The whole digital ad industry dodged a bullet.

Facebook (FB) CEO Mark Zuckerberg's wizardry on Capitol Hill will stave off the data regulation hyenas for the time being.

One company in particular is perfectly placed to reap the benefits.

The Facebook of online streaming - Roku (ROKU).

Roku is a cluster of in-house, manufactured, online streaming devices offering OTT (over-the-top) content in the form of channels on its proprietary platform.

The company has two foundational drivers propelling business - selling hardware devices and selling digital ads.

It pays dividends to be entrenched at the intersection of two monumental generational trends of cord cutters' mass migration to online streaming, and the disruption of the digital ad revolution that is shaking up traditional media giants.

The percentage of American homes paying for an online streaming service ripped higher to 55% of households, which is up from 49% the previous year.

This $2.1 billion per month spend on streaming service is specifically as a result of access to premium content at an affordable price relative to traditional cable bundles.

Roku is a microcosm of the healthy climate for quality technology stocks in 2018.

It is among countless other firms that leverage large-scale data or cloud tools to capture profits.

Roku is best of breed of smart TV platforms and is in the early stages of robust growth.

This year will be the first year Roku's ad revenue surpasses hardware sales, indicating strong platform growth.

Roku pinpointed building account user growth, top-line gross revenue, and enhancing the platform capabilities as ways to move the business forward.

This year will also be the first year Roku posts an overall profit.

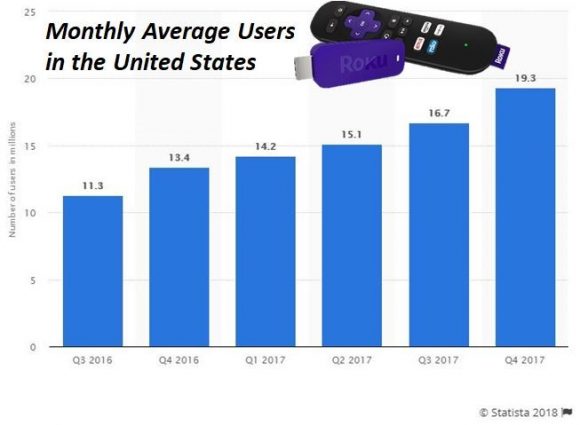

Active accounts grew 44% YOY to 19.3 million.

Roku offers consumers a cheap point of entry selling its Roku express box for only $29.99.

Its device is even free with a two-month purchase of Sling TV, which is the best online substitute to a legacy cable package. It has two sets of unique bundles available, charging $20 per month and $40 per month.

Once the Roku home screen populates, users can choose content through a la carte streaming options.

There is no monthly fee to operate Roku, and the device is used primarily by millennials.

More than 60% of 18- to 29-year-olds watch TV from online streaming, according to a Pew survey.

The quality and easy-to-use interface aids user navigation across the ecosystem.

It's the most convenient avenue to subscribe to multiple online streaming services all on one platform. It entices finicky users with extra mobility - those who love to jump around to different services based on particular upcoming content loaded up in the pipeline.

Many of these services offer no contract, cancel-anytime models that millennials love rather than the "old-school" rigid rules of cable providers that mostly charge a cancellation penalty of $300.

It is shocking how far traditional media fell behind the curve, but they are in rapid catch-up mode now.

Remember that content is king, and the overall boost in content quality has really shaken Hollywood executives to their core.

The golden age of streaming continues unabated with a Netflix 2018 annual content budget of $8 billion.

Roku does not create original content and it desires no skin in the game.

Content is expensive, and Roku would rather become the best place to host it.

Netflix's 2017 total revenue was a staggering $11.69 billion in 2017, and content costs will easily surpass 50% of total revenue in 2018. Overnight, it has become one of the biggest players in Hollywood, as its presence at the Emmy Awards amply demonstrates.

Exorbitant content costs are the new normal in 2018, and Spotify has reason to moan about the cost of content being 79% of total revenue.

Heightened content costs are the main reason why firms relying on content creation lose money each year.

However, as the overall pie grows, there is room for the tide to lift all boats. Being the premier platform to host premium content is why Roku's business model is eerily similar to Facebook's hyper-targeting ad model.

They make money the same way.

The incessant demand for online streaming functionality and smart TV operating systems show no signs of waning with Amazon (AMZN) announcing a new partnership with frenemy Best Buy (BBY) to produce smart TVs with Best Buy's in-house TV brand Insignia.

This is the first time Best Buy has been afforded a direct route to Amazon customers.

Disney (DIS) is turning around its legacy company into an online streaming behemoth announcing its first foray into online streaming with ESPN+.

Disney has tripled down on online streaming, acquiring New York-based BAMTech in late 2017, a company focused on developing streaming technology and made famous by its production of pro baseball's MLB TV.

BAMTech exudes pure quality. Anyone who has used MLB TV streaming service understands the great end-product it offers consumers.

The outstanding success with MLB TV attracted new online streaming converts to BAMTech to execute the transition to online streaming, including the WWE, Fox Sports, PlayStation Vue, and Hulu.

HBO went to BAMTech in 2014, after botching its attempt at creating a reliable stand-alone streaming service.

Disney's BAMTech-produced online streaming service will come to market in 2019, and will certainly be available on Roku TV.

Expect new blockbuster hits to debut on this new streaming service, such as new versions of Star Wars.

It is the perfect stock to mutate into an online streaming service because it possesses amazing content especially through ESPN.

The announcement of ESPN+ levitated Roku shares by 10% because investors understand this is the first baby step to shifting more of its content online.

This was on top of the announcement that Stephen A. Cohen's Point72 Asset Management had acquired a 5.1% stake in Roku for about $14 billion.

Furthermore, every major streaming service that enters Roku's system is worth an extra 5% to 10% bump in share price because of the wave of eyeballs and digital ads that grow Roku's coffers.

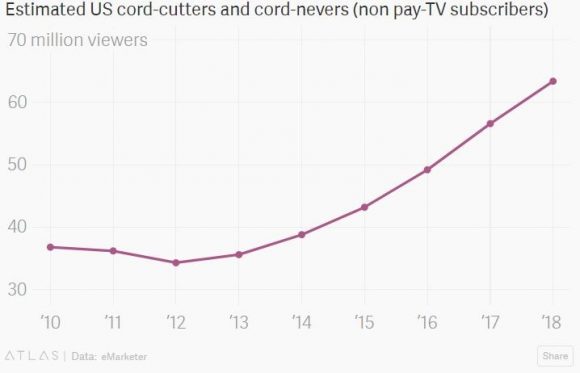

It is certain that 2018 and 2019 will sway more cord cutters to adopt Roku TV as this cohort approaches 70 million in 2018 on its way to 80 million in 2019.

The critical growth lever is its digital ad business as it hopes to take home a slice of this $70 billion per year business that is 75% controlled by Alphabet (GOOGL) and Facebook.

Roku has made great strides with half of Ad Age's top 200 advertisers already on the Roku interface.

Roku is taking the playbook right out from under Facebook's nose, piling funds into further enhancing its ad-tech division.

The blood, sweat, and tears shed is showing up in the financials with ARPU (Average Revenue per User) rocketing by 48% YOY, and more than 65% of this gap up is attributed to digital ad revenue.

Total revenue was up 29% YOY to $513 million, and platform revenue grew 129% in Q4 2017 to $85.4 million.

It is estimated that ad revenue will surpass $300 million in 2018, up from around $200 million in 2017.

Roku expects total revenue to grow 32% in 2018, approaching $700 million.

Profit margins are thriving under the platform segment, pumping out a stellar 74.6% in gross margin.

Roku does not make money on the hardware. Its push into ad distribution will ramp up as its digital ad revenue beelines toward an expected $700 million windfall by 2020.

Roku has a fantastic growth trajectory relative to other tech companies. Heightened volatility will make sell-offs hard to swallow but give fabulous entry points into a budding business.

The fertile path of international user adoption has barely scratched the surface. However, Netflix's successful foray abroad will inject confidence that Roku will have no problem expanding to greener pastures overseas as domestic account growth is always first to mature.

__________________________________________________________________________________________________

Quote of the Day

"AI is one of the most important things humanity is working on. It is more profound than electricity or fire." - said Google CEO Sundar Pichai