Tech investors want nothing to do with an aggressive Federal Reserve, but that’s what we have.

I don’t choose this and neither do many others out there.

We have been spoilt in a world with low inflation, global peace, low energy, and high liquidity which was the perfect scenario for tech stocks.

The reverse has happened almost overnight and now it’s that much harder to earn your crust of bread in the tech world.

Gone are the days of buying Facebook for peanuts then going for a sauna and a nap. It’s not that easy right now.

Tech stocks don’t go up in a straight line anymore – there will be many zigs and zags along the way moving forward.

Tech stocks aren’t immune to these exogenous stocks and as anointed growth companies, they inherently need to borrow capital and grow more than the cost of it.

That endeavor is stretched to the limit as bond yield explodes to the upside with this latest rate rise.

Raising interest rates by 0.75% for the third consecutive time this afternoon was the consensus, but in fact, there was a 25% chance of a full 1% rate rise. We avoided that bullet.

Tech stock doves were hoping US Federal Reserve Governor Jerome Powell would save them, by initiating a pivot to save the stock market, but no do this time around.

It underscores that Powell is adamant about continuing this inflation battle even if I do believe it’s too little too late.

The central bank’s new benchmark borrowing rate is now between 3.0% to 3.25%, up from the current range of 2.25% to 2.5%. This would bring the fed funds rate to its highest level since 2008.

Tech stock reacts most sensitively to the change in Fed Funds rates which is why we have seen CEO and Founder of Meta (META) or Facebook Mark Zuckerberg lose $71 billion of his net wealth this year.

Not only is the macroenvironment squarely against him, but his flagship product Facebook is losing steam, and his new product the Metaverse has garnered tepid reviews from outsiders.

How long does the Fed intend to increase rates?

The updated consensus for the Fed Funds Rate shows it at 4-4.25% by the end of 2022, another hike to 4.25-4.5% at end of 2023, and one more cut in 2024 and two more in 2025.

The answer is quite a while longer.

In the meantime, this will initiate a “reverse wealth effect” and tech stocks are the biggest losers, and the US dollar is an unmitigated winner.

Delaying lower Fed Funds rates means delaying the reversal in tech stocks which need lower rates to explode higher and without it, they are quite ordinary.

Signaling higher rates for longer is designed to tame inflation, but there are so many unintended consequences for US tech stocks.

The most important themes to be concerned about are revenue and financing.

The .75% increase in rates will mean that tech stocks will produce lower annual revenue because financing costs will be higher.

This is already at a time when general costs have exploded higher such as an uncontrollable wage spiral, supply chain bottlenecks, health care costs, transportation costs, and energy costs.

It’s a great deal harder to keep the numbers down enough to profit which basically means gross margins will compress further from today.

Tech stocks will come back because they always do. They are the profit engine of corporate America, and that will never change.

I see great tech companies like Apple (AAPL) installing the framework so they can maximize on the next move up when the bull market reignites.

They are doing this by moving iPhone production to India and other tablet production to Vietnam to get out of lockdown China.

Now is the time to reset before tech bounces back and it’s painful to see tech get slaughtered, but this is a necessary evil after a wonderful bull run from 2012 to November 2021.

US FED GOVERNOR GIVES NO LOVE TO TECH STOCKS

https://www.madhedgefundtrader.com/wp-content/uploads/2022/09/jerome-powel-e1663792363561.png240480Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-21 16:02:552022-09-29 22:35:33Potential Tech Reversal Pushed Back

That is what has been my magic formula for making money over the past 50 years.

But what happens if you get nothing?

What happens if you are stuck in a big fat middle of a range? That seems to be the case now that the market is nailed to the (SPY) 4,000 level, which it turns out is exactly the middle of a four-month trading range.

The market fought the Fed for two months from June and won. It has lost since Jackson Hole. The market has only seen that degree of whipsaw four times since 1950.

It now appears that it is front running a very weak number for the Consumer Price Index on September 13. After that, we get a 75-basis point rate rise on September 20. Good cop first, then bad cop.

That leaves me twiddling my thumbs along with everyone else, waiting for the market to throw up on its shoes. We were almost getting there last week when the Volatility Index (VIX) clawed its way back to $27. Then it gave it all up, falling back to $22. Some $5 is just not enough spread with which to make a living, or worth executing a trade.

And here is the key to the market right now.

You’re not buying stocks for headlines you are seeing today, which are universally dire, cataclysmic, and predicting Armageddon.

You are buying for the headlines that will appear in a year. This will include:

Russia loses the Ukraine War

The price of oil (USO) collapses below $50 a barrel

The European energy crisis ends

Gasoline prices fall below $2.00 a gallon

Inflation falls below 4%

Interest rates stabilize around 3.50%-4.00%

Corporate earnings reaccelerate

We get another $1 trillion in corporate share buybacks

That sounds like one heck of a market to buy into. Why not buy now when everything is on sale, rather than in a year when it is expensive once again?

You don’t have to bet the ranch today. Just scale in, buying 10% of a position a day in your favorite names until you are fully invested. That way, you’ll get an average close to a bottom. You’ll at least get a seat on the train and won’t be left behind waving goodbye from the platform.

That means adding technology stocks to your portfolio, which will be the top-performing sector for the rest of this century.

The other thing you can do is to start getting rid of your defensive names. If you think oil is going below $50 in a year as I do, you don’t want to have a single oil name in your portfolio.

You want to own boring stocks in falling markets and exciting ones in rising markets.

You can’t get THE bottom. I can’t do it, so how are you going to?

There is one other factor that I guarantee you no one is looking at. Do you know anyone who bought a spec home for a quick flip lately? I bet not.

That means there is a lot of speculative capital looking for a new home and I bet that a lot of it is going into the stock market. The same is true with bitcoin.

I just thought you’d like to know.

Apple Rolls Out Next-Gen iPhone. The focus will be on larger phones with faster processors and a better camera. There may also be an inflationary $100 price increase. A new watch and Airpods are also expected. Buzz kill: every two years, this event usually marks a six-month high in the stock. Apple may no longer be the safest stock in the market.

Russia Cuts Gas Supplies to Europe until Ukraine sanctions are lifted. That took the Euro to a 20-year low of under 99 cents. You get into bed with the devil, and you pay the consequences. Russia must desperately need that trade with Europe.

Germany Fights Russia with Coal. Coal is enjoying a renaissance in Germany where it is being used to replace the total cut-off in Russian natural gas. In 2022, coal has jumped from 27% to 33% of electricity production, while gas has plunged from 18% to 11.7%. It goes against the country’s strong environmental principles and will only be used as a bridge towards greatly accelerated alternative energy efforts. Importing all the natural gas they can from the US also helps. It will greatly help Europe hold together this winter to face down the Russian energy war.

Home Equity is Shrinking, down $500 billion from the $11.5 trillion peak. It means less money is available to go into stocks. But we are nowhere near a crash, like we saw in 2008, when home equity nearly went to zero. No liar loans, exaggerated appraisals, or financial crisis this time. This housing recession will be about ice, not fire. There won’t be much of a housing crash when we’re still short 10 million homes. If you sell, your new mortgage will have double the interest rate. Ergo, don’t sell.

Weekly Jobless Claims Hit 3-Month Low, down 6,000 to 222,000. This number is not even close to an economic slowdown. In the wake of the decent nonfarm payroll report last week, it shows that employment is anything but slowing.

Tesla (TSLA) Triples China Deliveries after expanding the Shanghai factory. Elon Musk seems able to accomplish what others can’t, increasing production and sales in the face of rolling Covid lockdowns, heat waves, and materials shortages. Buy (TSLA) on dips.

California Sets a $22 Minimum Wage for fast food workers starting from 2023. It’s a catch-up with minimum wages that haven’t changed for 20 years and represents a broader issue for the rest of the country. Think this may be inflationary? Count on all of this going straight into product price rises. It may become cheaper to make your cheeseburgers at home.

The Bond Market Crashes, with ten-year US Treasury bond soaring 20 basis points to a 3.35% yield. The (TLT) hit a new 2022 low at $107.49. Bonds are reading the writing on the wall from Jackson Hole, even if stocks aren’t. Avoid (TLT).

Oil Crashes $4 on recession fears. Most Russian sales are now taking place 20% below the market to China and India. We may be approaching an interim low as winter approaches unless the Ukraine war ends.

A US Rail Strike Threatens as wage talks stall. A recession could be the result. Negotiators have until September 16 to reach a deal for 115,000 workers. A strike would also spike inflation. This could be our next black swan.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil in a sharp decline, inflation falling, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

With markets now a snore, my September month-to-date performance ground up to +1.02%. I took profits in my last long in Microsoft (MSFT) going into a rare 100% cash position awaiting the next market entry point.

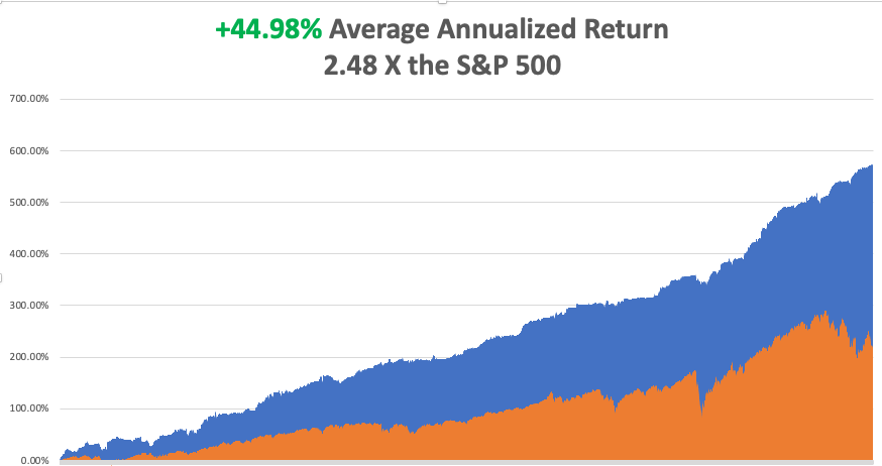

My 2022 year-to-date performance improved to +60.98%, a new high. The Dow Average is down -12% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +73.65%.

That brings my 14-year total return to +573.54%, some 2.48 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +44.98%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 95.2 million, up 300,000 in a week and deaths topping 1,050,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, September 12 at 8:30 AM, US Consumer Inflation Expectations for August is released.

On Tuesday, September 13 at 8:30 AM, the US Core Inflation Rate for August is out.

On Wednesday, September 14 at 7:00 AM, the Producer Price Index for August is published.

On Thursday, September 15 at 8:30 AM, Weekly Jobless Claims are announced. We also get Retail Sales for August. On Friday, September 16 at 7:00 AM, the University of Michigan Consumer Sentiment is disclosed. At 2:00 the Baker Hughes Oil Rig Count are out.

As for me, when you’re 6’4” and 180 pounds, there is not a lot of things that can seriously toss you around. One is a horse, and another is a wave.

It was the latter that took me down to Newport Beach, CA to a beachfront house for my annual foray into body surfing. Newport Beach has some of the best waves in California.

This is the beach that made John Wayne a movie star.

John, whose real name was Marion Morrison, grew up in a Los Angeles suburb and won a football scholarship to the University of Southern California. While still a freshman in 1925, he went bodysurfing at Newport Beach with a carload of buddies. A big wave picked him up and smashed him down on the sand, breaking his right shoulder.

At football practice, there was no way a big lineman could block and tackle with a broken shoulder, so he was kicked off the team and lost his scholarship.

He still had to eat, so he resorted to the famed student USC jobs bulletin board, which I have taken advantage of myself (it’s where I got my LA coroner’s job).

The 6’4” Wayne was hired as a stagehand by up-and-coming movie director John Ford, himself also a former college football star. In 14 years, Wayne worked himself up from gopher, to extra, to a leading man in 1930, and then his breakout 1939 film Stagecoach.

During WWII, Wayne, too old, was confined to entertainment for the USO shows and making propaganda films while the rest of his generation was at the front. He never recovered from that humiliation and spent the rest of his life as a super patriot.

I saw John Wayne twice. My uncle Charles, who was the CFO of the Penn Central Railroad in the 1960s, made a fortune selling short the stock right before it went bankrupt (maybe that was legal then?). He bought a big beach house on California Balboa’s Island right next door to John Wayne’s.

One day, the family was cruising by Wayne’s house, and he was sitting on his front patio in a beach chair. Then one of our younger kids shouted out “he’s bald” which he was. Wayne laughed and waved.

The second time was in the early 1970s. I was walking across the lobby of the Beverly Hills Hotel with the movie star and Miss America runner-up Cybil Shephard on my arm. He walked right up to us and with a big smile said, “hello gorgeous”. He wasn’t talking to me.

I learned a lot about Wayne from my uncle, Medal of Honor winner Mitchell Paige, who was hired as the technical consultant for the 1949 film Sands of Iwo Jima and spent several months working closely with him. The lead character, Marine Sargent John Striker, was based on Mitch.

Film critics complained that Wayne couldn’t act, that he was just himself all the time. But I knew my uncle Mitch well, a humble, modest, self-effacing man, and Wayne absolutely nailed him to a tee.

The Searchers, made in 1958, and directed by John Ford, is considered one of the finest movies ever made. I show it to my kids every Christmas to remind them where they came from because we have an ancestor who was kidnapped in Texas by the Comanches and survived.

John Wayne was a relentless chain smoker, common for the day, and lung cancer finally caught up with him. His first bout was in 1965 when he was making In Harm’s Way, the worst war movie he ever made. His last film, The Shootist, made in 1978, was ironically about an old gunslinger dying of prostate cancer.

John Wayne hosted the 1979 Academy Awards rail thin, racked by chemotherapy and radiation treatments. He died a few months later after making an incredible 169 movies in 50 years.

John Wayne was one of those people you’re lucky to run into in life. He was a nice guy when he didn’t have to be.

As for those waves at Newport Beach, I can vouch they are just as tough as they were 100 years ago.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/09/john-having-beer.jpg331305Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-12 10:02:422022-09-12 12:38:54The Market Outlook for the Week Ahead, or Stuck in the Middle

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE ROLLING RECESSION),

(AAPL), (NVDA), (TSLA), (USO), (BTC), (MSFT), (CRM), (V), (BA), (MSFT), (CRM), (DIS)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-06 11:04:562022-09-06 11:18:37September 6, 2022

The airline business is booming but homebuilders are in utter despair. Hotel rooms are seeing extortionate 56% YOY price increases, while residential real estate brokers are falling flat on their faces. It’s a recession that’s here, there, and nowhere.

Welcome to the rolling recession.

If you are lucky enough to work in a handful of in-demand industries, times have never been better. If you aren’t, then it’s Armageddon.

Look at single industries one at a time, as the media tends to do, business conditions are the worst since the Great Depression and pessimism is rampant. Look at Tesla, where there is a one-year wait to get a Model X, and there is either a modest recession on the menu, or simply slowing growth at worst.

Notice that a lot of commentators are using the word “normally”. News Flash: nothing has been normal with this economy for three years.

Which leaves us with dueling yearend forecasts for the S&P 500. It will either be at 3,900, where it is now, or 4,800. A market that is unchanged, worst case, and up 20% best case sounds like a pretty good bet to me. The prospects for individual stocks, like Tesla (TSLA), Microsoft (MSFT), or NVIDIA (NVDA) are even better, with a chance of 20% of downside or 200% of upside.

I’ll sit back and wait for the market to tell me what to do. In the meantime, I am very happy to be up 60% on the year and 90% in cash.

An interesting thing is happening to big-cap tech stocks these days. They are starting to command bigger premiums both in the main market and in other technology stocks as well.

That is because investors are willing to pay up for the “safest” stocks. In effect, they have become the new investment insurance policy. Look no further than Apple (AAPL) which, after a modest 14% decline earlier this year, managed a heroic 30% gain. Steve Jobs’ creation now boasts a hefty 28X earnings multiple. Remember when it was only 9X?

Remember, the stock sells off on major iPhone general launches like we are getting this week, so I’d be careful that my “insurance policy” doesn’t come back and bite me in the ass.

Nonfarm Payroll Report Drops to 315,000 in August, a big decline, and the Headline Unemployment Rate jumps to 3.7%. The Labor Force Participation Rate increased to 62.4%. The “discouraged worker” U-6 unemployment rate jumped to 7.0%. Manufacturing gained 22,000. Stocks loved it, but it makes a 75-basis point in September a sure thing.

Jeremy Grantham Says the Stock Super Bubble Has Yet to Burst, for the seventh consecutive year. If I listened to him, I’d be driving an Uber cab by now, commuting between side jobs at Mcdonald's and Taco Bell. Grantham sees stocks, bonds, commodities, real estate, precious metals, crypto, and collectible Beanie Babies as all overvalued. Even a broken clock is right twice a day unless you’re in the Marine Corps, which uses 24-hour clocks.

Where are the Biggest Buyers on the Dip? Microsoft (MSFT), Salesforce (CRM), and Disney (DIS), followed by Visa (V), and Boeing (BA). Analysts see 20% of upside for (MSFT), 32% for (CRM), and 21% for (DIS). Sure, some of these have already seen big moves. But the smart money is buying Cadillacs at Volkswagen prices, which I have been advocating all year. Take the Powell-induced meltdown as a gift.

The Money Supply is Collapsing, down for four consecutive months. M2 is now only up less than 1% YOY. This usually presages a sharp decline in the inflation rate. With a doubling up of Quantitative Tightening this month, we could get a real shocker of a falling inflation rate on September 13. Online job offers are fading fast and used cars have suddenly become available. This could put in this year’s final bottom for stocks.

California Heads for a Heat Emergency This Weekend, with temperatures of 115 expected. Owners are urged to fully charge their electric cars in advance and thermostats have been moved up to 78 as the electric power grid faces an onslaught of air conditioning demand. The Golden State’s sole remaining Diablo Canyon nuclear power plant has seen its life extended five years to 2030. This time, the state has a new million more storage batteries to help.

Oil (USO) Dives to New 2022 Low on spreading China lockdowns. Take the world’s largest consumer offline and it has a big impact. More lows to come.

NVIDIA (NVDA) Guides Down in the face of new US export restrictions to China. The move will cost them $400 million in revenue. These are on the company’s highest-end A100 and H100 chips which China can’t copy. (AMD) received a similar ban. It seems that China was using them for military AI purposes. The shares took a 9% dive on the news. Cathie Wood’s Ark (ARKK) Funds dove in and bought the lows.

Weekly Jobless Claims Plunge to 232,000, down from 250,000 the previous week for the third consecutive week. No recession in these numbers.

First Solar (FSLR) Increases Output by 70%, thanks to a major tax subsidy push from the Biden Climate Bill. The stock is now up 116% in six weeks. We have been following this company for a decade and regularly fly over its gigantic Nevada solar array. Buy (FSLR) on dips.

Home Prices Retreat in June to an 18% YOY gain, according to the Case Shiller National Home Price Index. That’s down from a 19.9% rate in May. Tampa (35%), Miami (33%), and Dallas (28.2%) showed the biggest gains. Blame the usual suspects.

Tesla (TSLA) Needs $400 Billion to expand its vehicle output to Musk’s 20 million units a year target. One problem: there is currently not enough commodity production in the world to do this. That sets up a bright future for every commodity play out there, except oil.

Bitcoin (BTC) is Headed Back to Cost, after breaking $20,000 on Friday. With the higher cost of electricity and mining bans, spreading the cost of making a new Bitcoin is now above $17,000. It doesn’t help that much of the new crypto infrastructure is falling to pieces.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil prices and inflation now rapidly declining, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

With a very troublesome flip-flopping market, my August performance still posted a decent +5.13%.

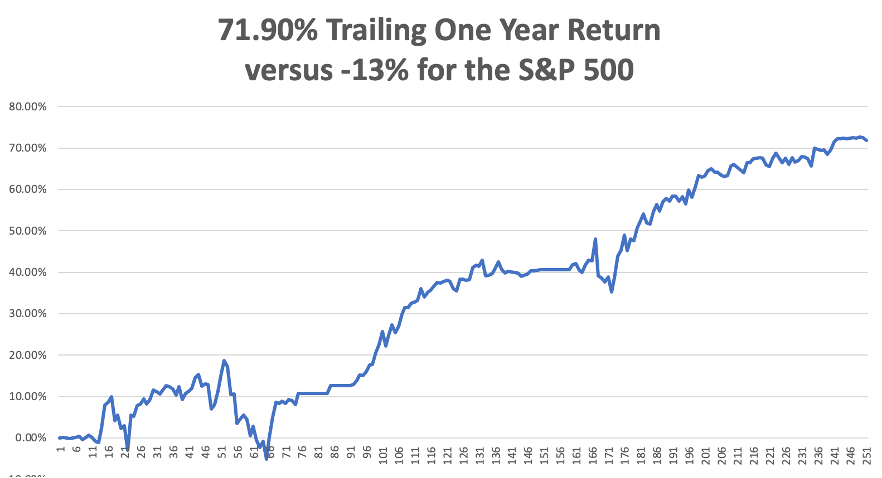

My 2022 year-to-date performance ballooned to +59.96%, a new high. The Dow Average is down -13.20% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +71.90%.

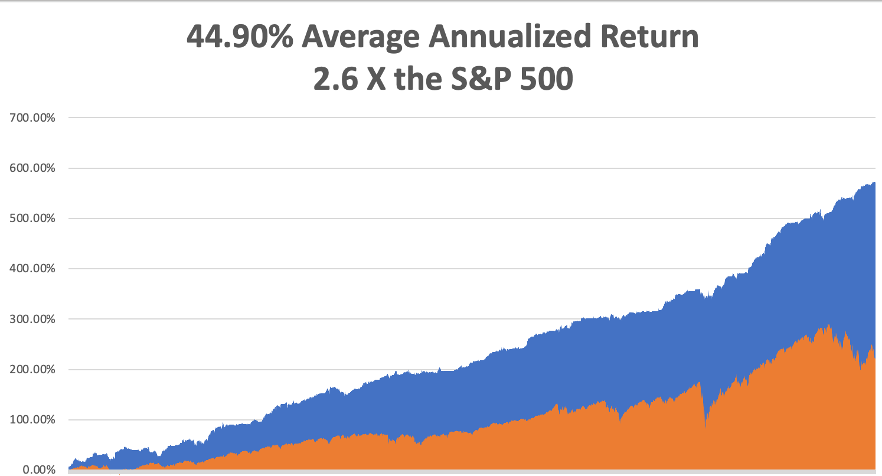

That brings my 14-year total return to +572.52%, some 2.60 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +44.90%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 94.7 million, up 300,000 in a week and deaths topping 1,047,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, September 5 markets are closed for Labor Day.

On Tuesday, September 6 at 7:00 AM, the ISM Non-Manufacturing PMI for August is out.

On Wednesday, September 7 at 11:00 AM, the Fed Beige Book for July is published.

On Thursday, September 8 at 8:30 AM, Weekly Jobless Claims are announced. On Friday, September 9 at 2:00 the Baker Hughes Oil Rig Count is out.

As for me, the first thing I did when I received a big performance bonus from Morgan Stanley in London in 1988 was to run out and buy my own airplane.

By the early 1980s, I’d been flying for over a decade. But it was always in someone else’s plane: a friend’s, the government’s, a rental. And heaven help you if you broke it!

I researched the market endlessly, as I do with everything, and concluded that what I really needed was a six-passenger Cessna 340 pressurized twin turbo parked in Santa Barbara, CA. After all, the British pound had just enjoyed a surge again the US dollar so American planes were a bargain. It had a range of 1,448 miles and therefore was perfect for flying around Europe.

The sensible thing to do would have been to hire a professional ferry company to fly it across the pond. But what’s the fun in that? So, I decided to do it myself with a copilot I knew to keep me company. Even more challenging was that I only had three days to make the trip, as I had to be at my trading desk at Morgan Stanley on Monday morning.

The trip proved eventful from the first night. I was asleep in the back seat over Grand Junction, CO when I was suddenly awoken by the plane veering sharply left. My co-pilot had fallen asleep, running the port wing tanks dry and shutting down the engine. He used the emergency boost pump to get it restarted. I spent the rest of the night in the co-pilot’s seat trading airplane stories.

The stops at Kansas City, MO, Koshokton, OH, Bangor, ME proved uneventful. Then we refueled at Goose Bay, Labrador in Canada, held our breath and took off for our first Atlantic leg.

Flying the Atlantic in 1988 is not the same as it is today. There were no navigational aids and GPS was still top secret. There were only a handful of landing strips left over from the WWII summer ferry route, and Greenland was still littered with Mustang’s, B-17’s, B24’s, and DC-3’s. Many of these planes were later salvaged when they became immensely valuable. The weather was notorious. And a compass was useless, as we flew so close to the magnetic North Pole the needle would spin in circles.

But we did have NORAD, or America’s early warning system against a Russian missile attack.

The practice back then was to call a secret base somewhere in Northern Greenland called “Sob Story.” Why it was called that I can only guess, but I think it has something to do with a shortage of women. An Air Force technician would mark your position on the radar. Then you called him again two hours later and he gave you the heading you needed to get to Iceland. At no time did he tell you where HE was.

It was a pretty sketchy system, but it usually worked.

To keep from falling asleep, the solo pilots ferrying aircraft all chatted on frequency 123.45 MHz. Suddenly, we heard a mayday call. A female pilot had taken the backseat out of a Cessna 152 and put in a fuel bladder to make the transatlantic range. The problem was that the pump from the bladder to the main fuel tank didn’t work. With eight pilots chipping in ideas, she finally fixed it. But it was a hair-raising hour. There is no air-sea rescue in the Arctic Ocean.

I decided to play it safe and pick up extra fuel in Godthab, Greenland. Godthab has your worst nightmare of an approach, called a DME Arc. You fly a specific radial from the landing strip, keeping your distance constant. Then at an exact angle you turn sharply right and begin a descent. If you go one degree further, you crash into a 5,000-foot cliff. Needless to say, this place is fogged 365 days a year.

I executed the arc perfectly, keeping a threatening mountain on my left while landing. The clouds mercifully parted at 1,000 feet and I landed. When I climbed out of the plane to clear Danish customs (yes, it’s theirs), I noticed a metallic scraping sound. The runway was covered with aircraft parts. I looked around and there were at least a dozen crashed airplanes along the runway. I realized then that the weather here was so dire that pilots would rather crash their planes than attempt a second go.

When I took off from Godthab, I was low enough to see the many things that Greenland is famous for polar bears, walruses, and natives paddling in deerskin kayaks. It was all fascinating.

I called into Sob Story a second time for my heading, did some rapid calculations, and thought “damn”. We didn’t have enough fuel to make it to Iceland. The wind had shifted from a 70 MPH tailwind to a 70 MPH headwind, not unusual in Greenland. I slowed down the plane and configured it for maximum range.

I put out my own mayday call saying we might have to ditch, and Reykjavik Control said they would send out an orange bedecked Westland Super Lynch rescue helicopter to follow me in. I spotted it 50 miles out. I completed a five-hour flight and had 15 minutes of fuel left, kissing the ground after landing.

I went over to Air Sea rescue to thank them for a job well done and asked them what the survival rate for ditching in the North Atlantic was. They replied that even with a bright orange survival suit on, which I had, it was only about half.

Prestwick, Scotland was uneventful, just rain as usual. The hilarious thing about flying the full length of England was that when I reported my position in, the accents changed every 20 miles. I put the plane down at my home base of Leavesden and parked the Cessna next to a Mustang owned by a rock star.

I asked my pilot if ferrying planes across the Atlantic was also so exciting. He dryly answered “Yes.” He told me that in a normal year, about 10% of the planes go missing.

I raced home, changed clothes, and strode into Morgan Stanley’s office in my pin-stripped suit right on time. I didn’t say a word about what I just accomplished.

The word slowly leaked out and at lunch, the team gathered around to congratulate me and listen to some war stories.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Flying the Atlantic in 1988

Looking for a Place to Land in Greenland

Landing on a Postage Stamp in Godthab, Greenland

No Such a Great Landing

No Such a Great Landing

Flying Low Across Greenland

Gassing Up in Iceland

Almost Home at Prestwick

Back to London in 1988

https://www.madhedgefundtrader.com/wp-content/uploads/2022/09/john-thomas-family-london-scaled.jpg16992560Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-06 11:02:332022-09-06 11:19:19The Market Outlook for the Week Ahead, or Welcome to the Rolling Recession

A fresh analysis from the C-suite at the top 1,000 U.S. companies by revenue offers us critical insight into the direction of tech management.

It’s important to keep our finger on the pulse of what’s happening at the higher level of tech companies because these are the key people that drive the game-changing decisions.

It’s no surprise that the banking and financial services industry has the oldest average CEO age at 60, and the technology and energy sectors have the youngest CEOs at an average age of 57.

Technology companies harness new technologies that can lead to new businesses so that would usually trend younger.

Compared to other industries, tech companies also have a boom-bust element to them because technologies go extinct quicker, and refreshing a CEO is always on the table if the bust element creeps in.

Interestingly, the current tenure is down from an average of 8 years to 6 years, meaning that the leash for tech CEOs is getting shorter and shorter.

Much like highly paid professional athletes these days, there’s no learning on the job type of mentality. It’s overperform now or face the sack.

This mentality emphasizes short-term performance which revolves around the quarterly earnings report and stock-based compensation to employees.

Then add in the wild card of forced lockdowns and China’s increasingly aggressive attitude to politics and it’s simple to understand that boards need to quickly change management if they believe they cannot navigate these herculean tasks.

Just a few instances where critical decisions are being made can be seen in Apple when CEO Tim Cook yanked China production and moved factories to Vietnam.

Vietnam is becoming the new factory of the world for tech companies because costs and political risks associated with China are accelerating.

Now, throw in the Taiwan situation after top U.S. government officials chose to visit the island and tech companies are now worrying about their supply of Taiwan chips needed to harness artificial intelligence.

CFOs are usually the second most important person in a company behind the CEO because they guard the balance sheet and usually possess a strong accounting background.

Yet they can be disposed of quickly for bad performance which is why tech CFOs only tenure 4.1 years if we compare with other more stable industries.

The key findings here is that tech management has never been so prone to high turnover.

Due to the internet, competition has supercharged the fight for highly paid positions and data can be calculated in real time because of superior analytic platforms.

Management won’t be able to hide poor performance because of the close tracking.

As much as it’s difficult to make a famous name as a C-suite manager, tech CEOs with a proven track record can expect elevated attention which is why if guys who have built successful tech firms like Jack Dorsey reach out to investors, they will get whatever starting funds they need.

This builds on the winning take mentality in technology which has a few outsized winners among the crowd.

On the trading front, I would hesitate to buy tech stocks from management that is unproven.

I would urge traders to go into long-term bets on guys like Tim Cook, Sundar Pichai, and Elon Musk and don’t compromise on the quality of tech management because it makes a big difference in the future price of the stock.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-02 15:02:252022-09-02 17:39:57Don't Compromise

Just as every cloud has a silver lining, every stock market crash offers generational opportunities.

September and October are now upon us, for the past 100 years, the two worst trading months of the year. That means they are also the best months for entering spectacular trades with LEAPS.

What are LEAPS you make ask?

This is the best strategy with which to cash in on the gigantic market swoons, which have become a regular feature of our markets, especially in 2022.

LEAPS, or Long Term Equity Anticipation Securities, are just a fancy name for a stock option spread with a maturity of more than one year.

You execute orders for these securities on your options online trading platform, pay options commissions, and endure options like volatility.

Another way of describing LEAPS is that they offer a way to rent stocks instead of buying them, with the prospect of enjoying years’ worth of stock gains for a fraction of the price.

While these are highly leveraged instruments, you can’t lose any more money than you put into them. Your risk is well defined. But you get 10X or more exposure to the stock. They are kind of like synthetic futures on individual stocks.

And there are many companies in the market where LEAPS is a very good idea, especially on those gut-wrenching 1,000-point down days.

Interested?

Currently, LEAPS are listed all the way out until January 2025.

However, the further expiration dates will have far less liquidity than near-month options, so they are not a great short-term trading vehicle. That is why limit orders in LEAPS, as opposed to market orders, are crucial.

These are really for your buy-and-forget investment portfolio, defined benefit plan, 401k, or IRA.

Because of the long maturities, premiums can be enormous. However, there is more than one way to skin a cat, and the profit opportunities here can be astronomical.

Like all options contracts, a LEAPS gives its owner the right to "exercise" the option to buy or sell 100 shares of stock at a set price for a given time.

LEAPS have been around since 1990, and trade on the Chicago Board Options Exchange (CBOE).

To participate, you need an options account with a brokerage house, an easy process that mainly involves acknowledging the risk disclosures that no one ever reads.

If a LEAPS expires "out-of-the-money" – when exercising, you can lose all the money that was spent on the premium to buy it. There's no toughing it out waiting for a recovery, as with actual shares of stock. Poof, and your money is gone.

LEAPS are also offered on exchange-traded funds (ETFs) that track indices like the Standard & Poor's 500 index (SPY) and the Dow Jones Industrial Average (INDU), so you could bet on up or down moves of the broad market.

One of my most profitable trades in 2021 was the (TLT) December 2022 $$150-$155 vertical bear put LEAPS, which generated a 100% profit for everyone who got into it. Those who bought the more aggressive (TLT) December 2022 $$140-$145 vertical bear put LEAPS made 200%.

I see you’re still interested. For example, the highly popular ProShares 2X Ultra Technology ETF (ROM) only offers maturities out only six months so it is not possible to do a proper LEAPS. No one is willing to take the risk on the other side of this highly volatile security.

Not all stocks have options, and not all stocks with ordinary options also offer LEAPS.

Note that a LEAPS owner does not vote proxies or receive dividends because the underlying stock is owned by the seller, or "writer," of the LEAPS contract until the LEAPS owner exercises.

Despite the Wild West image of options, LEAPS are actually ideal for the right type of conservative investor.

They offer more margin and more efficient use of capital than traditional broker margin accounts. And you don’t have to pay the usurious interest rates that margin accounts usually charge.

And for a moderate increase in risk, they present outsized profit opportunities.

For the right investor, they are the ideal instrument.

Let me go through some examples to show you their inner beauty.

By now, you should all know what vertical bull call spreads are. If you don’t, then please click here for a quickie video tutorial (you must be logged in to your account).

Let’s go back to February 9, 2018 when the Dow Average plunged to its 23,800 low for the year. I then begged you to buy the Apple (AAPL) June 2018 $130-$140 call spread at $8.10, which most of you did. A month later, that position is worth $9.40, up some 16.04%. Not bad.

Now let’s say that instead of buying a spread four months out, you went for the full year and three months, to June 2019.

That identical (AAPL) $130-$140 would have cost $5.50 on February 9. The spread would be worth $9.40 today, up 70.90%, and worth $10 on June 21, 2019, up 81.81%.

So, by holding a 15-month to expiration position for only a month, you get to collect 86.67% of the maximum potential profit of the position.

So, now you know why we leap into LEAPS.

When the meltdown comes, and that could be as soon as next week, use this strategy to jump into longer term positions in the names we have been recommending and you should be able to retire early.

Now you know why I like LEAPS so much. Please play around with the names and the numbers and I’m sure you will find something you like. But remember one thing. LEAPS are only a trade to consider at long time market bottoms, not tops!

They are also the perfect positions to own if you believe we have just entered a second Roaring Twenties and a second American Golden Age, as I do.

Time to Leap Into LEAPS

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/leap.png450372Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-02 10:04:022022-09-02 11:15:50Get Ready to Take a Leap Back into LEAPS

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-26 10:04:342022-08-26 11:10:50August 26, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.