Mad Hedge Technology Letter

July 12, 2021

Fiat Lux

Featured Trade:

(RIDE THE MOMENTUM)

(SHOP), (NFLX), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)

Mad Hedge Technology Letter

July 12, 2021

Fiat Lux

Featured Trade:

(RIDE THE MOMENTUM)

(SHOP), (NFLX), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)

Just as millions of people in the United States are sensing that life has returned to something that resembles normalcy, the Coronavirus’ delta variant has emerged as American technology stocks biggest upcoming inflection point.

This certainly ups the ante in the struggle to grapple with the pandemic and has wide-reaching consequences for your technology portfolio.

Fresh data from the U.S. Centers for Disease Control and Prevention shows that more than half of all new cases in the U.S. were attributed to the delta variant, which is believed to be easily transmissible.

About 50% of Americans are fully unvaccinated meaning 50% are not, which could lead to hellacious autumn for the 175 million who are not.

The tech market has sniffed this out.

Data suggesting this variant is three times as infectious as the original coronavirus strain is the catalyst for a massive rotation into premium big tech who boast glamorous balance sheets.

It is still unclear if this virus is actually deadlier or leads to more severe illness, but the health of Facebook, Google, Apple, Microsoft, and Amazon aren’t reliant on the outcome of the delta variant or at least relative to companies that have physical storefronts.

I believe the momentum in these names will continue in the short term as more countries prepare to carve up new movement restrictions and quasi lockdowns to combat the new variant.

The recent tech rotation has been inconspicuous but powerful and the who’s who of big tech are enjoying a stellar run in the past month with FB up 6%, GOOGL up 4.5%, AAPL up 13%, MSFT up 8%, and AMZN up 11%.

These premium tech stocks are acting almost like U.S. treasuries and are increasingly defined as a perceived flight to safety because of

the net high quality of the assets.

Whether there is another virus that kills another 4 million globally again, investors are confident that these prioritized tech stocks are immune to any meaningful weaknesses.

On a granular level, pullbacks are becoming highly rare and mini pullbacks are becoming the only practical entry points into these stocks.

Readers waiting for a 5% drop are still waiting.

Reading waiting for 10% drops risk never getting in when the going is good.

Fresh news of Japan banning spectators for the upcoming and badly organized Tokyo Olympics took down GOOGL and FB 2% intraday only for shares to make up half the losses in one afternoon.

The delta variant has strengthened the “buy the dip” philosophy that is deeply entrenched in these 5 tech names.

The strength of tech can be seen further down the totem pole in inferior names.

Shopify (SHOP), Canada’s ecommerce crown jewel, is another winner with shares up 19% in the past 30 days.

If this rotation continues, I can realistically expect dips or sideways price action in Uber (UBER), Lyft (LYFT), and Airbnb (ABNB) because their investment case weakens relative to the big 5 in a delta variant world.

Netflix (NFLX) is another one that will harvest the low-hanging fruit with strong near-term action resulting in a 9% gain in the past 30 days.

It’s highly likely that in more than several regions around the world, the delta variant will re-silo consumers and hamstring businesses.

Crushing any green shoots that the reopening is supposed to deliver isn’t an ideal runway to growth.

Epidemiologists are starting to come out of the woodwork with Hungarian virologist Ferenc Jakab saying Hungary will be lucky to “get away with August” when referring to a possible 4th wave.

This hasn’t been fully priced into the U.S. tech market and tech will enjoy a full-scale rotation if the 4th wave arrives in full force.

However, I don’t believe we are on the cusp of another $12+ trillion bailout for the delta like last time go around, which does cap momentum to the upside.

There will also be a lack of meme stock profit-taking and bitcoin profit-taking that can be rolled into the big tech safety trade.

Sensibly, this could be a short-term boost for emerging growth tech as well with the likes of DocuSign (DOCU), Zoom Video (ZM), and Teladoc (TDOC) benefiting from investors dusting off the 2020 playbook again.

I forgot to mention that U.S. treasuries falling to $1.36% is the primary reason why at the balance sheet level, growth tech will also get the benefit of the doubt in the short term.

This won’t just be a big 5 momentum encore, others will enjoy the fruits of labor.

Loss-making tech is inordinately reliant on rates being low to subsidize losses and as the 10-year rate has gone from 1.72% to 1.36%, it’s no surprise that growth tech looks like eye candy now too.

Big tech is certainly more durable and has the capacity to navigate around rising rates which is the deal-clincher for me.

I am inclined to get back into the market with any delta scare that cheapens tech before the next leg up.

The embarrassing loss in the judicial system against FB by the Feds is the cherry on top.

I am bullish tech in the short term.

Mad Hedge Technology Letter

July 9, 2021

Fiat Lux

Featured Trade:

(BUYER BEWARE)

(DIDI), (PGJ), (FB), (AMZN), (GOOGL), (NFLX), (AAPL)

Chinese regulators announced on our Independence Day that they were banning downloads of Uber’s China DiDi in the app stores in the country because it poses cybersecurity risks and broke privacy laws.

This was after DiDi raised $4.4 billion by listing its shares in New York.

However, unnamed sources leaked that China's cybersecurity watchdog suggested to DiDi that it delay its IPO before it happened.

Delaying a wealth generating event like the IPO is controversial.

At this point, DIDI, the Uber of China, is worth a speculative trade at $1 and that’s if the Chinese tech firm doesn’t delist before that.

No — scratch that — it’s not even worth your time at $1 if you hold currency denominated in USD or anything even half as credible.

But if you’re from somewhere like Venezuela wielding infamous bolivars then take a wild stab around $1 or double up at $0.50 for a trade.

There is a reason that I have never in the history of the Mad Hedge Technology Letter recommended buying a Chinese technology stock.

The astronomical risk isn’t justified.

The evidence is now out in public with Chinese big tech and the Chinese Communist Party (CCP) airing their dirty laundry.

Most sensitive business dealings are usually dealt with in-house in the land of pan-fried dumplings and Beijing roasted duck, so things must be spiraling out of control on the inside.

No doubt that inflation spikes are causing chaos everywhere, but China is particularly vulnerable because of the high volume of Chinese living in poverty.

It’s unrelated to this IPO, but another valid reason why Chinese “growth” is weakening fast.

Stateside, cashing out is normal for tech growth companies who want to reward earlier seed investors, their own management teams, and in this case the early-stage investors were Japanese Softbank (21.5%), Silicon Valley’s Uber (12.8%), and China’s Tencent (6.8%).

This was pretty much a big middle finger to these three along with the other Chinese investors which were about to profit big.

This is on the heels of the CCP nixing the Jack Ma Alipay IPO.

Chinese big tech has gone from darlings to pariahs in a short time proving that in the U.S., you get too big to fail, but in China, you get too big to exist.

Silicon Valley tech princelings are also validated for leaving China such as Facebook (FB), Google (GOOGL), Amazon (AMZN) and Netflix (NFLX).

If local Chinese tech can’t flourish in China, then forget about foreign tech in China.

It’s a non-starter.

Apple (AAPL) is the only exception because they are grandfathered in when China had no smartphone and now they provide too many local jobs to be kicked out.

There is definitely a plausible case that U.S. retail investors who were part of that $4.4 billion holdings should be refunded their capital because DiDi didn’t truthfully disclose the risk of potential Chinese regulations properly.

There is also the logic that Chinese companies should never be able to list in New York in the first place which would be sensible.

As it stands, Chinese companies don’t need to follow U.S. GAAP accounting standards and cannot be prosecuted by the U.S. legal system if they commit fraud, embezzlement, or any other financial crime and decline to leave Chinese soil.

This incentivizes Chinese companies listed in the U.S. to cheat U.S. investors with fraudulent accounting and deceitful behavior because they aren’t accountable at the end of the day.

The Invesco Golden Dragon China ETF (PGJ), which tracks the performance of US-listed Chinese stocks, has lost more than one-third of its value since February.

I can tell you from close friends who call themselves frontier investors that investing in China is not worth your time and the fear of missing out (FOMO) rationale is all marketing chutzpah and nothing much else.

China’s economy hasn’t had any positive growth in the past 10 years according to Chinese insiders off record.

This FOMO narrative is often peddled by Wall Street “professionals” who are making exorbitant fees for selling retail investors Chinese junk stocks masquerading as real companies.

Out of many financial pros I have talked to, China leads in terms of horror stories from foreign investors.

The Chinese financial system is a hoax created to lure foreign capital in and for it to never leave often viewed as a free lunch for the local recipients.

And I am not only talking about Chinese tech, but this phenomenon also extends to every reach of the financial system there.

At the end of the day, China’s tech aristocracy wished they originated in the United States which is why they went public here because our markets work and theirs don’t.

They got to New York in the first place by marketing false numbers to U.S. investors and concealing regulatory issues, and U.S. investors must not fall for this trap.

If you look at the Shanghai Stock Exchange Composite Index ($SSEC), it’s gone nowhere in the past year and rightly so.

Even Chinese investors don’t buy Chinese stocks because there is no trust in their financial system. They buy property instead or buy U.S. tech stocks.

Don’t be the next sucker.

Global Market Comments

July 7, 2021

Fiat Lux

Featured Trade:

(JUNE 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (BRKB), (GOOG), (NVDA), (FB), (TSLA), (JPM), (BAC), (C), (GS), (MS), (NASD), ((X), (FCX), (AMZN), (MSFT), (AAPL), (FCX)

Global Market Comments

July 6, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ALL EYES ON THE FANGS)

(FB), (AAPL), (AMZN), (MSFT), (NFLX), (NVDA), (AMD), (MU)

If you are a believer in the FANGS (FB), (AAPL), (AMZN), (MSFT), (NFLX), with NVIDIA (NVDA) as an add-on, last week was definitely your week.

They rose every day, ending the week with a melt-up of epic proportions. After eight months in the penalty box, tech came back with a vengeance and is now two months into their comeback tour.

The icing on the cake was Facebook’s big win in the antitrust suit from the FTC. That suitably deep-sixes the issue not just for (FB) but all of big tech, possibly for years. The five stocks above now account for a hefty 22% of the S&P 500 (SPY).

The question now on everyone’s mind is what’s next for tech? 25%? 30% 50%? The answer is all of the above, but you have to give it some time, like years.

We are now in an overbought market where big tech has become the cheapest sector. In addition, the global chip shortage promises to get worse before it gets better, with some products seeing a 10X increase in a single generation.

Companies that can’t get the chips they want are resigning products around the chips they can get on the fly.

This has created enormous spillover demand for marginal suppliers like Advanced Micro Devices (AMD) and Micron Technology (MU). It has also accelerated the evolution of technology.

Companies that already have decade-long supply chains already set up, like Tesla, now have a big advantage. That’s why (TSLA) has managed a healthy 27% gain in six weeks.

The severity of the chip shortage is wildly estimated if you look at future design plans of the biggest industries. A tech rally lasting months, if not years, was a totally natural progression.

I’ll tell you who else is dropping the ball. Analysts and strategists are consistently underestimating the strength of the economic recovery and the torrid growth of earnings. They are lagging by about six months. That is why 80% of announcements have delivered upside surprises.

There are more surprises to come.

When markets peaked in April, an eye-popping 92% of shares were above their 50-day moving average. Now, we are only at 52%. That suggests we have another month of excitement before we get another short-term correction.

June Nonfarm Payroll Report comes in hot, up 850,000, an eye-popping 150,000 better than expected. The headline Unemployment Rate moved up slightly to 5.9%. Accommodation gained 269,000, and Food Services & Drinking Places were up 194,000. It was a true Goldilocks number for the stock market, but not the million some had hoped for. My 30% forecast for the Dow Average is looking good.

The Infrastructure Bill extends the hot economy well into 2023 and longer. Analysts better start upgrading now, who have been badly lagging behind the recovery. Tech stocks saw this six weeks ago and began their torrid rally. Buy everything on dips and stick with the barbell strategy to catch all of the rotations.

Rents will continue to go through the roof. Good thing you don’t live in Boise, ID, which is seeing the fastest rent increases in the county at 39% YOY. Of course, having the Micron Technology (MU) HQ there is a major push. Don’t expect any respite. With home prices soaring, rents will get dragged up as prospective buyers are priced out of the market.

Weekly Jobless Claims moderate further, 364,000 Americans filed new claims for unemployment benefits last week - lowest since pandemic. Still elevated from a typical pre-pandemic week when we would see about 210,000 claims.

Softbank’s capital flooding into Crypto, with Japan's SoftBank Group Corp has invested $200 million in Mercado Bitcoin, one of the largest cryptocurrency exchanges in Latin America signaling the start of the first phase of big institutional money hoping to take advantage of the digital currency craze.

Goldman Sachs is the top financial pick according to JP Morgan Chase. All cylinders are firing and we’ve just come off a fabulous 15% dip. A move to more sustainable revenue streams, like wealth management, is the reason, which Morgan Stanley did decades ago under my watch. I’m looking for $450 on dips. Buy (GS) on dips.

Morgan Stanley doubles its dividend, now that it has passed the Fed stress test and the tethers are off. It also announced a share buyback of $12 billion over the next year which may be increased. Buy (MS) on dips.

S&P Case Shiller National Home Price Index for April hits new high, up 14.6%, the biggest increase in 30 years. Phoenix leads at +22.3%, followed by San Diego at +21.6% and Seattle at +20.2%. The numbers run from incredible to unbelievable.

CRISPR Therapeutics goes through the roof, up 12% at the highs, on successful drug trials by Intellia Therapeutics (NTLA) and Regeneron (REGN). The Mad Hedge Biotech Letter core holding provided the gene-editing technology behind the 45% gain in (NTLA) today. It enabled the 85% elimination of a rare inherited fatal liver disease, transthyretin amyloidosis. Say that fast three times. Buy (CRSP) on dips. With Editas, there are only three small companies that have a monopoly here.

Facebook wins antitrust action, a federal judge dismissing an FTC action against the company. The move set the entire tech sector on fire. It looks like all of NASDAQ is going to much higher highs. I bet you had a great day. The court found that (FB) did not enjoy a monopoly which might have forced them to sell off Instagram and WhatsApp.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

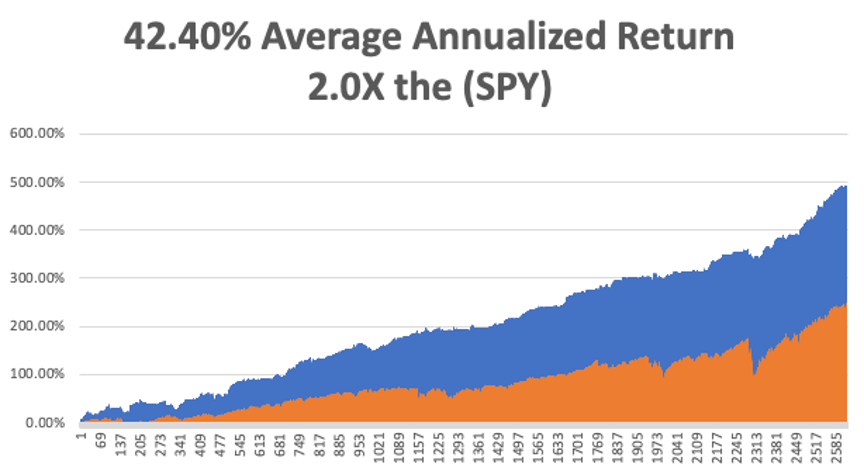

My Mad Hedge Global Trading Dispatch profit reached 0.71% gain so far in June on the heels of a spectacular 8.13% profit in May. That leaves me 100% in cash.

My 2021 year-to-date performance appreciated to 68.60%. The Dow Average is up 13.7% so far in 2021.

I spent the week sitting in 100% cash, waiting for a better entry point on the long side. Up this much this year, there is no reason to reach for the marginal trade, then maybe instead of the certainty. I’ll leave that for the Millennials.

That brings my 11-year total return to 491.15%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.40%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 112.59%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33.7 million and deaths topping 606,000, which you can find here.

The coming week will be a weak one on the data front.

On Monday, July 5, markets are closed for the US Independence Day celebration.

On Tuesday, July 6 at 10:00 AM, the ISM Non-Manufacturing Index for June is released.

On Wednesday, July 7 at 10:00 AM, the Federal Open Market Committee Meeting from the last meeting are published.

On Thursday, July 8 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, July 9 at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, with all the hiking I have been doing during the pandemic, I have been listening to a lot of WWII audio books lately. That reminds me of an old friendship I had with Toshiro Mifune, then the most movie famous star in Japan.

Mifune was drafted into the Japanese army during WWII where he served as an aerial reconnaissance photographer. After the war, that led him to work as a cameraman at Toho Productions, then the largest movie company in Japan.

A friend submitted his photo with an application for a casting call without his knowledge, and Toshiro, a good-looking guy, was one of 48 picked out of 4,000. He then met the legendary director, Akia Kurosawa, and the two launched the golden age of Japanese cinema in the late 1940s.

In just a couple of years, they produced blockbuster classic films like the Seven Samurai, Rashomon, and Throne of Blood, all of which are now required viewing by every American film school, and where Mifune demonstrated his impressive skills with a sword he picked up in the army.

I met Toshiro late in his career when he was cast as Admiral Isoroku Yamamoto for the 1976 Universal movie Midway. The problem was that Mifune couldn’t speak a word of English. I was brought in to bring Toshiro up to par in a crash course held at his west Tokyo mansion every afternoon seven days a week. We became good friends.

After a heroic effort, Mifune’s English was still awful, so the producers brought in a voice actor to dub Mifune’s part in Midway. That was Paul Frees, who provided the voice for the Disneyland’s Haunted House and Pirates of the Caribbean rides, as well as the cartoon Boris Badenov. His voice is still attached to those rides today, and I recognize it every time I take the kids.

Midway was a huge success and Mifune’s next big role was to play Commander Mitamura in Stephen Spielberg’s 1941. He followed that up with a role as Toranaga in James Clavell’s 1980 miniseries, Shogun, another old friend. (Clavell is a story for another day). My tutoring skills came back into demand once again, with better results.

Mifune died in 1997 at 77 and I miss him still.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

June 30, 2021

Fiat Lux

Featured Trade:

(BIG TECH WINS IN THE COURTROOM)

(AAPL), (AMZN), (GOOGL), (FB), (MSFT)

Federal court dismissed antitrust lawsuits against Facebook that the Federal Trade Commission (FTC) and 48 states seek to pin on the digital ad company.

This isn’t only a feather in the cap for FB, but it’s great news for Google, Snapchat, Twitter and the who’s who of selling digital ads and any tech company that might be perceived as “dominant.”

Many would have been led to believe that big tech and these ad giants were on the cusp of being controlled by legislation, only for the federal court to not even bother with advancing the case.

It means that the law is firmly on the side of big tech and it will be almost impossible to pin charges against big tech unless the law is changed to accommodate a situation that is more conducive to proving that American tech companies abuse their positions in the US economy.

Personally, I do believe they have a monopolistic position against its competitors, but to prove that in court is a different animal with arguments needing to hold up against the test of time.

There is no doubt that the company has a dominant share of the market in the “personal social networking” industry, but market dominance just means they are incredibly good at what they do which is serving ads to targeted audience.

Nothing they do is explicitly illegal and that is the tough part and they do provide “free” services.

Not only that, but Facebook users can also simply not use social media and its various platform as a choice because they can drop it altogether or use a different platform entirely.

The court also dismissed a supplementary complaint by the FTC with the judge ruling that the states had taken too long to take issue with Facebook’s acquisition of Instagram and WhatsApp, which were acquired in 2012 and 2014, respectively.

The ruling made the government’s FTC look bad and tardy.

They also are late to the game, unable to understand the tech of our time and enforce borderline fringe behavior.

This is why anti-trust, which many believe is big tech’s largest existential risk, is not really a risk when politicians fail so miserably at even understanding what they do until 9 years later.

Most tech companies are happy to know they have 9 years to skirt the law and aggressively push their business models until the FTC move their finger an inch.

Might as well bet the ranch, right?

Certainly, there will be another wave of amended filed complaints against Facebook within 30 days, which the court will re-review.

But after some convicting loss, prospects look poor for the FTC.

The way in which the law is worded today means that Facebook has to be on the radar of investors as a premier buy the dip trade now that one of the bigger risks is off the table.

Facebook's valuation has more than doubled since the onset of the pandemic as more people use its diversified network of apps to stay in touch with friends and family in a socially distant world.

The social network had over 2.85 billion monthly active users in Q1 2021 and join other tech firms over $1 trillion such as Apple, Microsoft, Amazon, and Alphabet.

I would execute a bullish position in Facebook after a retracement from the 4% pop on the good news.

Tech is expensive and has had another resurgence over the past few weeks.

It continues to be an industry you cannot bet against and that is why you have to be patient for entry points to come to you.

Global Market Comments

June 28, 2021

Fiat Lux

Featured Trade:

(BACK FROM MY 50-MILE HIKE)