Global Market Comments

December 11, 2020

Fiat Lux

FEATURED TRADE:

(DECEMBER 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (FXA), (FXE), (FXC), (UUP), (FXB), (ABNB), (DASH), (TAN), (TLT), (TBT), (NZD), (DKNG), (SNOW), (AAPL), (CRSP), (RTX), (NOC)

Global Market Comments

December 11, 2020

Fiat Lux

FEATURED TRADE:

(DECEMBER 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (FXA), (FXE), (FXC), (UUP), (FXB), (ABNB), (DASH), (TAN), (TLT), (TBT), (NZD), (DKNG), (SNOW), (AAPL), (CRSP), (RTX), (NOC)

Below please find subscribers’ Q&A for the December 9 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, NV with my guest and co-host Bill Davis.

Q: Is gold (GLD) about ready to turn around from here?

A: The gold bottom will be easy to call, and that’s when the Bitcoin top happens. In fact, we have a double top risk going on in Bitcoin right now, and we had a little bit of a rally in gold this week as a result. So, longer term you need actual inflation to show up to get gold any higher, and we may actually get that in a year or two.

Q: The US dollar (UUP) has been weak against most currencies including the Canadian dollar (FXC), but Canada has the same problems as the US, but worse regarding debt and so on. So why is the Canadian dollar going up against the US dollar?

A: Because it’s not the US dollar. Canada also has an additional problem in that they export 3.7 million barrels a day of oil to the US and the dollar value have been in freefall this year. Canada has the most expensive oil in the world. So, taking that out of the picture, the Canadian dollar still would be negative, and for that reason I've been recommending the Australian dollar (FXA) as my first foreign currency pick, looking for 1:1 over the next three years. Of the batch, the Canadian dollar is probably going to be the weakest, Australian dollar the strongest, and the Euro (FXE) somewhere in the middle. I don’t want to touch the British pound (FXB) as long as this Brexit mess is going on.

Q: Would you buy the IPO’s Airbnb (ABNB) and Dash (DASH)?

A: No on Dash. The entries to new competitors are low. Airbnb on the other hand is now the largest hotel in the world, and it just depends on what price it comes out at. If it comes out at a stupid price, like 50% over the IPO, I wouldn’t bother; but if you can get close to the IPO price, I would probably buy it for the long term. I think you would have another double if we got close to the IPO price, so that is worth doing. They have been absolutely brilliant in their management and the way they handled the pandemic; they basically captured all the hotel business because if you rent an apartment all by yourself, the COVID risk is much lower than if you go into a Hilton or another hotel. They also made a big push on local travel which was successful. They gave up long-distance travel, and they’re now trying to get you to explore your own area; and that worked beyond all expectations. Even I have rented some Airbnb’s out in the local area like in Carmel, Monterey, Mendocino, and so on and I came back disease-free.

Q: If the United States Treasury Bond Fund (TLT) goes to a 1.00% yield, what would that translate to in the (TBT) (2x short treasury ETF)?

A: My guess is probably about $18, which has been upside resistance for a long time, but it depends on how long it takes to get there. You have about a 3% a year cost of carry on the TBT that you don’t have in Treasuries.

Q: Should we buy China stocks when the current administration is so negative on China?

A: Yes, that’s when you buy them—when the current administration is negative on China; because when you get an administration that’s less negative on China, the Chinese stocks will all rocket. There’s an easy 20-30% in most of the headline Chinese stocks from here sometime in 2021. And I'm looking to add more Chinese stocks. I currently have Alibaba (BABA), and that’s working well. I want to pick up some more.

Q: What about the New Zealand currency ETF (NZD)?

A: It pretty much moves in sync with the Australian dollar, but it’s usually a few cents cheaper and more volatile.

Q: Legalized sports betting seems to be on the upswing. Where do you see DraftKings (DKNG) going?

A: I think it goes up. I think there’s going to be a recovery in all kinds of entertainment type activities. Draft Kings got a huge market share from the pandemic which they will probably keep.

Q: Do we use spreads when playing (FXA)?

A: Yes, you can probably do something like a $70-$72 here one month out and make some decent money.

Q: How do you feel about Snowflake (SNOW)?

A: I wanted to get into this from day one, but it doubled on the IPO, and then it doubled again. It’s one of the only technology stocks Warren Buffet has bought in the last several years besides Apple (AAPL). So, it’s just too popular right now, it’s hotter than hot. They have a dominant market share in their big data platform, so it’s a great place to be but it’s really expensive now.

Q: Do your options trade alerts have any risk of assignment?

A: Yes, they do, but when you get an assignment it’s a gift, because they’re taking you out of your maximum profit point, weeks before the expiration. All you do is tell your broker to use your long position to cover your short position, and you will get the 100% profit right then and there. I say this because the brokers always tell you to do the wrong thing when you get an assignment, such as going into the market to close out each leg separately. That is a huge mistake, and only makes money for the brokers. For more details, log in and search for “assignments” at www.madhedgefundtrader.com

Q: Congratulations on your great performance; what could derail your bullish prediction?

A: Well, we’ve already had a pandemic so obviously that’s not it, and then you have to run by your usual reasons for an out-of-the-blue crash; let’s say Donald Trump doesn't leave the presidency. That would be worth a few thousand points of downside. So would a major war. We could have both; we could have a major war before a disrupted inauguration. The president has essentially unlimited ability to go to war at any time, so there aren’t too many negatives on the near-term horizon, which is why everyone is super bullish.

Q: What’s your opinion on the solar area, stocks like First Solar (FSLR) and the Invesco Solar ETF (TAN)?

A: I’m bullish. Even though they're over 300% since March, we’re about to enter the golden age of solar. Biden wants to install 500,000 solar panels next year and provide the subsidies to accomplish that. This all looks extremely positive for solar. In California, a lot of people will go solar, because getting an independent power supply protects you from the power shut-offs that happen every time the wind picks up, in which response to wildfire danger. We had ten days of statewide power blackouts this year.

Q: What are your thoughts on lithium?

A: I’m not a big believer in lithium because there is no short supply. The key to producing lithium is finding countries with no environmental controls whatsoever because it’s a very polluting and messy process to mine. Better to let other countries mine your lithium cheap, refine it, and then send it to you in finished form.

Q: Since you love CRISPR (CRSP) at $130, what about shorting naked puts? The premiums are really high.

A: I never advocate shorting naked puts. Occasionally, I will at extreme market bottoms like we had in March, but even then, I do it only on a 1 for 1 basis, meaning don’t use any leverage or margin. Never short any more puts than you’re willing to buy the stock lower down. People regularly see the easy money, sell short too many puts, and then get a market correction and a total wipeout of their capital. And they won't have to do that liquidation themselves; their broker will do it for them. They’ll do a forced liquidation of your account and then close it because they don't want to be left holding the bag on any excess losses. You won’t find out until afterwards. So, I would not recommend shorting naked puts for the normal investor. If you want to be clever, just buy an in-the-money call spread, something like a $110-$120 out a couple of months. That's probably a far better risk reward than shorting a naked put. By the way, I came close to wiping out Solomon Brothers 30 years ago because my hedge fund was short too many Nikkei Puts. In the end, I made a fortune, but only after a few sleepless nights (remember that Mark?).

Q: What do you think about defense stock right now?

A: I’m avoiding defense stock because I don’t see any big increases in defense spending in the future administration, and that would include Raytheon (RTX), Northrop Grumman (NOC), and some of the other big defense stocks.

SEE YOU ALL IN 2021!

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

December 1, 2020

Fiat Lux

FEATURED TRADE:

(BET LIKE WARREN BUFFETT)

(MRK), (BRK.A), (AAPL), (JPM), (GILD), (PFE), (ABBV)

Warren Buffett’s moves via Berkshire Hathaway (BRK.A) showed some telling signs this third quarter.

For one, the Oracle of Omaha has surprisingly trimmed his holdings in Apple (AAPL) and even JPMorgan Chase (JPM).

Another telltale sign that change is coming can be seen in his positions in biopharmaceutical titans.

Let’s take a closer look at one of the three biggest biopharma investments of Berkshire to date: Merck.

While the New Jersey-based pharmaceutical titan has not been as widely reported as its counterparts in the COVID-19 race, Merck has actually been working on a promising coronavirus program.

In fact, the company is part of the first five COVID-19 programs included in Donald Trump’s Operation Warp Speed.

Just last week, the company added another promising COVID-19 treatment to its pipeline via the $425 million cash acquisition of Oncolmmune—a move that would give Merck access to the privately-owned company’s COVID-19 treatment, called CD24Fc.

If successful, CD24Fc will be a powerful treatment for mild to severe cases of COVID-19.

To date, only Gilead Sciences’ (GILD) Veklury has received FDA approval and even that treatment failed to address all the health concerns.

In comparison, CD24Fc is expected to undergo a smooth sailing journey from clinical trials to its market launch in 2021.

Meanwhile, Merck may have another ace in the hole with its COVID-19 program.

While the company is already months behind the frontrunners, Merck has a competitive advantage over the COVID-19 vaccine candidates submitted by Pfizer (PFE), Moderna (MRNA), and even AstraZeneca (AZN).

Its experimental COVID-19 vaccine does not require any freezing.

This means that unlike the candidates of Pfizer and Moderna, Merck’s vaccine does not need ultra-special handling and transportation.

On top of that significant advantage, Merck has been working with the nonprofit organization International AIDS Vaccine Initiative to develop a COVID-19 vaccine that only requires a single dose.

In contrast, the leading candidates today require two shots of their vaccines to become effective.

Apart from betting big on its COVID-19 program, Merck is also upping the stakes in its oncology pipeline.

Its recent move is the $2.75 billion acquisition of VelosBio—a partnership that adds another potent arrow to Merck’s already powerful quiver of cancer drugs.

This deal with VelosBio provides Merck with access to cancer treatments under development. Most of these home in on the deadly cancer cells but manage to spare the patients from several horrible side effects.

Prior to this, Merck shelled out $1 billion to gain an equity stake in Seagen (SGEN). The deal also grants Merck access to an extensive antibody drugs pipeline.

Aside from its oncology-related acquisitions—all of which have been home runs for its investors—Merck’s existing cancer pipeline has been consistent moneymakers.

Apart from lung cancer treatment Keytruda, which generated a whopping $11.9 billion in sales in 2019 alone, Merck has a virtually unbeatable arsenal against cancer.

In fact, its thyroid cancer drug Lenvima, which was initially approved for thyroid cancer in 2015, already expanded its indications to cover renal cell carcinoma and potentially even melanoma, endometrial cancer, NSCLC, and bladder cancer.

This could bring Keytruda-like success for Merck in the future.

Aside from Merck, Warren Buffett also invested in biopharmaceutical titans Pfizer and AbbVie.

As of September, Berkshire Hathaway holds 3.7 million Pfizer shares, 21.3 million AbbVie shares, and 22.4 million Merck shares.

These moves are especially noteworthy since the company has not owned any of these biopharma giants at the end of June.

Looking at the profile of these companies, there is no obvious connection or theme.

As discussed, Merck is heavily investing in its oncology pipeline.

AbbVie has been busy diversifying and building a pipeline independent from its megablockbuster Humira.

In fact, this biopharmaceutical giant has delved into dermatology with its massive acquisition of Allergan, aka the Botox-maker.

Meanwhile, Pfizer has been in the news thanks to its COVID-19 vaccine.

Aside from its coronavirus program, Pfizer has been focused on completing the merger between its Upjohn unit and generic drugmaker Mylan (MYL) to form a new company, called Viatris.

Analyzing all three closely though, one thing becomes clear: They are trading off their all-time highs and have been doing it for the entire 2020.

Do you know what that means?

Warren Buffett has been bargain shopping.

Say you owned 10% of Apple (AAPL) and you sold it for $800 in 1976.

What would that stake be worth today?

Try $80 billion.

That is the harsh reality that Ron Wayne, 84, faces every morning when he wakes up, one of the three original founders of the consumer electronics giant.

Wayne first met Steve Jobs when he was a spritely 21-year-old marketing guy at Atari who never took a bath, the inventor of the hugely successful “Pong” video arcade game.

Wayne dumped his shares when he became convinced that Steve Jobs’ reckless spending was going to drive the nascent startup into the ground, and he wanted to protect his assets in a future bankruptcy.

Co-founders Jobs and Steve Wozniak each kept their original 45% ownership.

Today, Jobs' widow has 0.5% ownership that is worth $4.2 billion, while the Woz’s share remains undisclosed.

Wayne designed the company’s original logo and wrote the manual for the Apple 1 computer which boasted all of 8,000 bytes of RAM (which is 0.008 megabytes to you non-techies).

Today, Wayne is living off of a meager monthly Social Security check in remote Pahrump, Nevada, about as far out in the middle of nowhere you can get where he can occasionally be seen playing the penny slots.

As they say in the stock market, timing is everything.

Mad Hedge Biotech & Healthcare Letter

November 17, 2020

Fiat Lux

FEATURED TRADE:

(WHY TELADOC IS A WIN-WIN-WIN STOCK)

(TDOC), (GOOG), (GOOGL), (AAPL)

Digital health was a struggling sector before COVID-19, but the pandemic changed the game, driving customers and even providers to embrace digital health solutions.

As expected, frontrunner Teladoc Health (TDOC) surfaced as a major beneficiary of this booming industry, reporting a record high in the number of virtual care visits during the ongoing health and financial crisis.

While there are concerns that these rewards could be fleeting, COVID-19 appears to have contributed longer-lasting changes, particularly in consumer behavior.

More and more users are opting for digital health solutions, with total virtual care visits up by 206% to hit 2.8 million in the third quarter of 2020 alone.

A noticeable change in Teladoc’s portfolio is the diversity of diseases they handle.

Previously accounting for only a third of its total care visits in 2019, non-infectious conditions like hypertension, depression, anxiety, and back pain now account for half.

As for the virtual care visits for dermatology and behavioral health in their business-to-business transactions, the company enjoyed a 500% boost year over year.

For context, the total number of virtual visits to Teladoc in 2019 was only 4.1 million.

Since the year 2020 started, though, the company has already recorded almost twice that number at 7.6 million—and the fourth quarter is projected to become its best-performing period yet.

The shift was also evident in the third-quarter earnings report of Teladoc, which showed that the company’s top line jumped by 109% year over year to reach $289 million.

This marks the company’s highest quarterly top-line growth rate.

In fact, this growth rate exceeded even the company's expectations.

When Teladoc released its second-quarter earnings, its Q3 projections were only somewhere between $275 million and $285 million.

As the number of COVID-19 cases continues to climb, it is highly possible that the company will once again deliver much better results than the forecasted numbers in the fourth quarter.

In terms of its fourth-quarter projections, Teladoc is expected to reach roughly 3 million virtual visits in the last months of 2020.

The conservative estimate for Teladoc’s total virtual visits this year is at 10 million.

So far, Teladoc shares are up 133% year-to-date, with the company expected to cross the $1 billion revenue mark in 2020—an almost 100% increase from its 2019 projection.

In terms of future growth, Teladoc recently completed an $18.5 billion mega-merger with Livongo Health (LVGO), making it a one-stop-shop for every virtual care need.

As a combined unit, the Teladoc-Livongo partnership is hailed as the next-generation virtual care provider. Simply put, this newly formed company is the future of the healthcare industry in America.

This means that while Teladoc has more than doubled this 2020, the stock is still expected to continue soaring thanks to its recent merger with Livongo.

Here’s a brief background of Livongo.

This company gathers data and sends reminders to its users suffering from chronic diseases to encourage them to implement lifestyle and even behavioral changes that would improve their health.

Prior to its cash-and-stock merger with Teladoc, Livongo was doubling its membership, particularly among diabetes patients.

This deal is anticipated to elevate virtual care and push Teladoc front and center of the $121 billion digital health market in the United States alone—a number that is projected to grow at a rate of 16.9% until 2025.

Needless to say, Teladoc has set itself up to control a huge part of that total value.

So far, the most notable competitors of Teladoc in this space are technology giants like Google (GOOG) via its parent company Alphabet (GOOGL) and Apple (AAPL).

With all the opportunities and even with the challenges of new competitors in the market, Teladoc remains the leader in this explosive digital health industry, making it extremely attractive for investors to ignore.

Looking at its risk-reward proposition, the company is clearly a solid growth pick.

After all, telemedicine offers a long-term win-win-win situation for everyone in the healthcare industry.

It is a win for doctors because they can see more patients.

It’s a win for patients because they get to see doctors with ease and convenience.

Finally, it is a win for insurance agencies because they generally pay lower bills for virtual visits.

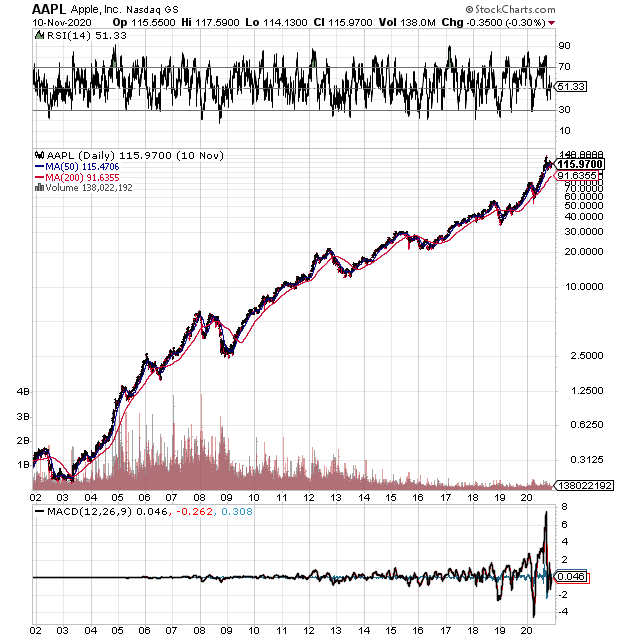

Global Market Comments

November 10, 2020

Fiat Lux

FEATURED TRADE:

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD),

(AAPL)

(THANK GOODNESS, I DON’T LIVE IN SWEDEN), (EWD),

Mad Hedge Technology Letter

October 26, 2020

Fiat Lux

Featured Trade:

(WHAT DOES DIGITAL UPSKILLING MEAN TO TECH?)

(AAPL), ($COMPQ)

The signals are there offering the impetus to the U.S. workforce to become increasingly tech-savvy in a hurry.

A word was even coined for it: “Digital upskilling.”

The idea of this development in digital skills is, in fact, the reason why every investor needs to look at tech growth stocks as the cornerstone of their investment portfolio.

To understand the trajectory of tech growth stocks, analyzing the entry level of industry employment offers a clearer snapshot of the meat and bones of the industry.

The tech workforce is upskilling precisely because they are incentivized with the opportunity to secure higher salaries.

The higher salaries exist precisely because tech corporations can afford to pay their workers more when they participate in a business cycle that delivers 40% higher revenue than the year before.

It’s a virtuous cycle that not only enriches the shareholder but is a golden chance for U.S. workers to secure a high-quality life when other U.S. industries like retail, hospitality, and energy have crashed and burned.

The very day that tech companies stop doling out larger than life salaries will be the cue that we are at ex-growth and investors must be able to pivot quickly to target the next growth part of the economy.

The great x-factor of technology is that there will always be a new start-up tech reshaping the industry and old technologies just become obsolete like the fax machine and Atari game console.

Therefore, the upskilling at all levels of the tech ladder means the possibility that someone will strike it rich by discovering a new technology that is able to revolutionize the industry.

Companies are even offering in-company courses to encourage employees to hone their skills.

This can often lead to exciting promotions even in a time where the economy has been throttled to a standstill.

The latest accelerator has been none other than the coronavirus as corporations have been forced to continue operations without the help of a physical office.

Corporations are fast-tracking their embrace of digital technologies and enabling workers to learn wherever they are, whenever they want, on any device.

Around 86% of top-performing companies reported that digital training programs boosted employee engagement and performance.

The aim of tech companies is to load itself with employees skilled in data science, data storage technology skills, tech support, and digital literacy.

Other marketable skills include software development, digital marketing, and IT administration.

The real hurdle in digital upskilling lies in execution, making an entire workforce digitally savvy is a tough chore and there will always be stragglers bringing up the rear.

Corporates have ploughed full steam into upskilling and even though Silicon Valley hasn’t moved on from the smartphone, it is squeezing as much juice from this grapefruit as it can.

We are now onto the Apple (AAPL) iPhone 12 and who knows, we might get to the iPhone 20 or 30.

We are onto the Apple iPhone 12 because it’s a cash cow and that won’t stop which is why investors need to feed their appetite for premium US tech stocks.

Stocks are divided into “value” and “growth” halves. The former consists of the stocks that are cheapest in relation to net assets, current cash flow, and so on. These tend to be older, duller, and less exciting companies.

The other half, “growth,” tends to consist of the glamorous companies that have monopolies.

Just look at the performance of value stocks. The average U.S. large company “value” mutual fund has lost 8% so far this year, even including reinvested dividends.

The average growth fund? It’s up a stunning 30%. And this gap has been going on for years: “Growth” funds have beaten “Value” funds since as far back as 2007, market data show.

From the upskilling at entry-level jobs, there are signs everywhere that investing in high growth tech is the way to go and if you compare tech to the rest of the market in 2020, the numbers are a no-brainer.