(MARKET OUTLOOK FOR THE WEEK AHEAD, or TRUMP DECLARES WAR ON THE WORLD),

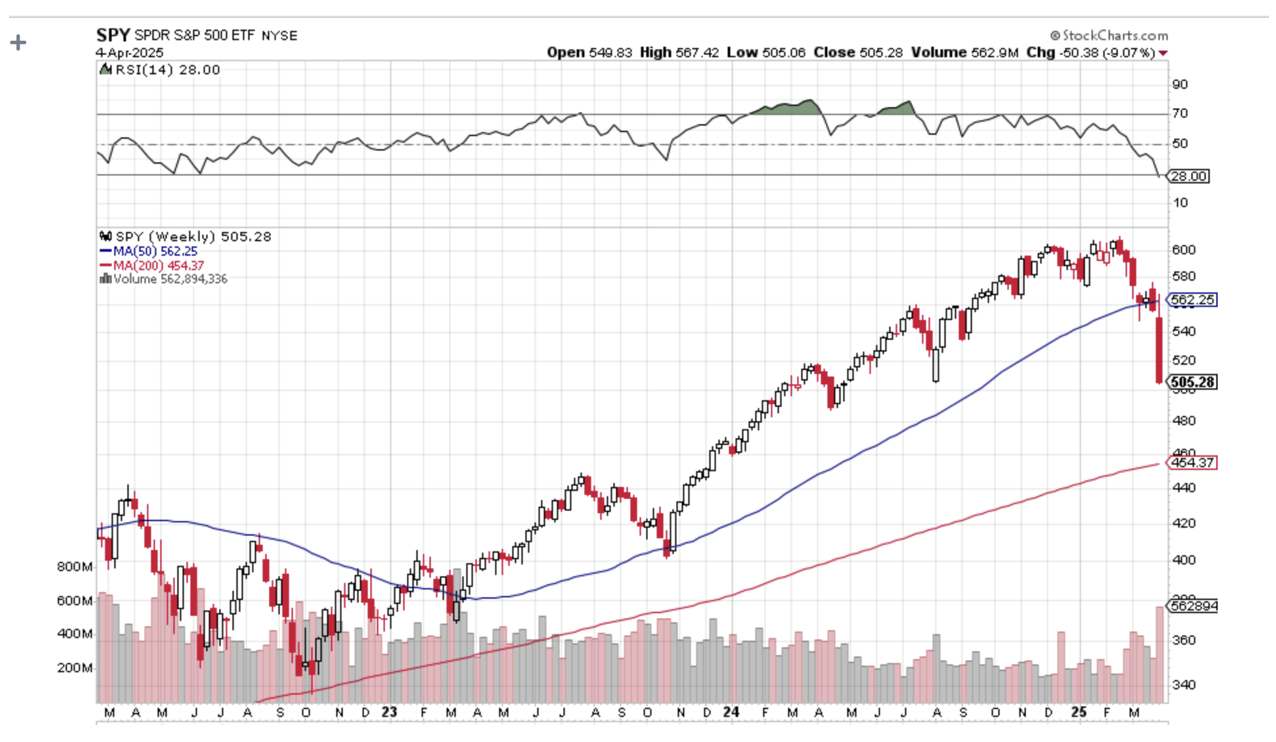

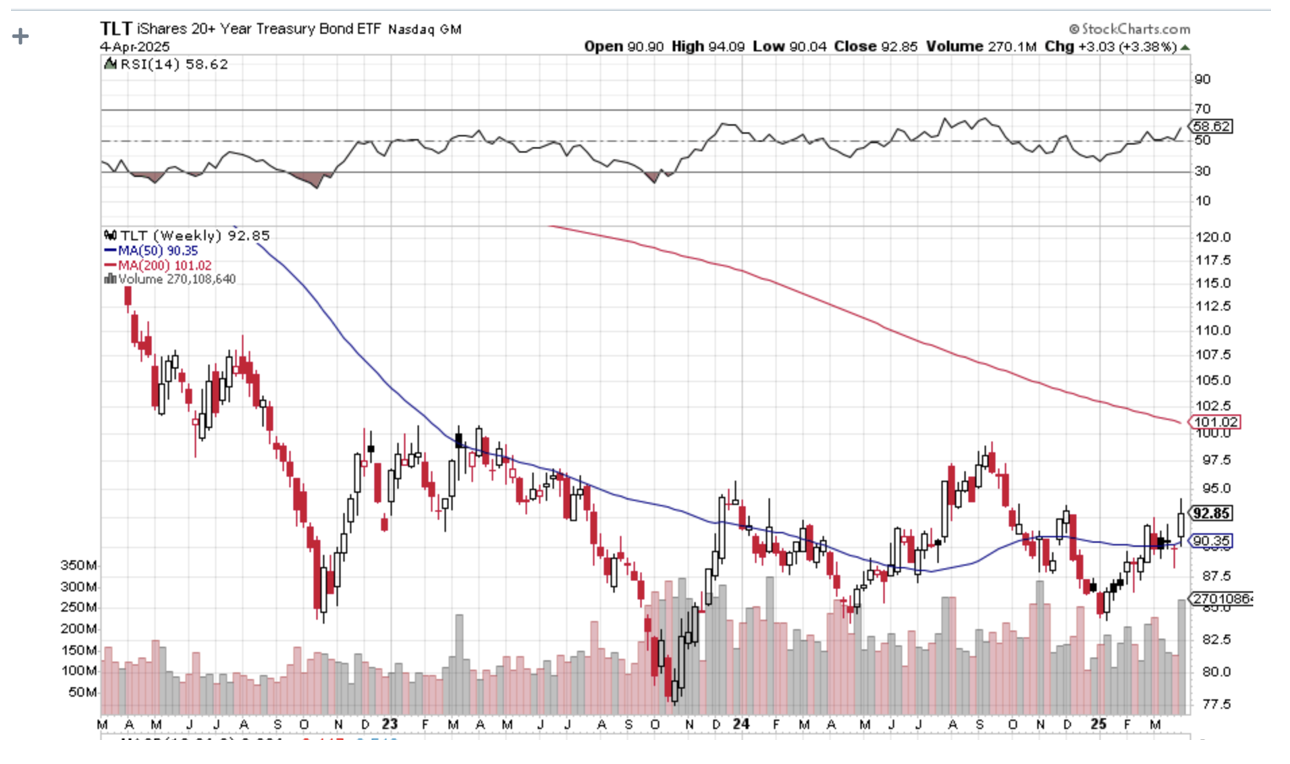

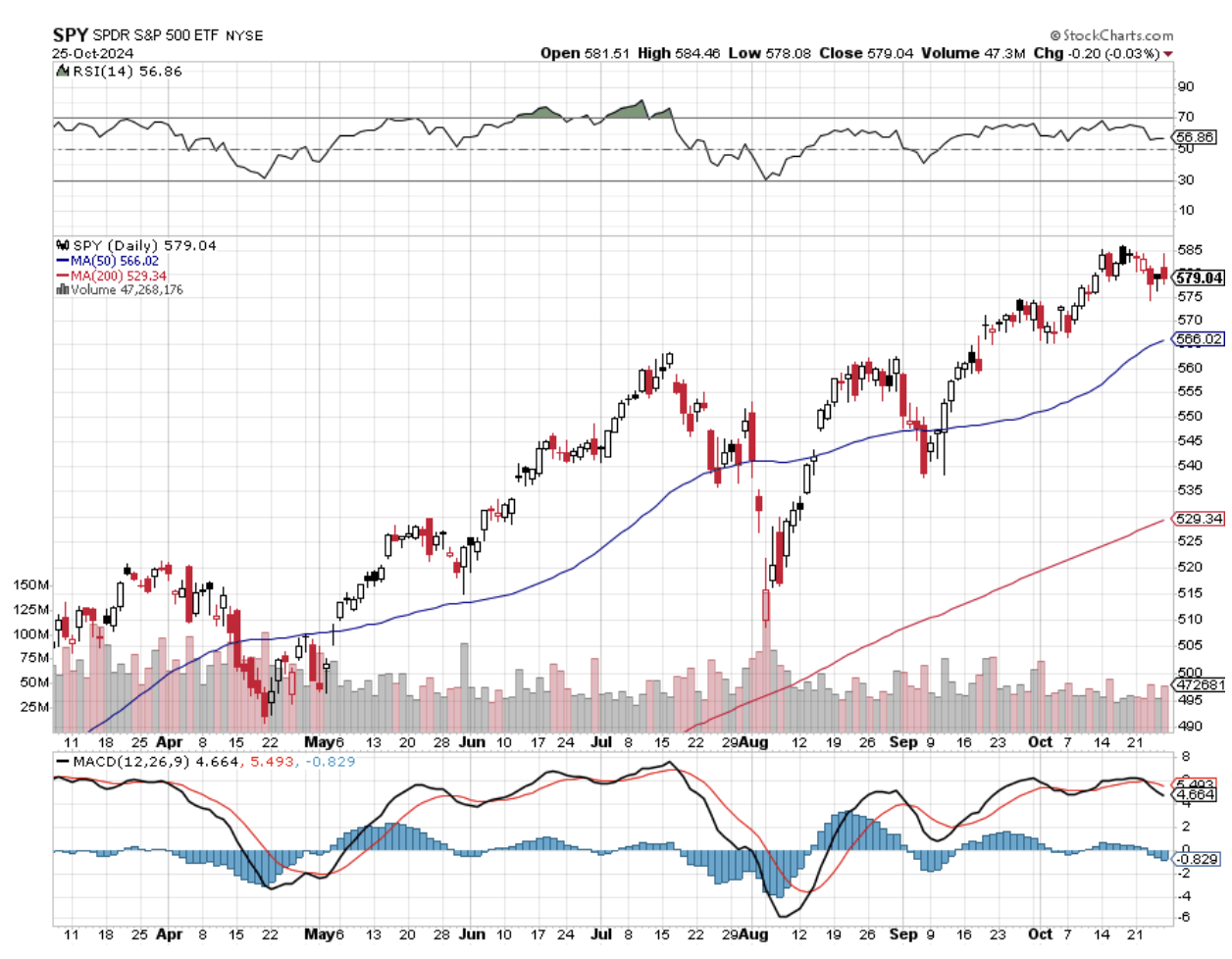

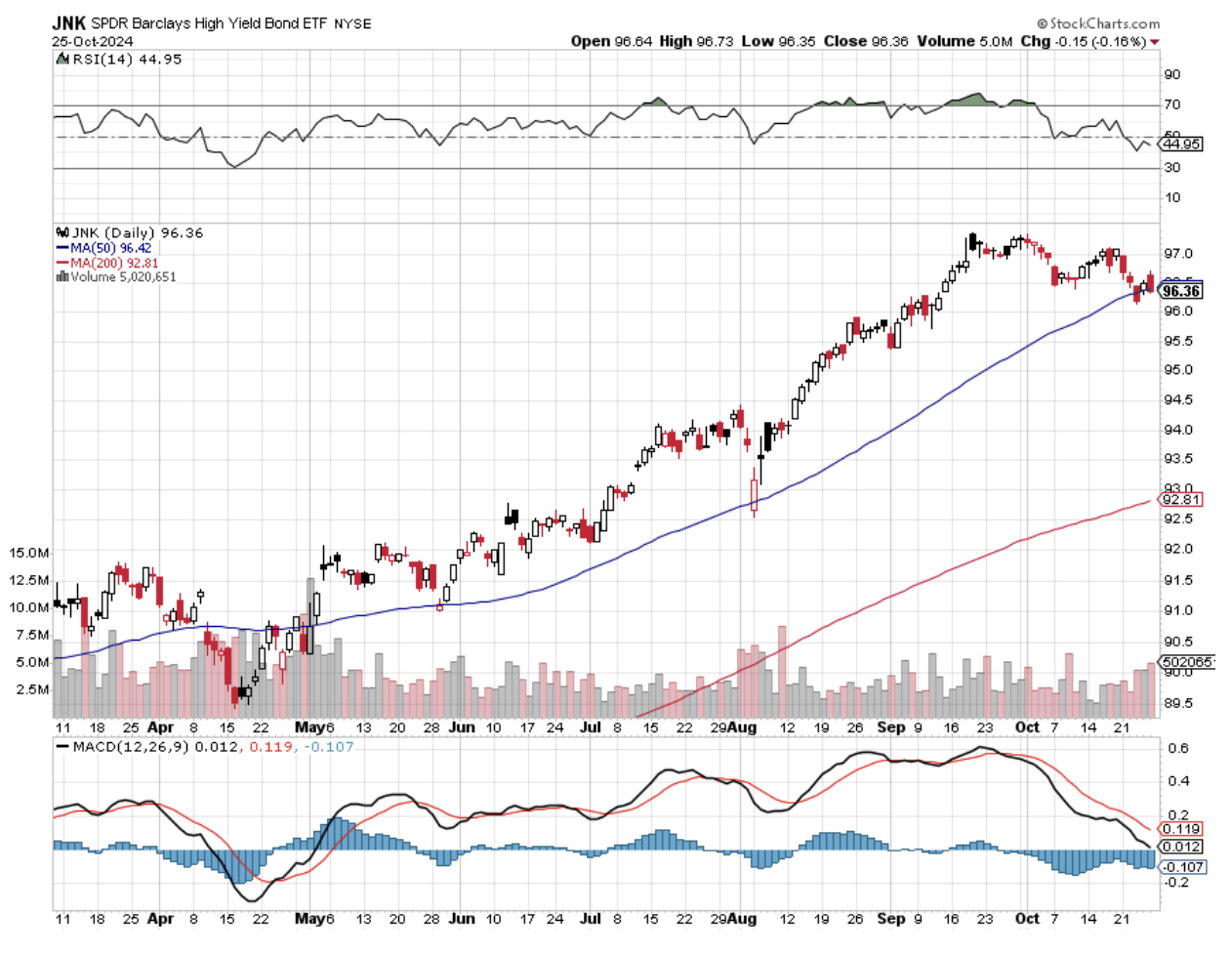

(SPY), (TLT), (META), (GOOGL), (MSFT), (CRM),

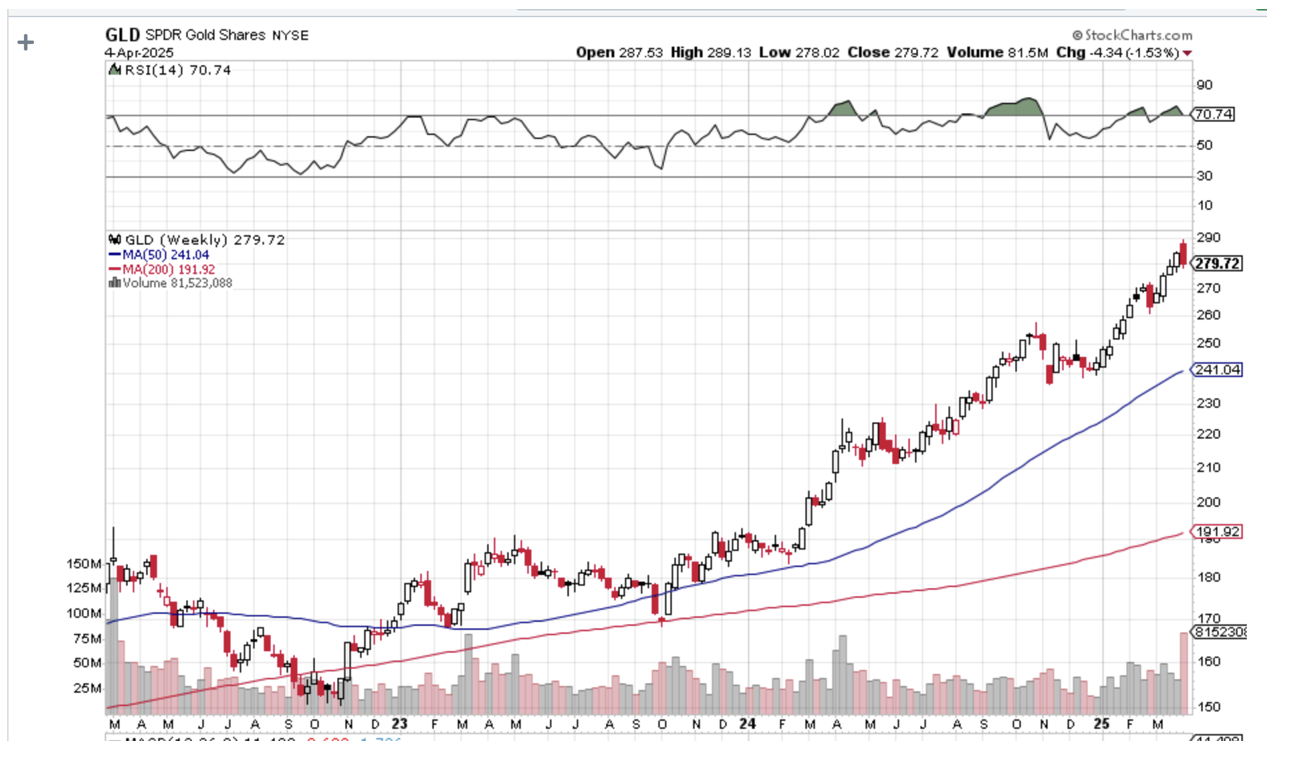

(COST), (NVDA), (NFLX), (NVDA), (TSLA), (GLD)

I often get asked why I am still working after 55 years in the stock market.

With five customers calling me this morning to thank me for saving their retirement funds, you might understand why.

It is now clear that in retrospect and with the wisdom of 20/20 hindsight, corporate America flipped the switch on the economy, shutting it off and sending all hiring and investment to a grinding halt. They wanted to wait and see how business would fare under the new Trump regime. We didn’t see this in the data until February.

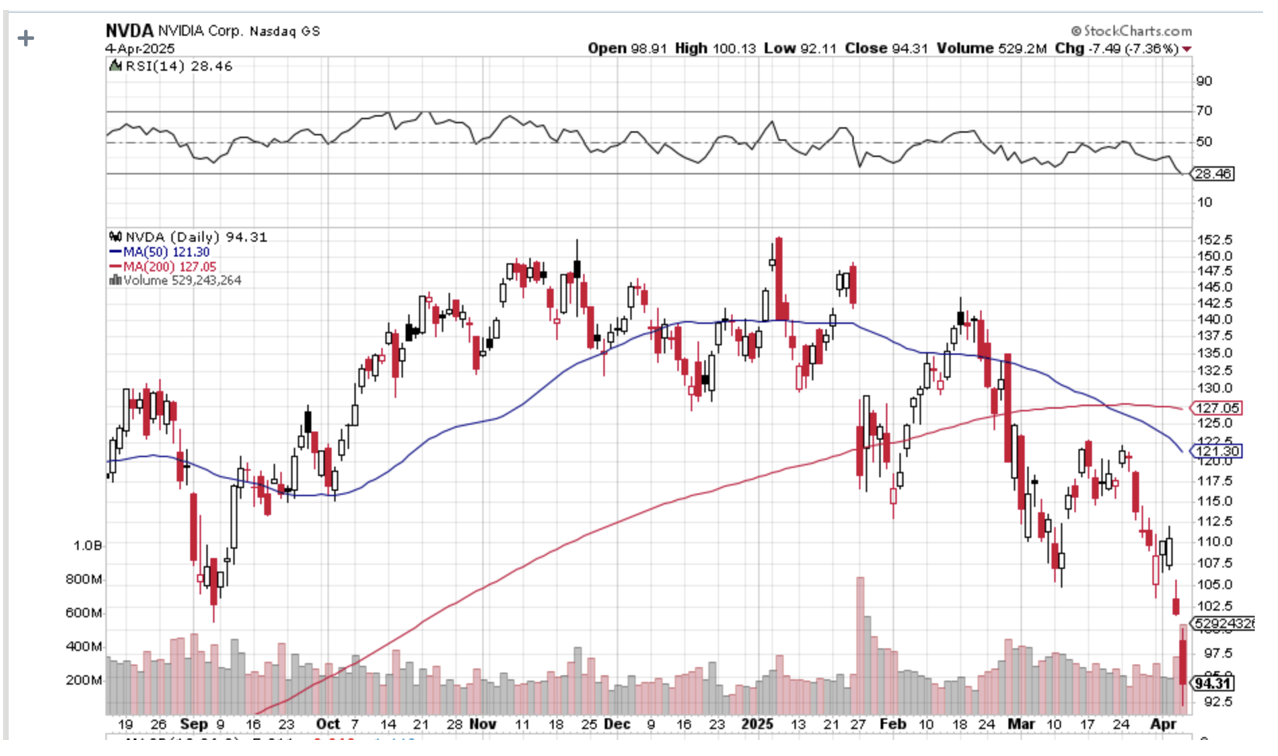

That’s when I started shouting from the rooftops that we were already in a recession and bear market and that you should sell everything, especially big tech stocks. If you waited until August for the data to confirm this, the move-down will be over.

T-bills, bonds, and gold were the only safe places to park your money. Gold just delivered the best quarter since 1986, up 19%. That month I took my short positions up to 80%, a 17-year high for the Mad Hedge Fund Trader.

Those now look like very wise decisions, with markets suffering their worst two-day crash since 1987, and the bad news has only just started. Option implied volatiles are at five-year highs, and risk positions everywhere are going to hell in a handbasket. Tariff-driven inflation could spike to 10% by next year.

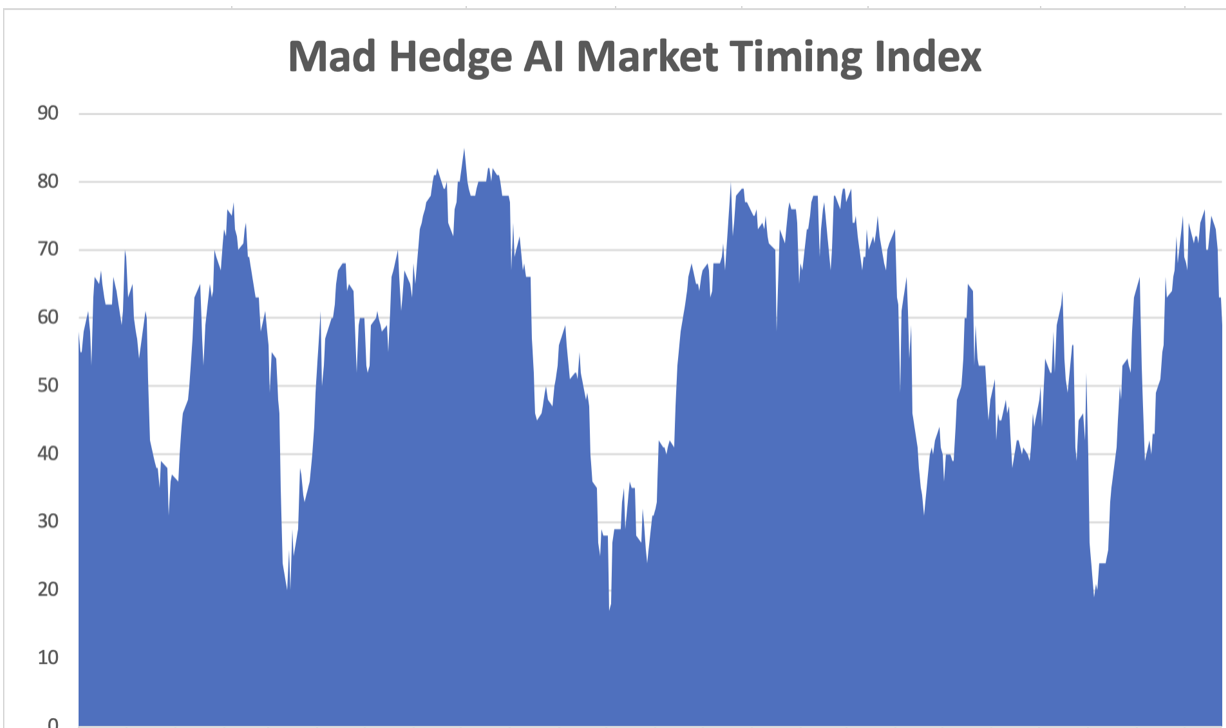

Even securities unrelated to stocks, like junk bonds (JNK), down $6 points in two weeks,were getting thrown out with the bathwater because of margin calls. The Mad Hedge AI Market Timing Index is at a five-year low at a reading of 4. Q1 saw the fastest reversal in market momentum in 38 years.

I even heard an expression new to me: “Hate selling”. That refers to a global disengagement from investment in the US and the return of capital to better-performing foreign markets and currencies. Trump is attacking their countries.

The global nature of the selloff is most disturbing, with every country seeking its stock markets rolling over all at once.That presages a global recession.

Analysts across Wall Street are tearing up their playbooks for 2025 and setting new downside targets as fast as they can like I did in February.

Instead of the $500 billion tax increase I expected tariffs would deliver, we got $1 trillion. The worst forward guidance from corporations since the Great Depression starts next week. Retaliatory 34% tariffs from China hit today, and those from Europe will come soon. Trump has promised retaliation.

That forces me to adjust my downside target for the S&P 500 from $5,000 to $4,500. That is a 26.6% selloff from the February top, or 11% more downside from here. How do we get there? Simply assign the 2019 earnings multiple low of 18 and multiply it by S&P 500 earnings pared back by the trade war from$270 to $250. That gets you to $4,500 in months, if not weeks (18 X $250).

No help is that we entered this crash with valuation highs that have only been seen in 1999 and 1929. The higher the high, the lower the lows that follow.

In fact, there is no bottom to this market.

This forecast is based on historical data and assumes that markets are rational and orderly. But as we all know too well, markets can be anything but rational and orderly once the panic selling and margin calls begin.

Of course, a tweet on social media about negotiations could trigger a massive short-covering rally at any time. In reality, the stock market has been negotiating on behalf of Europe and China quite successfully. The further stocks fall, the greater the pressure on Trump to fold.

Tariffs advertised at the White House announcement left our trading partners scratching their heads because they were completely bogus and were a large multiple of the true tariffs. The person who came up with these cockamamie figures remains anonymous, as they used an arbitrary, obscure formula made up from scratch that had never been seen before by the economic community.

For example, the White House claimed the tariff charged by Vietnam was 90%, when in fact it is 5.5%. The claimed tariff for Taiwan was 64%, while the actual one is 1.7%.

The White House numbers supposedly included a factor for non-tariff barriers. I happen to be an expert in these because Japan was notorious for its non-tariff barriers in the 1970s. For example, import documents have to be submitted in Japanese. Hey, I speak Japanese. All they had to do was ask me! How did they quantify this?

That’s anyone’s guess.

The saddest thing is that this new bear market was not caused by surprise external events as in all others in the past century, but is totally voluntary and self-inflicted. It is actually caused by the false assumptions of conspiracy theorists. But these days, it is the conspiracy theorists who have the upper hand.

Why do we suddenly need an emergency jobs program now, when the country is operating at full employment? Many of those skills needed to man the jobs Trump is trying to take back from China, such as in textiles, clothing, shoes, and toys,haven’t existed in the US for generations. Nor does the machinery.

Some three-quarters of the US trade deficits are offset by a monster surplus in services run up by the likes of Meta (META), Alphabet (GOOGL), Microsoft (MSFT), Oracle (ORCL), and Salesforce (CRM). And if you didn’t already know, the future is in services, not in manufacturing.

I don’t know about you, but I don’t lose a lot of sleep at night worrying about our trade deficit with Vietnam. Trump took what was a great economy and destroyed it in an effort to remake it in his own image. Is this crazy experiment with 20% of your retirement funds cost so far? How about 50%?

No wonder the Republican Party is panicking! Recent elections have shown unprecedented swings by voters away from them, fearful of their 401Ks.

How many factories will return to the US as a result of the tariffs? My bet is none. There will be many announcements but no actual action, as with the first Trump administration.

Labor costs are $5 an hour in Mexico and China, versus $25-$75 an hour in America. We keep the high-paying, high-value-added jobs and send the cheap, dangerous, highly energy-consuming, and high-polluting ones abroad. Foreigners get rich and earn the money to buy our services.

Their government then takes the excess funds and buys US Treasury bonds (China still has $760 billion worth) and finances our deficits with ever-depreciating paper. It is one big mutually enriching cycle. That’s why globalization has worked for 85 years.

The best thing for companies is to now sit on their hands and do nothing and wait out the next four years until a future administration eliminates the tariffs. That’s much cheaper than spending $20 billion on a new factory here which might become useless in four years.

What is a stock market worth that is walled off from the rest of the world that's in recession? Maybe half or less the February peak value, but I’m only guessing.

It might be much worse.

Keep all cash positions in 90-day T-bills and keep all hedges of existing equity portfolios also at a maximum until the stock market can find its own bottom. I’d rather miss the first 10% move and buy on the way up than catch a falling knife right now.

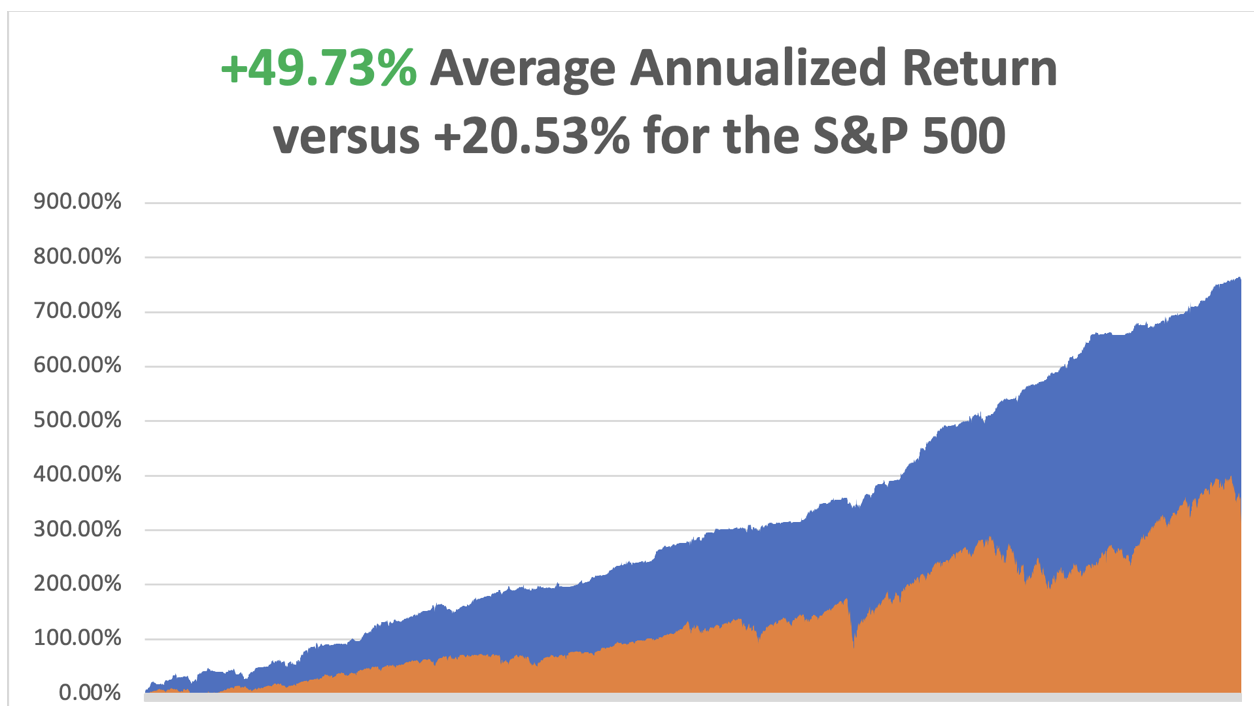

April is now down -7.25%so far due to the explosion in implied volatilities in our hedged positions. A lot of the Friday options prices made no sense and may reflect broker efforts to increase margin requirements. That takes us to a year-to-date profit of +6.58%so far in 2025. My trailing one-year return stands at a spectacular +74.93%. That takes my average annualized return to +49.73%and my performance since inception to +758.47%.

It has been another busy week for trading. I used the meltdown to add very deep in-the-money longs in (COST), (NVDA), and (NFLX). I stopped out of an existing (NVDA) long as we approached the upper strike price. I kept my very deep in-the-money long in (TSLA). I also kept my (GLD) long as a hedge.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades have been profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

Try beating that anywhere.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties is now looking at multiple gale-force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

Trump Announces Worst-Case Scenario Tariffs, tanking stocks and crypto, with big technology stocks taking the biggest hits. “RISK OFF” assets like gold, silver, bonds, and foreign currencies are soaring. The Dow Average could suffer a 1987-style crash on Monday. Volatility will explode. Duties on Chinese goods were raised to 34%, Europe 20%, and Southeast Asian countries up to 45%. All countries have been hit with high tariffs to avoid transshipments. Retaliation from the world is on the way. It’s another nail in the economy’s coffin, which is now almost certainly in recession. S&P 500 at 5,000 here we come. Is this the day the great depression started? Some $2 trillion in market capitalization was lost today. Tariffs to Push All Home Prices Higher, as much as 5%, as homebuilders wind down new construction because of higher costs. Drywall comes from Mexico, lumber from Canada, and 10% of the workforce are immigrants. It could explain the recent improvement in existing home sales. Jobless Claims Hit Three-Year High. Continuing claims, a proxy for the number of people receiving benefits, increased to 1.9 million in the week ended March 22, slightly higher than economists expected. Those applications have been hovering just under that level for several months now. Meanwhile, initial claims dipped last week, to 219,000, according to Labor Department data released Thursday. Auto Loan Defaults Hit 21-Year High, with 6.5% of subprime borrowers at least 60 days overdue on payments. It is the largest default rate since data began collection in 1994. Yet another recession indicator. Tesla Sales Fall off a Cliff,down 13% on the quarter, its weakest performance in nearly three years, as backlash to CEO Elon Musk's embrace of far-right politics grows and as consumers seek out newer models from rival electric-vehicle makers. The EV maker's stumbling sales indicate that the one-time leading brand is reeling from the fallout of the company not refreshing its vehicle lineup in years, and Musk's foray into politics in the United States and Europe. The company posted weak sales in numerous European markets and China, even as more consumers are opting for EVs. Sell (TSLA) on rallies.

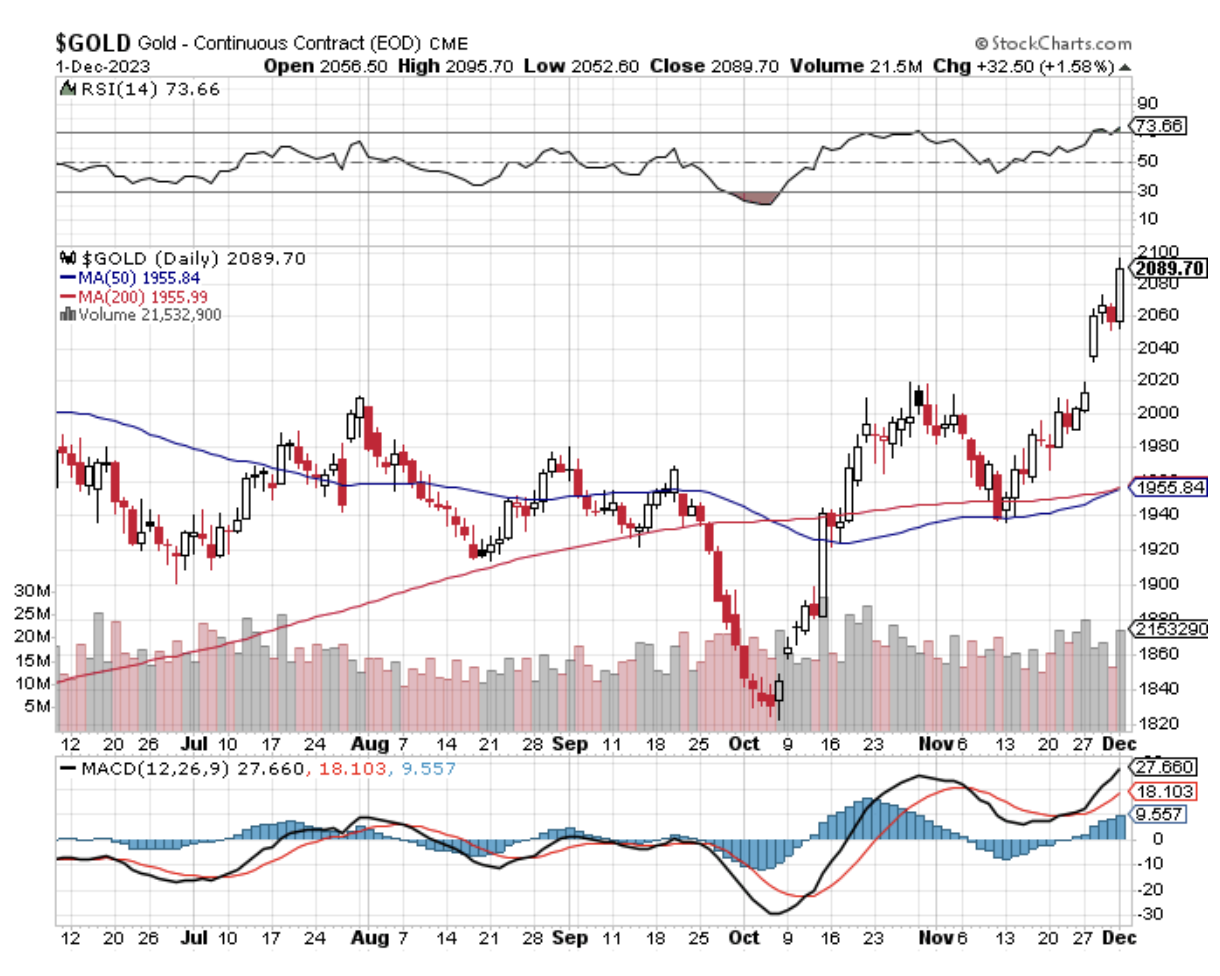

Global Sentiment is collapsing, over trade wars and recession fears. Business sentiment among big Japanese manufacturers worsened in the three months to March, a central bank survey showed on Tuesday, a sign escalating trade tensions were already taking a toll on the export-reliant economy. Auto exports to the US are a major support for the Japanese economy, which is an American ally. A global contagion is afoot. US Dollar Declines as a Reserve Currency, in the last quarter of 2024 while the percentage of actual dollars held as reserve ticked up, IMF data showed on Monday. Dollar-equivalent amounts dropped also among holdings in euro, pound sterling, yuan, yen, Swiss franc, and Australian and Canadian dollars, with only the latter showing a tick up in the percentage of holdings, the IMF's Currency Composition of Official Foreign Exchange Reserves (COFER) data showed. The end of American exceptionalism means a cheaper greenback. Vaccine Stocks Get Nailed, as the FDA moves the eliminate the vaccine establishment. Expect stocks to fall and disease to rise. The Food and Drug Administration's top vaccine official, Peter Marks, has been forced to resign, the most high-profile exit at the regulator as the Trump administration undertakes an overhaul of federal health agencies. Gold Stocks in Comex Warehouses Hit Record highs, due to the risk of import tariffs curtailing shipments to the United States from other countries. Latest data from Comex, part of CME Group, shows gold stored in its warehouses in the United States at an all-time high of 43.3 million troy ounces worth $135 billion at current prices compared with 17.1 million in November. Spot gold prices surged past $3,100 per ounce to a fresh record high on Monday. Bullion is up 19% so far this year after rising 27% in 2024. Buy (GLD) on dips.

On Monday, April 7, at 8:30 AM EST, the Used Car Prices are announced.

On Tuesday, April 8, at 8:30 AM, the NFIB Business Optimism Index isreleased.

On Wednesday, April 9, at 1:00 PM, the FOMC Minutes are published.

On Thursday, April 10, at 8:30 AM EST, the Weekly Jobless Claims are disclosed. We also get the Consumer Price Index and Inflation Rate.

On Friday, April 11, at 8:30 EST, the Producer Price Index for March is printed. We also get the University of Michigan Consumer Sentiment. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, with the 38th anniversary of the 1987 crash coming up this year, when shares dove 20% in one day, I thought I’d part with a few memories.

I was in Paris visiting Morgan Stanley’s top banking clients, who back then were making a major splash in Japanese equity warrants, my particular area of expertise.

When we walked into our last appointment, I casually asked how the market was doing (Paris is six hours ahead of New York). We were told the Dow Average was down a record 300 points. Stunned, I immediately asked for a private conference room so I could call the equity trading desk in New York to buy some stock.

A woman answered the phone, and when I said I wanted to buy, she burst into tears and threw the handset down on the floor. Redialing found all transatlantic lines jammed.

I never bought my stock, nor did I find out who picked up the phone. I grabbed a taxi to Charles de Gaulle airport and flew my twin Cessna as fast as the turbocharged engines took me back to London, breaking every known air traffic control rule.

By the time I got back, the Dow had closed down 512 points. Then I learned that George Soros asked us to bid on a $250 million blind portfolio of US stocks after the close. He said he had also solicited bids from Goldman Sachs, Merrill Lynch, JP Morgan, and Solomon Brothers, and would call us back if we won.

We bid 10% below the final closing prices for the lot. Ten minutes later, he called us back and told us we won the auction. How much did the others bid? He told us that we were the only ones who bid at all!

Then you heard that great sucking sound.

Oops!

What has never been disclosed to the public is that after the close, Morgan Stanley received a margin call from the exchange for $100 million, as volatility had gone through the roof, as did every firm on Wall Street. We ordered JP Morgan to send the money from our account immediately. Then they lost the wire transfer!

After some harsh words at the top, it was found. That’s when I discovered the wonderful world of Fed wire numbers.

The next morning, the Dow continued its plunge, but after an hour managed a U-turn, and launched on a monster rally that lasted for the rest of the year. We made $75 million on that one trade from Soros.

It was the worst investment decision I have seen in the markets in 53 years, executed by its most brilliant player. Go figure. Maybe it was George’s risk control discipline kicking in?

At the end of the month, we then took a $75 million hit on our share of the British Petroleum privatization because Prime Minister Margaret Thatcher refused to postpone the issue, believing that the banks had already made too much money.

That gave Morgan Stanley’s equity division a break-even P&L for the month of October 1987, the worst in market history. Even now, I refuse to gas up at a BP station on the very rare occasions I am driving a rental internal combustion engine from Enterprise.

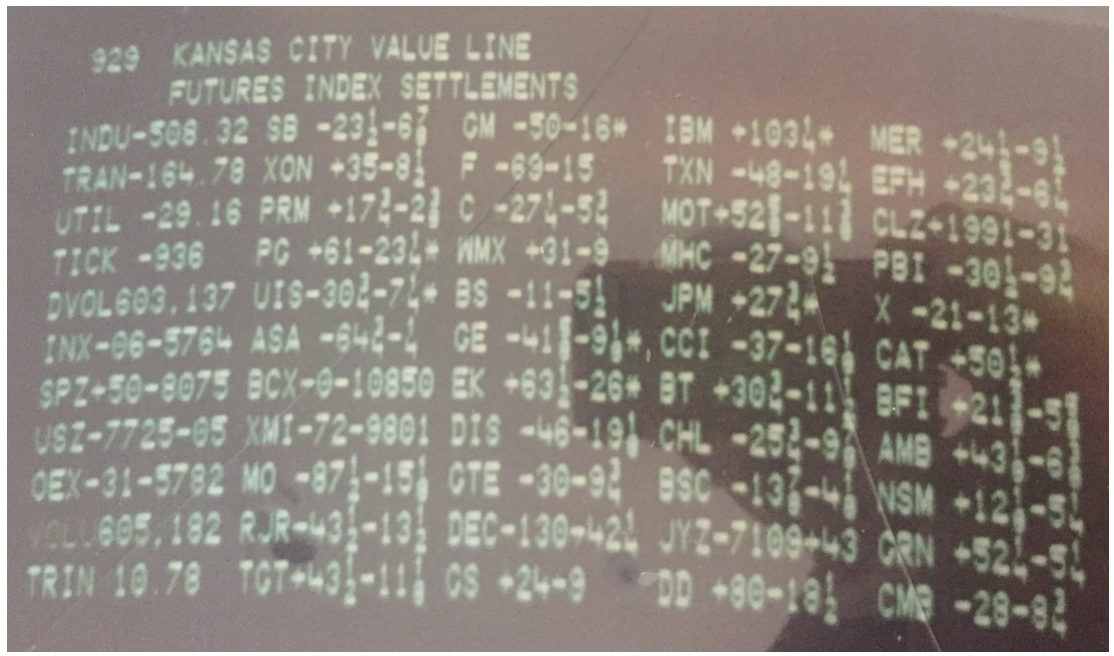

My Quotron Screen on 1987 Crash Day

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2025/03/morgan-stanley.png7181040april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-04-07 09:02:212025-04-07 13:07:53The Market Outlook for the Week Ahead, or Trump Declares War on the World

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE IS YOUR POST-ELECTION PORTFOLIO

plus THE LAST SILVER BUBBLE)

(NVDA), (META), (CRM), (TLT), (JNK), (CCI), (DHI), (LEN), (PHM),

(GLD), (SLV), (NEM), (FXE), (FXB), (FXA), (TSLA), (JPM),(BAC), (GS)

The world was supposed to end at midnight on December 31, 1999 because computers would be unable to cope with the turnover of the new millennium. I remember making presentations to big hedge funds, predicting that Y2K was a big nothing burger and, worst case, somebody’s toaster wouldn’t work.

I spent that New Year’s Eve with my kids at Disneyland in Orlando, watching one heck of a fireworks display. What happened the next morning? Even the toasters worked.

I think we are setting up for another Y2K outcome, except that this time, it’s the presidential election that has everyone in a tizzy.

The polls are tied at 48%-48% with a margin of error of 4%. In fact, for the last 50 years, the opinion polls have been wrong by an average of 3.4%. One side already has that 3.4% and probably more, plus all seven battleground states, but we won’t know for sure until November 6.

As an investment manager, it is not my job to pick a side or impose my view upon you but to deliver the best possible investment returns for my clients.

And let me tell you how.

Remember the Pandemic? Four years after the event, we now have the luxury of copious hard data. Out of 103,436,829 cases, some 1,203,648 Americans died, or 1.3%. But, the death rate in red states was much higher than in blue states.

For example, California suffered only 101,159 deaths out of a population of 39,128,162 for a death rate of 0.26%. Florida saw 86,850 deaths out of a population of 22,634,867 for a death rate of 0.38%. Deaths in Florida were 68% higher in the Sunshine State than in the Golden State.

Florida, in effect, traded lives for business profits. Florida also had a Typhoid Mary effect in that by staying open for spring breaks and vacations; it increased the death rates in surrounding red states.

Assume that half of those who died were voters and apply this math to the entire country, and Republicans lost 393,059 votes to the pandemic compared to only 268,935 for Democrats. Some 124,125 more Republican voters died than Democrats. Is 124,125 votes enough to decide this election?

Absolutely!

In the 2020 presidential election, Biden won the three battleground states of Georgia by the famous 11,779 votes, Arizona by 10,457 votes, and Nevada by 33,596 votes. That’s 33 electoral college votes right there out of 270 needed.

The opinion polls have missed these numbers by a mile because their algorithms don’t take the pandemic into consideration. They are counting dead voters, while the actual election polls only count live ones. I predict that the opinion polls will be spectacularly wrong….again.

Of course, these are back-of-the-matchbook ballpark calculations. I’ll leave it to some future aspiring PhD candidate to research his thesis with more precise figures. I have better things to do.

So, how do we make money off of all this? I have never seen investors so underweight and cautious going into a major risk event like this election. They have been scared out of the market by the media. Therefore, I expect the stock market to rise by 10% after the election, taking the S&P 500 as high as 6,400.

Let the great chase begin!

Here is your model portfolio for the rest of 2024.

(NVDA), (META), (CRM) – Underweight fund managers will chase this year’s best performers so they can look good at yearend. Similarly, they will dump their worst performers in the energy sector. So will individual investors for tax loss harvesting.

(TLT), (JNK), (CCI) – All interest rate plays make back recent losses as the threat of $10-$15 trillion in new borrowing by a future president, Trump, disappears.

(DHI), (LEN), (PHM) – There is no better interest rate play than new homebuilding. It’s tough to beat a structure shortage of 10 million homes.

(GLD), (SLV), (NEM) – Precious metals also do very well as they have less yield competition from other interest rate plays. These have become the principal savings vehicle for Chinese individuals.

(FXE), (FXB), (FXA) – A falling interest rate advantage for the US dollar means you want to buy all the currencies.

(JPM), (BAC), (GS) – Banks also do exceedingly well in a falling interest rate environment, and brokers and money managers will cash in on exploding stock market volume.

Also, on November 6, your toaster will probably still work. And I will never understand why the Center for Disease Control never accepted my application out of college. So, I went to Vietnam instead.

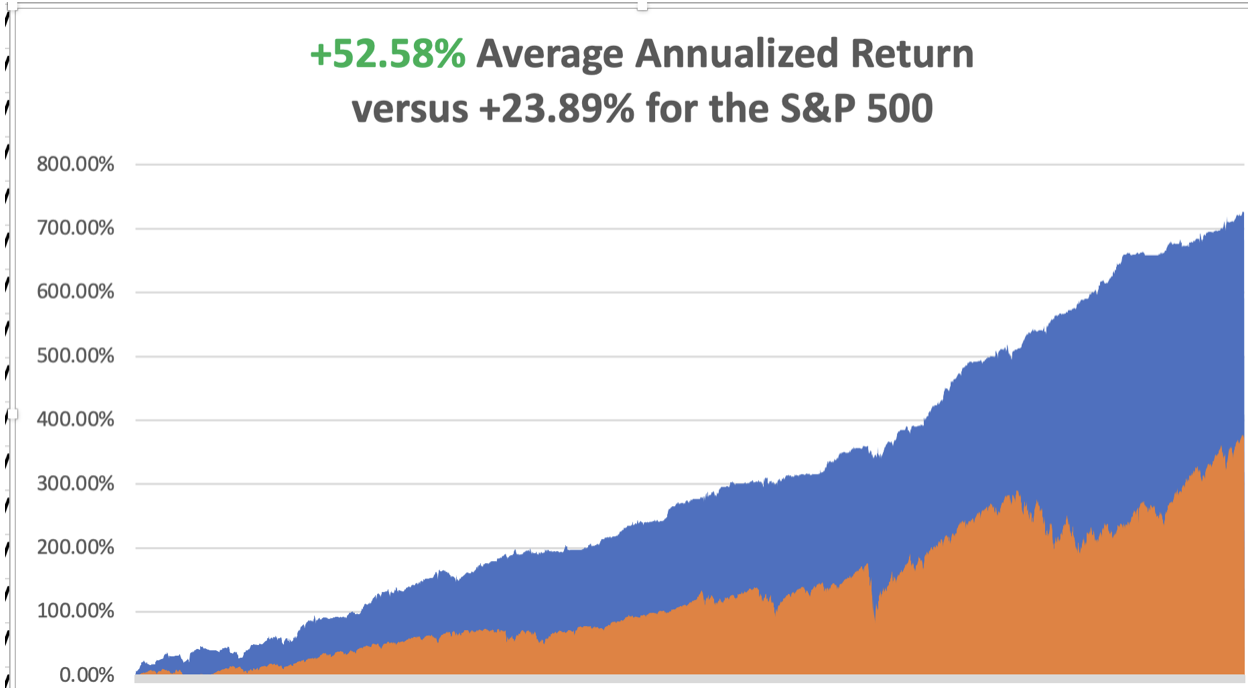

So far in October, we have gained a breathtaking +5.46%.My 2024 year-to-date performance is at an amazing+50.70%.The S&P 500 (SPY) is up +21.38%so far in 2024. My trailing one-year return reached a nosebleed +66.31. That brings my 16-year total return to +727.33%.My average annualized return has recovered to +52.58%.

I am remaining cautious with a 70% cash, a 20% long, and a 10% short. I maintained two longs in (GLD) and (JPM) that are well in the money. I sold short (TSLA) to take advantage of a massive 29% gain in two days off the back of blockbuster earnings.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 61 of 81 trades have been profitable so far in 2024, and several of those losses were really break evens. Some 16 out of the last 19 trade alerts were profitable. That is a success rate of +75.30%.

Try beating that anywhere.

New Home Sales Jumped 4.1% in September at 738,000 seasonally adjusted units on a signed contract basis. The median home price rose to 426,300. This despite a roller coaster month on interest rates, falling to 6.0% for the 30-year, then jumping back up to 7.0%.

Fusion is going Commercial in San Francisco, with a German company, Focused Energy, making a $65 million investment. The firm will draw heavily from staff from nearby Lawrence Livermore National Labs, which achieved a net energy gain for the first time in 2022. Focused Energy is one of eight companies given grants to accommodate a doubling of power demand by 2050. Commercial fusion will be the next big thing, where three soda cans of heavy hydrogen can power San Francisco for a day.

Money Market Funds See Massive Pre-Election Inflows, as investors see to avoid promised post-election violence. According to LSEG data, investors acquired a net $29.98 billion worth of money market funds during the week, posting their fourth weekly net purchase in five weeks. Personally, I think it is another Y2K moment.

Tesla Earnings Shock to the Upside, with both third-quarter profits and margins topping estimates. Elon Musk said that he expects 20% to 30% vehicle growth next year, sending the company's shares up 11% in post-market trading. The company still sees 2025 production of a cheaper model, maybe the Model 2. The Cybertruck has reached profitability for the first time and is reaching mass production. Tesla will see “slight growth” in deliveries this year. I am using the spike in the share price to take profits on my long to avoid election risk.

Apple iPhone Sales are Lagging, according to a leading analyst, with a drop in 10 million orders expected, down to 84 million units. The stock dropped 4% from an all-time high.

Boeing Reports $6 Billion Loss, a disastrous report from a dying company with awful management. This is going to be a very long-term workout. A strike resolution may market the bottom. Avoid (BAC) like a stalling airplane.

Newmont Mining Dives 7% after missing Wall Street expectations for third-quarter profit on Wednesday. Higher costs and lower production in Nevada took the shine away from a rise in total output. Newmont said that its costs rose due to planned maintenance at the Lihir project in Papua New Guinea — which it acquired following a $17 billion buyout of Newcrest — and higher expenditure for contract services across its portfolio. Buy (NEM) on dips.

McDonald's Kills Two in E.Coli Outbreak, linked to quarter pounders sold in Colorado and Nebraska. The stock dropped 10%. It’s clearly a supply chain problem. Given their vast size, with 45,000 stands in 100 countries, it’s amazing that this doesn’t happen more often. Avoid (MCD).

Bonds Plunge Anticipating a Trump Win, with the (TLT) down $10 from the recent high. If he does win, expect another $10 decline to $82. If Harris wins, expect a $10 rally. This is the best election trade out there.

Nvidia Tops $3.5 Trillion, as the shares hit a new all-time high at $144.45. It looks like it’s on a run to $150, then $160. Earnings are about to double when reported on November 20. Before then, investors will get some insight into demand for Nvidia’s newest Blackwell chips with earnings reports from big technology companies, including Microsoft (MSFT) coming at the end of this month. Buy (NVDA) on dips.

Hedge Funds Pour into Technology Stocks, such as semiconductors and hardware, at the fastest in five months amid the start of the third-quarter earnings season, according to Goldman Sachs on Friday. Outside the U.S., diverging reports from chipmaker Taiwan Semiconductor Manufacturing (TSM) and chipmaking equipment supplier ASML Holding (ASML) in opposite directions while investors await semiconductor companies such as Advanced Micro Devices (AMD) and Nvidia (NVDA) to unveil their earnings as they seek a trend. They are betting on a big post-election move-up.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy is decarbonizing, and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000, here we come!

On Monday, October 28 at 8:30 AM EST, the Dallas Fed Manufacturing Index is published. On Tuesday, October 29 at 6:00 AM, the S&P Case Shiller National Home Price Index is out. We also get the US JOLTS Job Openings Report. Alphabet (GOOGL) and (AMD) report.

On Wednesday, October 30 at 11:00 AM, the ADP Employment Change Report is printed. (META) and (MSFT) report.

On Thursday, October 31 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the US Core PCE Price Index. (AMZN) reports.

On Friday, November 1 at 8:30 AM, the October Nonfarm Payroll Report is announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, with silver on fire once again and at 12-year highs, I thought I’d recall the last time a bubble popped for the white metal. I picked up this story from my late friend Mike Robertson, who ran the Dallas-based Robertson Wealth Management, one of the largest and most successful registered investment advisors in the country.

Mike is the last surviving silver broker to the Hunt Brothers, who in 1979-80 were major players in the run-up in the “poor man’s gold” from $11 to a staggering $50 an ounce in a very short time. At the peak, their aggregate position was thought to exceed 100 million ounces.

Nelson Bunker Hunt and William Herbert Hunt were the sons of the legendary HL Hunt, one of the original East Texas wildcatters and heirs to one of the largest Texas fortunes of the day. Shortly after President Richard Nixon took the US off the gold standard in 1971, the two brothers became deeply concerned about financial viability of the United States government. To protect their assets, they began accumulating silver through coins, bars, the silver refiner, Asarco, and even tea sets, and when it opened, silver contracts on the futures markets.

The brother’s interest in silver was well-known for years, and prices gradually rose. But when inflation soared into double digits, a giant spotlight was thrown upon them, and the race was on. Mike was then a junior broker at the Houston office of Bache & Co., in which the Hunts held a minority stake and handled a large part of their business.The turnover in silver contracts exploded. Mike confesses to waking up some mornings, turning on the radio to hear silver limit up, and then not bothering to go to work because they knew there would be no trades.

The price of silver ran up so high that it became a political problem. Several officials at the CFTC were rumored to be getting killed in their personal silver shorts. Eastman Kodak (EK), whose black and white film made them one of the largest silver consumers in the country, was thought to be borrowing silver from the Treasury to stay in business.

The Carter administration took a dim view of the Hunt Brothers’ activities, especially considering their funding of the ultra-conservative John Birch Society. The Feds viewed it as an attempt to undermine the US government. The proverbial sushi hit the fan.

The CFTC raised margin rates to 100%. The Hunts were accused of market manipulation and ordered to unwind their position. They were subpoenaed by Congress to testify about their motives. After a decade of litigation, Bunker received a lifetime ban from the commodities markets, a $10 million fine, and was forced into a Chapter 11 bankruptcy.

Mike saw commissions worth $14 million in today’s money go unpaid. In the end, he was only left with a Rolex watch, his broker’s license, and a silver Mercedes. He still ardently believes today that the Hunts got a raw deal and that their only crime was to be right about the long-term attractiveness of silver as an inflation hedge. Nelson made one of the greatest asset allocation calls of all time and was punished severely for it. There never was any intention to manipulate markets. As far as he knew, the Hunts never paid more than the $20 handle for silver and that all of the buying that took it up to $50 was nothing more than retail froth.

Through the lens of 20/20 hindsight, Mike views the entire experience as a morality tale, a warning of what happens when you step on the toes of the wrong people.

The white metal’s inflation-fighting qualities are still as true as ever, and it is only a matter of time before prices once again take another run to the upside.

Unfortunately, Mike won’t be participating in the next silver bubble. Suffering from morbid obesity, he died from a heart attack a decade ago.

Silver is Still a Great Inflation Hedge

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/10/man-with-glasses.png606468april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-28 09:02:442024-10-28 11:23:59The Market Outlook for the Week Ahead, or Here is your Post Election Portfolio

Featured Trade: (The Mad Hedge December Traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GOLDILOCKS IS BACK!),

(TLT), (FCX), (CAT), (JNK), (HYG), (NLY), (GM), (MSFT), (NLY), (BRK/B), (CCJ), (GOOGL), (SNOW), (XOM), (CRM)

After too long of an absence, Goldilocks has moved back in once again. She arrived with Santa Claus too, a month ahead of schedule.

Can life get any better than that, Goldilocks and Santa Claus?

Santa confused Thanksgiving with Christmas this year. I saw it coming a mile off, and it’s not because my failing eyesight has suddenly improved.

Since October 26, Mad Hedge followers have earned an impressive 25%. We are on track to top an 86.5% profit for 2023, the best in the 15-year history of the service.

Concierge members who own our substantial LEAPS portfolio, now at 33 names, are up much more.

I hate to boast but let me take my victory lap. I earned it.

Stocks and bonds should continue rising but at a much slower rate. More likely is the diversification of the rally from Big Tech and big bonds (TLT) to medium tech, commodities (FCX), industrials (CAT), junk bonds (JNK), (HYG), and REITS (NLY).

Buy everything on dips.

And here are your assumptions. Collapsing energy prices will lead the inflation rate down to the Fed’s well-publicized 2% inflation rate target in the coming months. Accelerating technology and AI will reign in this year’s runaway wage increases, if not reverse them.

The UAW’s 25% salary increase over four years will only hasten the demise of General Motors (GM), as well as their own. Interest rates have to take a swan dive, supercharging all risk assets.

Goldilocks is not moving in for a fling, but a long-term relationship. Your retirement funds will love it.

Last spring, with 75 feet of snow over the winter, the rivers pouring out of the High Sierras were at record levels. That brought the solo hobbyist gold miners out in force.

It is widely believed that the 1849 gold rush extracted only 10% of the gold in the mountains and the remaining 90% is still up there. Heavy rainfalls like we received last winter flushed out some of the rest.

Rounding a turn in the river, I spotted a group of modern-day 49ers equipped with shoulder-high waders and inner tubes floating pumps and sluice boxes. So I parked the car and waded out in the freezing, fast-running water to get an update on this market.

One man proudly showed off a one-ounce gold nugget that he had found only that morning worth about $1,800. Nuggets are worth more than spot gold because they attract a collector’s market.

A record eight-ounce nugget was discovered in a river near Merced the week earlier. This year, the state government in Sacramento issued a record number of gold mining licenses.

I explained to my newfound friend that he should hang on to his gold because it would be worth a lot more the following year. Inflation was falling and that would eventually induce the Federal Reserve to cut interest rates sharply.

That meant less interest rate competition for gold and silver, which yielded nothing taking prices upward. Personally, I think this gold could hit $3,000 an ounce and silver $50 an ounce in 2025.

In addition, there was a constant bid from Russia, China, and North Korea looking to dodge financial sanctions. Money managers are also picking up the yellow metal as a hedge against any unanticipated volatility in 2024.

My friend looked at me quizzically, wondering if perhaps I was some kind of nutjob who had waded out mid-river to rob him of his prized nugget.

I’ll do anything to gain a trading edge, even freezing off my cajones.

It was a tough week for 90- and 100-year-olds with the passing of Charlie Munger, Henry Kissinger, and Supreme Court Justice Sandra Day O’Connor. I had the privilege of knowing all three.

I was in the White House Press Room one day when the press secretary James Brady asked if any of the press could ride a horse. Sheepishly, I was the only one to raise a hand.

I was ordered to pick up my riding boots and report to the White House Stables on 17th Street. I had no idea why. Back then, even the press didn’t ask some questions.

When I arrived, I understood why. Supreme Court Justice Sandra Day O’Connor was already there kitted out ready to ride. It turns out that the justice from Arizona rode weekly with Ronald Reagan. This week, an international crisis prevented the president from doing so. I was the fill-in escort.

We talked about growing up in the Colorado Desert, and pre-air conditioning, as we enjoyed a peaceful ride along the Potomac River. A security detail kept a safe distance.

A lot of history is being in the right place at the right time.

The clock is ticking.

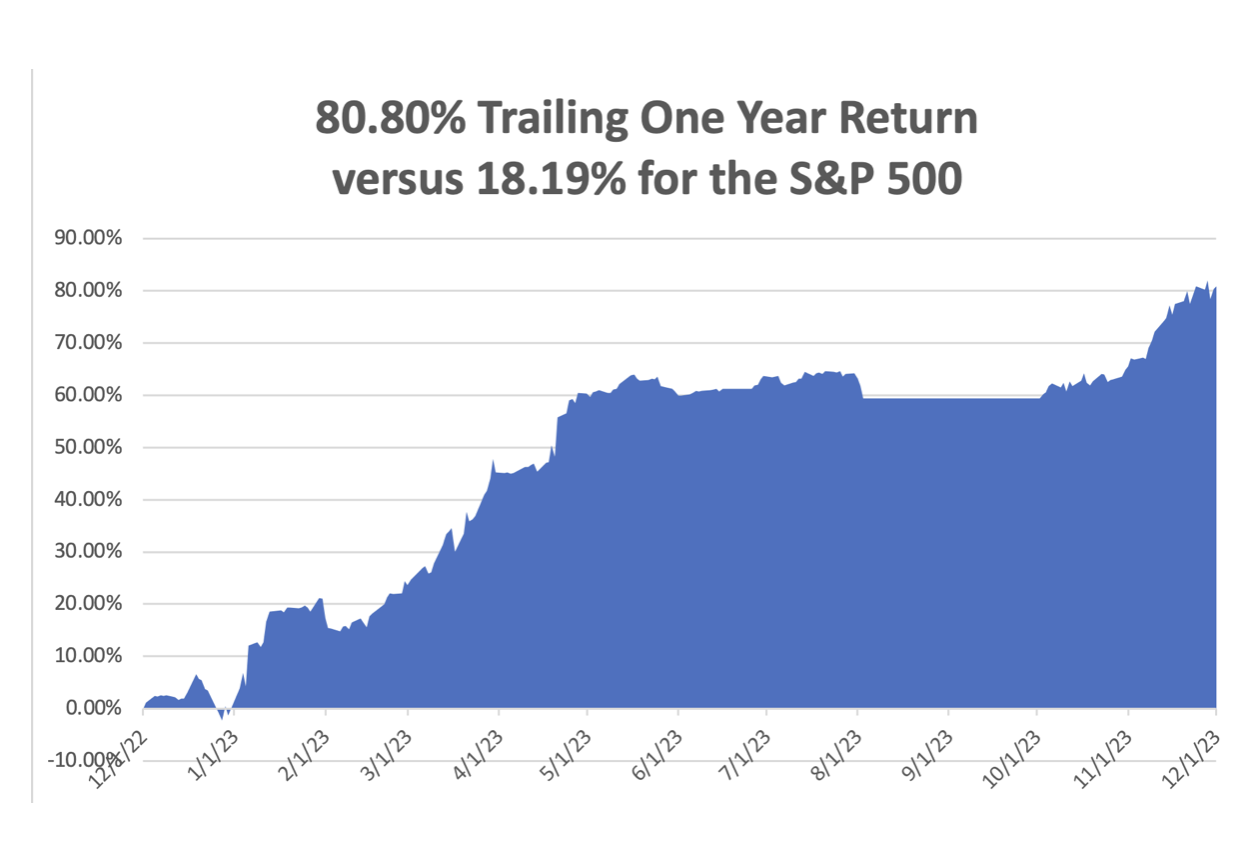

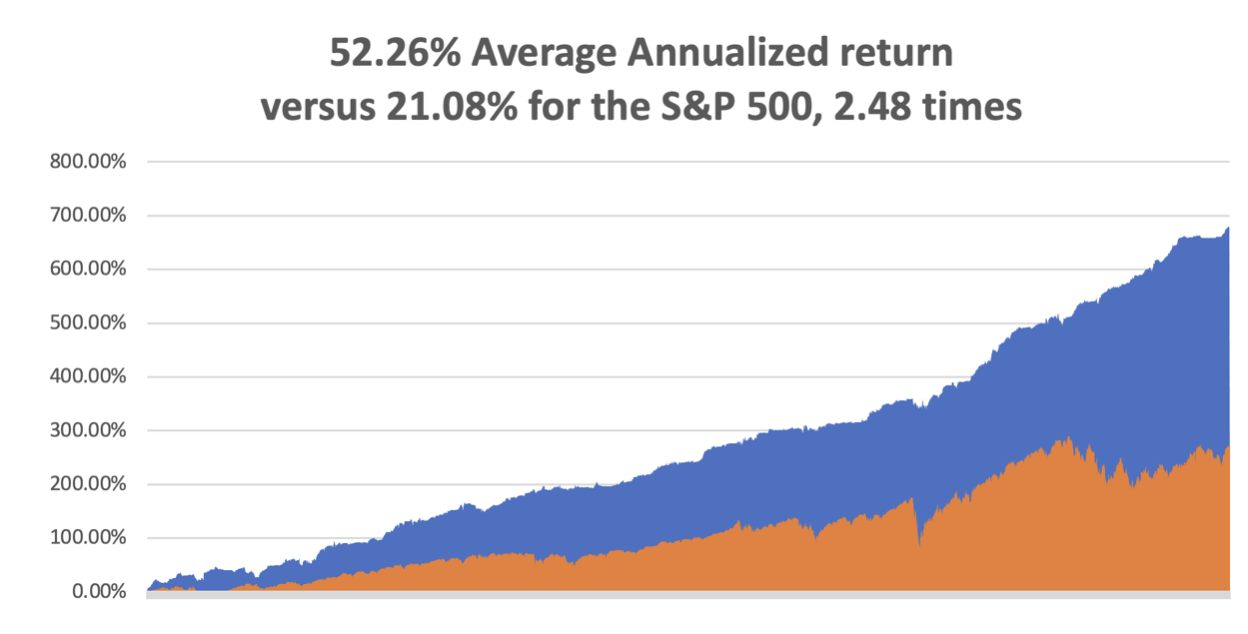

November closed out at +15.54%. My 2023 year-to-date performance is still at an eye-popping +81.71%.The S&P 500 (SPY) is up +19.73%so far in 2023. My trailing one-year return reached +80.80% versus +18.19% for the S&P 500.

That brings my 15-year total return to +678.90%. My average annualized return has exploded to +52.26%,another new high, some 2.48 times the S&P 500over the same period.

I am 90% fully invested, with longs in (MSFT), (NLY), (BRK/B), (CCJ), (GOOGL), (SNOW), (CAT), and (XOM). I have one short in the (TLT). I took profits on (CRM) on Friday.

Some 56 of my 61 trades this year have been profitable this year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, December 4, at 8:30 AM EST, the US Factory Orders are out.

On Tuesday, December 5 at 2:30 PM,the JOLTS Job Openings Report is released.

On Wednesday, December 6 at 8:30 AM, the ADP Private Employment Report is published.

On Thursday, December 7 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, December 8 at 2:00 PM the Baker Hughes Rig Count is printed and at 2:30 PM, the November Nonfarm Payroll Report is published.

As for me, back in the early 1980s, when I was starting up Morgan Stanley’s international equity trading desk, my wife Kyoko was still a driven Japanese career woman.

Taking advantage of her near-perfect English, she landed a prestige job as the head of sales at New York’s Waldorf Astoria Hotel.

Every morning we set off on our different ways, me to Morgan Stanley’s HQ in the old General Motors Building on Avenue of the Americas and 47th street and she to the Waldorf at Park and 34th.

One day, she came home and told me this little old lady living in the Waldorf Towers needed an escort to walk her dog in the evenings once a week. Back in those days, the crime rate in New York was sky-high, and only the brave or the reckless ventured outside after dark.

I said “Sure” “What was her name?”

Jean MacArthur.

I said THE Jean MacArthur?

She answered “Yes.”

Jean MacArthur was the widow of General Douglas MacArthur, the WWII legend. He fought off the Japanese in the Philippines in 1941 and retreated to Australia in a dramatic night PT Boat escape.

He then led a brilliant island-hopping campaign, turning the Japanese at Guadalcanal and New Guinea. My dad was part of that operation, as were the fathers of many of my Australian clients. That led all the way to Tokyo Bay where MacArthur accepted the Japanese in 1945 on the deck of the battleship USS Missouri.

The MacArthur then moved into the Tokyo embassy where the general ran Japan as a personal fiefdom for seven years, a residence I know well. That’s when Jean, who was 18 years the general’s junior, developed a fondness for the Japanese people.

When the Korean War began in 1950, MacArthur took charge. His landing at Inchon Harbor broke the back of the invasion and was one of the most brilliant tactical moves in military history. When MacArthur was recalled by President Truman in 1952, he had not been home for 13 years.

So it was with some trepidation that I was introduced by my wife to Mrs. MacArthur in the lobby of the Waldorf Astoria. On the way out, we passed a large portrait of the general who seemed to disapprovingly stare down at me taking out his wife, so I was on my best behavior.

To some extent, I had spent my entire life preparing for this job.

I had stayed at the MacArthur Suite at the Manila Hotel where they had lived before the war. I knew Australia well. And I had just spent a decade living in Japan. By chance, I had also read the brilliant biography of MacArthur by William Manchester, American Caesar, which had only just come out.

I also competed in karate at the national level in Japan for ten years, which qualified me as a bodyguard. In other words, I was the perfect after-dark escort for Midtown Manhattan in the early eighties.

She insisted I call her “Jean”; she was one of the most gregarious women I have ever run into. She was grey-haired, petite, and made you feel like you were the most important person she had ever run into.

She talked a lot about “Doug” and I learned several personal anecdotes that never made it into the history books.

“Doug” was a staunch conservative who was nominated for president by the Republican party in 1944. But he pushed policies in Japan that would have qualified him as a raging liberal.

It was the Japanese that begged MacArthur to ban the army and the navy in the new constitution for they feared a return of the military after MacArthur left. Women gained the right to vote on the insistence of the English tutor for Emperor Hirohito’s children, an American Quaker woman. He was very pro-union in Japan. He also pushed through land reform that broke up the big estates and handed out land to the small farmers.

It was a vast understatement to say that I got more out of these walks than she did. While making our rounds, we ran into other celebrities who lived in the neighborhood who all knew Jean, such as Henry Kissinger, Ginger Rogers, and the UN Secretary-General.

Morgan Stanley eventually promoted me and transferred me to London to run the trading operations there, so my prolonged free history lesson came to an end.

Jean MacArthur stayed in the public eye and was a frequent commencement speaker at West Point where “Doug” had been a student and later the superintendent. Jean died in 2000 at the age of 101.

I sent a bouquet of lilies to the funeral.

Kyoko passed away in 2002.

In 2014, Chinas Anbang Insurance Group bought the Waldorf Astoria for $1.95 billion, making it the most expensive hotel ever sold. Most of the rooms were converted to condominiums and sold to Chinese looking to hide assets abroad.

The portrait of Douglas MacArthur is gone too. During the Korean War, he threatened to drop atomic bombs on China’s major coastal cities.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/08/macarthur-family-e1661786429655.jpg345450april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-12-04 09:02:522023-12-04 09:30:03The Market Outlook for the Week Ahead, or Goldilocks is Back!

Dealing with the Cloud works, and for every relevant tech company, this division serves as the pipeline to the CEO position.

If this isn’t the case for a tech company, then there’s something egregiously wrong with them!

Take Andy Jassy, the mastermind behind Amazon’s (AMZN) lucrative cloud computing division and the man who succeeded company founder Jeff Bezos.

He was rewarded with this important position based on his performance in the cloud and faced the daunting proposition of following Bezos as CEO.

Bezos incorporated Amazon almost 30 years ago.

Jassy developed a highly profitable and market-leading business, Amazon Web Services, that runs data centers serving a wide range of corporate computing needs.

Cloud 101

If you've been living under a rock for the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape, or form.

Amazon leads the cloud industry it created.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon relies on AWS to underpin the rest of its businesses and that is why AWS contributes most of Amazon's total operating income.

Total revenue for just the AWS division would operate as a healthy stand-alone tech company if need be.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day.

If you work in Silicon Valley, you can quadruple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations.

Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that is where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained, and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

No Maintenance

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing the IT staff of prima donnas.

Greater Flexibility

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them work remotely which effectively happened because of the public health situation. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

Better Collaboration and Communication

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Data Protection

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

And we haven’t talked about the ransomware attacks by Eastern Europeans on energy company Colonial Pipeline and meat producer JBS Foods.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

Lower Overhead

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time, and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

The cloud is where you want to be.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-12-01 14:02:292023-12-01 11:13:43The Place To Be

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.