Mad Hedge Technology Letter

July 2, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Mad Hedge Technology Letter

July 2, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape or form.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose from 10% to 13% and is catching up to Amazon Web Services (AWS).

Amazon leads the cloud industry it created, and the 49% growth in cloud sales from the 42% in Q3 2017 is a welcome sign that Amazon is not tripping up.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes 73% to Amazon's total operating income.

Total revenue for just the AWS division is an annual $5.5 billion business and would operate as a healthy stand-alone tech company if need be.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day. If you work in Silicon Valley you can triple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy remember that the original Department of Defense packet switching design was intended to make the system atomic bomb proof.

As a user you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at anytime from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved through letting them telecommute. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees. According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document, so they can stay on top of real-time changes, which can help businesses to better manage work flow, regardless of geographical location.

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

_________________________________________________________________________________________________

Quote of the Day

"Life is not fair; get used to it," said founder of Microsoft Bill Gates.

Mad Hedge Technology Letter

June 25, 2018

Fiat Lux

Featured Trade:

(IT'S NOT HEAVEN FOR ALL CLOUD STOCKS)

(ORCL), (MSFT), (AMZN), (CRM), (GOOGL)

The year of the Cloud takes no prisoners.

Cloud stocks have been on a tear resiliently combating the leaky macro environment.

Many of my cloud recommendations have been outright winners such as Salesforce (CRM).

However, there are some unfortunate losers I must dredge up for the masses.

Oracle (ORCL) announced quarterly earnings and it was a real head-scratcher.

I have been banging on the table to ditch this legacy tech company since the inception of the Mad Hedge Technology Letter.

It was the April 10, 2018 tech letter where I prodded readers to stay away from this stock like the black plague.

At the time, the stock was trading at $45, click here to revisit the story "Why I'm Passing on Oracle."

The first quarter was disappointing and abysmal guidance of 1% to 3% for annual total revenue topped off a generally underwhelming cloud forecast.

Investors spotlight one part of the business requiring the utmost care and nurturing - its cloud business.

The second quarter was Oracle's chance to revive itself demonstrating to investors it is serious about its cloud direction.

What did management do?

They announced a screeching halt to the reporting of cloud revenue and it would avoid reporting on specific segments going forward.

Undoubtedly, something is wrong behind the scenes.

To withdraw financial transparency is indicative of Oracle's failure to pivot to the cloud and this has been my No. 1 gripe with Oracle.

It is simply getting pummeled by the competition of Amazon (AMZN), Alphabet (GOOGL), and Microsoft (MSFT).

Stuck with an aging legacy business focused on database software, transformation has been elusive.

To erect a giant cloak around its cloud business means that growth is far worse than initially thought to the point where it is better to sweep it under the carpet.

Instead of taking a direct hit on the chin, management decided to wriggle itself out of the accountability of bad cloud numbers.

A glaringly bad cloud business should be the cue for management to kitchen sink the whole quarter and start afresh from a lower base.

The preference to shroud itself with opaqueness is bad management. Period.

Instead of turning over a new leaf, Oracle could be penalized on future earnings reports for the way it reports financials for the simple reason it confuses analysts.

Wars were fought for less.

Bad management runs bad companies. The stock has floundered while other cloud stocks have propelled to new heights - another canary in the coal mine.

Amazon and Netflix are two examples of tech growth stocks that have celebrated all-time highs.

Even rogue ad seller Facebook broke to all-time highs lately.

The champagne is flowing for the top-level tech companies.

As expected, Oracle was punished heavily upon this news with the stock down almost 8% intraday to $42.70, and it sits throttled at $43.60 as I write this.

Diverting attention from the cloud will mire this stock in the malaise it deserves. Shielding its investors from the only numbers that really matter will give analysts a great reason to label this dinosaur stock with sell ratings.

Analysts are usually horrific stock predictors, but they will be able to wash their hands of this beleaguered stock.

Even if the stock goes up, analysts will still be geared toward sell ratings.

Oracle reported a $1.7 billion in total cloud revenue last quarter, a disappointing 9% increase QOQ.

Oracle's cloud revenue is only up 25% YOY.

For an up and coming cloud business, the minimum threshold to please investors is 20% QOQ, and the 9% QOQ expansion will do nothing to get investors excited.

The deceleration of growth is frightening for investors to stomach and Oracle's admission the cloud business is uncompetitive will detract many potential buyers from dipping in at these levels.

In short, Oracle is not growing much. There is no reason to buy this stock.

I always divert subscribers into the most innovative tech stocks because they are most in demand from investors.

Innovative inertia has reverberated through the corridors at its massive complex in Redwood City, California.

A major shake out in product development and business strategy is vital for Oracle clawing back to relevance.

This is the fourth sequential quarter with unhealthy guidance.

Much of the weakness comes from Amazon siphoning business out of Oracle.

Completed surveys suggest the conversion to AWS has one clear loser and that is Oracle.

Cloud vendors are now ramping up their smorgasbord of cloud offerings attracting more business.

The second and third cloud players, Alphabet and Microsoft, have been particularly active in M&A, attempting to make a run at AWS for pole position.

It is most likely that Oracle's capital spending will dip from $2 billion in 2017 to $1.8 billion in 2018.

Considering Salesforce spent $6.5 billion on MuleSoft, a software company integrating applications, an annual $1.8 billion capital expenditure outlay is a pittance and shows that Oracle is functioning at a pitiful scale.

Oracle won't be able to make any noteworthy transactions with such a miniscule budget.

Without enhancing its cloud offerings, Oracle will fall further behind the vanguard exacerbating cloud deceleration.

Oracle pinpointed data center expansion as the targeted cloud segment after which they would chase. Oracle will quadruple two data centers in the next two years.

One of the data centers will be placed in China collaborating with Tencent Holdings Limited to satisfy government rules requiring outsiders partnering with local companies.

Saudi Arabia is locked in for a data center, desperate to attract more tech ingenuity to the kingdom.

Saudi Arabia's iconic state-owned oil giant will form an "Aramco-Google partnership focused on national cloud services and other technology opportunities."

It will be interesting going forward to analyze the stoutness of the data center commentary considering foes such as Alphabet are boosting spending.

Alphabet quarterly spend tripled to $7.56 billion QOQ including the $2.4 billion snag of New York's Chelsea Market skyscraper Google will spin into new offices.

Alphabet has splurged on $30 billion on digital infrastructure alone in the past three years.

That bump up in infrastructure spending is to support the spike in computer power needed for the surging growth across Alphabet's ecosystem.

Apparently, Oracle is not experiencing the same surge.

If investors start to question global growth, investors will migrate into the top-grade names and the marginal names such as Oracle will be taken behind the woodshed and beaten into submission.

Oracle is much more of a sell the rally than buy the dip stock fueled by its growth deceleration challenges.

_________________________________________________________________________________________________

Quote of the Day

"If you don't have a mobile strategy, you're in deep turd," - said Nvidia CEO Jensen Huang.

Mad Hedge Technology Letter

June 19, 2018

Fiat Lux

Featured Trade:

(TRAVIS IS BACK!),

(UBER), (RDFN), (Z), (LEN), (CRM), (MSFT), (AAPL)

Travis Kalanick is back in full force after his Uber fiasco.

His creation kicked him to the curb preferring a more rigid approach to corporate governance as the 2019 IPO draws closer.

It didn't take much time for him to take stock of his piggy bank.

Yes, the $1.4 billion payout he received means he has nothing to do with Uber anymore.

Some piggy bank.

Travis intends to wield this wad aggressively using his new fund "10100" as his finance vehicle to pounce on hot, new tech names.

Travis doesn't know any other way, and investors should be alert to where he turns to find his new Uber and his new baby.

Future foes should understand Kalanick is one of the most feared disruptors on the face of the earth.

He co-founded Uber in 2009 growing it into the premier transportation platform.

The whirlwind few years launched him from a nobody to one of the premier tech names in Silicon Valley.

So, what's the deal?

What I can tell you is that house prices are about to get a whole lot pricier and there is nothing you can do about it.

Travis Kalanick's investment into house flipping app Opendoor will be the first stage of a torrential stampede of tech capital flowing into this sector.

More importantly, it's a sign of intent by Kalanick.

The real estate industry is the unequivocal prehistoric dinosaur that hasn't changed for decades.

It's almost a matter of time before the process of buying a house becomes digitized, either partially or fully.

Remember, Uber functions as a broker app matching drivers and passengers through a platform built on algorithmic software.

It would make logical sense for tech companies to attack the low-hanging fruit - meaning every industry that places brokers at the heart of business.

The broker app software is tried and tested with a gold stamp of approval. It works, and tech executives understand how to monetize the data.

Traditional brokers would get pummeled in this scenario, as the data applied to a new real estate broker app would eclipse anything a real human would be able to accomplish removing human error.

Real estate is next on disruption pecking order, and tech is coming for its bacon because of the huge sums of money associated with American real estate.

The real estate industry is not a scooter sharing business and requires boat loads of money to get ahead.

Tech has the cash but needs to figure out execution and its future road map.

The bulk of tech capital has been funneled into M&A that has seen tech companies pay multiples above what were guessed as fair value.

Share buybacks have been another hot source of investment.

Opendoor is a house-flipping firm intent on changing the status quo.

The business model entails snapping up distress properties, fixing them up, and selling them for a profit.

Opendoor receives a 6% commission for facilitating this whole process.

Opendoor has already served 20,000 customers saving more than 400,000 of prep time.

It is already on the hook for $1.5 billion in loans. SoftBank's vision fund is knocking on the door eager to become the next investor.

In 2016, this company was valued at $1 billion and after the latest round of financing giving Opendoor another $325 million, that number has crept up to $2 billion.

I have heard from solid sources that the SoftBank capital could be delivered in the next few months, likely paying another solid premium boosting tech valuations across the board.

Paying up has been a universal theme in 2018.

Microsoft's (MSFT) purchase of GitHub and Salesforce's (CRM) purchase of MuleSoft seem like overpaying but appear cheap in hindsight.

With the new cash ready to deploy, Opendoor seeks to expand to 50 cities by 2020, a swift upward jolt from its current 10 cities.

Not only will tier 1 cities feel the brunt of this new development, Opendoor plans to go into the lesser known cities and plans to double its staff from 650 to 1,300 in the upcoming year.

Kalanick caught onto this investment opportunity after one of his former Uber minions, Gautam Gupta, made the jump to Opendoor as COO and liaised CEO Eric Wu with Kalanick to hash out a deal.

It's nice to have friends in high places as Kalanick knows very well.

Even traditional home builders are getting in on the venture capitalist act.

Lennar was one of the investors in the latest round of Opendoor investment, underscoring the existential threat these traditional companies face.

It makes more sense to partner now and form a budding relationship than get utterly wiped out down the road.

Uber hopes to deploy this strategy with Waymo as Kalanick's former company knows it will never possess superior self-driving technology over Waymo.

The Lennar investment also gave Jon Jaffe, the COO of home builder Lennar, a seat on Opendoor's board.

Opendoor is the first serious tech foray into the housing business. It is initiating business on the periphery by focusing on fixer uppers.

This will allow Opendoor to cut its teeth and learn more about the industry before it migrates into higher margin business such as downtown condos that Millennials love.

A swift migration of other tech names will briskly follow into this undisrupted industry if Opendoor can pry open its floodgates.

Fixing up distressed houses is the gateway into brokering and the holy grail of constructing.

Tech could eventually wipe out everyone and control the whole process just like what investors have seen in the transportation industry.

I can imagine a future where tech companies will be the best firms to construct smart houses, which all houses will eventually become.

One massive aftereffect is that the average quality of housing will rise dramatically in all metropolitan areas.

Once the data amasses, Opendoor will be able to identify every property from where it can extract value allowing America to transform into a nation of pristine, smart houses.

Renovating a house and selling it will boost the prices of current houses.

Effectively, tech with gentrify housing creating higher quality but higher priced properties.

Millennials, who have had an awful time jumping on the property ladder, will have an even more difficult task finding a starter home if every starter house turns into a beautiful Tuscan-styled villa from a shabby shed.

Vice-versa, beautiful Tuscan-styled villas that cannot be "flipped" will become smart homes creating even more demand for IoT smart products and higher prices per square foot.

Andreessen Horowitz, a venture capitalist firm based in Menlo Park, California, has been one of the avant-garde tech investors seizing stakes in Twitter, Facebook, Skype, Coinbase, and Lyft.

And these were just some of its investments before 2014!

An industry where Travis Kalanick, SoftBank, and Andreesen Horowitz are piling in must have real estate agents shivering in their wake.

If the general trend keeps up, the Oracle of Omaha Warren Buffett could be next on this powerful list.

He usually likes to buy things he understands with healthy cash flow. I am sure he understands real estate more than Apple (AAPL), in which he had no problem investing.

Traditional home builders and real estate agents aren't the only players that could be left in the dust.

Zillow (Z), the online real estate database company, reacting from the Opendoor threat launched its new business to buy and sell homes.

It was only three years ago that Zillow CEO Spencer Rascoff determinedly hunkered down telling investors "we sell ads, not houses."

Innovation, tech disruption, and competition changes everything.

The stock sold off hard due to the exorbitant costs related to buying homes on the announcement of buying and selling houses.

Margins will get massacred in this scenario, but I applaud the decision to move up higher on the value chain diminishing the existential threat.

This whole industry is about to be flipped on its head, and the winners will be the most innovative companies that incorporate data best.

Rascoff further expanded saying, "I can say without exaggeration, that no company understands the American homebuyer and home seller better than Zillow Group."

Zillow is 12 years old and the12-year treasury trove of data will give it an optimal chance to pivot from selling ads to buying and selling houses.

Seattle-based Redfin (RDFN), Zillow's arch nemesis competitor founded in 2004, has an even larger treasure trove of data dating back 14-plus years and has moved in the same direction.

Redfin was anointed the top tech company to work for in Seattle in 2017 by Hired.com.

There is enormous potential to add another monstrous business to Redfin and Zillow's top line.

The real estate industry is next in line to be digitized, and the Mad Hedge Technology Letter will be the first to know when it's time to dip your toe in.

_________________________________________________________________________________________________

Quote of the Day

"As a tech entrepreneur, I try to push the limits. Pedal to the metal," - said former cofounder of Uber Travis Kalanick.

Mad Hedge Technology Letter

May 31, 2018

Fiat Lux

Featured Trade:

(HOW SALESFORCE RAN OVER ORACLE),

(CRM), (ORCL), (MU), (RHT), (MSFT), (INTC), (AMZN), (GOOGL)

Modern tech has an unseen dark side to it.

Coders relish the opaqueness surrounding the industry infatuated with developing the next big thing to take Silicon Valley by storm.

There is nothing opaque about the Mad Hedge Technology Letter.

I grind out recommendations and you follow them. Period. End of story.

To put it mildly, the letter has gotten off to a flying start since its inception in February 2018, and there is no looking back, only looking forward.

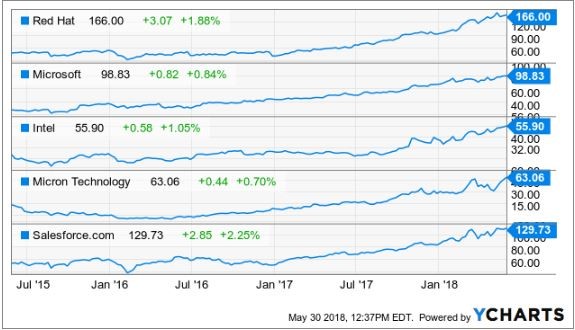

Micron (MU), Red Hat (RHT), Microsoft (MSFT), and Intel (INTC), just to name a few, have been solid recommendations standing up to all the nonsense and mayhem permeating throughout the periodically irrational markets.

Have you noticed lately when you open up the morning paper while sipping on a steaming mug of Blue Bottle Coffee, that almost every story is about technology?

It's not a mistake. I swear.

Technology is permeating into the nooks and crannies of our society and the leaders of this movement are laughing all the way to the bank.

One of those aforementioned pioneers is no other than local lad, Salesforce CEO and perennial Facebook basher Marc Benioff.

I recommended Salesforce at $110 and it was one of the first positions in the Mad Hedge Technology portfolio.

You can't blame me.

I saw this stock pick from a million miles away and I will explain why.

Salesforce set ambitious targets that nobody thought were realistic at the time.

How high in the sky does Benioff want to build his castles?

By 2022, Marc Benioff set out sales targets of a colossal $20 billion per year.

Then Benioff gushed that Salesforce would pass the $40 billion mark, done and dusted by 2028 and $60 billion by 2034.

Remember that tech CEOs are incentivized to forecast ludicrous sales targets because it lures in the unknowledgeable investor.

Unknowledgeable or pure genius, it does not matter, Salesforce is an emphatic buy.

Salesforce is the ultimate growth stock.

In 2016, annual revenue came in at $6.67 billion, which is about the same size as a middle level semiconductor company.

They followed that up with $8.38 billion in 2017, demonstrating the parabolic shaped trajectory of the company.

At the end of fiscal year 2017, Salesforce announced that it expects revenue of around $12.60 billion in 2019.

The latest earnings report, Benioff disclosed full year guidance of $13.13 billion.

This puts Salesforce in the running to achieve its lofty aspirations.

Apparently, the castles Benioff is building aren't in the sky after all.

Theoretically, if Benioff expands the business into a $16 billion to $16.5 billion business by 2019, Salesforce will have a more than likely chance to pass the $20 billion mark by the end of 2020, a full two years than initially thought.

Salesforce will have ample wiggle room on the way to $20 billion if it is 2022 for which it aims.

Why am I rambling on about revenue?

It's the only metric that Salesforce investors value.

The company registered two straight years of less than $200 million in profits then followed it up with a less than stellar 2016 where it lost almost $50 million.

Don't expect any dividends from this neck of the woods anytime soon especially after acquiring MuleSoft, an integration software company, for $6.5 billion last quarter.

This purchase will add another $315 million of annual revenue to Salesforce's quest of eclipsing its future sales targets. This was after MuleSoft made $296.5 million in 2017 before it became a part of Marc Benioff's stable.

Benioff has proved a shrewd dealmaker, taking advantage of cheap capital to add suitable parts to his business.

Since 2016, Benioff has snapped more than 50 niche software companies that he rebrands as Salesforce products and sells them as add-on products.

This is further evidence that any funds available will be allocated toward reinvestment into products and services deeming any future dividend inconceivable, especially with the elevated revenue targets to surpass.

As for the business. Do we still need to talk about it?

Rip-roaring growth was seen across the board with total revenue increasing 25%.

Investors should stay away from any cloud company that is growing less than 20%.

Market intelligence firm International Data Corporation (IDC) voted Salesforce as the No. 1 client relationship management (CRM) platform for the fifth consecutive year.

It is the industry leader in sales, marketing, service, and increased market share in 2017, more than its closest competitors.

Larry Ellison must be tearing his hair out as Oracle's (ORCL) share price has been excommunicated to purgatory indefinitely.

Oracle is a company that I have been pounding on the tables to stay away from.

The Mad Hedge Technology Letter seldom recommends legacy companies that are still legacy companies.

Driving past his former estate, emanating from a sparkling perch in Incline Village overlooking Lake Tahoe, my neighbor gives me the goose bumps.

The property was later sold for $20.35 million. All told, Larry has around $100 million invested in real estate dotted around Incline Village. I sarcastically mentioned to him last time we bumped into each other to call me immediately when his $90 million estate in Kyoto, Japan, hits the market.

Oracle's position in the pecking order is a telltale sign of the inability to land the creme de la creme government contracts that ostensibly fall into Amazon (AMZN), Alphabet (GOOGL), and Microsoft's lap.

And it's not surprising that Larry is spending more time tending to his vast array of glittering luxury properties around the world rather than running Oracle.

Oracle is like a deer caught in the headlights and Marc Benioff is at the wheel.

On the Forbes 500 rankings, Salesforce has moved up almost 200 spots.

This position will rise as Salesforce is under contract booking a further $20.4 billion of commitments driven by its subscription services offering cloud products.

On the domestic contract front, it was much of the same for Salesforce, which inked premium deals with the U.S. Department of Agriculture, Kering, and sports apparel giant Adidas.

International companies such as Philips and Santander UK are expanding their relationships with Salesforce. A firm nod of approval.

Salesforce has been voted in the top three of most innovative companies for the past eight years by reputable Forbes magazine. The list was started in 2011, and it has never dropped out of the top three.

The gobs of innovation are the main logic behind the top five financial institutions expanding their relationship with Salesforce by an extra 70%.

Once companies start using the CRM platform, they become mesmerized with the premium add-ons that help companies run more efficiently.

Benioff has been a huge proponent of artificial intelligence (A.I.) and is an outsized catalyst to product enhancement gains.

Salesforce has taken Einstein, it's A.I. platform, and allowed all the applications to run through it.

The integration of Einstein has resulted in more than 2 billion correct predictions per day paying homage to the quality of A.I. engineering on display.

Instead of hiring a whole team of in-house data scientists, Salesforce is A.I. functionality by the bucket full and it is easy to use on its platform.

In some cases, incorporating Salesforce's A.I. into the business has bolstered other companies' top line by 15%.

Often, Salesforce's A.I. tools are declarative meaning the technology can identify solutions without a fixed formula.

Benioff has choreographed his strategy perfectly.

He is betting the ranch on unlocking data from legacy companies that migrate to his platform.

MuleSoft will help in this process of extracting value, then A.I. will supercharge the data, which is being unlocked.

What does this mean for Salesforce?

Higher revenue and more clients leading to accelerated growth. The share price has powered on north of $130, and after I recommended it at $110, I am convinced this stock will surge higher.

Salesforce is an absolute no-brainer buy on the dip.

Growth Means Shiny New Office Buildings

_________________________________________________________________________________________________

Quote of the Day

"If we become leaders in Artificial Intelligence, we will share this know-how with the entire world, the same way we share our nuclear technologies today." - said current President of Russia, Vladimir Vladimirovich Putin.

Mad Hedge Technology Letter

May 8, 2018

Fiat Lux

Featured Trade:

(BUFFETT GOES ALL IN WITH APPLE),

(SNAP), (WDC), (GOOGL), (AMZN),

(CRM), (RHT), (HPQ), (FB), (AAPL)

Not every stock comes with Warren Buffett's confession that he would like to own 100% of it. But, of course that stock would have to be a tech stock.

As it stands, the Oracle of Omaha owns 5% of Apple (AAPL), and his confession is still a bold statement for someone who seldom forays outside his comfort zone.

Buffett also continues to concede that he "missed" Google (GOOGL) and Amazon (AMZN).

What a revelation!

The outflow of superlatives invading the airwaves is indicative of the strength technology has assumed in the bull market.

The tech sector has been coping with obstacles such as higher interest rates, trade wars, data regulation, IP chaos, and the globalization backlash.

However, the tech companies have come through unscathed and hungry for more.

Their power is not contained to one industry, and techs' capabilities have been spilling over into other sectors digitizing legacy industries.

Every CEO is cognizant that enhancing a product means blending the right amount of tech to suit its needs.

It is not halcyon times in all of tech land either.

There have been some companies that have faltered or were naturally cannibalized by other tech companies that disrupt business.

Times are ruthless and this is just the beginning.

There will be winners and losers as with most other secular paradigm shifts.

Particularly, there are two types of losers that investors need to avoid like the plague.

The first is the prototypical tech company hawking legacy products such as Western Digital Corp. (WDC) that I have been banging on the table telling investors not to buy the stock.

The lion's share of revenue is still in the antiquated hard drive business that has a one-way ticket to obsolescence.

Yes, they are turning around product mixes to factor in its pivot to solid state drives (SSD), but they are late to the game and deservedly punished for it.

Compare WDC to companies that have completed the transition from legacy reliance to the cloud, and it is simple to understand that companies such as Microsoft, which struggled for years to turn around with CEO Satya Nadella, finally can claim victory.

The problem with WDC is the stock's price action performs miserably because the company is tagged as an ongoing turnaround story.

On the other hand, headliner cloud plays experience breathtaking gaps up due to the strength of the cloud such as Amazon (AMZN), Red Hat (RHT), and Salesforce (CRM), just to name a few.

To pour fuel on the fire, speculative reports citing NAND chip price "softening" beat down the stock into submission.

Effectively, legacy companies become sell the rallies type of stocks.

Transforming a legacy company into a high-octane cloud company is perilous to say the least. Jeff Bezos recently gloated that Amazon Web Service's (AWS) seven-year head start is all investors need to know about the cloud. There is some merit to his statement.

Examples are rife with bad executive decisions by legacy companies such as HP Inc. (HPQ), another legacy tech company that makes computers and hardware. It ventured out to buy Palm for $1.2 billion plus debt after a bidding war with legacy competitor Dell in 2010.

In 1996, the Palm PDA (Personal Digital Assistant) was the first smart phone on the market that predated BlackBerry's smart phone with the full keyboard made by RIM (Research in Motion).

The demise of Palm emerged from a hodgepodge of mismanagement, failed spin-offs, misplaced mergers, and resource wastefulness even with the preeminent technology of its time.

(HPQ)'s stab at the smartphone market resulted in purchasing Palm. However, after heavy selling pressure in its shares, HP shut down this division and sold off the remaining technology to Chinese electronics company TCL Corporation.

The sad truth is many transformations fail at step one, and there is no guarantee a newly absorbed business will perform as expected.

RIM, now changed to BlackBerry (BB), soon found out how it felt to be Palm when Steve Jobs dropped the first iPhone on the market, and the world has never been the same.

(BB) gradually morphed into an autonomous vehicle technology company after the writing was on the wall.

The other types of losers are companies with inferior business models such as Snapchat (SNAP), which I have written about extensively from the bearish side.

In an age where disruptors are being disrupted by other disruptors, CEOs must live in fear that their business will get undercut and hijacked at any time.

Instagram, a subsidiary of Facebook (FB), has permanently borrowed numerous features from Snapchat. Its Instagram "stories" feature is now used by more than 300 million daily users.

Snapchat is serving as Instagram's guinea pig while CEO Evan Spiegel finds an alternative way to survive against Facebook's unlimited resources.

Both are in the game of selling ads and nobody does it better than Facebook and Alphabet or has the degree of scale.

The recent redesign was met with a chorus of universal boos. The 60 minutes I spent testing the new design reconfirmed my fears that the new design was an unmitigated washout.

In short, Snap's redesign seemed like a different app and became incredibly difficult to use.

Compounding the deteriorating situation, Snapchat laid off 120 engineers due to sub-par performance and withheld last year's performance bonuses even though co-founder Evan Spiegel received $637 million in 2017.

The latest earnings report was a catastrophe.

Daily active user (DAU) growth, the most sought out metric for Snapchat, failed to deliver the goods. The street expected 194.2 million DAU and Snap reported 191 million. A miss of 3.2 million users and a deceleration of growth QOQ.

Remember that Snapchat is substantially smaller than Instagram and should have no problems surpassing expectations on a smaller scale, thus investors voted with their feet and bailed on the stock after the catatonic performance last quarter.

Instagram is six times larger with more than 800 million users as of the end of 2017.

Top line fell short of expectations and average revenue per user (ARPU) dropped to $1.21, far less than the expected $1.27.

The less than stellar redesign faced a rebellion from long-term Snapchat disciples. More than 1.2 million Snap diehards signed a petition hoping to revert back to the old interface, and its updated ratings in Apple's app store has fallen to 1.6 stars out of 5.

Then the perpetual question of why would advertisers want to pay for Snapchat digital ads when they earn more by buying Instagram ads?

This remains unsolved and appears unsolvable.

Snapchat is befuddled by the pecking order and the company is on a train to nowhere.

To hammer the nail in the coffin, Snapchat announced to investors that it expects revenue to "decelerate substantially" next quarter.

In an era where technology companies will lead the economy and stock market, and has an outsized influence in politics and culture, not all tech companies are one-foot tap-ins.

Investors need to separate the wheat from the chaff or risk losing their shirt.

_________________________________________________________________________________________________

Quote of the Day

"We have to stop optimizing for programmers and start optimizing for users." - said American software developer Jeff Atwood