Global Market Comments

August 31, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or A TALE OF FOUR CHARTS),

(NASD), (TLT), (GLD), (JPM), (FB), (AAPL), (AMZN), (TSLA)

Global Market Comments

August 31, 2020

Fiat Lux

Featured Trade:

Listening to 27 presentations during the Mad Hedge Traders & Investors Summit last week (click here for the replays), I couldn’t help but notice something very interesting, if not alarming.

All the charts are starting to look the same.

You would expect all the technology charts to be similar on top of the historic run we have seen since the March 23 bottom.

But I wasn’t only looking at technology stocks.

Analyzing the long-term charts for stock indexes, bonds, real estate, and gold, it is clear that they ALL entered identical parabolic moves that began during the notorious Christmas bottom in December 2018.

With the exception of the pandemic induced February-March hiccup this year, it has been straight up ever since.

The best strategy of all for the past three years has been to simply close your eyes and buy EVERYTHING and then forget about it. It really has been the perfect idiot’s market.

This isn’t supposed to happen.

Stocks, bonds, real estate, and gold are NEVER supposed to be going all in the same direction at the same time. The only time you see this is when the government is flooding the financial system with liquidity to artificially boost asset prices.

This latest liquidity wave started when the 2017 Trump tax bill initiated enormous government budget deficits from the get-go. It accelerated when the Federal Reserve backed off of quantitative tightening in mid-2019.

Then it really blew up to tidal wave proportions with the Fed liquidity explosion simultaneously on all fronts with the onset of the US Corona epidemic.

Asset classes have been going ballistic ever since.

From the March 23 bottom, NASDAQ is up an astounding 78%, bonds have gained an unprecedented 30%, the US Homebuilders ETF has rocketed a stagging 187%, and gold has picked up an eye-popping 26%.

That’s all well and good if you happen to be long these asset classes, as we have been advising clients for the past several months.

So, what happens next? After all, we are in the “What happens next?” business.

What if one of the charts starts to go the other way? Is gold a good hedge? Do bonds offer downside protection? Is there safety in home ownership?

Nope.

They all go down in unison, probably much faster than they went up. If fact, such a reversal may be only weeks or months away. If you live by the sword you die, by the sword.

Assets are now so dependent on excess liquidity that any threat to that liquidity could trigger a selloff of Biblical proportion, possibly worse than what we saw during February-March this year.

And you wouldn’t need simply a sudden tightening of liquidity to prompt such a debacle. A mere slowdown in the addition of new liquidity could bring Armageddon. The Fed in effect has turned all financial markets into a giant Ponzi scheme. The second they quit buying, they all crash.

The Fed and the US Treasury have already started executing this retreat surreptitiously through the back door. Some Treasury emergency loan programs were announced with a lot of fanfare but have yet to be drawn down in size because the standards are too tight.

The Fed has similarly shouted from the rooftops that they would be buying equity convertible bonds and ETFs but have yet to do so in any meaningful way.

If there is one saving grace for this bull market, it's that it may get a second lease on life with a new Biden administration. Now that the precedent for unlimited deficit spending has been set by Trump, it isn’t going to slow down anytime soon under the Democrats. It will simply get redirected.

One of the amazing things about the current administration is that they never launched a massive CCC type jobs program to employ millions in public works as Roosevelt did during the 1930s to end that Great Depression. Instead, they simply mailed out checks. Even my kids got checks, as they file their own tax returns to get a lower tax rate than mine.

I think you can count on Biden to move ahead with these kinds of bold, expansionist ideas to the benefit of the nation. We are still enjoying enormously the last round of such spending 85 years ago, the High Sierra trails I hiked weeks ago among them.

Stocks soared on plasma hopes. Trumps cited “political” reasons at the FDA for the extended delay. Scientists were holding back approval for fears plasma was either completely useless and would waste huge amounts of money or would kill off thousands of people. At best, plasma marginally reduces death rates for those already infected, but you’re that one it’s worth it. Anything that kills Covid-19 is great for stocks.

Existing Home Sales were up the most in history in July, gaining a staggering 24.7% to 5.86 million units. Bidding wars are rampant in the suburbs. Investors are back in too, accounting for 15% of sales. Inventories drop 21% to only 3.1 months. These are bubble type statistics. Can’t hold those Millennials back! This will be a lead sector in the market for the next decade. Buy homebuilders on dips.

Goldman said a quarter of job losses are permanent, as the economy is evolving so fast. Many of these jobs were on their way out before the pandemic. That could be good news for investors as those cost cuts are permanent, boosting profits. At least, that’s what stocks believe.

Hedge funds still love big tech, even though they are now at the 99th percentile of historic valuation ranges. Online financials, banks, and credit card processors also rank highly. Live by the sword, die by the sword.

Massive Zoom crash brought the world to a halt for two hours on Monday morning. It looked like a Chinese hack attack intended to delay online school opening of the new academic year. Unfortunately, it also delayed the start of the Mad Hedge Traders & Investors Summit.

The Dow Rebalancing is huge. Dow Jones rarely rejiggers the makeup of its famed but outdated index. But changing three names at once is unprecedented. One, Amgen (AMGN) I helped found, working on the team the discovered its original DNA sequencing. All of the founding investors departed yonks ago. The departure of Exxon (XOM) is a recognition that oil is a dying business and that the future is with Salesforce (CRM), whose management I know well. One big victim is Apple (AAPL) whose weighting in the index has shrunk.

The end of the airline industry has begun, with American (AAL) announcing 19,000 layoffs in October. That will bring to 40,000 job losses since the pandemic began. The industry will eventually shrink to a handful of government subsidized firms and some niche players. Avoid like a plat in a spiral dive.

30 million to be evicted in the coming months, as an additional stimulus bill stalls in Congress. It will no doubt be rolling evictions that stretch out over the next year. This will be the true cost of failing to deal with the virus.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch suffered one of the worst weeks of the year, giving up most of its substantial August performance. If you trade for 50 years, occasionally you get a week like this. The good news is that it only takes us back to unchanged on the month.

Longs in banks (JPM) and gold (GLD) and shorts in Facebook (FB) and bonds (TLT) held up fine, but we paid through the nose with shorts in Apple (AAPL), Amazon (AMZN), and Tesla (TSLA).

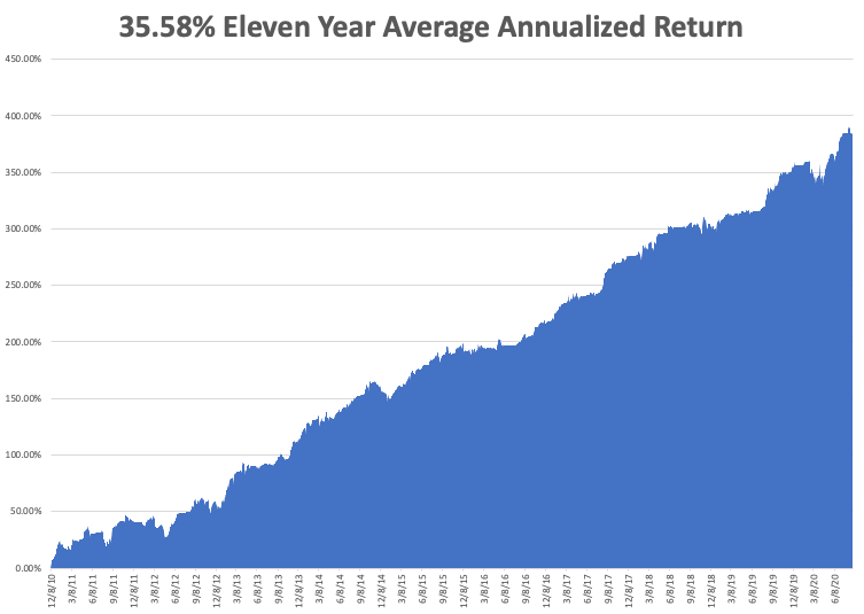

That takes our 2020 year to date down to 26.56%, versus +0.05% for the Dow Average. That takes my eleven-year average annualized performance back to 35.58%. My 11-year total return retreated to 382.47%.

It is jobs week so we can expect a lot of fireworks on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, August 31 at 10:30 AM EST, the Dallas Fed Manufacturing Index for August is released.

On Tuesday, September 1 at 9:45 AM EST, the Markit Manufacturing Index for August is published.

On Wednesday, September 2, at 8:13 AM EST, the August ADP Employment Change Index for private-sector job is printed.

At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, September 3 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, September 4, at 8:30 AM EST, The August Nonfarm Payroll Report is released.

At 2:00 PM The Bakers Hughes Rig Count is released.

As for me, I’ll be catching up on my sleep after hosting 27 speakers from seven countries and entertaining a global audience of 10,000 from over 50 countries and all 50 US states. We managed to max out Zoom’s global conferencing software, and I am now one of their largest clients.

It was great catching up with old trading buddies from decades past to connect with the up-and-coming stars.

Questions were coming in hot and heavy from South Africa, Singapore, all five Australian states, the Persian Gulf States, Saudi Arabia, East Africa, and every corner of the United Kingdom. And I was handling it all from my simple $2,000 Apple laptop from nearby Silicon Valley.

It is so amazing to have lived to see the future!

To selectively listen to videos of any of the many talented speakers, you can click here.

See you there.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 27, 2020

Fiat Lux

Featured Trade:

(WHY YOU MISSED THE TECHNOLOGY BOOM AND WHAT TO DO ABOUT IT NOW),

(AAPL), (AMZN), (MSFT), (NVDA), (TSLA), (WFC), (FB)

I often review the portfolios of new subscribers looking for fundamental flaws in their investment approach and it is not unusual for me to find some real disasters.

The Armageddon scenario was quite popular a decade ago. You know, the philosophy that said that the Dow ($INDU) was plunging to 3,000, the US government would default on its debt (TLT), and gold (GLD) was rocketing to $50,000 an ounce?

Those who stuck with the deeply flawed analysis that justified those conclusions saw their retirement funds turn to ashes.

Traditional value investors also fell into a trap. By focusing only on stocks with bargain-basement earnings multiples, low price to book values, and high visible cash flows, they shut themselves out of technology stocks, far and away the fastest growing sector of the economy.

If they are lucky, they picked up shares in Apple a few years ago when the earnings multiple was still down at ten. But even the Giant of Cupertino hasn’t been that cheap for years.

And here is the problem. Tech stocks defy analysis because traditional valuation measures don’t apply to them.

Let’s start with the easiest metric of all, that of sales. How do you measure the value of sales when a company gives away most of its services for free?

Take Google (GOOG) for example. I bet you all use it. How many of you have actually paid money to Google to use their search function? I would venture none.

What would you pay Google for search if you had to? What is it worth to you to have an instant global search function? Probably at least $100 a year. With 70% of the global search market comprising 2 billion users that means $140 billion a year of potential Google revenues are invisible.

Yes, the company makes a chunk of this back by charging advertisers access to these search users, generating some $38.94 Billion in revenues and $9.95 billion in net income in the most recent quarter. It would have been an $8.2 billion profit without the outrageous $5 billion fine from the European Community.

But much of the increased value of this company is passed on to shareholders not through rising profits or dividend payments but through an ever-rising share price. If you’re looking for dividends, Google doesn’t exist. It is also very convenient that unrealized capital gains are tax-free until the shares are sold.

I’ll tell you another valuation measure that investors have completely missed, that of community. The most successful companies don’t have just customers who buy stuff, they have a community of members who actively participate in a common vision, which is then monetized. There are countless communities out there now making fortunes, you just have to know how to spot them.

Facebook (FB) has created the largest community of people who are willing to share personal information. This permits the creation of affinity groups centered around specific interests, from your local kids’ school activities to municipality emergency alerts, to your preferred political party.

This creates a gigantic network effect that increases the value of Facebook. Each person who joins (FB) makes it worth more, raising the value of the shares, even though they haven’t paid it a penny. Again, it’s advertisers who are footing your tab.

Tesla (TSLA) has 400,000 customers willing to lend it $400 billion for free in the form of deposits on future car purchases because they also share in the vision of a carbon-free economy. When you add together the costs of initial purchase, fuel, and maintenance savings, a new Tesla Model 3 is now cheaper than a conventional gasoline-powered car over its entire life.

REI, a privately held company, actively cultivates buyers of outdoor equipment, teaches them how to use it, then organizes trips. It will then pursue you to the ends of the earth with seasonal discount sales. Whole Foods (WFC), now owned by Amazon (AMZN), does the same in the healthy eating field.

If you spend a lot of your free time in these two stores, as I do, The United States is composed entirely of healthy, athletic, good looking, and long-lived people.

There is another company you know well that has grown mightily thanks to the community effect. That would be the Diary of a Mad Hedge Fund Trader, one of the fastest growing online financial services firms of the past decade.

We have succeeded not because we are good at selling newsletters, but because we have built a global community of like-minded investors with a common shared vision around the world, that of making money through astute trading and investment.

We produce daily research services covering global financial markets, like Global Trading Dispatch and the Mad Hedge Technology Letter. We teach you how to monetize this information with our books like Stocks to Buy for the Coming Roaring Twenties and the Mad Hedge Options Training Course.

We then urge you to action with our Trade Alerts. If you want more hands-on support, you can upgrade to the Concierge Service. You can also meet me in person to discuss your personal portfolios at my Global Strategy Luncheons.

The luncheons are great because long term Mad Hedge veterans trade notes on how best to use the service and inform me on where to make improvements. It’s a blast.

The letter is self-correcting. When we make a mistake, readers let us know in 60 seconds and we can shoot out a correction immediately. The services evolve on a daily basis.

It all comes together to enable customers to make up to 50% to 60% a year on their retirement funds. And guess what? The more money they make, the more products and services they buy from me. This is why I have so many followers who have been with me for a decade or more. And some of my best ideas come from my own subscribers.

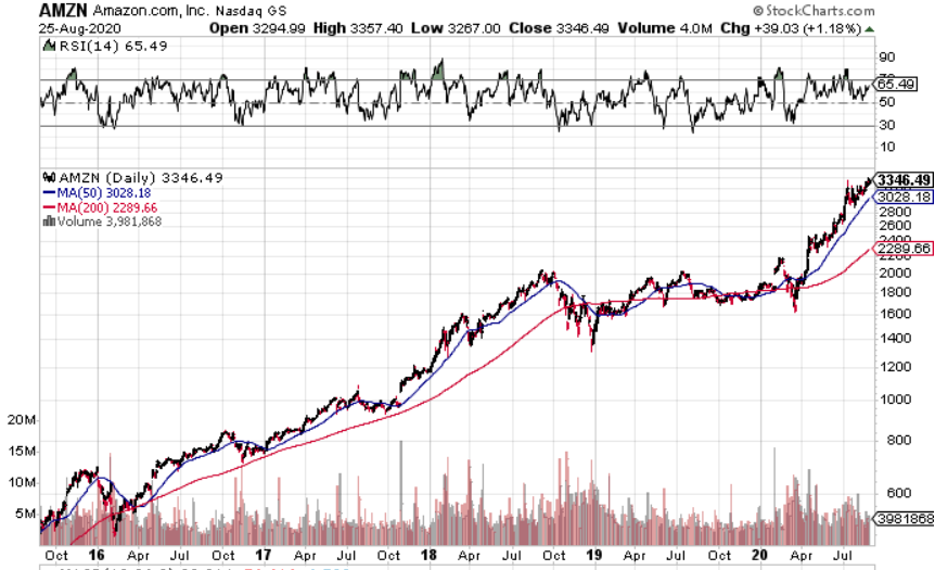

So, if you missed technology now, what should you do about it? Recognize what the new game is and get involved. Microsoft (MSFT) with the fastest-growing cloud business offers good value here. Amazon looks like it will eventually hit my $3,000 target. You want to be buying graphics card and AI company NVIDIA (NVDA) on every 10% dip.

You can buy the breakouts now to get involved, or patiently wait until the 10% selloff that usually follows blowout quarterly earnings.

My guess is that tech stocks still have to double in value before their market capitalization of 26% matches their 50% share of US profits. And the technologies are ever hyper-accelerating. That leaves a lot of upside even for the new entrants.

Mad Hedge Technology Letter

August 26, 2020

Fiat Lux

Featured Trade:

(THE EMPTY PIPELINE OF TECH INNOVATION)

(AAPL), (FB), (AMZN), (GOOGL), (NFLX), (TSLA), (SNAP), (MSFT), (ORCL), (TWTR)

The oligarchical regime of Northern Californian tech companies stopped innovating because they don’t have to.

When you have a monopoly – you have one objective – to crush anything that remotely resembles competition.

That has been happening for years now by the Silicon Valley oligarchs and the government still hasn’t taken their finger out to do much about it.

Honestly, my bet is that most of U.S. Congress own stock portfolios and these portfolios are spearheaded by the likes of Apple (AAPL), Facebook (FB), Amazon (AMZN), Google (GOOGL), Netflix (NFLX), and possibly even Tesla (TSLA), if they want a little growth.

It’s a direct conflict of interest, but that's not surprising for politics in 2020, is it?

The government likes to jawbone to the public saying they will make competition a level playing field, but actions show they are doing the opposite.

The Silicon Valley oligarchs are whispering in the ear of Congress and they listen.

Who would want Congress to lose money in their retirement portfolios, right?

Well, what now?

Fast forward to the future - mid-September, TikTok — the Chinese-owned, video-sharing phenomenon — MUST sell its U.S. operations.

Given the app’s 100 million U.S. users, this forced divestment by President Trump has triggered a delirious auction now pitting tech giants Microsoft (MSFT), Oracle (ORCL), and Twitter (TWTR) against one another.

The White House and Big Tech are boiling the free for all down to a combined story of national security and opportunistic capitalism amid unfortunate geopolitical tension between the U.S. and China.

But the ultimatum to ByteDance, TikTok’s owner, is more accurately understood as a dark window into Silicon Valley’s utter failure to innovate, and a warning signal of its transformation into a mere protector of long-established turf.

Silicon Valley has long adhered to the motto, “Move fast and break things” – but that was long ago when Steve Jobs was busy making the first iPhone.

The truth is Silicon Valley couldn’t be more corporate than it is now, and they use the corporate machine to serve the ends they desire.

Big Tech is just in love with buybacks like the rest of corporate America and the only reason they avoid it now is to appear as if they are in tune with public discourse and not tone deaf.

Huawei, another punching bag of the Trump administration’s tech war with China, best foreshadowed the optics.

In remarks to reporters in March 2019, Chinese politician Guo Ping said, “The U.S. government has a loser’s attitude. They want to smear Huawei because they can’t compete with us.”

ByteDance produced the hottest new social media platform on a global scale, and Facebook, in typical fashion, responded by brazenly copying TikTok, adding a feature called Reels to Instagram.

Don’t forget that Mark Zuckerberg has been attempting to destroy Snapchat (SNAP) for years after CEO Evan Spiegel refused to sell it to Zuckerberg.

The rest of the tech ecosphere has turned a blind eye to the anti-trust violations because they don’t want to be the next takeout target.

Make no bones about it, Silicon Valley, with the help of the Trump administration, is about to do a smash and grab job on China’s best tech growth asset.

This cunning maneuver alone has the knock-on effect of not only extending the tech rally in U.S. public markets but increasing the scarcity value and emboldening the Silicon Valley oligarchs.

I’m all about good deals and robbing Chinese tech in broad daylight is overwhelmingly bullish for the U.S. tech sector.

Imagine adding another Instagram to the appendage of an already mammoth tech company.

So why innovate? Why deploy capital into research and development when you can just nick a foreign company's crown jewel?

Even if you hate Silicon Valley at a personal level, it is literally impossible to short them, and now they are resorting to stealing companies, what other passes will government, society, and corporate America give American tech?

In either case, it’s not for me to judge, and as a technology analyst - I am bullish U.S. tech.

Global Market Comments

August 24, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ON FIRE EVERYWHERE)

(INDU), (JPM), (GLD), (GDX), (GOLD), (FB),

(TLT), (AAPL), (AMZN), (TSLA)

I am no longer able to breathe. The pandemic demands that I wear a mask. The wildfires prevent me from going outside, as the air is so heavy from smoke.

So, I decided to flee the San Francisco Bay Area south to Big Sir for a couple of days to catch up on my writing. On the way, I passed dozens of sadly abandoned schools as the pandemic has moved all of California to online distance learning.

By the second day, I was surrounded by fire. At an afternoon wine tasting, I tipped the waiter to hurry up as my glass was filling with ash and fire trucks were passing every five minutes.

By the next morning, I was surrounded by out-of-control wildfires and there was only one open road out of town. What really lit a fire under my behind was a text message from Tesla stating they would shut down charging at the Monterey station after 3:00 PM to help head off rolling blackouts.

The Golden State was not the only place on fire last week. Stocks were en flagrante as well, led by Tesla, Amazon, and Apple. The S&P 500 hit a new high for the year. It is the most concentrated market in history, with only 12 technology names accounting for 85% of the 2020 gains. Yet, 57% of shares are showing losses for 2020.

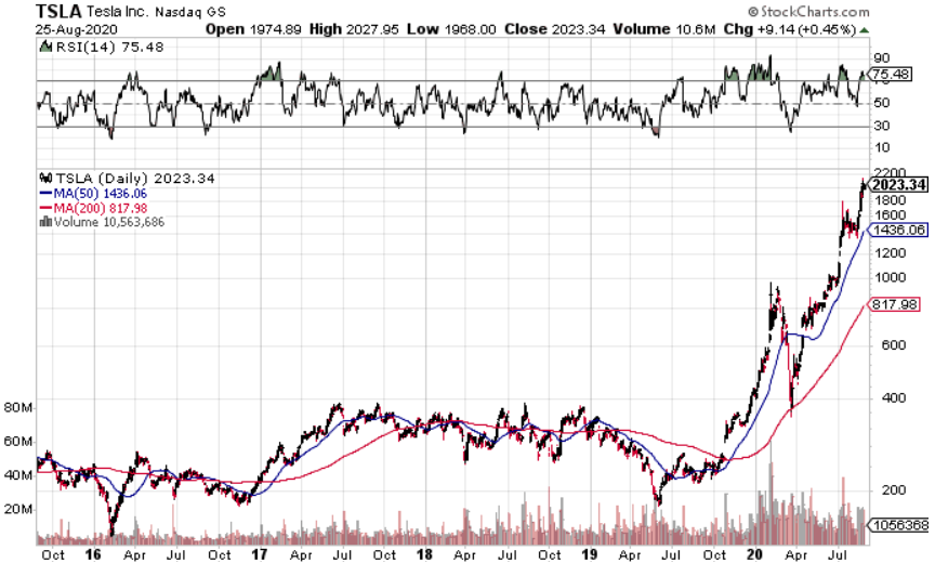

With a 33X multiple, Apple is pricing in only a 3% annual gain in the coming years. The price of Tesla at $2,100 a share is assuming the 2040 earnings have already arrived. We are firmly in bubble territory.

Having been in many bubbles over my half-century of trading, I can tell you they all have one thing in common. They run a lot longer than anyone imagines possible. In the meantime, traders, analysts, and investors are tearing their hair out wondering why they are so underweight stocks.

So trade if you must. But understand that the risk/reward here is terrible. You are better off here buying gold and banks and selling short US Treasury bonds and the US dollar.

Much has been made about share splits, which were the primary drivers of markets last week. However, the history of these things as that share prices fade shortly after the splits are completed. That was last Friday for Tesla and this Friday for Apple.

Apple may run a little longer, as it typically sees shares peak right after new generational cell phone launches, due in October.

Weekly Jobless Claims topped 1.1 million, ending a four-month downtrend. New Jersey, New York, and Texas were worst hit. Without further stimulus, they should continue to rise from here. These are Great Depression levels, and now massive layoffs from state and local governments are starting to kick in.

Apple topped $2 trillion in market cap. It is hard for those of us to believe it who bought the stock under $1 in 1998. It looks like more gains are to come. The coming 5G iPhone is going to market the peak in the shares this year, as new generational phones always do.

Uber and Lyft received a stay of execution, for 60 days, over whether they must treat drivers as full-time employees with benefits. Looks like I won’t have to take BART until October.

The U.S. Economy is falling back into the abyss. Last week’s total for new claims was well above the pre-pandemic Great Recession high of 665,000. Over 57.4 million Americans have now filed new unemployment insurance claims.

The airline industry is about to implode. With six months of operating at 20% capacity, how can they not? At least 75,000 in layoffs are imminent. Avoid the sector at all costs. You won’t recognize what comes out the other end. The next administration won’t be so generous to shareholders.

US Corona cases are slowing, even though we’ve just seen five consecutive days above 1,000 deaths. It’s the temporary ebb in the epidemic I was expecting that would rally the “recovery” stocks and sink the bond market. It’s sad, but we are celebrating suffering another 9/11 every three days instead of two.

Warren Buffet hates gold (GLD), but loves gold miners (GDX), loading the boat on Barrick Gold (GOLD) in Q2. It’s a rare move for the Oracle of Omaha into precious metals and the only way the cash flow king can collect a dividend in the sector. Warren seems to share my own long-term view on rising inflation caused by massive government bond issuance and spending.

U.S. Housing Starts mushroomed, surging 22.6% on the month to a seasonally adjusted annual rate of 1.496 million. Building permits also came in ahead of expectations, up 18.8% to 1.495m. Migration to the suburbs may explain some of the increase in activity but record-low mortgage rates and tight existing home inventory are the primary drivers. Soaring lumber prices mean growth in single-family starts will slow over the remainder of the year, not to mention the extra 0.50% fee on refinances.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch suffered one of the worst weeks of the year, giving up most of its substantial August performance. If you trade for 50 years, occasionally you get a week like this. The good news is that it only takes us back to unchanged on the month.

Longs in banks (JPM) and gold (GLD) and shorts in Facebook (FB) and bonds (TLT) held up fine, but we paid through the nose with shorts in Apple (AAPL), Amazon (AMZN), and Tesla (TSLA).

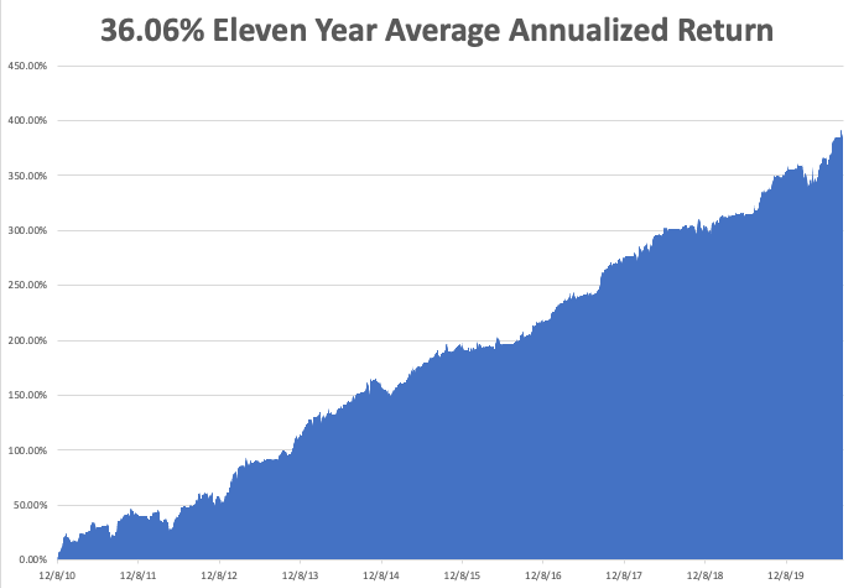

That takes our 2020 year to date down to 28.88%, versus -2.00% for the Dow Average. That takes my eleven-year average annualized performance back to 36.06%. My 11-year total return retreated to 384.79%.

It's a relatively low rent week on the data front. The only numbers that count for the market are the number of US Corona virus cases and deaths, which you can find here.

On Monday, August 24 at 8:30 AM EST, the Chicago Fed National Activity Index is out.

On Tuesday, August 25 at 9:00 AM EST, the S&P Case Shiller National Home Price Index for June is released.

On Wednesday, August 26, at 8:30 AM EST, Durable Goods for July are printed. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, August 27 at 8:30 AM EST, the Weekly Jobless Claims are announced. We also get the second estimate for Q2 GDP.

On Friday, August 28, at 8:30 AM EST, US Personal Spending is announced. At 2:00 PM, the Bakers Hughes Rig Count is released.

As for me, I am reading up on bios and generally preparing for my upcoming Mad Hedge Traders & Investors Summit, which I will be hosting for three days and starts on Monday morning at 9:00 AM EST. The attend please click here.

See you there.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

August 17, 2020

Fiat Lux

Featured Trade:

(U.S. STYMIES THE ADVANCEMENT OF FOREIGN BAD ACTORS)

(BABA), (AAPL), (IQ), (NFLX), (FB), (GOOGL), (AMZN)

Stay away from Chinese tech companies listed on the U.S. exchanges. I wouldn’t touch them with a 10-foot pole.

Not only are these firms unscrupulous, but the U.S. administration is specifically attacking them as a cornerstone campaign strategy as we close in on the November election.

The blitzkrieg has been increasing at a rapid clip with U.S. President Donald Trump banning social media asset TikTok and chat app WeChat.

Just in the last few hours, the U.S. administration has said they are also “looking at” going after Chinese eCommerce firm Alibaba (BABA) who is the Chinese Amazon.

If the trends continue, there could be no Chinese tech companies freely extracting American revenue by this November.

Things will only get worse.

No doubt the coronavirus fiasco has exacerbated tensions between the countries with both sides dealing with a plunging economy.

The only reason we do not hear about the depths of despair going on in the Chinese economy is because the media is suppressed there.

Chinese media is tightly controlled disabling any negative news that shines an unfavorable light on the Chinese communist party.

Then there is the immoral fraud aspect of Chinese tech companies as every mainland Chinese firm wishes to go public in New York because company financials are never audited, and they are immune from any criminal liability.

This is a recipe to enable reckless Chinese management who state opaque numbers in their financials in the hope that American investors will take the bait.

Another cheater has been unearthed by Wolfpack Research who along with Muddy Waters have made it their mission to root out the bad actors.

The supposed “Netflix (NFLX) of China” Chinese streaming service iQiyi (IQ) plunged in after-hours trade in the U.S. after it announced the Securities and Exchange Commission (SEC) has launched a probe into the company.

The case revolves around iQiyi falsifying their subscription numbers which everyone knows is the key to exhibiting growth in the company.

iQiyi said the SEC is “seeking the production of certain financial and operating records dating from January 1, 2018, as well as documents related to certain acquisitions and investments that were identified in a report issued by short-seller firm Wolfpack Research in April 2020.”

Wolfpack Research has accused iQiyi of inflating 2019 revenue by around 44%.

Wolfpack also said iQiyi artificially overexaggerated expenses among other data.

The SEC probe into iQiyi comes amid rising scrutiny on U.S.-listed Chinese companies following the Luckin Coffee debacle in which they committed the same act of falsifying numbers.

This copycat crime is clearly seen as a big winner in Mainland China encouraging a slew of companies to decide on the same strategy.

The Coffee company admitted to fabricating sales numbers for 2019. The company was subsequently delisted from the Nasdaq in June.

China and its tech firms are one of the few bipartisan issues with strong support from both sides of the aisle and I can only see the temperature in the kitchen getting hotter.

The side effect of purging the Chinese tech out of the U.S. is that it bolsters the investor case for American tech.

Not that they needed help in the first place.

If the government won’t allow foreign companies to compete with Silicon Valley, then the monopolies built by the likes of Apple (AAPL), Facebook (FB), Google (GOOGL), and Amazon (AMZN) will feel protected because of the government effectively widening their moats.

One might argue that the crimes these American companies have committed are just as bad as the Chinese firms, but they get a free pass for being American.

Remember this is the age of de-globalization with national governments protecting national companies and not the other way around.

Silicon Valley companies have tried to pervert the U.S. employment situation by maneuvering around U.S. nationals by applying for the foreign HB-1 visas in droves and underpaying mostly Chinese and Indian nationals to work for the likes of Google and Facebook.

We can’t say these Silicon Valley companies are saints. They certainly are not, but that doesn’t matter in today’s climate when government, billionaires, and tech moguls are assumed as scum from the get-go.

Then there is the personal data issue that can’t be said to be much better than what the Chinese companies are doing.

The double standard is not surprising, and a heavy dose of politics has been injected into the global tech ecosphere to the detriment of cross border trade.

In the fog of war, this is why I have largely focused on U.S. software companies with subscription revenue because it offers more visibility than an unstable revenue model like Uber or Lyft.

In any case, nobody can blame the U.S. government for going this route since, after all, Facebook, Google, Amazon, and Netflix are all banned in China as well.

You don’t see U.S. tech companies trading on the Shenzhen tech index for a reason and after this monster run-up from the March nadir, it’s obvious why Chinese tech firms want to keep that funnel to U.S. investor capital clear.

This series of events that effectively coddles American big tech will insulate them from any real share weakness. The trend is your friend and I am bullish on American big tech.