(The Mad MARCH traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HIGHER HIGHS)

(NVDA), (META), (IWM), (AMZN), (RIVN), (SNOW), (GLD), (GOLD), (NEM), (FXI), DELL), (AAPL), (TSLA), (CCJ), ($NIKK), (USO), (GOLD)

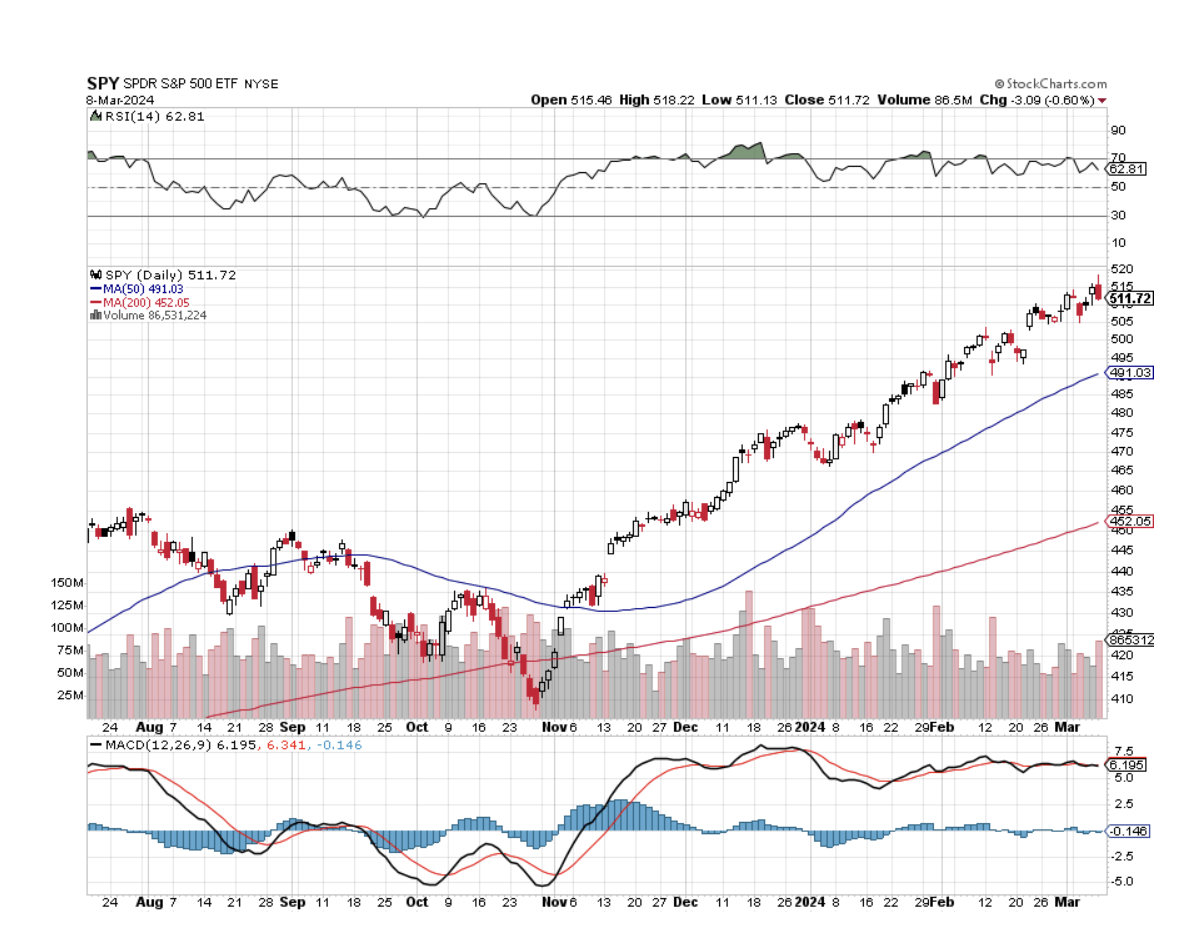

I was all ready to write another hyper-bullish report for the week. That was at least until noon EST on Friday. That’s when NVIDIA (NVDA) Peaked at $955 and then free fell $100 to $855. New all-time and then a new intraday low on huge volume and that is the textbook definition of a market top.

Not that we should be complaining. At the high, (NVDA) was up an unimaginable 105% so far this year. I spent my week buying back short put options for 50 cents that I initially sold for $20. With a quarterly quadruple witching due this Friday, anything can happen.

By the end of February, more than half of all analyst 2024 yearend targets were met. The response was a rush to raise yearend targets, triggering the current melt-up.

It always ends in tears.

And I’m about to tell you something that you will absolutely love to hear. Lower interest rates dramatically increase corporate stock buybacks, already set at $1.25 trillion for 2024. That’s because of the lower cost of capital.

What do more share buybacks automatically bring? High stock prices, especially for large positive cash flow companies like big tech.

As much as the permabears hate to admit it, good news really is good news.

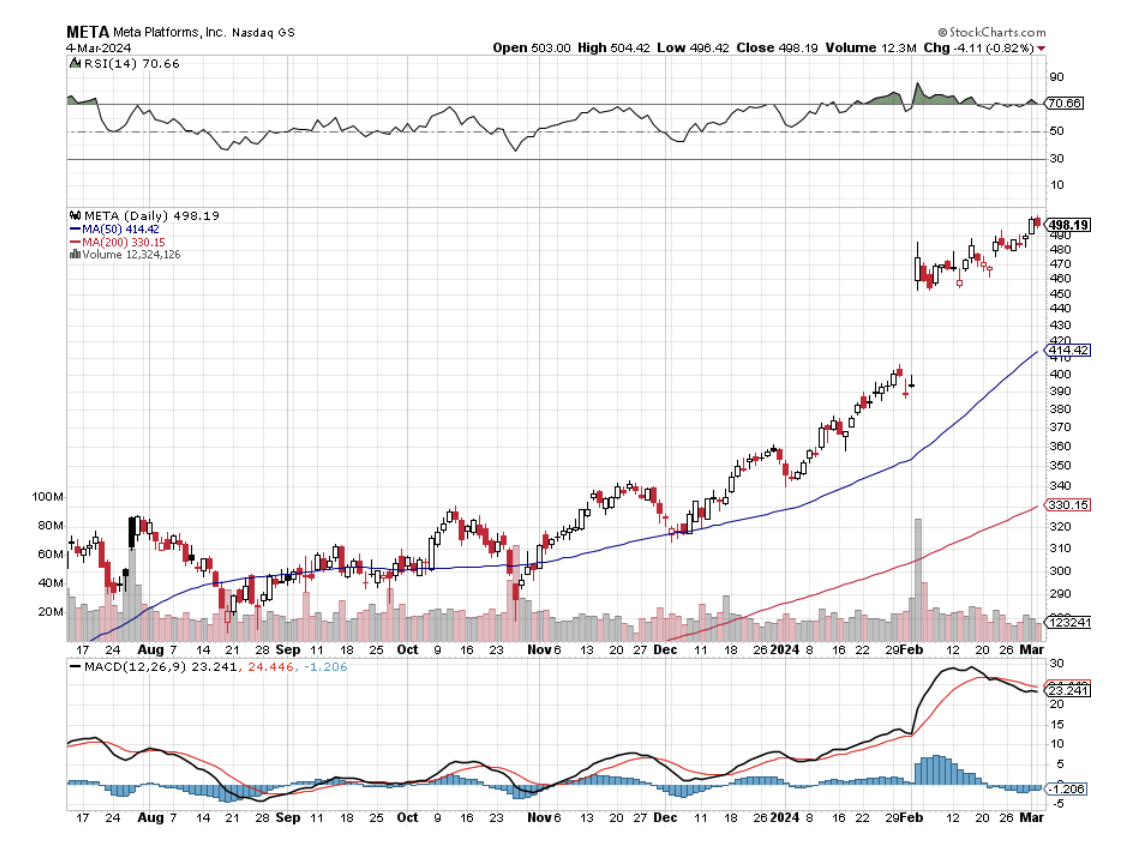

With all of the media obsession with NVIDIA (NVDA), my largest holding, and Meta (META), the fact is that the rally is broadening out. More than half of all industrial stocks are trading at all-time highs. Long-forgotten small caps (IWM) are also approaching 2021 all-time highs.

Going into this week managers were either overweight big tech and extremely nervous or out of big tech and kicking themselves. The urge to rotate is strong. But your standby rotation sectors, industrials, biotech, and banking have also seen big moves.

Which brings us to the subject of gold (GLD).

After a tedious one-year sideways consolidation, the barbarous relic blasted out to the upside above $2,200 an ounce, a new all-time high. After soaking up as much gold as they could over the past decade, China and Russia have finally taken the gold market net short, which is why we saw such dramatic price action.

With interest rates in the US soon to fall, the opportunity cost of owning non-yielding gold is about to shrink. That will cut the knees out from under the US dollar prompting a stampede into precious metals and Bitcoin.

Except this time, it’s different.

Gold miners usually outperform the yellow metal by four to one to the upside. Not so this time. Barrick Gold (GOLD) and Newmont Mining (NEM) were barely able to keep pace with the barbarous relic. That’s because inflation has boosted their costs and cut profit margins. After all, they are stock first and gold plays second.

Still, if gold reaches my $3,000 target in 2025 the LEAPS I sent out for (GOLD) last June should easily hit its maximum profit point of 298%.

That other weak dollar play, oil (USO) may not deliver the joys of past cycles and may in fact be trapped in a fairly narrow $60-$80 range. The futures markets are saying that the price of Texas tea will be lower in a year.

The US is now the world’s top oil producer at 13 million barrels/day and that is rising (thanks to enormously generous tax breaks), capping prices. Non-OPEC+ production is increasing, especially from Brazil and Canada. China, the world’s largest oil importer is missing in action. But low inventories, especially at the American Strategic Petroleum Reserve, are preventing a crash as well. Shale production is growing.

Still, even a $20 rally can have a dramatic impact on the share prices of the big US producers, like Exxon (XOM) and Occidental Petroleum (OXY), some 25% of which is now owned by Warren Buffet. Even without some sexy price action, this sector pays some of the highest dividend yields in the markets.

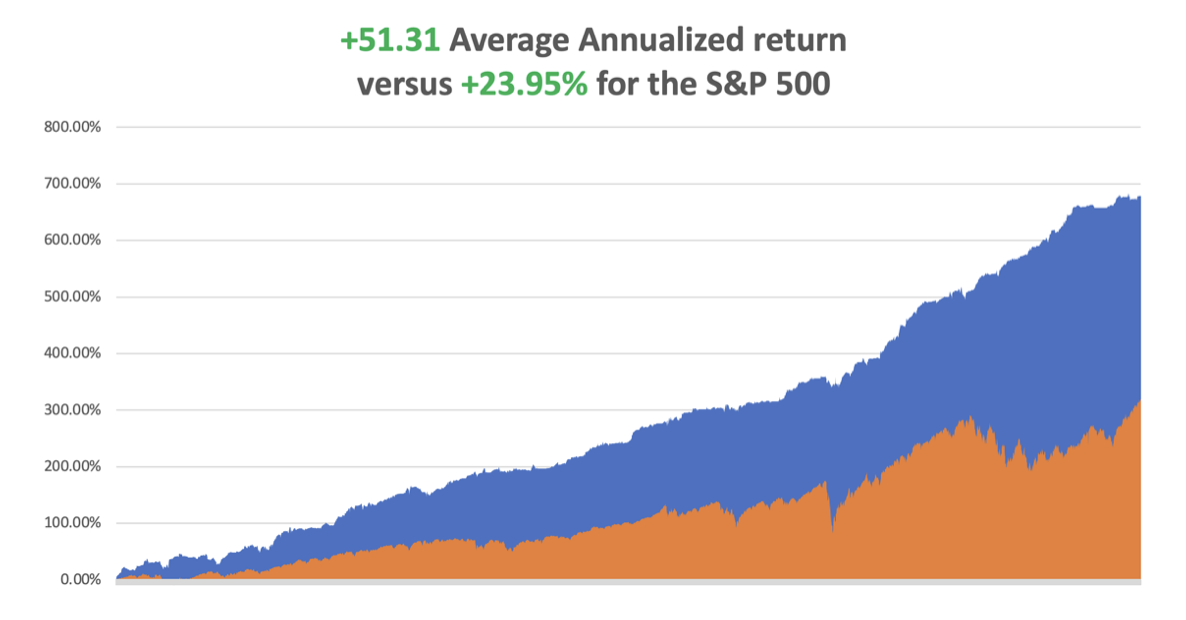

In February we closed up +7.42%. So far in March, we are up +0.70%. My 2024 year-to-date performance is at +3.21%. The S&P 500 (SPY) is up +7.11% so far in 2024. My trailing one-year return reached +54.28% versus +40.94% for the S&P 500.

That brings my 16-year total return to +689.74%. My average annualized return has recovered to +52.05%.

Some 63 of my 70 trades last year were profitable in 2023. Some 11 of 15 trades have been profitable so far in 2024.

I used the ballistic move in (NVDA) to take profits in my double long there. I am maintaining longs in (AMZN) and Snowflake (SNOW). I am both long and short the bond market (TLT) and I am 60% in cash given the elevated level of the stock markets.

Nonfarm Payroll Report Rose 275,000 in February. The Headline Unemployment Rate rose to 3.9%, a two-year high. The report illustrates a labor market that is gradually downshifting, with more moderate job and pay gains that suggest the economy will keep expanding without much risk of a reacceleration in inflation. These are very Fed friendly numbers.

JOLTS Job Openings Report Rises by 140,000 to 8,890,000, less than expected. Leisure and hospitality led with 41,000 new jobs, construction added 28,000 and trade, transportation and utilities contributed 24,000. Growth was concentrated among larger companies, as establishments with fewer than 50 employees contributed just 13,000 to the total.

Rivian Shares Soar, on news it is halting plans to build a new $2.25 billion factory in Georgia, an abrupt reversal aimed at cutting costs while the company prepares to launch a cheaper electric vehicle. Shifting planned production of the forthcoming R2 model to an existing facility in Illinois will allow Rivian to begin deliveries in the first half of 2026, earlier than expected. Buy (RIVN) on dips.

New York Community Bancorp Bailed Out, with a cash infusion led by former Treasury secretary Steve Mnuchin. The shares soared from $2 to $3.41. That takes the heat off the sector….until the next one. The US is shrinking from 4236 banks to only six banks. Who says politics doesn’t pay?

Europe Moves Towards Interest Rate Cuts, igniting a global bond market rally. Staff projections now see economic growth of 0.6% in 2024, from a previous forecast of 0.8%. They presented a more positive picture of inflation, with the forecast for the year brought to an average 2.3% from 2.7%. Market bets increased on rate cuts taking place as early as June, with the euro trading 0.35% lower against the British pound following the news.

Beige Book Comes in Moderate, saying "labor market tightness eased further," in February but noted "difficulties persisted attracting workers for highly skilled positions." The Beige Book is a review of economic conditions across all 12 Fed districts. Fed Chair Jerome Powell told Congress on Wednesday that the U.S central bank expected "inflation to come down, the economy to keep growing," but shied away from committing to any timetable for interest rate cuts.

China Targets 5% Growth for 2024, but nobody buys it for a second. A covid hangover, residential real estate crisis triggering a financial crisis, and constant invasion threats over Taiwan, make this target a pipe dream. Avoid (FXI) and all Middle Kingdom plays.

Gold Hits New All-Time High, at $2,141 an ounce on expectations of imminent rate cuts by the Fed. Gold, often used as a safe store of value during times of political and financial uncertainty, has climbed over $300 dollars since the start of the Israel-Hamas war. Buy (GLD), (GOLD), and (NEM) on dips.

Dell (DELL) Becomes an AI Stock, sending the shares up 47% in a Day. That’s been changing over the past year, as Dell has been reporting strong orders of servers designed to power generative AI workloads—many of which use chips supplied by AI kingmaker Nvidia. The company’s fourth quarter results convinced any doubters. Can Apple (AAPL) do the same?

Tesla Plunges on Poor China Sales, down $14.50 on sales data dimmed the outlook for Tesla's global deliveries, at a time when the top EV maker is battling a decline in demand and is weighed down by a lack of entry-level vehicles and the age of its product line-up. Not the time to be in EVs or solar. Buy (TSLA) on bigger dip.

US National Debt is Rising by $1 Trillion Every 100 Days. A trillion here, a trillion there, sooner or later that adds up to a lot of money. Eventually, someone is going to have to do something about this. The US national debt stands at $34.5 trillion, or $104,545 per person.

The Uranium Shortage is Getting Extreme, with yellow cake up 112% in a year. Owners of left-for-dead uranium mines are restarting operations to capitalize on rising demand for the nuclear fuel. Most of those American mines were idled in the aftermath of Fukushima when uranium prices crashed and countries like Germany and Japan initiated plans to phase out nuclear reactors. Now, with governments turning to nuclear power to meet emissions targets and top uranium producers struggling to satisfy demand, prices of the silvery-white metal are surging. Buy (Cameco (CCJ) on dips.

Japan’s Nikkei ($NIKK) Tops 40,000, a new 34-year high. The ultra-weak Japanese economy is giving the economy there a free lunch, but better hedge your currency exposure. Good thing I missed a dead market for 34 years.

NVIDIA Replaces Tesla as Top Traded Stock, with volumes migrating to the options market as well. Blockbuster profits are catnip for traders, while EV price wars aren’t. Tesla is down 52% from its all-time high two years ago and is one of the biggest percentage decliners in the Nasdaq 100 Index this year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 11 at 7:00 AM EST, the Consumer Inflation Expectations are announced.

On Tuesday, March 12 at 8:30 AM, Inflation Rate for February is released.

On Wednesday, March 13 at 2:00 PM, MBA Mortgage Applications are published

On Thursday, March 14 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index.

On Friday, March 15 at 2:30 PM, the University of Michigan Consumer Sentiment is published. At 2:00 PM the Baker Hughes Rig Count is printed.

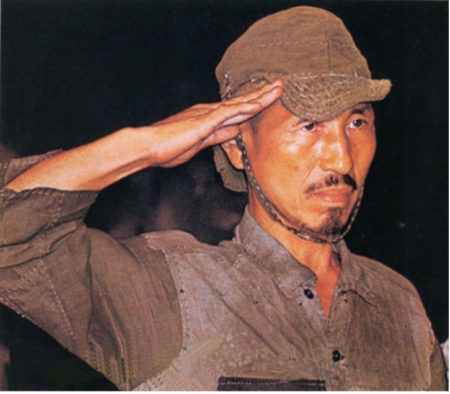

As for me, I have met many interesting people over a half-century of interviews, but it is tough to beat Corporal Hiroshi Onoda of the Japanese Army, the last man to surrender in WWII.

I had heard of Onoda while working as a foreign correspondent in Tokyo. So, I convinced my boss at The Economist magazine in London that it was time to do a special report on the Philippines and interview President Ferdinand Marcos. That accomplished, I headed for Lubang island where Onoda was said to be hiding, taking a launch from the main island of Luzon.

I hiked to the top of the island in the blazing heat, consuming two full army canteens of water (plastic bottles hadn’t been invented yet). No luck. But I had a strange feeling that someone was watching me.

When the Philippines fell in 1945, Onoda’s commanding officer ordered the remaining men to fight on to the last man. Four stayed behind, continuing a 30-year war.

As a massive American military presence and growing international trade raised Philippine standards of living, the locals eventually were able to buy their own guns and kill off Onoda’s companions one by one. By 1972 he was alone, but he kept fighting.

The Japanese government knew about Onoda from the 1950s onward and made every effort to bring him back. They hired search crews, tracking dogs, and even helicopters with loudspeakers, but to no avail. Frustrated, they left a one-year supply of the main Tokyo newspaper and a stockpile of food and returned to Japan. This continued for 20 years.

Onoda read the papers with great interest, believing some parts but distrusting others. His worldview became increasingly bizarre. He learned of the enormous exports of Japanese automobiles to the US, so he concluded that while still at war, the two countries were conducting trade.

But when he came to the classified ads, he found the salaries wildly out of touch with reality. Lowly secretaries were earning an incredible 50,000 yen a year, while a salesman could earn an obscene 200,000 yen.

Before the war, there was one Japanese yen to the US dollar. In the hyperinflation that followed the yen fell to 800, and then only recovered to 360. Onoda took this as proof that all the newspapers were faked by the clueless Americans who had no idea of true Japanese salary levels.

So he kept fighting. By 1974 he had killed 17 Philippino civilians.

After I left Lubang island, a Japanese hippy named Norio Suzuki with long hair, beads, and sandals followed me, also looking for Onoda. Onoda tracked him as he had me but was so shocked by his appearance that he decided not to kill him. The hippy spent two days with Onoda explaining the modern world.

Then Suzuki finally asked the obvious question: what would it take to get Onoda to surrender? Onoda said it was very simple, a direct order from his commanding officer. Suzuki made a beeline straight for the Japanese embassy in Manila and the wheels started turning.

A nationwide search was conducted to find Onoda’s last commanding officer and a doddering 80-year-old was turned up working in an obscure bookstore. Then the government custom-tailored a prewar Imperial Japanese Army uniform and flew him down to the Philippines.

The man gave the order and Onoda handed over his samurai sword and rifle, or at least what was left of it. Rats had eaten most of the wooden parts. You can watch the surrender ceremony by clicking here on YouTube.

When Onoda returned to Japan, he was a sensation. He displayed prewar mannerisms and values like filial piety and emperor worship that had been long forgotten. Emperor Hirohito was still alive.

When I finally interviewed him, Onoda was sympathetic. I had by then been trained in Bushido at karate school and displayed the appropriate level of humility, deference, mannerisms, and reference.

I asked why he didn’t shoot me. He said that after fighting for 30 years he only had a few shells left and wanted to save them for someone more important.

Onoda didn’t last long in the modern Japan, as he could no longer tolerate modern materialism and cold winters. He moved to Brazil to start a school to teach prewar values and survival skills where the weather was similar to that of the Philippines. Onoda died in 2014 at the age of 91. A diet of coconuts and rats had extended his life beyond that of most individuals.

Onoda wasn’t actually the last Japanese to surrender in WWII. I discovered an entire Japanese division in 1975 that had retreated from China into Laos and just blended in with the population. They were prized for their education and hard work and married well.

During the 1990’s a Japanese was discovered in Siberia. He was released locally at the end of the war, got a job, married a Russian woman, and forgot how to speak Japanese. But Onoda was the last to stop fighting.

The Onoda story reminds me of the fact that journalists learn very early in their careers. You can provide all the facts in the world to some people. But if they conflict with their own deeply held beliefs, they won’t buy them for a second.

Hiro Onoda Surrenders

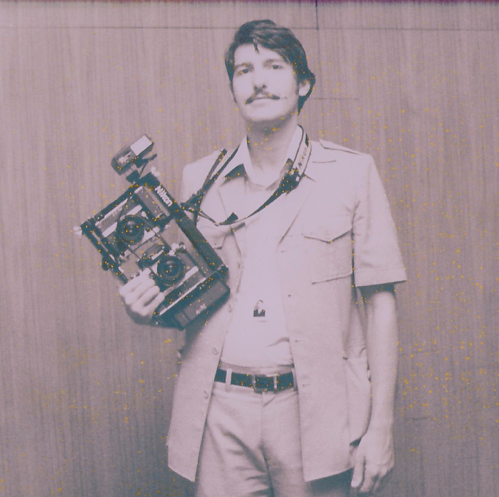

Budding Journalist John Thomas

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-11 09:02:232024-03-11 12:13:02The Market Outlook for the Week Ahead, or Higher Highs

Below please find subscribers’ Q&A for the March 6 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: With your projections of the Dow going to $240,000 in 10 years, would it be wise to invest in the Dow?

A: The Dow is just an indicator that everybody understands and is familiar with what the media uses. What I tell people to do is if you are not an aggressive person, put half your money in the S&P 500 (SPX), which is getting most of the gains, and half in the technology (QQQ), which is getting all of the gains. If you're an aggressive person, say in your twenties, thirties, or forties, then you put all of your money in the Invesco QQQ NASDAQ Trust (QQQ) because you'll live long enough to survive the inevitable downturns.

Q: What should we do now with Palo Alto Networks (PANW)?

A: Keep it. It’s a fantastic long-term company. This is a rare opportunity to get in on the long side, as this is a company that I think could double over the next 3 to 5 years. Hacking is never going out of style and now they have AI. The selloff was caused by a major platform upgrade which may cause profits to dip for a quarter. That’s now in the price.

Q: With the successful launch of Bitcoin, should we allocate 5% or 10% of our portfolio to Bitcoin?

A: Only if you can handle a 90% decline at any time without warning because that's exactly what it did in 2021. Calling it a store of value is a fantasy. You also still have big theft issues with Bitcoin. You don't have theft issues if you have all your money at Morgan Stanley, Goldman Sachs, Merrill Lynch, and so on, so there is a security issue (with Bitcoin). The only way to bypass the security issues is to have a hot wallet, and the only way to have a hot wallet is to be a computer programmer yourself or have a degree in computer science—so it's not for most people. If you can navigate all of that, then maybe; but again, nobody knows when the next 90% decline is going to come. By the way, if I can find stocks with Mad Hedge Fund Trader that go up faster than Bitcoin, I'd much rather own the stocks, because at least I know what they make.

Q: Is Snowflake (SNOW) a buy here at $155?

A: Absolutely. Another great cybersecurity database company. But if we drop to $155, we're going to stop out of the front month call spread and try to buy it back lower down.

Q: Do you think it's wise to sell the semiconductor stocks now and buy them back lower down, and pay the taxes?

A: Probably not. They are really the most volatile sector in the market. If you sell now, it's unlikely you'll be able to pick up the next bottom and get back in, and you have to pay the taxes. So it's probably better just to keep a core long-term position in the semis, especially Nvidia (NVDA); and if it drops 200 points, just buy more. That's what I'm doing. I'm keeping all of my Nvidia LEAPS. All my call spreads and short put positions are about to expire at max profit, and I even have a little bit of stock that I'm keeping. So I think Nvidia goes to $1,000 at one point and now, the forecast of $1,400 is out there. So as Nvidia goes, so goes the entire rest of the semiconductor industry.

Q: You're only 30% invested. Are you looking for a pullback, or are you just waiting for new opportunities to appear?

A: Yes and Yes. I'm waiting for a fantastic company to come up with conservative guidance, which these days means an immediate 20 to 25% sell-off. That is your entry point for these good companies. That's how we got into Palo Alto Networks (PANW), and that's how we got into Snowflake (SNOW). In an extremely overbought market, those are your only opportunities until the market generally sells off or until the domestic plays finally start to take off, and we got the first hints of that last week.

Q: What is your view on junior gold mining stocks?

A: They are a buy here, absolutely, but you get enough volatility in the majors that you don't need to bother with the minors—that's always been my view. Because minors go out of business, they close mines, they don't find gold. A lot of minors have stocks go up on the possibility of gold being found, whereas the majors like Barrick Gold (GOLD) and Newmont Mining (NEM) actually have the gold, and it's just an industrial process of mining it. You know the minors, the juniors, are extremely speculative and high-risk, and that's why most of them are listed in Canada. They can't get a US listing. So that's enough of a tell for me to stay away.

Q: I just realized I have the wrong expiration date on my Amazon (AMZN) spread. Should I exit immediately?

A: What I would do is exit what you have and then wait for another down day on Amazon, and then put it back on. That's the way to deal with that one. The answer to all mistakes is to exit immediately. That's an automatic rule at Morgan Stanley; if you don't do that, you get fired. Or come up with a new set of logic as to why you own this position, which has been done by more than a few traders, I imagine.

Q: Would you be willing to be a Boeing 737 Max passenger right now or ever?

A: Yes! If you don't fly Boeings (BA), your life is suddenly very narrow and limited because you’re stuck on the ground. Boeing is the biggest-selling airplane in the world, and most fleets are made of Boeings. However, I'm a pilot, so if anything goes wrong I can run up front and take control, or at least tell the pilot what to do. I also have 25 parachute jumps, if they're handing those out in first class. So remember, every airplane without engines is a glider and I can land a glider anywhere. The company has major problems to sort out until it becomes a “BUY”.

Q: I cannot get into the (TLT) trade to save my life. Is the (TLT) April $89-$92 vertical bull call debit spread pushing the risk limits?

A: Yes. I would walk away from the trade and wait for a better entry point rather than chase.The whole fixed-income space has flipped from the bid side to the offered side, meaning we've gone from net sellers to net buyers. All asset classes have done that; you're seeing that in gold, silver, and even uranium. All the REITs are having a fantastic week. All interest rate plays are now being bid, and it's hard to buy stuff when things are being bid.

Q: What's it like being 6’4” and living in Japan?

A: Well, I did knock myself out a couple of times, banging myself on the door. You get used to bowing a lot, but bowing is a part of the culture in Japan. If you're watching the new Hulu miniseries, Shogun, you would know that. Once I was working for Sony and I was late for work, so I was running up the stairs, and they had a steel lintel to their door, and I just ran bang into that and knocked myself out. The Sony people thought, “Oh my gosh, we just killed a foreigner!” So yes, it was hard. The only clothes I could buy in Japan for ten years were belts and ties. I had to fly to Hong Kong and had everything else custom-made in those days.

Q: What's your opinion of Masters of the Air?

A: I absolutely love it. It's heartbreaking to watch. I knew a lot of guys who were there, and I was one of the last people trained on how to fly a Boeing B-17 Flying Fortress. Anybody who watched Masters of the Air with me gets to watch it with someone who is one of the last living people who rated on a B-17 as a pilot.

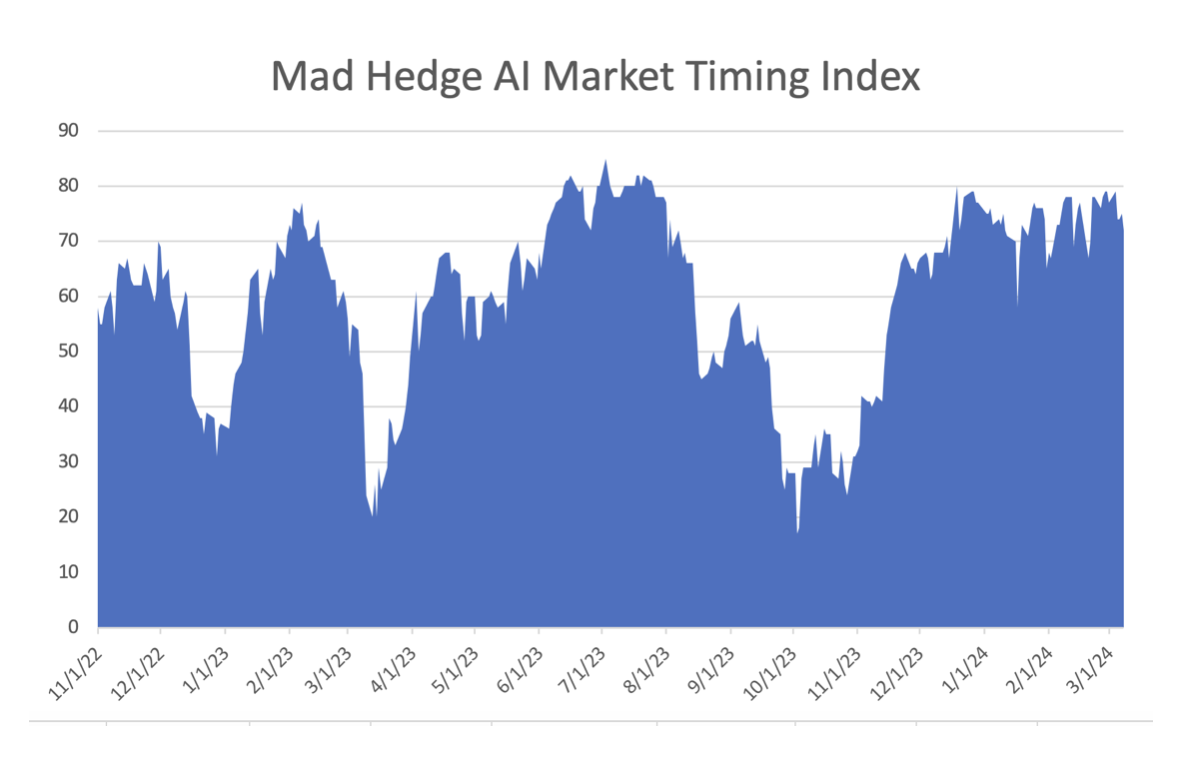

Q: Are we in a liquidity bubble right now?

A: Yes, we are, and boy, I love every minute of it. But we're not in the year 2000 in a liquidity bubble, we're in 1995 just getting started. And the profits from AI are just getting started which is what's creating this endless liquidity that people are seeing now.

Q: What should I buy the dip in Tesla (TSLA)?

A: There's no downside target for Tesla right now. We just have to wait for the meltdown in demand to finish, and who knows where that is. But with BYD entering the market, Tesla is definitely going to get more competition in emerging markets—that's where BYD is selling the cars now. I also understand they're selling them in Australia.

Q: How much longer can tech stocks keep rising?

A: 5 to 10 more years, but we are way overdue for some kind of pullback.

Q: What are your thoughts on Apple's (APPL) weakness?

A: Apple has become that great backward-looking company. It could drop to $160 or even $140, then we’ll be taking a serious look at some call spreads and LEAPS. You just wait. In four months when they announce their next batch of new products suddenly, they’ll become an AI company and recover the $200 level in no time.

Q: Should I dive into Coinbase (COIN)?

A: Absolutely not on pain of death! It's made its move. You're better off buying Nvidia (NVDA) at that kind of inclination because at least you know what they make.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

How high are we talking? How about a Dow Average of 240,000 by 2035, up another 515% from here? That is a 40-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion or more in corporate stock buybacks for the past decade.

I’m not talking pie-in-the-sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th-century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000, the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my dad’s generation that meant loading your portfolio with US Steel (X), IBM (IBM), and General Motors (GM).

For my generation, that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on NVIDIA (NVDA), Netflix (NFLX), Amazon (AMZN), Meta (META), and Alphabet (GOOGL). Oh, and they like Bitcoin too (BITO).

That’s why the Magnificent Seven account for all of the past year’s monster gains.

There is another gale force tailwind pushing stocks up. The enormous profits created by artificial intelligence are essentially replacing the Federal Reserve as an unlimited source of liquidity. If you missed the quantitative easing and the free money of the 2010s, you get another pass at the brass ring. But you have heard me talk about this before so I won’t bore you.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 240,000, we need to squeeze in a recession. Bear markets in stocks historically precede recessions by an average of seven months. But for the time being, it looks like smooth sailing.

When I get a better read on precise dates and market levels, you’ll be the first to know.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/03/john-thomas-snow.jpg285259april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-06 09:02:172024-03-06 10:09:22Why the Dow is Going to 240,000

People will be sitting around campfires trading stories about last week’s NVIDIA move for decades.

Analysts have been struggling to outdo each other in describing their earnings report that came out on Thursday. Here’s my favorite: The gain in the company’s market capitalization on that day, at $278 billion the largest in history, exceeded its TOTAL market capitalization at the pandemic bottom.

And here I deserve some bragging rights. Mad Hedge followers went into last week’s melt-up, UP TO THEIR EYEBALLS in (NVDA). They owned the stock, call options, and call spreads. The LEAPS alone delivered a 12X return, and some readers who customize their own strike prices (the $295-$300s) received a 50X return. It was almost everyone’s largest position.

It was easy for me to do the NVIDIA trade. When the company launched its first high-end graphics card in 1993, every computer geek out there flocked to them. I used to tear apart my company’s PCs, throw out the graphics cards they came with, and install NVIDIA cards. The performance improvement was remarkable, especially for advanced mathematical calculations.

The company is blessed. It went public at $12 a share just before the Dotcom Bust and the IPO window closed for years. Adjusted for 12:1 splits over the years and that drops the original IPO price to $1. A dollar invested in 1999 would be worth $750 at last week’s high. NVIDIA’s CEO, Jensen Huang, is now one of the richest men in the world solely through the ownership of his NVIDIA shares.

God Bless America!

Also last week, my inbox was jammed with inquiries on what company will become the next NVIDIA. And here is the bad news. There aren’t any 750:1 returns anywhere on the horizon. There are not even any 175:1 opportunities that we earned from Tesla (TSLA) over the years either where we also had heavy exposure.

And the reason is very simple. You are not going to get the entry points today with the Dow Average at 39,000 that you got in 2009 when it was at only 6,000, or when it was at a mere 600 when I joined Morgan Stanley in 1982. The last decent entry point for (NVDA) was the $100 pandemic low in April 2020.

Want to own the next (NVDA)? Try buying (NVDA), where an analyst raised his target to $1,420, up 80% from the Friday close. It’s just a matter of time before its market cap jumps from $2 trillion to $3 trillion, making it the largest company in the world. That’s what an airtight monopoly in the world’s most valuable product gets you.

Technology earnings are now exploding at such a rapid pace that it is time to consider the unthinkable: What if stocks don’t need interest rate cuts for the bull market to continue? After all, the companies seem to be doing just fine without any such assistance.

Why try to fix what isn’t broken?

In fact, these large cash flow companies would take a hit on their income statements as they are already net creditors to the financial system. Apple (AAPL) alone would lose $8 billion in annual income if interest rates went back to zero.

While that may be true for the Magnificent Seven or the AI Five, it is not true for the Unimagnificent 493. They actually need cheaper money for their stock prices to get going or even just to survive. That is especially true for all the falling interest rate plays, like bonds, utilities, real estate, precious metals, energy, and foreign currencies.

And don’t even talk to me about small caps, which depend on low interest rates for the breath of life.

It says a lot that Warren Buffet believes there is nothing left to buy in his annual letter to shareholders, an early Mad Hedge subscriber. His spectacular annual compounded returns of 19.8% a year, more than double that of the S&P 500 (SPY), are now a thing of the past.

The few targets left out there are few and far between and heavily picked over. (BRK/B) has also lost the advice of its principal mentor, Charlie Munger at the ripe old age of 99. Last year Berkshire acquired Dairy Queen and Berkshire Energy. But at $905 billion in assets under management, those will hardly move the needle. The 93-year-old Buffet has outperformed the S&P 500 by 141:1 since 1964.

Who says age is an impediment?

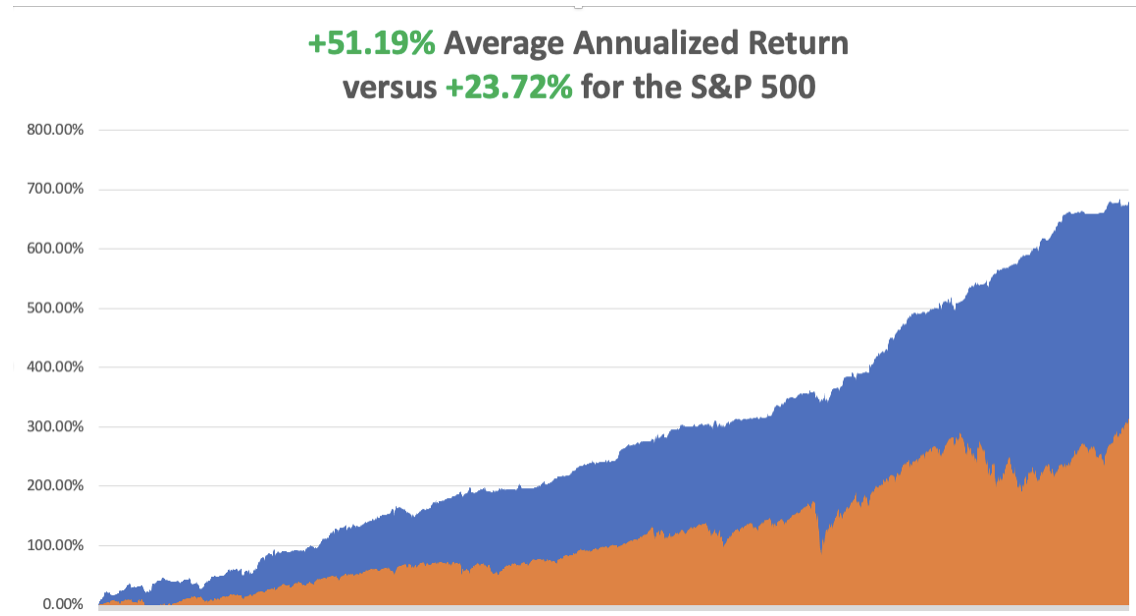

So far in February, we are up +5.92%. My 2024 year-to-date performance is also at +1.64%.The S&P 500 (SPY) is up +6.50%so far in 2024. My trailing one-year return reached +57.73% versus +38.67%for the S&P 500.

That brings my 15-year total return to +678.27%. My average annualized return has recovered to +51.19%,another new high.

Some 63 of my 70 trades last year were profitable in 2023.

I used the ballistic move-in (NVDA) to take profits in my double long there. I am maintaining a single long (AMZN) and am 90% in cash given the elevated level of the markets.

NVIDIA Announces Blowout Earnings, with AI reaching the “tipping point” according to the CEO Jensen Huang. Revenues came in at a spectacular $22.1 billion versus an expected $20.6 billion off the backing of exploding data center demand, up 33%. Earnings were up 22% QOQ and 225% YOY. The shares exploded $100 in the aftermarket at one point, up 15.6%. Forward guidance was ramped up too. Buy NVDA on dips. At a PE multiple of 18X, it is the cheapest AI stock out there.

Mad Hedge Clocks Biggest One Day Gain in 16 Years, with a double weighting in NVIDIA (NVDA), up +6.072%. If you like that the Mad Hedge Technology Letter is doing even better, up +13% YTD. And we are still early days into the tech melt-up, which could go on for another decade. Our YOY gain is up +59.62%. The harder I work, the luckier I get.

Existing Home Sales Jumped 3% YOY, boosted by lower mortgage interest rates in November and December. Inventories of homes for sale in January increased to 1.01 million units, up 3.1% from January 2023, but still at a low 3-month supply. The median existing home price for all housing types in January was $379,100, up 5.1% from a year earlier and an all-time high for the month of January.

Weekly Jobless Claims Dropped to a one-month low, down 12,000 to 201,000. No recession here. California and Kentucky saw the largest declines.

China Bans Stock Selling, by institutional investors at market openings and closes when liquidity is the greatest. It’s part of the government’s most forceful attempt yet to prop up the nation’s $8.6 trillion stock market. It’s another sign of a weakening China. When restrictions are placed on markets, capital flees. Whoever thought of this one must have a hole in their head. Avoid (FXI).

California demolishes Solar Providers, cutting the price the utility PG&E has to pay for home power providers by 75%. Solar companies like SunPower (SPWR), are down 89% since last year. Avoid solar providers for now, which was always a low value-added business.

Amazon (AMZN) is getting added to the Dow Average, opening it up to massive index buying. Retailer Walgreens Boots Alliance (WBA) is getting bumped. Since 1896, the blue-chip index has made few changes to its 30-stock lineup, having altered its constituents about 60 times in its 128-year history. Buy (AMZN) on dips.

US Stocks now account for 70% of Global Stock Market Capitalization, thanks to the ballistic moves in big tech. This level represents the largest country weighting since I helped create this index way back in 1986. It also now has the lowest exposure to non-US stocks. Money is pouring into the US from all corners of the world, the planet's most successful economy.

Natural Gas Hits (UNG) Three Year Low, at $1.63MM BTU, and down an eye-popping 50% in a month. Warm weather, high inventories, and overproduction due to cheap capital are the price killers. An LNG train broke down, cutting export demand. If you didn’t get out on the double in December you’re toast. Avoid (UNG).

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, February 26, the New Home Sales are announced.

On Tuesday, February 27 at 8:30 AM EST,the Durable Goods are released. The S&P Case Shiller for December is announced.

On Wednesday, February 28 at 2:00 PM, the Q2 GDP second readis published.

On Thursday, February 29 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Core Consumer Price Expectations.

On Friday, March 1 at 2:30 PM, the December ISM Manufacturing PMI is published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, the telephone call went out amongst the family with lightning speed, and this was back in 1962 when long-distance cost a fortune. President Dwight D. Eisenhower was going to visit my grandfather’s cactus garden in Indio the next day, said to be the largest in the country, and family members were invited.

I spent much of my childhood in the 1950s and 1960s helping grandpa look for rare cactus in California’s lower Colorado Desert, where General Patton trained before invading Africa. That involved a lot of digging out a GM pickup truck from deep sand in the remorseless heat. SUVs hadn’t been invented yet, and a Willys Jeep (click here) was the only four-wheel drive then available in the US.

I have met nine of the last 13 presidents, but Eisenhower was my favorite. He certainly made an impression on me as a ten-year-old boy, who I remember as a kindly old man.

I walked with Eisenhower and my grandfather plant by plant, me giving him the Latin name for its genus and species and citing unique characteristics and uses by the Indians. The former president showed great interest and in two hours we covered the entire garden. I still make my kids learn the Latin names of plants.

Eisenhower lived on a remote farm at the famous Gettysburg, PA battlefield given to him by a grateful nation. But the winters there were harsh, so he often visited the Palm Springs mansion of TV Guide publisher Walter Annenberg, a major campaign donor.

Eisenhower was a one-of-a-kind brilliant man that America always came up with when it needed them the most. He learned the ropes serving as Douglas MacArthur’s Chief of Staff during the 1930’s. Franklin Roosevelt picked him out of 100 possible generals to head the Allied invasion of Europe, even though he had no combat experience.

After the war, both the Democratic and Republican parties recruited him as a candidate for the 1952 election. The latter prevailed, and “Ike” served two terms, defeating the governor of Illinois Adlai Stevenson twice. During his time, he ended the Korean War, started the battle over civil rights at Little Rock, began the Interstate Highway System, and admitted Hawaii as the 50th state.

As my dad was very senior in the Republican Party in Southern California during the 1950s, I got to meet many of the bigwigs of the day. New York prosecutor Thomas Dewy ran for president twice, against Roosevelt and Truman, and was a cold fish and aloof. Barry Goldwater was friends with everyone and a decorated bomber pilot during the war.

Richard Nixon would do anything to get ahead, and it was said that even his friends despised him. He let the Vietnam War drag out five years too long when it was clear we were leaving. Some 21 guys I went to high school with died in Vietnam during this time. I missed Kennedy and Johnson. Wrong party and they died too soon. Ford was a decent man and I even went to church with him once, but the Nixon pardon ended his political future.

Peanut farmer Carter was characterized as an idealistic wimp. But the last time I checked, the Navy didn’t hire wimps as nuclear submarine commanders. He did offer to appoint me Deputy Assistant Secretary of the Treasury for International Affairs, but I turned him down because I thought the $15,000 salary was too low. There were not a lot of Japanese-speaking experts on the Japanese steel industry around in those days. Biggest mistake I ever made.

Ronald Reagan’s economic policies drove me nuts and led to today’s giant deficits, which was a big deal if you worked for The Economist. But he always had a clever dirty joke at hand which he delivered to great effect….always off camera. The tough guy Reagan you saw on TV was all acting. His big accomplishment was not to drop the ball when it was handed to him to end the Cold War.

I saw quite a lot of George Bush, Sr. whom I met with my Medal of Honor Uncle Mitch Paige at WWII anniversaries, who was a gentleman and fellow pilot. Clinton was definitely a “good old boy” from Arkansas, a glad-hander, and an incredible campaigner, but he was also a Rhodes Scholar. His networking skills were incredible. George Bush, Jr. I missed as he never came to California. And 22 years later we are still fighting in the Middle East.

Obama was a very smart man and his wife Michelle even smarter. Stocks went up 400% on his watch and Mad Hedge Fund Trader prospered mightily. But I thought a black president of the United States was 50 years early. How wrong was I. Trump I already knew too much about from when I was a New York banker.

As for Biden, I have no opinion. I never met the man. He lives on the other side of the country. When I covered the Senate for The Economist, he was a junior member.

Still, it’s pretty amazing that I met 10 out of the last 14 presidents. That’s 20% of all the presidents since George Washington. I bet only a handful of people have done that, and the rest all live in Washington DC. And I’m a nobody, just an ordinary guy.

It just makes you think about the possibilities.

Really.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It’s Been a Long Road

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/john-thomas-white-house.jpg500665april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-26 09:02:552024-02-26 10:54:29The Market Outlook for the Week Ahead, or Who Needs Rate Cuts?

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HOW THE CPI LIED),

(NVDA), (MSFT), (AMZN), (V), (PANW), (CCJ) (AAPL), (TSLA), (GOOGL), (MSFT), (AMZN), (META), (UBER), (UUP)

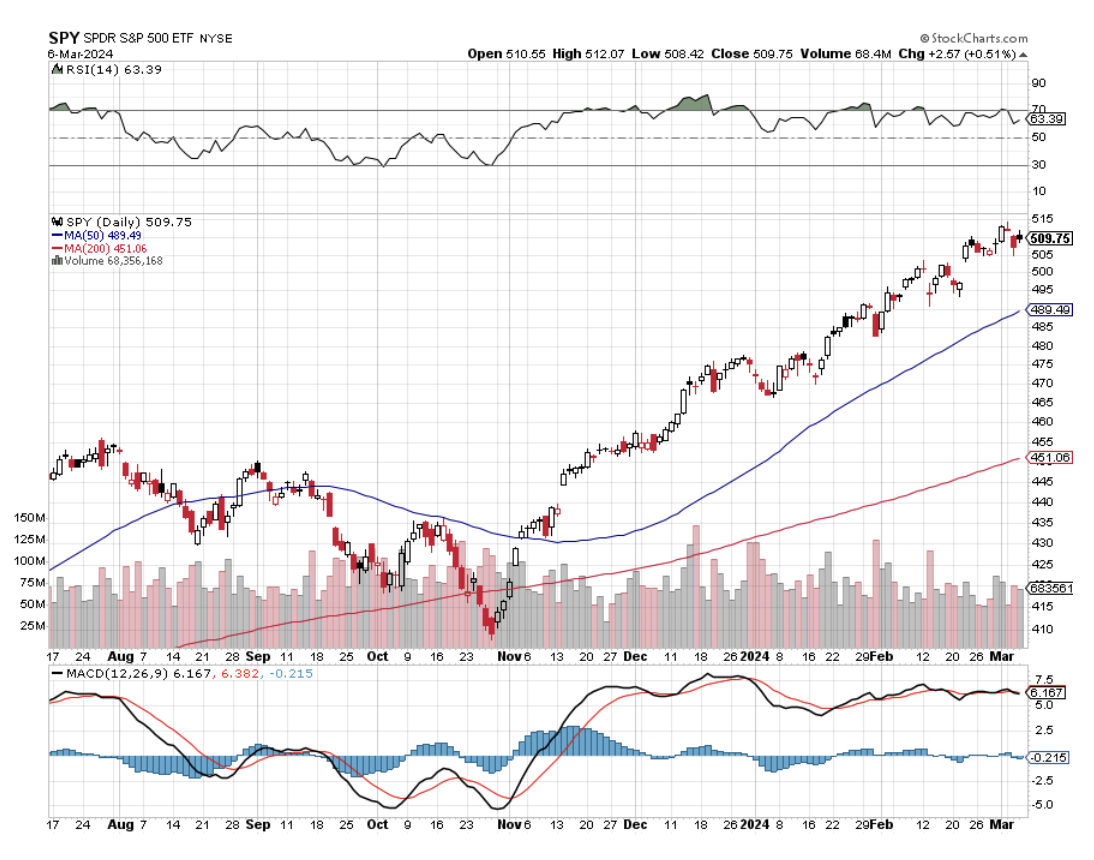

It’s pretty obvious that when the Consumer Price Index was released last Tuesday, the data point was lying through its teeth. The 0.4% increase in the Core CPI brought the YOY gain to a heart-palpitating 3.9%, much higher than expected. The stock market thought it was telling God’s home truth by plunging 740 points at its low.

Interest rate sensitives, like bonds, utilities, real estate, precious metals, energy, and foreign currencies were particularly hard hit.

I have been in the financial markets quite a long time now and as a result, am pretty used to being told porky pies (lies in London’s East End). Take the CPI for example. The reported number came in at a sizzling 3.3% for January. That is enough to kill off any hopes of a Fed interest rate cut in 2024, thus the ensuing wreckage in the market.

However, back out a single number, the 6.0% rise in housing rental costs, and the inflation rate drops all the way to 2.0%, bang on the Fed’s long-term inflation target. In other words, interest rates should be cut RIGHT NOW!

That is clearly the view that the markets came around to on Wednesday, which saw the Dow Average recover 151 points.

Unfortunately, lying is a fact of life in the stock market at every conceivable level. But learn to tolerate it and you can make millions of dollars. That works for me. Like my old college statistics professor used to tell me: “Statistics are like a bikini bathing suit; what they reveal is fascinating, but what they conceal is essential.”

In fact, we may see the stock market bouncing back and forth like a ping pong ball between big technology and the interest rate sectors, depending on what the bond market is doing that day driving traders nuts. After all, it was YOU who wanted to be in show business!

In the meantime, complacency rules all. Cash flows into stocks are near all-time highs. Market strategists have been ratcheting up their yearend targets on a daily basis, even me (I’m now at SPX 6,000). The option put/call ratio is about as low as it gets, meaning there is a universal belief that stocks will continue to appreciate. That’s with the S&P 500 earnings multiple trading at a rich 20.5.

I would be remiss in my duties as a financial advisor if I did not also warn you that these are all market-topping signals, at least for the short term.

Double Yikes, and Heavens to Betsy!

Of course, all eyes will be on the Q4 NVIDIA earnings this week, out after the close on Wednesday and probably the most important data release of the year. Everything else this week is essentially meaningless.

If earnings come in anything less than perfect, up 100% YOY, it could trigger a long overdue correction in the stock market in general and (NVDA) in particular. On the other hand, earnings just might come in more than perfect.

I have been covering (NVDA) for more than a decade back when it was just a video game play and I describe it today as a monopoly on the world’s most valuable product. Their top-end H100 graphics cards are now selling for a breathtaking $30,000 each and Meta (META) just ordered 450,000 of these babies, partly so their competitors can’t get their hands on them. For those who don’t have a calculator that is a single order worth a mind-blowing $13.5 billion.

That is why the stock is up 224% in a year and 50X since the first Mad Hedge trade alert on the company went out at a split-adjusted $2.00. Those who think they can clone (NVDA) and their products overnight can dream on. Most employees have golden handcuffs in the form of vested options at the same $2.00 strike price or lower.

The Magnificent Seven are still cheap relative to the rest of the market. Their price-to-growth ratio (PEG Ratio) is still only half the rest of the market. The Mag Seven will see earnings grow 20% this year with a price-earnings multiple of 30X giving you a PEG of 1.5X. The Unmagnificent 493 are selling at a PEG ratio of 3.0X, meaning they are twice as expensive.

Just thought you’d like to know.

So far in February, we are up +3.42%. My 2024 year-to-date performance is also at -0.86%.The S&P 500 (SPY) is up +4.72%so far in 2024. My trailing one-year return reached +59.62% versus +24.57%for the S&P 500.

That brings my 15-year total return to +675.77%. My average annualized return has retreated to +51.32%.

Some 63 of my 70 trades last year were profitable in 2023.

I am maintaining a double long in, you guessed it, (NVDA). My longs in (MSFT), (AMZN), (V), (PANW), and (CCJ) all expired at their maximum potential profits with the February option expiration.

CPI Smacks Market, coming in at 0.3% in January instead of the expected 0.2%. The highflyers took the biggest hit. Bonds were destroyed, taking ten-year US Treasury yields up to 4.30%. Is the falling interest rate story dead, or just resting? Rising rents were the big villain here.

US Retail Sales Dive 0.8% in January, a shocking decline from the blowout in December. Consumers didn’t bite on those New Year Sales because they actually started in November. Winter storms as well as technical factors had distorted the data.

Weekly Jobless Claims Dropped to 212,000, an improvement of 8,000 from the previous week. Continuing claims rose to 1,895,000. https://www.dol.gov/ui/data.pdf

Here are Dan Niles’ Tech Shorts, Apple (AAPL), (TSLA), and Alphabet (GOOGL). He is long Microsoft (MSFT), (AMZN), (META), and of course NVIDIA (NVDA). Sounds like a good call to me. Dan knows what he is doing.

Uber Announces First Ever Share Buy Back, some $7 billion. In the meantime, they have to cope with a driver strike. Buy (UBER) on dips.

$929 Billion in US Commercial Real Estate Loans are Due this Year or 20% of the total. Will there be widespread defaults or will borrowers get rescued by falling interest rates in the second half? Will they extend and pretend? Avoid regional banks like the plague, which lack the capital to cope with this.

US Dollar (UUP) Hits Three Month High, on the hot CPI. You need a falling CPI to get a weak buck. The Euro plunged to $1.07, the British pound to $1.25, the Australian dollar to 65 cents, and the Japanese yen to ¥151.

NVIDIA Now Tops Amazon in Market Value, at $1.2 trillion now the fourth most valuable company in the US. It could eventually top Microsoft’s (MSFT) market cap as it is growing much faster. Those (NVDA) LEAPS are looking pretty good. The shares are up 50% so far in 2024. Buy (NVDA) on dips.

Biden to Ban Chinese EV Car Imports.The measures would apply to electric vehicles and parts originating from China, no matter where they are assembled, in a bid to prevent Chinese makers from moving cars and components into the United States through third countries such as Mexico. Chinese cars will never meet US safety standards. Try driving in China.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, February 19, the markets are closed for Presidents Day.

On Tuesday, February 20 no data of importanceis released.

On Wednesday, February 21 at 2:00 PM EST, the Minutes from the previous Federal Open Market Committee meetingare published. NVIDIA earnings are released after the market closes.

On Thursday, February 22 at 8:30 AM EST, the Weekly Jobless Claims are announced. Existing Home Sales are Released.

On Friday, February 23 at 2:30 PM the Baker Hughes Rig Count is printed.

As for me,the first thing I did when I received a big performance bonus from Morgan Stanley in London in 1988 was to run out and buy my own airplane.

By the early 1980s, I’d been flying for over a decade. But it was always in someone else’s plane: a friend’s, the government’s, a rental. And Heaven help you if you broke it!

I researched the market endlessly, as I do with everything, and concluded that what I really needed was a six-passenger Cessna 340 pressurized twin turbo parked in Santa Barbara, CA. After all, the British pound had just enjoyed a surge against the US dollar so American planes were suddenly a bargain. It had a maximum range of 1,448 miles and therefore was perfectfor flying around Europe.

The sensible thing to do would have been to hire a professional ferry company to fly it across the pond.But what’s the fun in that? So, I decided to do it myself with a copilot I knew to keep me company. Even more challenging was that I only had three days to make the trip, as I had to be at my trading desk at Morgan Stanley on Monday morning.

The trip proved eventful from the first night. I was asleep in the back seat over Grand Junction, Colorado, when I was suddenly awoken by the plane veering sharply left. My co-pilot had fallen asleep, running the port wing tanks dry and shutting down the engine. He used the emergency boost pump to get it restarted. I spent the rest of the night in the co-pilot’s seat trading airplane stories.

The stops at Kansas City, MO, Koshokton, OH, and Bangor, ME proved uneventful. Then we refueled at Goose Bay, Labrador in Canada, held our breath, and took off for our first Atlantic leg.

Flying the Atlantic in 1988 is not the same as it is today. There were no navigational aids and GPS was still top secret. There were only a handful of landing strips left over from the WWII summer ferry route, and Greenland was still littered with Mustangs, B-17s, B24s, and DC-3s. Many of these planes were later salvaged when they became immensely valuable. The weather was notoriously bad. And a compass was useless, as we flew so close to the magnetic North Pole the needle would spin in circles.

But we did have NORAD, or America’s early warning system against a Russian missile attack.

The practice back then was to call a secret base somewhere in Northern Greenland called “Sob Story.” Why itwas called that I can only guess, but I think it has something to do with a shortage of women. An Air Force technician would mark your position on the radar. Then you called him again two hours later and he gave you the heading you needed to get to Iceland. At no time did he tell you where HE was.

It was a pretty sketchy system, but it usually worked.

To keep from falling asleep the solo pilots ferrying aircraft all chatted on a frequency of 123.45 MHz. Suddenly, we heard a mayday call. A female pilot had taken the backseat out of a Cessna 152 and put in a fuel bladder to make the transatlantic range. The problem was that the pump from the bladder to the main fuel tank didn’t work. With eight pilots chipping in ideas, she finally fixed it. But it was a hair-raising hour. There is no air-sea rescue in the Arctic Ocean.

I decided to play it safe and pick up extra fuel in Godthab, Greenland. Godthab has your worst nightmare of an approach, called a DME Arc. You fly a specific radial from the landing strip, keeping your distance constant. Then at an exact angle, you turn sharply right and begin a decent. If you go one degree further, you crash into a 5,000-foot cliff. Needless to say, this place is fogged 365 days a year.

I executed the arc perfectly, keeping a threatening mountain on my left while landing. The clouds mercifully parted at 1,000 feet and I landed. When I climbed out of the plane to clear Danish customs (yes, it’s theirs), I noticed a metallic scraping sound. The runway was covered with aircraft parts. I looked around and there were at least a dozen crashed airplanes along the runway. I realized then that the weather here was so dire that pilots would rather crash their planes than attempt a second go.

When I took off from Godthab, I was low enough to see the many things that Greenland is famous for polar bears, walruses, and natives paddling in deerskin kayaks. It was all fascinating.

I called into Sob Story a second time for my heading, did some rapid calculations, and thought “damn”. We didn’t have enough fuel to make Iceland. The wind had shifted from a 70 MPH tailwind to a 70 MPH headwind, not unusual in Greenland. I slowed down the plane and configured it for maximum range.

I put out my own mayday call saying we might have to ditch, and Reykjavik Control said they would send out an orange bedecked Westland Super Lynch rescue helicopter to follow me in. I spotted it 50 miles out. I completed a five-hour flight and had 15 minutes of fuel left, kissing the ground after landing.

I went over to Air Sea Rescue to thank them for a job well done and asked them what the survival rate for ditching in the North Atlantic was. They replied that even with a bright orange survival suit on, which I had, it was only about 50%.

Prestwick, Scotland was uneventful, just rain as usual. The hilarious thing about flying the full length of England was that when I reported my position, the accents changed every 20 miles. I put the plane down at my home base of Leavesden and parked the Cessna next to a Mustang owned by rock star Randy Newman.

I asked my ferry pilot if ferrying planes across the Atlantic was always so exciting. He dryly answered “Yes.” He told me in a normal year about 10% of the planes go missing.

I raced home, changed clothes, and strode into Morgan Stanley’s office in my pin-stripped suit right on time. I didn’t say a word about what I just accomplished.

The word slowly leaked out and at lunch, the team gathered around to congratulate me and listen to some war stories.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Flying the Atlantic in 1988

Looking for a Place to Land in Greenland

Landing on a Postage Stamp in Godthab Greenland

On the Ground in Greenland

No Such a Great Landing

Flying Low Across Greenland

Gassing Up in Iceland

Almost Home at Prestwick

Back to London in 1988

https://www.madhedgefundtrader.com/wp-content/uploads/2022/09/flying-1988-scaled.jpg15432560april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-20 09:02:342024-02-20 10:40:04The Market Outlook for the Week Ahead or How the CPI Lied

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.