Automation is taking place at warp speed, displacing employees from all walks of life.

According to a recent report, the U.S. financial industry will depose of 400,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird, and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the $150 billion annually that banks spend on technological development in-house, which is higher than any other industry.

Welcome to the world of lower costs, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up 50% of bank expenses.

The 400,000 job trimmings would result in 20% of the U.S. banking sector getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

This iteration of mobile and online banking has delivered functionality that no generation of customers has ever seen.

The most gutted part of banking jobs will naturally occur in the call centers because they are the low-hanging fruit for automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware that they are communicating with an artificial engineered algorithm.

The wholesale integration of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers, sullying the predated ideology that front-office staff are irreplaceable heavy hitters.

Front-office staff has already felt the brunt of downsizing, with purges carried out from 2022 representing a twelfth year of continuous decline.

Front-office traders and brokers are being replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 30%, and the accumulation of hordes of data will advance the marketing effort into a smart, multi-pronged, hybrid cloud-based, and hyper-targeted strategy.

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008, adding around half a million jobs on top of the 1.5 million that existed then.

After the subsidies wear off from the pandemic, I do believe that the banking sector will quietly put in the call to trim even more.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

Recomposing banks through automation is crucial to surviving as fintech companies like PayPal (PYPL) and Square (SQ) are chomping at the bit, and even tech companies like Amazon (AMZN) and Apple (AAPL) have started tinkering with new financial products.

And if you thought that this phenomenon was limited to the U.S., think again, Europe is by far the biggest culprit by already laying off 102,000 employees in 2021, more than 10x higher the number of U.S. financial job losses, and that has continued in 2022, 2023 and 2024.

In a sign of the times, the European outlook has turned demonstrably negative, with Deutsche Bank announcing layoffs of 40,000 employees as it scales down its investment banking business.

Don’t tell your kid to get into banking because they will most likely be feeding on scraps at that point.

THE LAST STAGE OF HUMAN-FACING BANK SERVICES IS NOW!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-12-27 14:02:492024-12-27 13:39:35The Truth About Automation And Banking

Unshackling the restraints on human labor – that is where tech is headed.

I’m talking about AI.

Robots aren’t able to perform complicated tasks, and that is the holy grail of AI.

If headway is made just on this one issue, then the sky is the limit.

Profits are then unlimited, and the world will change into something we could have never imagined.

If stakes weren’t high enough, the next explosive leg up in tech shares is now centered on this concept.

There is only so much balance sheet maneuvering can add to the bottom line.

Magnificent 7 stocks who are experts are juicing up the balance sheet will gradually run out of levers to pull.

Technology stocks demand that management move the needle along because the alternative is that the company will get left behind.

When the Department of Defense commenced its robotics challenge in 2015, the stated goal was to develop ground robots that can aid in disaster recovery with the help of human operators.

Nearly a decade later, generative AI is accelerating that learning curve, pushing human-like machines to pick up new tasks in real-time.

And in June, Tesla (TSLA) presented an updated version of its Optimus robot at Tesla’s Investor Day and showed it roaming a factory floor. CEO Elon Musk touted the robot’s potential, saying it had the ability to push the company’s market cap to $25 trillion.

Humanoids that can adapt to existing environments have long been seen as the ultimate test if they can work alongside humans in spaces built for them.

Nvidia (NVDA) is driving rapid development through an ecosystem built specifically for humanoids. It combines high-powered chips that process data at high speeds with a digital world that allows users to train robots on skills applied in the real world.

Nvidia has already unveiled “NIM Microservices,” a visual training ground that allows generative AI models to visually interpret their surroundings in 3D.

Nvidia’s ecosystem now enables robots to train using text and speech input in addition to live demonstrations.

Humanoids have already begun taking their first steps into reality. Musk has said two Optimus robots are working at Tesla’s Fremont factory, and he expects a few thousand to be deployed by next year. Amazon (AMZN) has partnered with Oregon-based Agility to utilize its Digit robot at a test facility. Apptronik is working with Mercedes-Benz to integrate Apollo into its manufacturing line.

The goal is to adapt humanoid for the future, which will allow them to operate beyond industrial use. They could become as ubiquitous if companies are able to scale and bring costs down to $10,000 per machine.

Technology is still in the stage of calculating how they bring the expenses under control.

It is not very cost-effective if a company needs to spend 5 times the actual cost of running the AI division on retrofitting the environment for a humanoid and resetting the language models for different tasks.

Much of these technical aspects are being worked out, and these companies are inching their way closer to a day when companies might be able to work fully without a human worker or alongside a minimum amount of workers.

Tesla is a company long-term that needs to be looked at, and this assumption is solely based on their robotics and humanoid business. It is highly plausible that Elon Musk is at peace with sacrificing his EV business in the medium time as long as moving up the value chain to become the leader of what is next, which is looking more like robotics using AI.

Musk is skating to where the puck is next, and that is where the future will be.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-12-18 14:02:552024-12-18 14:22:29Unlocking The Future Of Tech

Below, please find subscribers’ Q&A for the December 11 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, Nevada.

Q: I was assigned options—called away on both my short-call positions in BlackRock (BLK) and Bank of America (BAC).

A: What you do there is call your broker and exercise your long to cover your short; that should get you 100% of the profit 10 days ahead of expiration, and that is the best way to get out of that position. If you get hit with the dividend, then you're at break-even on the total trade. The way to get around this is you have 10 positions, including several non-dividend paying positions, so you don't have a call-away risk. You really only have about a 1 in 100 chance to get called away, so it's worth doing. If the worst case is you break even, the best case is you make 15% or 20% on the position in a month. That is worth doing.

Q: What do you think of the situation in Syria?

A: We don't know. For us, it's a huge win because it eliminates the last Russian position in the Middle East. They have lost Egypt, Syria, Iraq, and at one point Algeria—so they have no more positions in the Middle East. They lose all their air bases, military bases, and naval bases in Syria, and they also lose their only warm water port in the Mediterranean. It happened because they couldn't afford to draw troops away from Ukraine to help support Syria. Given the choice between Syria and Ukraine, they'll pick Ukraine. It is another argument for the US to maintain support for Ukraine.

The trouble is in the Middle East, whenever you get a chance, you often end up getting somebody else that's worse. Did we just trade one terrorist for another one? We'll have to wait and see. Fortunately, this war didn't cost us any money. It cost Russia a lot. We had no troops in Syria and no weapons commitments, so we got off easily on this one. It’s probably the most important foreign policy achievement of the last four years.

In the meantime, we're destroying all their weapons stockpiles, just in case the new people coming in are bad guys. We'd rather not wait until after they identify themselves as bad guys—we might as well destroy all the weapons now while nobody is defending them. So, as I speak, we're destroying weapons stockpiles for its ships and rocket facilities. Also, this is a huge loss for Iran because they lose easy sea access to Gaza. They used to just truck weapons to the coast in Lebanon, put them on a boat, and send them to Gaza. Now, they have to go all the way around Africa to supply Gaza. So basically it's a huge win for us, and I'll write more about that in the Monday letter.

Q: Do the spread positions need to be actively closed out to achieve profits?

A: No, they don't. You don't have to touch them. That's the beauty of these positions. All ten I expect to expire in the money at maximum profit point, and on the following Monday morning opening, you will find that the margin is freed up, the cash profit is credited to your account, and you're in a 100% cash position. So don't do anything, even if your broker will tell you to individually buy and sell the individual legs and wipe out your profit. I sent out a research piece on this today about how to handle when calls are called away.

Q: I sold BlackRock (BLK) last week because Schwab called and warned me I could owe $6,000 due to the dividend. They did not suggest I close my long position.

A: Again, it goes back to how to handle option call-aways. The only reason they call you is to eliminate any liability for Charles Schwab because, in the past, people would get options called away, they'd say my broker never told me, and they sued the broker. So, the reason they emailed you and called you with warnings is to avoid liability for themselves. In actual fact, only 1 out of 100 different options actually get called away. It's done randomly by a computer, and you're far better off holding the position. And then, if you do get called away, use your long to exercise your short. It's a perfectly hedged position, so you have no actual outright risk. The only real risk is if you don't check your email every day and you don't know you've been called away, so you don't call your broker to exercise your long to cover your short.

Q: Do you envision other countries trending towards more tariffs? How would that affect global growth?

A: Any time we raise a tariff on another country, they're going to raise by an equal amount, and it becomes a perfect growth destruction machine. That's why every economic agency in the world is predicting lower growth for next year.

Q: Why are stocks so expensive? Can the high prices be an impediment for new investors to participate or not?

A: It's obviously not an impediment because we're at an all-time high, and we keep going to new all-time highs. Most investors, not just a few, are still underweight stocks, and they're chasing the market. I predicted this would happen all year basically, and now it's happening, and we're 100% invested in making a fortune. So that's what happens when you make big predictions far into the future, and they happen.

Q: What do you think about meme stocks like GameStop (GME)?

A: Don't bother with the meme stocks like GameStop when the good stuff like Tesla (TSLA), Meta (META), and Amazon (AMZN) are going up like a rocket. Why buy the garbage when the high-quality stuff is doing well? And, of course, most of the people buying that stuff, the meme stocks, are kids who don't know what the good stuff is, but they'll find out someday.

Q: If you like Japanese cars, what do you think of Korean cars and, therefore, those companies’ stocks?

A: I don't like them. When you take your Tesla in for a service, sometimes you get a KIA in return. Ouch. You can literally hear every bolt rattle as you drive down the freeway, and you leave behind a trail of parts; the quality difference is enormous.

Q: How do you determine the limit price on spread trades?

A: I don't like making less than a 5% profit in a month. It's just not worth the risk. So let's say if I do a trade alert at $9.00, I'll create a spread of, say, $9.00, $9.10, $9.20, $9.30, $9.40, and that's it. We tell people to not pay more than $9.40. Before we told people not to do that, they used to buy at market, and they would end up paying $10.00 for a $10.00 spread, and it is absolutely not worth it. That is the reason we do that.

Q: Ihave trouble getting your recommended price.

A: When we put out a trade alert, and 6,000 people are trying to do it at once, you'll never get the recommended price. You may get it at the close because a lot of the high-frequency traders that pile into these positions and pay the maximum price have to be out of that position by the end of the day, so they often dump their positions at the close. And if you just leave your limit order in there, it'll get filled. If it doesn't get filled at the close, it will get filled at the opening the next morning. So that's why I'm telling people on every alert now to put in a spread, put in good-until-cancelled orders, and most of the time, you'll get some or all of those orders done. That is a good way to make money; if you don't believe me, just go to our testimonials page (click here), where hundreds of people have sent in recommendations on their experience.

Q: What do you think about crypto here (BITO)?

A: I wouldn't touch it with a 10-foot pole. The time to get involved in crypto was when it was at $6,000 two years ago, not at $100,000 now. And when the quality is trading and rising up almost every day, why bother with crypto? You'd never know if your custodian is going to steal your position. And by the way, if anyone knows an attorney expert at recovering stolen crypto, please send me their name because I have a few clients who took someone else's advice, invested in crypto, and had their accounts completely wiped out.

Q: Should I bet big on oil stocks (USO) because of the possible deregulation starting in 2025?

A: Absolutely not. “Drill, baby, drill” means oil glut—lower oil prices, which is terrible for oil companies, so you shouldn't touch them. The only plus for oil under the new administration is they'll probably refill the Strategic Petroleum Reserve in Texas and Louisiana from the current 425 million barrels to 700 million barrels by buying on the open market and enriching the oil companies.

Q: Would you sell long-term holds in pharma stocks?

A: No. If it's a long-term hold, your holding will survive the new administration. They'll probably go back up starting from a year going into the next election unless they find ways to deal with the current administration. But if you're in the vaccine business and the head of Health and Human Services is a lifetime anti-vaxxer, that is not going to be good for business, no matter how you cut it, sorry.

Q: Why is Walgreens (WBA) doing so poorly?

A: Terrible management and too late getting into online commerce. The service there is terrible. Every time I go to Walgreens to get a prescription filled, there's a line a mile long. It seems to be a dying company. Someone actually is making a takeover offer for the company today, so I would stand aside on that.

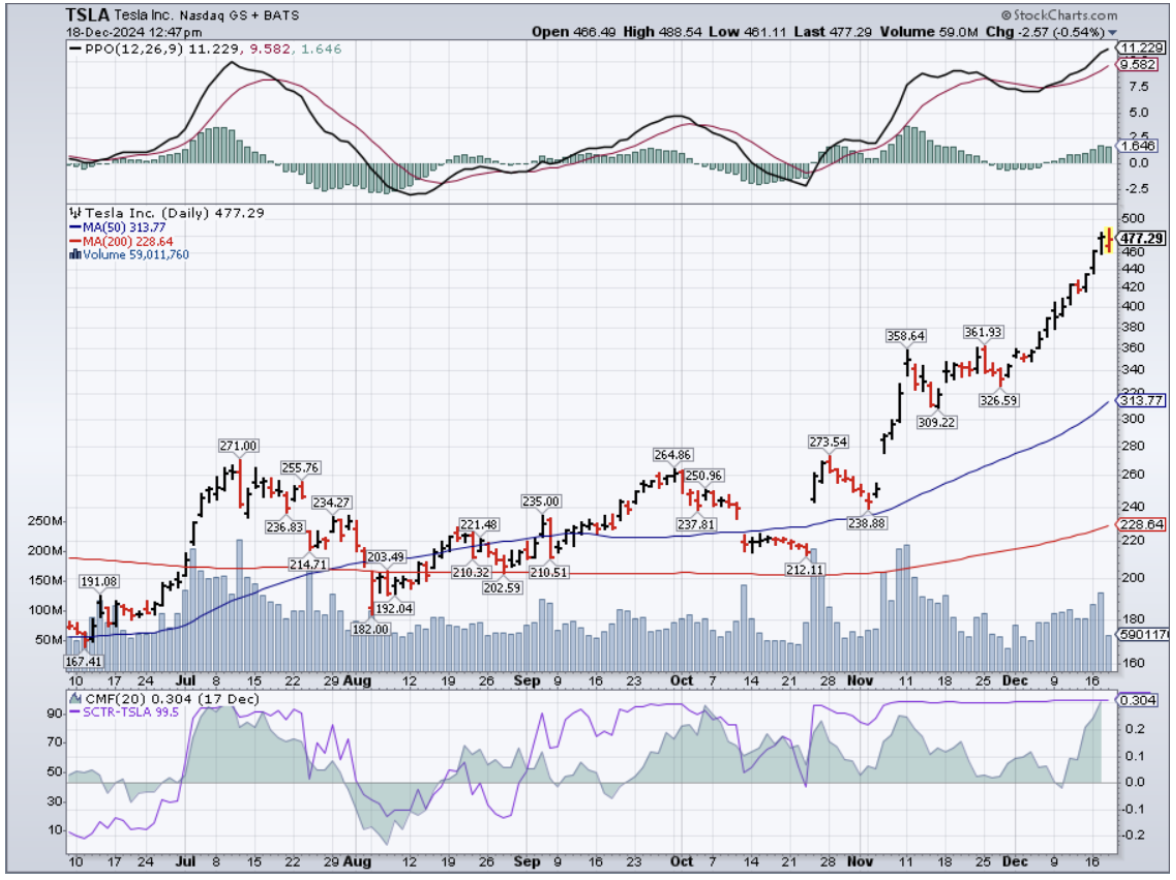

Q: Is Tesla (TSLA) risky?

A: Any stock that's tripled in four months is risky. But the rule of thumb with Tesla is that it always goes up more than you expect and then down more than you expect. Here is where high risk means high reward. My $1,000 target is now looking pretty good.

Q: If you're receiving Global Trading Dispatch, do you get the stock option service?

A: Yes, every trade alert we send out gives you the choice of a stock, an ETF, or an option to buy to take advantage of that alert.

Q: The EV stock Lucid (LCID) just got an analyst upgrade, but the chart looks terrible. Should I buy this cheap stock?

A: Absolutely not. Never confuse “gone down a lot" with “cheap.” Lucid only exists because it's supported by the Saudi royal family. They own about 75% of the company. They have no chance of ever competing with Tesla. Period. End of story.

Q: I have LEAPS on Google (GOOG), Amazon (AMZN), and Microsoft (MSFT). They expire in January, February, and March.

A: I would keep all of those—those are all good stocks. I expect them to keep rising at least until January 20th. After that, the Trump administration may announce antitrust actions against all three of these companies, but you'll probably have most of your profit by then. So from here on, if I had longs in all of these companies, I would definitely run them over the holidays because you'll probably get another pop sometime in January.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

(MARKET OUTLOOK FOR THE WEEK AHEAD or S&P 500 6,000 TARGET ACHIEVED, plus REPORT FROM THE FROZEN WASTELANDS OF THE WEST),

(CCI), (DHI), GLD), (SLV) (JPM), (MS), (BLK),

(CCJ), (NVDA), (AMZN), (TSLA), (DGE)

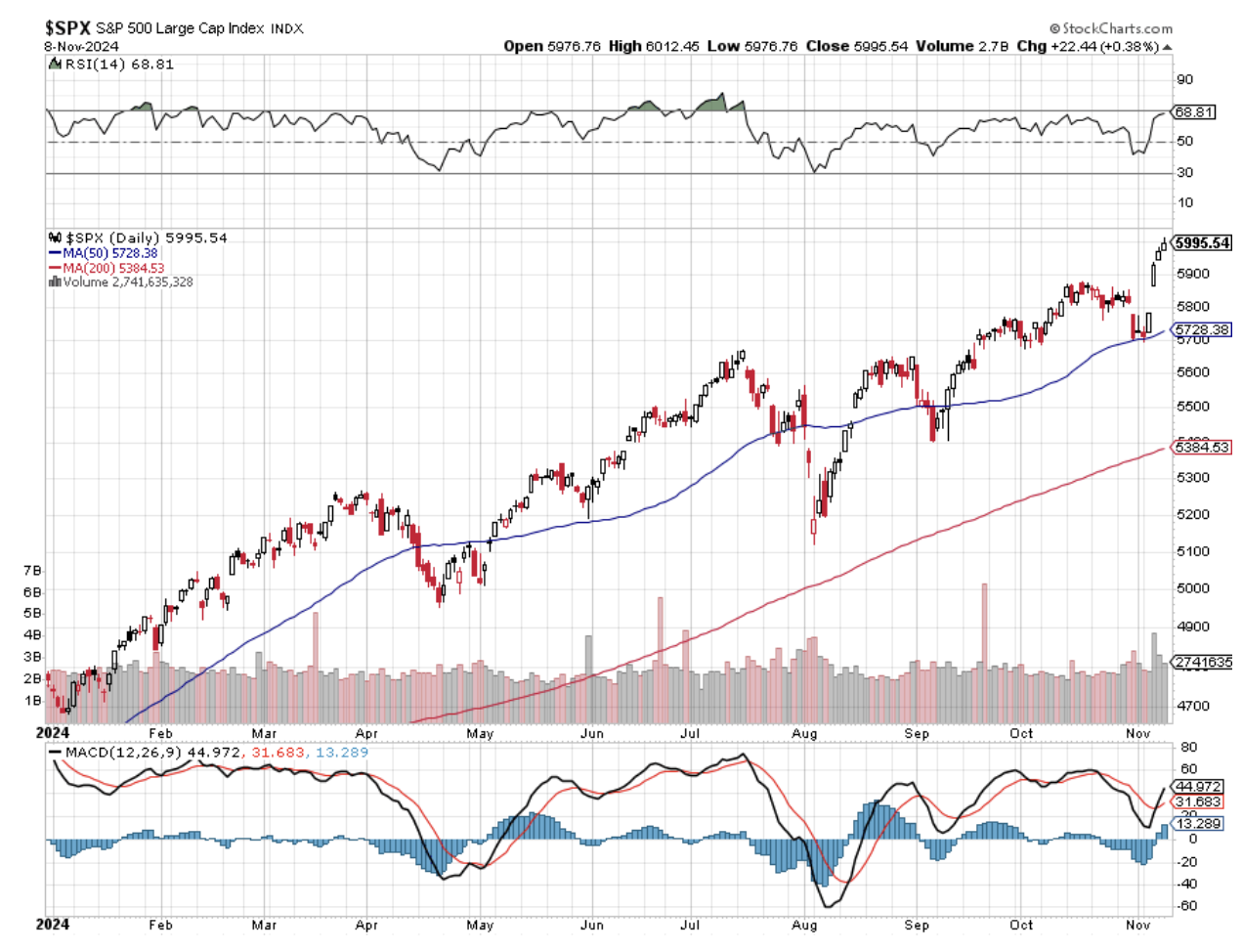

I was reviled, abused, and outright laughed at by the investment community when, last January 5, I predicted that the S&P 500 would hit 6,000 by yearend, click here for the link. I was accused of sending out clickbait.

Yet here, ten months and change into the year here, we are with an intraday high today of 6,013.

Of course, in this business, you’re only as good as your last trade. So, the big question now is, what happens next?

The next two months are a gimme. The $8 trillion that has been sitting on the sideline is now pouring into the market. An S&P 500 target of 6,600 is within range. Speaking to fund managers around the country, the big concern was not over who won but whether we had a winner at all.

Three months of litigation with no outcome would have raised uncertainty to extremes and crashed the market. The risk of that scenario is now gone, which was worth a $1,500 rally in a day.

However, while the bull market continues, the targets have changed. As you will hear many times over the next four years, elections have consequences.

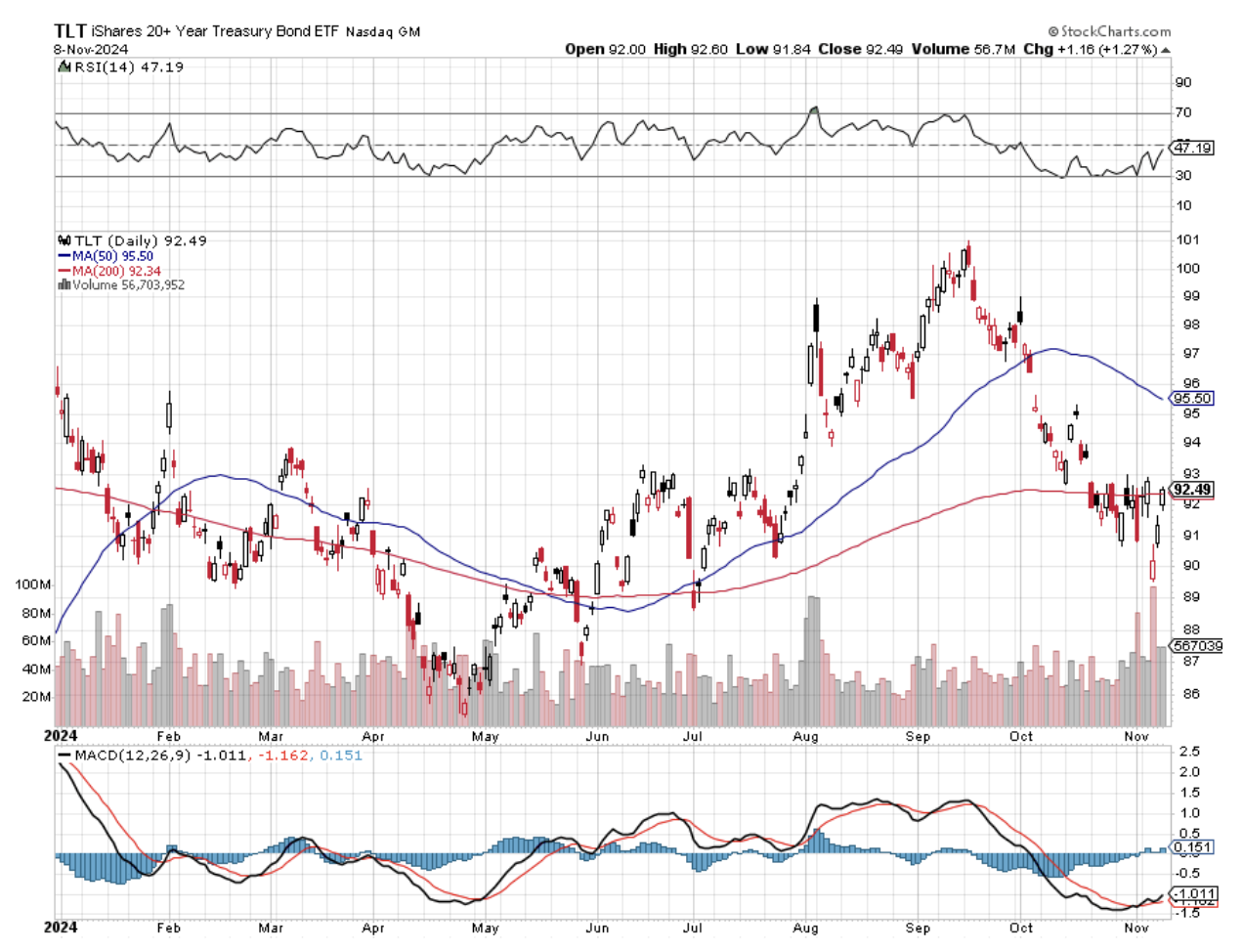

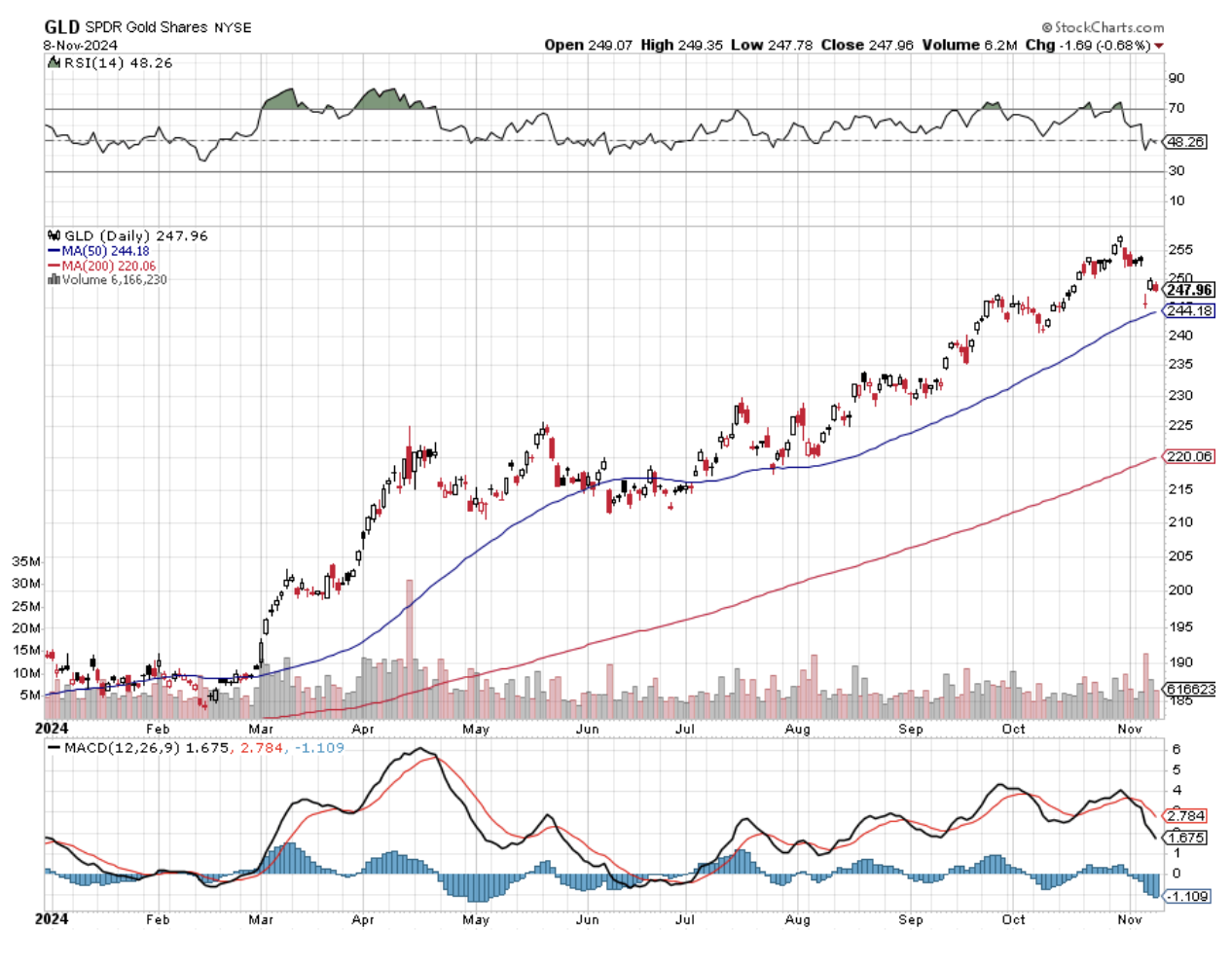

Falling interest rate plays are out. Don’t expect much performance from real estate, REITS (CCI), new homebuilders (DHI), gold GLD), and silver (SLV).

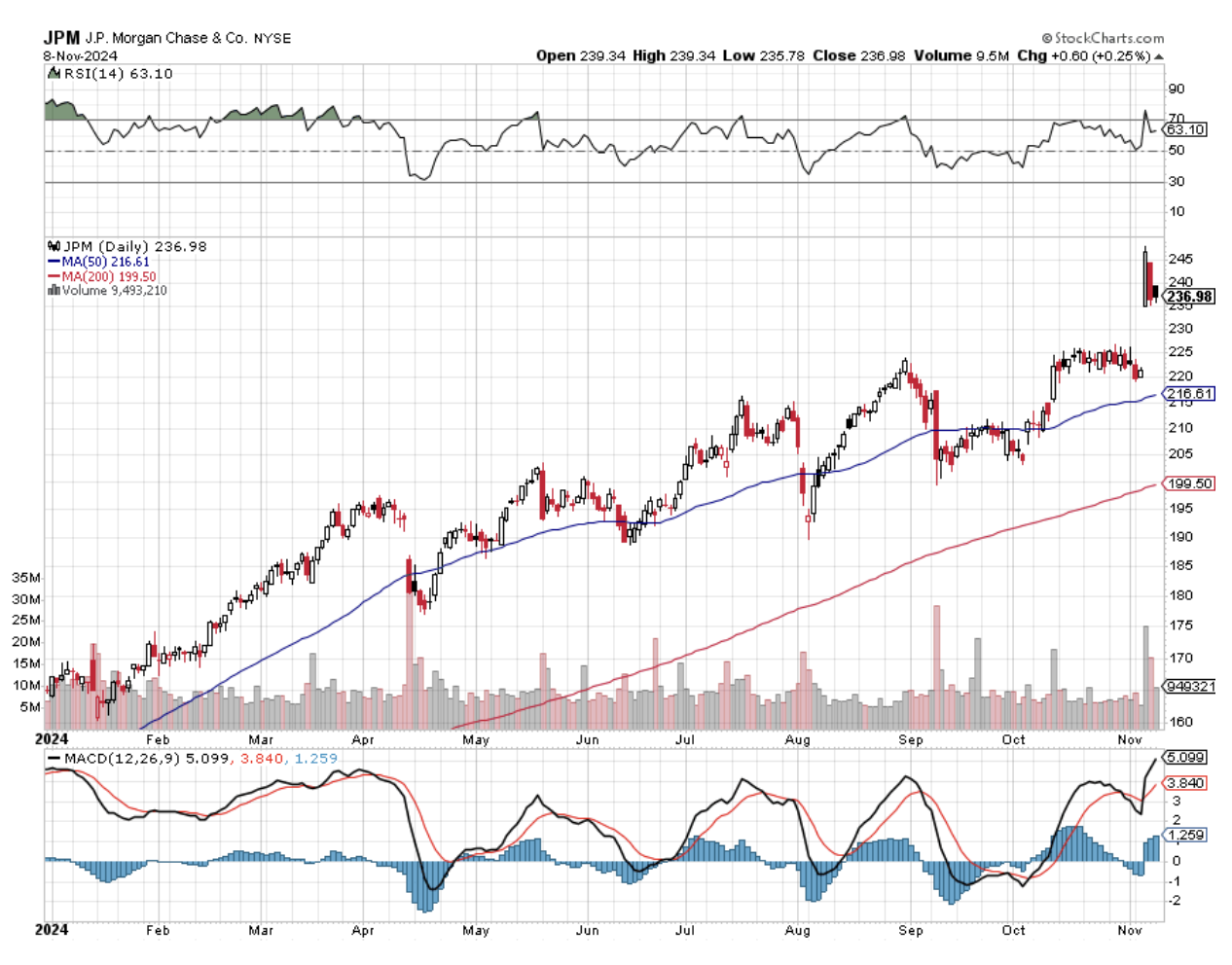

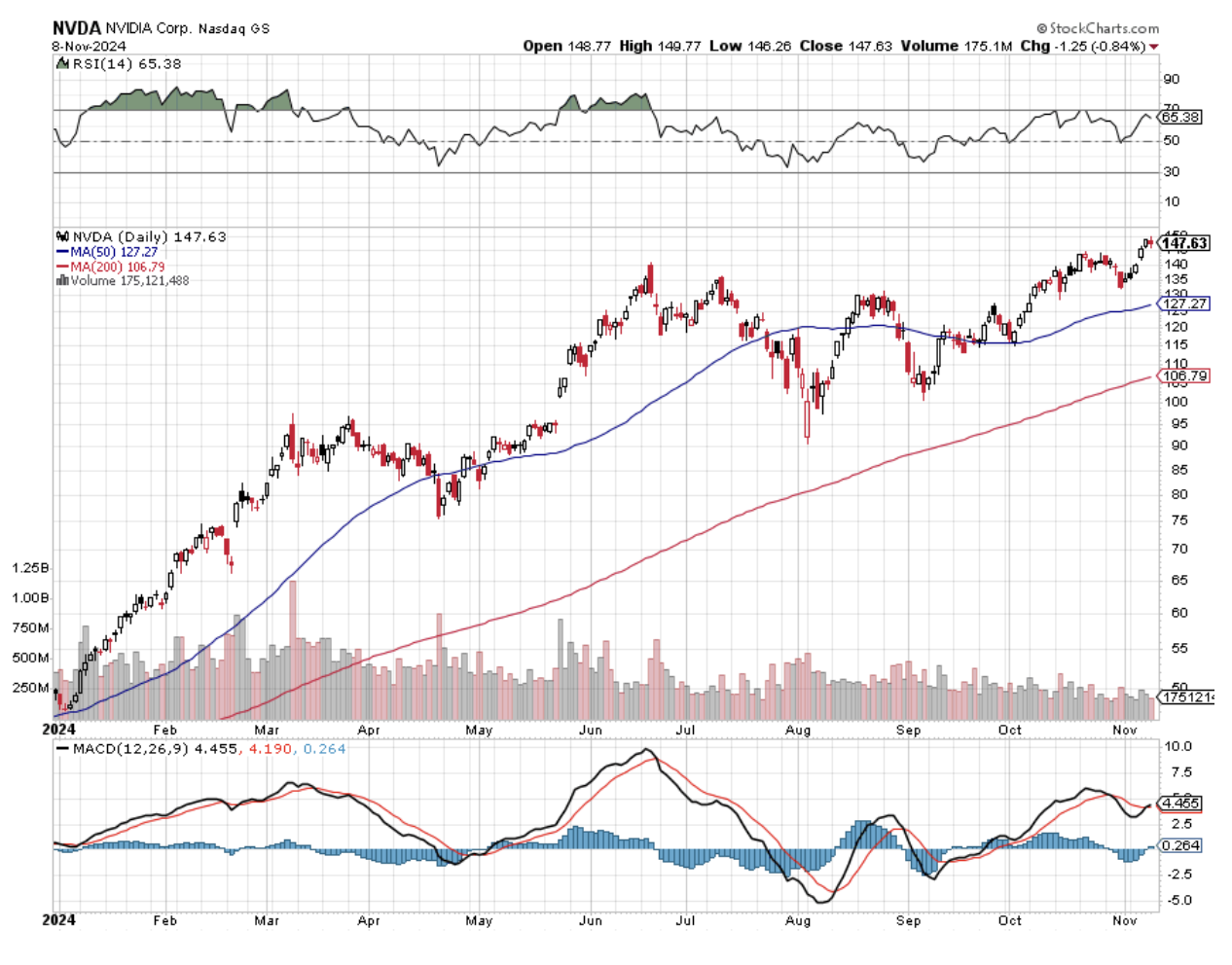

Deregulation plays are in. The good news is that this is a fairly wide sector. It includes banks (JPM), brokers (MS), money managers (BLK), new nuclear (CCJ), big tech that had been targeted by antitrust (NVDA) and (AMZN), and Tesla (TSLA).

Bonds are toast.

Promised Trump policies of tax cuts and spending increases will balloon the National Debt by $10-$15 trillion. The bond market is unlikely to be able to handle this amount of new issuance, especially with annual interest payments owed by the government already at $1 trillion. It is the second largest budget item after Social Security.

Selling into a national debt of $50 trillion is going to be completely different than selling into a national debt of $27 trillion when Trump last left office. This is the reason why major hedge funds are running Treasury bond shorts as their biggest positions, who were all Trump supporters and donors.

It all depends on inflation. This is not some far-distant theoretical thing. It is happening already. I got hit with several price increases today, and I am hearing about rises in other industries, like steel. The expectation is that a stronger economy can handle the price hikes.

So, the best case for bonds is that the (TLT) chops around here. The worst case is that we retest new lows at $82. It won’t help that the Federal Reserve is cutting interest rates by another 25 basis points on December 18. The Fed controls only overnight interest rates, not the 10–20-year bond market. Even if Trump appoints an ultra-dove as chairman of the Federal Reserve in 2026, bond vigilantes may have other ideas.

Then there is the matter of trade tariffs. I have been through many of these. Remember when Nixon banned the import of Japanese textiles in 1972? They don’t make textiles in Japan anymore because their rising labor costs drove that industry to China.

Trade wars are a negative sum game. There are only losers. The game is to punish your neighbors faster than they are punishing you. They shrink the pie.

If we raise tariffs on our allies, they will retaliate in kind. This will be a problem for big tech, which gets 50%-60% of their sales from abroad. Europe will target uniquely American products, like Captain Morgan rum. Notice that the brand owner, major exporter Diageo (DGE), saw its shares slaughtered last week. As a result, the price of everything here will soon start going up.

The (TLT) will be a great position to have going into the next recession. But the market won’t start discounting that for two or three years. That makes the (TLT) a trade for another day. In any case, there are better fish to fry.

Sell all (TLT) LEAPS now before they go down even more.

About that recession. Every bear market in my lifetime started with a Republican president. The pattern is always the same. Tax cuts, an excess stimulus, and deregulation lead to a higher high in the stock market as euphoria prevails. This leads to inflation, high interest rates, and recession.

This is not exactly an original thought. High rates caused the bear markets of 2008, which took the Dow Average down -52%, 2000 (-30%), 1990 (-30%), 1987 (30%). Previous bear markets in 1979 and 1973 were caused by oil shocks. 2027?

We shall see.

So make hay while the sun shines. The current euphoria binge will last three to six months. After that, we will need to reassess and start shopping for short plays among the most extreme moves, which I have already done with Tesla.

The bottom line for all of this is that equity returns for the next four years will be lower than the last four. If a recession hits, they could well be zero. This won’t be a problem if you get out at the top, as I did in 2008, 2000, 1990, and 1987. Conclusion: You need me now more than ever.

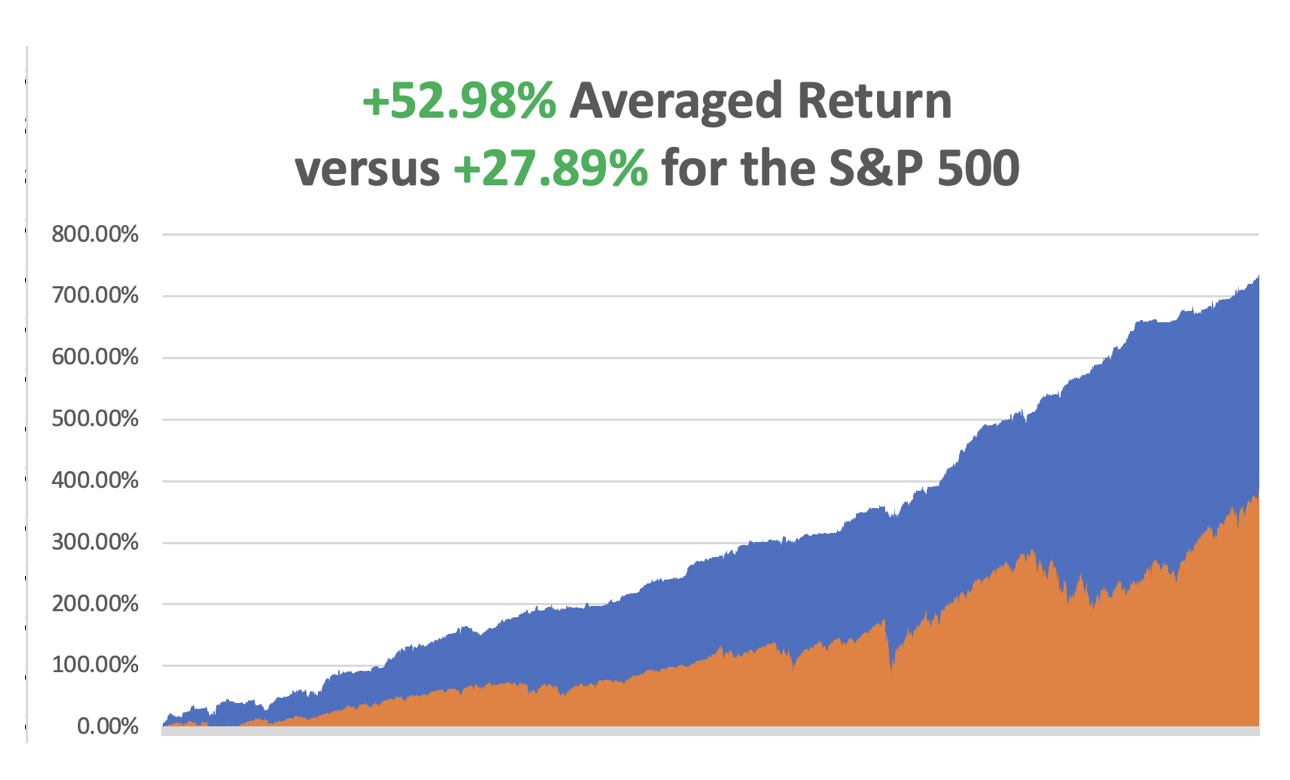

In November, we have gained a breathtaking +7.63%, thankfully because we went into the election with 70% cash and then poured money into deregulation plays. My 2024 year-to-date performance is at an amazing +60.77%.The S&P 500 (SPY) is up +25.73%so far in 2024. My trailing one-year return reached a nosebleed +69.73%. That brings my 16-year total return to +737.30%.My average annualized return has recovered to +52.98%.

I went into the election with two positions in (JPM) and (NVDA), which turned out to be great deregulations plays. I stopped out of my one interest-sensitive play in (GLD) near cost. I piled on new deregulation plays in (TSLA), (CCJ), and (MS). I also added a new short in (TSLA), taking advantage of a monster 60% implied volatility for the options.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 69 of 89 trades have been profitable so far in 2024, and several of those losses were really break evens. Some 22 out of the last 25 trade alerts were profitable. That is a success rate of +88.80%.

Try beating that anywhere.

My Ten-Year View – A Reassessment

When we have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at a headwind. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

My Dow 240,000 target has been pushed back to 2035.

On Monday, November 11 is Veterans Day, so banks, the bond market, and the post office will be closed. On Tuesday, November 12 at 6:00 AM EST, the NFIB Business Optimism Index takes place.

On Wednesday, November 13 at 8:30 PM, the Consumer Price Index rate is announced.

On Thursday, November 14 at 8:30 AM, the Producer Price Index is out.

On Friday, November 15 at 8:30 AM, the Retail Sales are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, I am writing this from a High Sierra peak at 12,000 feet in the at the beginning of winter. It is 15 degrees, and the wind is gusting at 70 miles an hour, turning my backpack into a sail and practically blowing me off the mountain. Over the side, the next stop is 1,000 feet below. I am thirsty, but the water in my canteen is frozen solid.

I had planned to follow my tracks in the snow back down to my car, but the wind had totally obliterated them. So, I am using an old-fashioned army compass to navigate back in total whiteout conditions. Good thing I got the letter out early today!

Actually, I am not writing this, I am thinking it. If I took my hands out of my heavy mittens, my fingers would freeze in seconds. Remember, no fingers, no Trade Alerts!

A couple of times a year, I feel the need to abandon civilization and contemplate the meaning of life while accomplishing a great physical challenge. For me, this is a mandatory religious experience.

This time, I attempted to emulate one of the great physical feats in history. In October 1847, the Donner Party’s wagon train was hopelessly snowed in at a Sierra pass. Starvation loomed. When word reached Sacramento, four rescue parties were sent out, only to be repulsed by driving blizzards.

Finally, a giant of heroic strength, the famous Snowshoe Thompson, who stood at 6’6”, broke through. He emptied his massive wood frame backpack of food and then stuffed it with the two smallest children he could find. He snowshoed back to safety 120 miles over three days, nonstop. The kids grew up to become the founding fathers of modern-day Marin County, California.

I thought, “Gee, I wonder if I could do that?”

So, I sought to replicate the feat, subject to a few modern compromises. Today, Interstate 80 sits astride Thompson’s original route. Instead, I determined to snowshoe 120 miles of the Tahoe Rim Trail around Lake Tahoe, with an average elevation of 9,000 feet. I figured that the 60-pound pack I usually carry was worth the weight of two kids.

My one concession to my advanced age was that instead of going nonstop or camping out at night, I would break the epic trek into ten days at 12 miles each. That allowed me to repair my Tahoe lakefront estate nightly to thaw out my toes, treat injuries, and get some shuteye. Howling winds keep you awake at night.

I fasted while accomplishing this, eating only 600 calories a day of raw fruit and nuts. I’m down about ten pounds since I began.

Hint to readers: almonds have unique, hunger-fighting chemical properties. Eat a handful before you go to sleep, and hunger pangs won’t wake you in the middle of the night. I plan on eating some industrial strength this Christmas, things like Tom and Jerry’s and See's Peanut Brittle, so I need to get ahead of the curve. (note to self: 223 calories in a cup of eggnog).

My friends call this a death march, make excuses why they can’t come, and worry about my sanity. I think of it as a cleansing and a general stocktaking, and I feel great! I always go alone. How many other 72-year-olds do you know who are in a condition to do this sort of thing?

Sure, I might break my ankle someday, die of exposure, and have my bones scattered by wild animals. Who cares? It would be a good death. It’s worth it.

The scenery up here is so spectacular that I almost didn’t feel the pain. Almost. On more than one occasion, while gazing at the endless shades of blue the pristine waters of Lake Tahoe offered, I tripped on my snowshoes.

Once, I landed on some tree roots, which cut right through to the bone in my left forearm. I managed to stop the bleeding by tying off a tourniquet with my teeth. When I got home, I then soaked the wound in Jack Daniels to ward off infection. It works every time! (see pics below). In a pinch, Stolichnaya Vodka works just as well. It’s an old combat first-aid trick.

While hiking along the East Ridge, succeeding mountain ranges in northern Nevada explored every shade of purple. I managed to summit each major peak around the body of water the Washoe Indians called “da-ow-a-ga”, or edge of the lake, which they considered the origin of the universe. Those included Squaw Peak (8,885), Mt Tallac (9,735 feet), Monument Peak (10,067), and Mount Rose (10,776 feet). When the trail got too steep, my trusty ice ax and crampons saw me through.

I was constantly reminded that I was in the “Old West” by the many artifacts I encountered. Prominent granite boulders displayed prehistoric Indian petroglyphs. I found a few abandoned log cabins, complete with potbelly stoves and canned food from the 1850s. Rusted-out cast iron mining equipment was strewn about everywhere, covered with snow. Along the old Pony Express Trail, one finds old horseshoes and the occasional ancient bottle turned purple by the sun.

Lake Tahoe supplied all the water and bracing wood for the Comstock silver mining boom of the 1870s. A hundred years ago, not a single tree was left standing, except for the southwest section of the lake owned by mining baron “Lucky Baldwin” who won it in a card game and made it his private retreat. It was all covered in meticulous and colorful detail for the Virginia City newspaper, The Territorial Enterprise, by a budding young newspaperman who went by the name of Mark Twain.

My ambitious goals often saw me hiking well into darkness. After the batteries died on my three backup headlamps, that flashlight app on the iPhone 5s proved a real lifesaver. It’s good for a full hour and illuminates the eyes of onlooking wildlife a bright yellow up to 200 yards away.

One night, I got back to the car and found that my keys had frozen and were useless. So, I sat on them. In 15 minutes, the car flashed its lights, and the doors magically opened. There was barely enough charge to get the engine started, a trick I accomplished by holding the key right up to the ignition button. Toyota designs them to do this. It’s no fun getting stranded at 10,000 feet at 10 degrees in the middle of nowhere. No Auto Club here!

I often looked behind to make sure a mountain lion was not stalking me. Don’t worry. Only 20 people have been killed by mountain lions in California over the last 100 years. More are killed by their pet dogs every year in the Golden State, mostly by pit bulls. Besides, I am good at staring down mountain lions and black bears. It is just a matter of attitude.

The old souvenir stand for the Ponderosa Ranch, of the TV series Bonanza fame, is now the Tunnel Creek Station Café and mountain bike rental. Good luck to Patty and Max! The nearby Flume Trail offers some of the best cross-country skiing in the world.

Of course, I am not just thinking Great Thoughts during these hikes. An endless series of economic and market data points are constantly churning around in the back of my mind, and I occasionally reach a “Eureka” moment. I keep a pen and notebook in my pack so I don’t forget these earth-shaking revelations.

It was during a similar expedition up the face of the Matterhorn in the Swiss Alps (14,692 feet) last summer when I realized that the S&P was beginning a long run up that would take it to 6,000 by yearend. I’ll never forget the expression on my guide’s face when I stopped midpoint through an abseil and started feverishly writing notes. That little maneuver cost me a bottle of schnapps. The readers and Trade Alert followers prospered mightily.

What is this year’s “Eureka” conclusion? The stock market could keep going up into 2025 but with more volatility. This year was a cakewalk, as my 69.3% trailing return testifies. After that, stocks will be unable to ignore the consequences of a Trump election.

I have been doing this sort of thing since I was 22 and was in somewhat better shape. Then, I was one of the few foreigners attending karate school in Japan, learning the iron discipline and focus of samurai warriors, known as “bushido”. The actor, Steven Segal, studied at a competing school down the street.

Every February, we underwent “kangeiko”, or “winter training. This involved the entire class running the five miles around Tokyo’s Imperial Palace in a pack, suffering freezing temperatures, barefoot, every day for a week. When we returned to the dojo, we were hosed down with ice-cold water, our feet senseless, bloody stumps. Then we would train for three more hours.

The idea was that the extreme pain and exhaustion would deliver insights into us and the world at large. It worked. At least one current reader endured the experience with me and is still alive. Remember that, David? By the way, thanks for knocking out my front teeth.

On the way home, I stopped in Sacramento for a well-deserved double cheeseburger, fries, and chocolate shake at In and Out Burger. You can’t take this diet and health thing too seriously. Snowshoe Thompson would have envied me.

Well, next week, it is back to normal. I’ll be glued in front of my screens, scouring the planet for the next great trading opportunity, although I’m not sure I’ll find many. Buying market tops is against my nature. What are you supposed to do when all of your forecasts and predictions come true? I have a feeling that the answer is not to make more forecasts and predictions.

Perhaps the right answer is to take another hike. Anyone care to join me?

Your Intrepid Reporter

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2013/12/John-Thomas-Hiking.jpg321426april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-11-11 09:02:442024-11-11 11:22:56The Market Outlook for the Week Ahead, or S&P 500 6,000 Target Achieved

Through the vast whole spectrum of public markets, the U.S. stock market, and specifically technology stocks, are dominating versus their peers from other countries.

Heck, even Apple, just one company from a small suburb in California, is valued at a price that is greater than the entire German economy.

Does that speak to how bad the German economy is, or does it speak to the potency of public tech companies in America?

The truth is probably a bit of both.

Then, take a second and try to absorb the fact that Apple hasn’t even integrated AI into its own products yet.

The future is bright for many tech stocks, and the rally will broaden out to non-Magnificent 7 stocks.

More granularly, the US will continue to lead by market cap share as artificial intelligence benefits expand beyond a few large tech names that have dominated the market rally over the past year to companies in various industries.

Revenue production and margin improvement will be the critical levers of expansion.

The first will come from the money pouring into AI benefiting companies outside of Big Tech. This plays out as tech companies buy AI chips from the likes of Nvidia (NVDA), and as they need more power, these AI operators are forced to spend with companies in the Utilities (XLU) and Energy (XLE) sectors.

As AI makes companies more efficient and eliminates the simplest work, eventually cutting down costs, US corporates should get a boost to profit margins.

Global equity markets, including retirement allocations to equities, are basically leveraged to Nvidia.

A non-US tech company will rise over the next decade and unseat the large tech companies currently driving the US market share, like Apple (AAPL), Nvidia, Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), and Meta (META) are almost zero.

When we look at the revenue possibilities and understand that AI will directly cut expenses by creating efficiencies, it’s hard to see tech stocks do anything but go higher in the long term.

Even then, there will be some dips, and they should absolutely be characterized as buying opportunities.

Just look at a 3-month chart of Apple, and each month has presented a dip buying opportunity on August 6th, September 16th, and October 7th.

Apple stock is up 7.5% in the past 3 months.

When everyone complains that tech stocks are too expensive, well, they will get more expensive.

As long as leverage is able to be tapped, institutions will tap it and look for that asymmetric trade to the upside.

Tesla has also proved how hard it is to bet against tech and Elon Musk.

It usually is a terrible idea.

The setup to Tesla’s earnings meant a very low bar, and Musk jumped over it to the tune of a 22% pop in Tesla stock.

Tech is clearly in a secular bull trend, and trying to get artsy to squeeze in a microdip on the short side usually has meant a loss-taking event.

Why even try?

It’s my job to tell readers to bet on tech going to the upside, especially the quality companies that accelerate revenue by harnessing the superpowers of AI.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-28 14:02:172024-10-28 15:42:32The Future Of Tech Stocks

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.