Global Market Comments

July 22, 2020

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO),

(PFE), (BMY), (AMGN), (CELG), (CRSP), (FB), (PYPL), (GOOGL), (AAPL), (AMZN), (SQ), (JPM), (BAC), (BABA), (EEM), (FXA), (FCX), (GLD)

Global Market Comments

July 22, 2020

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO),

(PFE), (BMY), (AMGN), (CELG), (CRSP), (FB), (PYPL), (GOOGL), (AAPL), (AMZN), (SQ), (JPM), (BAC), (BABA), (EEM), (FXA), (FCX), (GLD)

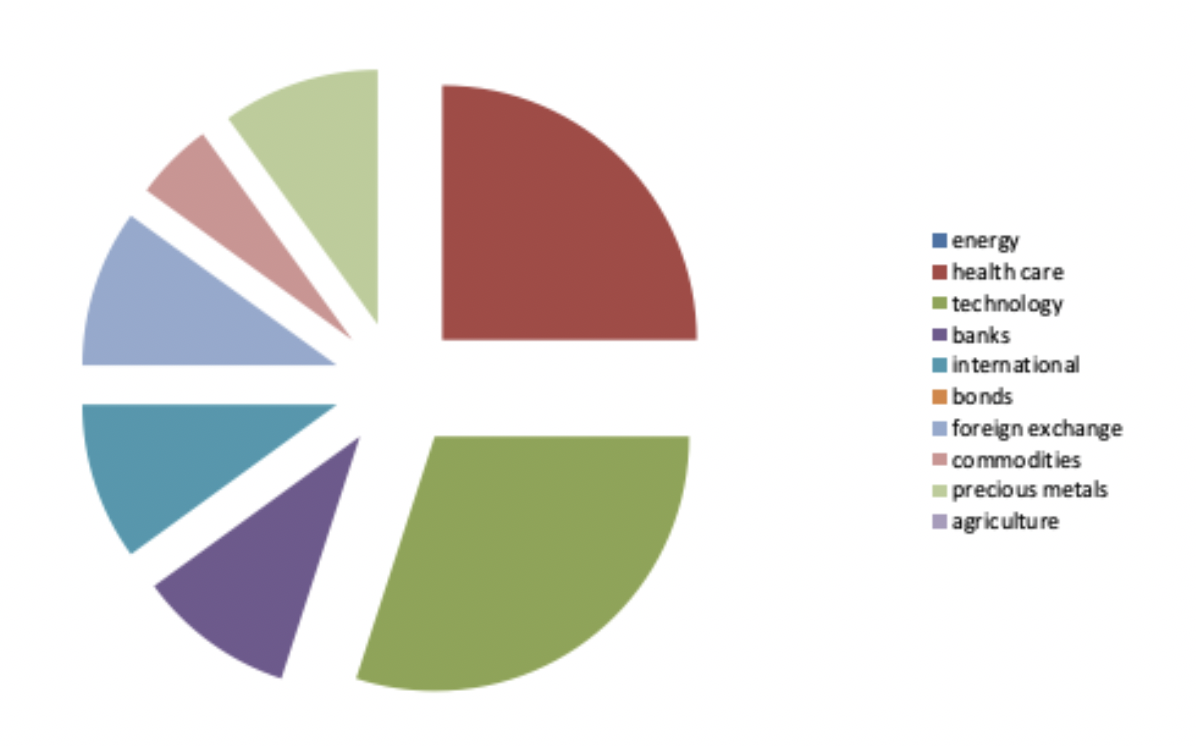

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on October 17, 2019. In fact, not only did we nail the best sectors to go heavily overweight, we completely dodged the bullets in the worst-performing ones, especially in energy.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 70 ½.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted in red.

To download the entire portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com , log in, go to “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

My 5% holding in Biogen (BIIB) was taken over by Bristol Myers (BMY) at a hefty premium at an all-time high, so I’ll take the win. I am replacing it with Covid-19 vaccine frontrunner Bristol Myers (BMY) itself.

I am also taking out healthcare provider Cigna (CI), whose profits have been hammered by the pandemic. A future Biden administration might also move to a national healthcare system that will cap profits. I am replacing it with another Covid-19 vaccine leader Pfizer (PFE).

My 30% weighting in technology remains the same. Even though these stocks are 30% more expensive than they were three years ago, I believe they will lead the charge into the 2020s. It’s where the big growth is. These have doubled or more over the past nine months.

I am sticking with a 10% weighting in banking. Thanks to trillions in stimulus loans, they are now the most government-subsidized sector of the economy. I also believe that massive bond issuance by the US Treasury will deliver a sharply steepening yield curve, another pro bank development.

With my 10% international exposure, I am taking out a 5% weight in slow-growth Japan and replacing it with Chinese Internet giant Alibaba (BABA). The US will most likely dial back its vociferous anti-Chinese stance next year and (BABA) will soar.

I am executing another switch in my foreign currency exposure, taking out a long in the Japanese yen (FXY) and a short in the Euro (EUO) and substituting in a double long in the Australian dollar (FXA).

Australia will be a leveraged beneficiary of a recovery in the global economy, both through a recovery on commodity prices and gold which has already started, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

I’m quite happy with my 10% holding in gold (GLD), which should move to new all-time highs imminently….and then go ballistic.

As for energy, I will keep my weighting at zero, no matter how cheap it has gotten. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free.

My ten-year assumption for the US and the global economy remains the same.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

July 9, 2020

Fiat Lux

Featured Trade:

(DOUBLING UP AGAIN ON BIOTECH),

(BMRN), (VRTX), (GILD), (MRNA), (CRSP)

If the volatility of the stock market lately has been making you sick, then it might be time to add more biotechnology and healthcare stocks to your portfolio. They’re all having the effect of dragging each other up in this superheated environment.

Investors looking for these businesses can find a safe haven in rare diseases big player BioMarin Pharmaceutical (BMRN), which has $16.5 billion in market capitalization.

While most businesses languished since the pandemic broke this 2020, this biotechnology company’s shares rose by 12% this year. That’s not where it ends, though.

BioMarin could still pick up even more momentum despite the second wave of COVID-19.

The company currently has an extensive pipeline aimed at rare genetic diseases, with seven already approved and marketed in over 75 countries across the globe.

Looking at BioMarin’s first quarter earnings report for 2020, the company recorded a revenue of $502.1 million. This shows a 25% increase from the $400.7 million it raked in during the same period in 2019. It also handily beat the analysts’ estimate of $468.8 million.

Among BioMarin’s products, genetic metabolic disorder infusion Naglazyme is considered the top-selling treatment.

Sales of this product climbed 32% year over year in the first quarter to hit $27.4 million, with the jump primarily attributed to an increase in sales in Russia and Brazil.

However, the rising stars of BioMarin are two enzyme replacement treatments.

One is genetic blood disorder treatment Palynziq, which skyrocketed by 181% year over year to reach $22.3 million.

The other is Batten disease treatment Brineura, which soared by a whopping 97% to rake in $24 million.

Three of BioMarin’s drugs also performed well during this quarter.

Phenylketonuria drug Kuvan recorded $15.1 million in sales, up by 14% from the same period in 2019.

Meanwhile, Morquio A syndrome medication Vimizim generated $11.4 million in sales, showing off a 9% year over year jump as well. As for Aldurazyme, this Hurler syndrome drug’s sales rose by 23% to reach 10.4 million.

Now, the company is looking into another rare-disease treatment, which could cover Hemophilia A therapies via its experimental gene therapy Roctavian. This can open up a huge market for BioMarin, with over 20,000 Americans suffering from this disease.

Roctavian is expected to receive the FDA green light earlier than its August 21 decision date, possibly marking another blockbuster drug added to BioMarin’s pipeline.

Needless to say, the steady sales growth of these products served as the major driver of the company’s improving bottom line.

Over the past 10 years, the annual revenue of BioMarin has consistently climbed and beat analysts’ expectations -- a trend that’s likely to go on in the next decade as well.

Another company that built its name on rare diseases treatments is Vertex Pharmaceuticals (VRTX).

While most stocks struggle to deal with black swan situations like the COVID-19 pandemic, Vertex is poised to enter the $100 billion market cap club soon.

In fact, the company recently updated its 2020 guidance, increasing its initial estimate from $5.1 billion and $5.3 billion to $5.3 billion to $5.6 billion.

In sum, Vertex is poised to continue its upward trajectory despite the current economic landscape.

The confidence in its growth is bolstered by its recent earnings report for the first quarter of 2020, which indicated an impressive 77% year over year to reach a net revenue of $1.5 billion.

At the moment, Vertex has $61.7 billion in market capitalization, with the company transforming into the most dominant player in the cystic fibrosis (CF) space. Actually, Vertex holds the monopoly on the approved drugs used to treat CF, namely, Kalydeco, Orkambi, and Symdeko.

Apart from its efforts to continuously dominate the CF sector, Vertex also has several moonshots that can eventually turn into major catalysts.

Among those is its partnership with CRISPR Therapeutics (CRSP).

The two biotechnology companies are developing a gene therapy called CTX001 which can cure rare genetic blood diseases. Specifically, CTX001 is designed to cure beta-thalassemia and sickle cell disease.

Apart from its partnership with CRISPR Therapeutics, Vertex also acquired Semma Therapeutics in 2019 with the goal of coming up with a cure for Type 1 diabetes. If things go as planned, a gene therapy for this genetic disease will advance to clinical testing by early 2021.

While the world is mired in crisis, the biotechnology sector has been fueled with excitement particularly because of the potential COVID-19 vaccines and cures from companies like Gilead Sciences (GILD) and Moderna (MRNA).

With insistent whispers that a second wave of the deadly COVID-19 is well on its way, opportunistic investors are actively seeking defensive stocks with businesses that can withstand the second wave of infections.

Both BioMarin and Vertex offer safe bets in this increasingly unpredictable world. Aside from proving their capacity to expand, both also have incredible room for growth.

Mad Hedge Biotech & Healthcare Letter

April 16, 2020

Fiat Lux

Featured Trade:

(CRISPR THERAPEUTICS’ CANCER BREAKTHROUGH),

(CRSP), (VRTX)

The findings for the first-ever human trial that uses CRISPR gene-editing technology to alter the immune cells of cancer patients have been announced.

The trial, which is hailed as the first of its kind to ever publish its results, centered on three patients suffering from advanced cancer who are all in their 60s. The goal is to determine whether or not their bodies could tolerate the genetically edited immune cells.

The patients received doses of CRISPR-modified variants gathered from their own T cells, which were specifically edited to transform into more efficient cancer-killing cells.

The results showed that there were no issues reintroducing the edited cells back into the bodies of the patients. More impressively, the modified cells managed to survive longer than the anticipated period.

In fact, these cells were detected in the patients’ bodies nine months following the novel treatment.

Doctors also noted that the patients’ symptoms stabilized throughout the treatment period. One of them even saw a reduction in tumor size.

While the treatment was only a one-time injection and was not carried on for a longer time, the fact that no major complication happened during the trial has health experts hailing it a success. Hence, more trials of this nature can be expected in the near future.

As expected, this trial boosted gene-editing stocks -- and CRISPR Therapeutics (CRSP) is one of the beneficiaries of this positive news.

This development is anticipated to further fuel investor interest in CRISPR Therapeutics especially after it released an impressive fourth-quarter financial report that beat revenue expectations.

The company’s profits grew to $77 million, indicating a substantial jump from the measly $100,000 it reported in the fourth quarter of 2018. As for its cash and cash equivalents, the amount increased by 106.7% from $456.6 million last year to $943.8 million.

Meanwhile, its total annual income increased from $3.1 million to a whopping $289.6 million.

A quick look at the changes done by the company revealed that the surge can be mostly attributed to CRISPR Therapeutics’ collaboration with Vertex Pharmaceuticals (VRTX) and not product sales.

Nonetheless, the improvement in the gene-editing company’s performance is still impressive considering that analysts only estimated their earnings to reach $45.2 million in the said quarter.

While these numbers are already turning heads, CRISPR Therapeutics is expected to dominate more headlines in 2020.

So far, the company has four major treatments in development.

One is called CTX001, which is for genetic blood disorders specifically sickle cell disease and transfusion-dependent beta thalassemia. Results involving this treatment should be out sometime this year.

The other three, CTX110, CTX120, and CTX130, are cancer treatments commonly known as CAR-T therapies.

CRISPR Therapeutics is an obvious leader in the race to commercialize CRISPR/Cas9 gene-editing services and products.

The lowdown is that its treatments under development, which involve groundbreaking innovations focused on rare diseases, have the potential to turn in hundreds of billions in sales. More impressively, CRISPR Therapeutics is poised to achieve this in record time --- way ahead of its competitors.

So, what’s the catch?

Well, CRISPR Therapeutics’ whole platform could end up amounting to nothing more than a fascinating science experiment. If that happens, then this stock would be worthless.

However, Vertex Pharmaceuticals has a stellar track record of picking winners. Its decision to splurge on CRISPR Therapeutics and back the latter’s research speaks volumes of the mid-cap biotechnology company’s potential to turn into a frontrunner in this novel world of gene editing.

Needless to say, CRISPR Therapeutics’ current valuation arguably indicates a once-in-a-lifetime buying opportunity. However, this high-risk investment would only appeal to aggressive investors.

Global Market Comments

April 16, 2020

Fiat Lux

Featured Trade:

(MORE LONG-TERM LEAPS TO BUY AT THE BOTTOM),

(TSLA), (CRSP), (MU)

The final bottom in this bear market is fast approaching. It may come in weeks or months. After the cataclysmic meltdown in March, markets are becoming more orderly and tradable. What does this mean for LEAPs?

It means the next bid dip in share prices is the one you want to buy.

Readers have been besieging me with more ideas on long term LEAPS to buy at the next bottom. So, here is another generous serving of red meat.

I am often asked how professional hedge fund traders invest their personal money. They all do the exact same thing. They wait for a market crash like we are seeing now and buy the longest-term LEAPS (Long Term Equity Participation Securities) possible for their favorite names.

The reasons are very simple. The risk on LEAPS is limited. You can’t lose any more than you put in. At the same time, they permit enormous amounts of leverage.

Two years out, the longest maturity available for most LEAPS, allow plenty of time for the world and the markets to get back on an even keel. Recessions, pandemics, hurricanes, oil shocks, interest rate spikes, and political instability all go away within two years and pave the way for dramatic stock market recoveries.

You just put them away and forget about them. Wake me up when it is 2022.

I put together this new portfolio using the following parameters. I set the strike prices just above the all-time highs set in February. I went for the maximum maturity. I used today’s prices. And of course, I picked the names that have the best long-term outlooks based on our own intensive in-house research.

You should only buy LEAPS of the best quality companies with the rosiest growth prospects and rock-solid balance sheets to be certain they will still be around in two years. I’m talking about picking up Cadillacs, Rolls Royces, and even Ferraris at fire-sale prices. Don’t waste your money on speculative low-quality stocks that may never come back.

If you buy LEAPS at these prices and the stocks all go to new highs, then you should earn an average 400% profit from an average stock price increase of only 75%.

That is a staggering return 5.3 times greater than the underlying stock gain. And let’s face it. None of the companies below are going to zero, ever. Now you know why clever hedge fund traders only employ this strategy.

There is a smarter way to execute this portfolio. Put in throw-away crash bids at levels so low they will only get executed on the next cataclysmic 1,000-point down day in the Dow Average.

You can play around with the strike prices all you want. Going farther out of the money increases your returns, but raises your risk as well. Going closer to the money reduces risk and returns, but the gains are still a multiple of the underlying stock.

Buying when everyone else is throwing up on their shoes is always the best policy. That way your return will rise to ten times the move in the underlying stock.

If you are unable or unwilling to trade options, then you will do well buying the underlying shares outright. I expect the list below to rise by 50% or more over the next two years.

Enjoy.

Tesla (TSLA) - June 17 2022 $1,080-$1,100 vertical bull call spread at $4.00 delivers a 400% gain with the stock at $1,100, up 51% from the current level. The pandemic is vastly accelerating all trends. One big one is the migration from internal combustion engines to electric power where Tesla has a ten-year and expanding head start. Sales at its new Shanghai factory in the first country to recover from the Coronavirus are blowing away its most optimistic view. The Model Y small SUV at the end of this year is expected to be the company’s biggest-selling model ever.

CRISPR Therapeutics (CRSP) - January 15 2021 $85-$90 vertical bull call spread at $1.00 delivers a 400% gain with the stock at $85, up 77% from the current level. It’s shorter-dated than the others, but this was the longest maturity posted on my trading platform. CRISPR Therapeutics is the dominant player in gene-editing technology, which is key to many biotech developments going forward. That includes beating the Coronavirus. The stock is an incredible bargain at this level, off 36% from its all-time high.

Micron Technology (MU) – January 21 2021 $85-$90 vertical bull call spread at $1.00 delivers a 400% gain with the stock at $90, up 96% from the current level. Coming out on the other side of the pandemic, there will be a massive global shortage of the computer chips that Micron Technology makes with already huge profit margins. A total no-brainer and I love visiting their Boise, Idaho headquarters.

To review my last list of Ten Long-Term LEAPS to Buy at the Market Bottom, please click here.

Yup, I Think I See Another Great LEAPS Opportunity

Global Market Comments

February 14, 2020

Fiat Lux

Featured Trade:

(FEBRUARY 12 BIWEEKLY STRATEGY WEBINAR Q&A)

(SQ), (TSLA), (FB), (GILD), (BA), (CRSP), (CSCO), (GLD)

(FEYE), (VIX), (VXX), (USO), (LYFT), (UBER)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader February 12 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What do you think about Facebook (FB) here? We’ve just had a big dip.

A: We got the dip because of a double downgrade in the stock from a couple of brokers, and people are kind of nervous that some sort of antitrust action may be taken against Facebook as we go into the election. I still like the stock long term. You can’t beat the FANGs!

Q: If Bernie Sanders gets the nomination, will that be negative for the market?

A: Absolutely, yes. It seems like after 3 years of a radical president, voters want a radical response. That said, I don't think Bernie will get the nomination. He is not as popular in California, where we have a primary in a couple of weeks and account for 20% of total delegates. I think more of the moderate candidates will come through in California. That's where we see if any of the new billionaire outliers like Michael Bloom or Tom Steyer have any traction. My attitude in all of this is to wait for the last guy to get voted off the island—then ask me what's going to happen in October.

Q: When should we come back in on Tesla (TSLA)?

A: It’s tough with Tesla because although my long-term target is $2,500, watching it go up 500% in seven months on just a small increase in earnings is pretty scary. It’s really more of a cult stock than anything else and I want to wait for a bigger pullback, maybe down to $500, before I get in again. That said, the volatility on the stock is now so high that—with the short interest going from 36% down to 20%—if we get the last of the bears to really give up, then we lose that whole 20% because it all turns into buying; and that could get us easily over $1,000. The announcement of a new $2 billion share offering is a huge positive because it means they can pay off debt and operate with free capital as they don’t pay a dividend.

Q: Is Square (SQ) a good buy on the next 5% drop?

A: I would really wait 10%—you don't want to chase trades with the market at an all-time high. I would wait for a bigger drop in the main market before I go aggressive on anything.

Q: What about CRISPR Technology (CRSP) after the 120% move?

A: We’ve had a modest pullback—really more of a sideways move— since it peaked a couple of months ago; and again, I think the stock either goes much higher or gets taken over by somebody. That makes it a no-lose trade. The long sideways move we’re having is actually a very bullish indication for the stock.

Q: If Bernie is the candidate and gets elected, would that be negative for the market?

A: It would be extremely negative for the market. Worth at least a 20% downturn. That said, according to all the polling I have seen, Bernie Sanders is the only candidate that could not win against Donald Trump—the other 15 candidates would all beat Trump in a 1 to 1 contest. He's also had one heart attack and might not even be alive in 6 months, so who knows?

Q: I just closed the Boeing (BA) trade to avoid the dividend hit tomorrow. What do you think?

A: I’m probably going to do the same, that way you can avoid the random assignments that will stick you with the dividend and eat up your entire profit on the trade.

Q: When do you update the long-term portfolio?

A: Every six months; and the reason for that is to show you how to rebalance your portfolio. Rebalancing is one of the best free lunches out there. Everyone should be doing it after big moves like we’ve seen. It’s just a question of whether you rebalance every six months or every year. With stocks up so much a big rebalancing is due.

Q: I have held onto Gilead Sciences (GILD) for a long time and am hoping they’ll spend their big cash hoard. What do you think?

A: It’s true, they haven’t been spending their cash hoard. The trouble with these biotech stocks, and why it's so hard to send out trade alerts on them, is that you’ll get essentially no movement on them for years and then they rise 30% in one day. Gilead actually does have some drugs that may work on the coronavirus but until they make another acquisition, don’t expect much movement in the stock. It’s a question of how long you are willing to wait until that movement.

Q: Is it time to get back into the iPath Series B S&P 500 VIX Short Term Futures ETN (VXX)?

A: No, you need to maintain discipline here, not chase the last trade that worked. It’s crucial to only buy the bottoms and sell the tops when trading volatility. Otherwise, time decay and contango will kill you. We’re actually close to the middle of the range in the (VXX) so if we see another revisit to the lows, which we could get in the next week, then you want to buy it. No middle-of-range trades in this kind of market, you’re either trading at one extreme or the other.

Q: Could you please explain how the Fed involvement in the overnight repo market affects the general market?

A: The overnight repo market intervention was a form of backdoor quantitative easing, and as we all know quantitative easing makes stocks go up hugely. So even though the Fed said this wasn't quantitative easing, they were in fact expanding their balance sheet to facilitate liquidity in the bond market because government borrowing has gotten so extreme that the public markets weren’t big enough to handle all the debt; that's why they stepped into the repo market. But the market said this is simply more QE and took stocks up 10% since they said it wasn't QE.

Q: What about Cisco Systems (CSCO)?

A: It’s probably a decent buy down here, very tempting. And it hasn't participated in the FANG rally, so yes, I would give that one a really hard look. The current dip on earnings is probably a good entry point.

Q: Should we buy the Volatility Index (VIX) on dips?

A: Yes. At bottoms would be better, like the $12 handle.

Q: When is the best time to exit Boeing?

A: In the next 15 minutes. They go ex-dividend tomorrow and if you get assigned on those short calls then you are liable for the dividend—that will eat up your whole profit on the trade.

Q: Do you like Fire Eye (FEYE)?

A: Yes. Hacking is one of the few permanent growth industries out there and there are only a half dozen listed companies that are cutting edge on security software.

Q: What are your thoughts on the timing of the next recession?

A: Clearly the recession has been pushed back a year by the 2019 round of QE, and stock prices are getting so high now that even the Fed has to be concerned. Moreover, economic growth is slowing. In fact, the economy has been growing at a substantially slower rate since Trump became president, and 100% of all the economic growth we have now is borrowed. If the government were running a balanced budget now, our growth would be zero. So, certainly QE has pushed off the recession—whether it's a one-year event or a 2-year event, we’ll see. The answer, however, is that it will come out of nowhere and hit you when you least expect it, as recessions tend to do.

Q: Would you buy gold (GLD) rather than staying in cash?

A: I would buy some gold here, and I would do deep in the money call spreads like I have been doing. I’ve been running the numbers every day waiting for a good entry point. We’re now at a sort of in between point here on call spreads because it’s 7 days to the next February expiration and about 27 days to the March one after that, so it's not a good entry point this week. Next week will look more interesting because you’ll start getting accelerated time decay for March working for you.

Q: When are you going to have lunch in Texas or Oklahoma?

A: Nothing planned currently. Because of my long-term energy views (USO), I have to bring a bodyguard whenever I visit these states. Or I hold the events at a Marine Corps Club, which is the same thing.

Q: Would you use the dip here to buy Lyft (LYFT)? It’s down 10%.

A: No, it’s a horrible business. It’s one of those companies masquerading as a tech stock but it isn’t. They’re dependent on ultra-low wages for the drivers who are essentially netting $5 an hour driving after they cover all their car costs. Moreover, treating them as part-time temporary workers has just been made illegal in California, so it’s very bad news for the stocks—stay away from (LYFT) and (UBER) too.

Q: Is the Fed going to cut interest rates based on the coronavirus?

A: No, interest rates are low enough—too low given the rising levels of the stock market. Even at the current rate, low-interest rates are creating a bubble which will come back to bite us one day.

Q: Household debt exceeded $14 trillion for the first time—is this a warning sign?

A: It is absolutely a warning sign because it means the consumer is closer to running out of money. Consumers make up 70% of the economy, so when 70% of the economy runs out of money, it leads to a certain recession. We saw it happen in ‘08 and we’ll see it happen again.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader