Global Market Comments

March 25, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR GAME CHANGER)

(SPY), (TLT), (BIIB), (GOOG), (BA), (AAPL), (VIX), (USO)

Global Market Comments

March 25, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR GAME CHANGER)

(SPY), (TLT), (BIIB), (GOOG), (BA), (AAPL), (VIX), (USO)

“When the facts change, I change. What do you do sir?” is a famous quote from the great economist John Maynard Keynes which I keep taped to the top of my monitor and constantly refer to.

The facts certainly changed on Wednesday when the Federal Reserve announced a change in the facts for the ages. Not only did governor Jay Powell announce that there would be no further rate increases in 2019.

He also indicated that the Fed would end its balance sheet unwind much earlier than expected. That has the effect of injecting $2.7 trillion into the US financial system and is the equivalent of two surprise interest rate CUTS.

The shocking move opens the way for stocks to trade up to new all-time high, with or without a China trade deal. Only the resumption of all-out hostilities, like the imposition of new across the board 25% tariffs, would pee on this parade.

As if we didn’t have enough to discount into the market in one shot. I held publication of this letter until Sunday night when we could learn more about the conclusion of the Mueller Report. There was no collusion with Russia and there will be no obstruction of justice prosecution.

However, the report did not end the president’s legal woes as it opened up a dozen new lines of investigation that will go on for years. The market could care less.

At the beginning of the year, I listed my “Five Surprises for 2019”. They were:

*The government shutdown ended and the Fed makes no move to raise interest rates

*The Chinese trade war ends

*The US makes no moves to impeach the Trump, focusing on domestic issues instead

*Britain votes to rejoin Europe

*The Mueller investigation concludes that he has an unpaid parking ticket in

NY from 1974 and that’s it

Notice that three of five predictions listed in red have already come true and the remaining two could transpire in coming weeks or months. All of the above are HUGELY risk positive and have triggered a MONSTER Global STOCK RALLY

Make hay while the sun shines because what always follows a higher high? A lower low.

The Fed eased again by cutting short their balance sheet unwind and ending quantitative tightening early. It amounts to two surprise interest rate cuts and is hugely “RISK ON”. New highs in stocks beckon. This is a game changer.

Bonds soared and rates crashed taking ten-year US Treasury bond yields down to an eye-popping 2.42%, still reacting to the Wednesday Fed comments. This is the final nail in the bond bear market as global quantitative easing comes back with a vengeance. German ten years bonds turn negative for the first time since 2016.

Interest rates inverted with short term rates higher than long term ones for the first time since 2008. That means a recession starts in a year and the stock market starts discounting that in three months.

Interest rates are now the big driver and everything else like the economy, valuations, and earnings are meaningless. Foreign interest rates falling faster than ours making US assets the most attractive in the world. BUY EVERYTHING, including stocks AND bonds.

Biogen blew up canceling their phase three trials for the Alzheimer drug Aducanumab. This is the worst-case scenario for a biotech drug and the stock is down a staggering 30%. Some $12 billion in prospective income is down the toilet. Avoid (BIIB) until the dust settles.

Europe fined Google $1.7 billion, in the third major penalty in three years. Clearly, there’s a “not invented here” mentality going on. It's sofa change to the giant search company. Buy (GOOG) on the dip.

More headaches for Boeing came down the pike. What can go wrong with a company that has grounded its largest selling product? Answer: they get criminally prosecuted. That was the unhappy news that hit Boeing (BA), knocking another $7 off the shares. It can’t get any worse than this, can it? Buy this dip in (BA).

Indonesia canceled a massive 737 order for 49 planes, slapping the stock on the face for $9. Apparently, they are unwilling to wait for the software fix. Buy the dip in (BA).

Oil prices hit a new four-month high at $58 a barrel as OPEC production caps work and Venezuela melts down. At a certain point, high energy prices are going to hurt the economy. Buy (USO) on dips.

The CBOE suspended bitcoin futures due to low volume and weak demand. It could be a fatal blow for the troubled cryptocurrency. Avoid bitcoin and all other cryptos. They’re a Ponzi scheme.

Equity weightings hit a 2 ½ year low as professional institutional money managers sell into the rally. They are overweight long defensive REITs and short European stocks. Watch out for the reversal.

December stock sellers are now March buyers. Expect this to lead to a higher high, then a lower low. Volatility is coiling. Don’t forget to sit down when the music stops playing.

Volatility hits a six-month low with the $12 handle revisited once again down from $30. (VIX) could get back to $9 before this is all over. Avoid (VIX) as the time decay will kill you.

Weak factory orders crush the market, down 450 points at the low. Terrible economic data is not new these days. But it ain’t over yet. Buy the dip.

The Mad Hedge Fund Trader was up slightly on the week. That’s fine, given the horrific 450 point meltdown the market suffered on Friday. We might have closed unchanged on the day but for rumors that the Mueller Report would be imminently released.

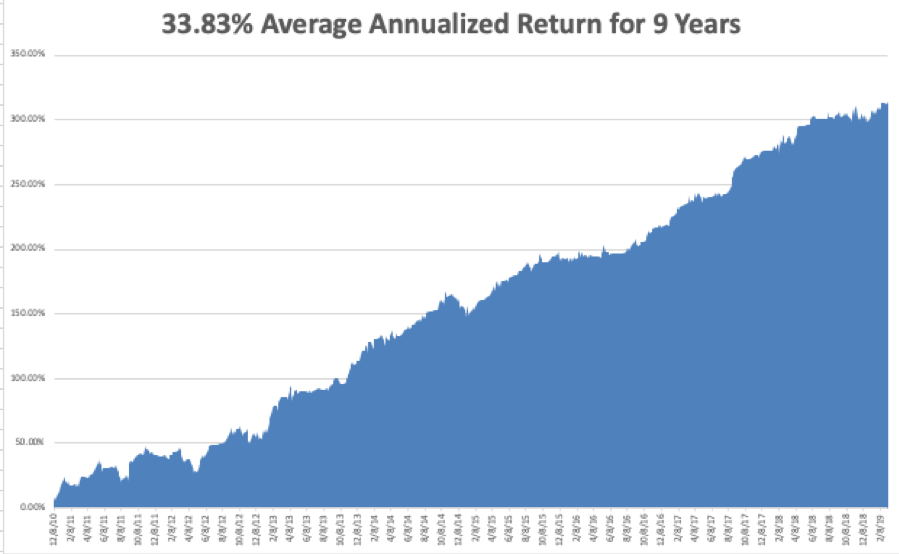

March is still negative, down -1.54%. My 2019 year to date return retreated to +11.74%, boosting my trailing one-year return back up to +24.86%.

My nine-year return recovered to +311.88%. The average annualized return appreciated to +33.71%. I am now 40% in cash, 40% long and 20% short, and my entire portfolio expires at the April 18 option expiration day in 14 trading days.

The Mad Hedge Technology Letter used the weakness to scale back into positions in Microsoft (MSFT), Alphabet (GOOGL), and PayPal (PYPL), which are clearly going to new highs.

The coming week will be a big one for data from the real estate industry.

On Monday, March 25, Apple will take another great leap into services, probably announcing a new video streaming service to compete with Netflix and Walt Disney.

On Tuesday, March 26, 9:00 AM EST, we get a new Case Shiller CoreLogic National Home Price index which will almost certainly show a decline.

On Wednesday, March 27 at 8:30 AM, we get new Trade Deficit figures for January which have lately become a big deal.

Thursday, March 28 at 8:30 AM EST, the Weekly Jobless Claims are announced. We also then get another revision for Q4 GDP which will likely come down.

On Friday, March 29 at 10:00 AM, we get February New Home Sales. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’m praying that it stops snowing in the High Sierras long enough for me to get over Donner Pass and spend the spring at Lake Tahoe. We are at 50 feet for the season, the second highest on record.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

March 25, 2019

Fiat Lux

Featured Trade:

(APPLE’S BIG PUSH INTO SERVICES)

(AAPL), (GS), (NFLX), (GOOGL), (ROKU)

The future of Apple (AAPL) has arrived.

Apple has endured a tumultuous last six months, but the company and the stock have turned the page on the back of the anticipation of the new Apple streaming service that Apple plans to introduce next week at an Apple event.

The company also recently announced a partnership with Goldman Sachs (GS) to launch an Apple-branded credit card.

In the deal, Goldman Sachs will pay Apple for each consumer credit card that is issued.

These new initiatives indicate that Apple is doing its utmost to wean itself from hardware sales.

Effectively, Apple's over-reliance on hardware sales was the reason for its catastrophic winter of 2018 when Apple shares fell off a cliff trending lower by almost 35%.

This new Apple is finally here to save the day and will demonstrate the high-quality of engineering the company possesses to roll out such a momentous service.

Frankly speaking, Apple needs this badly.

They were awkwardly wrong-footed when Chinese consumers in unison stopped buying iPhones destroying sales targets that heaped bad news onto a bad situation.

I never thought that Apple could pivot this quickly.

Apple's move into online streaming has huge ramifications to competing companies such as Roku (ROKU).

In 2018, I was an unmitigated bull on this streaming platform that aggregates online streaming channels such a Sling TV, Hulu, Netflix and charges digital advertisers to promote their products on the platform through digital ads.

I believe this trade is no more and Roku will be negatively impacted by Apple’s ambitious move into online streaming.

What we do know about the service is that channels such as Starz and HBO will be subscription-based channels that device owners will need to pay a monthly fee and Apple will collect an affiliate commission on these sales.

Apple needs to supplement its original content strategy with periphery deals because Apple just doesn’t have the volume to offer consumers a comprehensive streaming product like Netflix.

Only $1 billion on original content has been spent, and this content will be free for device owners who have Apple IDs.

Apple's original content budget is 1/9 of Netflix annual original content budget.

My guess is that Apple wants to take stock of the streaming product on a smaller scale, run the data analytics and make some tough strategic decisions before launching this service in a full-blown way.

It's easier to clean up a $1 billion mess than a $9 billion mess, but knowing Apple and its hallmarks of precise execution, I'd be shocked if they make a boondoggle out of this.

Transforming the company from a hardware to a software company will be the long-lasting legacy of Tim Cook.

The first stage of implementation will see Apple seeking for a mainstay show that can ingrain the service into the public's consciousness.

Netflix was a great example, showing that hit shows such as House of Cards can make or break an ecosystem and keep it extremely sticky ensuring viewers will stay inside a walled pay garden.

Apple hopes to convince traditional media giants such as the Wall Street Journal to place content on Apple's platform, but there has already been blowback from companies like the New York Times who referenced Netflix’s demolition of traditional video content as a crucial reason to avoid placing original content on big tech platforms.

Netflix understands how they blew up other media companies and don’t expect them to be on Apple’s streaming service.

They wouldn’t be caught dead on it.

Tim Cook will have to run this race without the wind of Netflix’s sails at their back.

Netflix has great content, and that content will never leave the Netflix platform come hell or high water.

Apple is just starting with a $1 billion content budget, but I believe that will mushroom between $4 to $5 billion next year, and double again in 2021 to take advantage of the positive network effect.

Apple has every incentive to manufacture original content if third-party original content is not willing to place content on Apple's platform due to fear of cannibalization or loss of control.

Ultimately, Apple is up against Netflix in the long run and Apple has a serious shot at competing because of the embedment of 1 billion users already inside of Apple's iOS ecosystem that can easily be converted into Apple streaming service customers.

If you haven't noticed lately, Silicon Valley's big tech companies are all migrating into service-related SaaS products with Alphabet (GOOGL) announcing a new gaming product that will bypass traditional consoles and operate through the Google Chrome browser.

Even Walmart (WMT) announced its own solution to gaming with a new cloud-based gaming service.

I envision Apple traversing into the gaming environment too and using this new streaming service as a fulcrum to launch this gaming product on Apple TV in the future.

The big just keep getting bigger and are nimble enough to go where internet users spend their time and money whether it's sports, gaming, or shopping.

Apple is no longer the iPhone company.

I have said numerous times that Apple's pivot to software was about a year too late.

The announcement next week would have been more conducive to supporting Apple’s stock price if it was announced the same time last year, but better late than never.

Moving forward, Apple shares should be a great buy and hold investment vehicle.

Expect many more cloud-based services under the umbrella of the Apple brand.

This is just the beginning.

Mad Hedge Technology Letter

March 19, 2019

Fiat Lux

Featured Trade:

(GOOGLE’S AGGRESSIVE MOVE INTO GAMING),

(GOOGL), (AAPL), (FB), (NFLX), (MSFT) (EA), (TTWO), (ATVI)

The saturation of tech is upon us.

That is the takeaway from Google’s (GOOGL) hard pivot into gaming.

The goal of their new gaming service is to become the Netflix (NFLX) of gaming allowing gamers to skip purchasing third-party consoles and playing games directly from an Android-based Google device.

Middlemen in the broad economy are getting killed and this is the beginning.

What we are really seeing is a last-ditch effort to protect gaming consoles - these devices will become extinct in less than 20 years boding ill for companies such as Sony and Nintendo

The cloud is still all the rage and companies such as Microsoft (MSFT), Alphabet (GOOGL), and Apple (AAPL) have the natural infrastructure in place to offer cloud-based gaming solutions.

Phenomenon such as internet game Fortnite have shown that consoles are outdated and relying on the cloud as a fulcrum to extract gaming revenue by way of add-ons and in-game enhancements will be the way forward

Another key takeaway from this development is that passive investment is dead, even more so in tech, where these big tech companies are starting to bleed over into each other's territory.

This dispersion will create opportunity and pockets of weakness.

I blame this on a lack of innovation with companies still trying to extract as much as they can from the current smartphone-based status quo which has pretty much run its course.

Technology is itching for something revolutionary and we still have no idea what that new idea or device will be.

The rollout of 5G is promising and companies will need some time to adapt to this super-fast connection speed.

In either case, I can tell you the revolution won’t include foldable smartphones.

In 2018, the gaming industry flourished on accelerating momentum by registering over $136 billion in sales, and the revenue growth rate is already about 15% and increasing.

Naturally, companies such as Amazon and Google want a piece of this action and are hellbent on making inroads in the gaming environment such as Amazon's ownership of Twitch, which is a game streaming service where viewers can watch live tournament-style competitions proving extremely popular with Generation Z.

I applaud this move by Google because they already have proved they can execute on certain mature assets such as YouTube which has become the Netflix replacement of 2019.

Doubling down in the gaming sector would be a bonus as they search a second accelerating revenue driver that will dovetail nicely with the overperformance in YouTube this year.

It’s even possible that YouTube could be modified to support live stream gaming, certainly various synergistic dynamics are at play here.

Even if they fail - it's worth the risk.

Revenue extraction will be painful for certain companies like Facebook (FB) in this new environment, who has seen a horde of top executives abort after the company drastically changed directions, believing the company is on a suicide mission to fines and more regulatory penalties.

I've mentioned in the past that Facebook no longer commands the same type of employee brand recognition they once cultivated.

Facebook will find a tougher time to find the right people they need to execute their private chat plan, by linking the likes of WhatsApp, Instagram, and Facebook Messenger.

This is a high-risk high-reward proposition that could end up with Facebook's co-founder Mark Zuckerberg in tears if regulators give him the cold shoulder, and that is why many executives who are risk-adverse want to cash in now because they sink with the Titanic.

Not only are gaming assets becoming saturated, but the general online streaming environment is attracting a tsunami of supply all at one time.

Online content is already veering into the same type of pricing structures that cable offered traditional customers.

Investors will have to ask themselves, how much will the average consumer spend in content-based entertainment per month?

My guess is not more than $100 per month.

The saturation will cause tech companies to become even more draconian.

Be prepared for some more epic in-fighting until a new gateway of internet monetization opens up.

There has never been a better time to be a tactical and active investor in tech.

The Fang trade has splintered off with each company facing unpredictable futures.

Unearthing value will become more difficult because these traditional bellwether tech stocks have decoupled and aren't going straight up anymore.

Those zigs and zags will still be buttressed by a secular tailwind of the migration to digital, but there are certain winners and losers that will result of this.

Apple announcing a new streaming product is proof that these Silicon Valley tech firms are desperate for new profit drivers as the woodchips that fuel the fire start to run noticeably short on supply.

At the bare minimum, this looks disastrous for the traditional gaming companies of Electronic Arts (EA), Take-Two Interactive (TTWO), and Activision (ATVI) whose shares have been effectively shelved due to the Fortnite revolution.

EA has fought back with their own Fortnite lookalike called Apex Legends which showed a Fortnite-like trajectory sucking in 10 million players in the first 72 hours.

The stock exploded 16%, signaling this is the new way forward for gaming companies.

As a whole, these traditional gaming studios simply don’t have the firepower to compete with the big boys, let alone possess a strong cloud infrastructure.

Global Market Comments

March 18, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR A STIFF DOSE OF HUMILITY),

(FCX), (AAPL), (IWM), (SPY), (BA), (FXI), (FXB)

Sometimes markets have to give you a solid dose of humility, blindside you with a sucker punch, and slap you across the face with a wet kipper. Last week was definitely one of those weeks for me.

It was only just a matter of time before this happened. We posted new record gains for the first ten weeks of 2019. It was just a matter of time before the reality check kicked in.

I believed that we have seen the sharpest rally in stocks since the 2009 bottom, we were overdue for a respite. That respite came and only lasted a week. It has been an especially frustrating week for those few of us who watch economic data because it has been unremittingly awful while stocks rose daily.

There were really no reasons for shares to rise that week. There were also no reasons to sell, other than a dozen or so complete disasters that are looming just over the horizon. Still, to quote an old friend of mine, “Markets can remain irrational longer than you can remain liquid.”

The bull market reached ten years old last week, and if you read this letter you caught every dollar of the move up since then, plus some. But how much longer will it last? The technicals say it’s already in its death throes.

China trade negotiations (FXI) endlessly continued as they have for a year, but now the Chinese have thrown up a roadblock. They want everything in writing. In the wake of the North Korean disaster, can you blame them? This will weigh heavily on stocks until it's done.

Another day, another Brexit vote failed again. The pound (FXB) is doing the Watusi. Avoid all UK plays until the issue is decided.

The share buyback blackout started on Friday for many companies which are not allowed to repurchase their own shares up to 30 days ahead of the Q1 earnings reports. If you take the largest buyers of shares out of the market, what is left? Look to play the short side for the market.

Boeing (BA) hit bottom as the US became the last country to ban the 737 Max 8. Imagine being 35,000 feet in the air and you find out your plane is grounded for safety reasons, as 6,000 people did last week. Buy more (BA) on the dip. The next move is from $360 to $450.

Weekly Jobless Claims jumped, by 6,000 to a seasonally adjusted 229,000. Notice claims aren’t falling anymore. Another sign the tax cut stimulus is shrinking? Or that there is no one left to hire with any skills whatsoever?

Tesla (TSLA) released its Model Y SUV, but the cheaper $39,000 version won’t be available until 2021 and the stock dove. We are approaching the make or break level for the stock, the bottom of a two-year range. Get ready to buy on the meltdown. This is a ten bagger in a decade. Buy (TSLA).

The Mad Hedge Fund Trader lost ground last week. The tenth rally in 11 weeks made my short positions lose money faster than my long positions could make it back.

The Mad Hedge Technology Letter was stopped pit of a short position in Apple (AAPL) for a small loss a heartbreaking three days before its options expiration.

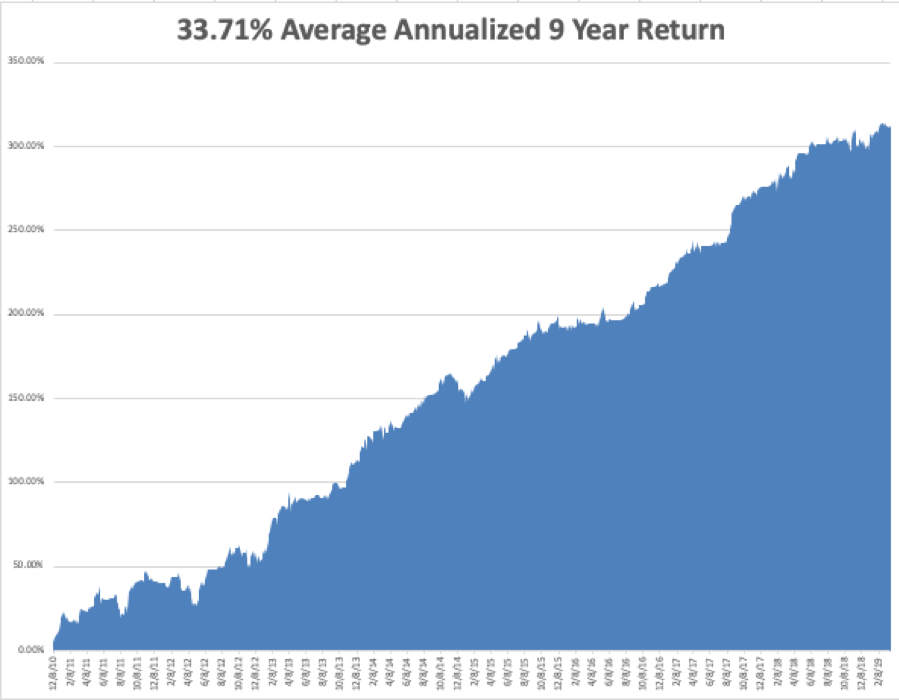

February came in at a hot +4.16% for the Mad Hedge Fund Trader. March started negative, down -2.18%.

My 2019 year to date return retreated to +11.46%, a new all-time high and boosting my trailing one-year return back up to +23.72%.

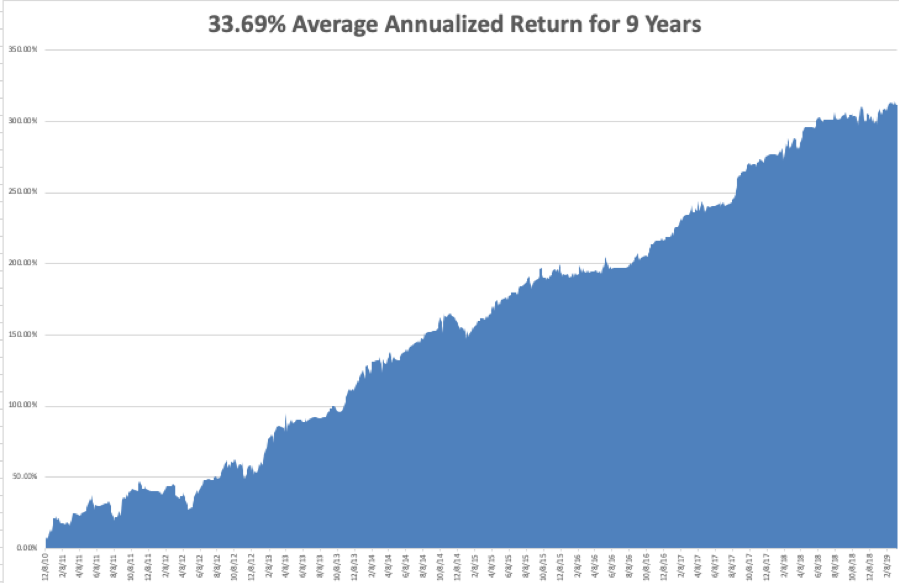

My nine-year return pared back to +311.60%. The average annualized return appreciated to +33.69%.

I am now 60% in cash, 20% long Freeport McMoRan (GLD), 10% short the S&P 500, and 10% short the Russell 2000. My short bond position (TLT) expired at its maximum profit point of $1,140.

As for the Mad Hedge Technology Letter, it covered its short in Apple (AAPL) for a small loss.

Q4 earnings reports are pretty much done, so the coming week will be pretty boring on the data front after last week's fireworks.

On Monday, March 18, at 10:00 AM EST, the March Homebuilders Index is out.

On Tuesday, March 19, 8:30 AM EST, February Housing Starts is published.

On Wednesday, March 20 is the first official day of Spring, at last!

Thursday, March 21 at 8:30 AM EST, the Weekly Jobless Claims are announced. At 10:00 AM, we get a new number for Leading Economic Indicators.

On Friday, March 22 we get a delayed number for Existing Home Sales.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, it’s fundraising time here in the San Francisco Bay Area for local schools and gala balls are now a weekly event. I, who have pursued a lifelong pursuit of low prices and great deals, ended up paying $1,000 for a homemade coffee cake, $7,000 for tickets to the Golden State Warriors, and $10,000 for the best table in the house. Hey, what’s the value of money if you can’t spend it? You can’t take it with you.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 8, 2019

Fiat Lux

Featured Trade:

(MARCH 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (SDS), (TLT), (TBT), (GE), (IYM),

(MSFT), (IWM), (AAPL), (ITB), (FCX), (FXE)

Well, that was some week!

After moving up in a straight line for ten weeks, markets are now doing their best impression of a Q4 repeat.

The transports Index (XTN), the most important leading indicator for markets, has been down for 11 straight days, the worst run in 40 years.

And now for the bad news.

Look at a long term chart for the S&P 500 (SPY) and the head and shoulder top practically leaps at you and grabs you by the lapels (that is, if you are one of the few who still wears a suit).

It makes you want to slit your wrist, jump off the nearest bridge, or binge watch all nine seasons of The Walking Dead. It neatly has the next bear market starting around say May 10 at 4:00 PM EST, a rollover point I put out two years ago.

However, hold that move! As long as we have a free Fed put under the market in the form of Jay Powell’s “patience’ policy, we are not going to have a major crash any time soon. That is 2021 business.

It's more likely we trade in a long sideways range until the economy finally rolls over and dies. So when we hit my first (SPY) downside target at the 50-day moving average at $269, which is a very convenient 5% down from the recent top, could well bounce hard and I might add some longs in the best quality names. It all sets of my dreaded flatline of death scenario for the rest of 2019.

Last week saw an unremitting onslaught of bad news from the economy.

The February Nonfarm Payroll report came in at a horrific 200,000 when 210,000 was expected, sending traders to man the lifeboats. The headline Unemployment Rate dropped 0.2% to 3.8%. Average Hourly Earnings spiked 11 cents to $27.66, a 3.4% YOY gain and the biggest pop since 2009.

Construction lost 31,000 jobs, while leisure and Hospitality added no jobs at all. The stunner is that the U6 long term structural “discouraged worker” unemployment rate dropped an amazing 0.8% to 7.4%, the sharpest drop on record. Fewer jobs, but at higher wages is the takeaway here, the exact opposite of what markets want to hear.

US Construction Spending fell off a cliff, down 0.6% in December. It seems that nobody wants to invest ahead of a recession.

The dollar soared (UUP), and gold (GLD) got hammered. You can blame the slightly stronger GDP print on Thursday the week before, which came in at 2.2% instead of 1.8%. As long as Jay doesn’t raise interest rates this is just a brief short covering rally for the buck.

China cut its growth forecast from 6.5% to 6.0% GDP growth for 2019. The trade war with the US and the stimulus hasn’t kicked in yet. The last time they did this, the market fell 1,000 points. Buy (FXI) on the dip.

US Trade Deficit hit ten-year high at $59.8 billion for December, and a staggering $419 billion for the year. It’s funny how foreigners stop buying your goods when you declare war on them. Even Teslas (TSLA) are being stopped at the border in China. Who knew?

New trade tariffs hit US consumers the hardest adding $69 billion to their annual bill. Falling real earnings and rising costs is hardly a sustainable model. Will someone please tell the president?

US growth is fading, says the Fed Beige Book, slowing to a “slight to moderate rate”. The government shutdown is the cause. With Europe already in recession, I’ll be using rallies to increase my shorts. Sell (SPY) and (IWM).

The European Central Bank axed its growth forecast sharply, from 1.7% to 1.1%. Stimulus to renew on all front, including more quantitative easing. It’s just a matter of time before their recession pulls the US down. Sell the Euro (FXE).

You lost $3.7 trillion in Q4, or so says the Fed about the decline of national personal net worth during the stock market crash, the sharpest decline in a decade. You’re now only worth $104.3 trillion.

The Mad Hedge Fund Trader actually gained ground last week, thanks to profits on our short positions rising more than our offsetting losses on our longs.

I have doubled up my overall positions, finally taking advantage of the rollover in all risk assets from a historic ten-week run to the upside. I added shorts in the S&P 500 (SPY) and the Russell 2000 (IWM) against a very deep in-the-money long in Freeport McMoRan (FCX) the world’s largest copper producer.

The thinking here is that with China the only economy in the world that is stimulating its economy and the planet’s largest copper consumer, copper makes a nice long side hedge against my short positions.

The Mad Hedge Technology Letter is happily running a short position is Apple (AAPL) which is now almost at its maximum profit point. We only have four days to run to expiration when the position we bought for $4.60 will be worth $5.00.

February came in at a hot +4.16% for the Mad Hedge Fund Trader. March started out negative, down -0.84%, thanks to a wicked stop loss on Gold (GLD). We had 80% of the maximum potential profit at one point but left the money on the table at the highs.

My 2019 year to date return ratcheted up to +12.84%, a new all-time high and boosting my trailing one-year return back up to +29.92%.

My nine-year return clawed its way up to +312.94%, another new high. The average annualized return appreciated to +33.83%.

I am now 50% in cash, 20% long Freeport McMoRan (FCX), and 10% short bonds (TLT), 10% short the S&P 500, and 10% short the Russell 2000.

We have managed to catch every major market trend this year, loading the boat with technology stocks at the beginning of January, selling short bonds, and buying gold (GLD). I am trying to avoid stocks until the China situation resolves itself one way or the other.

As for the Mad Hedge Technology Letter, it is short Apple (AAPL).

Q4 earnings reports are pretty much done, so the coming week will be pretty boring on the data front after last week's fireworks.

On Monday, March 11, at 8:30 AM EST, January Retail Sales is ut.

On Tuesday, March 12, 8:30 AM EST, the February Consumer Price Index is published.

On Wednesday, March 13 at 8:30 AM EST, the February Durable Goods is updated.

On Thursday, March 14 at 8:30 AM EST, we get Weekly Jobless Claims. These are followed by January New Home Sales.

On Friday, March 15 at 9:15 AM EST, February Industrial Production comes out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be headed to the De Young Museum of fine art in San Francisco to catch the twin exhibitions for Monet and Gaugin. When it rains every day of the week, there isn’t much to do but go cultural.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader