(MARKET OUTLOOK FOR THE WEEK AHEAD or DID JAY POWELL BLOW IT?) and CHASING EARNEST HEMINGWAY),

($VIX), (INTC), (CCI), (TLT), (COPX), (BHP), (USO) (NVDA), (SLV), (FXY), (CAT), (IWM), (IBKR), (AMZN), (GLD), (BRK/B), (DE)

Before I took off for the current trip to Europe, I logged into my Amazon Prime account to buy some lightweight polyester T-shirts, size 4XL. Not only are these ideal for long-distance hiking but they can be washed in a hotel sink and dried quickly when I am traveling too fast to use the house laundry.

The next morning when I logged into my laptop, my email account was flooded with ads for every kind of T-shirt in the world, from heavy-duty sports types FOR $100 to bargain basement $5 ones from China (although the Chinese ones were a little light on the 4X sizes).

That is Amazon’s AI at work. And you know what? It is getting smarter. And while the big fear among investors is that the US government will break up this retail giant for antitrust reasons, Amazon is integrating faster than ever. The impact on profits will be enormous.

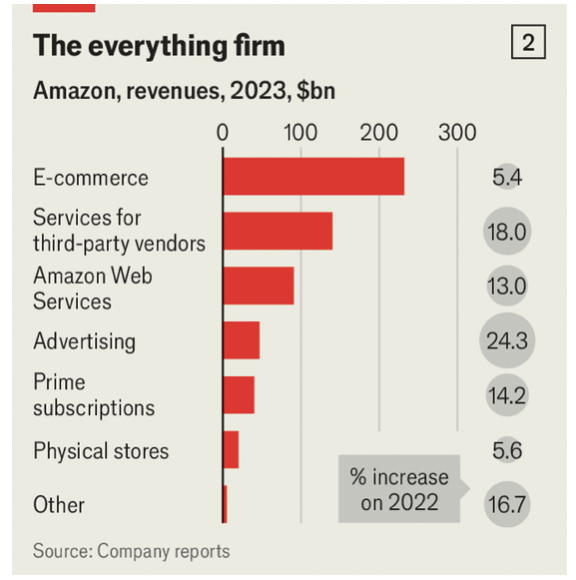

My friend Jeff Bezos’ creation has a lot to work with. Amazon not only pioneered online retail. It subsequently invented the Kindle, an e-reader (click here where the John Thomas autobiography is for sale) Alexa, a smart speaker and, more consequentially, cloud-computing—Amazon Web Services has a 31% share of that $300bn market (full disclosure: Mad Hedge uses their service).

It also runs Prime Video, America’s fourth-most-watched video-streaming service (full disclosure: Mad Hedge is a Prime member). Its newish, high-margin advertising business is already the third largest in the world behind Alphabet (GOOGL) (Google’s parent company) and Meta (META) (Facebook’s).

Amazon also has a few moonshot projects of its own. One subsidiary, Zoox, is building self-driving cars. Another, Kuiper, is developing a fleet of communications satellites in low-Earth orbit, in competition with SpaceX Starlink (full disclosure: Mad Hedge is a Starlink user).

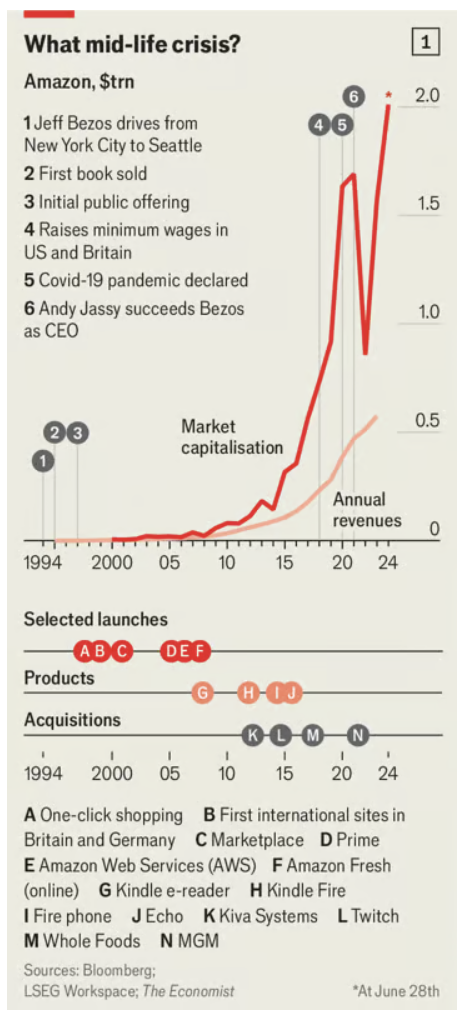

This year, Amazon’s websites will sell a staggering $554bn-worth of goods in America. That gives it a 42% share of American e-commerce, far beyond the 6% captured by Walmart (WMT), its nearest online competitor (and the country’s biggest retailer overall). The reward for all these efforts was a $2 trillion market capitalization in June and an all-time high share price of $203.

Amazon’s fourth decade looks poised to be an era of integration. The company has grown to the size that any needle-moving new investment is costly and high-risk. Andy Jassy, the former boss of AWS whom Bezos appointed as his successor as CEO in 2021, therefore appears keen to generate value by stitching the company’s existing businesses together more tightly.

Jeff, who I knew at Morgan Stanley, still retains a 9% stake after some hefty recent sales and a big say over strategy, seems to approve. This metamorphosis would make Amazon more similar to Apple (AAPL) and Microsoft (MSFT), two older big-tech rivals that have bundled and cross-sold their way to world domination in consumer devices and business software, respectively—and to $3trn valuations.

Retail and advertising appear to be the first to integrate. The thread running through the two businesses is Prime, Amazon’s $139 a-year subscription service, which has 300m-odd members around the world, providing shoppers with free delivery and access to Prime Video. Prime members like me spend twice as much on Amazon’s websites as non-members do and they tend to be logged in more often. Amazon also has intimate knowledge of their shopping behavior, which allows it to target ads more accurately.

Advertising is another great hope at Amazon. Advertisers are willing to pay handsomely for this service: analysts estimate that Amazon’s ads business enjoys operating margins of around a mind-blowing 40%, higher even than those of the cloud operation, not to mention the much less lucrative retail division.

Most of these ads, responsible for four-fifths of the company’s ad sales, are nestled among search results on its app or next to information about products, as with my above-mentioned T-shirts. But a growing share is coming from third-party websites and, most recently, from Prime Video. In January Amazon started showing commercials to viewers in America, Britain, Canada, and Germany.

Analysts reckon that video ads alone will boost Amazon’s ads sales by about 6% this year, adding $3bn to the top line. Given the ad operation’s fat margins, the impact on profit will be considerably larger.

To turn more Prime members into actual ad-watchers, Amazon is splurging on content. It recently signed a contract with Mr. Beast (??), a YouTube superstar, rumored to be worth $100m. It is trying to seal a deal in which it would pay $2bn a year for the rights to show National Basketball Association games on Prime Video. It is already reportedly spending $1bn annually to stream some National Football League (NFL) fixtures.

This hefty price tag is worth it, the company thinks, because popular sporting moments, such as “Thursday Night Football”, have turned out to be among the biggest sign-up days for Prime. Ads aired during sports events are some of the most lucrative in all of the ad business.

Analysts speculate that clever AWS software may also be assisting the retail operation’s 750,000 warehouse robots in sorting shoppers’ packages. And having a business as gigantic as Amazon’s retail arm as a captive customer gives AWS the confidence to scale up, helping spread costs.

The most important thread stitching Amazon’s two main businesses together is generative AI. Most rivals will struggle to match Amazon’s access to specialized AI hardware, which is in short supply but which it has in abundance thanks to long-standing commercial partnerships with companies like Nvidia (NVDA), which makes advanced AI semiconductors.

Amazon’s recent share-price rise was uninterrupted by a Fair Trade Commission lawsuit. But for every cloud customer that AWS loses to rivals such as Microsoft Azure or Google Cloud Platform, it could win one that is repelled by Microsoft’s and Google’s new businesses in their own increasingly tightly-knit empires.

It all looks like a giant, super-efficient machine to me which should justify at least a 50% gain in Amazon’s share price in the next year or two.

https://www.madhedgefundtrader.com/wp-content/uploads/2024/08/The-everything-firm.png580576april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-08-01 09:02:372024-08-01 10:14:35Why Amazon is the Most Undervalued AI Play Out There

Below please find subscribers’ Q&A for the June 12 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: How will Nvidia (NVDA) trade post-split?

A: Well, it’ll probably keep going up, because I think the year-end target—the old $1400, which is now $140—is still good. And I have a whole bunch of LEAPS, which are post-split $40, $50, $60 in-the-money, and I’m just keeping those. It’s a good cash management tool to have. So, even $500 points in the money, you’re still looking at about 20% returns by the end of the year on a January LEAPS. If you can buy the January 2025 $70-$71 LEAPS for 83 cents that’s a 20.48% profit at expiration in six months. So if you want a safe, very high return, that is the best way to do it in the financial markets, is to go way in the money. LEAPS will still pay you a lot of money amazingly. This trade will disappear someday but it’s there now and I’m taking it. Screw 90-day T-bills—I’m going into $500 in-the-money LEAPs on Nvidia, which pays four times as much.

Q: Is Broadcom Inc (AVGO) the next Nvidia?

A: There is no next Nvidia—the next Nvidia is Nvidia. Buy Nvidia on a 20% decline, which I think we may get sometime this summer. That’s a dip you want to buy for a year-end run to $140. Also, Broadcom isn’t exactly undiscovered at this point. It has doubled since October, while Nvidia is up 4 times. So if the bargain in the market for you is double in six months, I’m not sure you should be in the market. That said, I put out a report on split candidates last week and (AVGO) is very high on the list.

Q: What’s the best way to trade split candidates?

A: I actually just wrote a newsletter about this last week. There are in fact 36 high-priced, good money-earning split candidates, and I listed them all. You can buy really any of those if you’re looking for a high-priced stock that is growing. And management has a huge incentive to do splits because it makes the stock go up faster, and they’re all paid in stock options. So that is another reason you go into these. The best way to trade splits is buying the candidates because the biggest move is on the announcement of the split—you usually get 10%, 15%, or even 20% returns on the announcement.

Q: How do you envision AI in 10 years?

A: Well, it’s unimaginable. I can tell you from experiencing a lot of these big technology changes—it’s always tremendously underestimated by the markets, and you can safely bet on that. It’ll go up a lot more than you realize. That’s what happened when we jumped from six track tapes to cassettes, Betamax to VHS, teletypes to faxes, and faxes to emails. I thought Steve Jobs was crazy when he introduced the iPhone. Nobody makes money in handsets. But he proved me wrong.That makes my $240,000 DOW by 2030 projection completely reasonable.

Q: What will inflation do for the rest of the year, and how will it affect stocks?

A: Inflation will go flat to down for the rest of the year. And that is being driven by artificial intelligence—the greatest deflationary product ever created in the history of the economy. It’s unbelievable the rate at which AI is replacing real people in jobs. If you want a good example of that, I had to call Verizon yesterday to buy an international plan, and I never even talked to a human. They listed out three international plans in a calm, even male voice, and I picked one. Or go to McDonald's where $500 machines are replacing $40,000 a year workers. This is going on everywhere at the same time at the fastest speed I have ever seen any new technology adopted. So buy stocks, that’s all I can say.

Q: What’s your opinion on Arm Holdings (ARM)?

A: I love it. There are very few serious companies in the chip area, and this is one of them.

Q: Do you expect gold mining stocks to continue upward?

A: Yes, but the better play here is the metal. Gold and silver aren't being held back by inflation while the miners are. Plus, the main buyers in the market now are the Chinese, and they don’t buy gold miners—they buy gold, silver, copper, platinum, and uranium outright.

Q: What about Tesla (TSLA) long-term? Kathy Woods's target is $2000 long-term.

A: I think Kathy Woods is right. But we have to get through the nuclear winter in the EV space first, where suddenly the market got saturated. I think Tesla is the only one who could come out of this alive by cutting costs and advancing technology, as they have always done. When I bought my first Tesla Model S1 in 2010, the battery cost $32,000. Now it’s $6,000, and you get a lot more range. Did (GM) offer an equivalent cost improvement with internal combustion engines? So, yes, never bet against Elon Musk—that’s a good 25-year lesson on my part, and should be for you too.

Q: Can you elaborate on the lithium trades?

A: I listed three names in my letter last week, (SQM), (FMC), (ALB),and the only thing you know for sure is that they’re cheap now. They could stay cheap for another six or 12 months. But when you get a turnaround in the global EV market and the manufacturers start screaming for more lithium, and all of the lithium stocks will double, or triple and they’ll do it fairly quickly. You can’t beat a market bottom for getting involved. Just look at my above (NVDA) trade. Not only would they be good stocks buy, but it would be a good LEAPS buy down here because then you could get 4 or 5 times your money on a small move.

Q: Can you suggest Amazon (AMZN) LEAPS?

A: January 2025 $195-200 just out of the money, should give you a return of about 120% over the next 6 months. That gets you the annual yearend run-up. And that’s my conservative position. My aggressive ones are all in Nvidia.

Q: Do you think zero-day options have permanently forced the Volatility Index ($VIX) to the $12 handle?

A: Yes, I do; it’s killed that market. Something like 40% of all the optiontraders on the CBOE were trading the ($VIX) from the short side. Shorting the ($VIX) now would be madness. That has to bring tough times for that whole industry. Trading call spreads at a $12 volatility, you’re better off buying the LEAPS because the LEAPS give you much bigger returns with much less risk. And a $12 ($VIX) means you’re getting your LEAPS at half the historic price. I’m just waiting for a new market low to start pumping out the LEAPS recommendations. All the more reason to sign up for the Mad Hedge Concierge Service to get an early read into the LEAPS recommendations. For more information on that, contact support at support@madhedgefundtrader.com

Q: What will happen to Apple (AAPL) after the 11% surge?

A: It goes to $250 by the end of the year. Now that it has the kiss of AI on it, people will pour into it.

Q: Why is value lagging?

A: Because AI is entirely a growth story, and you look at all the domestic value stocks, they’re going absolutely nowhere. Value has been in the dog house for years and I’m in no hurry to get in there.

Q: What is the best dividend stock I can invest in right now?

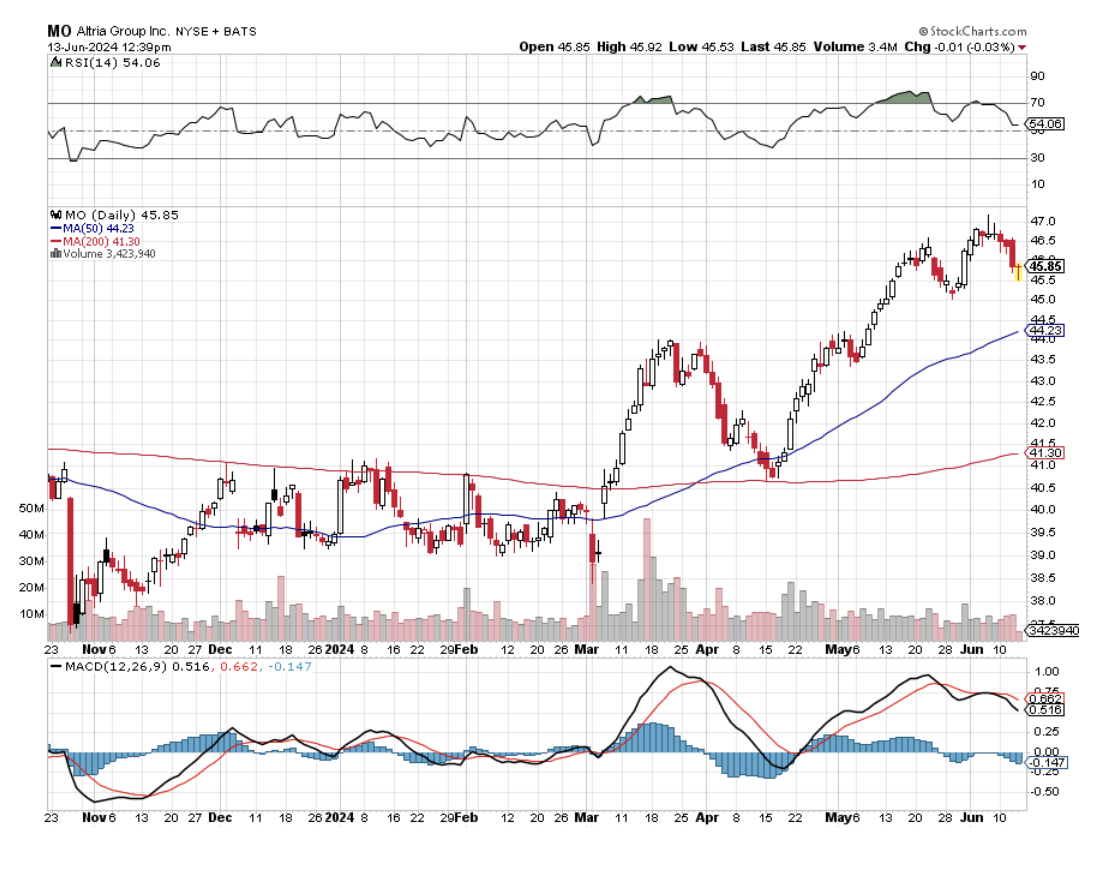

A: That’s an easy one.Altria (MO) has a 9% dividend—you can’t beat that. But you have to hold your nose when you buy this stock because they are in the cigarette business. However, their big growth now is in Asia ex-Japan where the government has a monopoly on tobacco, particularly China. Note that this is not an undiscovered idea; lots of people like a 9% dividend stock and (MO) has already gone up 20% this year, but I think there is still some money to be made here.

Q: How can we subscribe to get early LEAPS recommendations?

A: That would be the Concierge Service. Contact Filomena at customer support, and they will get you taken care of right away.

Q: What about the small nuclear plays?

A: I actually happen to know quite a lot about nuclear plant design, having worked for the Atomic Energy Commission in my youth, and the new designs address every major issue that held back nuclear power with the old 1950s designs. For example, building them underground and eliminated the need for these giant billion-dollar four-foot-thick reinforced concrete containment structures that dot the horizon. Not using pure Uranium alloys that can’t go supercritical is another great idea. So I like them. Are they good stock plays? Not right now. It takes a long time to introduce a new energy technology. Bill Gates is financing a new plant built by Terrapower in Wyoming, and it looks like a fantastic plant, but only Bill Gates could invest at this stage and expect to make money on it. He has very long-term money and you don’t. I would wait until you get a working model plant in the United States before going into these things, but potentially you’re looking at a 10 to 100 times return on your money if it works.

Q: Should I invest in Airbnb (ABNB) because of increased international travel?

A: Yes, we like Airbnb. Especially since they will get a push with the Paris Olympics next month. Not only does that get people to Paris, but it gets people to all of Europe because they usually add on additional trips to a visit to the Olympics.

Q: What would you do in Netflix (NFLX), and what strikes would you use?

A: I would do a LEAPS. Wait for a correction, at least 10%, preferably 20%, and then I would go at the money one year out and that would get you about 100% return. So, that’s the way to do that. This is not LEAPS territory right here —all-time highs are not LEAPS territory. You want to put on LEAPS when everyone else is throwing up on their shoes; the last time they did that was October 26.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

(The Mad June traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE MALLARD MARKET and ME AND 23 AND ME),

(AAPL), (GOOGL), (AMZN), (TSLA), (MSFT), (META), (AVGO), (LRCX), (SMCI), (NVR), (BKNG), (LLY), (NFLX), (VIX), (COPX), (T), (NVDA), (LEN), (KBH)

There’s nothing like the comfort and self-satisfaction of having a 100% cash position in a falling market. While everyone else is bleeding red ink, I am happily plotting my next trades.

Of course, the rest of the market isn’t really bleeding red ink, just giving up windfall profits. Still, it’s better to trade from a position of strength than weakness. It makes identifying the next winners easier.

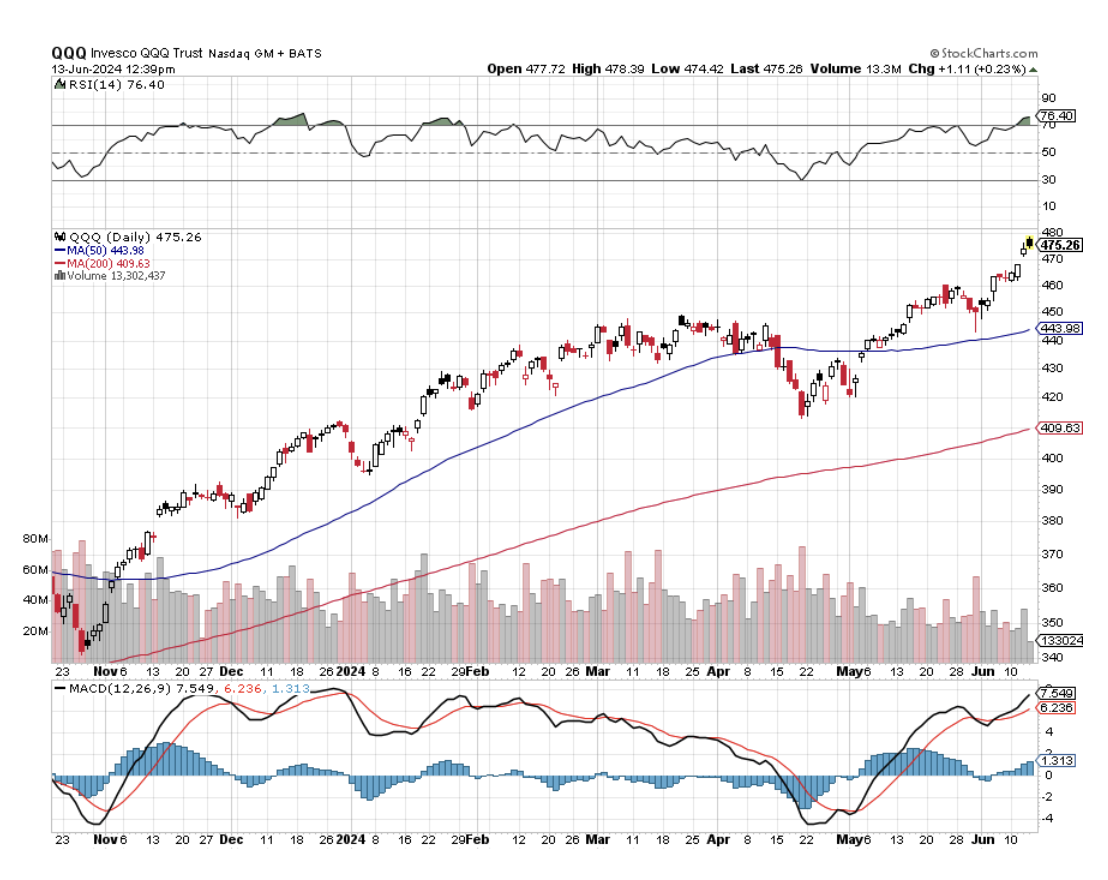

Think of this as the “Mallard Market”. On the surface, it seems calm and peaceful, while underwater, it is paddling along like crazy. The damage has been unmistakable. Dell, the faux AI stock (DELL) crashed by 28%, Salesforce (CRM) got creamed for 34%, and ServiceNow (NOW) got taken to the woodshed for 22%.

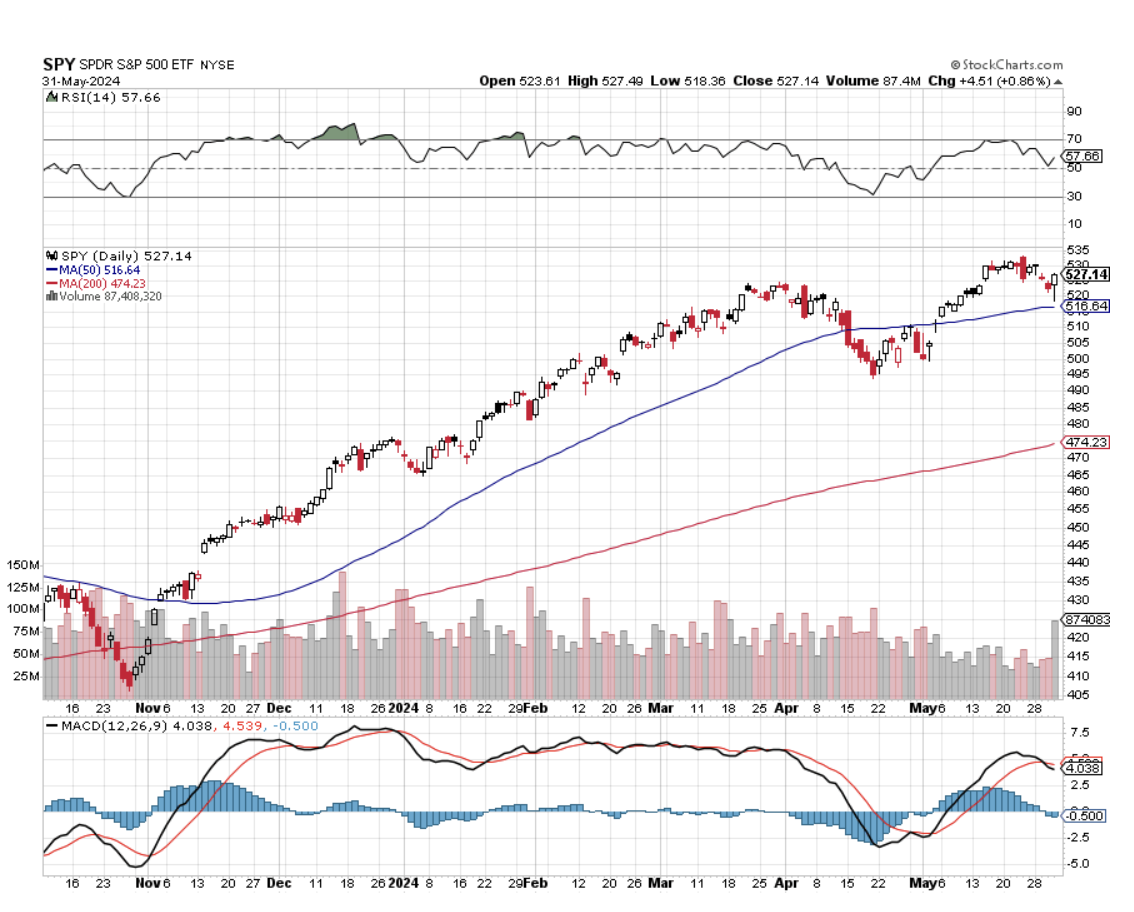

It all belies a market that is incredibly nervous and fast on the trigger. The tolerance for any bad news is zero. Yet there has been no market crash as I expected. The 5,300 level for the (SPX) seems to possess a gravitational field, powered by $250 earnings per share and a multiple of 51X.

It was NVIDIA that put the writing on the wall by announcing a 10:1 split that has opened the floodgates for similar prosperous and high-priced companies.

There are now 36 stocks with share prices of $500 or more ripe for splits with $7 trillion in market cap, or 16% of the total market. While splits don’t change the value of a company, perceptions are everything, as they prove shareholder-friendly policies. While individual investors are confused by an onslaught of contradictory research recommendations, splits are a great “tell” on what to buy next.

Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), and Tesla (TSLA) have already carried out splits, some multiple times, to great success. Of the Magnificent Seven, only Microsoft (MSFT) and Meta (META) have yet to split.

In the tech area Broadcom (AVGO), Lam Research (LRCX), Super Micro Computer (SMCI), and Service Now (NOW) have yet to split. In the non-tech area, there are NVR Inc. (NVR), Booking Holdings (BKNG), Eli Lilly (LLY), and Netflix (NFLX). Many of these are well-known Mad Hedge recommended stocks.

History has shown that stocks rise 25% one year after a split compared to 12% for the market as a whole. A stock’s addition to the Dow Average or the S&P 500 (SPY) provides a boost. If both occur, stocks will absolutely explode. Stock splits are also much more attractive than buybacks at these high prices.

So, I’ll be trolling the market for split-happy candidates.

You should too.

Since it may be some time before we capitulate and take a worthwhile run at new highs, I thought I’d update you on the global demographic outlook, which is always a long-term driver of economies and markets.

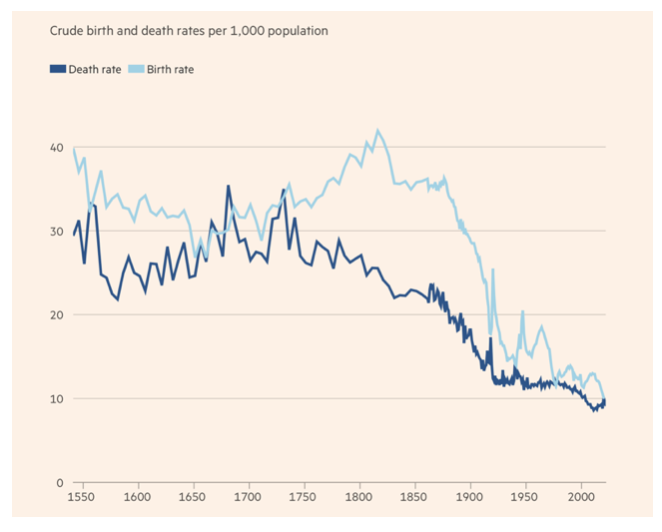

People are now living longer than ever before. But postponing death is only a part of the demographic story. The other is the decline in births. The combination of the two is creating huge changes in the global economy.

The notion of a “demographic transition” is almost a century old. Human societies used to have roughly stable populations, with high mortality matched by high fertility. Families had eight kids and 3-5 usually died in childhood, barely maintaining population growth.

In England and Wales in the 18th and 19th centuries, death rates suddenly plummeted. But fertility did not. The result was a population explosion. As the benefits of economic growth and advances in medicine and public health spread, most of the world has followed a similar transition, but far faster. As a result, human numbers rose fourfold over the last hundred years, from 2 billion to 8 billion.

In time, fertility followed mortality on a downward path across most of the world. As a result, fertility rates in more than half of all countries and territories in 2021 fell below the replacement level. For the world as a whole, the fertility rate was 2.3 in 2021, barely above the replacement of 2.1, down from 4.7 in 1960.

For high-income countries, the fertility rate was a mere 1.6, down from 3.0 in 1960. In general, poor countries still have higher fertility rates than richer ones, but they have been falling there, too.

What explains this collapse in fertility rates? An important part of the answer is the wonderful surprise that more children survived than expected. So, people started to practice various forms of birth control.

But the desire to have many children also shrank sharply. When husbands realized that smaller families meant high standards of living for themselves, family sizes dropped sharply. Even in ultra-conservative Iran, the fertility rate has collapsed from 6.6 in 1980 to only 1.7 in 2021.

A big reason for this shift was that, for their parents, children have moved from being a valuable productive asset in the 19th century to an expensive luxury today. That was back when 50% of our population worked on farms. Today it’s only 2%.

In the meantime, female participation in the economy rose dramatically in the 20th century, including in highly skilled careers. That raised the “opportunity cost” of producing children, especially for mothers. So, they have children later, or even not at all.

Where public childcare is more generous women are encouraged to combine careers with having children. The absence of such help helps explain the exceptionally low fertility rates in much of East Asia and Southern Europe, where parental support is limited.

This global shift towards very low fertility, with the exception (so far) of sub-Saharan Africa, is among the most important events driving the global economy. One implication is that the population of Africa is forecast to be larger than that of all today’s high-income countries, plus China by 2060, thanks to the elimination of many diseases there.

Why is all this important?

Because rising populations create larger markets, more profits for corporations, and rising share prices. Shrinking populations have the opposite effect, as China is learning about its distress now. One reason the US is growing faster than the rest of the world is that a continuous stream of new immigrants since its foundation has created endless numbers of new workers and customers. Dow 240,000 here we come!

Just thought you’d like to know.

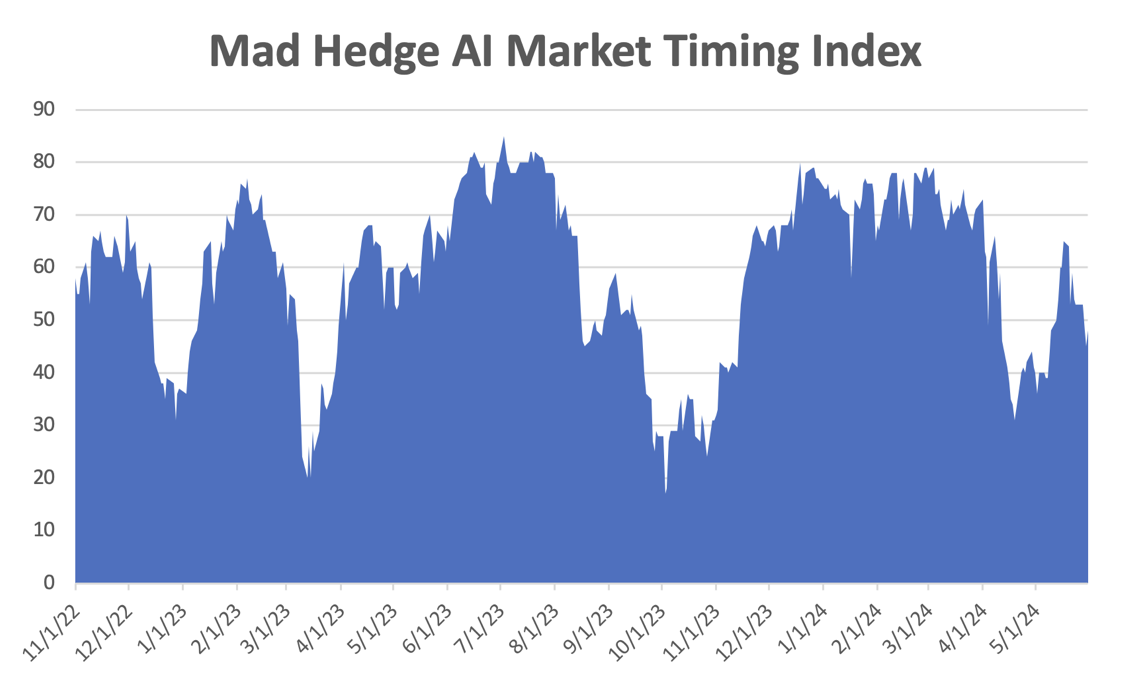

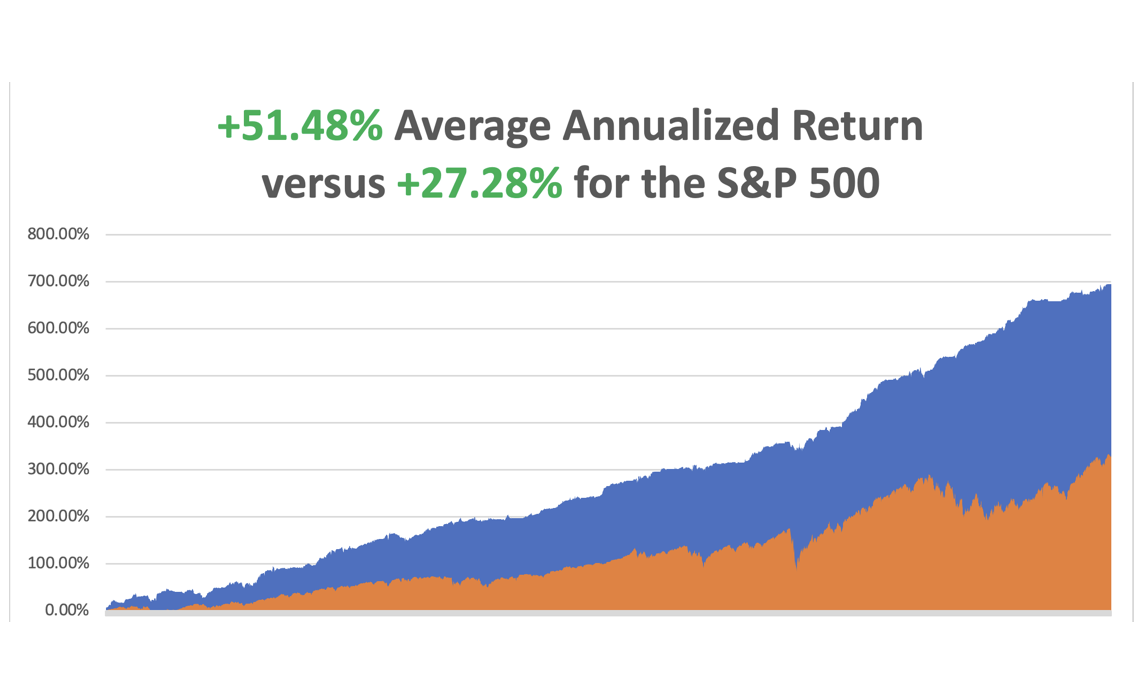

So far in May, we are up +3.74%. My 2024 year-to-date performance is at +18.35%.The S&P 500 (SPY) is up +10.48%so far in 2024. My trailing one-year return reached +35.74%. That brings my 16-year total return to +694.78%.My average annualized return has recovered to +51.48%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I bailed on my last position early in the week, covering a short in Apple for a profit.

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

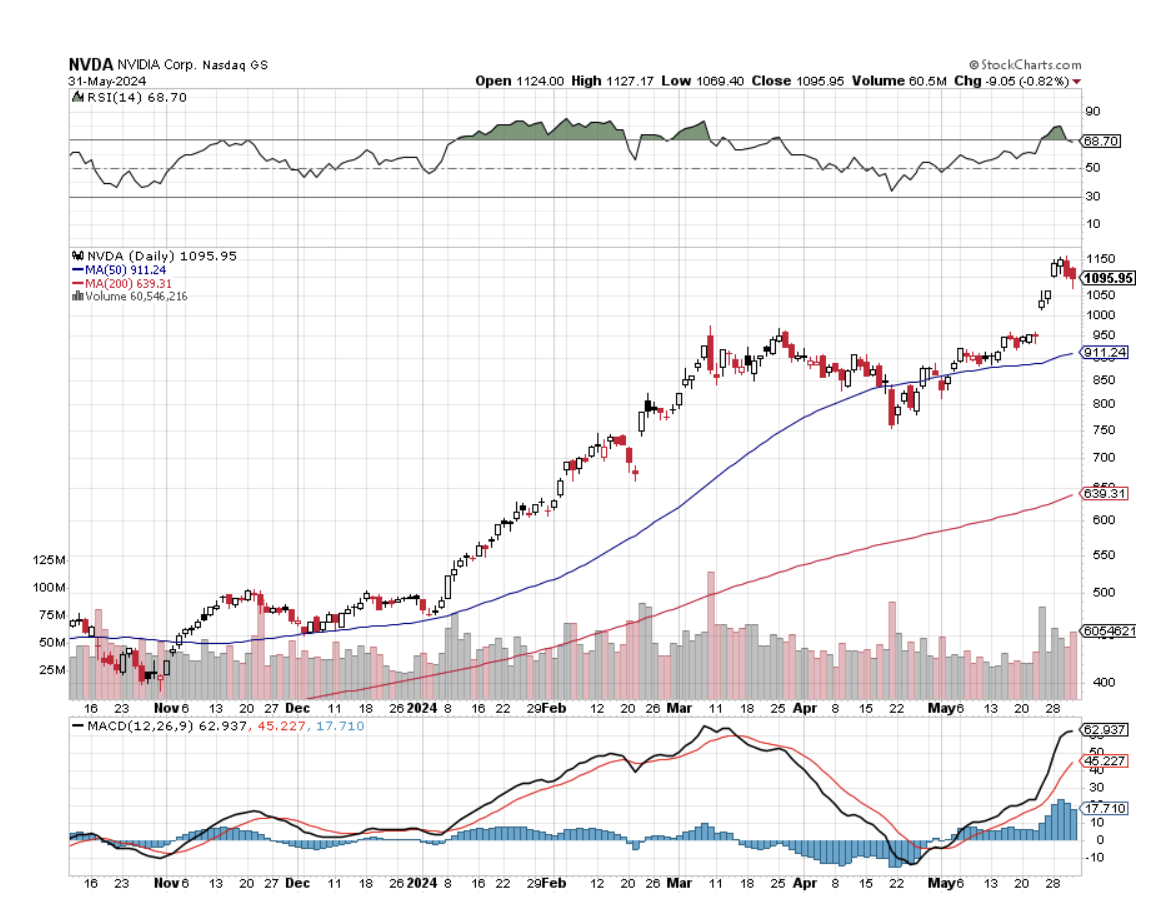

The Fed’s Favorite Inflation Gauge Cools by 0.2% in April, with the PCE, or the Personal Consumer Inflation Expectations Price Index. This one strips out the volatile food and energy components. It gives more credibility to a September rate cut and gave bonds a good day. NVIDIA Shares Continues to Go Ballistic, creating another $800 billion in market capitalization in three trading days. That is the most in history. That took NASDAQ to a new all-time high at 17,000. At $2.8 trillion (NVDA) could become the largest publicly traded company in the world in another day. Today’s tailwind came from an Elon Musk comment that his new xAI start-up would buy the company's high-end H100 graphics cards. Buy (NVDA) on the next 20% dip.

Pending Home Sales Dive, down 7.7% in April, the worst since the Covid market three years ago. The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market. But the anticipated rate cuts later this year should lead to better conditions, with improved affordability and more supply. Buy (LEN) and (KBH) on dips.

Money Supply Rises for the First Time in More than a Year. Remember money supply? As measured by M2, it sums up the currency, coins, and savings deposits held by banks, balances in retail money-market funds, and more. Data for April released on Tuesday afternoon showed an increase of 0.6% from a year ago. The Fed balance sheet has shrunk by $1.5 trillion in two years, the fastest decline in history, slowing the economy.

AT&T’s (T) Copper is Worth More Than the Company, and with plans to convert half its copper network to fiber by 2025 could free up billions of tons of the red metal to sell on the market. Copper prices have doubled over the past two years, and they could double again by next year. Worldwide there are 7 trillion tons of copper wire in place. Fiber is cheaper and exponentially more efficient than copper, which is facing huge demands from AI, EVs, and the electrification of the grid. Buy copper (COPX) on dips.

Markets are Underpricing Low Volatility (VIX), not a good thing at all-time highs. Volatility across equity and currency markets is low. The Volatility Index (VIX) at $12.46 compares with an average over five years of $21.5 and over the longer term of $19.9. Markets are heavily discounting good news and a disinflationary environment. It is not only stocks. There is also low volatility across currency markets. The DB index of foreign exchange volatility is at $6.3 versus an average of $7.6 over five years and $9.3 over the longer term. This will end in tears.

S&P Case Shiller Jumps to New All-Time High, with its National Home Price Index. The index rose by 1.29%, the fastest growth since April 2023. All 20 major metro cities were up last month and gained 6.5% YOY. Four cities are currently at all-time highs: San Diego, Los Angeles, Washington, D.C., and New York. Prices in San Diego saw the biggest gain, up 11.4% from February of 2023. Both Chicago and Detroit reported 8.9% annual increases. Portland, Oregon, saw the smallest gain in the index of just 2.2%. Unaffordability is the big story in the market right now. The sunbelt is seeing the most weakness, thanks to a post-pandemic construction boom.

Space X’s Starlink Tops 3 million Subscribers, and is rapidly moving towards a global WiFi network. I set up a dozen of these in Ukraine last October and even the Russians couldn’t hack them. It sets a global 200 Mb standard usable in most countries, even the remote Galapagos Islands in the Pacific. It’s only a VC investment now but could become Elon Musk’s next trillion-dollar company.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 3, the ISM Manufacturing PMI is released.

On Tuesday, June 4 at 7:00 AM, the JOLTS Job Openings Report will be published.

On Wednesday, June 5 at 7:00 AM, the ISM Services PMI is published.

On Thursday, June 6 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Challenger Job Cuts Report.

On Friday, June 7 at 8:30 AM, the Nonfarm Payroll and headline Unemployment Rate are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when Anne Wojcicki founded 23andMe in 2007, I was not surprised. As a DNA sequencing pioneer at UCLA, I had been expecting it for 35 years. It just came 70 years sooner than I expected.

For a mere $99 back then they could analyze your DNA, learn your family history, and be apprised of your genetic medical risks. But there were also risks. Some early customers learned that their father wasn’t their real father, learned of unknown brothers and sisters, that they had over 100 brothers and sisters (gotta love that Berkeley water polo team!), and other dark family secrets.

So, when someone finally gave me a kit as a birthday present, I proceeded with some foreboding. My mother spent 40 years tracing our family back 1,000 years all the way back to the 1086 English Domesday Book (click here)

I thought it would be interesting to learn how much was actually fact and how much fiction. Suffice it to say that while many questions were answered, alarming new ones were raised.

It turns out that I am descended from a man who lived in Africa 275,000 years ago. I have 311 genes that came from a Neanderthal. I am descended from a woman who lived in the Caucuses 30,000 years ago, which became the foundation of the European race.

I am 13.7% French and German, 13.4% British and Irish, and 1.4% North African (the Moors occupied Sicily for 200 years). Oh, and I am 50% less likely to be a vegetarian (I grew up on a cattle ranch).

I am related to King Louis XVI of France, who was beheaded during the French Revolution, thus explaining my love of Bordeaux wines, women wearing vintage Channel dresses, and pate foie gras.

Although both my grandparents were Italian, making me 50% Italian, I learned there is no such thing as pure Italian. I come out only 40.7% Italian. That’s because a DNA test captures not only my Italian roots, plus everyone who has invaded Italy over the past 250,000 years, which is pretty much everyone.

The real question arose over my native American roots. I am one-sixteenth Cherokee Indian according to family lore, so my DNA reading should have come in at 6.25%. Instead, it showed only 3.25% and that launched a prolonged and determined search.

I discovered that my French ancestors in Carondelet, MO, now a suburb of Saint Louis, learned of rich farmland and easy pickings of gold in California and joined a wagon train headed there in 1866. The train was massacred in Kansas. The adults were all killed, and the young children were adopted into the tribe, including my great X 5 Grandfather Alf Carlat and his brother, then aged four and five.

When the Indian Wars ended in the 1880s, all captives were returned. Alf was taken in by a missionary and sent to an eastern seminary to become a minister. He then returned to the Cherokees to convert them to Christianity.By then, Alf was in his late twenties so he married a Cherokee woman, baptized her, and gave her the name of Minto, as was the practice of the day.

After a great effort, my mother found a picture of Alf & Minto Carlat taken shortly after. You can see that Alf is wearing a tie pin with the letter “C” for his last name Carlat. We puzzled over the picture for decades. Was Minto French or Cherokee? You can decide for yourself.

Then 23andMe delivered the answer. Aha! She was both French and Cherokee, descended from a mountain man who roamed the western wilderness in the 1840s. That is what diluted my own Cherokee DNA from 6.50% to 3.25%. And thus, the mystery was solved.

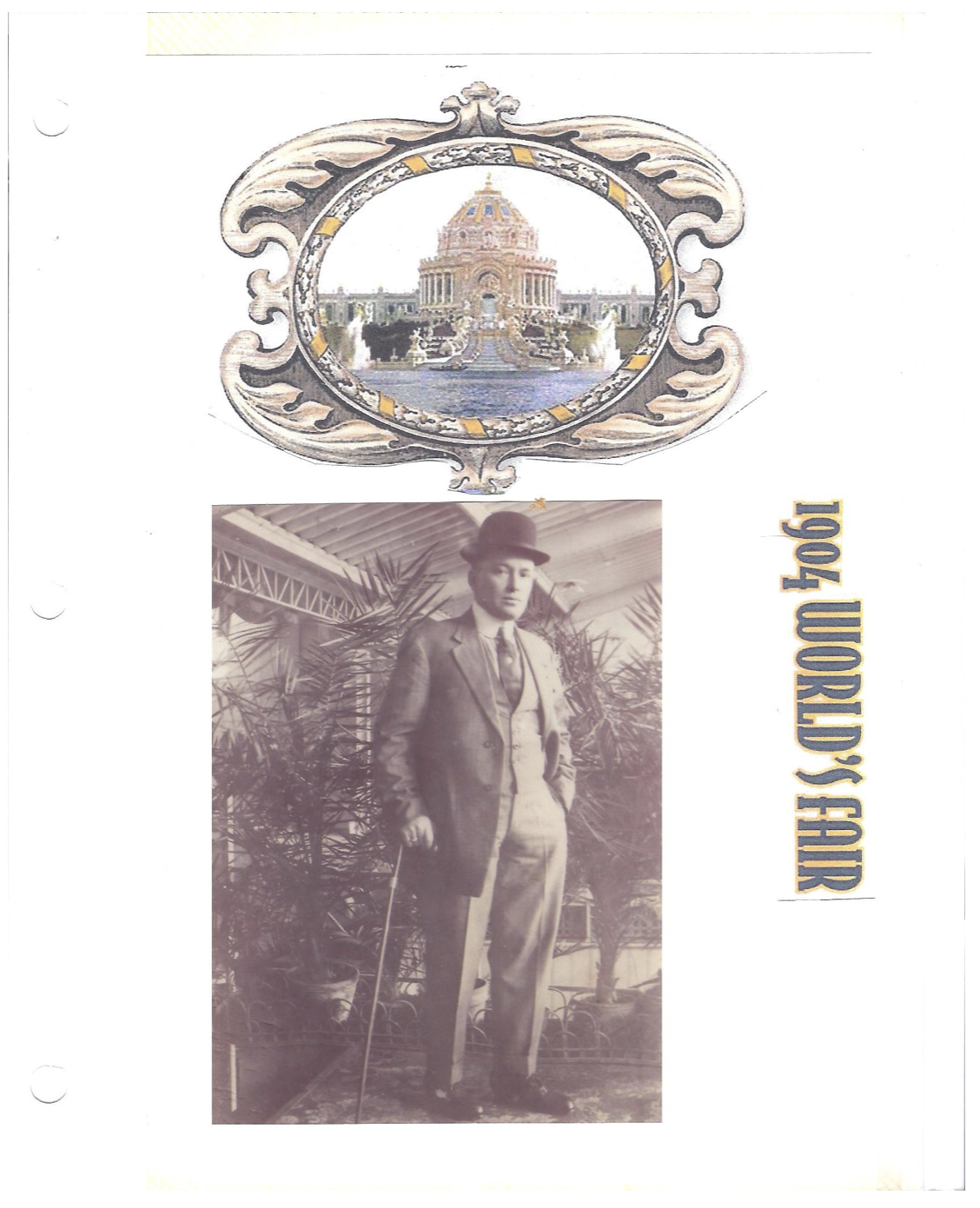

The story has a happy ending. During the 1904 World’s Fair in St. Louis (of Meet Me in St. Louis fame), Alf, then 46, placed an ad in the newspaper looking for anyone missing a brother from the 1866 Kansas massacre. He ran the ad for three months and on the very last day, his brother answered and the two were reunited, both families in tow.

Today, getting your DNA analyzed starts from $119, but with a much larger database, it is far more thorough. To do so, click here.

My DNA Has Gotten Around

It All Started in East Africa

1880 Alf & Minto Carlat, Great X 5 Grandparents

The Long-Lost Brother

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/01/alf-minto.jpg252293april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-03 09:02:142024-06-03 11:56:52The Market Outlook for the Week Ahead, or Welcome to the Mallard Market

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.