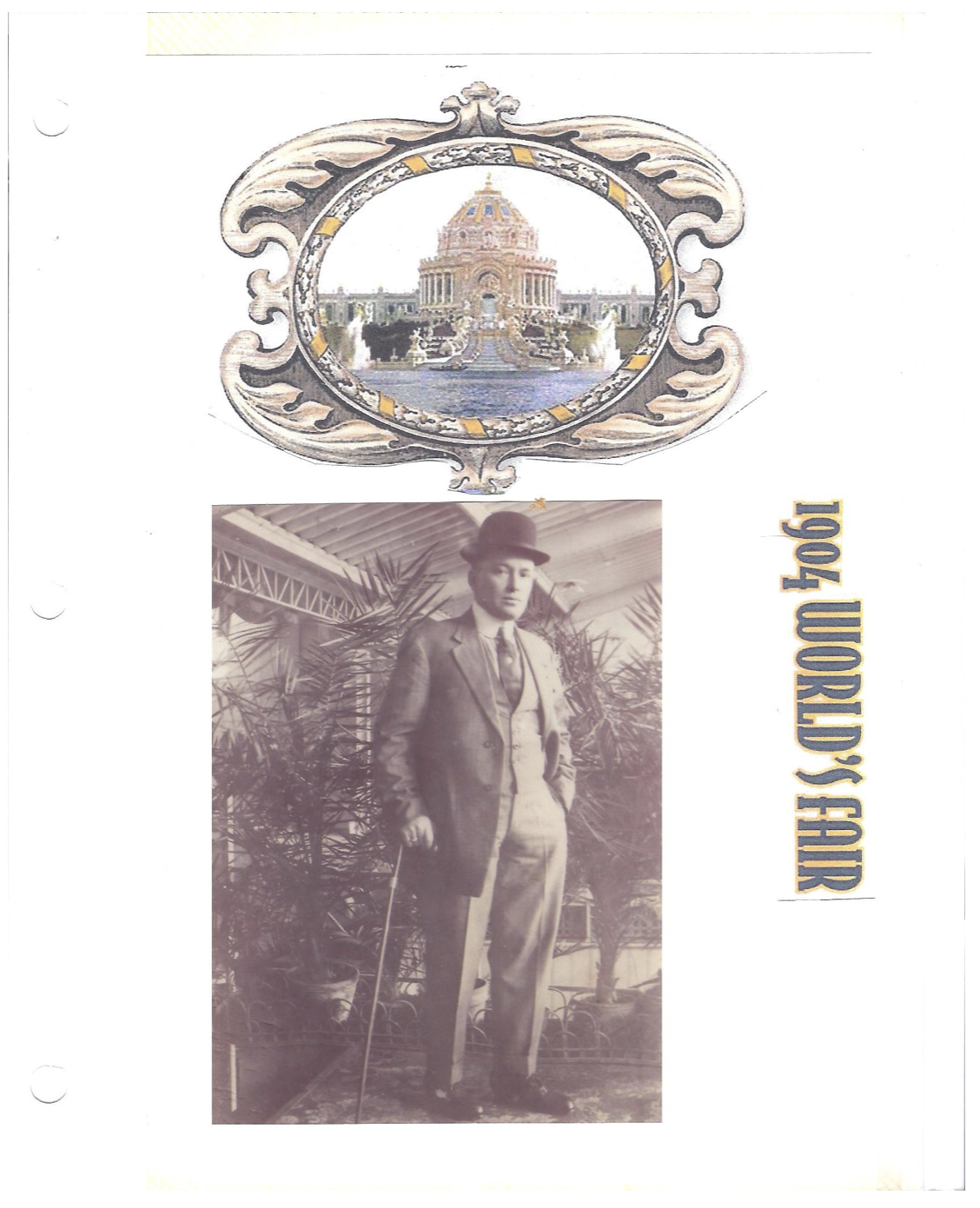

The story has a happy ending. During the 1904 World’s Fair in St. Louis (of Meet Me in St. Louis fame), Alf, then 46, placed an ad in the newspaper looking for anyone missing a brother from the 1866 Kansas massacre. He ran the ad for three months and on the very last day, his brother answered and the two were reunited, both families in tow.

Today, getting your DNA analyzed starts from $119, but with a much larger database, it is far more thorough. To do so, click here.

My DNA Has Gotten Around

It All Started in East Africa

1880 Alf & Minto Carlat, Great X 5 Grandparents

The Long-Lost Brother

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/01/alf-minto.jpg252293april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-03 09:02:142024-06-03 11:56:52The Market Outlook for the Week Ahead, or Welcome to the Mallard Market

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DOW 40,000 AND HANGING WITH THE AMAZON HEADHUNTERS)

(TLT), (JNK), (WES), (ET), (GLD), (SLV), (MSFT),

(NVDA), (AAPL), (SPY), (FXI), (COPX), (FCX)

When I entered the stock market in 1982 when the Dow was at 600 and you told me the Average would reach 40,000 in 42 years, I would have thought you delusional, out of your mind, and stark raving mad.

Yet, here it is 2024 and here we are, with the index up an eye-popping 66.6 times. The good news is that we are now only one triple away from reaching my long-term target of 120,000. Never underestimate the power of compounding, which my friend Warren Buffet describes as a snowball.

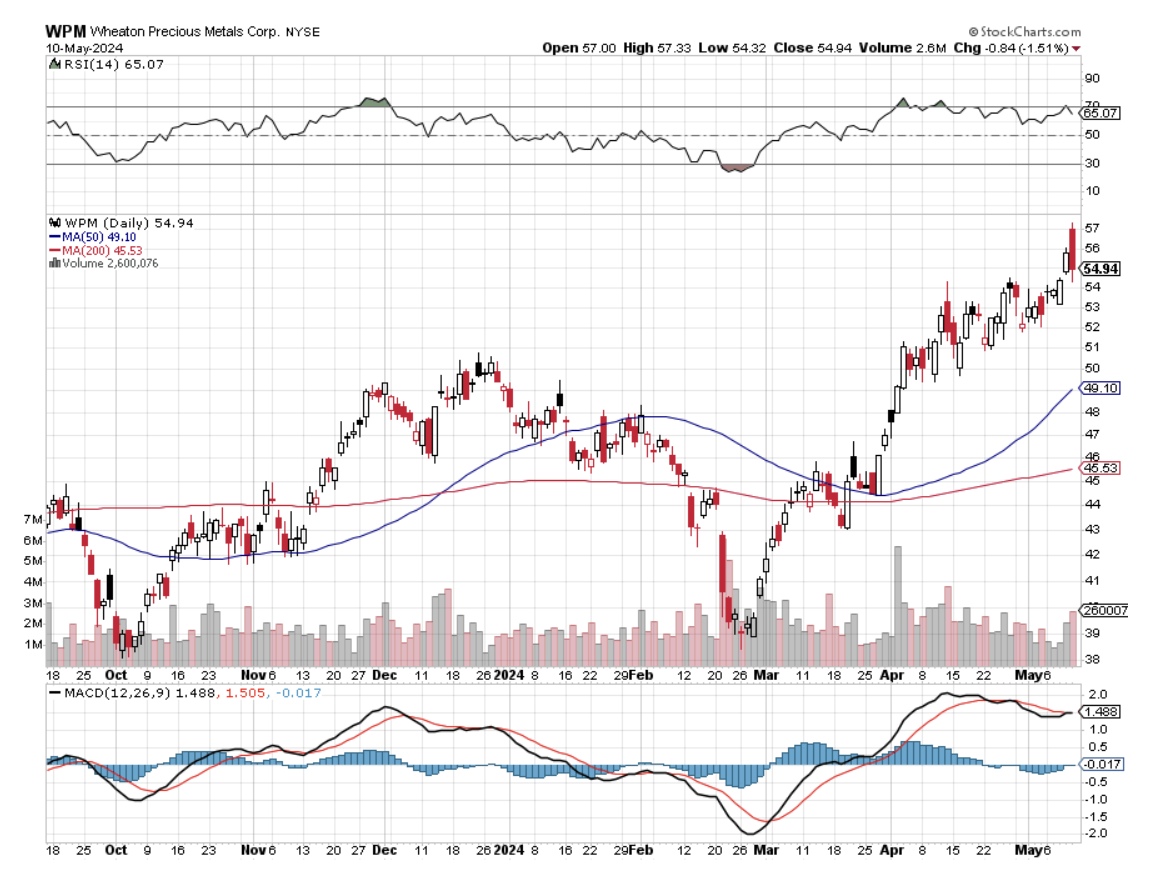

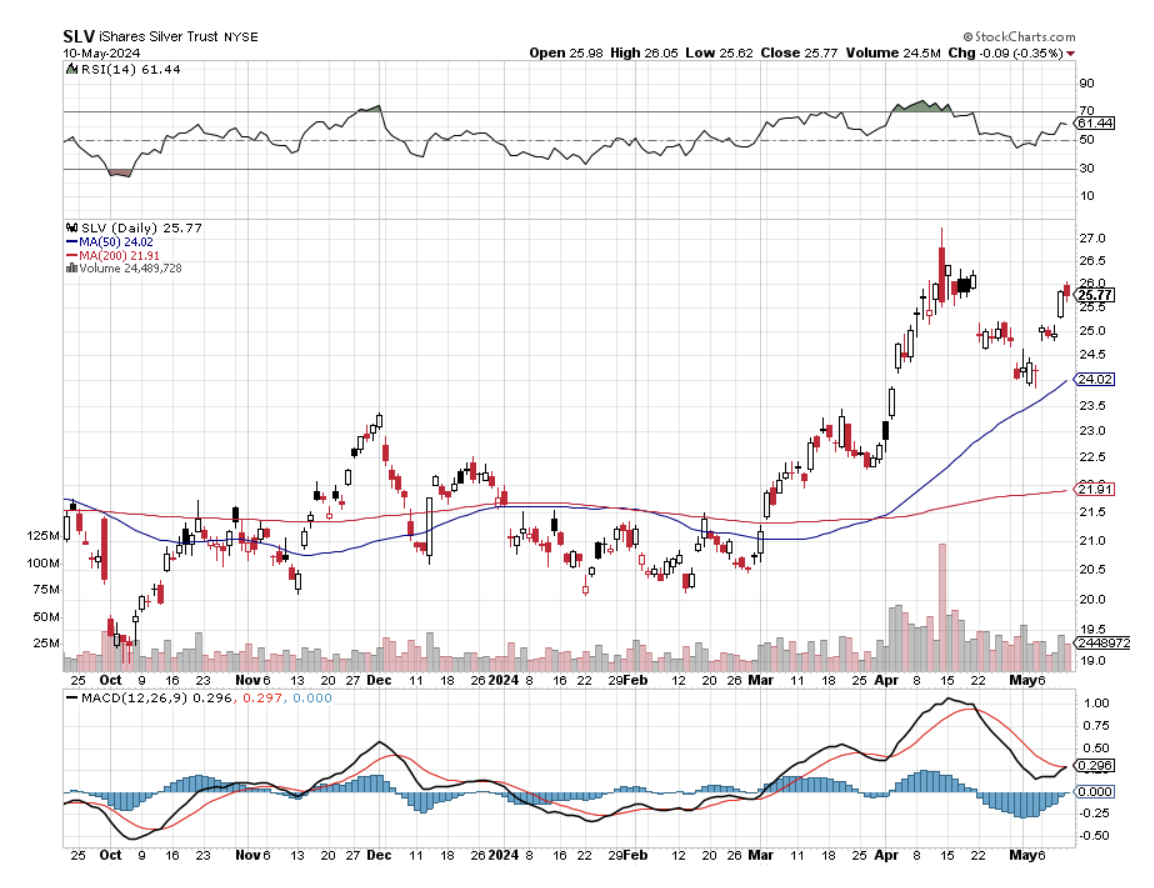

You can’t help but be impressed with the performance of precious metals over the last two weeks, up 6.50% for (GLD) and a ballistic 20% for (SLV). Metals producers are unable to rush supplies to the market fast enough to cover their shorts in the futures market, creating a massive short squeeze.

Long may it continue.

The moves validate my own forecasts for the barbarous relic to hit $3,000 and the white metal to reach $50 sometime in 2025.

One cannot underestimate the power of the weakening economic data over the last fortnight. As a result, we have gone from “Higher for longer” to “Lower sooner”, with huge consequences for all asset classes.

That brings to the fore investment in fixed-income securities. There are two ways to make money on a fixed income. Coupon interest rates are still at historically high levels. And as rates fall, fixed-income prices rise, opening the door to capital gains, which could reach 10%-20% in the coming year.

The fixed-income market, at $100 trillion is double the size of the stock market. And there are many more bond listings than stock ones. So the number of possible investments is almost endless. I shall give you a brief overview of some of the more interesting subsectors.

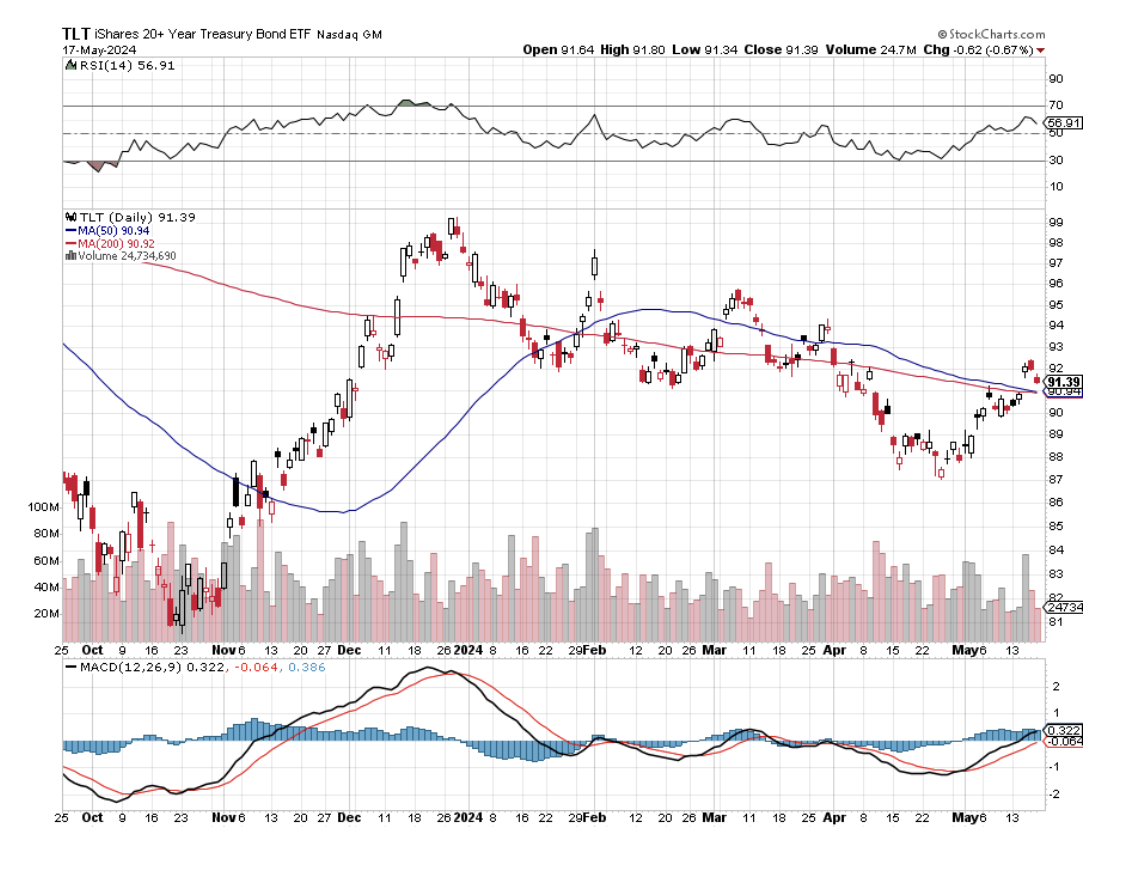

US Government bonds – are the gold standard with a guaranteed return. But you pay for the extra security with lower rates; the current ten-year US Treasury bond yield is 4.42%, much lower than the present 90-day T-bill of 5.25%. The easiest way to buy these is through the (TLT). The 30-year government bond should be avoided as the extra 0.14% in yield doesn’t adequately compensate you for the extra 20 years of risk

Junk Bonds – Also known as “high yield” bonds have always been misnamed. The default rates never remotely approached the levels that justified their high yields, not even during the financial crisis, as my old friend former junk bond king Michael Milliken has amply proven. The (JNK) is currently yielding 6.59% and has the potential for larger capital gains than government bonds.

Master Limited Partnerships – These are partnerships granted generous tax benefits with the goal of producing oil. They issue annual Form K-1’s to include with your tax return. Dividends are deferred until the MLP’s investment reaches the end of its useful lives, which can be decades. MLP’s used to be a huge industry with dozens of listed companies.

When the price of oil went to negative numbers during the pandemic, most of them got wiped out. Because of this rocky past, there are a handful of large, well-capitalized MLP’s that with extremely high yields. One is Western Midstream Partners (WES) with a 9.20% yield. Energy Transfer Partners (ET) pay a 7.96% yield.

These yields will remain safe as long as oil prices are stable or rising, as I expect in a long-term global economic recovery. Take oil back to zero again in another pandemic and these returns will get turned on their head.

With the normalizing of interest rates, it's time to normalize investment strategies as well. That means bringing back the old 60/40 strategy where one half of the portfolio ensures the other, with a modern twist. You can put 60% of your assets in stocks, with half on technology and half on domestic cyclicals.

The other 40% should be allocated to some mix of the above fixed-income investments guaranteeing annual high returns. In not a bad strategy for mature investors, especially if they would rather be on a golf course instead of spending all day in front of a screen picking bottoms and tops for stocks, like Millennials.

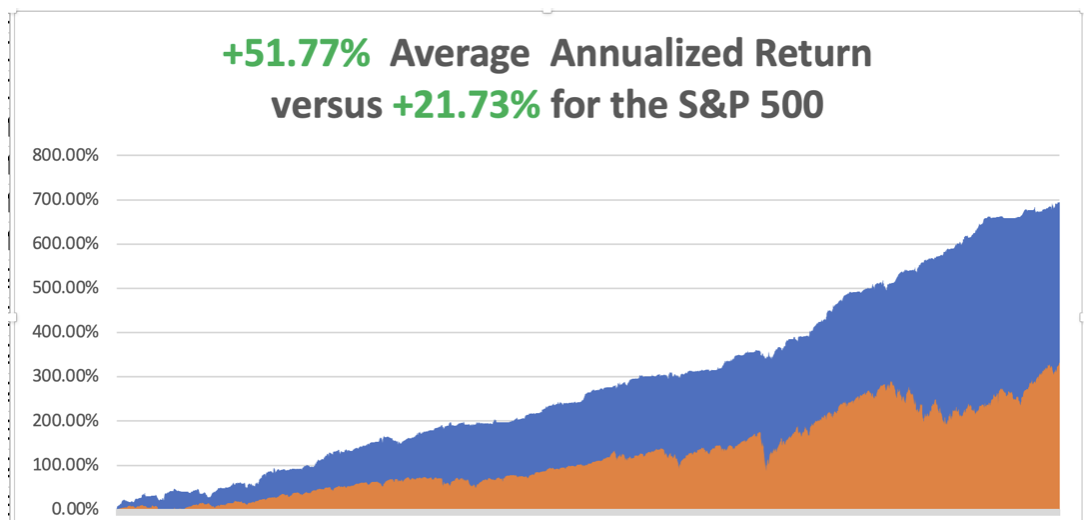

So far in May, we are up +3.01%. My 2024 year-to-date performance is at +17.62%.The S&P 500 (SPY) is up +10.90%so far in 2024. My trailing one-year return reached +32.80%versus +29.02% for the S&P 500. That brings my 16-year total return to +694.56%.My average annualized return has recovered to +51.77%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I let my (GLD) and (SLV) positions expire at max profit. I did the same with my (MSFT) short. I sold my (NVDA) and (TLT) shorts for a nice profit. That leaves me with just two positions, a long in (SLV), which has gone ballistic, and a short in (AAPL).

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Bull Market has Five More Years to Run, with S&P 500 (SPY) growing earnings at 10% a year for the foreseeable future. Last year brought in $222 per share, 2024 will see $250, 2025 $270, and $300 for 2026. The Great American Golden Age has only just begun. Profit margins will expand to all-time record highs. Falling rates and a weak dollar will boost exports to a recovering Europe and Japan. Inflation should hit the Fed’s 2% in 2025 as AI chatbots replace workers at a breakneck rate, cutting costs dramatically. The future is happening fast. Buy everything on dips, even bonds.

CPI Comes in Cool, in April at 0.3% versus 0.4% expected, taking stocks to new all-time highs. Inflation resumed its downward trend at the start of the second quarter in a boost to financial market expectations for a September interest rate cut. Buy em!

PPI Comes in Hot at 0.5%, and up 2.2% YOY, putting up another potential roadblock to interest rate cuts anytime soon. The PPI is a gauge of prices received at the wholesale level that came in higher than the 0.3% estimate. Higher for longer rules. The last mile, or the last 1$ drop in inflation is always the hardest and usually requires a recession. Higher for longer rules.

Retail Sales Come in Surprisingly Flat in April, setting up a Goldilocks economy for the Fed to cut rates in September. The unchanged reading in retail sales last month followed a slightly downwardly revised 0.6% increase in March, the Commerce Department's Census Bureau said on Wednesday. Retail sales were previously reported to have risen 0.7% in March.

Biden to Increase China Tariffs (FXI) to 100%, on key sectors including electric vehicles, batteries, solar cells, steel, and aluminum. Biden has previously announced the steel and aluminum tariffs, which will increase to 25% on some products that have a 7.5% rate or no tariffs now. The EV rate aims to protect the US from a potential flood of Chinese autos that could upend the politically sensitive auto sector. The total tariff on Chinese electric vehicles will rise to 102.5% from 27.5. Biden’s union support is clear for all to see.

Copper Hits Record Highs, as hedge funds, trend followers, bearish shorts, and Chinese speculators pile in. New York prices hit $5 a pound, while London reached $11,000 per metric tonne. The price action is similar to other commodities with disrupted supplies like Cocoa and Nickel. The runaway market will continue. Buy (FCX) and (COPX) on dips.

As the Dow Tops 40,000, investors are pouring money into both bonds and stocks, according to the Bank of America. Equity funds saw $11.9 billion in inflows, while bond funds drew in $11.7 billion. Within fixed income, Treasury inflation-protected securities (TIPS) saw outflows of $700 million, the most in nine weeks. Keep buying those dips.

Weekly Jobless Claims Drop 10,000, to 222,000, after seasonal factors caused a significant increase in New York claims in the prior week. The four-week moving average, which helps smooth short-term fluctuations in weekly claims figures, increased to 217,750, the highest level since November.

Solar Storm Hits Starlink, taking out several hundred satellites and degrading service, says Elon Musk. Starlink, the satellite arm of Elon Musk's SpaceX, is suffering as the Earth is battered by the biggest geomagnetic storm due to solar activity in two decades. Starlink owns around 60% of the roughly 7,500 satellites orbiting Earth and is a dominant player in satellite internet.The U.S. National Oceanic and Atmospheric Administration has said the storm is the biggest since October 2003 and is likely to persist over the weekend, posing risks to navigation systems, power grids, and satellite navigation.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 20, nothing of note takes place.

On Tuesday, May 21 at 1:30 PM EST, API Crude Oil Stocks are released.

On Wednesday, May 22 at 2:00 PM, the Existing Homes Sales are published

On Thursday, May 23 at 7:00 AM, we get New Home Sales. And at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, May 24 at 8:30 AM, the Durable GoodsReport is announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

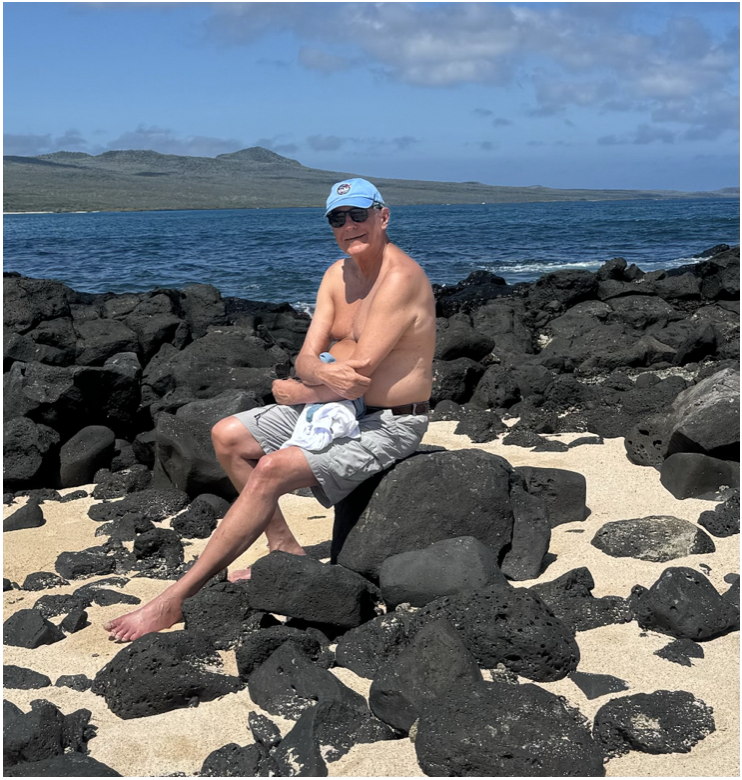

As for me, when I crossed the Continental Divide at 13,300 in the Andes Mountains of Ecuador last week, the vast expanse of the Amazon Basin lay before me. Clouds danced in and out of the treetops, waterfalls plunged down precipitous slopes, and the jungle spread out for 2,000 miles east. I was somewhat buzzed by the altitude but still enjoyed every minute.

My destination was the Termos Papallacta spa on the slopes of an ancient volcano which offered steaming hot sulfuric waters and a brisk massage for $50. Colorful exotic flowers abounded. This is where the wealthy of Quito come to salve arthritis and aches and pains in magical waters.

How do you get wealthy in Ecuador? Bananas, tourism, real estate speculation, and flower exports to the US. Given my experience with Japanese onsens, I had no problem with their ultra-hot waters.

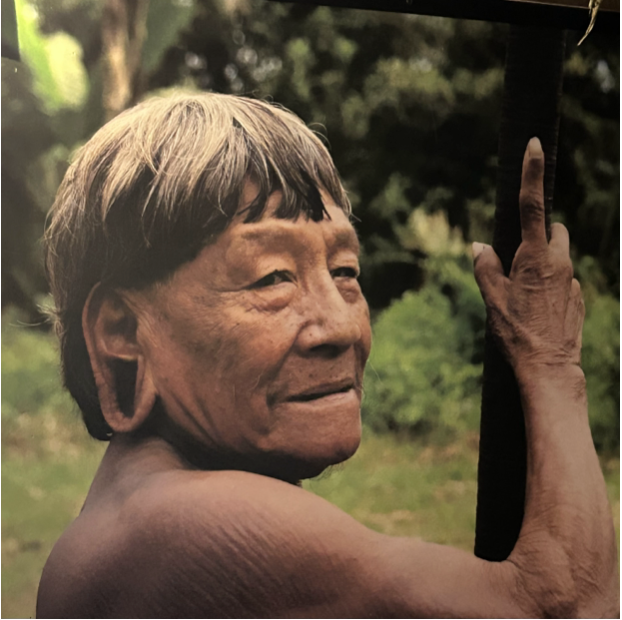

This is the land of the Jivaro Clan, the world’s last known headhunters. Their final victim was a National Geographic Society explorer in 1961. Recently, his grandson traveled to Ecuador to retrieve the head and return it to the US for a respectful burial, all to great fanfare in the local press. The Jivaro still shrinks heads, but only of animals which they sell to tourists just to keep the practice alive.

Ecuador is the great test bed for monetary experts around the world. In 1999, they suffered a financial crisis where the value of their currency, the Sucre, collapsed to 25,000 to the dollar. The central bank responded by changing the national currency to the US dollar and only permitting conversion from the old currency at $2 per person.

The move had several unintended consequences. The savings of everyone in the country were wiped out overnight. But it also eliminated their debt. Those with relatives sending back remittances from the US suddenly became wealthy and bought up all the real estate they could. In the end, it created an economic boom that continues to today.

Today, Ecuador is one of the friendliest, and cheapest countries in South America. It elected Daniel Noboa as president in 2023, the scion of a banana fortune, who has been hugely popular. The government cracked down on the drug gangs, arresting everyone with a suspect tattoo. Today the police and army are everywhere, and the streets are safe. There are armed checkpoints at key intersections. The ownership of firearms and even long knives has been banned.

The country has no seasons, sitting right on the Equator, and is temperate all year long. Even at 13,300 feet, there is no snow. I had no problem with the food, but then I had a cast iron stomach battle-tested in 135 countries. Not even the locals drink the tap water, which is only used for washing. It has to be all bottled water all the time or you die and you often see people lugging around one-gallon bottles.

Retiring Americans have noticed and some 20,000 now live in the country on their Social Security checks at one-third the cost of home. They concentrate on cultural hot spots, like the ancient city of Cuenca, where the local hospitals speak English, are experts in gerontology, and accept Medicare. You can buy a nice home in a mountain urban area for $250,000 and beachfront digs for $500,000. The Marriot Hotel in Quito cost me $160 a night and a steak dinner was $19 and to die for.

You can’t go to Quito without visiting the Equator for which the country was named, a tourist mecca where everyone gets pictures straddling the northern and southern hemispheres. The country has two summer solstices a year, one in the spring and one in the fall, as the sun transits from north to south, then south to north.

I passed on the shrunken head, which I thought grotesque, and got the T-shirt instead. Besides, US Customs might have questions (Do you have any shrunken heads to declare?). I think I’ll be returning to Ecuador soon.

Descending into the Amazon

Jivaro Indian

Shopping for Breakfast

A Slow Day at the Flower Market

A Smoothie for Lunch

Standing on the Equator, One Foot in Each Hemisphere

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/05/John-thomas-equator.png764572april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-05-20 09:02:552024-05-20 11:41:39The Market Outlook for the Week Ahead, or Dow 40,000

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT AMERICAN GOLDEN AGE HAS ONLY JUST BEGUN and SWIMMING WITH THE SHARKS)

(AAPL), (NVDA), (META), (GLD), (GOLD), (SLV), (WPM), (MSFT), (NVDA), (TLT), (FCX), (FXI), (BRK/B)

The Bull Market has Five More Years to Run, with S&P 500 growing earnings at 10% a year for the foreseeable future. Last year brought in $222 per share, 2024 will see $250, 2025 $270, and $300 for 2026. The Great American Golden Age has only just begun.

Profit margins will expand to all-time record highs. Falling interest rates and a weak dollar will boost exports to a recovering Europe and Japan. Inflation should hit the Fed’s 2% in 2025 as AI chatbots replace workers at a breakneck rate, cutting costs dramatically as they already have at some firms. The future is happening fast. Buy everything on dips, even bonds.

The stock market couldn’t even manage a 10% correction in April. We got a measly 6.10% instead. It’s all about the economy, stupid. Leftover massive Covid spending and the $280 billion CHIPS Act have created a tidal wave of cash surging through the system with much of it ending up in stocks.

The top eight tech companies (the Magnificent Seven plus Netflix (NFLX)) accounting for 30% of the entire market cap are only getting stronger. The (SPY) has a current price-earnings multiple of 20X with the Big 8 and 17X without them going forward. It’s not cheap but better than a poke in the eye with a sharp stick.

Boring old high-yielding utilities will become a big play as the electric power grid has to triple in size to accommodate the voracious appetites of EV’s and AI. And as we have already seen in California and much of the country, utilities have no reservations about raising prices.

We are back to normal with interest rates, returning to pre-financial crisis levels. Certainly, a stock market at all-time highs is happy with rates. The real concern here is that the Fed DOES cut rates too fast to bail out the loan-dependent half of the economy and the US Treasury as well. That could trigger a melt-up in stocks that would make the last six months pale in comparison and make my own $6,000 target for the (SPX) look ridiculously conservative.

There is also a major generational change in demographics underway. Previous retiring generations, having experienced the Great Depression, hoarded savings and were a drag on the economy. The Baby Boomers are spending like there is no tomorrow because after going through COVID-19, there might not BE a tomorrow. The Boomers have thus turned into the greatest job creators of all time through their spending.

I’ve seen them everywhere in recent weeks in Florida, Cuba, Ecuador, the Galapagos Islands, Panama, and of course, San Francisco where a Big Mac Happy Meal costs $11. What they don’t spend is being passed on to Gen Xers and Millennials, creating a $75 trillion wealth transfer, the largest in history. A lot of this is going into stocks as well. Wonder where all that “meme stock” money is coming from?

And from the “Department of I Told You So”, notice that precious metals were on an absolute tear last week, with gold (GLD) up 4.78% and silver posting a gob-smacking 7.40%. The new demand that I was aware of but had no hard data on finally became public. Solar Panels are Driving Global Silver Demand in an unprecedented fashion. Global investment in solar PV manufacturing more than doubled last year to around $80 billion.

Miners are expanding their operations and ramping up production as prices for the precious metal climb to decade highs, sending gross revenues to the moon. Demand for silver from the makers of solar PV panels, particularly those in China, is forecast to increase by almost 170% by 2030, to roughly 273 million ounces—or about one-fifth of total silver demand.

That’s a lot of silver. Buy (SLV) and (WPM) on dips.

So far in May, we are up +4.14%. My 2024 year-to-date performance is at +18.75%, a new all-time high.The S&P 500 (SPY) is up +10.48%so far in 2024. My trailing one-year return reached +35.79%versus +30.58% for the S&P 500. That brings my 16-year total return to +695.38%.My average annualized return has recovered to +51.83%.

I stopped out of short positions for small losses in (AAPL) and (NVDA) last week. I took profits on my long in (META). I am running my longs in (GLD) and (SLV) and my shorts in (MSFT) and (NVDA) into the Friday, May 17 options expiration. The only new position I added last week was a short in the (TLT).

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

Weekly Jobless Claims Hit a Nine Month High at 233,000, the bitter fruit of persistently high interest rates. New York City public school workers such as bus drivers are allowed to apply for benefits during winter and spring breaks, which tend to boost weekly claims numbers. Claims also picked up in California, Indiana, and Illinois.

Underwater Home Mortgages are Soaring, with the South taking the biggest hit. Roughly one in 37 homes are now considered seriously underwater in the US and that share is much higher across a swath of southern states. Nationally, 2.7% of homes carried loan balances at least 25% more than their market value in the first few months of the year. That’s up from 2.6% in the previous quarter. It’s another cost of high rates.

Online Retail Spending Up 7%, during the January-April period YOY. Cheaper items are seeing the fastest growth. Consumer discretionary spending has been in focus over the past several months, as sticky inflation has forced shoppers in various categories to trade down to more affordable products. It’s another sign of a modest slow, 1.6% growing economy.

Morgan Stanley (MS) Pushes Back Rate Cut Expectations to September. I couldn’t agree more. You see this in the $4 rally in bonds since last week. Sell short (TLT) for the very short term.

TikTok Sues the US Government, claiming its first amendment rights have been violated in a ban imposed on Congress. They will probably win. The national security threat posed by millions of dancing teenagers has never been showed. It’s just another talking point for technology-ignorant politicians egged on by Facebook (META) and other competitors. No one ever said the people in Silicon Valley were nice.

Social Security Trust Fund to Go Broke by 2035, according to US Treasury estimates. I knew they wouldn’t pay me after 55 years of contributions. Medicare is in less bad shape, not running out until 2036, a five-year extension. Retirees, the baby boomers, and exceeding new contributors, the Gen Xers. Expect your taxes to go up to fill the gap.

Berkshire Hathaway Delivers Blockbuster Earnings in Q1, thanks to a $9 billion pop in (AAPL) stock last year. Buffet just cut his massive position by 13% and will cut more. Total 2023 profits came in at a mind-numbing $93 billion. The company — whose divisions include insurance, the BNSF railroad, an expansive power utility, Brooks running shoes, Dairy Queen and See’s delivered a sharp swing from its $22 billion loss in 2022 because of the bear market. Its vast insurance operations that include Geico car insurance and reinsurance reported $5.3 billion in after-tax earnings for 2023, thanks to steep premium increases which we have all felt. Sell (AAPL), buy (BRK/B).

Bond Investors are Making a Killing, with the US Treasury paying out $900 billion in interest in 2023. That’s double the annual cost of the past decade. Remember those coupons? That’s another reason for the Fed to cut rates soon, to lessen this backbreaking burden on the government. After being held hostage by zero-rate policies for almost two decades, US Treasuries are finally reverting to their traditional role in the economy. Bonds are becoming respectable again after a long winter. Buy (TLT) on dips.

China Home Sales Plunge by 47%, as the real estate crisis deepened, indicating that a recovery may be far off. But when it does bounce back, expect all commodities to hit record highs. Buy (FCX) on dips.

Biden Piles on the Foreign Tariffs, announcing new China tariffs aimed at the EV Industry that is currently decimating Europe. Europe is in danger of giving away its edge in cars to the Chinese and a proactive response would ensure American car manufacturers can stand up to the low-priced onslaught.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 13, at 10:30 AM EST, the Consumer Inflation Expectations are announced.

On Tuesday, May 14 at 8:30 AM EST, Producer Price Index for Aprilis released.

On Wednesday, May 15 at 8:30 AM EST, the Consumer Price Index is published

On Thursday, May 16 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, May 17 at 8:30 AM the Monthly Options Expiration takes place at the close.

At 2:00 PM the Baker Hughes Rig Count is printed.

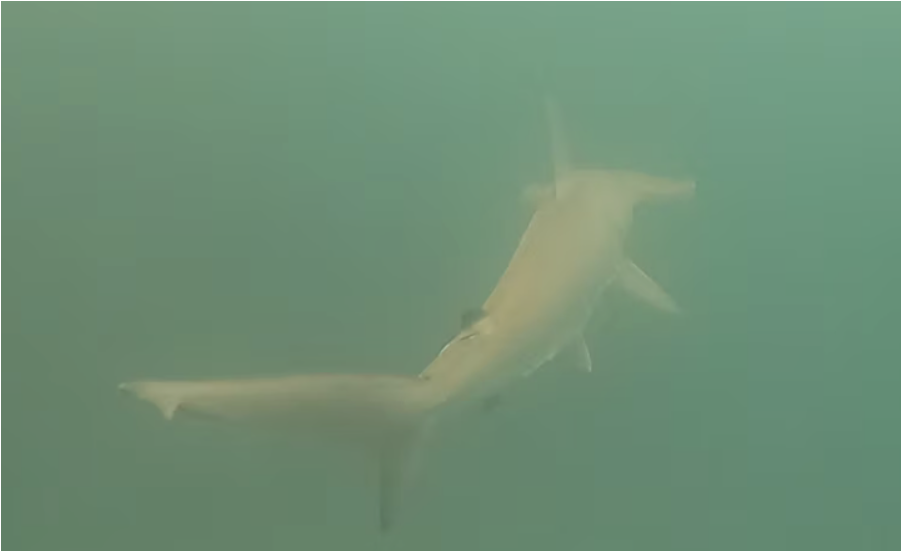

As for me, I will never forget the words from my underwater guide: “Stay where you are and the current will bring the sharks to you.”

Is that something we want, I queried in my fractured Spanish. “Don’t worry”, he answered, “The sharks are vegetarians.” Yes, but did anyone tell the sharks that they were vegetarians?

Sure enough, two six-foot-long hammerhead sharks hungrily swam by me within feet in the green murk, not even pausing to give me the time of day. They swam so close that one almost slapped me in the Face with his tailfin. I guess I wasn’t on the menu that day, not even as a special.

Fortunately, I brought a GoPro underwater video with me and filmed the whole thing. Otherwise, you wouldn’t believe me for a second (click here for the link.)

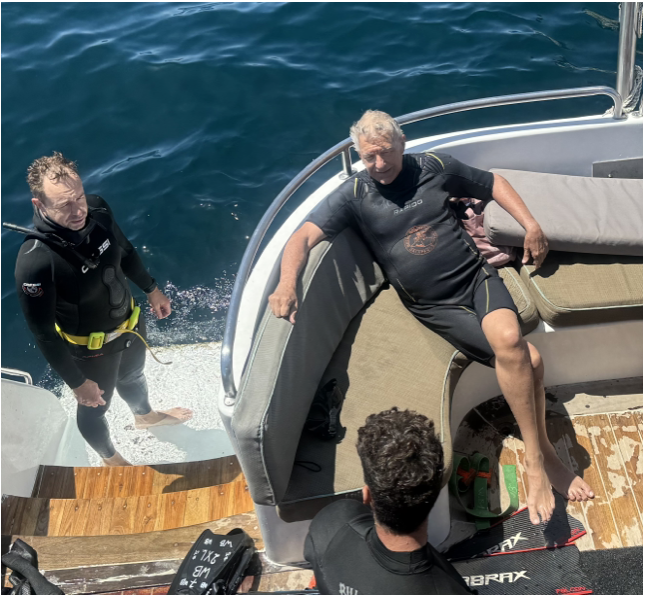

Such was the high point of my week in the Galapagos Islands last week, a remote archipelago of 13 volcanic islands some 600 miles west of Ecuador, 2 degrees South Latitude in the Pacific Ocean. Sitting in my beachfront house in San Cristobal, I worked all morning, knocking out some eight trade alerts on the week, and explored every afternoon.

It was bliss.

You scientists out there will already know the Galapagos Islands as the place where Charles Darwin landed in 1835 on the HMS Beagle and collected the data that led to the Theory of Evolution and the concept of the Survival of the Fittest. (It was all about black Finches, now known as Darwin’s finches, of which I saw hundreds).

Darwin was at first widely ridiculed, as are the creators of all new revolutionary advances. Critics highlighted his close relationship with monkeys. Now it’s required reading for all high school students. While I was there a reproduction of the Beagle sailed in from Holland to celebrate the 200th anniversary of Darwin’s discoveries….11 years early.

The Galapagos Islands are not an easy place to get to. It was a four-hour flight from Miami to Quito in Ecuador, the worlds third highest airport at 9,500 feet. A lot of transients get altitude sickness. Then an hour's flight to Guayaquil on the coast where the Ecuadorian drug trade is run and another hour to San Cristobal. When I tried to visit here in the 1970’s there was only one ship a week and no planes.

Galapagos connected to the outside world just last year when Space X’s Starlink service initiated a 200mb/sec service. With that, I can trade stocks as if I were in downtown Manhattan. This is true for virtually every remote location in the world now, the consequences of which we have yet to imagine. I set up a Starlink in Ukraine last October while under fire and the Russians never were able to jam it.

The Ecuadorian government has gone through great lengths to keep the Galapagos Islands a pristine eco-tourism destination and they have largely succeeded. I counted only one Cessna G5 jet at the airport. Incoming luggage is X-Rayed for foreign fruit and sniffed for drugs by German Shepherds. Residents are limited to a tiny southwestern sliver of San Cristobal island and the rest is a national park.

A friend charitably turned down a $20 million offer from the Four Seasons international hotel chain for his 120 acres of land there. There are not a lot of places in the world left where you can walk out of your front door to a deserted beach unscarred by footprints. Yet, it offers Ecuadorian prices, about one-third of those found in the US.

I think you should visit there.

HMS Beagle, kind of

55 Years of Trading and Finally my Own Beach!

Let the Current Bring the Sharks to You

Chillin with the Crew

My New Office

The View from Home

My New Neighbors

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/05/John-thomas-beach.png700820april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-05-13 09:02:232024-05-13 11:52:14The Market Outlook for the Week Ahead or The Great American Golden Age has Only Just begun and Swimming with the Sharks

Occasionally, I get a call from Concierge members asking what to do when their short positions options were assigned or called away. The answer was very simple: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position instantly.

We have the good fortune to have FOUR spreads that are deep in the money going into the May 17 option expiration in 8 days. They include:

Risk On

(GLD) 5/$200-$205 call spread 10.00%

(SLV) 5/$21-$23 call spread 10.00%

Risk Off

(NVDA) 5/$980-$990 put spread -10.00%

(MSFT) 5/$430-$440 put spread -10.00%

Total Net Position 0.00%

Total Aggregate Position 40.00%

In the run-up to every options expiration, which is the third Friday of every month, there is a possibility that any short options positions you have may get assigned or called away.

Most of you have short-option positions, although you may not realize it. For when you buy an in-the-money vertical option debit spread, it contains two elements: a long option and a short option.

The short options can get “assigned,” or “called away” at any time, as it is owned by a third party, the one you initially sold the put option to when you initiated the position.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it correctly.

Let’s say you get an email from your broker telling you that your call options have been assigned away. I’ll use the example of the in-the-money SPDR Gold Shares SPDR (GLD) May $200-$205 vertical BULL CALL debit spread, which you bought at $4.55 or best.

For what the broker had done in effect is allow you to get out of your call spread position at the maximum profit point 8 trading days before the May 17 expiration date. In other words, what you bought for $4.55 on April 30 is now $5.00!

All have to do is call your broker and instruct them to exercise your long position in your (GLD) May 200 calls to close out your short position in the (GLD) May $205 calls.

This is a perfectly hedged position, with both options having the same expiration date, and the same number of contracts in the same stock, so there is no risk. The name, number of shares, and number of contracts are all identical, so you have no net exposure at all.

Calls are a right to buy shares at a fixed price before a fixed date, and one option contract is exercisable into 100 shares.

To say it another way, you bought the (GLD) at $200 and sold it at $205, paid $4.55 for the right to do so for 13 days, so your profit is $0.45 cents, or ($0.45 X 100 shares X 25 contracts) = $1,125. Not bad for a 13-day defined limited-risk play.

Sounds like a good trade to me.

Callaways most often happen in the run-up to a dividend payout. If you can collect a full monthly or quarterly dividend the day before the stock registration dates by calling away someone’s short option position, why not? If fact, a whole industry of this kind of strategies has arisen in recent years in response to the enormous growth of the options market.

(GLD) and most tech stocks don’t pay dividends so callaways are rare.

Weird stuff like this happens in the run-up to options expirations like we have coming.

A call owner may need to buy a long (GLD) position after the close, and exercising his long May 205 call is the only way to execute it.

Adequate shares may not be available in the market, or maybe a limit order didn’t get done by the market close.

There are thousands of algorithms out there that may arrive at some twisted logic that the calls need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, options even get exercised by accident. There are still a few humans left in this market to make mistakes.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it. They’ll tell you to take delivery of your long stock and then post an additional margin to cover the risk.

Or they will tell you to sell your remaining long option position at whatever price you can get, wiping out most, if not all of your great profit. This generates the maximum commission for your broker.

Either that, or you can just sell your shares on the following Monday and take on a ton of risk over the weekend. This generates a oodles of commission for the brokers but impoverishes you.

There may not even be an evil motive behind the bad advice. Brokers are not investing a lot in training staff these days. It doesn’t pay. In fact, I think I’m the last one they did train 50 years ago.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many legal ways to steal money that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Calling All Options!

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/Call-Options.png345522april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-05-07 09:02:002024-05-07 13:56:59A Note on Assigned Options, or Options Called Away

At the once-per-year shareholder meeting for Berkshire Hathaway (BRK/A) in Omaha, Nebraska, the shindig has become a caricature of itself.

A company that does so well, but the leader has self-proclaimed to understand nothing about technology.

It was fascinating to see the Oracle of Omaha Warren Buffett dabble in the cooler talk that is talk about artificial intelligence.

Ironically enough, his pep talk about AI was littered with negatives about the consequences of AI.

Warren Buffett's warning about AI’s potential harm has everything to do with his conservative risk tolerance to not beeline straight to the front of the most modern developments in the tech industry.

He’s late on most stocks but he’s right on them in the end.

It wasn’t too far back when Buffett only would invest in a company as complicated as Coca-Cola, because he famously stated that he doesn’t invest in companies that he doesn’t understand.

Insurance also made Buffett a killing pouring capital into companies like Aflac.

He finally came around to Apple which for better or worse is known as the iPhone company.

His risk tolerance of tech increasing to the almighty smartphone was quite a jump for Buffett that took many years, so don’t expect another leap of faith anytime soon.

In fact, Buffett claiming he doesn’t understand AI too well means there is a lot of capital sitting on the sidelines waiting to enter once they finally do “understand.”

I should also just note the general stockpile of money that has been waiting on the sideline since the Covid-era is enormous.

Any meaningful dip in any meaningful tech company will be met by a torrent of new buying demand.

That’s exactly what happens when the number of great tech companies can be counted on 2 hands.

Almost like what is happening with American restaurants – it’s not that American restaurants are going through a generational renaissance, no, they are packed because so many small restaurants closed after COVID.

Tech is experiencing the same playbook with investor money.

The past 7-12 years have seen the spurring on competition squelched, and the tech industry has never been closer to a full-blown monopoly in some sub-sectors.

Once the bulls get back in control, we are off to the races again, because a few companies move markets now.

That’s what I believe we are seeing in the short-term with the US 10-year inching up only for Central Bank Fed Chair Jerome Powell to deliver us a monumental dovish speech to the sticky inflation we are seeing in numbers now.

Buffett chose to talk about the darker side of AI and the potential for scamming people.

He said that scamming using AI will become a “growth industry of all time.”

Buffett pointed to the technology’s ability to reproduce realistic and misleading content in an effort to send money to bad actors.

Just because we don’t like it, we cannot write it off or afford it as investors.

Readers must deal with AI and the manifestations of it.

One of the big side effects is that it accelerates the winner-takes-all dynamics of tech.

If I were a newbie investor, Super Micro Computers (SMCI) would be on the radar as a powerful growth stock with bountiful potential and exposure to AI.

More tech companies will fail, and they will fail faster, without a trace of even existing sometimes.

It also puts extreme pressure on tech management to implement AI, lose funding, or lose the momentum the business model.

It almost makes tech management over-reliant on AI to fix any and every mess.

The reality is that there will be a lot of losers from AI and punishes companies that never figure out AI.

It is best to identify them before the stock goes to 0.

I don’t necessarily share the same dark outlook as Buffett and I commend him for doing so well on his performance, but when it comes to technology stocks, he shows up late, but it is better than never showing up.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-05-06 14:02:012024-05-06 20:43:12Buffett Chimes In On AI

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.