Below please find subscribers’ Q&A for the April 2 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

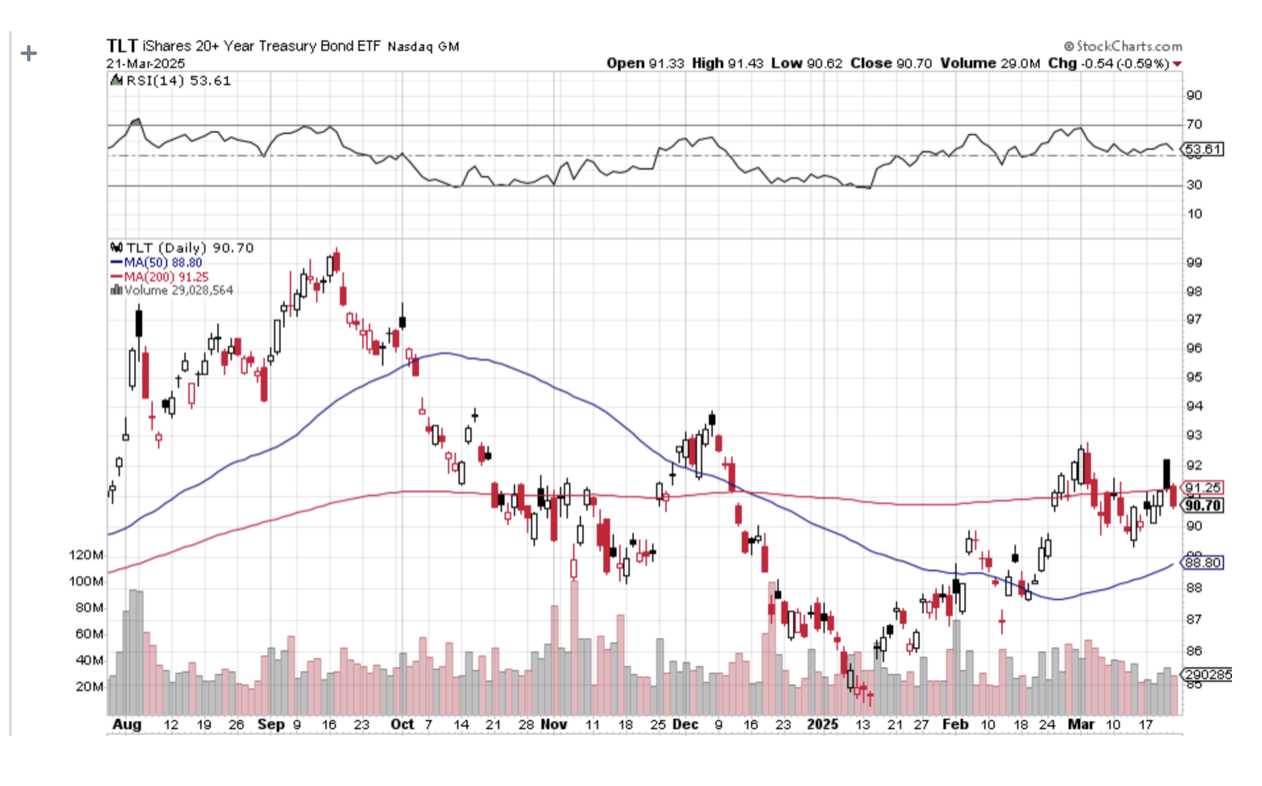

Q: Why are there days when both bonds and interest rates are going up?

A: Well, there is a tug-of-war going on in the bond market. When recession fears are the dominant theme of the day, interest rates go down and bond prices go up. Remember, it's an inverse relationship. When the deficit and inflation are the big fears and you get those on the inflation announcement days—we get three or four of those a month—then interest rate goes up and bonds go down. That will be a big driver of stock prices because they are very sensitive to interest rates always.

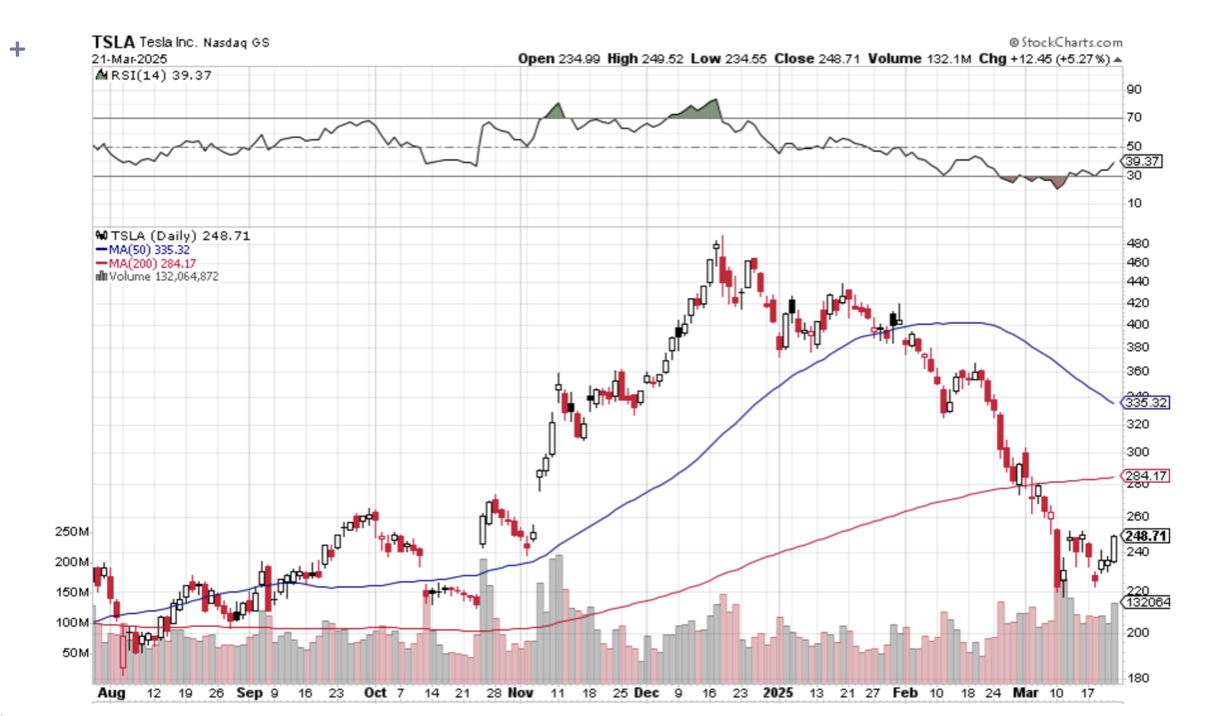

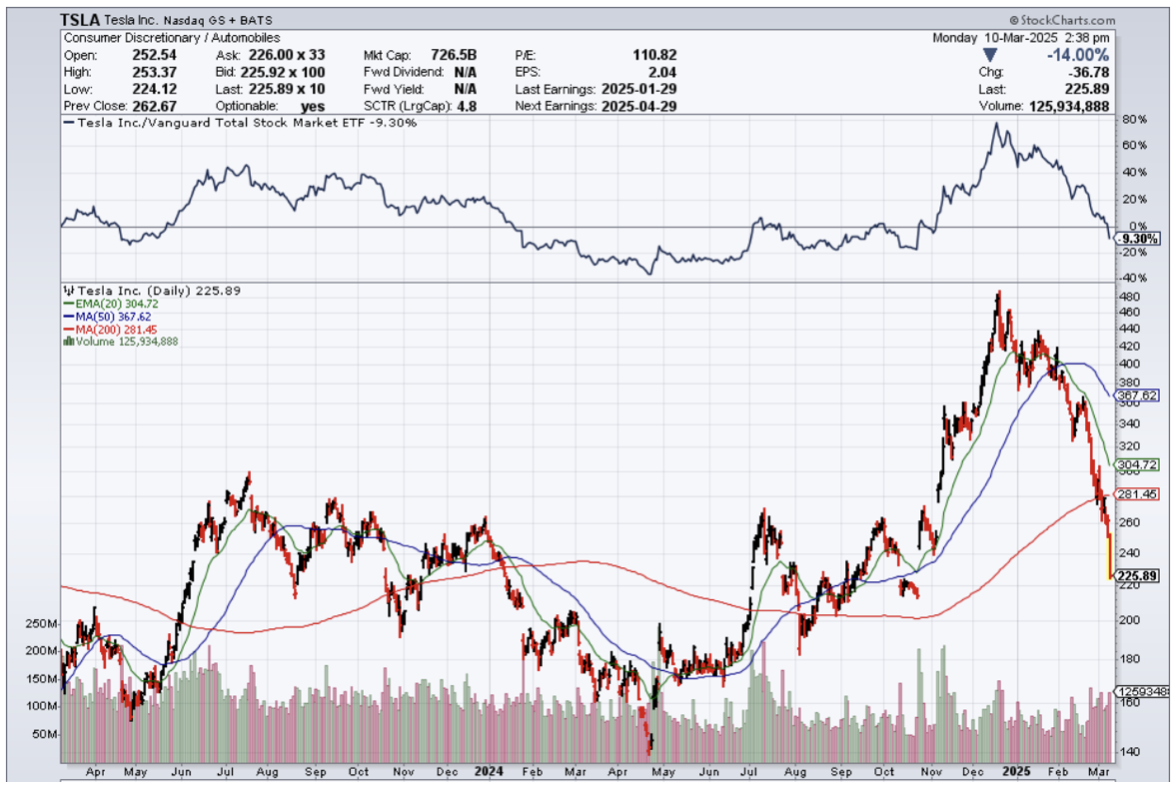

Q: Do you think Tesla (TSLA) has hit bottom?

A: I don't think so. I think the declining sales continue. I think the Tesla brand has been severely damaged as long as Elon Musk stays in politics. Also, no one buys cars in recessions—sorry, but that is the last thing that people or companies want to buy is a brand-new car.

Q: What will happen to the smaller EV makers?

A: They will all go bankrupt. You know, unless they have a very rich uncle like Lucin Group (LCID) does—Saudi Arabia can keep pumping money in there forever. Amazon owns a big piece of Rivian Motors (RIVN) I don't think any of the small EV makers will make it because they now have Tesla to compete against.

Q: Do you have any way to short restaurant stocks as an industry?

A: I don't know of a single industry ETF for restaurants only. Restaurants are not an industry I have spent a lot of time studying because the margins are so low. I prefer a 70% margin to a 3% margin ones. There are a lot of things like consumer discretionary, so you just have to go shopping in the ETF world. There are more than 3,000 listed ETFs these days in every conceivable subsector of the economy, more than there are listed stocks, so there might be something out there somewhere. Yes, you are correct in wanting to short restaurants going into a recession as well as airlines, rental car companies, and hotels, but these things are already down a lot—you know, 40% or so. So, be careful shorting after these things have already had enormous declines in a very short time.

Q: Will the recession cause Democrats to win midterm elections?

A: If I were a betting man—and of course I'm not, I only go after sure things, —I would say yes. But, you know, 18 months might as well be 18 years in the political world. So, who knows what will happen? Suffice it to say that yesterday's election results were overwhelmingly positive for the Democrats and represent a very strong “no vote” for Trump policies and Musk policies. Even in Florida where they won, the victory margin shrank from 35% six months ago to 12%. That is an enormous swing in the electorate away from Republicans, and that's why the Republicans are very nervous about any election. That's why the Texas governor is blocking a by-election there. He’s afraid he’ll lose.

Q: Is Tesla (TSLA) toast for good?

A: If Elon Musk went back to Silicon Valley and just managed Tesla and kept his mouth shut on non-Tesla issues, I bet the stock would double from these levels over the medium term. So yes, it just depends on how much Elon Musk wants his $200 billion back. That's how much he's lost on the stock depreciation since December.

Q: Is it time to short Delta Air Lines (DAL)?

A: You kind of missed the boat. No point in closing the barn door after the horses have bolted. This was a great short in February, and the same with hotels and rail companies. So be careful of your biggest recession indicators; they have all already collapsed and are more likely to bounce along the bottom.

Q: What are the probabilities that the tariff war could backfire, and we end up with massive job losses and a shortage of goods?

A: Actually, that is the most likely outcome. In my humble opinion, we know big layoffs are coming already. Prices are going to go up, so people will buy less. And prices will go up a lot because of the tariffs, so it's the perfect, perfect economy destruction strategy. And of course, that all feeds directly into the stock market.

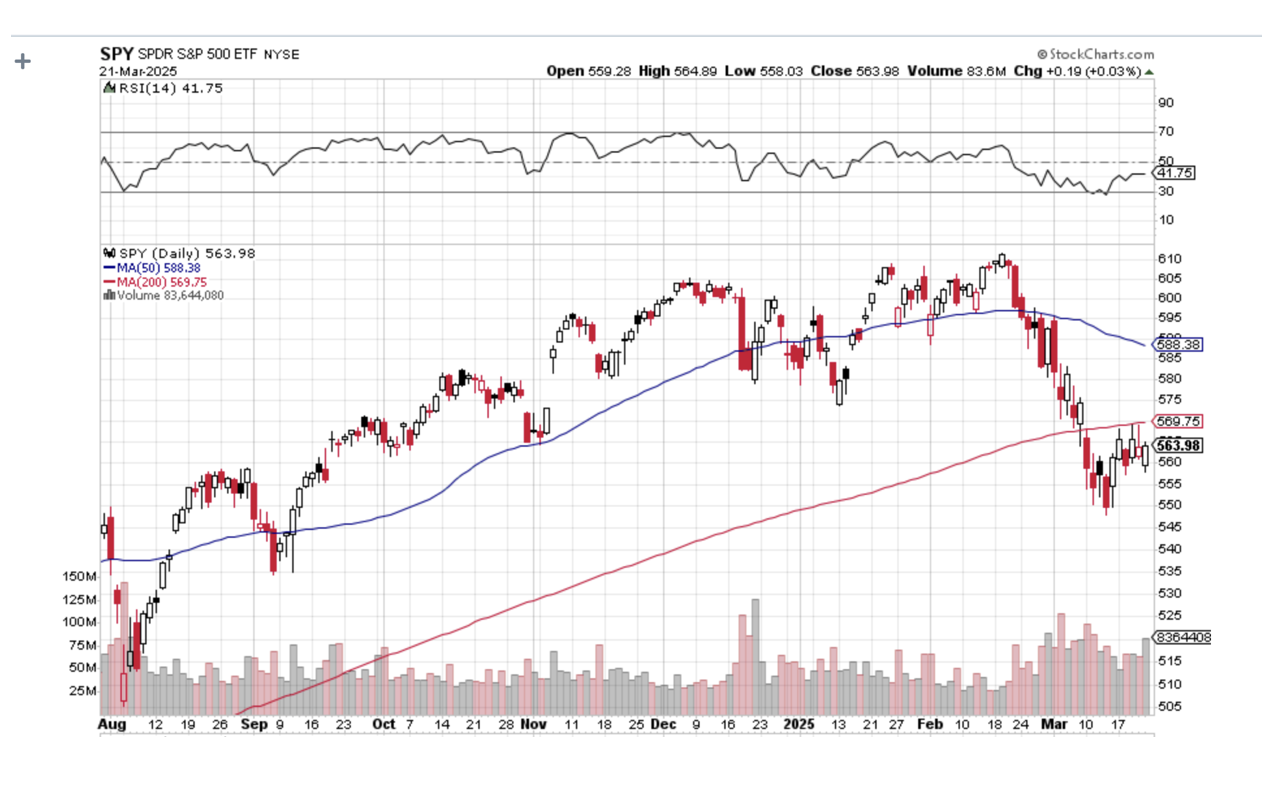

Q: Do you think a 10% decline is enough to reflect all of that?

A: Absolutely not. More like down 20% or down 30% to discount the destruction of the economy—some say by half. So, that's an easy question to answer.

Q: Do you think Palantir (PLTR) will recover from this dip?

A: Only when government spending resumes. That could happen sooner once we get some clarity on where the government is actually going to spend its money. Palantir claims they can save masses of money for the government by getting it just to use their software, and a lot of companies are making that claim, like Arthur Anderson, who also had all their contracts axed. So, we don't know. “We don't know” is the most commonly heard expression in the country today. We just don't know what's going to happen.

Q: And is Palantir (PLTR) cheap after a 40% sell-off?

A: No. It's still incredibly expensive and that is the concern.

Q: Is crypto a good short-term bet in this type of high volatility?

A: No, it's not. It's a horrible bet. A 10% decline in the S&P 500 delivered a 30% decline in crypto. If we drop another 10%, you can expect crypto to drop another 30%. You know, it's like a 3x long NASDAQ ETF. That's how it's behaving. So, I watch it very carefully as a risk indicator. If we get a substantial rally, I'm looking to short the big players in crypto, which would be MicroStrategy (MSTR) and ProShares Bitcoin Strategy ETF (BITO). Looking for a good short there or at least to write calls. The call premiums are extremely high on all these crypto plays—sometimes they're 84%.

Q: How much more inflation can the economy handle before we are in a deep recession?

A: Well, I think we're in recession now. Almost every inflation indicator is pointing to lots of upside and, of course, the tariffs haven't even started yet. They start today, and it'll take at least a month or two to see what the actual impact of the tariffs will be on local prices.

Q: Why do you think the tariffs will be damaging to the economy?

A: Virtually every economist in the world has agreed that the trade wars of the 1930s were a major cause of the Great Depression, but not the sole cause. The only economists that have changed their minds now are the ones that have just gotten Trump appointments. I mean, that's it, clear and simple. You raise the price, you get less demand—basic supply and demand economics. I'm not inventing anything new here. It’s basic economics 101.

Q: Here's a good question that has puzzled people for a century: If Copper is up, why is Freeport McMoRan (FCX) down?

A: Freeport is a stock first and a commodity producer second. When stocks crash, people flee to commodities, and that is what is happening. Chinese are buying up copper ingots as a gold alternative, and people are dumping Freeport because it's in an index. Some 80% of all the selling is index selling. So if you're in that index, your stock goes down regardless of your individual fundamentals. Whether it's a good company or not, whether your earnings are expanding or not, I'm seeing this happen in lots of other great companies.

Q: Is gold (GLD) subject to 25% import duties? What will that do to the pricing of gold?

A: Physical gold got an exemption, so it is not. However, gold stocks in COMEX warehouses in New York hit record highs as the managers rushed to bring in gold to beat the tariffs to meet the ETF demand in the United States. So there’s a lot of turmoil in that market, as there are in all markets now—people trying to beat the tariffs. By the way, I bought all the computer equipment my company needs for the rest of this year in order to beat the tariff increases because all my Apple (AAPL) stuff comes from China and they're looking at 60% tariffs.

Q: If the silver (SLV) does go to a new all-time high, does that mean the S&P 500 is going to an all-time high?

A: No, if anything (SPY) goes to a multi-year low. We may be losing a generation of stock investors here. That puts silver within easy range at $50.

Q: Will biotech stocks shift because of the policy changes?

A: They're losing their government research funding, the authorization process for new drug approvals has had sand thrown at it. Time delays have been greatly extended on new approvals and suffice to say, the leadership does not have the confidence of the industry, and biotech stocks are doing horribly. You know, when you appoint someone to head a department whose main job is to dismantle that department, that's generally really horrible for the industry, especially when the industry is dependent so much on government grants for research. We are losing a generation of new scientists. That puts off any cures for cancer, Alzheimer’s, or diabetes into the far future.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader