Mad Hedge Technology Letter

April 17, 2018

Fiat Lux

Featured Trade:

(WHY THE CLOUD IS WHERE TRADING DREAMS COME TRUE),

(ZS), (ZUO), (SPOT), (DBX), (AMZN), (CSCO), (CRM)

Mad Hedge Technology Letter

April 17, 2018

Fiat Lux

Featured Trade:

(WHY THE CLOUD IS WHERE TRADING DREAMS COME TRUE),

(ZS), (ZUO), (SPOT), (DBX), (AMZN), (CSCO), (CRM)

Dreams don't often come true - but they do frequently these days.

Highly disruptive transformative companies on the verge of redefining the status quo give investors a golden chance to get in before the stock goes parabolic.

Traditional business models are all ripe for reinvention.

The first phase of reformulation in big data was inventing the cloud as a business.

Amazon (AMZN) and its Amazon Web Services (AWS) division pioneered this foundational model, and its share price is the obvious ballistic winner.

The second phase of cloud ingenuity is trickling in as we speak in the form of companies that focus on functionality, performance, and maintenance on the cloud platform.

This is a big break away from the pure accumulation side of stashing raw data in servers.

However, derivations of this type of application are limitless.

Swiftly identifying these applied cloud companies is crucial for investors to stay ahead of the game and participate in the next gap up of tech growth.

The markets' reaction to Spotify's (SPOT) and Dropbox's (DBX) hugely successful IPOs was head-turning.

Both companies finished the first day of trading firmly well above their respective, original opening prices -- or for Spotify, the opening reference price.

The pent-up momentum for anything "Cloud" has its merits, and these two shining stars will give other ambitious cloud firms the impetus to go public.

If Spotify and Dropbox laid an egg, momentum would have screeched to a juddering halt, and companies such as Pivotal Software would reanalyze the idea of soon going public.

Now it's a no-brainer proposition.

There are more than 40 more public cloud companies that are valued at more than a $1 billion, and more are in the pipeline.

To understand the full magnitude of the situation, evaluating recent IPO performance is a useful barometer of health in the tech industry.

The first company Zscaler (ZS) is an enterprise company focused on cloud security that closed 106% above its opening price when it went public this past March 16.

It opened up at $16 a share and finished the day at $33.

Zscaler CEO, Jay Chaudhry, audaciously rebuffed two offers leading up to the March 16 IPO. Both offers were more than $2 billion, and both were looking to acquire Zscaler at a discount.

The decision to forego these offers was a prudent move considering (ZS)s current market cap is around $3.3 billion and rising.

One of the companies vying for (ZS) was Cisco Systems (CSCO), which is also in the cloud security business. Cisco is looking to add another appendage to its offerings with the cash hoard it just repatriated from abroad.

Cisco has been willing to dip into its cash hoard by buying San Francisco-based AppDynamics for $3.7 billion in 2017, which specializes in managing the performance of apps across the cloud platform and inside the data center.

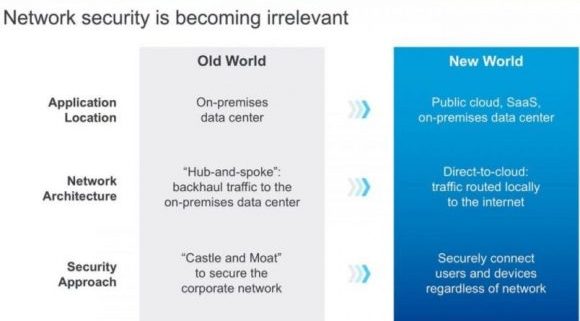

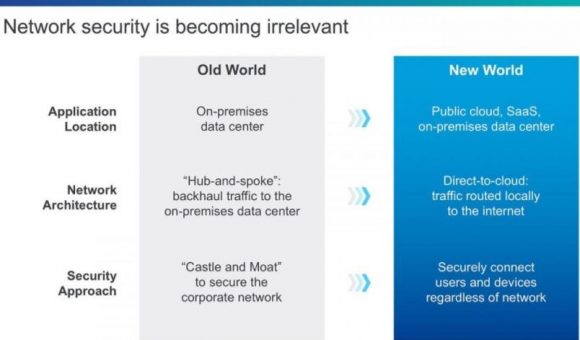

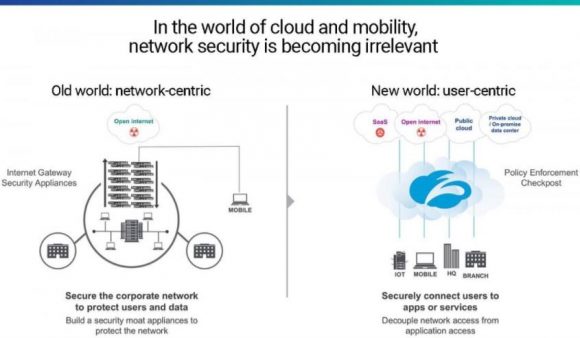

Cloud security is critical for outside companies to feel comfortable implementing universal cloud technology.

Storing sensitive data online in a storage server is also a risk and difficult to migrate back once on the cloud.

Without solid security to protect data, data-heavy companies will hesitate to vault up their data in a public place and could remain old-school with external data locations storing all of a firm's secrets.

However, this traditional approach is not sustainable. There is just too much generated data in 2018.

Cybersecurity has expeditiously evolved because hackers have become greatly sophisticated. Plus, they are getting a lot of free PR.

Data center and in-house applications secured operations by managing access and using an industrial strength firewall.

This was the old security model.

Security became ineffective as companies started using cloud platforms, meaning many users accessed applications outside of corporate networks and on various devices.

The archaic "moat" method to security has died a quick death, as organizations have toiled to ziplock end points that offer hackers premium entry points into the system.

Zscaler combats the danger with a new breed of security. The platform works to control network traffic without crashing or stalling applications.

As cloud migration accelerates, the demand for cloud security will be robust.

Another point of cloud monetization falls within payments.

Tech billing has evolved past the linear models that credit and debit in simplistic fashion.

SaaS (Software as a Service), the hot payment model, has gone ballistic in every segment of the cloud and even has been adopted by legacy companies for legacy products.

Instead of billing once for full ownership, companies offer an annual subscription fee to annually lease the product.

However, reoccurring payments blew up the analog accounting models that couldn't adjust and cannot record this type of revenue stream 10 to 20 years out.

Zuora (ZUO) CEO Tien Tzuo understood the obstacles years ago when he worked for Marc Benioff, CEO of Salesforce (CRM), during the early stages in the 90s.

Cherry-picked after graduating from Stanford's MBA program, he made a great impression at Salesforce and parlayed it into CMO (Chief Marketing Officer) where he built the product management and marketing organization from scratch.

More importantly, Tzuo built Salesforce's original billing system and pioneered the underlying system for SaaS.

It was in his nine years at Salesforce that Tzuo diagnosed what Salesforce and the general industry were lacking in the billing system.

His response was creating a company to seal up these technical deficits.

Other second derivative cloud plays are popping up, focusing on just one smidgeon of the business such as analytics or Red Hat's container management cloud service.

SaaS payment model has become the standard, and legacy accounting programs are too far behind to capture the benefits.

Zuora allows tech companies to seamlessly integrate and automate SaaS billing into their businesses.

Tzuo's last official job at Salesforce was Chief Strategy Officer before handing in his two-week notice. Benioff, his former boss, was impressed by Tzuo's vision, and is one of the seed investors for Zuora.

These smaller niche cloud plays are mouthwateringly attractive to the bigger firms that desire additional optionality and functionality such as MuleSoft, integration software connecting applications, data and devices.

MuleSoft was bought by Salesforce for $6.5 billion to fill a gap in the business. Cloud security is another area in which it is looking to acquire more talent and products.

If you believe SaaS is a payment model here to stay, which it is, then Zuora is a must-buy stock, even after the 42% melt up on the first day of trading.

The stock opened at $14 and finished at $20.

One of the next cloud IPOs of 2018 is DocuSign, a company that provides electronic signature technology on the cloud and is used by 90% of Fortune 500 companies.

The company was worth more than $3 billion in a round of 2015 funding and is worth substantially more today.

These smaller cloud plays valued around $2 billion to $3 billion are a great entry point into the cloud story because of the growth trajectory. They will be worth double or triple their valuation in years to come.

It's a safe bet that Microsoft and Amazon will continue to push the envelope as the No. 1 and No. 2 leaders of the industry. However, these big cloud platforms always are improving by diverting large sums of money for reinvestment.

The easiest way to improve is by buying companies such as Zuora and Zscaler.

In short, cloud companies are in demand although there is a shortage of quality cloud companies.

__________________________________________________________________________________________________

Quote of the Day

"The great thing about fact-based decisions is that they overrule the hierarchy." - said Amazon founder and CEO, Jeff Bezos

Mad Hedge Technology Letter

April 10, 2018

Fiat Lux

Featured Trade:

(WHY I'M PASSING ON ORACLE),

(ORCL), (MSFT), (AMZN), (CRM)

To say 2018 is the Year of the Cloud is an understatement.

Oracle (ORCL) felt the tremors of investors' fickle preference for quality cloud growth when the stock sold off hard after earnings that were relatively solid but unspectacular.

Oracle is a Silicon Valley legacy firm established in 1977 under the name of Software Development Laboratories. The company was co-founded by Larry Ellison, Bob Miner, and Ed Oates and the name later was changed to Oracle.

The company made its name through database software and still relies on it for the bulk of its $37 billion in annual revenue.

Legacy companies are put through the meat grinder by investors, and analysts are micro-sensitive to just a few narrow-defined metrics.

Not all cloud companies are treated equally.

It has become consensus that the only way to move forward is through advancing the cloud model, and neglecting this segment is a death knell for any quasi-cloud stock.

Oracle skirted any sort of calamitous earnings performance but left a lot to be desired.

Cloud SaaS (software-as-a-service) revenue for the quarter was $1.2 billion, up 21% YOY, and growth rates were in line with many that are part of the winners' bracket.

Oracle's overall cloud business is still a diminutive piece of its overall business constituting just 16%, which is incredibly worrisome.

This number accentuates the lack of brisk execution and its late entrance into this industry.

Gross cloud margin only increased 2% to 67%, up from 65% QOQ, providing minimum incremental growth.

Total cloud revenue guidance was substantially weak, which includes SaaS, PaaS (platform-as-a-service) and IaaS (infrastructure-as-a-service) expected to grow 19% to 23% in 2018, much less than the forecasted guidance of 27%.

Oracle should be growing its cloud segment faster, especially since its cloud business is many times smaller than competition, and growing pains habitually occur later in the growth cycle.

The outsized challenge is attempting to leverage its foundational database business to convince existing corporate clients to adopt Oracle's in-house cloud services instead of diverting capital toward cloud offerings from Microsoft (MSFT), Salesforce (CRM), or Amazon (AMZN).

It could be doing a better job.

Weak guidance of 1%-3% for annual total revenue topped off a generally underwhelming cloud forecast.

The lack of over-performance is highly disappointing for a company that has been touting its pivot to cloud.

The message from Oracle is the transformation is nowhere close to finished. That was investors' queue to stampede for the exits.

Investors only need to look a few miles up the coast at the competition.

Salesforce is putting up solid numbers, and many cloud companies are judged solely on a relative basis to the industry leaders.

The turnaround companies are getting crushed by these growth magnates. Salesforce is sequentially increasing total revenue over 20% each quarter and expects total revenue to rise more than 20% in 2019. It has set ambitious revenue targets for 2020, 2030, and 2040.

Microsoft Azure grew cloud revenue 98% QOQ, and Microsoft Windows, its legacy business, only makes up 42% of Microsoft's total revenue and is shrinking by the day.

Microsoft has earned its positon as the King of the Legacy Businesses offering proof by way of its position as the industry's second-best cloud company, engineering cloud quarterly revenue of $7.8 billion and gaining on Amazon Web Services (AWS).

Microsoft was in the same situation as Oracle a few years ago, stuck with a powerful business in a declining industry. It then turned to the cloud and never looked back.

Instead of leveraging databases, Microsoft leveraged its operating system and proprietary software to persuade new clients to adopt its cloud platform - and the numbers speak for themselves.

Oracle still has the chance to pivot toward the cloud because its database product is a brilliant entrance point for potential cloud converts.

In the meantime, Amazon has its sights set on Oracle's database product and plans to go after market share.

Oracle believes its database product is the best in the business - more affordable, quicker, and dependable. However, technology is evolving at such a rapid pace that these nimble companies can flip the script on their opponents in no time.

It's a dangerous proposition to compete with Amazon because of the nature of competing means dumping products, and unlimited cash burn battering opponents into submission by crushing profitability.

Oracle's margins would get hammered in this circumstance at a time when Oracle's gross margins have been a larger sore spot than first diagnosed.

Legacy companies are unwilling to enter price wars with Amazon because they still have dividends to defend and profit margins to nurture skyward.

Concurrently, Salesforce and Microsoft Dynamics CRM are attacking Oracle's CRM products (Customer Relationship Management), which could further impair margins.

The breadth of competition showed up to the detriment of margins with PaaS and IaaS gross margins eroding from 46% YOY, down to 35% YOY.

Microsoft's cloud revenue eked out a better than 60% gross margin even with its gargantuan size.

Investors punished Oracle for whispers of its cloud business plateauing with a size that is just a fraction of Microsoft Azure.

The leveling out is hard to take after Larry Ellison claimed cloud margins would soon breach 80% in upcoming quarters.

Conversely, Microsoft has claimed margins could start to erode as the company reallocates capital into expanding its cloud infrastructure, but it is understandable for maturing companies that must battle with the law of large numbers.

At the end of the day, Oracle's cloud business is failing to grow enough.

Oracle's competitors are speeding down the autobahn while Oracle has been dismissed to the frontage road.

Growth impediments with the small size of Oracle's cloud business is a red flag.

Avoid this legacy turnaround story that hasn't turned around yet.

Oracle looks like a value play at this point and could rise if it gets its cloud act together or the mere anticipation of a resurgence.

But with margins and competition pressuring its attempts at transformation, I would take a wait-and-see approach.

It's clear that Oracle is in the third inning of its turnaround, and teething problems are expected.

If you get the urge to suddenly buy cloud stocks, better look at any dip from Microsoft, Salesforce, and Amazon, which all directly compete with Oracle but are performing at a much higher level.

__________________________________________________________________________________________________

Quote of the Day

"A company is like a shark, it either has to move forward or it dies." - said Oracle co-founder Larry Ellison.

Mad Hedge Technology Letter

April 4, 2018

Fiat Lux

Featured Trade:

(SPOTIFY KILLS IT ON LISTING DAY),

(SPOT), (DBX), (GOOGL), (AAPL), (AMZN), (CRM), (NFLX), (FB)

The banner year for the cloud continues as Dropbox's (DBX) blowout IPO passed with flying colors.

Investors' voracity for anything connecting to big data continues unabated.

Big data shares are now fetching a big premium, and recent negative news has highlighted how important big data is to every business.

Let's face it, Spotify (SPOT) needs capital to reinvest into its platform to achieve the type of scale that deems margins healthy enough to profit, even though it says it doesn't.

Big data architecture takes time to cultivate, but more importantly it costs a huge chunk of money to construct a platform worthy enough to satisfy consumers.

The daunting proposition of competing with the FANGs for users only makes sense if there is a reservoir of funds to accompany the fight.

Spotify CEO Daniel Ek has milked the private market for funding, making himself a multibillionaire in the process. And as another avenue of capital raising, he might as well go to the public to fund the venture in the future.

Cloud and big data companies have identified the insatiable investor appetite for their services. Crystalizing this sentiment is Salesforce's (CRM) recent purchase of MuleSoft - integration software that connects apps, data, and devices - for 18% more than its original offer for $6.5 billion.

The price was so exorbitant, analysts speculated that a price war broke out, but Salesforce paid such a high price because it is convinced that MuleSoft will triple in size by 2021. That is another great trading opportunity missed by you and me.

An 18% premium to the original price will seem like peanuts in five years. The year 2018 is unequivocally a sellers' market from the chips up to the end product and everything in between on the supply chain.

Spotify cannot make money if it's not scaled to 150 million users, compared to its current 76 million. And 200 million and 300 million would give CEO Daniel Ek peace of mind, but it's a hard slog.

Pouring gas on the fire, Spotify is going public at the worst possible time as tech stocks have been the recipient of a regulatory witch hunt pounding the NASDAQ, sending it firmly into correction territory.

Next up was Spotify's day to shine in the sun directly listing its stock.

Existing investors and Spotify employees are free to unload shares all they want, or load up on the first day. In addition, no new shares are being issued. This is unprecedented in the history of new NYSE listings.

Spotify is betting on its brand recognition and massive desire for big data accumulation. It worked big time, with a first day's closing price of $149, verses initial low ball estimates of $49.

Cloud companies are the cream of the big data crop, but Spotify's data hoard will contain every miniscule music preference and detail a human can possibly exhibit for potentially 100 million-plus people.

Spotify's data will become the most valuable music data in the world and for that it is worth paying.

But at what price?

Spotify has no investment bankers, and circumnavigating the hair-raising fees a bank would earn is a bold statement for the entire tech industry.

Sidestepping the traditional process has ruffled some feathers in the financial industry.

The mere fact that Spotify has the gall to execute a direct listing is just the precursor to big banks being phased out of the profitable investment banking sector.

Goldman Sachs (GS) was the lead advisor on Dropbox's (DBX) traditional IPO, and it was a resounding success rocketing 40% a few days after going public.

IPOs are not cheap.

The numbers are a tad misleading because Spotify paid about $40 million in advisory to the big investment banks leading up to the big day.

This is about a $28 million less than when Snapchat (SNAP) went public last year.

Uber and Lyft almost certainly would consider this option if Spotify nails its IPO day.

Banks are being squeezed from all sides as nimble, unregulated tech firms have proved better adaptable in this quickly changing environment.

Spotify's business model is based on spectacular future growth, which may occur.

It is a loss-making company that produces no proprietary solutions but is overlooked for its valuable data.

The company is the market leader in paid subscribers at 76 million, far outpacing Apple Music at 39 million and Pandora at 5.5 million.

Total MAUs (Monthly Active Users) expect to reach more than 200 million users, and paid subscribers could hit the 96 million mark by the end of 2018.

Spotify's business model bets on transforming the free subscribers who use Spotify with ad-supported interfaces into paid subscribers that are ad-free. Converting a small amount would be highly positive.

Gross margin is a number that sheds light on the real efficiencies of the company, and Spotify hopes to hit the 25% gross margin point by the end of 2018.

I am highly skeptical that gross margins can rise that high unless they solve the music royalty problem.

Royalty costs are killer, forcing Spotify to shell out a massive $9.75 billion in music royalties since its inception in 2006.

Spotify is paying too much for its content, but that is the cruel nature of the music industry.

The ideal solution would eventually amount to producing high quality original entertainment content on its proprietary platform akin to Netflix's (NFLX) business model with video content.

Spotify's capital is being drained by royalty fees amounting to 79% of its revenue.

This needs to be stopped. It's a losing strategy.

Considering Google (GOOGL) and Facebook (FB) do not pay for their own content, it frees up capital to pile into the pure technical side of the operations, enhancing their ad platforms luring in new users.

This is why the Mad Hedge Technology Letter sent you an urgent Trade Alert to buy Google yesterday when it was trading at $1,000.

All told, Spotify has managed to lose $2.9 billion since it was created 12 years ago - enough capital to create a new FANG in its own right.

Dropbox was an outstanding success and attaching itself to the parabolic cloud industry is ingenious.

However, potential insane volatility should temper investors' expectations for the first day of trading.

The lack of a road show, no lockup period, and no underwriting or book building will sacrifice stability in the short term.

There is incontestably a place for Spotify, and the expected 30% to 36% growth in 2018 looks attractive.

But then again, I would rather jump into sturdier names such as Lam Research (LRCX), Nvidia (NVDA), and Amazon (AMZN) once markets quiet down.

The private deals that took place before the IPO changed hands were in the range of $99 to $150. Considering the reference point will be set at $132, nabbing Spotify under $100 would be a great deal.

The market will determine the opening price by analyzing the buy and sell orders for the day with the help of Citadel Securities.

It's a risky proposition that 91% of shares are tradable upon the open. Theoretically, all these shares could be sold immediately after the open.

Legging into limit orders below $140 is the only prudent strategy for this gutsy IPO, but better to sit and observe.

__________________________________________________________________________________________________

Quote of the Day

"One of the only ways to get out of a tight box is to invent your way out." - Amazon CEO Jeff Bezos