Global Market Comments

June 7, 2019

Fiat Lux

Featured Trade:

(SUNDAY, JUNE 30 MANILA, PHILIPPINES STRATEGY LUNCHEON)

(THE CONTINUING DEATH OF RETAIL),

(AMZN), (WMT), (M), (JWN),

(TESTIMONIAL)

Global Market Comments

June 7, 2019

Fiat Lux

Featured Trade:

(SUNDAY, JUNE 30 MANILA, PHILIPPINES STRATEGY LUNCHEON)

(THE CONTINUING DEATH OF RETAIL),

(AMZN), (WMT), (M), (JWN),

(TESTIMONIAL)

Global Market Comments

June 5, 2019

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 26 BRISBANE, AUSTRALIA STRATEGY LUNCHEON)

(WHY CONSUMER STAPLES ARE DYING),

(XLP), (PG), (KO), (PEP), (PM), (WMT), (AMZN),

(WHY YOUR OTHER INVESTMENT NEWSLETTER IS SO DANGEROUS)

Mad Hedge Technology Letter

June 4, 2019

Fiat Lux

Featured Trade:

(THE GOVERNMENT’S WAR ON GOOGLE)

(GOOGL), (FB), (AMZN)

I told you so.

It’s finally happening.

The Department of Justice (DOJ) preparing an antitrust probe on Google (GOOGL) was never about if but when.

The Federal Trade Commission is in the fold as well, as they have secured the authority to investigate Facebook (FB).

The probe will peel back the corrosive layers of Facebook and Google’s businesses such as search, ad marketplace and its other assets in order to excavate the truth.

Investors will get color on whether these businesses are gaining an unfair advantage and perverting the premise of fair competition that every tech company should abide by.

Tech companies skirting the law and living on the margins are in for a stifling reckoning if these probes pick up steam.

Facebook is about to get dragged through the mud kicking and screaming facing an unprecedented existential crisis that have repercussions to not only the broad economy for the next 50 years, but far beyond American shores with America mired in a trade war pitted against the upstart Chinese most powerful tech companies.

Even though I have consistently propped up Alphabet on a pedestal as possessing a few of the most robust assets in tech, I have numerous times flogged their dirty laundry in public view, referencing the regulatory risks that could rear its ugly head at any time.

These companies have been playing with fire and everyone knows it, but in the world of short-term results via stock market earnings report, this trade kept working until governments decided to get their act together because of the accelerating erosion of government trust partly facilitated by technology apps.

As much as a handful of Americans have monetized Silicon Valley to great effect, I can tell you that I spend a great deal of my time abroad, and American soft power is at a generational low ebb.

Blame technology - our dirty secrets are not only exposed in frontal view but it’s pretty much a 3D view of the good, bad, and the ugly and there is a lot of ugly.

I am not saying that punishment is a given for these ultra-rich firms swimming in money.

Historically, Alphabet has stymied regulators before beating out an antitrust investigation in 2013 after a two-year inquiry ended with the FTC unanimously voting to halt the investigation.

Remember that this time around, the probe follows the fine in Europe when The European Union slapped Google with a $1.69 billion for actively disrupting competition in the online advertisement sector.

The European Commission claimed that Google installed exclusivity contracts on website owners, preventing them from populating on non-Google search engines.

It was quite a dirty trick, but do you expect much of anything else from one of the most crooked industries in the economy?

And this wasn’t the first time that Google has run amok.

EU regulators levied a $5 billion penalty on Google for egregious violations regarding its dominance of its Android mobile operating system.

Google was accused by the EU of favoring its in-house apps and services on Android-based smartphones giving manufacturers no alternative but to bundle Google products like Search, Maps and Chrome with its app store Play ensuring that Alphabet would benefit from a lopsided arrangement.

Anti-trust legislation has a myriad of supporters including the current administration who have stepped up its onslaught on Silicon Valley.

President of the United States Donald Trump has even hurled insults at Amazon (AMZN) creator Jeff Bezos and even claimed that Alphabet’s artificial intelligence has aided China’s technological rise.

To say FANG companies are in the good graces of Washington would be laughable.

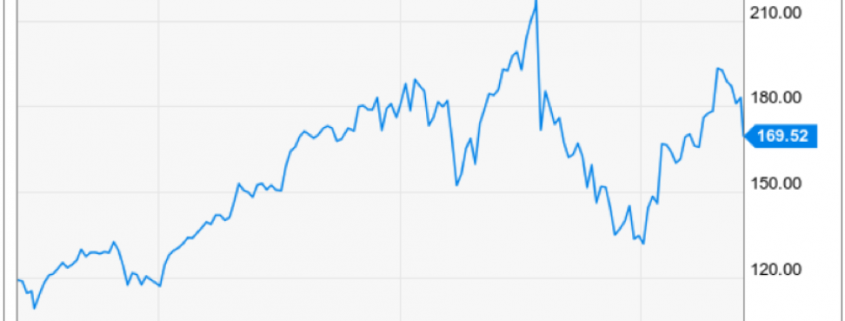

I would point to Facebook to accelerating the regulatory headwinds as investors have seen Co-Founder and CEO Mark Zuckerberg fire every major executive that has opposed his vision of merging Facebook, Instagram, and WhatsApp into a cesspool of apps that pump out precious big data.

The tone-deaf boss has doubled down to reinvigorate the growth after Facebook sold off from $210.

Board members want Zuckerberg out and he is defiant against any attack on his leadership spinning it around as a vendetta on his reign.

Facebook is walking straight into a minefield and the rest of Silicon Valley is guilty by association, the contagion is that bad.

Facebook is the one to blame because of the daily nature of social interaction on its platform and the pursuance of revenue through hyper-targeting data that 3rd party companies pay access for.

They have no product.

Amazon sells consumer goods which is not as bad.

Facebook facilitates the social dialogue that has unwittingly boosted extremism of almost every type of form possible.

It has given the marginal and nefarious characters in society a platform in which to engineer devastating results and Facebook have an incentive to turn a blind eye to this because of the lust for user engagement.

This has resulted in heinous activities such as terror attacks being broadcasted live on Facebook like the 2019 New Zealand massacre at a mosque.

The former security chief at Facebook Alex Stamos hinted that Mark Zuckerberg’s tenure should wind down and the company needs to shape up and hire a replacement.

The security implications are grave, and many Americans have uploaded all their private information onto the platform.

What is the end game?

Facebook is in hotter water than Google, not by much, but their business model engineers more mayhem than Google currently.

Facebook could get neutered to the point that their ad model is dead and buried.

If Facebook goes down, this would unlock a treasure chest full of ad dollars looking for new avenues.

Facebook’s most precious asset is their data which might be blocked from being monetized moving forward.

Without data, they are worth zero.

The existential risk is far higher for Facebook than Alphabet.

No matter what, Alphabet will still be around, but in what form?

Assets such as YouTube, Google Search, and Waymo, which are all legitimate services, could get spun out to fend for themselves creating many offspring left to sink or swim.

In this case, YouTube, Google Maps, Chrome, Google Play, and Google Search would still possess potent value and offer shareholders future value creation.

Waymo would become a speculative investment based on the future and would be hard to predict the valuation.

Then there is the issue of whether Chinese companies would dominate the collection of FANGs after the split or not.

As I see it, Chinese tech companies will not be allowed to operate in the U.S. at all, and anti-trust repercussions will have many of these homegrown tech companies carved out of their parents to reset a level playing field in a way to re-democratize the tech economy.

This would spur domestic innovation allowing smaller companies to finally compete on a national stage.

The government finally clamping down epitomizes the current volatile tech climate and how Alphabet who has some of the best assets in the industry can go from barnstormer to pariah in a matter of seconds.

As for Facebook, they have always had a bad stench.

The cookie could still crumble in many ways, each case looks high risk for Facebook and Google for the next 365 days.

Stay away from these shares until we get any meaningful indication of how things will play out, but I have a feeling this is just the beginning of a tortuous process.

Global Market Comments

June 3, 2019

Fiat Lux

Featured Trade:

(MONDAY, JUNE 24 MELBOURNE, AUSTRALIA STRATEGY LUNCHEON)

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR WHAT A WASTE OF TIME!),

(SPY), ($INDU), (JPM), (MSFT), (AMZN), (TSLA)

“Sell in May and go away” has long suffered from the slings and arrows of non-believers, naysayers, and debunkers.

Not this time.

Looking at the trading since April 30, we have barely seen an up day. Since then, the Dow Average has plunged 1,900 points from a 26,700 high, a loss of 7.1%. We are now sitting right at my initial downside target of the 200-day moving average.

The Dow has now given up virtually all its 2019 gains, picking up only 2.0%. In fact, the market is dead unchanged since the end of 2017. If you have been an index investor for the past 17 months, your return has been about zero. In other words, it has been a complete waste of time.

There are a lot of things I would have preferred to do rather than invest in index funds for the past year and a half. I could have hiked the Pacific Crest Trail….twice. I might have taken six Cunard round-the-world cruises and met several rich widows along the way. I might even have become fluent in Italian and Latin. Such is the value of 20-20 hindsight.

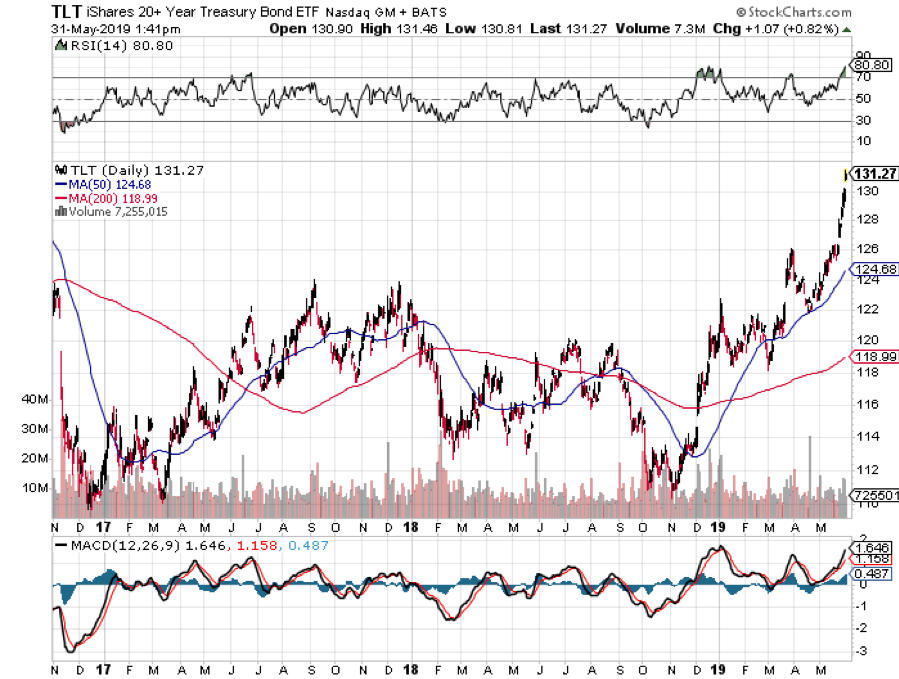

You would have done much better investing in the bond market, which has exploded to a new two-year high, taking the ten-year US Treasury yield down to a once unimaginable 2.16%. During the same period, the (TLT) has gained 11 points, or 9.0% plus another 3.0% worth of interest. You did even better if you invested in lower grade credits.

Which leads us to the big question: Will stocks bottom out here, or are we in for a full-on retrace to the December lows?

Unfortunately, recent events have conspired to point to the latter.

The United States has now declared trade wars against all neighbors and allies around the world: China, Mexico, Europe, and Canada. On Friday, it announced 25% punitive tariffs against Mexico before NAFTA 2.0 was even ratified before Congress, thus rendering it meaningless. Businesses are dropping like flies.

As a result, GDP forecasts have been falling off a cliff, down from 3.2% in Q1 to under 1% for Q2. The administration’s economic policy seems to be a pain now, and more pain later. It is absolutely not what stock investors want to hear.

If you are a business owner now, what do you do with the global supply chain being put through a ringer? Sit as firmly on your hands as possible and do nothing, waiting for either the policy or the administration to change. Stock investors don’t want to hear this either. The fact that stock markets entered this cluster historically expensively is the fat on the fire.

Having hummed the bear national anthem, I would like to point out that stocks could rally from here. We enter a new month on Monday. There will be plenty of opportunities to make amends and the G-20 meeting which starts on June 20. This should provide a backdrop for a rally of at least one-third of the recent losses, or about 600 points.

But quite honestly, if that happens, I’ll be a seller. The economy is doing the best impression of going down the toilet that I can recall, and that includes 2008. Only this time, all the injuries are self-inflicted.

As the trade war ramped up, China moved to ban FedEx (FDX) and restrict rare earth exports (REMX) to the US essential for all electronics manufacture. Most modern weapons systems can’t be built without rare earths. The big question in investors' minds becomes “Is Apple next?”

The OECD cut its global growth forecast from 3.9% to 3.1% for 2019 because of you know what. Stock markets are now down for their sixth week as the 200-day moving average comes within striking distance.

There was more bad news for real estate with April Pending Home Sales down 1.5%. If rates this low can’t help it, nothing will. Where are those SALT deductions?

The bear market in home prices continued in March with the Case Shiller CoreLogic National Home Price Index showing a 3.7% annual price gain, down 0.2%. Home price in San Francisco is posting negative numbers. When will those low-interest rates kick in?

The bond market says the recession is already here with ten-year interest rates at 2.16%, a new 2019 low. German bunds hit negative -0.21%. JP Morgan (JPM) CEO Jamie Diamond says the trade war could cause real damage to the US economy.

US Capital Goods fell out of bed in April, down 0.9%, in another important pre-recession indicator. No company with sentient management wants to expand capacity ahead of an economic slowdown.

Despite all the violence and negativity, the Mad Hedge Fund Trader managed to crawl to new all-time highs last week, thanks to some very conservative positioning on the long side in the right names.

Those would include Microsoft (MSFT), Amazon (AMZN), and Tesla (TSLA). All of these names were down on the week, but the vertical bull call spreads were up. You see, there is a method to my madness!

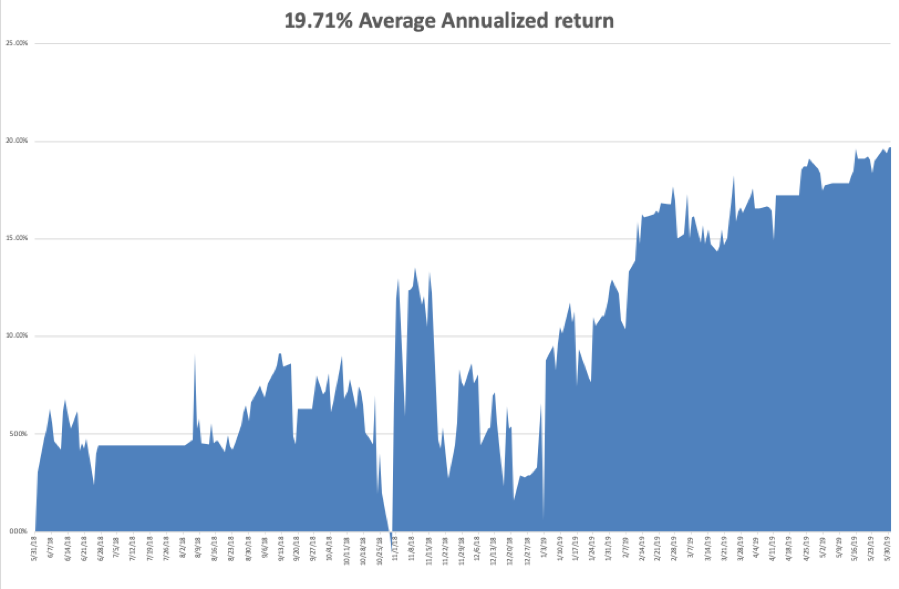

Global Trading Dispatch closed the week up 16.30% year-to-date and is up 0.51% so far in May. My trailing one-year declined to +19.71%.

The Mad Hedge Technology Letter did fine, making money on longs in Microsoft (MSFT) and Amazon (AMZN). Some 10 out of 13 Mad Hedge Technology Letter round trips have been profitable this year.

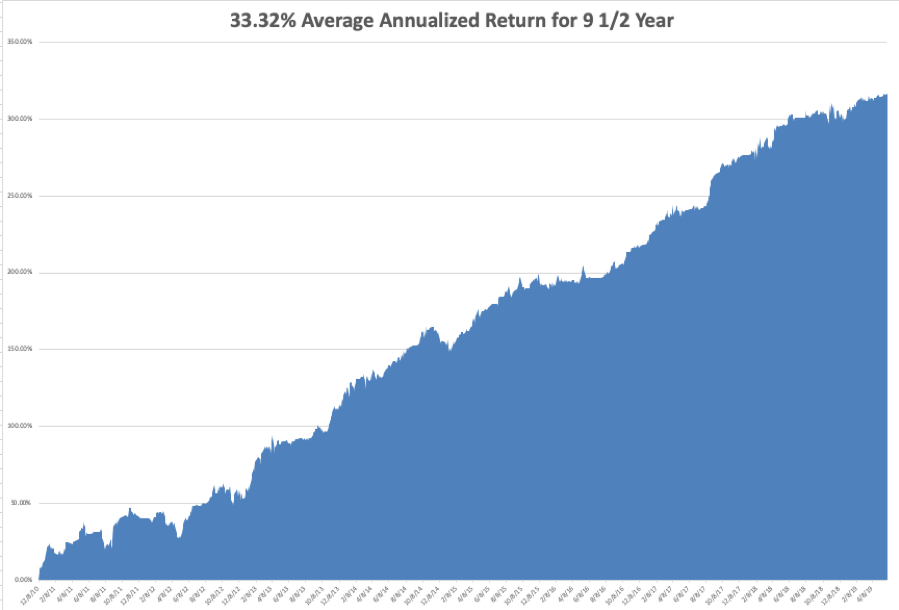

My nine and a half year profit jumped to +316.55%. The average annualized return popped to +33.32%. With the trade war with China raging, I am now 70% in cash with Global Trading Dispatch and 80% cash in the Mad Hedge Tech Letter.

I’ll wait until the markets enjoy a brief short-covering rally before adding any short positions to hedge my longs.

The coming week will be a big one with the trifecta of big jobs reports.

On Monday, June 3 at 7:00 AM, the May US Manufacturing PMI is out.

On Tuesday, June 4, 9:00 AM EST, the April US Factory Orders are published.

On Wednesday, June 5 at 5:15 AM, the May US ADP Employment Report of private hiring trends is released.

On Thursday, June 6 at 5:30 AM, the April US Balance of Trade is printed. At 8:30 Weekly Jobless Claims are published.

On Friday, June 7 at 8:30 AM, we learn the May Nonfarm Payroll Report is announced which lately has been incredibly volatile.

As for me, I am going to be leading the local Boy Scout troop on a 20-mile hike with a 2,500-foot vertical climb in the Oakland Hills. Hey, you never know when Uncle Sam is going to come calling again. I need to stay boot camp-ready at all times.

At least I can still outpace the eleven-year-olds. I’ll be leaving my 60-pound pack in the garage so it should be a piece of cake.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

May 30, 2019

Fiat Lux

Featured Trade:

(IS TARGET THE NEXT FANG?)

(TGT), (AMZN), (WMT)

Mad Hedge Technology Letter

May 29, 2019

Fiat Lux

Featured Trade:

(CHINA TO BAN FEDEX)

(HUAWEI), (AMZN), (FDX), (UPS), (DPSGY), (BABA), (ZTO)

Sell any and all rallies in FedEx (FDX) – that’s my quick takeaway from the Chinese communist party publishing a sharp retort to their de-facto mouthpiece of a publication called the Global Times signaling FedEx’s imminent demise in greater China.

The Global Times is often used as thinly veiled statements to a wider global audience and mimics the ideology of the ruling communist party and their main positions on critical issues.

As regards to FedEx’s business in China, it said:

“There are rising calls for China's postal service regulator to cut off FedEx from China market, as Huawei has accused the US express courier of diverting and rerouting its packages.”

FedEx is crushing the Chinese logistics market currently and is the go-to carrier holding firm at 54.6% market share.

They have been around in China for as long as the economic boom has percolated inside the mainland from 1984, far before any of its local competitors were even up and running by a decade or two.

FedEx’s latest acquisition of Dutch-based TNT Express in 2016 solidified its dominance.

Foreign competition is a mainstay of international shipping patterns in China with the top three rounded out by DHL (DPSGY) with a 25.07% market share and United Parcel Service (UPS) with a 16.94% market share.

If these assertive claims do result in FedEx meaningfully losing China revenue, UPS wouldn’t stand to pick up the leftovers and could be put out to pasture by the same issue of hailing from a country that has an active adversarial economic policy against China’s.

If anyone would benefit, it would by DHL, given that Germany has a far less hawkish stance towards China, and they are unwilling to bite off the hand that feeds them.

The current situation is a concerning sign for the future of Germany as an industrial power and ability to sustain itself against China Inc.

It could be somewhat true that Germany has overextended themselves and only time, Made in China 2025 project, and the mood of the Chinese communist party can delay the inevitability of full tech hegemony over their western European counterpart.

The communist party could choose to just bypass DHL altogether and kick out all foreign invaders gifting courier responsibilities to Alibaba-based (BABA) subsidiaries and the likes of ZTO Express (ZTO) who provide express delivery and other value-added logistics services in China.

DHL will hope that China delays any draconian measures and pray that its active partnership with a local logistic firm has real legs.

DHL's revenue sharing agreement with SF Express does not preclude them from the anger of Chinese regulators, but the risk of Chinese regulators favoring local couriers has risen another 25%.

Playing by the rules goes a long way in China, even if they change every day, and for customers across DHL’s target audience of industries including technology, health care, retail, automotive, and e-commerce.

DHL CEO Frank Appel said, "Combined with our global operations standards and network support, the agreement provides a solid foundation to continue exploring further opportunities in China in the coming years."

From an outside perspective, this sounds more like forced cooperation with forced technology transfers with the mainland companies slurping up Germany tech knowhow.

Doing a deal with the devil for access to a 1.3 billion customer market is being put through the ringer.

When I view the snippets through the lens of geopolitics, it’s hard to believe that at such a sensitive time, FedEx would actively “reroute” packages and knowingly approved this behavior, they simply can’t be that clumsy.

The situation smells like an overt show of nationalism by a group of individuals, and it questions the longevity of FedEx operating in China all the same.

FedEx promptly responded confessing:

“We regret that this isolated number of Huawei packages were inadvertently misrouted.”

An unintentional mistake offered a golden opportunity to tie the logistics company to the U.S. government’s aggressive nature and going forward FedEx will remain in a shroud of mystery until investors can get further grips on the rates of growth of their Chinese operations.

If FedEx were afraid about this, then they must be tearing their hair out about the domestic behemoth that is Amazon (AMZN) and their desires to install a full-service logistic service to blanket FedEx from e-commerce deliveries.

This has been the initial premise of my short call on FedEx, which has proved correct, and the regulatory nightmare in China will cast another cloud around its business.

Any strength in FedEx shares will be met with a cascade of selling activity, and as the economy slows down because of tariff-induced headwinds, this is a stock to outright short.

Back to China, FedEx slashed its full-year profit forecast for the second time in three months after reporting weaker-than-expected third quarter earnings.

The Chinese economy is absolutely slowing down, and its effects are impacting surrounding Asian nations.

Manufacturing cuts will cause the number of courier packages to slide in China and there is no telling how bad this trade stand-off could get.

It doesn’t look good for FedEx, and I reiterate my short stance on the company.

Mad Hedge Technology Letter

May 22, 2019

Fiat Lux

Featured Trade:

(WHY YOU NEED TO CONSIDER ALIBABA)

(BABA), (AMZN)