Mad Hedge Technology Letter

June 4, 2021

Fiat Lux

Featured Trade:

(RIDING THE COATTAILS OF ELLIOT MANAGEMENT)

(DBX), (TWTR), (EBAY), (CRM), (BOX)

Mad Hedge Technology Letter

June 4, 2021

Fiat Lux

Featured Trade:

(RIDING THE COATTAILS OF ELLIOT MANAGEMENT)

(DBX), (TWTR), (EBAY), (CRM), (BOX)

Renowned Vulture Fund Elliott Management is at it again, looking to feast on the frail like the predator fund it is.

It was recently announced they own a large stake in cloud provider Dropbox (DBX) and has been holding private discussions with the file-sharing service provider for some time.

The hedge fund owns a stake of more than 10% which is valued at more than $800 million, the source said, declining to reveal the exact size of the investment.

Dropbox currently has a market cap of around $11 billion.

This is a cloud company that allows users to store documents, videos, and photos online, listed its shares in March 2018 at $21 a share.

Elliott has previously gotten their way at other tech companies like Twitter (TWTR) and eBay (EBAY).

Now Elliott Management is assumed to own the second biggest holding in Dropbox after CEO Drew Houston.

Elliot’s previous 13-F filing form has shown they are scooping up shares of Dropbox.

Dropbox shares also gained in March on news of a potential takeover that never came to fruition, and it smells a lot like that was Elliot.

I have heard other analysts mention Dropbox as a short-listed acquisition candidate for a handful of big players.

An acquisition looked close especially after Salesforce (CRM) announced the purchase of Slack Technologies and it’s logical that Dropbox could have been a retaliation purchase for a bigger tech company looking to keep pace with Salesforce's acquisitive thirst.

Elliot Management overtook Vanguard Group Inc. as the largest shareholder outside of Houston. Vanguard had a stake just below 10% as of March 31, according to Bloomberg.

The hedge fund has not made it clear whether it is seeking board seats on Dropbox’s board or other changes at the company.

But I will tell you there is a standard playbook that Elliot loves to roll out each time they buy into a tech company.

These changes almost always revolve around switching management and squeezing out more efficiencies in operations.

They even threatened Founder and CEO of Twitter Jack Dorsey to become more attuned to revenue acceleration so he could keep his job.

There are those who want to play the moral compass card out there, but I can say that almost any tech company Elliot Management has bought into experience a significant boost in asset appreciation 3-6 months after the acquisition.

Elliot is hyper-targeted in what they do, and they usually seek out management who has become too comfortable in their routine.

I believe they do not go after tech companies if they feel they cannot boost the underlying stock shares by 30% within a year.

They have a brilliant track record and any tech investor who doesn’t want to overcomplicate tech investing buys the same tech companies Elliot acquires.

Why?

Because changes are in the pipeline and every management or board seat change is usually met with a 5-7% surge in share price.

What’s not to like about that?

Then there are many up days on the operational front from cutting costs, and forcing through other changes that are first and foremost beneficial for the stakeholders of the company.

Other vulture fund specialists do this too like Starboard Value when they launched a proxy fight earlier this year at Box (BOX), where it has nominated four directors for the three seats that are coming available this year.

To play it simple, buy into Dropbox on the next dip and hold onto shares for the first part of the turnaround.

Once the pace of changes starts to plateau, by then, you should already have a decent-sized profit and can dump the shares.

Mad Hedge Technology Letter

June 2, 2021

Fiat Lux

Featured Trade:

(WHEN TO GET BACK INTO SALESFORCE?)

(CRM), (SONO), (HON), (SAP)

Looking for that optimal balance between growth and profitability is the ideal but of course if a tech firm in that state is also leaning towards driving growth...

That company is Salesforce (CRM) and it looks attractive now after pulling back from its peak.

Investing in growth, especially in this insatiable demand environment, is simply the best thing a tech firm can do for a company.

That said, I am also a staunch believer that a focus on discipline makes for a stronger and more durable company.

Over the long term, I believe tech firms need to be able to deliver both revenue acceleration and versatility in its revenue acceleration.

That shows up for Salesforce in the $3.2 billion in cash flow on $5.96 billion in revenue which adds up to being up 74% year over year.

CRM’s numbers reflect a strong performance since the onset of the public health situation and their operating margin is producing almost as if it was completely redesigned from the bottom up.

CRM has raised its operating margin to 18% and they are on track to doing $50 billion by 2025.

Then there are unbelievable stories to digest that make readers understand the true power of CRM.

The Sonos (SONO) story is just one to absorb — they just had this 84% growth when they went to consumer using CRM products.

More importantly, how to integrate operations with a cloud platform is at the forefront of every CEO’s thinking.

This takes looking at the trends of this past year and again, the individual stories where CRM has made that big difference, like the Honeywell (HON) story when they shifted 7,000 salespeople from in-person to virtual customer meetings — customer meetings aren't going back to conference rooms only.

Then when the business environment dictates that CRM is helping through the Service Cloud, together with Field Service and Experience Cloud to enable Honeywell to seamlessly dispatch technicians for on-site product maintenance and proactive asset management, connected service partner experiences, and customer experience for scheduling appointments and instantly solving troubleshooting problems.

It’s field service capability that helped CRM to amplify an already close-knit relationship with Honeywell, and that's when management started to collaborate and say, wow, we could bring this to the aviation business in Honeywell to transform and streamline the work they do via the cloud.

To succeed in the all-digital work-anywhere world enabling you to digitize your entire customer experience and get back to growth is the overarching goal in this incredible 2021 economy.

The outperformance really stretches across the portfolio. When we talk about the fact that of the seven-figure deals, they, on average, included more than four of CRM cloud services, meaning they are not selling individual products.

CRM’s AI Einstein started doing over 100 billion predictions per day. And it's a great example of these platform investments that CRM did multiple years ago that customers and the whole economy go digital are benefiting from.

It means every email is more personalized and every e-commerce you paid for is suited to your interest and your needs, driving growth and success for customers.

MuleSoft is now doing 4.86 billion integration transactions every day. That is up 28% quarter over quarter.

Integrating these legacy systems so customers can move faster in the face of an economy that’s shifting more rapidly than ever before shows the importance of CRM’s acquisitions as it relates to the overall value proposition of Customer 360.

Total revenue for the first quarter was $5.96 billion, up 23% year over year and CRM’s vertical strategy continues to align products to strategic industries.

In particular, we saw strength in the public sector, which continues to accelerate as governments around the world turn to Salesforce Solutions. Service Cloud demonstrated another quarter of incredible growth at scale with Q1 revenue of $1.5 billion, growing 20% year over year, and Tableau continues to perform well.

In Q1, Tableau was in eight of CRM’s top 10 deals for the company and in more than 60% of seven-figure plus deals.

The company expects Q2 revenue of $6.23 billion or approximately 21% growth year over year and CRM even raised annual revenue guidance by $250 million.

They are about to pass SAP as the largest enterprise applications company in the world. And all the analysts have their models. I know they track SAP and Salesforce.

It really shows the whole world is going digital, and customers are connecting with their customers in a new way, and everyone needs CRM to do it or get left behind.

They also need CRM’s analytics — they need integration and CRM just happens to be the leader in that area.

CRM has undergone an M&A consolidation after heavily paying for acquisitions. This earnings report signaled to investors to expect these headwinds to drop off towards the end of the year and since the stock market is forward-looking, CRM will start to transform into the buy the dip tech firm it was once before these expensive acquisitions took place.

Readers should keep an eye out for Salesforce for really any substantial pullback and long-term, this software company is a reliable revenue accumulator with a strong brand name.

Global Market Comments

May 24, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or IT'S ALL ABOUT THE NUMBERS),

(TLT), (SPY), (FCX), (QQQ), (VIX), (UUP), (AMAT), (CRM), (GOOG), (AMZN), (AAPL), (FB)

I know that not all of you are mathematicians, nor blessed with math degrees from UCLA, as I am. However, the future of your retirement funds relies on a few simple numbers. So, I will try to be gentle.

S&P tech stocks are trading at a 27 price earnings multiple. The S&P 500 Index, as a whole, trades at a 21 multiple. S&P value stocks, financials, and old-line recovery stocks like industrials and materials are trading at a 17 multiple.

Historically, companies with double the earnings power of the index trade at a 5-point premium to the main market. As long as this disparity exists, tech stocks will go down and value with go up.

However, we are getting close to a reversal. Allowing for market noise, I don’t see tech dropping more than 10% from here over the coming months. Then we will see the mother of all Q4 rallies taking it to new highs.

That explains why investors have been nibbling on tech lately, especially the best ones like NVIDIA (NVDA), Applied Materials (AMAT), and Salesforce (CRM). You also want to pick up big cap money machines like Alphabet (GOOG), Amazon (AMZN), Apple (AAPL), and Facebook (FB). Their LEAPS are begging for attention.

That means the downside from here is limited. Sorry Cassandras, no crashes here.

I am more convinced of this outcome than ever, given the substantial number of crashes and disasters, markets have weathered this year. These are truly Teflon markets. Last week, Bitcoin collapsed an amazing 55% in six weeks, wiping $1 trillion off the value of that market.

The fear had been that a crypto crash of this size would ignite a system contagion that would take everything down. A few years ago, it would have. But with massive Fed liquidity and unprecedented deficit spending, all we got was down 600 points one day and 600 up the next.

No crash here.

We’ve also had smaller crashes in sectors that were the most egregiously overpriced in February, like SPACS, meme stocks, and shares trading at 100 times sales with no earnings. Again, no harm no foul. It was a comeuppance that was well earned.

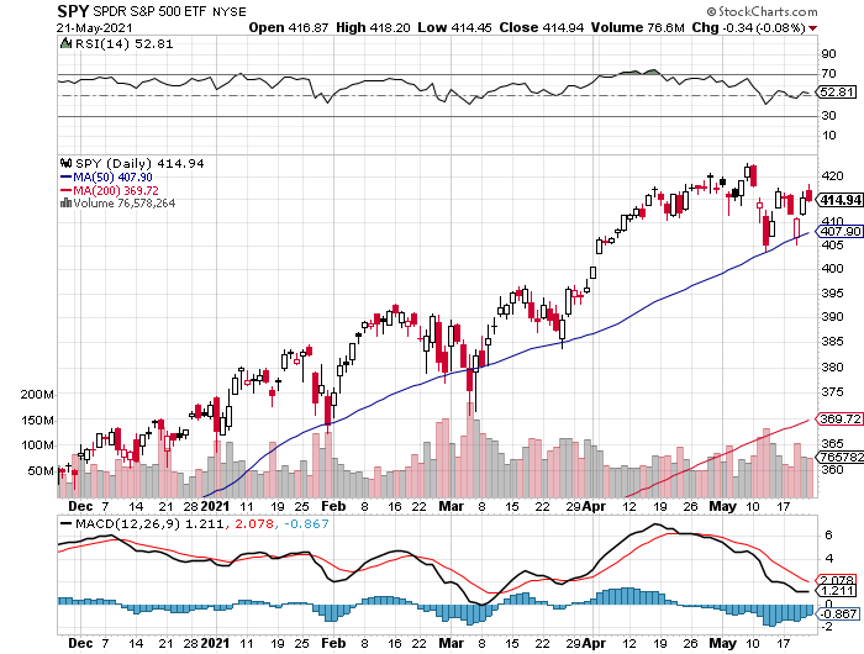

The big tell that I am right came screaming loud and clear last week from the US dollar, which hit a new 2021 low. A cheaper greenback means cheaper US stocks for foreign investors, which means they buy more of them. A weak buck also means that interest rates will stay lower for longer, which is great news for stocks, especially tech.

So, take it easy for the next few months. Keep positions small and rejoin the human race.

It seems odd going out into civilization and seeing live people walking around without masks. All the batteries on my watches are dead, as they have not been used for nearly two years, so they are getting replaced. I walked into my closet, and it was like adventuring into an archeological dig, with dozens of Turnbull & Asser shirts untouched by human hands. I’ve been living in Marine Corps sweats since 2019.

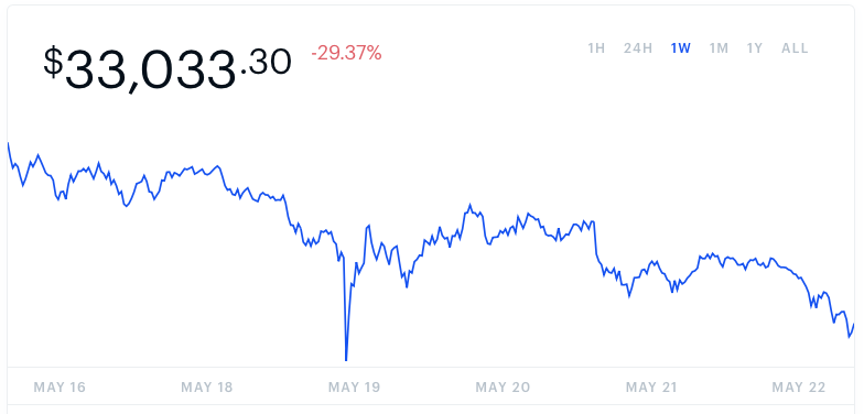

Bitcoin Crashes, down 33% on the day at the lows to $30,000, and off a heart-palpitating 55% from the April high. You wanted volatility, you got volatility! The problem for the rest of us is whether this will cause a real systemic financial crisis, with the Dow already down 560 at today’s low. Was Elon Musk the shoeshine boy giving tips at the market top?

Chip Shortage causes $110 Billion in US Car Industry Sales, in 2021 and will take years to address. Supply chains will need to be rebuilt. My neighbor just had to wait 11 months to take delivery of his Ford F-150.

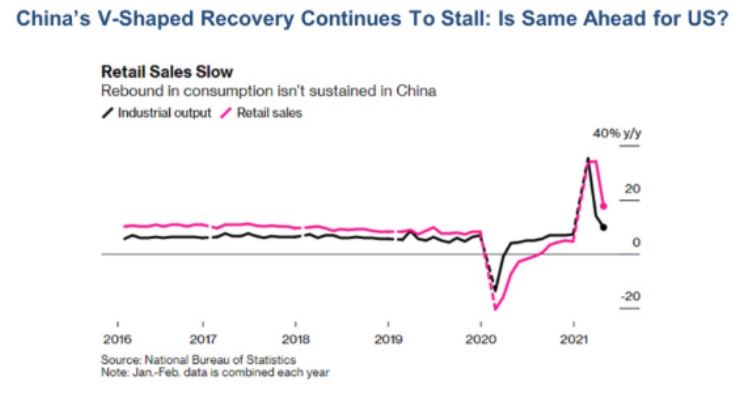

China’s Industrial Production Slows, from 14.1% in March to only 9.8% in April. That gives us a hint to our own future, as the Middle Kingdom emerged from the pandemic a year before we did. Retail sales also disappointed. After rocketing in 2020, the Chinese economy started slowing at the beginning of this year. The dead cat bounce in the economy is over. If this continues, it's bad news for copper prices of which the Middle Kingdom is the largest producer. If (FCX) closes under $40, stop out of all short-term longs immediately.

Housing Starts Dive, as builders run out of materials at reasonable prices. It gave the Dow Average a punch in the nose worth $220. Single family homes took the big hit, down 13.4% to 1.08 million. Permits are still up 70% YOY from when Covid completely shut the industry down. This is the most inflationary sector of the economy right now but barely registers in the CPI numbers. Prices must go even higher for frustrated buyers which are accelerating their rate of increase. Builders are including contingency clauses that allow price rises after the sale, a first. The South has dominated in starts where the population is moving and took the biggest hit. Buy (LEN), (KBH), and (PHM) on dips.

Existing Home Sales Drop 2.7%, in April to 5.85 million units. Inventories are down 20% YOY to only an unimaginable two-month supply. There’s nothing for sale. With the strongest YOY price gains in history, there is nothing for sale. It’s all about high prices, high prices, high prices. Homes over $1 million are up an incredible 214% YOY. The 70-year migration from North to South continues, costing democrats 5 seats in the House. Millennials are entering their peak home-buying years and that $150,000 four-bedroom home in Savannah, GA doesn’t look so bad.

Bitcoin is the Most Crowded State in the World, according to a survey of investment managers. That may explain the 35% plunge in cryptocurrency since April. Is this the end of the Ponzi scheme? Technology and ESG stocks are the second and third most over-owned, which may explain their recent flaccid performance.

Why is the Gold Hedge Working this Time? The Barbarous relic is finally giving investors the insurance and the downside hedge they need, after failing to do so during the last correction in February. That’s because interest rates were spiking in the winter but aren’t now. Interest rates are the enemy of all no-yielding assets, like precious metals.

Fed Hints of Early Rate Rise, trashing both stocks and bonds. The big one could be here, a complete collapse of the US Treasury bond market. I’m already running the biggest (TLT) shorts ever. We should fall from the current $135 to $120 by yearend. Sell all (TLT) rallies.

Lumber Futures Collapse by 40%. There goes your inflation. Now if only Biden will end the Trump-era import duty on Canadian lumber. It gives a big boost to the “transitory” camp, arguing that this is just a one or two-month spike spawned by the cover recovery. Soaring lumber prices had been a key factor igniting new home prices.

Applied Materials Knocks the Cover off the Ball, reporting blowout earnings. The semiconductors equipment maker has been the best performing chip-related stock of 2021, up 72%. (AMAT) sees a structural chip shortage lasting for years. DRAMs are speeding up, while NAN is slowing down. Customers are placing orders years in advance for the first time ever. A new $7.5 billion stock buyback plan and 9% dividend increase were announced. Buy (AMAT) on the dips.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 7.48% gain so far in May on the heels of a spectacular 15.67% profit in April. That leaves me 50% invested and 50% cash. We actually have a shot at reaching a double-digit performance for the seventh month in a row.

My 2021 year-to-date performance soared to 67.24%. The Dow Average is up 11.79% so far in 2021.

We got another major meltdown last week followed by an immediate recovery. I used the dip to reinitiate new positions in the (TLT), Goldman Sachs (GS), and Berkshire Hathaway (BRKB) to replace ones that expired on the Friday options expiration.

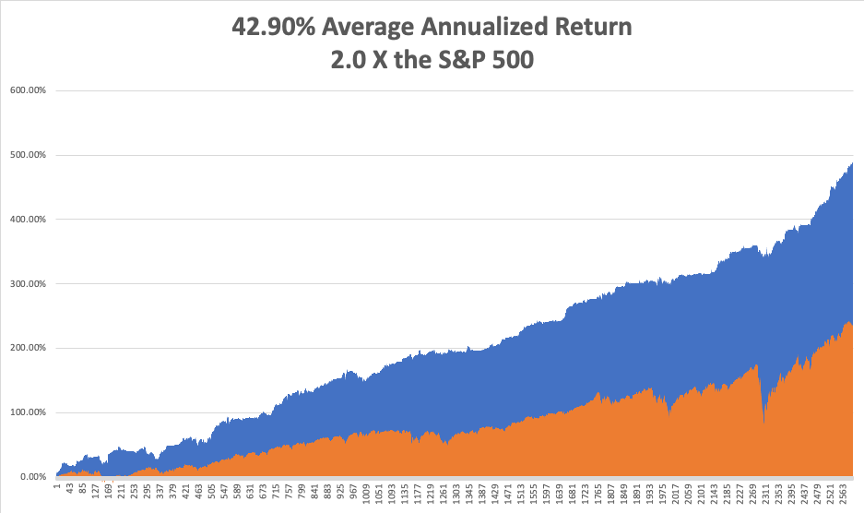

That brings my 11-year total return to 489.79%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.90%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 124.92%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33.1 million and deaths topping 590,000, which you can find here. Some 33.1 million Americans have contracted Covid-19.

The coming week will be a weak one on the data front.

On Monday, May 24, at 8:30 AM, the Chicago Fed National Activity Index is released.

On Tuesday, May 25, at 10:00 AM, the S&P Case Shiller National Home Price Index for March is announced.

On Wednesday, May 26 at 8:30 PM, MBA Mortgage Applications are revealed.

On Thursday, May 27 at 8:30 AM, the Weekly Jobless Claims are Published. We also get a second estimate for the red hot Q2 GDP.

On Friday, May 28 at 8:30 AM, the even hotter Personal Spending for April is disclosed. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, as this pandemic winds down, I am reminded of a previous one in which I played a role in ending.

After a 30-year effort, the World Health organization was on the verge of wiping out smallpox, a scourge that had been ravaging the human race since its beginning. I have seen Egyptian mummies at the Museum of Cairo that showed the scarring that is the telltale evidence of smallpox, which is fatal in 50% of cases.

By the early 1970s, the dread disease was almost gone but still remained in some of the most remote parts of the world. So, they offered a reward to anyone who could find live cases.

To join the American Bicentennial Mt. Everest Expedition in 1976, I took a bus to the eastern edge of Katmandu and started walking. That was the furthest roads went in those days. It was only 150 miles to basecamp and a climb of 14,000 feet.

Some 100 miles in, I was hiking through a remote village, which was a page out of the 14th century, back when families threw buckets of sewage into the street. The trail was lined with mud brick two-story homes with wood shingle roofs, with the second story overhanging the first.

As I entered the town, every child ran to their windows to wave, as visitors were so rare. Every smiling face was covered with healing but still bleeding smallpox sores. I was immune, since I received my childhood vaccination, but I kept walking.

Two months later, I returned to Katmandu and wrote to the WHO headquarters in Geneva about the location of the outbreak. A year later, I received a letter of thanks at my California address and a check for $100 telling me they had sent in a team to my valley in Nepal and vaccinated the entire population.

Some 15 years later, while on customer calls in Geneva for Morgan Stanley, I stopped by the WHO to visit a scientist I went to school with. It turned out I had become quite famous, as my smallpox cases in Nepal were the last ever discovered.

The WHO certified the world free of smallpox in 1980. The US stopped vaccinating children for smallpox in 1972, as the risks outweighed the reward.

Today, smallpox samples only exist at the CDC in Atlanta frozen in liquid nitrogen at minus 346 degrees Fahrenheit in a high-security level 5 biohazard storage facility. China and Russia probably have the same.

That’s because scientists fear that terrorists might dig up the bodies of some British sailors who were known to have died of smallpox in the 19th century and were buried on the north coast of Greenland remaining frozen ever since. If you need a new smallpox vaccine, you have to start from somewhere.

As for me, I am now part of the 34% of Americans who remain immune to the disease. I’m glad I could play my own small part in ending it.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

On Mt. Everest, Smallpox-Free in 1976

Bitcoin

Mad Hedge Technology Letter

April 16, 2021

Fiat Lux

Featured Trade:

(SHOULD I BUY COINBASE TODAY?)

(COIN), (CRM), (ADBE), (PYPL), (SQ)

For all the cryptocurrency haters in the world, it’s getting harder to take that stand.

I’ll tell you why.

Coinbase (COIN) was the first major crypto business to go public in the U.S. when it began trading at $381 Wednesday morning on the Nasdaq and its IPO symbolizes the acceptance of an alternative digital asset class in technology.

Prior to this watershed moment, the only way to play crypto was through second derivatives plays like PayPal (PYPL) and Square (SQ) who have been handsomely rewarded through higher share prices.

Now, we get the biggest U.S. cryptocurrency exchange trading publicly that will allow exposure to mainstream stock-market investors.

The event has also been tabbed as a catalyst that might drive the adoption of incremental digital assets.

At the very least, this lays down a marker for further crypto-related companies eyeing the Nasdaq after Coinbase’s blowout success.

This also shows that the cryptocurrency infrastructure is developing rapidly and its budding credibility is something that needs to be acknowledged.

The Coinbase IPO was also the catalyst in sending bitcoin prices to almost $65,000.

No doubt that the appreciating asset has been the most attractive use case for the incremental investor and cryptocurrency buyer.

Many early investors who got into bitcoin at 20 cents are now billionaires many times over.

After such stunning success, it’s hard to believe that any fintech or cryptocurrency start-up would ever consider doing their IPO anywhere else but New York.

New York has the liquidity, the US dollar, and the capacity to receive such type of growth companies in bulk.

This is not only an emphatic victory for digital assets, but also for the US tech sector and a stamp of validation for the Nasdaq market.

Ironically enough, even during this trade war, Chinese tech companies are clamoring to go public in New York and not mainland China for the above reasons.

Here are a few other highly positive data points to digest that were talking points in their S-1 filing.

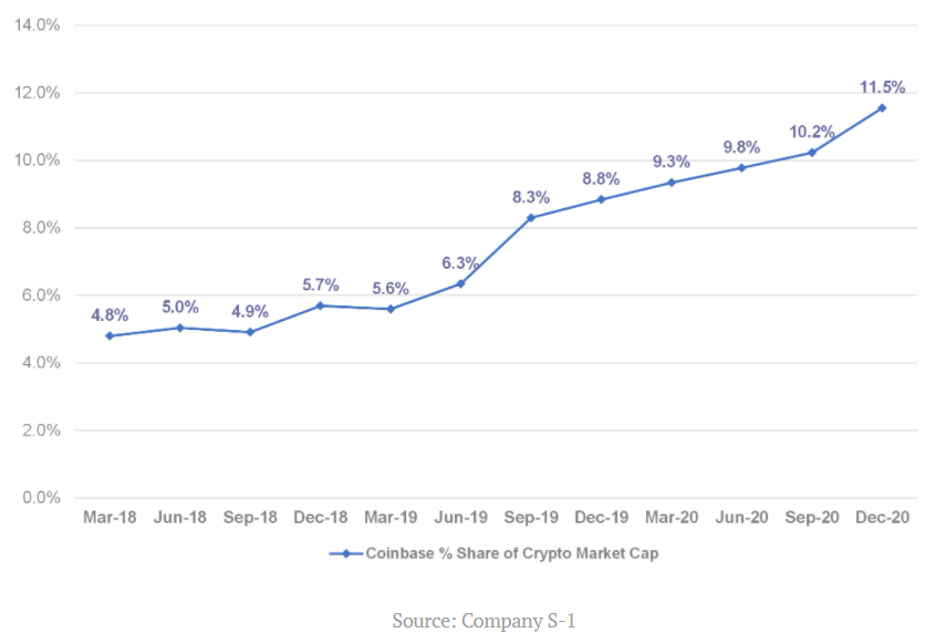

The overall market capitalization of crypto assets grew from less than $500 million to $782 billion between December 31, 2012, and December 31, 2020, representing a CAGR (compound annual growth rate) of over 150%.

Over the same period, Coinbase retail users grew from less than 13,000 to 43 million, a 175% CAGR.

I believe the total market cap of crypto is now around $2 trillion in April 2021.

And more recently, Coinbase has experienced significant growth in the number of institutions on their platform, increasing from over 1,000 as of December 31, 2017, to 7,000 as of December 31, 2020.

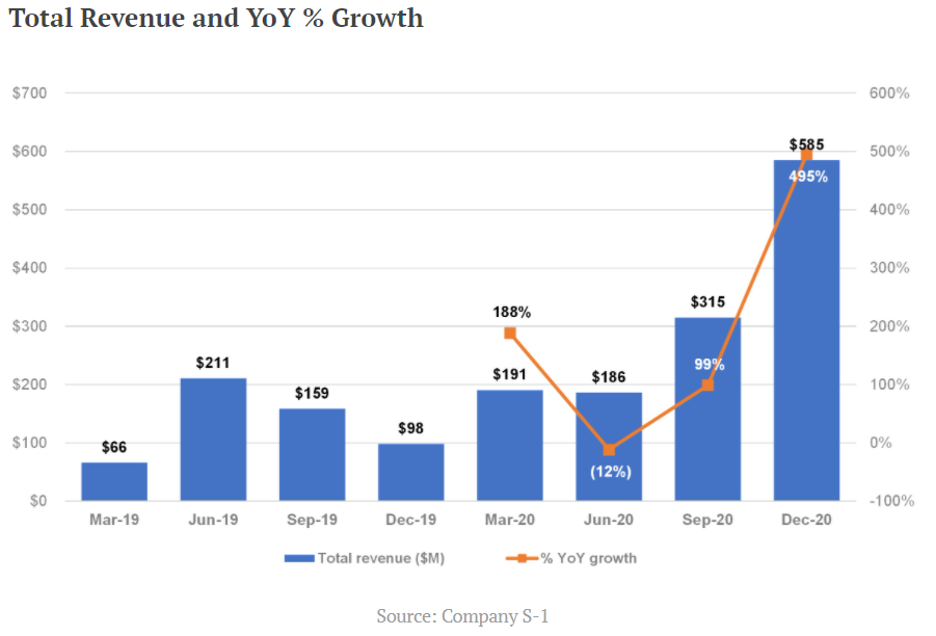

Bitcoin reported a nine-fold increase in Q1 revenue, to $1.8B, up from $190.6M the previous year.

Just like Google and Facebook benefit from a duopoly, Coinbase will benefit from being the only pure cryptocurrency option on the Nasdaq and that will put a floor under shares in the short-term.

The growth metrics of the company are also robust via a helping hand by the increasingly expensive price of bitcoin.

No doubt that this company’s prospects are tied to the hip with the prices of cryptocurrencies.

If the price of bitcoin retraces to $30,000, which it could because of the high volatility of it, expect Coinbase shares to dive with it.

This for all intents and purposes is a bet on the health and price trajectory of bitcoin for better or worse until other crypto-based choices are introduced which would give more layers and complexity to this sub-sector.

Bitcoin calls out Binance which they state as a competitor and Kraken is another exchange that is large and vying for the same capital.

I believe these two companies have a chance to go public and that is when you will really see the institutions jump on this crypto bandwagon.

More options and a foundational investment base will also promote stability in this new technology sub-sector.

Should you buy Coinbase today?

No.

I understand Coinbase’s growth metrics are off the charts with revenue growing 900%, but it’s not worth $100 billion market cap on just $1.8 billion of quarterly sales.

Investors would need solid tailwinds such as bitcoin passing $100,000 in 2021 for this company to be worth $100 billion and I just don’t see it.

Then also understand the cybersecurity and possible regulations are two risks that could blow up the business model at any moment which would take down the premium in the stock.

Yes, the meteoric rise of crypto at the start of 2021 has turned heads, but as the economy reopens, I do believe money will rotate from crypto back into traditional technology that is underpinned by cash cow businesses.

Highly profitable companies that aren’t FANGs are also set to deliver share appreciation to shareholders such as Salesforce (CRM) or a company like Adobe (ADBE) who earn profits of $5.27 billion on $13 billion of annual revenue.

I acknowledge that Coinbase’s IPO was the perfect time to go public.

They are taking advantage of easy money and low rates while the acceptance of this alternative asset class has never been higher.

However, I don’t see any more incremental growth in the short term and the stock is more than fully priced today.

The risk-reward is not favorable to pile into this stock now unless you have a bullish 50-year view on crypto and can’t wait.

This stock will go through volatility because of the inherent dynamics they are tied to and I would seriously look at buying Coinbase only on a massive sell-off.

Don’t go chasing unicorns.

At the end of the day, this is a real company with real revenue growth of 900% year-over-year. Slice it up anyway, and these numbers are numbers that attract investors, but the stock is too expensive right here.

Mad Hedge Technology Letter

March 31, 2021

Fiat Lux

Featured Trade:

(TIME TO LOOK AT SALESFORCE)

(CRM)

The incredible secular trend toward digital is something a lot of CEOs talk about; and essentially, what happened last year might have taken a decade to happen in terms of the adoption of digital technology. Just take the Service Cloud at Salesforce (CRM) for an example.

Their digital service capability has grown at just unprecedented rates with the adoption of tools like chatbots powered by artificial intelligence software Einstein, they experienced a 91% quarter-over-quarter growth in chatbots alone.

Take data coming from Cyber Week this past quarter, mobile push notifications were up 131% year over year.

SMS was up 171% year over year.

The unprecedented adoption of digital really opens the playbook up for cloud companies and especially Salesforce.

Delivering success from anywhere has become their de facto motto.

Their revenue rose to more than $5.8 billion, up 20% year over year, which is expected but difficult for a company of their size.

And for the full fiscal year 2021, revenue was $21.25 billion which was up 24% year over year.

Salesforce even raised their fiscal year 2022 guidance to $25.75 billion which is now at the high end of their range, representing 21% projected growth year over year.

Salesforce’s long-term revenue target for the fiscal year 2026 is now $50 billion or basically, they plan to double the company from where we are right now.

Doubling revenue in five years would make Salesforce the second largest independent software company in the world which is breathtaking.

And a big part of Salesforce’s thesis as a company is, they’re not going back, I mean, not going back to business pre-Covid.

It’s really everyone who has experienced all these digital trends, whether it's bought online, curbside pickup, that direct-to-consumer trend in the consumer packaged goods industry, the move to telemedicine.

Salesforce is accelerating at such a rapid speed because the new world is here already, this work-from-anywhere world.

The great news for cloud companies is that they can achieve success from anywhere, but unfortunately, Salesforce is currently grappling with expensive M&A acquisitions that have penalized the recent price action in shares.

This includes costs like $190 million from Acumen, and $600 million from Slack.

For fiscal 2022, Salesforce expects an operating margin of 17.7% or flat year over year because of an expected 160 basis points headwind from Slack and Acumen.

Also, other heightened costs include investments in the core business and the anticipated gradual increase of travel in the second half of fiscal 2022.

The decrease in profitability will translate into much lower earnings per share (EPS).

As a result, this puts CRM stock on a high price-earnings (P/E) multiple of 48 which definitely isn’t cheap.

Last year, EPS was $4.92, up 64.6% from last year’s $2.99. But going forward, Salesforce forecasts that its EPS will be between just $3.39-$3.41 for 2022.

Real estate consolidation would also hurt their earnings in the year.

If you remember correctly, the company has splashed out on building Salesforce Tower in the middle of downtown San Francisco which gave them 1.4 million square feet of workspace.

Now, it sits unused because of remote work policies.

Salesforce is paying $27.7 billion in cash for the Slack acquisition which was considered way too much at the time and the all-cash transaction will mean the company will have to borrow at least $15 billion, since it has just $11.96 billion in cash and securities at the end of January 2021.

The consolidation in shares from $270 to $210 reflects the time needed to absorb these higher costs, lower profitability, and M&A transitions at a time when many cloud stocks doubled in 2020.

I do believe that when Salesforce turns around its profitability with higher trending EPS growth, stocks will gain sense of it and the direction will turn for the better.

That being said, most of the bad news is already in the stock, and we are getting close to the inflection point when Salesforce would be a favorable reversal trade.