Global Market Comments

February 28, 2020

Fiat Lux

Featured Trade:

(FEBRUARY 26 BIWEEKLY STRATEGY WEBINAR Q&A),

(VIX), (VXX), (SPY), (TLT), (UAL), (DIS), (AAPL), (AMZN), (USO), (XLE), (KOL), (NVDA), (MU), (AMD), (QQQ), (MSFT), (INDU)

Global Market Comments

February 28, 2020

Fiat Lux

Featured Trade:

(FEBRUARY 26 BIWEEKLY STRATEGY WEBINAR Q&A),

(VIX), (VXX), (SPY), (TLT), (UAL), (DIS), (AAPL), (AMZN), (USO), (XLE), (KOL), (NVDA), (MU), (AMD), (QQQ), (MSFT), (INDU)

Tech shares are hoping to stage a rebound after the coronavirus-fueled rout that saw the Nasdaq’s 2-day drop by 6.38%, which is its worst since June 2016.

Readers can now pencil in a fresh readjustment to growth expectations of zero to low single digits in tech shares for fiscal year of 2020.

That is why Thursday morning was greeted by another 3% drop at the open - proceed with caution to not get trapped in the proverbial dead cat bounce vortex in the short-term.

A major tech consolidation could take place because let’s get real, the unpredictability is having a major impact on technology companies and uncertainty is a substantial input in heightened risk.

What are the realistic scenarios that are still left on the table?

Firms trading on the Nasdaq will slash price targets and profit estimates that could uncoil another leg down in the Nasdaq index.

In fact, it has already happened as PayPal (PYPL), Microsoft (MSFT), and Apple (AAPL) issued revenue warnings saying they do not expect to meet their revenue goals because of the coronavirus.

On an operational level, softness is what I see when delving into the semantics of Amazon (AMZN) whose ranking algorithm demotes product sellers who go out of stock.

The coronavirus has crippled supply chains, and to avoid a lack of stock, sellers are raising prices to slow sales, while planning to move production to other countries.

This is on top of the backbreaking supply problems that companies face because of the ill-effects of the trade war.

If the Amazon algorithm punishes the seller, once stock is replenished, they must overspend on advertising to climb back to the top of product searches.

The surveys I have taken out with Amazon sellers in the last few days show a precarious situation where sellers are stretched to the limit relying on numerous uncertain variables that are completely out of their control,

Even if the local government allows Chinese factories to restart, it will be understaffed while workers from other provinces self-quarantine.

The third-party marketplace accounts for more than half of Amazon’s retail sales with a robust base of manufacturers and sellers in China.

Google (GOOGL) and Microsoft are accelerating efforts to shift hardware production to Southeast Asia amid the worsening coronavirus outbreak, opening factories in Vietnam and Thailand as well.

Google is set to begin production of the Pixel 4A smartphone and also plans to manufacture its next-generation flagship smartphone called the Pixel 5 in Vietnam.

Google is also on the verge of building factories in Thailand for "smart home" related products, including voice-activated smart speakers like the Nest Mini.

Google and Microsoft’s plans are a giant shift away from their prior generation-long China manufacturing strategy and the coronavirus has only supported a strategy to remove China as a core manufacturing hub.

It is getting so bad in China that they are evaluating the feasibility and cost implications to uninstall some production equipment and ship it from China to Vietnam, literally packing up and taking their show on the road.

The have already initiated the process by asking a key sourcing contact to convert an old Nokia factory in the northern Vietnamese province of Bac Ninh to handle the production of Pixel phones.

Data center server production was also rerouted to Taiwan last year.

The coronavirus threat is only speeding up the move into South East Asia and Google and Microsoft hope to avoid the geopolitical risk in the region.

Remember that all of this rejigging of production will add costs and only the biggest can absorb mega hits to the balance sheets.

As for the coronavirus, business is becoming more complicated as the ban on Chinese nationals and flights from China could build barriers to business, and now South Korea has joined the list.

Korea’s Samsung Electronics, the world's largest smartphone maker, has operated a smartphone supply chain in northern Vietnam for years but still relies on some components made in China.

While there are many moving parts, the average investor needs to wait on optimal entry points.

Japan announced school shutdowns for a month and tech shares have only priced in the coronavirus eventually entering the U.S., but if there are mass shutdowns of American cities and schools, then tech shares will see another stinging sell-off.

The contagion could eventually lead to the Olympics in Tokyo being canceled, high-profile corporate management getting infected, and the Chinese economy being sidelined for most of 2020.

All of these events are highly negative to the global economy which is why potential risks have exploded through the roof in such a short time.

Slinging mud at the wall will not work in times like this, but this does have the makings of a once-in-a-year entry point into tech shares.

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader February 26 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: There’s been a moderation of new coronavirus cases in China. Is this what the market needs to find a bottom?

A: Absolutely it is; of course, the next risk is that cases keep increasing overseas. The final bottom will come when overseas cases start to disappear, and that could be a month or two off.

Q: How low will interest rates go after the coronavirus?

A: Well, interest rates already hit new all-time lows before the virus became a stock market problem. The virus is just giving it a turbocharger. Our initial target of 1.32% for the ten-year US Treasury bond was surpassed yesterday, and we think it could eventually hit 1.00% this year.

Q: What is the best way to know when to buy the dip?

A: When the Volatility Index (VIX) starts to drop. If you can get the volatility index down to the mid-teens and stay there, then the market will stabilize and start to rise fairly sharply. A lot of the really high-quality stocks in the market, like United Airlines (UAL), Walt Disney (DIS), Apple (AAPL) and Amazon (AMZN), have really been crushed by this selloff. So those are the names people are going to look at for quality at a discount. That’s going to be your new investment theme, buying quality at a discount.

Q: Do recent events mean that Boeing (BA) is headed down to 200?

A: I wouldn't say $200, but $280 is certainly doable. And if you get to $280, then the $240/$250 call spread all of a sudden looks incredibly attractive.

Q: What does a Bernie Sanders presidency mean for the market?

A: Well, if he became president, we could be looking at like a 50-80% selloff—at least a repeat of the ‘09 crash. However, I doubt he will get elected, or if elected, he won’t have control of congress, so nothing substantial will get done.

Q: Is this the beginning of Chinese (FXI) bank failures that will cause an economic crisis in mainland China?

A: It could be, but the actual fact is that the Chinese government is doing everything they can to rescue troubled banks and companies of all types with short term emergency loans. It’s part of their QE emergency rescue package.

Q: Can you explain what lower energy prices mean for the global economy?

A: Well, if you’re an oil consumer (USO), it’s fantastic news because the price of gas is going down. If you’re an oil producer (XLE), like for people in the Middle East, Texas, Louisiana, Oklahoma, and North Dakota, it’s terrible news. And if you’re involved anywhere in the oil industry, or own energy stocks or MLPs, you’re looking at something like another great recession. I have been hugely negative on energy for years. I’ve seen telling people to sell short coal (KOL). It’s having a “going out of business” sale.

Q: Should I aggressively short Tesla (TSLA) here? Surely, they couldn’t go up anymore.

A: Actually, they could go up a lot more. I would just stay away from Tesla and watch in amazement—there’s no play here, long or short. It suffices to say that Tesla stock has generated the biggest short-selling losses in market history. I think we’re up to about $15 billion now in short losses. Much smarter people than us have lost fortunes trying in that game.

Q: Was that an Amazon trade or a Google trade?

A: I sent out both Amazon and an Apple trade alert this morning. You should have separate trade alerts for each one.

Q: Are chips a long term buy at today’s level?

A: Yes, but companies like NVIDIA (NVDA), Micron Technology (MU), and Advanced Micro Devices (AMD) may be better long-term buys if you wait a couple of weeks and we test the new lows that we’ve been talking about. Chips are the canary in the coal mine for the global economy, and we have not gotten an all-clear on the sector yet. If you’re really anxious to get into the sector, buy a half of a position here and another half 10% down, which might be later this week.

Q: When will Foxconn reopen, the big iPhone factory in China?

A: Probably in the next week or so. Workers are steadily moving back; some factories are saying they have anywhere from 60-80% of workers returning, so that’s positive news.

Q: Are bank stocks a sell because of lower interest rates?

A: Yes, absolutely. If you think the 10-year treasury is running to a 1.00% yield as I do, the banks will get absolutely slaughtered, and we hate the sector anyway on a long-term basis.

Q: What about future Fed rate cuts?

A: Futures markets are now pricing in possibly three more rate cuts this year after discounting no more rate cuts only a few weeks ago. So yes, we could get more interest rates. I think the government is going to pull all the stops out here to head off a corona-induced recession.

Q: Once your options expire, is it still affected by after-hours trading?

A: If you read the fine print on an options contract, they don’t actually expire until midnight on a Saturday night after options expiration day, even though the stock market stops trading on a Friday. I’ve never heard of a Saturday exercise, but you may have to get a batch of lawyers involved if you ever try that.

Q: What’s the worst-case scenario for this correction?

A: Everything goes down to their 200-day moving averages, including Indexes and individual stocks. You’re talking about Apple dropping to $243 and Microsoft (MSFT) to $144, and NASDAQ (QQQ) to 8,387. That could tale the Dow Average (INDU) to maybe 24,000, giving up all the 2019 gains.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

February 14, 2020

Fiat Lux

Featured Trade:

(DATA TELLS THE WHOLE STORY)

(FB), (GOOGL), (NFLX), (AMZN), (EBAY), (TWTR)

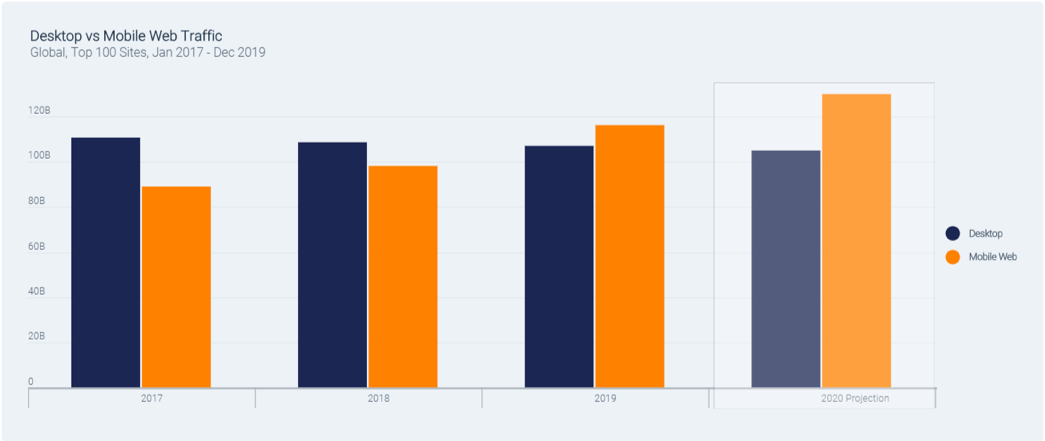

Behavioral trends have a sizable say in which tech companies will outperform the next and a recent report from SimilarWeb offers insight into how much users navigate around the monstrosity known as the internet.

The optimal way to comprehend the trends are from a top-down method by absorbing the divergence between desktop traffic and mobile traffic.

It’s no secret that the last decade delivered consumers a massive leap in mobile phone performance in which tech companies were able to neatly package applications that acted as monetization platforms by offering software and services to the end-user.

Thus, it probably won’t shock you to find out that desktop traffic is down 3.3% since 2017 as users have migrated towards mobile and the trend has only been exaggerated by the younger generations as some have become entirely mobile-only users.

All told, the 30.6% expansion in mobile traffic has penalized tech firms who have neglected mobile-first strategies and one example would be Facebook (FB), who even though has a failing flagship product in Facebook.com, are compensated by Instagram, who is showing wild growth numbers.

The fact that mobile screens are smaller than desktop screens means that users are staying on web pages not as long as they used to – precisely 49 seconds to be exact.

This trend means that content generators are heavily incentivized to frontload content and scrunch it up at the top of the page. This also means that sellers who don’t populate on Google’s first page of search results are practically invisible.

The high stakes of internet commerce are not for the faint of heart and numerous companies have complained about algorithm changes toppling their algorithm-sensitive businesses.

Even using a brute force analysis and investing in companies that are in the top 15 of internet traffic, then the companies that scream undervalued are Twitter (TWTR) and eBay (EBAY).

Twitter is a company I have liked for quite a while and is definitely a buy on the dip candidate.

The asset is the 7th most visited property on the internet behind the likes of Instagram, Google, Baidu, Wikipedia, Amazon, and Facebook.

This position puts them just ahead of Pornhub.com, Netflix, and Yahoo.

And if you take one step back and analyze traffic from the top 100 sites, traffic is up 8% since 2018 and 11.8% since 2017 averaging 223 billion visits per month.

Rounding out the top 15 is eBay who I believe is undervalued along with Twitter - these two are legitimate buy and holds.

Ebay was the recipient of poor management for many years and they are now addressing these sore points.

Certain content is suitable for mobile such as adult sites, gambling sites, food & drink, pets & animals, health, community & society, sports, and lifestyle.

And just over the last year or two, other categories are gaining traction in mobile that once was dominated by desktop such as news and media, vehicle sites, travel, reference, finance, and others.

Many consumers are becoming more comfortable at doing more on mobile and spending more to the point where people are making large purchases on their iPhones.

The biggest loser by far was news - they are losing traffic in droves.

Traffic at the top 100 media publications was down 5.3% year-over-year from 2018 to 2019, a loss of 4 billion visits, and down by 7% since 2017.

Personally, I believe the state of the digital news industry is in shambles, and Twitter has moved into this space becoming the de facto news source while pushing the relevancy of news sites down the rankings.

Facebook and Twitter are essentially undercutting the news by forcing news companies to insert them between the reader and the news company because they have strategized a position so close to the user’s fingertips.

The negative sentiment in news is broad based on popular news, entertainment news and local news all showing decreases of more than 25%.

Finance and women’s interest news categories are the only ones showing positive traffic growth.

The state of internet traffic growth supports my underlying thesis of the big getting bigger and the subsequent network effect stimulating further synergies that drop straight down to the bottom line.

The top 10 biggest sites racked up a total of 167.5 billion monthly visits in 2019, up 10.7% over 2018 and the remaining 90 largest sites out of the top 100 only increased 2.3%.

This has set the stage for just five gargantuan tech firms to become worth more than $5 trillion or 15.7% of the S&P 500’s market value and 19.7% of the total U.S. stock market’s value.

Now we have real data backing up my iron-clad thesis and these cornerstone beliefs underpins my trading philosophy.

Many of the biggest wield a two-headed monster like Google who has Google.com and YouTube video streaming and Facebook, who have Facebook.com and Instagram.

It doesn’t matter that Facebook has lost 8.6% of traffic over the past year because Instagram compensates for Facebook being a poor product.

And if you are searching for another Facebook growth driver under their umbrella of assets then let’s pinpoint chat app WhatsApp who experienced 74% year-over-year traffic.

Beside the news sites, other outsized losers were Yahoo’s web traffic shrinking by 33.6% and Tumblr, which banned adult sites in 2018, leading to a 33% loss in traffic.

If I can sum up the data, buy the shares of companies who are in the top 15 of internet traffic and be on the lookout for any dip in eBay or Twitter because they are relatively undervalued.

Global Market Comments

February 13, 2020

Fiat Lux

Featured Trade:

(I HAVE AN OPENING FOR THE MAD HEDGE FUND TRADER CONCIERGE SERVICE),

(MAD HEDGE FUND TRADER CELEBRATES ITS 12-YEAR ANNIVERSARY)

Mad Hedge Technology Letter

February 12, 2020

Fiat Lux

Featured Trade:

(UBER’S DARK FUTURE)

(UBER), (LYFT), (FB), (AMZN), (NFLX), (GOOGL)

Autonomous or bankrupt; that is the ultimate fate of Uber (UBER).

In the short-term, Uber is a master at moving the goalposts in order to breathe life in the stock.

CEO of Uber Dara Khosrowshahi can only pray that the Fed will continue to pump cheap money into the market because without artificially low-interest loans, tech firms like Uber would implode.

Is it really time to give Uber the benefit of the doubt?

No more hype, just profits? Is the calculus to profits legitimate?

That's what we call a bubble. Bubbles always burst. Here's the scary part.

Many people are counting on the continued existence of Uber and Lyft to provide "cheap transportation."

Commuters will have to get suddenly unused to it.

There are many companies today that are running the same scheme as Uber in the “gig economy.”

It’s true that management loves to use a lot of flowery language to disguise a lack of profitability.

But as the conditions are ripe for a leg up in tech, the tide rises, and even Uber’s boat rises with it.

I have yet to see even one realistic analysis of how Uber or Lyft is going to become profitable - not even basic math!

I have met a plethora of drivers for both companies, and hope they do well, but there is only so long that one can put lipstick on a pig.

So here we are, Uber in the green everyday because they moved the goalposts yet again and promise us earlier than expected profitability but still losing billions of dollars.

Lyft and Uber have apparently increased revenues somewhat by reducing promotional discounts to riders, but that does not project to even a breakeven point and the unit economics tell me no even if my heart says yes.

The only trick up their sleeve seems to be fare increases, but where is the roadmap detailing this treacherous path?

Once we get to the point in time when Uber is supposed to be profitable, I bet that management will call in another trick play and move the goal posts yet again.

It is quite laughable when so called “tech experts” want Uber to join the ranks of Facebook Inc. (FB), Amazon.com Inc. (AMZN), Netflix Inc. (NFLX), and Alphabet Inc.’s Google (GOOGL) as part of a FANGU acronym.

Reasons for this new bundle is thought to be because of the ability to take advantage of its massive scale while working toward profitability.

Uber is the global ridesharing leader and is becoming the global food delivery leader, but do they really add value?

What if the local government finally got their finger out and built a proper transport system?

They are merely taking advantage of a broken system and passing on the costs of paying drivers to the drivers themselves by designating them as hourly workers.

Are we supposed to celebrate when Uber becomes more “rational?”

Meaning that players have limited their attempts to undercut one another with the sorts of pricing and big discounts that had at one time suggested the business might be a race to the bottom.

Uber projected a lower loss than analysts were expecting for 2020, does less loss mean profits in 2020?

And I do agree that it is encouraging that the company is finally disclosing more data, but shouldn’t they be doing that in the first place?

Love it or hate it, there is a “war” going on between profitability and growth at Uber as the company manages the trade-offs.

Uber had previously talked up that it would become Ebitda profitability by the end of 2021, but Khosrowshahi now forecasts profitability for the fourth quarter of this year.

He says it is possible because Uber initiated a “belt-tightening program” in the last half of 2019, exiting unprofitable ventures and laying off about 1,000 employees.

For instance, Uber sold its food-delivery business in India to a local startup, Zomato, in return for a 9.9% stake in that company.

I do believe that they haven’t done enough to build credibility with investors and the stock’s price action is behaving as we should trust Uber’s management with whatever comes out of their mouths.

The lack of visibility and uncertainty around trends in ridesharing and Eats outside the U.S. continue to be hard to quantify.

So that sounds great! Uber is more serious than ever about becoming profitable and investors have backed them up with the stock flying to the moon.

The trend is your friend and I would suggest readers to get out of the way of this one because you could get trampled on just like the Tesla bears.

And I do support Uber in making steps in the right direction and it also can be said that stocks appreciate the fastest when they transform from a horrible company to a less horrible company.

But there is no way that I am giving Khosrowshahi a pass for Uber’s current situation and no chance I am praising him to the hills.

It is what it is, and Uber is less bad than before, and if they don’t meet their targets, I don’t think investors will believe Khosrowshahi version of a spin doctor forecast anymore.

Uber will rise in the foreseeable future and if they fail to become profitable by 4th quarter, expect a massive drawdown.

If they succeed, expect a vigorous wave of new players to buy into Uber shares.

The stakes have never been higher for Uber and Khosrowshahi.

Global Market Comments

February 10, 2020

Fiat Lux

Featured Trade:

(LEARN MORE ABOUT ME THAN YOU PROBABLY WANT TO KNOW),

(GOOG), (AMZN), (AMGN)

(WHO SAYS THERE AREN’T ANY GOOD JOBS?),

(TESTIMONIAL)

As you may imagine, the most interesting man in the world is impossible to shop for when it comes to Christmas and birthdays.

So, it was no surprise when I opened a box and found a DNA testing kit from 23 and Me. So, I spit into a small test tube to humor the kids, mailed it off, and forgot about it.

I have long been a keeper of the Thomas family history and legends, so it would be interesting to learn which were true and which were myths.

A month later, what I discovered was amazing.

For a start, I am related to Louis the 16th, the last Bourbon king of France who was beheaded after the 1789 revolution.

I am a direct descendant from Otzi the Iceman who is 5,000 years old and was recently discovered frozen in an Alpine glacier. He currently resides in mummified form in an Italian museum.

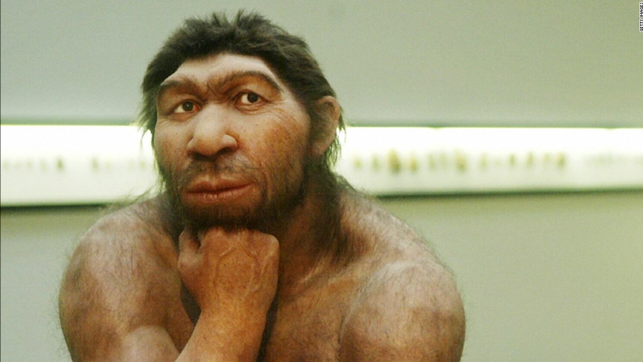

Oh, one more. The reason I don’t have any hair on my back is that I carry 346 gene fragments that I inherited directly from a Neanderthal. Yes, I am part caveman, although past girlfriends suspected as much.

There were other conclusions.

I have a higher than average probability of getting prostate cancer, advanced macular degeneration (my mother had it), celiac disease, and melanoma.

The service also offered to introduce me to 1,107 close relatives around the world who I didn’t know, mostly in New York, California, and Florida.

The French connection I already knew about. During the 16th century, my ancestors rebelled against the French kings over the non-payment of taxes and were exiled to Louisiana. Fleeing a malaria epidemic, they moved up the Mississippi River to St. Louis and stayed there for 200 years. When gold was discovered in California in 1849, they joined a wagon train west. We have been here ever since.

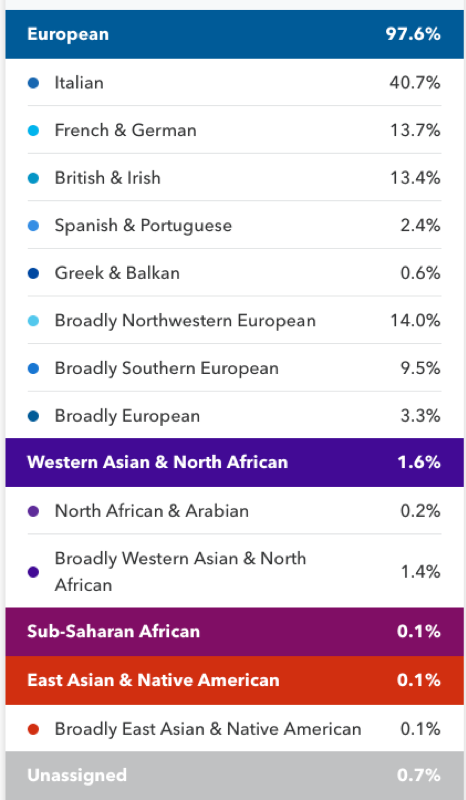

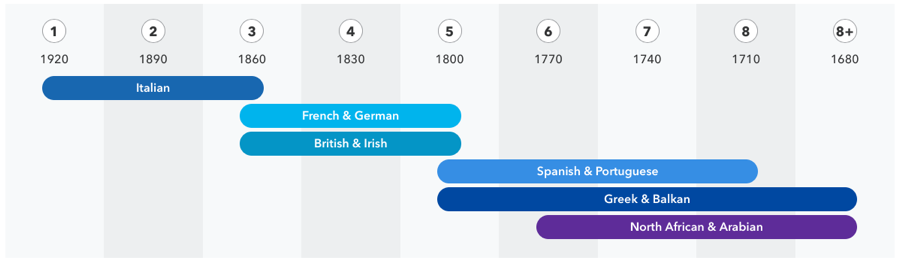

I am half Italian and have birth certificates going back to 1800 to prove it. But 23 and Me says that I am only 40.7% Italian (see table below). It turns out that your genes show not only where you came from, but also who invaded your home country since the beginning of time.

In Italy’s case that would include the ancient Greeks, Vikings, Arabs, the Normans, French, Germans, and the Spanish, thus making up my other 9.3%. Your genes also reflect the slaves your ancestors owned, for obvious reasons, as well as many of the servants who may have worked for them.

It gets better.

All modern humans are decended from a single primordial “Eve” who lived in Eastern Africa 180,000 years ago. Of the thousands of homo sapiens who probably lived at that time, the genes of no other human made it into the modern age. We are all decended from a single “Adam” who lived 275,000 years ago. Obviously, the two never met, debunking some modern conventions.

Around 53,000 years ago, my intrepid ancestors cross the Red Sea to a lush jungle in the Sinai Penninsula probably pursuing abundant game. 53,000 years ago, they moved on the vast grasslands of the Cental Asian Steppes. As the last Ice Age retreated, they moved into the warmer climes of South Europe. We have been there ever since.

23 and Me was founded in 2006 by Anne Wojcicki, wife of Google founder Sergei Brin. It is owned today by her and a few other partners. Its name is based on the fact that humans' entire DNA code is found on 23 chromosomes.

23 and Me and other competitors like Ancestry.com, MyHeritage, and Living DNA have sparked a DNA boom that has led to once unimaged economic and social consequences. DNA promises to be for the 21st century what electricity was to the 20th century. The investment consequences are amazing.

Talk about unintended consequences with a turbocharger.

A common ancestor going back to the early 1800s enabled Sacramento police to capture the Golden State killer. Unsolved for 40 years, it took a week for them to find him after a DNA sample was sent to a DNA database.

Thirty and 40-year cold cases are now being solved on a weekly basis. Long ago kidnapped children are being reunited with parents after decades of separation.

California just froze all executions. That’s because DNA evidence showed that approximately 30% of all capital case convictions were of innocent men. That was enough for me to change my own view on the death penalty. The error rate was just too high. Dozens of men around the country have been freed after new DNA evidence surfaced, some after serving 30 years or more in prison.

23 and Me had some medical advice for me as well. They strongly recommended that I get tested for diabetes and high blood pressure as these maladies are rife among my ancestors. They even name the specific guilty gene and haploid group.

This explains why major technology companies, like Amazon (AMZN) and Apple (AAPL), are pouring billions of dollars into genetic research.

I have long had a personal connection with DNA research. I worked on the team that sequenced the first ever string of DNA at UCLA in 1974. It was groundbreaking work. We obtained our raw DNA from Dr. James Watson of Harvard who, along with Francis Crick, was the first to discover its three-dimensional structure. As for my UCLA professor, Dr. Winston Salser, he went on to found Amgen (AMGN) in 1980 and became a billionaire.

The developments that are taking place today then seemed to us like science fiction that was hundreds of years into the future. To see the paper created by this work, please click here.

As research into DNA advances, it is about to pervade every aspect of our lives. Do you have a high probability of getting a disease that costs a million dollars to cure and is counting on getting health insurance? Think again. That may well bring forward single-payer national healthcare for the US, as only the government could absorb that kind of liability.

And if you can only hang on a few years, you might live forever. That’s when DNA-based monoclonal antibodies and gene editing are about to cure all major human diseases. DNA is about to become central to your physical health and your financial health as well.

To learn more about 23 and Me please visit their website here.

Maybe the next time I visit the Versaille Palace outside of Paris, I should ask for a set of keys now that I’m a relative? Unfortunately, it’s much more likely that I’ll get the keys to my Neanderthal ancestor’s cave.