Mad Hedge Technology Letter

April 15, 2024

Fiat Lux

Featured Trade:

(APPLE RUNNING OUT OF TIME)

(AAPL)

Mad Hedge Technology Letter

April 15, 2024

Fiat Lux

Featured Trade:

(APPLE RUNNING OUT OF TIME)

(AAPL)

At some point, Apple (AAPL) might realize that they won’t be able to find that “next big thing.”

That would be a death sentence.

I’ve been warning Apple shareholders for years that they are headed into a growth winter if they can’t find the next big thing to replace the iPhone.

The consensus was that Apple had time to figure it out.

When I say time, Apple management was quite relaxed about it because the iPhone had been making so much money for years.

Management didn’t think they had much to worry about for 5 to 7 years.

But that was then and things have changed.

Tech has advanced with lightning speed and has left Apple in the dust.

The iPhone numbers keep getting worse and Apple is still scratching their head.

The insurmountable lead they had in smartphones should have been used as a springboard into something even grander and more impressive.

Yet here we are over a decade later with Apple barely moving the needle such as changing the color of the lock screen and trying to pass over other minuscule changes as real upgrades.

Other tech behemoths migrating into artificial intelligence have made Apple look even more outdated in 2024.

Reports show Apple has been exploring a mobile robot that can follow users around their homes.

The iPhone company also has developed an advanced tabletop home device that uses robotics to move a display around.

It shelved an electric vehicle project in February, and a push into mixed-reality goggles is expected to take years to become a major moneymaker.

With robotics, Apple could gain a bigger foothold in consumers’ homes and capitalize on advances in artificial intelligence. But it’s not yet clear what approach it might take. Though the robotic smart display is much further along than the mobile bot, it has been added and removed from the company’s product roadmap over the years.

The iPhone accounted for 52% of the company’s $383.3 billion in sales last year leading to many calling the company the iPhone company.

A car had the potential to add hundreds of billions of dollars to Apple’s revenue.

If the work advances, Apple wouldn’t be the first tech giant to develop a home robot. Amazon.com Inc. introduced a model called Astro in 2021 that currently costs $1,600.

A silver lining to Apple’s failed car endeavor is that it provided the underpinnings for other initiatives. The neural engine — the company’s AI chip inside of iPhones and Macs — was originally developed for the car. The project also laid the groundwork for the Vision Pro because Apple investigated the use of virtual reality while driving.

Apple stock is slightly down from the end of 2021.

That’s disheartening news for many shareholders because this stock was the perennial gem that overdelivered on every metric including the share price which is what matters most.

Apple was once the cornerstone of the stock market, and that title has disappeared unceremoniously with its smartphone lead.

With earnings fast approaching, I expect a lackluster report from Apple at best.

Any rallying will be done on less bad news than first expected and many companies already know that is a game you cannot win.

Even worse, the price to find the “next big thing” has multiplied significantly from 10 years ago with the cost of labor, supply parts, and the regulatory mood has soured.

The longer this goes on, the more Apple will be forced to deliver a royal flush when least expected.

The probability of Apple taking back the mantle as the forerunner of tech is dissipating by the day, and I would avoid the stock in the short term.

There is a reason why the stock has slightly down over the past 365 days.

If the stock pops on the earnings, I would be inclined to sell the rally.

Mad Hedge Technology Letter

March 27, 2024

Fiat Lux

Featured Trade:

(TAIWAN IS ON THE MAP)

(AAPL), (TSM)

I know it’s not the sexiest choice but there is a chip company in Taiwan that readers need to look at.

This company has investments all over the world and is the leader in what they do.

They are also involved in AI which lately has been the ticket to riches.

Taiwan Semiconductor Manufacturing Company (TSM) may not seem like a glamorous AI stock, but it's as critical to the AI future.

To understand TSMC's role in AI, you need to understand how we get to end consumer-facing products like ChatGPT, Bard, and other generative AI applications.

For AI to be effective, it must be trained using lots of data -- quantities that must be stored in specialized data centers.

Data centers rely on graphic processing units (GPUs), which are essentially the brains of AI computing systems.

TSMC and the semiconductors it manufactures for its client companies are crucial in this process. These GPUs rely heavily on TSMC's best-in-class manufacturing processes.

This AI knock-on effect hasn't impacted TSMC's financials yet, but management said they expect sales of its AI-related semiconductors to grow at a compound annual rate of 50% for at least the next few years.

By 2027, AI-related semiconductors are expected to be responsible for a large part of the company's revenue.

TSMC will absolutely be additive to the AI ecosystem.

Let’s talk about their products.

TSMC's 3nm fabrication process accounted for 15% of the company's revenue in 2023.

Only one of TSMC's customers used it at the time:

Apple (AAPL).

The three-nanometer product is where it’s at.

Wasn’t it just a year or 2 ago we were at 7 nanometers?

As more customers adopt the manufacturing process, 3nm process nodes will account for a considerably larger share of TSMC's revenue.

This year TSMC's N3-series nodes — including N3B and N3E — will account for over 20% of the foundry's revenue in 2024.

Apple currently exclusively uses TSMC's N3B to make its A17 Pro system-on-chip (SoC) for smartphones, as well as the M3-series processors for iMac desktops and MacBook laptops.

AMD is preparing to launch its new Zen 5-based processors made on 3nm- and 4nm-class process technologies later this year.

Apple's new iPhone 16 series will be equipped with the A18-series processor, and the upcoming M4-series processors for Mac PCs will also be produced using TSMC's 3nm technology.

This marks the first time Intel has entrusted TSMC with the full range of chips for its mainstream consumer platform, the report notes.

This collaboration highlights TSMC's expanding role in serving Intel, which also happens to be the company's rival in the foundry market.

With three major customers using TSMC's 3nm family of process technologies, this company needs to be on readers’ radar.

More companies are expected to adopt TSMC's N3 nodes in 2025, including performance-enhanced N3P, and the report suggests 3nm will account for over 30% of TSMC earnings in 2025.

It’s easy to see with the mushrooming of business for TSMC, how they are a highly sought-after stock.

It also explains why the stock has been on a tear.

It was only just last May they were trading at $82 per share and fast forward to today at the stock sits at $136 per share.

Holding this stock long term has borne fruit and every big should be bought.

They will continue to be the best at what they do.

Mad Hedge Technology Letter

March 25, 2024

Fiat Lux

Featured Trade:

(REGULATIONS REGULATE TECH)

(AAPL), (GOOGL), (META)

I’m not saying the time is up for big tech.

The Magnificent 7 are still by and far great companies who print money.

They dominate in a way that was unfathomable just a generation ago.

Trillion-dollar companies are now commonplace in tech and we have pushed into valuations of over 2 and pushing towards $3 trillion.

Success like this easily could make them easy targets and that is what has become of them in Europe as Apple (AAPL), Google (GOOGL), and Meta (META) are in the firing line under the sweeping new Digital Markets Act tech legislation.

Apple has already been slapped on the wrist quite hard with a $2 billion fee after the European Commission said it found that Apple had applied restrictions on app developers that prevented them from informing iOS users about alternative and cheaper music subscription services available outside of the app.

In a third inquiry, the commission said it is investigating whether Apple has complied with its DMA obligations to ensure that users can easily uninstall apps on iOS and change default settings. The probe also focuses on whether Apple is actively prompting users with choices to allow them to change default services on iOS, such as for the web browser or search engine.

The fourth probe targets Alphabet, as the European Commission looks into whether the firm’s display of Google search results to choosing its own products over other services.

The fifth and final investigation focuses on Meta and its so-called pay and consent model. Last year, Meta introduced an ad-free subscription model for Facebook and Instagram in Europe. The commission is looking into whether offering the subscription model without ads or making users consent to terms and conditions for the free service is in violation of the DMA.

If any company is found to have infringed the DMA, the commission can impose fines of up to 10% of the tech firms’ total worldwide turnover. These penalties can increase to 20% in case of repeated infringement.

Preferring one’s own product from companies like Apple, Amazon, and Google is not a shocking phenomenon. Business can be a dirty game and self-selecting ones products because they own the platform they are sold on is almost common knowledge to the average consumers.

Organizational bodies like the European Commission have an incentive to fine American tech companies that do business in Europe.

Europe has no alternative apps and aren’t competitive in the tech space.

The desperate reach of European bureaucracy has decided to just steal the money in the form of tech fines instead.

One big takeaway that sticks out like a sore thumb is the clear trend to the low-hanging fruit being plucked.

The incremental dollar will be harder to earn for big tech as regulatory commissions around the world zone in on their anti-competitive practices.

I doubt that fines will get so big to the point that these tech firms will go bankrupt, but this could set the stage for a slew of earnings misses which could knock down the share prices.

I still believe these stocks are buys, but only after they are beaten down and repriced.

I wouldn’t go chasing here with regulatory issues rearing its ugly head and revenue forecasts disappointing.

If I had to choose one to avoid then it would be Apple.

Global Market Comments

March 25, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BEST WEEK OF THE YEAR),

(PANW), (NVDA), (LNG), (UNG), (FCX), (TLT), (XOM), (AAPL), (GOOG), (MSTR), (BA), (FXY)

You need to have a sense of humor and a strong dose of humility to work in this market. After predicting last week that the market would NOT crash but grind sideways, it then posted the next week of the year. Stocks are actually accelerating their move to the upside.

Of course, we got a big assist from Fed Governor Jay Powell who practically wrote in his own blood a promise that interest rates would be cut at least three times by the end of the year. That is quite a gesture, and all risk assets loved it, even the ones that have been asleep for a year, like gold (GLD) and silver (SLV).

Miraculously, this does happen and there has been a big one over the last two years that nobody knows about.

Cheniere Energy (LNG) shipped 640 tankers full of natural gas (UNG) to Europe last year and 630 in 2022. One tanker provides enough gas to heat one million homes for a month. You can do the math. In total, it has sent out 3,400 tankers since 2016, mostly to China.

When Russia invaded Ukraine in 2022, Europe was totally dependent on Vladimir Putin for gas. Any doubt about the Russian supply was ended when the Nordstream undersea pipeline was mysteriously blown up. A total cut-off would have been an economic disaster and caused the collapse of NATO.

Two years ago, it was believed that even if we could get the gas to Europe, there were no facilities to liquefy natural gas as it is shipped back into natural gas. Then 16 floating de-liquefaction plants showed up out of nowhere.

Natural gas demand has been soaring in the US as well. Over the past 20 years, coal has dropped from generating 50% of the US electric power supply to only 19% (the unused American share of the coal was sold to China). That has eliminated 500 million tons of carbon dioxide from entering the atmosphere.

If you noticed that the skies over American cities are getting clearer, this is the reason.

Much has been made over Biden’s “pause” of permitting for new natural gas facilities. The reality is that it will take four years to build the 16 new gas export facilities that have already been approved. By then, we’ll have a new president. All Biden did was throw a bone at the environmental wing of his party. Such are the ways of Washington.

By the way, the Republican Party now has an environmental wing too. Who knew? It’s all proof that if you live long enough, you see everything.

One of the reasons I have been in love with cybersecurity stocks like Palo Alto Networks (PANW) for the past decade is that hacking is the ultimate growth industry. It never goes out of style, is recession-proof, and is growing at an exponential rate.

It is also getting more sophisticated. The big hackers are franchising their business models, inviting in criminals with minimal computer knowledge, vastly increasing their numbers. They are attacking small vendors to large companies to get access to the big ones. They are also picking targets too poor to afford the big cybersecurity companies. The City of Oakland is a classic example, which was prevented from paying its teachers for six months. And now they have AI.

Spending on cybersecurity is expected to grow from $188 billion in 2023 to $215 billion this year, a gain of 14.36%. The number of data breaches has rocketed by 78% over the past two years. Buy (PANW) on dips, which we are seeing right now.

“We’re going to need a bigger GPU” to borrow a famous line from Stephen Spielberg’s blockbuster Jaws.

If you want a peak at the future, both of our own and NVIDIA stock, check out the company’s latest entry into the chip wars, the $50,000 Blackwell GPU, available in a few months. In layman’s terms, it offers four times the computing ability but requires only one-quarter of the electric power, which is increasingly becoming an AI issue. It also uses deep learning to write its own software.

The chip was introduced by CEO Jensen Huang at the Developers conference in San Jose, which I attended in a venue normally occupied by rock stars. Huang started the conference by warning he was not there to sing. But perform he did, accompanied by a group of dancing robots powered by AI.

And while NVIDIA’s sales have tripled over the past year, you ain’t seen anything yet. When I recommended (NVDA) for the millionth time at $400 a share last October, my long-term target was $1,000. It recently hit $975, now stands at $943, and shows no sign of abating. NVIDIA could well keep powering on until the actual release of the Blackwell chip.

As in Jaws, I sense a feeding frenzy coming and (NVDA) shorts are the bait.

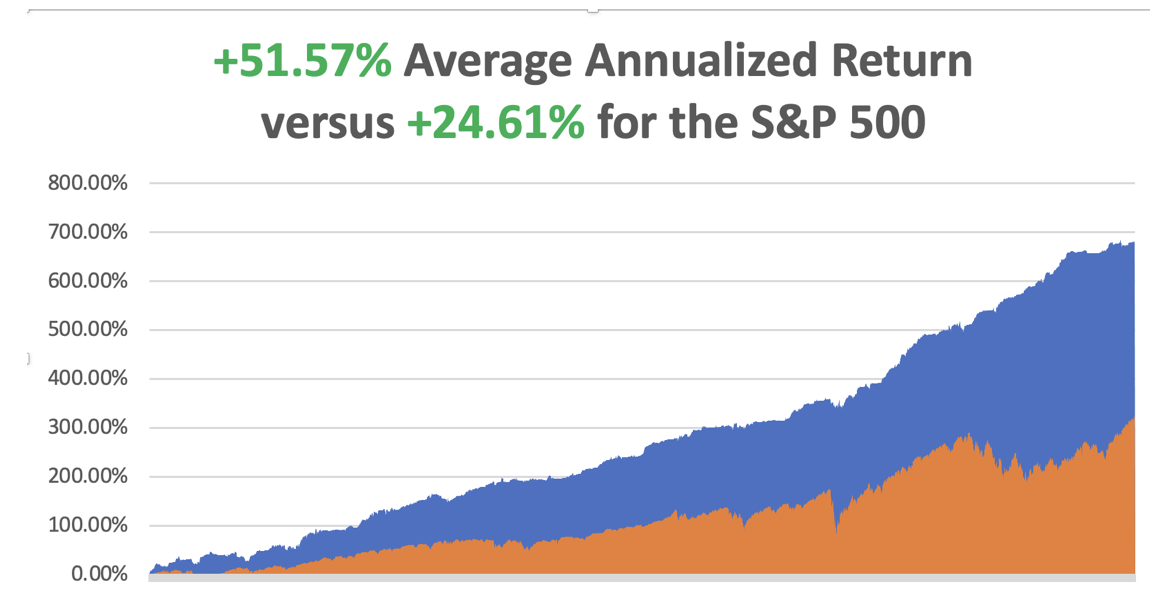

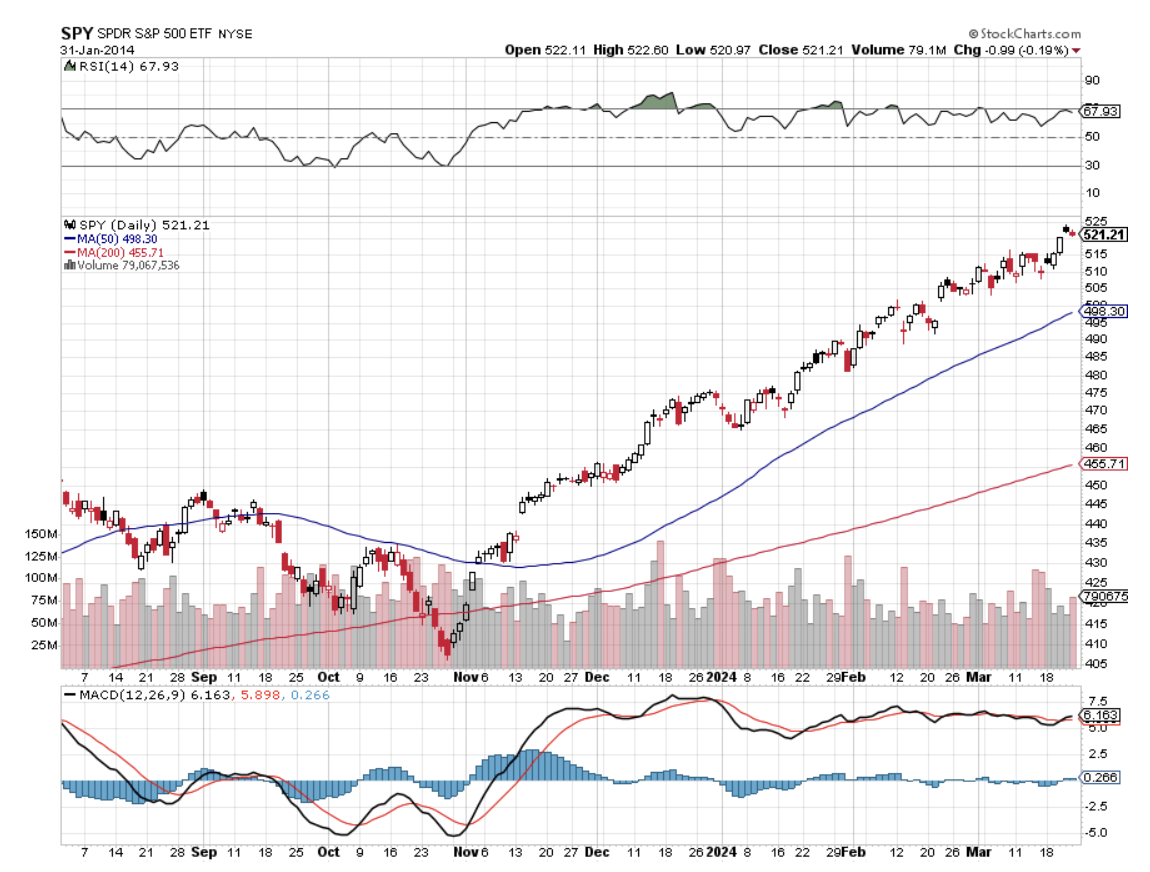

In February we closed up +7.42%. So far in March, we are up +3.53%. My 2024 year-to-date performance is at +6.67%. The S&P 500 (SPY) is up +9.22% so far in 2024. My trailing one-year return reached +56.98% versus +52% for the S&P 500.

That brings my 16-year total return to +683.30%. My average annualized return has recovered to +51.57%.

Some 63 of my 70 round trips were profitable in 2023. Some 11 of 19 trades have been profitable so far in 2024.

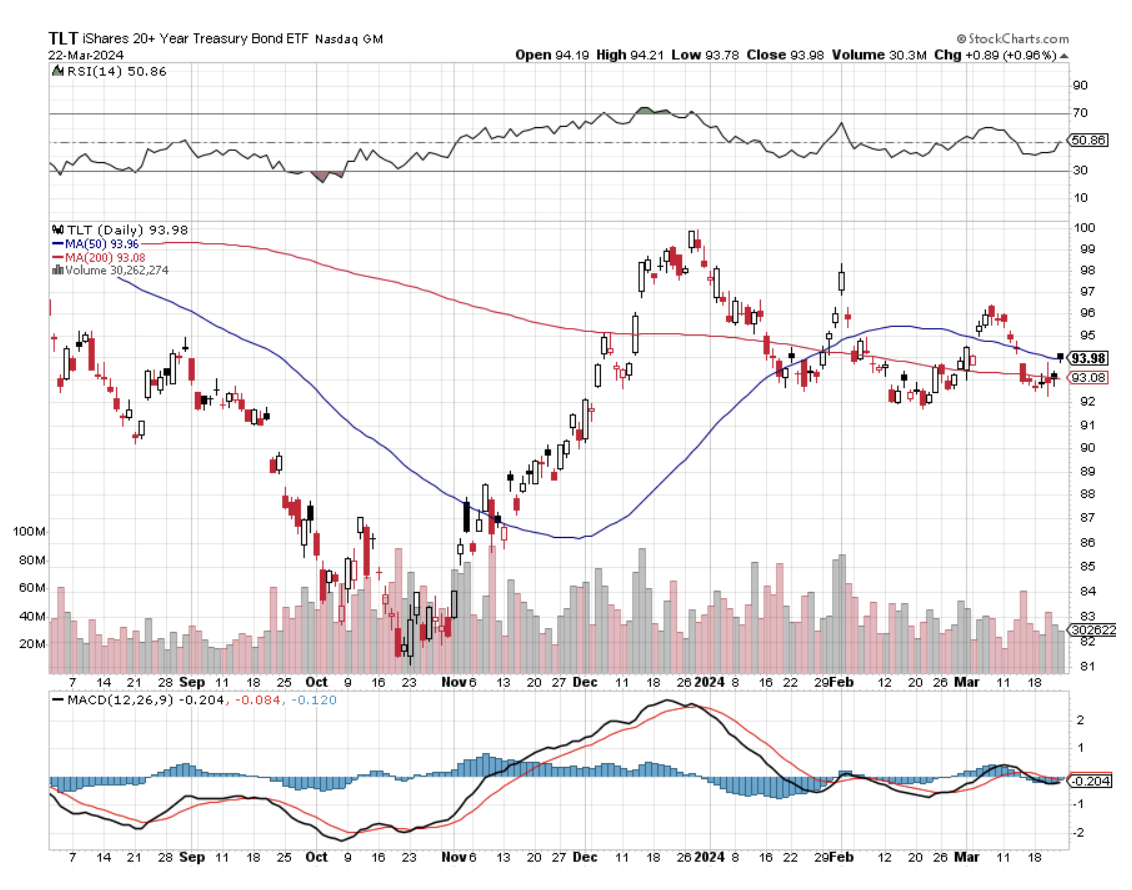

I miniated no new longs last week, content to let my existing longs run in Freeport McMoRan (FCX), bonds (TLT), and ExxonMobile (XOM). I am 70% in cash given the elevated state of the market and am looking for new commodity and energy plays to pile into.

Fed Chair Jay Powell Promises Three Interest Rate Cuts of 25 basis points each, at his press conference on Wednesday. Powell said he did not see "cracks" in the labor market, which he described as "in good shape," noting that "the extreme imbalances that we saw in the early parts of the pandemic recovery have mostly been resolved." These are very pro-risk statements. Buy the dips in everything.

Fed to Dial Back Quantitative Tightening, or QT from the current $120 billion a month. It’s a huge plus for risk assets and explains why the most liquidity-driven ones like gold and silver had such a great day. Buy (GLD) and (SLV) on dips.

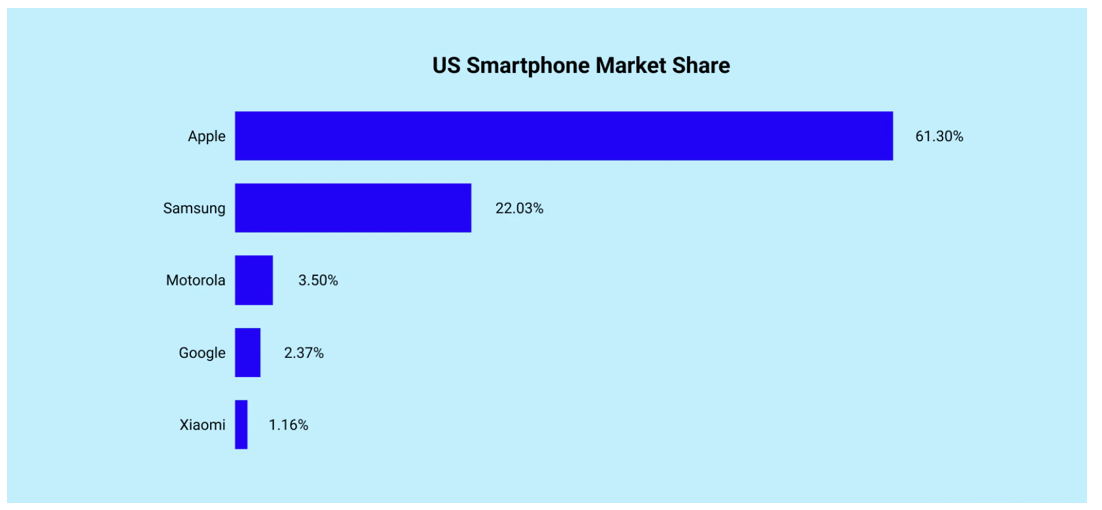

The Dept of Justice Goes After Apple on Antitrust, on its 61.3% share of the US smartphone market. It accused the iPhone maker of blocking rivals from accessing hardware and software features on its popular devices. Google’s (GOOG) Android actually has a bigger global market share at 70.3% with Apple at only 24%. This is another waste of time that will last ten years and go nowhere.

Bank of Japan to Cut Interest Rates as Early as April, bringing to an end a 34-year stimulus program that was a dismal failure. The Japanese yen (FXY) should rocket, but Japanese stocks not so much.

MicroStrategy (MSTR) Dives 18%, the largest owner of Bitcoin, on a crypto correction. MicroStrategy is the largest corporate owner of Bitcoin. (MSTR) just completed a massive borrowing to buy more crypto at the top. After SEC approval of ETFs and the imminent halving, what is left to drive crypto? Avoid (MSTR) which was blindsided by the last 90% crypto correction.

Existing Homes Sales Soar 9.7% in February to 4.38 million units, on a seasonally adjusted annualized basis. Inventory rose 5.9% year over year to 1.07 million homes for sale at the end of February. That represents a still low 2.9-month supply at the current sales pace. Higher demand continued to push the median price higher, up 5.7% from the year before to $384,500.

Home Prices Have Risen by 2.4 Times the Inflation Rate Since 1960. The cost of a typical house in the U.S. is nearly half a million dollars: the median price for a home in the U.S. is $412,778, according to Redfin data. That’s what successful demographic tailwinds leading to a chronic housing shortage get you.

Boeing is Leasing 36 Airbuses, to meet its own unfilled orders caused by production delays. Another panel fell off an airborne plane last week in Medford, OR. Looking for missing parts has become a regular part of every Boeing landing. This is an act of desperation. Avoid (BA)

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 25, at 7:00 AM EDT, the US Building Permits are announced.

On Tuesday, March 26 at 8:30 AM, S&P Case Shiller for February is released.

On Wednesday, March 27 at 11:00 AM, the MBA Mortgage Data is published

On Thursday, March 28 at 8:30 AM, the Weekly Jobless Claims are announced. The final read of the Q2 US GDP is also out.

On Friday, March 29 at 2:00 PM, Personal Income and Spending is out. The Baker Hughes Rig Count is printed.

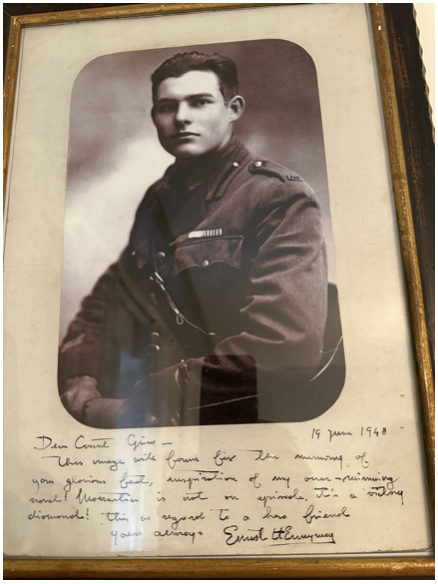

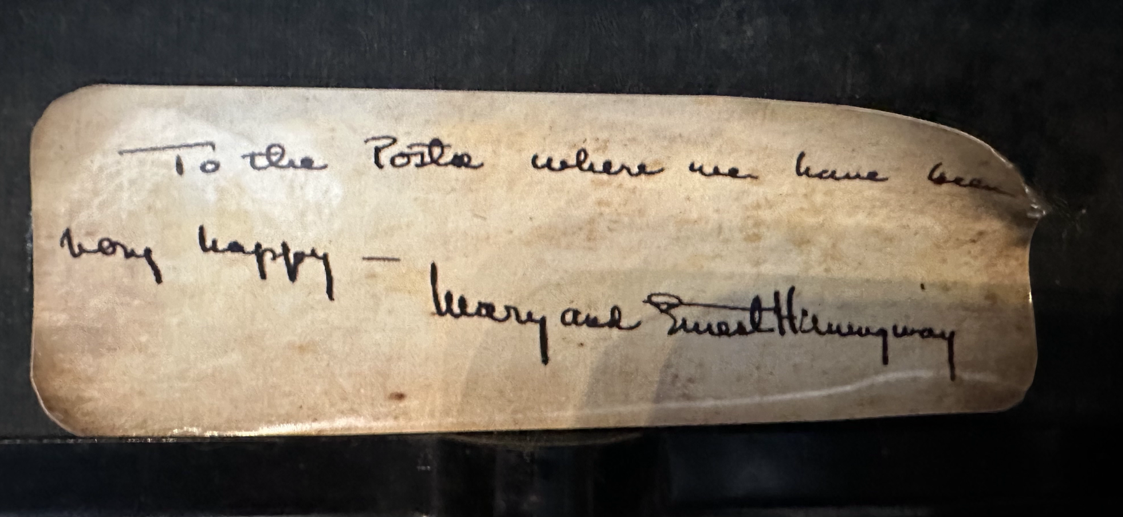

As for me, as I am about to take off for Cuba to visit Finca Vigia (Lookout Farm), the home of Earnest Hemingway and Martha Gellhorn I thought I’d review my long history with this storied family. This is where he finished For Whom the Bells Toll, his epic novel about the Spanish Civil War.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there going back over 100 years.

Since I read Hemingway’s books in my mid-teens, I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete work.

I visited his homes in Key West and Ketchum Idaho. In 2023, he stayed at his Hotel Poste room in Cortina, Italy where he lived for five months during the 1950s. His Cuban residence was high on my list, now that Castro is gone.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Ernest shot a German colonel in the face at point-blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping-off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was still being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish this newsletter.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are now glued to the tables.

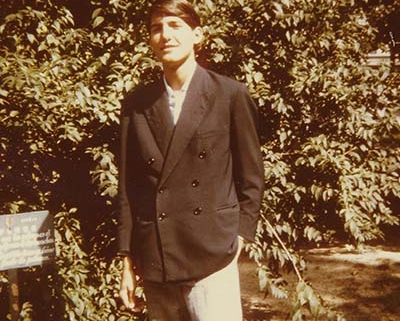

Hemingway in 1917

At Work on Hemingway’s Typewriter

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 20, 2024

Fiat Lux

Featured Trade:

(WELCOME TO THE DEFLATIONARY CENTURY),

(TLT), (TBT), (AAPL), (MSFT)

Ignore the lessons of history, and the cost to your portfolio will be great. Especially if you are a bond trader!

Meet deflation, upfront and ugly.

If you look at a chart for data from the United States consumer prices are rising at an annual 3.2% rate. The long-term average is 3.0%.

This is above the Federal Reserve’s own 2.0% annual inflation target, with most of the recent gains coming from housing costs.

We are not just having a deflationary year or decade. We may be having a deflationary century.

If so, it will not be the first one.

The 19th century saw continuously falling prices as well. Read the financial history of the United States, and it is beset with continuous stock market crashes, economic crises, and liquidity shortages.

The union movement sprung largely from the need to put a break on falling wages created by perennial labor oversupply and sub-living wages.

Enjoy riding the New York subway? Workers paid 10 cents an hour built it 125 years ago. It couldn’t be constructed today, as other more modern cities have discovered. The cost would be wildly prohibitive. Look no further than the California Bullet Train, now expected to cost $100 billion. A second transbay tube in San Francisco will cost $29 billion.

The causes of the 19th-century price collapse were easy to discern. A technology boom sparked an industrial revolution that reduced the labor content of end products by ten to a hundredfold.

Instead of employing 100 women for a day to make 100 spools of thread, a single man operating a machine could do the job in an hour.

The dramatic productivity gains swept through the developing economies like a hurricane. The jump from steam to electric power during the last quarter of the century took manufacturing gains a quantum leap forward.

If any of this sounds familiar, it is because we are now seeing a repeat of the exact same impact of accelerating technology. Machines and software are replacing human workers faster than their ability to retrain for new professions. If you want to order a Big Mac at McDonald’s these days, you need a PhD in Computer Science from MIT. The new stores have no humans to take orders.

This is why there has been no net gain in middle-class wages for the past 40 years. That is until the pandemic hit which created labor shortages that are still working their way out. It is the cause of the structurally high U-6 “discouraged workers” employment rate, as well as the millions of millennials still living in their parent’s basements.

To the above add the huge advances now being made in healthcare, biotechnology, genetic engineering, DNA-based computing, and big data solutions to problems. Did anyone say “AI”?

If all the major diseases in the world were wiped out, a probability within 10 years, how many healthcare jobs would that destroy?

Probably tens of millions.

So the deflation that we have been suffering in recent years isn’t likely to end any time soon. In fact, it is just getting started.

Why am I interested in this issue? Of course, I always enjoy analyzing and predicting the far future, using the unfolding of the last half-century as my guide. Then I have to live long enough to see if I’m right.

I did nail the rise of eight-track tapes over six-track ones, the victory of VHS over Betamax, the ascendance of Microsoft (MSFT) operating systems over OS2, and then the conquest of Apple (AAPL) over Motorola. So, I have a pretty good track record on this front.

For bond traders especially, there are far-reaching consequences of a deflationary century. It means that there will be no bond market crash, as many are predicting, just a slow grind up in long-term bond prices instead.

Amazingly, the top in rates in this cycle only reaches the bottom of past cycles at 5.49% for ten-year Treasury bonds (TLT), (TBT).

The soonest that we could possibly see real wage rises will be when a generational demographic labor shortage kicks in during the late 2020s.

I say this not as a casual observer, but as a trader who is constantly active in an entire range of debt instruments.

I just thought you’d like to know.

Hey, Have You Heard About John Deere?