Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(THE ARTIFICIAL INTELLIGENCE CONUNDRUM),

(TSLA), (AMZN), (FB)

Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(THE ARTIFICIAL INTELLIGENCE CONUNDRUM),

(TSLA), (AMZN), (FB)

Anti-A.I. physicist Professor Stephen Hawking was a staunch supporter of preserving human interests against the future existential threat from machines and artificial intelligence (A.I.).

He was diagnosed with motor neuron disease, more commonly known as Lou Gehrig's disease, in 1963 at the age of 21 and sadly passed away March 14, 2018 at the age of 76.

Famed for his work on black holes, Professor Hawking represented the human quest to maintain its superiority against quickly advancing artificial acculturation.

His passing was a huge loss for mankind as his voice was a deterrent to A.I.'s relentless march to supremacy. He was one of the few who had the authority to opine on these issues. Gone is a voice of reason.

Critics have argued that living with A.I. poses a red alert threat to privacy, security, and society as a whole. Unfortunately, those most credible and knowledgeable about A.I. are tech firms. They have shown that policing themselves on this front is remarkably unproductive.

Mark Zuckerberg, CEO of Facebook (FB), has labeled naysayers as "irresponsible" and dismissed the threat. After failing to prevent Russian interference in the last election, he is exhibiting the same defensive posture translating into a de facto admission of guilt. His track record of shirking accountability is becoming a trend.

Share prices will materially nosedive if A.I. is stonewalled and development stunted. Many CEOs who stake careers on doubling or tripling down on A.I. cannot see it die out. There is too much money to lose.

The world will see major improvements in the quality of life in the next 10 years. But there is another side to the coin which Zuckerberg and company refuse to delve into...the dark side of technology.

Defective Amazon (AMZN) Alexa recently produced unexplained laughter because of a mistaken command to start laughing. Despite avoiding calamity, these small events show the magnitude of potential chaos capable of haywire A.I. functions. If one day a user attempts to order a box of tissues and Alexa burns down the house, who is liable?

Tesla's (TSLA) CEO Elon Musk has shared his anxiety about robots flipping the script on humans. Elon acknowledges that A.I. and autonomous vehicles are important factors in the battle for new technology. The winner is yet to be determined as China has bet the ranch with unlimited resources from Chairman Xi.

The quagmire with China has been squarely centered around the great race for technological supremacy.

A.I. is the ultimate X factor in this race and whoever can harness and develop the fastest will win.

Musk has hinted that robots and humans could merge into one species in the future. Is this the next point of competition among tech companies? The future is murky at best.

Bill Gates noted that robots should be taxed like humans. This reflects the bubble in which the ultra-elite reside. This comment implies that humans and robots are at the same level. It shows a severe lack of empathy for the 40% of working Americans who will be replaced by machines over the next 10 years.

The West is comprised of a deeply hierarchical system of winners and losers. Hawking's premise that evolution has inbuilt greed can be found in the underpinnings of America's economic miracle.

Wall Street has bred a culture that is entirely self-serving regardless of the bigger system in which it finds itself.

Most of us are participating in this perpetual money game chase because our system treats it as a natural part of life. A.I. will help more people do well in this paper chase to the detriment of the majority.

Quarterly earnings performance is paramount for CEOs. Return value back to shareholders or face the sack in the morning. It's impossible to convince anyone that America's capitalist model is deteriorating in the greatest bull market of all time.

Wall Street has an insatiable hunger for cutting-edge technology from companies that sequentially beat earnings and raise guidance. Flourishing technology companies enrich the participants creating a Teflon-like resistance to downside market risk.

The issue with Professor Hawking's work is that his timeframe is too far in the future. Professor Hawking was probably correct, but it will take 25 years to prove it.

The world is quickly changing as science fiction becomes reality. The year 2019 will signal the real beginning of A.I. in tangible form when autonomous fleets flood main streets and is another step in the direction of human's overreliance on machines.

People on Wall Street are a product of the system in place and earn a tremendous amount of money because they proficiently execute a specialized job. Traders are busy focusing on how to move ahead of the next guy.

Firms building autonomous cars are free to operate as is. Hyper-accelerating technology spurs on the development of A.I., machine learning, and enhanced algorithms. Record profits will topple, and investors will funnel investments back into an even narrower grouping of technology stocks after the weak hands are flushed out.

Professor Hawking said we need to explore our technological capabilities to the fullest in order to avoid extinction. In 2018, exploring these new capabilities still equals monetizing through the medium of products and services.

This is all bullish for equities as the leading companies associated with A.I. will not be subject to any imminent regulation, blowback, or government intervention.

And let me remind you that technology is still the least regulated industry on the planet.

It has its cake and is eating it too. Hence, technology is starting to cross over into other industries demonstrating the powerful footprint tech has extracted in economics and the stock market.

The only solution is keeping companies accountable by a function of law or creating a third-party task force to regulate A.I. In 2018, the thought of overseeing robots sounds crazy.

However, by 2019, it might be as normal as uncontrollable laughter from your smart home.

There is only so much juice you can squeeze from a lemon before nothing is left.

Silicon Valley has been focused mainly on squeezing the juice out of the Internet for the past 30 years with intense focus on the American consumer.

In an era of minimal regulation, companies grew at breakneck speeds right into families' living quarters and it was a win-win proposition for both the user and the Internet.

The cream of the crop ideas was found briskly and the low hanging fruit was pocketed by the venture capitalists (VCs).

That was then, and this is now.

No longer will VCs simply invest in various start-ups and 10 years later a Facebook (FB) or Alphabet (GOOGL) appears out of thin air.

That story is over. Facebook was the last one in the door.

VCs will become more selective because brilliant ideas must withstand the passage of time. Companies want to continue to be relevant in 20 or 30 years and not just disintegrate into obsolescence as did the Eastman Kodak Company, the doomed maker of silver-based film.

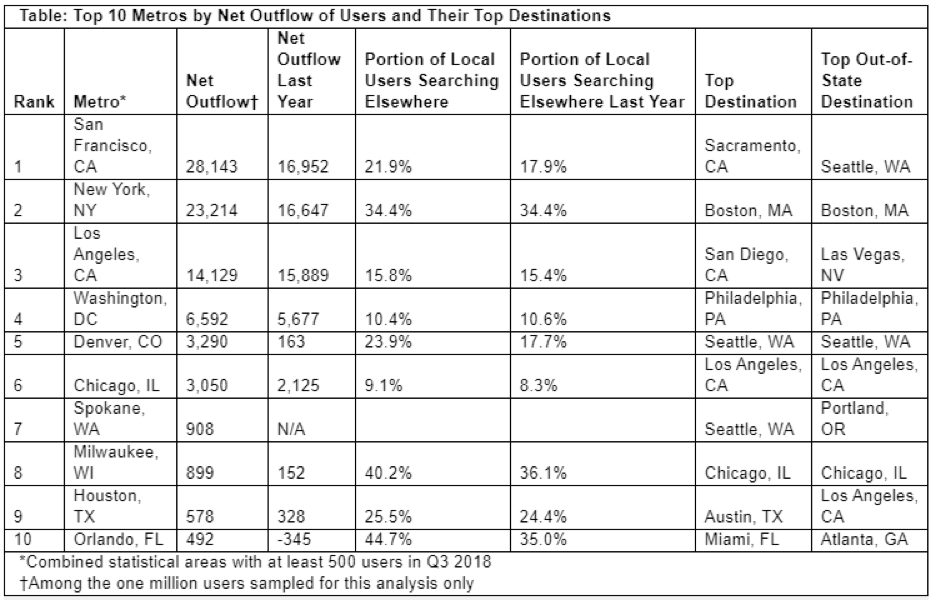

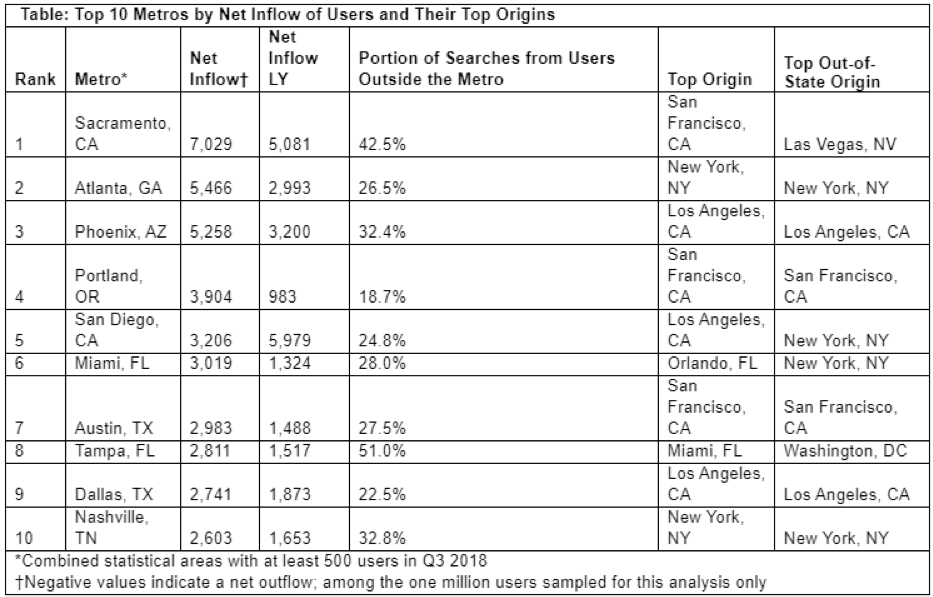

The San Francisco Bay Area is the mecca of technology but recent indicators have presaged the upcoming trends that will reshape the industry.

In general, a healthy and booming local real estate sector is a net positive creating paper wealth for its local people and attracting money slated for expansion.

However, it's crystal clear the net positive has flipped and housing is now a buzzword for the maladies young people face to sustain themselves in the ultra-expensive coastal Northern California megacities.

The loss of tax deductions in the recent tax bill makes conditions even more draconian.

Monthly rental costs are deterring tech's future minions. Without the droves of talent flooding the area, it becomes harder for the industry to incrementally expand.

It also boosts the costs of existing development/operations staffers whose capital feeds back into the local housing market buying whatever they can barely afford for astronomical prices.

Another price spike ensues with first-time home buyers piling into already bare-bones inventory because of the fear of missing out (FOMO).

After surveying HR tech heads, it's clear there aren't enough artificial intelligence (A.I.) programmers and coders to fill internal projects.

Compounding the housing crisis is the change of immigration policy that has frightened off many future Silicon Valley workers.

There is no surprise that millions of aspiring foreign students wish to take advantage of America's treasure of higher education because there is nothing comparable at home.

The best and brightest foreign minds are trained in America and a mass exodus would create an even fiercer deficit for global dev-ops talent.

These U.S.-trained foreign tech workers are the main drivers of foreign tech start-ups.

Dangling carrots and sticks for a chance to start an embryonic project in the cozy confines of home is hard to pass up.

Ironically enough, there are more A.I. computer scientists of Chinese origin in America than there are in all of China.

There is a huge movement by the Chinese private sector to bring everyone back home as China vies to become the industry leader in A.I.

Silicon Valley is on the verge of a brain drain of mythical proportions.

If America allows all these brilliant minds to fly home not only to China but everywhere else, America is just training these workers to compete against American workers.

A premier example is Baidu co-founder Robin Li who received his master's degree in computer science from the State University of New York at Buffalo in 1994.

After graduation, his first job was at Dow Jones & Company, a subsidiary of News Corp., writing code for the online version of the Wall Street Journal.

During this stint, he developed an algorithm for ranking search results that he patented, flew back to China, created the Google search engine equivalent, and named it Baidu (BIDU).

Robin Li is now one of the richest people in China with a fortune of close to $20 billion.

To show it's not just a one-hit-wonder type scenario, three of the top five start-ups are currently headquartered in Beijing and not in California.

The most powerful industry in America's economy is just a transient training hub for foreign nationals before they go home to make the real moola.

More than 70% of tech employees in Silicon Valley and more than 50% in the San Francisco Bay Area are foreign, according to the 2016 census data.

Adding insult to injury, the exorbitant cost of housing is preventing burgeoning American talent from migrating from rural towns across America and moving to the Bay Area.

They make it as far West as Salt Lake City, Reno, or Las Vegas.

Instead of living a homeless life in Golden Gate Park, they decide to set up shop in a second-tier American city after horror stories of Bay Area housing starts to populate their friends' Instagram feeds and are shared a million times over.

This trend was reinforced by domestic migration statistics.

Between 2007 and 2016, 5 million people moved to California, and 6 million people moved out of the state.

The biggest takeaways are that many of these new California migrants are from New York, possess graduate degrees, and command an annual salary of more than $110,000.

Conversely, Nevada, Arizona, and Texas have major inflows of migrants that mostly earn less than $50,000 per year and are less educated.

That will change in the near future.

Ultimately, if VCs think it is expensive now to operate a start-up in Silicon Valley, it will be costlier in the future.

Pouring gasoline on the flames, Northern California schools are starting to fold like a house of cards due to minimal household formation wiping out student numbers.

The dire shortage of affordable housing is the region's No. 1 problem.

A 1,066-sq.-ft. property in San Jose's Willow Glen neighborhood went on sale for $800,000.

This would be considered an absolute steal at this price but the catch is the house was badly burned two years ago. This is the price for a teardown.

When you combine the housing crisis with the price readjustment for big data, it looks as if Silicon Valley has peaked or at the very least, it's not cheap.

Yes, the FANGs will continue their gravy train but the next big thing to hit tech will not originate from California.

VCs will overwhelmingly invest in data over rental bills. The percolation of tech ingenuity will likely pop up in either Nevada, Arizona, Texas, Utah, or yes, even Michigan.

Even though these states attract poorer migrants, the lower cost of housing is beginning to attract tech professionals who can afford more than a burned down shack.

Washington state has become a hotbed for bitcoin activity. Small rural counties set in the Columbia Basin such as Chelan, Douglas, and Grant used to be farmland.

The bitcoin industry moved three hours east of Seattle for one reason and one reason only - cost.

Electricity is five times cheaper there because of fluid access to plentiful hydro-electric power.

Many business decisions come down to cost, and a fractional advantage of pennies.

Globalization has supercharged competition, and technology is the lubricant fueling competition to new heights.

Once millennials desire to form families, the only choices are regions where housing costs are affordable and areas that aren't bereft of tech talent.

Cities such as Las Vegas and Reno in Nevada; Austin, Texas; Phoenix, Arizona; and Salt Lake City, Utah, will turn into hotbeds of West Coast growth engines just as Hangzhou, China-based Alibaba (BABA) turned that city into more than a sleepy backwater town with a big lake at its center.

The overarching theme of decentralizing is taking the world by storm. The built-up power levers in Northern California are overheated, and the decentralization process will take many years to flow into the direction of these smaller but growing cities.

Salt Lake City, known as Silicon Slopes, has been a tech magnet of late with big players such as Adobe (ADBE), Twitter (TWTR), and EA Sports (EA) opening new branches there while Reno has become a massive hotspot for data server farms. Nearby Sparks hosts Tesla's Gigafactory 1 along with massive data centers for Apple, Alphabet, and Switch.

The half a billion-dollars required to build a proper tech company will stretch further in Austin or Las Vegas, and most of the funds will be reserved for tech talent - not slum landlords.

The nail in the coffin will be the millions saved in state taxes.

The rise of the second-tier cities is the key to staying ahead of the race for tech supremacy.

Mad Hedge Technology Letter

December 24, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape or form.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose from 10% to 13% and is catching up to Amazon Web Services (AWS).

Amazon leads the cloud industry it created and the 49% growth in cloud sales from 42% in Q3 2017 is a welcome sign that Amazon is not tripping up.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes 73% to Amazon's total operating income.

Total revenue for just the AWS division is an annual $5.5 billion business and would operate as a healthy stand-alone tech company if need be.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day. If you work in Silicon Valley you can triple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them telecommute. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees. According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

Mad Hedge Technology Letter

December 18, 2018

Fiat Lux

Featured Trade:

(THE BIG TECHNOLOGY TRENDS OF 2019)

(MSFT), (AMZN), (BBY), (SONO), (ROKU), (ADBE), (AAPL), (BAC)

As an astute purveyor of technology, it is my job to share with you the upcoming tech trends of 2019.

Some might be easily discernable and some might be a headscratcher, but all must be tabbed up and considered in the current tech outlook that is unpredictable and fluctuating, to say the least.

Part of the moody tech sentiment has been influenced by a changeable macro landscape - the tech sector’s winter freeze was woefully volatile and unfairly capsized good companies with the bad.

There is no means to get around it – the administration's delicate situation as it relates to Beijing and the American tech sector is front and center, and any movement of tech stocks must carefully absorb the ongoings from this complicated relationship.

The number of obstacles that confront this sensitive situation means that the 90-day window granted to solve the trade quagmires appear too brief of a timeframe to really knock out every single disagreement on the table.

The uncertainty over trade policy has really ruffled some of tech’s strongest feathers such as America’s pride and joy Apple (AAPL).

Apple is a great long-term story, but it does not preside over many short-term positive catalysts that can resuscitate the stock.

Analysts' downgrade after downgrade has been most harrowing for the chip components that make up Apple and other consumer electronic devices such as televisions and tablets.

This scenario is expected to extend into 2019 with Bank of America Merrill Lynch (BAC) slashing their price target by nearly 30% on electronics retailer Best Buy (BBY) then sticking the fork in them by downgrading it to underperform.

The premise behind this downgrade was that Best Buy carved out 25% of revenue from television sales and even though Adobe (ADBE) analytics has calculated record online sales in the holiday season, the follow-through has largely been without television sales participating in the seasonal bonanza.

Piggybacking on this trope, I believe electronic device sales could be hard-pressed to eke out growth next year and are set up for a rude awakening.

Therefore, it is sensible to extrapolate this idea out and assume that smart hardware competing against the big boys such as smart speaker firm Sonos (SONO), who I urged readers to stay away at $16 in September, is set up for a painstaking 2019.

To reread the story, please click here.

The stock is now trading at $11 and a mix of weakening consumer device demand layered with the domination that is the Amazon Alexa has pushed up this company’s risk-reward levels to untold heights.

Rounding out the negatives is that content streaming platform Roku has also debuted its own version of a smart speaker.

Roku (ROKU) is one of my favorite long-time tech plays but has been dragged down by the broader trade war because a portion of its revenue is still captured by hardware such as the new speakers and Roku OTT boxes.

Differing from Apple, Roku earns most of their revenue from targeted ads on their proprietary platform, and this is its reason why most investors are in this stock that is set to capture a secular migratory wave of cord-cutters traversing to online streaming.

However, Roku TVs made by Chinese company TCL still draw in small portion of revenue and even though the China revenue is not as high on a relative basis as Apple’s 20%, the stock has floundered in the short-term.

If disruptors such as Roku can get hit savagely with a small portion of revenues from China, then I am convinced that any tech investor going into 2019 should stay away from hardware and hardware that is made in China.

The consensus is that the drawn-out trade war could become the X-factor in the 2020 election because the Chinese are willing to wait for the next guy on the carousel searching for a better deal.

If you thought Chinese supply chains had a tough time of it in 2018, then 2019 is poised to be even more treacherous.

What 2018 convincingly demonstrated was that the late economic price action is getting into later and later stages boding negative for tech stocks.

To construct a healthy tech portfolio going into 2019, the change in the tech partiality has made the pivot towards software much more important.

Investors need to mitigate Chinese supply chain risk and seek out domestic software plays.

That should be the playbook as tech investors are on pins and needles going into the new year.

The domestic economy is robust and tech investors should be attracted to top-quality cloud-based enterprise stocks that are profitable.

The FANG story collapsing in our face signaled to investors that it is time to cautiously consider whether to invest heavily into deep loss-maker tech growth stories.

A healthy rotation to premium quality tech with superior cash flow is one way to lock up stocks and slyly deflect the external factors shaking up the tech momentum.

PayPal (PYPL) is a stock that has large international exposure mainly in Europe, but none in China whose 3-year EPS growth rate is 26% and still driving sequential sales in the mid-20% range.

This is just one example of a stock that has the correct make-up in a harsh and brutal tech environment planted with invisible booby traps.

And the most tell-tale sign that the American economy is in for an all-out software frenzy is the number of head-spinning investments from big tech companies looking to expand their footprint into new talent spots around the country.

First, the farcical Amazon beauty pageant came to an end with the e-commerce giant announcing a three-part package deploying new operations in New York, Washington D.C., and Nashville as the next phase of digital growth ramps up.

Google (GOOGL) followed that up by plopping a software office in New York City devouring a huge chunk of the Chelsea neighborhood aimed at doubling the 7,000 employees already there.

Then it was Apple’s turn choreographing a significant investment in Austin, Texas that will cost them $1 billion along with juicing up operations in Seattle, San Diego, and Los Angeles.

They weren’t finished there and promised to double down its presence in Pittsburgh, New York and Boulder, Colorado over the next three years.

It’s clear that big tech has finally understood that it’s not invincible and milking the China supply chain for all its worth is now a taboo business practice that has bipartisan support firmly against it.

Like I said before, the trade war came 1-2 years too early for Apple, and these headline-grabbing talent investments in data centers and its staff underscore the sense of urgency to fully and comprehensively pivot towards a software and services company.

The transition has certainly been an excruciating process exposing the weak spots at a brilliant company at the worst possible time.

I blame CEO of Apple Tim Cook who is the operations expert in the building grappling with Apple overextending themselves in the Middle Kingdom that has come back to haunt him at night.

You would have thought that with the troves of big data on their hands, Apple’s consultants might have found a country allied with America to invest in such a massive supply chain.

This leads me to communicate with conviction that Microsoft (MSFT) is my favorite tech stock going into 2019 because it is the purest, scalable, high-quality software name with minimal hardware drag devoid of weak spots in its armor.

That was what the investment in GitHub for $7.5 billion was about, highlighting the value of owning the meeting place for coders, literally buying up a stash of over 28 million users and 57 million coding repositories in which 28 million are public.

Microsoft has also bought up six video game studios in 2018 attempting to capture a bigger piece of the pie for the video game market that has been throttled by Fortnite.

If the Microsoft baby gets thrown out with the bathwater, then the tech bear market is upon us in full force.

If you didn’t really believe content is king in 2018, then you will really feel the phenomenon further embedded into the economy and society in 2019.

Next year, almost all tech investments will result in more data centers and software engineers in the hope of pumping out the best content and data, whether it’s enterprise software, video games, or pure data storage.

In 2019, I am bullish on companies with a cloud-based bedrock able to grind out the best content in the world, backed by a strong balance sheet that dovetails nicely with a lack of China-based revenue exposure.

The uber-growth models could be taking a rest boding negatively for Uber, Lyft, and Airbnb who must convince a more skeptical tech audience with tighter purse strings as they inject yet another unique dimension into the tech world next year.

Global Market Comments

December 17, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THERE’S NO SANTA CLAUS IN CHINA)

($INDU), (SPY), (TLT), (AAPL), (AMZN), (NVDA), (PYPL), (NFLX)

On Friday, five serious hedge fund managers separately called me out of the blue and all had the same thing to say. They had never seen the market so negative before in the wake of the worst quarter in seven years. Therefore, it had to be a “BUY”.

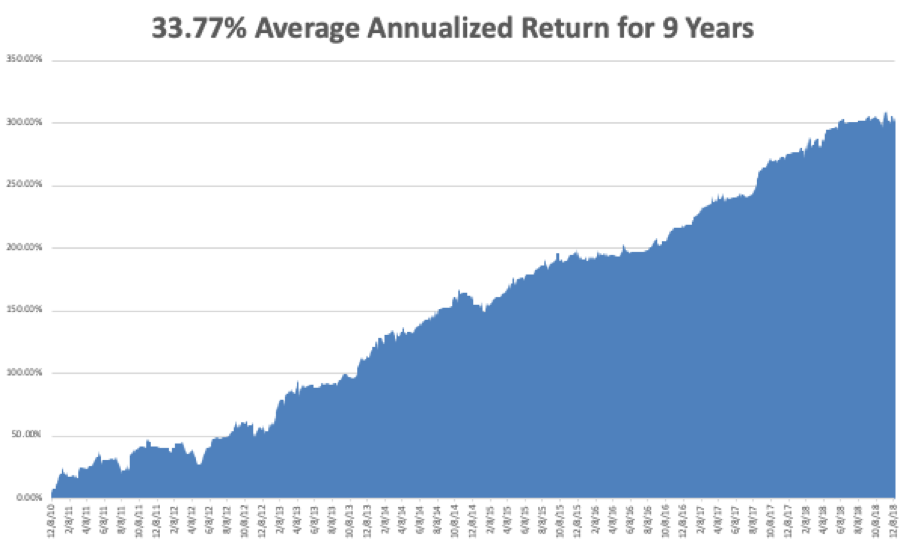

I, on the other hand, am a little more cautious. I have four 10% positions left that expire on Friday, in four trading days, and on that day I am going 100% into cash. At that point, I will be up 3.5% for the month of December, up 31.34% on the year, and will have generated positive return for one of the worst quarters in market history.

I’m therefore going to call it a win and head for the High Sierras for a well-earned Christmas vacation. After that, I am going to wait for the market to tell me what to do. If it collapses, I’ll buy it. If it rockets, I’ll sell short. And I’ll tell you why.

These are not the trading conditions you would expect when the economy is humming along at a 2.8% annual rate, unemployment is running at a half-century low, and earnings are growing a 26% year on year. You can’t find a parking spot in a shopping mall anywhere.

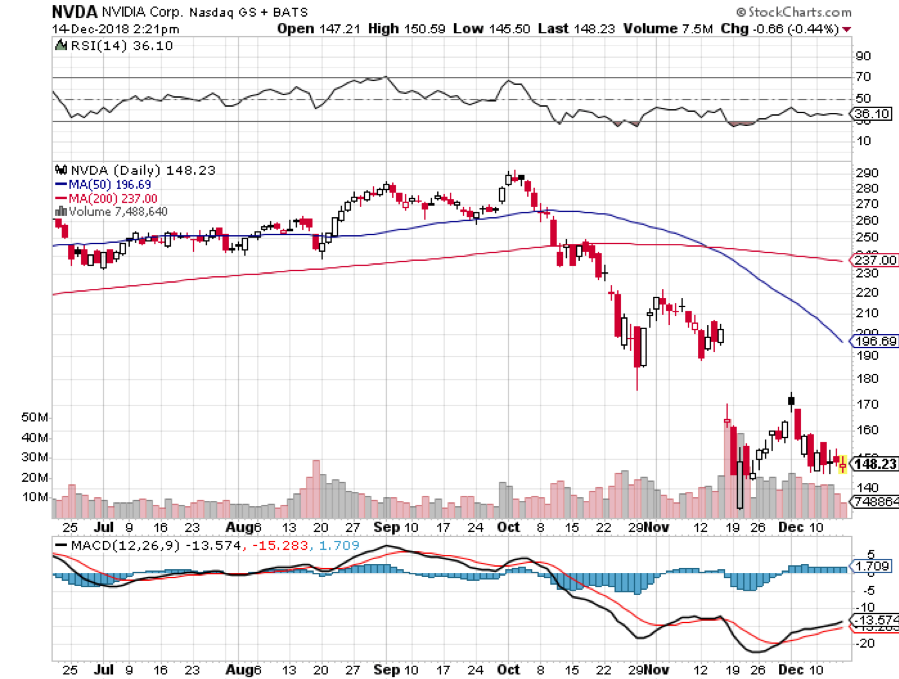

However, the lead stocks like Apple (AAPL), Amazon (AMZN), and Netflix (NFLX) have plunged by 30%-60%. Price earnings multiples dropped by a stunning 27.5% from 20X to 14.5X in a mere ten weeks. Half of the S&P 500 (SPY) is in a bear market, although the index itself isn’t there yet. I would rather be buying markets on their way up than to try and catch a falling knife.

There is only one catalyst for that apparent yawning contradiction: The President of the United States.

Trump has created a global trade war solely on his own authority. Only he can end it. As a result, asset classes of every description are beset with uncertainty, confusion, and doubt about the future. Analysts are shaving 2019 growth forecasts as fast as they can, businesses are postponing capital spending plans, and investors are running for the sidelines in droves. Business confidence is falling like a rock

To paraphrase a saying they used to teach you in Marine Corps flight school, “It’s better to be in cash wishing you were fully invested than to be fully invested wishing you were in cash.”

The Chinese have absolutely no interest in caving into Trump’s wishes. They read the New York Times, see the midterm election result and the opinion polls, and are willing to bet that they can get a much better deal from a future president in two years.

I have been dealing personally with both Trump and the Chinese government for four decades. The Middle Kingdom measures history in Millenia. The president lives from tweet to tweet. The Chinese government can take pain by simply ordering its people to take it. We have elections every two years with immediate consequences.

The best we can hope for is that the president folds, declares victory, and then retreats from his personal war. This can happen at any time, or it may not happen at all. No one has an advantage in predicting what will happen with any certainty. Not even the president knows what he is going to do from minute to minute.

It is the possibility of trade peace at any time that has kept me out of the short side of the stock market in this severe downturn. That robs a real hedge fund manager of half his potential income. Trade peace could be worth an instant rally of 10% in the stock market. Even a lesser move, like the firing of trade advisor Peter Navarro, would accomplish the same.

The market was long overdue for a correction like the one we have just had. Investors were getting overconfident, cocky, and excessively leveraged. In October, we really needed the tide to go out to see who was swimming without a swimsuit. But if the tide goes out too far, we will all appear naked.

Thanks to some very artful trading, my year to date return recovered to +27.54% boosting my trailing one-year return back up to 27.54%. I covered an aggressive short position in the bond market (TLT) for a welcome 14.4% profit. I also took profits with an instant winner in PayPal (PYPL). On the debit side, I stopped out of an Apple call spread for a minimal loss.

December is showing a very modest loss at -0.26%. The market has become virtually untradeable now, with tweets and China rumors roiling markets for 500 points at a pop. And this is against a Dow Average that is down a miserable -2.8% so far in 2018. I should have listened to my mother when she wanted me to become a doctor.

My nine-year return nudged up to +304.01. The average annualized return revived to +33.77.

The upcoming week is all about housing data, with the big focus on the Fed’s interest rate hike on Wednesday.

Monday, December 17 at 10:00 AM EST, the November Homebuilders Index is out.

On Tuesday, December 18 at 8:30 AM, November Housing Starts are published.

On Wednesday, December 19 at 10:00 AM EST, November Existing Home Sales are released.

At 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

At 2:00 PM the Federal Reserve Open Market Committee announces a 25 basis point rise in interest rates, taking the overnight rate to 2.25% to 2.50%. An important press conference with governor Jay Powell follows.

Thursday, December 20 at 8:30 AM EST, we get Weekly Jobless Claims.

On Friday, December 21, at 8:30 AM EST, we learn the latest revision to Q3 GDP which now stands at 2.8%.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be battling snow storms driving up to Lake Tahoe where I’ll be camping out for the next two weeks. Mistletoe, eggnog, and endless games of Monopoly and Scrabble await me.

Good luck and good trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

December 14, 2018

Fiat Lux

Featured Trade:

(DECEMBER 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (MU), (PYPL), (SPOT), (FXE), (FXY), (XLF), (MSFT), (AMZN), (TSLA), (XOM),

(SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS)