Global Market Comments

August 30, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE HIGHER WE GO THE CHEAPER WE GET),

(JPM), (BAC), (C), (GS), (MS), (BLK), (FCX), (X),

(WYNN), (MGM), (ALK), (LUV), (HAL), (SLB), (TLT)

Global Market Comments

August 30, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE HIGHER WE GO THE CHEAPER WE GET),

(JPM), (BAC), (C), (GS), (MS), (BLK), (FCX), (X),

(WYNN), (MGM), (ALK), (LUV), (HAL), (SLB), (TLT)

I am sitting here holed up in my office in San Francisco.

Lake Tahoe is being evacuated as the Caldor fire is only ten miles away and the winds are blowing towards it. The visibility there is no more than 500 yards. The ski resorts are pointing their snow cannons towards their buildings to ward off flames.

Conditions are not much better here in Fog City. We are under a “stay at home” order due to intense smoke and heat. Even here, the fire engines are patrolling by once an hour.

The Boy Scout trip got cancelled this weekend, so the girls are having a cooking competition, chocolate chip waffles versus a German chocolate cake.

To make matters worse, I have been typing with only one finger all week, thanks to the elbow surgery I had on Tuesday. Next time, I’ll think twice before taking down a 300-pound steer. When I told the doctor how I incurred this injury, he laughed. “At your age?”

Which leaves me to contemplate this squirrelly stock market of ours. I have always been a numbers guy. But the higher the indexes rise, the cheaper stocks get. That’s not supposed to happen, but that is the fact.

We started out 2021 with an S&P 500 price earnings multiple of 25X. Now, we are down to a lowly 21X and the (SPY) is 20% higher, rising from $360 to $450.25.

The analyst community, ever the lagging indicator that they are, had S&P forward earnings for 2022 all the way down to $175. They have been steadily climbing ever since and are now touching $200 a share.

This is what 20/20 hindsight gets you. That and $5 will get you a cup of coffee at Starbucks. It takes a madman like me to go out on a limb with high numbers and then be right.

So what follows an ever-cheaper market? A more expensive one. That means stocks will continue to my set-in-stone target of $475 for the (SPY) for yearend, and (SPY) earnings of over $200 per share.

It gets better.

(SPY) earnings should hit $300 a share by 2025 and $1,400 a share by 2030. That makes possible my (SPY) target of $1,800 and my Dow Average target of 240,000 in a decade.

What are markets getting right that analysts and bears are getting wrong?

The future has arrived.

The pandemic brought forward business models and profitability by a decade. Technology is hyper-accelerating on all fronts.

Cycles are temporary but adoption is permanent. We are never going back to the old pre-pandemic economy. As a result, stocks are now worth a lot more than they were only two years ago.

So what do we buy now? There is a second reopening trade at hand, the post-delta kind. That means buying banks (JPM), (BAC), (C), brokers (GS), (MS), money managers (BLK), commodities (FCX), (X), hotels (WYNN), (MGM), airlines (ALK), (LUV), and energy (HAL), (SLB).

And what do we avoid like the plague? Bonds (TLT), which offer only confiscatory yields in the face of rising inflation with gigantic negative interest rates.

As for technology stocks, they will go sideways to up small in the aftermath of their ballistic moves of the past three months.

You all know that I am a history buff and there are particular periods of history that are starting to disturb me.

In August, we saw ten new intraday highs for the S&P 500 (SPY). That has not happened since 1987. Remember what happened in 1987?

We have not seen 11 new highs in August since 1929. The only negative three months seen since 1929 are August, September, and October. Remember what happened in 1929?

If that doesn’t scare the living daylights out of you, then nothing will. So, it seems we are in for some kind of correction, even if it’s just the 5% kind.

As for me, I’m looking forward to 2030.

The “Everything” Rally is on, according to my friend, Strategas founder Tom Lee. You can see it in the recent strength of epicenter stocks like energy, hotels, airlines, and casinos. It could run into 2022.

The Taper is this year and interest rate rises are later, said Jay Powell at Jackson Hole last week. Markets will be jumpy, especially bonds. Fed governor Jay Powell’s every word was parsed for meaning. Dove all the way. The larger focus will be on the August Nonfarm Payroll report out this week.

Pfizer Covid vaccination gets full FDA approval, requiring millions more to get shots and bringing forward the end of the pandemic. All 5 million government employees will now get vaccinated, including the entire military. It’s the fastest drug approval in history. Some 37,000 new cases in one day. The stock market likes it. Take profits on (PFE)

Bitcoin tops $50,000 after breaking several key technical levels to the upside. Next stop is a double top at $66,000. It helps that Coinbase is buying $500 million worth of crypto for its own portfolio. Buy (COIN) on dips.

The US Dollar will crash in coming years, says Jeffry Gundlach and I think he is right. Emerging markets will become the next big play but not quite yet. Gold (GLD) will be a great hideout once it comes out of hibernation. China will soon return to outperforming the US. The dollars reserve currency status is at risk.

The lumber crash is saving $40,000 per home, says Toll Brothers (TOL) CEO, Doug Yearly. Last year, lumber prices surged from $300 per board foot to an insane $1,700, thanks to a Trump trade war with Canada and soaring demand. It all flows straight through the bottom line of the homebuilders which should rally from here. Buy (TOL) on dips.

China’s crackdown creates investment opportunities, says emerging investing legend Mark Mobius. He sees corporate governance improving over the long term. The gems are to be found among smaller companies not affected by Beijing’s hard-line. Mobius loves India too.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a healthy +7.62% gain in August. My 2021 year-to-date performance appreciated to 76.83%. The Dow Average was up 15.87% so far in 2021.

That leaves me 80% in cash at 20% in short (TLT) and long (SPY). I’m keeping positions small as long as we are at extreme overbought conditions.

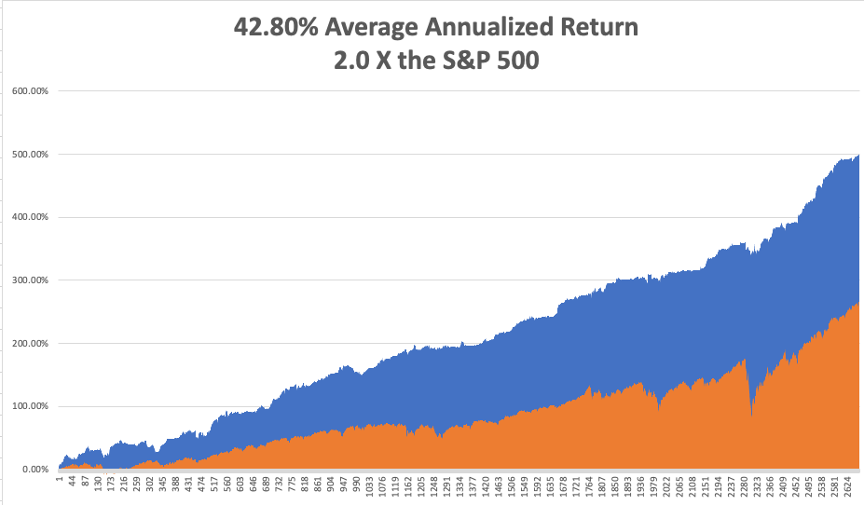

That brings my 12-year total return to 499.38%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.80%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 116.67%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 39 million and rising quickly and deaths topping 638,000, which you can find here.

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 30 at 11:00 AM, Pending Home Sales are published. Zoom (ZM) reports.

On Tuesday, August 31, at 10:00 AM, S&P Case Shiller National Home Price Index for June is released. CrowdStrike (CRWD) reports.

On Wednesday, September 1 at 10:45 AM, the ADP Private Employment report is disclosed.

On Thursday, September 2 at 8:30 AM, Weekly Jobless Claims are announced. DocuSign (DOCU) reports.

On Friday, September 3 at 8:30 AM, the all-important August Nonfarm Payroll report is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

Oh and the German chocolate cake won, but please don’t tell anyone.

As for me, given the losses in Afghanistan this week, I am reminded of my several attempts to get into this troubled country.

During the 1970s, Afghanistan was the place to go for hippies, adventurers, and world travelers, so of course, I made a beeline for straight for it.

It was the poorest country in the world, their only exports being heroin and the blue semiprecious stone lapis lazuli, and illegal export of lapis carried a death penalty.

Towns like Herat and Kandahar had colonies of westerners who spent their days high on hash and living life in the 14th century. The one cultural goal was to visit the giant 6th century stone Buddhas of Bamiyan 80 miles northwest of Kabul.

I made it as far as New Delhi in 1976 and was booked on the bus for Islamabad and Kabul ($25 one-way). Before I could leave, I was hit with amoebic dysentery.

Instead of Afghanistan, I flew to Sydney, Australia where I had friends and knew Medicare would take care of me for free. I spent two months in the Royal North Shore Hospital where I dropped 50 pounds, ending up at 125 pounds.

I tried to go to Afghanistan again in 2010 when I had a large number of followers of the Mad Hedge Fund Trader stationed there, thanks to the generous military high-speed broadband. The CIA waved me off, saying I wouldn’t last a day as I was such an obvious target.

So, alas, given the recent regime change, it looks like I’ll never make it to Afghanistan. I won’t live long enough to make it to the next regime change. It’s just one more concession I’ll have to make to my age. I’ll just have to content myself reading A One Thousand and One Nights at home instead. The Taliban blew up the stone Buddhas of Bamiyan in 2001.

In the meantime, I am on call for grief counseling for the Marine Corps for widows and survivors. Business has been thankfully slow for the last several years. But I’ll be staying close to the phone this weekend just in case.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

India in 1976

Mad Hedge Technology Letter

July 19, 2021

Fiat Lux

Featured Trade:

(THE LARGEST SHADOW BANKER AND U.S. TECH)

(BLK), (AMZN), (MSFT), (AAPL)

In the top-heavy global media landscape, there seems to be this notion that the U.S. and its capital is the primary alpha male swaying asset prices.

The close to $6 trillion in recent stimulus chasing too few services demonstrably has an outsized vote on the matter of asset pricing.

But the dirty little secret about this stimulus is that U.S. private equity is spilling into Nordic and Western European markets effectively forcing a rapid Americanization of asset prices across the Atlantic.

Shadow banks finance financial transactions that are too risky for banks.

In the US, they already grant half of all loans.

In times of low or even negative interest rates for credit, fewer and fewer investors bring their money to a normal bank, but rather to a so-called shadow bank.

This is a term that has become established to describe a phenomenon for financial participants who are not a bank.

What a shadow bank is is not exactly defined, because there are no shadow banking licenses; but tech companies and the U.S. wielding of this critical function have changed the financial world.

In some cases, a few large private families who now have the means to invest in such funds are also focused on funding through these shadow banks and most of the time to buy American tech stocks.

And they deliberately invest not just in a single fund, but across all countries in the world, and shadow banks make up around a third of the financial sector.

In Germany, it is more than a third and on the EU average, it is almost exactly a third.

Pension funds and pension funds work like small insurance companies: employees of a company pay part of their gross wages directly, free of tax and social security contributions. At the end of their working life, they will then be paid a supplementary pension from the income generated.

The fact that “their” money is mandated to be invested in the global financial markets - at least if people hope to receive a pension after their active working life.

These European pension funds are also turning to U.S. branded shadow banking.

According to the Financial Stability Board, shadow banks had a total of $80 trillion in business in 2021.

Compared to the previous year, this was an increase of 8.5%. The FSB information is based on data from 29 countries. These in turn represent 80% of global economic output.

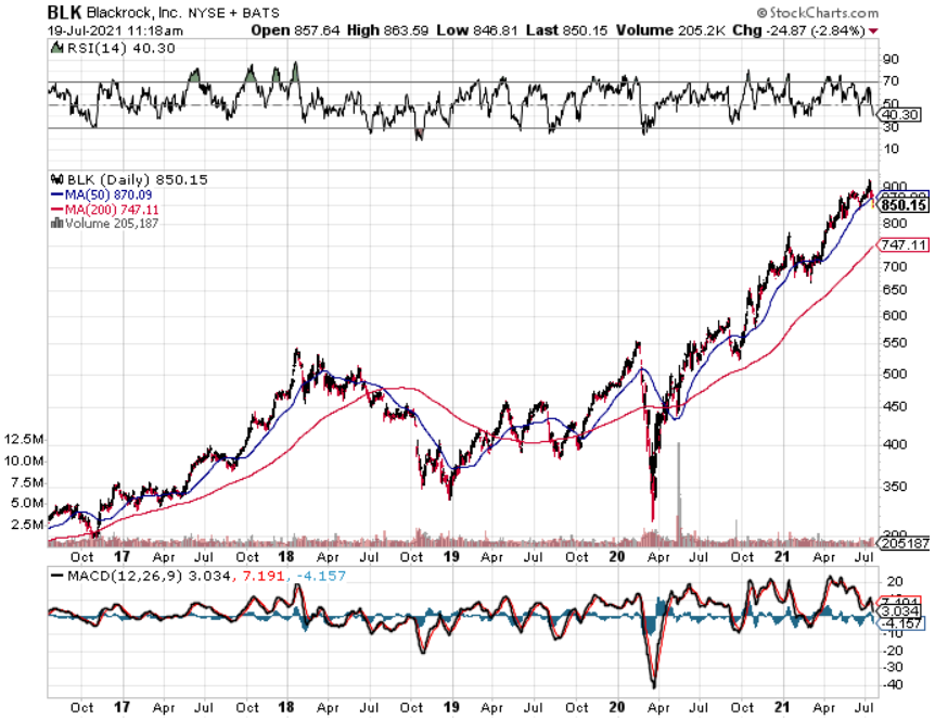

Many deals and transactions are outsourced from the banks now. That means: The financial business tries to circumvent the regulations and the largest shadow bank is BlackRock (BLK) - involved in 20,000 companies.

Many of these outsourced financial service providers are also nothing more than subsidiaries of BlackRock.

This outsourcing offers their customers the prospect of significantly higher interest rates.

BlackRock is an influential major shareholder in all listed global corporations from Europe and the USA.

Although it was founded in 1988, BlackRock was unknown to most people in Germany for decades.

That only changed in 2018, when the politician and lobbyist Friedrich Merz announced his candidacy for the CDU party chairmanship.

At this point in time, Friedrich Merz had been head of the supervisory board of the German offshoot of BlackRock for two years.

This is a company that currently manages a fortune of over nine trillion dollars which is far more than what is produced in Germany, every year, in terms of goods and services - considerably more.

At BlackRock, they harness the smorgasbord of mechanisms that define this new area of shadow banking: hedge funds, VC, real estate, index funds, and money market funds.

BlackRock holds considerable blocks of shares through various subsidiaries, including in normal commercial banks - such as Bank of America, Citigroup, and Deutsche Bank.

But that’s not all.

BlackRock is by far the largest owner in the German share index - with a share of 15 to 17%.

That means: every sixth share of the 30 largest German corporations is controlled by one of the BlackRock funds.

That BlackRock's ownership structure rotates in circles. The asset management companies control themselves, or are actually not subject to any control.

It’s an almost incestuous system where you pursue your own interests through a network of participation. While banks are systemically relevant, BlackRock is still uncontrolled, and they refuse to classify this company as systemically relevant.

But that is BlackRock and that is part of what made them highly successful.

It is extremely well connected. It has long-standing, important politicians in its ranks. Friedrich Merz is just one example in the big picture.

French President Emmanuel Macron recently said he wanted to see the creation of at least 10 tech companies in Europe worth over 100 billion euros each by 2030.

While Europe is now home to many unicorns — start-ups valued at over $1 billion — it is yet to produce a company with the scale of American and Chinese tech giants.

But I am ready to argue that Europeans no longer have control over their own narrative in their own financial system, it is now U.S. private equity.

Assuming that this holds true, even if President Macron’s wish bears fruit, the owners of these “European” tech companies will of course be Americans who are dressed up as European pension funds and maybe even perhaps somehow a company starting with a B and ending with ROCK?

The oversupply of capital from the U.S. that has overcharged U.S. tech shares will get any piece of the action that Europe creates if they are to create a tech renaissance, which I highly doubt.

And the real truth is that any unicorn created in Europe will most likely go public in New York anyway.

The pandemic has also supercharged the influence of Blackrock in Germany and Europe as a whole and that cannot be diminished.

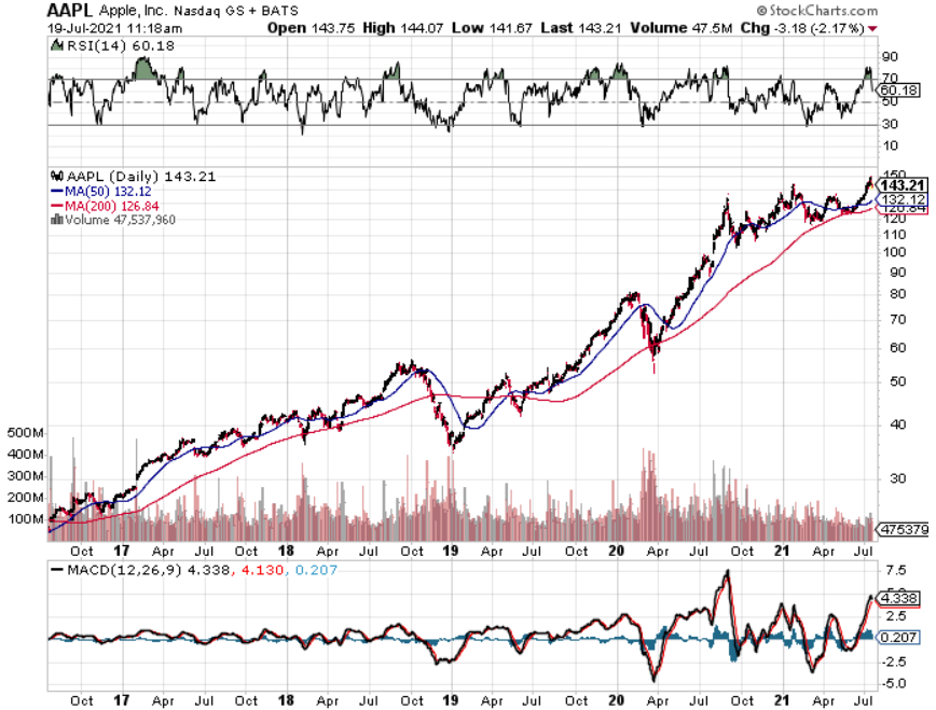

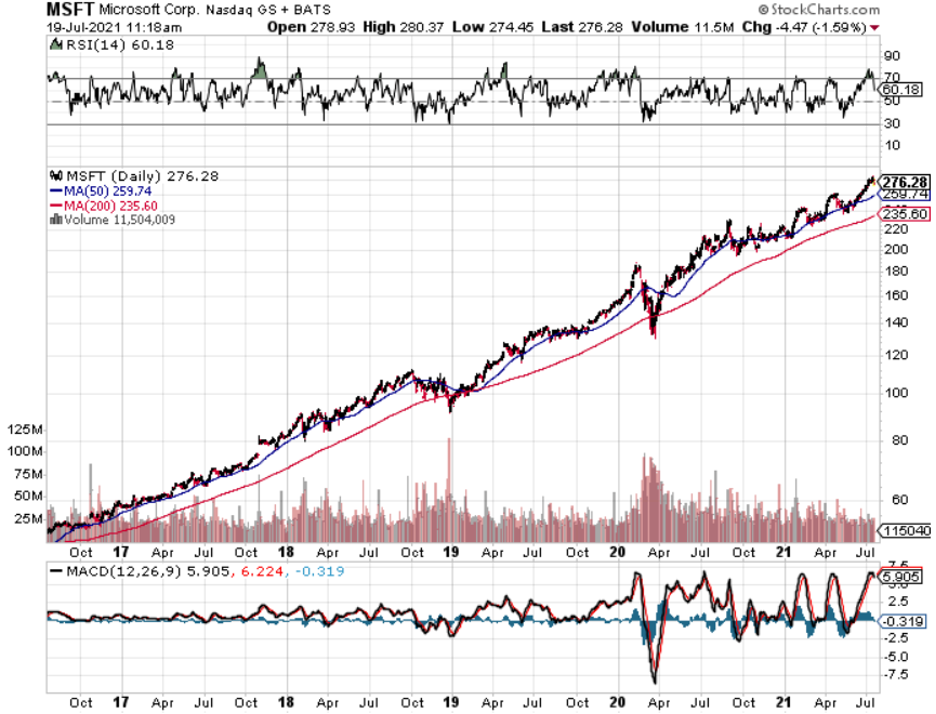

According to Blackrock’s 13F, 10% of their portfolio is Apple (AAPL), Microsoft (MSFT), and Amazon (AMZN) - holding $128 billion in AAPL, $123 billion in MSFT, and only $87 billion in AMZN.

Their largest 7 holdings are in U.S. tech stocks.

This is just a 13F in their main fund, and it wouldn’t be shocking to find out some of their European subsidiaries are also doing the same thing even if not with the same amount of capital.

The European financial system has effectively been gamed by Blackrock and its copycats, so next time you hear of a large Nordic or German equity fund making a big splash in U.S. tech shares, the eventual originator of that decision could be Blackrock.

This is the type of sophistication we are dealing with at this point in global markets and essentially nothing beats the eye test anymore because we have no idea what is happening unless we follow the trail of money.

Mad Hedge Biotech & Healthcare Letter

April 6, 2021

Fiat Lux

FEATURED TRADE:

(HIGH-YIELD STOCK UP FOR GRABS)

(ABBV), (PFE), (BRK.B), (BLK)

Something curious is happening at the FDA, and it’s causing investors to be jittery. Drugs that are sure to gain approval keep encountering roadblocks.

What began as a handful of biotechnology stocks getting trampled is turning out to be a broader pullback caused by fears of a tougher and stricter regulatory environment for drug developers.

Following these changes, the SPDR S&P Biotech (XBI) slid by roughly 12% this month.

The idea that the somewhat predictable regulatory results in the past four or five years may no longer be as predictable obviously ramped up the perceived riskiness of this industry.

One bellwether of this change is AbbVie (ABBV), which submitted an application for the expanded use of rheumatoid arthritis Rinvoq in March. It recently announced that the regulatory board is extending the evaluation for three months.

While this isn’t a cause for alarm, it’s enough to unsettle some investors since Rinvoq is expected to replace AbbVie’s blockbuster drug Humira when the latter loses its patent exclusivity in 2023.

However, the reason behind FDA’s extension is likely because of the safety concerns found in a similar drug, Xeljanz, by Pfizer (PFE).

Considering the similarities of the two, it makes sense for the regulatory board to exercise more caution on AbbVie’s product.

The rise and fall of AbbVie has always centered on Humira, with this top-selling drug raking in $19.8 billion in sales in 2020 alone. That’s actually lower than its usual revenue a few years back.

Humira’s loss of exclusivity is projected to result in medium-term headwind to the company as more and more biosimilars pressure revenue.

However, AbbVie has been working on offsetting the estimated losses by expanding its other programs.

For instance, the revenue for AbbVie’s non-Humira immunology sector, led by Skyrizi and Rinvoq, is projected to double to reach $4.6 billion in 2021.

By 2025, AbbVie expects Rinvoq and Skyrizi sales to reach $15 billion annually.

Meanwhile, a considerable uptick is anticipated from its neuroscience division’s revenue, led by Vraylar, to generate $5.7 billion in 2021.

As for its hematologic oncology franchise, spearheaded by Imbruvica and Venclexta, this sector’s revenue is expected to increase in double digits to reach $7.5 billion this year as well.

On top of these, AbbVie has been busy looking for suitable acquisitions to diversify its revenue stream.

A notable deal it made was in 2015 with Pharmacyclics. This acquisition actually added the mega-blockbuster drug Imbruvica to AbbVie’s portfolio.

In May 2020, AbbVie completed its deal to purchase Allergan. This $63 billion merger is expected to boost the global distribution capacity of AbbVie and bolster its therapeutic sales channels.

By 2023, sales of the products acquired from Allergan’s pipeline are estimated to add at least $2 billion to AbbVie’s annual revenue.

All in all, these sectors are all well-positioned to substantially offset the fall of Humira’s revenue thanks to the rapid growth and aggressive indication expansion efforts of the company.

Nonetheless, the anxiety of the delayed FDA approval for Rinvoq’s expanded use is understandable.

After all, AbbVie expects this particular drug to contribute to doubling the 2021 sales of the franchise from $2.3 billion to $4.6 billion.

Moreover, this is a cornerstone in the company’s post-Humira era in less than two years.

However, the three-month delay will have a minimal impact on the 2021 revenues of the company and a negligible effect when we consider the long term.

Realistically, this would cost AbbVie roughly less than $1 billion in sales, which amounts to less than 2% of the total projected revenues of the company this year.

During times like these, it’s crucial to remember that the pharmaceutical industry is an extremely bumpy road.

There’s no such thing as a linear progression in this line of business, which is why it’s vital to choose companies with established track records and highly capable management teams.

If it helps ease any anxiety, then it might be useful to think that AbbVie is a favored stock by Warren Buffett’s Berkshire Hathaway (BRK.B).

The Oracle of Omaha currently holds 4.27 million shares of this company. Meanwhile, BlackRock (BLK) holds 2.41 million shares, while Ken Griffin’s Citadel Advisors has 786,000 shares.

AbbVie is a mature, larger-cap biopharmaceutical stock that’s selling at an affordable price these days.

Despite the revenue declines and plunges in earnings of countless businesses in 2020, AbbVie still managed to deliver strong operating and financial results—and the company still has a long way to go.

AbbVie is expected to deliver at least 4.8% in annual earnings growth over the course of the next five years—a highly conservative estimate considering that the company reported 21.9% growth in the past five years.

Moreover, AbbVie is safely positioned to deliver 6% long-term annual dividend growth.

AbbVie was able to generate 3.3% growth in its operational revenue in 2020, recording $45.804 billion in net revenues.

In the past weeks, I’ve seen AbbVie shares go down by roughly 6%. However, I think the fear here is exaggerated and the market might be overreacting to the uncertainty caused by stricter FDA guidelines.

Instead of letting the anxiety take control, I believe it’s best to heed the advice of Warren Buffett in this situation: “The market is a device for transferring money from the impatient to the patient.”

Therefore, I think patient investors should take a look at AbbVie stock today.

Global Market Comments

February 17, 2021

Fiat Lux

Featured Trade:

(HOW TO HANDLE THE FRIDAY, FEBRUARY 19 OPTIONS EXPIRATION),

(TSLA), (MS), (BA), (BLK), (GS), (AMD), (KO), (BAC), (NFLX), (AMZN), (AAPL), (INTU), (QCOM), (CRWD), (AZN), (GILD)

Followers of the Mad Hedge Fund Trader Alert Services have the good fortune to own no less than 16 deep in-the-money options positions, all of which are profitable. All but one of these expire in two trading days on Friday, February 19, and I just want to explain to the newbies how to best maximize their profits.

It was time to be aggressive. I was aggressive beyond the pale.

These involve the:

Global Trading Dispatch

Mad Hedge Technology Letter

Mad Hedge Biotech & Healthcare Letter

Provided that we don’t have a huge selloff in the markets or monster rallies in bonds, all 15 of these positions will expire at their maximum profit point.

So far, so good.

I’ll do the math for you on our oldest and least liquid position, the Tesla February 19 $650-$700 vertical bull call spread, which I initiated on January 25, 2021 and will definitely run into expiration. At the Friday high, Tesla shares were at a lowly $816, some $53 lower than the $869.70 that prevailed when I strapped on this trade.

Provided that Tesla doesn’t trade below $700 in two days, we will capture the maximum potential profit in the trade. That’s why I love call spreads. They pay you even when you are wrong on the direction of the stock. All of the money we made was due to time decay and the decline in volatility in Tesla stock.

Your profit can be calculated as follows:

Profit: $50.00 expiration value - $44.00 cost = $6.00 net profit

(4 contracts X 100 contracts per option X $6.00 profit per options)

= $2,400 or 20% in 18 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning February 22 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and find it.

Although the expiration process is now supposed to be fully automated, occasionally machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears, and the spreads substantially widen, when security has only hours, or minutes until expiration on Friday, February 19. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

If for some reason, your short position in your spread gets “called away,” don’t worry. Just call your broker and instruct them to exercise your long option position to cover your short option position. That gets you out of your position a few days early at your maximum profit point.

If your broker tells you to sell your remaining long and cover your short separately in the market, don’t. That makes money for your broker, but not you. Do what I say, and then fire your broker and close your account because they are giving you terrible advice. I’ve seen this happen many times among my followers.

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next month-end.

Take your winnings and go out and buy yourself a well-earned dinner. Just make sure it’s take-out. I want you to stick around.

Well done, and on to the next trade.

Global Market Comments

February 8, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE SWEET SPOT CONTINUES),

(INDU), (SPY), (SLV), (GME), (TLT), (JPM), (BAC), (C), (BLK)

We just completed the best week in the 13-year history of the Mad Hedge Fund Trader.

Kudos have been coming in from all over the world, with stories of retirements financed, mortgages paid off, and college educations paid for. Some Mad Hedge Concierge clients are reporting windfall profits of $1 million a day.

The key was calling the GameStop (GME) fiasco the one hit wonder that it was, and using it as an opportunity to go 100% long, pedal to the metal, and bet the ranch. When the market gives you a gift, you grab it with both hands as if your life depended on it and don’t let go.

It worked.

That’s what 50 years of practice gets you, the ability to spot the gold coins lying on the street ignored by everyone else and pocket them immediately.

A record $4.2 billion poured into technology stock funds last week as investors call the end of the six-month big tech correction. The barbell approach is working like a charm, with buying bouncing back and forth like a ping pong ball between domestics, technology, or both sectors go up at the same time. It’s better than owning a printing press for $100 bills.

The Mad Hedge Technology Letter also spotted which way the gale force winds were blowing and piled on the longs as well. (AMZN), (QCOM), and (CRWD), it’s all music to my ears. My old friend Jeff retired, paving the way for another doubling in his stock (AMZN).

We now are getting a clearer picture of how 2021 will play out in the stock market. Periods of sideways action will be followed by big gaps up, eventually taking us to a Dow Average of 40,000.

The sweet spot continues. As low as interest rates and inflation remain low and a tidal wave of new money is pouring into the economy, you have a rich uncle writing you a check every month from the stock market.

We have not had a correction of more than 4% since October. This could go on for years.

Where will the next surprise come from?

When Joe Biden gets his full $1.9 trillion in upfront rescue spending. With the grim tidings of three disastrous monthly jobs reports out, it couldn’t go any other way. The cost of waiting is just too high, especially for the 18 million U-6 unemployed and millions of small businesses hanging on by their fingernails.

The Nonfarm Payroll Report came in very weak, at 49,000 in January. The headline Unemployment Rate was at 6.3%, a decline as more people are leaving the workforce. The U-6 broader “discouraged worker” unemployment rate is still at 11%. December was revised down to an even bigger 227,000 loss. Construction was down 10,000, Retail down 37,000, and Government Jobs were up 43,000. It’s the third disappointing month in a row so a double-dip recession is still on the table. We have a very long road to recovery.

Weekly Jobless Claims improved, dropping to 779,000, the lowest since November. The correlation with falling Covid-19 cases is almost perfect, which have declined by 35% in two weeks. Is the stock market getting ready to roar?

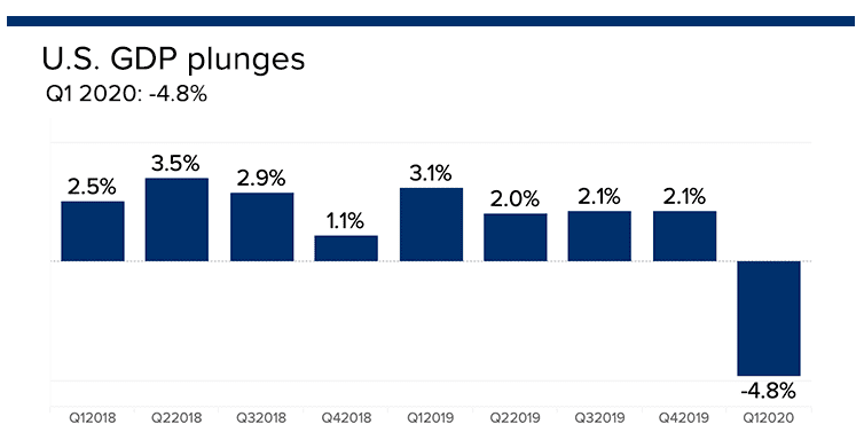

US GDP fell by 3.5% in 2020, wiping out all of 2019 and a good chunk of 2018 as well. The last quarter of 2020 came in at -4.8%, much worse than expected, and further downward revisions are coming, according to the Bureau of Economic Analysis. The economy won’t recover pre-pandemic levels until late 2022 or 2023. The biggest drags on the economy were dramatic falls in consumer spending, nonresidential fixed investment, and a trade war-induced plunge in exports.

Pending Home Sales fell, 0.3% in December, but are still up a staggering 21.4% YOY. It is the highest December reading on record, but the fourth straight month of declines. A historic shortage of supply is the main reason.

The short squeeze play moved to silver, with prices hitting an eight-year high. Many local dealers are seeing business rise tenfold over the weekend and are running out of inventory. The white metal was up 35% in two days. It’s the largest one-day volume every. This time, the kids may have got it wrong, since all short positions in the options market are fully hedged with long positions in silver futures or silver bars. The GameStop players only saw the short side. Long term, I love (SLV) for industrial demand from electric cars and solar panels and see it going from today’s $28 to $50, but not today.

Apple (AAPL) is boosting share buybacks and is borrowing to do it. It’s issuing $14 billion in bonds out to 40 years in maturity at 95 basis points above Treasuries. If Apple is so aggressive in buying its own stock, maybe you should too.

The Apple car is moving forward, as incredible as it may seem. The company is in talks with South Korea’s Hyundai to produce autonomous self-driving electric vehicles that will be available by 2024. I’ll believe it when I see it. I’ve seen Apple self-driving cars in the Bay Area for years. It’s an interesting combination: Apple software, a South Korean design, and non-union Georgian metal bashing combined. Sounds like a winner to me.

The GameStop (GME) game ends. Back to selling used video games in shopping malls. Millions were lost in the crash from $483 to $49. Back to buying real stocks with the systemic threat to the main market over.

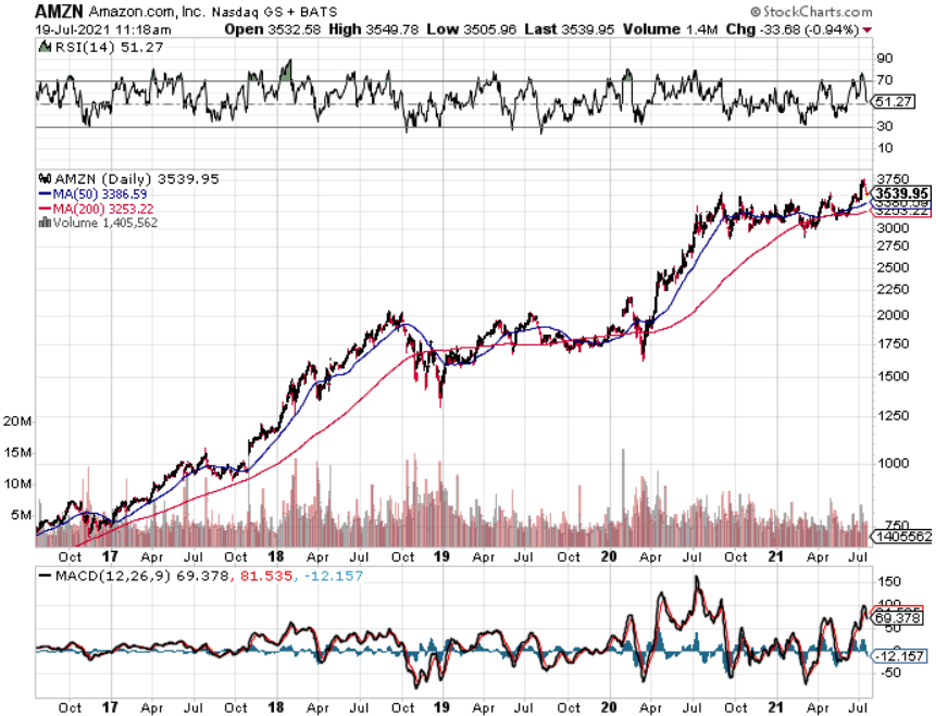

Jeff Bezos retired, putting the operation of Amazon into the hands of Andy Jassy, the inventor and head of the cloud unit AWS. No move in the stock beyond the first few seconds. Jassy has been there since the beginning. If I were the second richest man in the world, after Elon Musk, I’d take some time off too. Now, maybe my former Morgan Stanley colleague will have drinks with me. Buy (AMZN) on dips. My two-year target is $5,000.

Bombs away for the bond market, as the (TLT) hits a new 2021 low, taking ten-year yields up to 1.13%. I’m taking profits on the last of my bond shorts and piling money into financials, which love higher interest rates. Buy (JPM), (BAC), (C), and (BLK) on dips. A 1.50% yield on the ten-year US Treasury bond here we come! This is the quality trade of 2021.

The ADP Private Employment recovered, up 174,000 in January after a 74,000 plunge in December. Leisure & Hospitality is the big variable.

PayPal transactions were up 25% in 2020, showing the incredible extent of the online migration of the economy. Keep going with Fintech. There’s another double in (PYPL).

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned an amazing 14.15% during the first week of February after a blockbuster 10.21% in January. The Dow Average is up 3.47% so far in 2021. This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 24.36%.

I absolutely nailed the market bottom created by the GameStop fiasco, which I didn’t expect to last any more than days. I went 100% leveraged long, which enabled me to achieve the astounding numbers I am reporting today.

Not only did I get the market right, I picked the perfect sectors as well. I jumped 60% into financials, 20% in Tesla, 10% for commodities, and 10% in chips. I used the bond market meltdown to cover the last of my bond shorts. But all of my financial longs are essentially bond shorts.

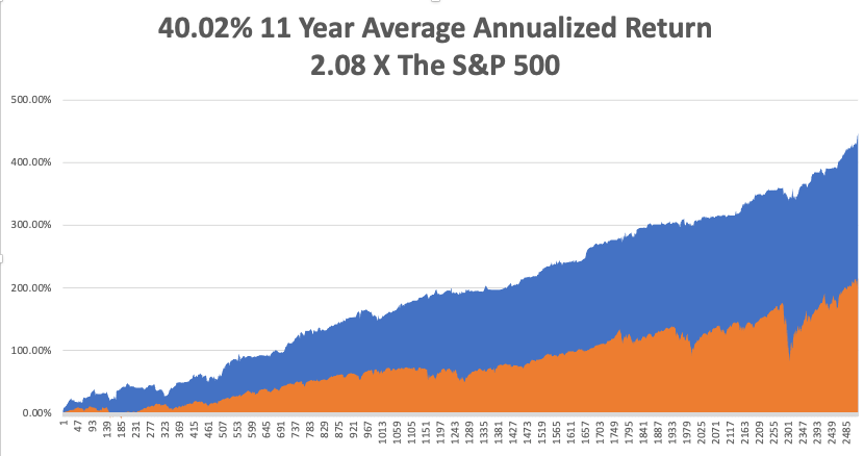

That brings my 11-year total return to 446.81%, some 2.08 times the S&P 500 over the same period. My 11-year average annualized return now stands at an Everest-like new high of 40.02%.

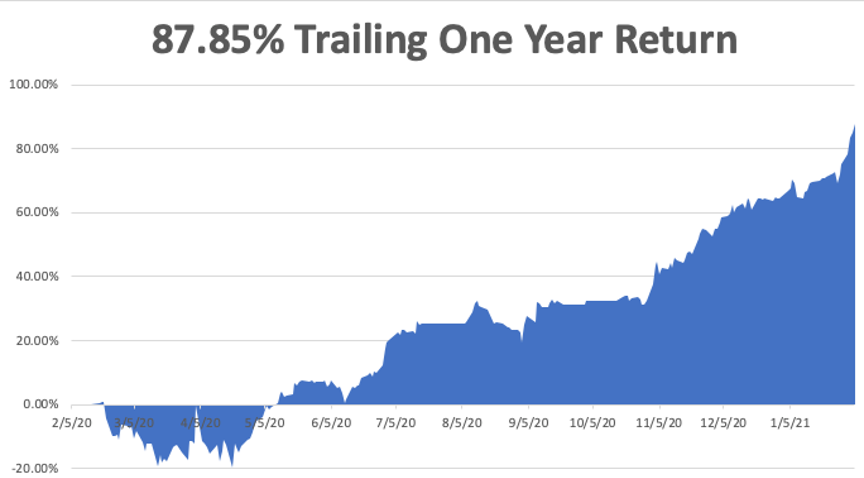

My trailing one-year return exploded to 87.85%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 105.58% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 27 million and deaths 465,000, which you can find here. We are now running at a heartbreaking 3,000 deaths a day. But that is down 35% from the recent high.

The coming week will be a boring one on the data front.

On Monday, February 8 at 11:00 AM EST, Consumer Inflation Expectations for January are out. Softbank (SFTBY) and KKR & Co. (KKR) report.

On Tuesday, February 9 at 6:00 AM, the NFIB Business Optimism Index is released. Cisco Systems (CSCO) and Twitter (TWTR) report.

On Wednesday, February 10 at 8:30 AM, the US Core Inflation Rate is announced. Coca-Cola (KO) and Uber (UBER) report.

On Thursday, February 11 at 9:30 AM, Weekly Jobless Claims are printed. Walt Disney (DIS) and AstraZeneca (AZN) report.

On Friday, February 12 at 2:00 PM, we learn the Baker-Hughes Rig Count. As we have a three day weekend following, option volatility should collapse. Moody’s (MCO) reports.

As for me, I went into Reno last week to replace the windshield on my Toyota Highlander, my Tahoe car, which below zero temperatures had cracked. One-third of the town was shut down and boarded up, while what remained was booming. A giant shopping mall near downtown has resumed construction, but with less retail and more residential. Reno is the third fastest-growing city in the US and has become a metaphor for the entire country.

Still waiting for my Covid-19 vaccination. I’m at the top of four lists. Even the military can’t get enough. With any luck, I’ll have it in weeks.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader