Global Market Comments

March 15, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LISTEN TO THE (VIX),

(SPY), (IWM), (QQQ), (TLT), (VIX), (DAL), (BA), (ALK)

Global Market Comments

March 15, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LISTEN TO THE (VIX),

(SPY), (IWM), (QQQ), (TLT), (VIX), (DAL), (BA), (ALK)

I decided to take a day off over the weekend and see what was happening in the real economy.

As I drove over the Bay Bridge, I spotted over 30 very large container ships from China loaded to the gills. They were diverted from Los Angeles where the delay to unload ships has extended to two months.

The San Francisco farmers market was jammed with a mask-wearing crowd. Standing in front of me in the line to buy lavender salt was former 49ers quarterback Joe Montana, who took his team to the Super Bowl four times. He was in great shape, looking at least 30 pounds lighter than in his heyday.

Leaving Half Moon Bay after picking up some driftwood for my garden, the traffic to get into town was at least an hour long.

It all underlies a theme for the economy and the markets that I have been expounding upon for the last year.

The Roaring Twenties have begun, the number of consumers and investors who believe this is increasing every day, and the impact on business and stocks is still being wildly underestimated.

You can see this in the Volatility Index (VIX), which has made a rare two roundtrips over the past month, and that means two possible things. Markets are undecided. When they make up their minds, they will either crash, or make a new leg up.

I vote for the latter.

I keep especially close attention on the (VIX) these days because it tells me when I can turn on or off my printing press for $100 bills. Anywhere over a (VIX) of $30 and I can strap on “free money” trades where the chances of losing money are virtually nil.

You can see this in my performance this year, where 40 roundtrips trade alerts in 11 weeks generated 38 wins and only two losses. That’s a success rate of an unprecedented 95%.

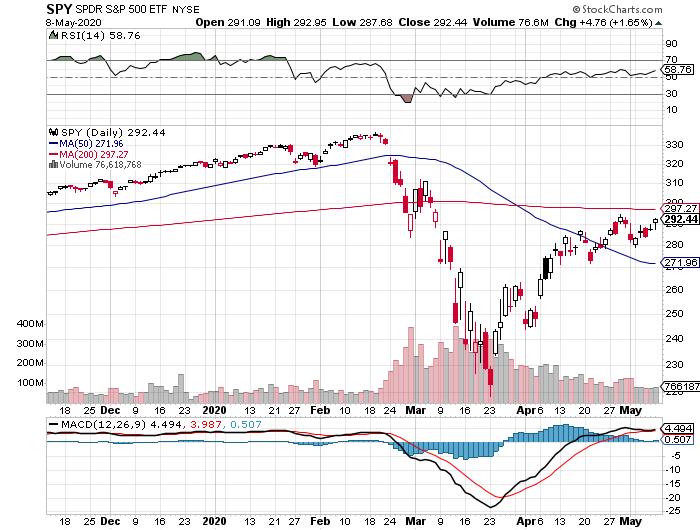

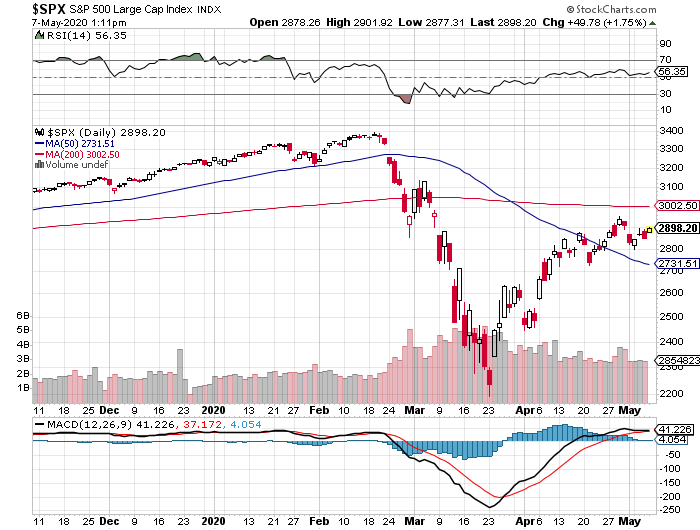

The indecision in the markets is obvious in the charts below. The large cap S&P 500 (SPX) and the small cap Russell 2000 (IWM) clawed their way to new highs last week, but the tech heavy NASDAQ (QQQ) made a feeble, halfhearted effort at best. Technology alone is being punished for rising interest rates as the ten-year US Treasury yield hit 1.62%.

This makes absolutely no sense as the larger tech companies are massive cash generators, run huge cash balances, and are enormous let lenders to the financial system. That means they make millions in interest payments from rising rates. What they are really being punished for is doubling from the pandemic low a year ago.

But never argue with Mr. Market.

Biden signs, with a record $1.8 trillion hitting the economy immediately. Money could start hitting your bank account this weekend if you are signed up for electronic payments with the IRS. Let the party begin! I already spent my money a long time ago. The Fed is forecasting a 10% GDP growth rate in Q2. Money is about to come raining down upon the economy….and the stock market. The big question is how much of this is already in the market. “Buy the rumor, sell the news”. Given the wild swings in the market, and multiple visits to a $32 (VIX), it’s clear that markets don’t know….yet.

The Next Battle is over infrastructure, which the democrats want to have an environmental. “green” slant. Look for a big gas tax rise to pay for it. They may get what they want with Senate control. Look for a September target. The economy needs $2 trillion a year in new government spending to keep the stock market rising and it will probably happen.

Nonfarm Payroll comes in at a blockbuster 379,000 in February, far better than expected. It's a preview of explosive numbers to come as the US economy crawls out of the pandemic. That’s with a huge drag from terrible winter weather. The headline Unemployment Rate is 6.2%. The U-6 “discouraged worker” rate of still a sky high 11%, those who have been jobless more than six months. Leisure & Hospitality were up an incredible 355,000 and Retail was up 41,000. Government lost 86,000 jobs. See what employers are willing to do when they see $20 trillion about to hit the economy?

Weekly Jobless Claims dive to 712,000 has pandemic restrictions fall across the country, the lowest since November. However, ongoing claims still stand at an extremely high 4.1 million. Total US joblessness still stands at 18 million. Will the pandemic come back to haunt us from these early reopenings?

California Disneyland (DIS) to reopen April 1, lifting a very dark cloud and huge expenses off the company. Cases on the west coast have fallen so dramatically that the state feels it can get away with this. Maybe this is an effort to derail the recall movement against the government. Stock is up 2% in the after-market, which Mad Hedge followers are long. Time to dig out my mouse ears. Keep buying (DIS) on dips.

Oil (USO) soars 3% on an attack on Saudi oil facilities and a building US economic recovery. $69 a barrel is printed. This is setting up as a great short. High prices in a decarbonizing economy have no future. A (USO) $34-$36 put LEAP with a January 2023 maturity might make all the sense in the world here.

Boeing (BA) announced Fist Positive Deliveries, in 14 months, finally turning around the mess with the 737 MAX. United Airlines was the biggest buyer. The perfect storm is finally over. And Boeing is about to snag another giant order, this time from Southwest (LUV). This comes on the heels of similar big order from Alaska Air (ALK). Keep buying (BA) on dips. An upside breakout is imminent.

Consumer Price Index Comes in at 0.4%, and 0.1% ex food and energy. It’s still at a nonexistent level. Rising gasoline prices were a factor, but airline ticket prices remain at all-time lows. I’ll worry about inflation when I see the whites of its eyes. Commodity prices have doubled in a year but show nowhere in the inflation numbers. With a headline Unemployment Rate at 6.1% and a U-6 at 18 million, it's unlikely we’ll see wage any time soon, which is 70% of the inflation calculation.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

It’s amazing how well selling tops and buying bottoms can help your performance. My Mad Hedge Global Trading Dispatch profit reached a super-hot 16.32% during the first half March on the heels of a spectacular 13.28% profit in February. The Dow Average is up a miniscule 8.2% so far in 2021.

It was a total rip your face off rally in the markets last week, so I took off my hedged and covered shorts in the S&P 500 (SPY) and the NASDAQ (QQQ). That leaves me to run my seven remaining profitable positions into the March 19 options expiration.

I also had my hands full running the three-day Mad Hedge Traders & Investors Summit, introducing some 27 speakers to a global audience of 10,000. The speakers’ videos go up on Tuesday at www.madhedge.com.

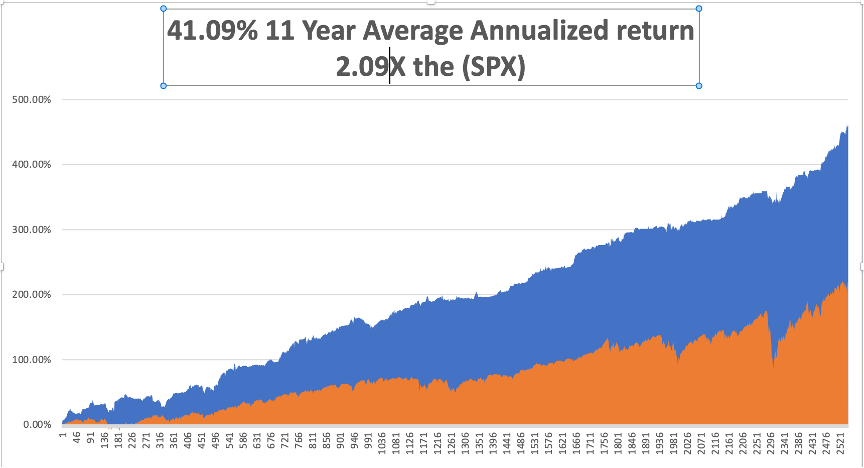

This is my fifth double-digit month in a row. My 2021 year-to-date performance soared to 39.81. That brings my 11-year total return to 465.36%, some 2.12 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.09%. I am concerned because numbers any higher than this will look fake.

My trailing one-year return exploded to 122.6%, the highest in the 13-year history of the Mad Hedge Fund Trader. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

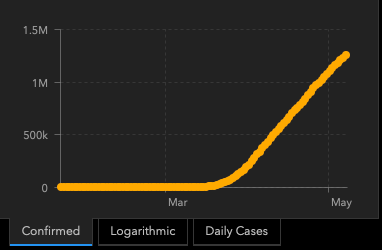

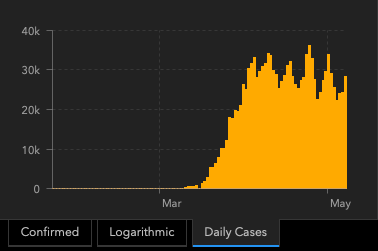

We need to keep an eye on the number of US Coronavirus cases at 29.5 million and deaths topping 535,000, which you can find here. Thankfully, death rates have slowed dramatically, but Obituaries are still the largest sector in the newspaper.

The coming week will be a boring one on the data front.

On Monday, March 15, at 7:30 AM EST, the New York Empire State Manufacturing Index for March is released.

On Tuesday, March 16, at 8:30 AM, US Retail Sales for February are published.

On Wednesday, March 17 at 8:30 AM, we learn Housing Starts for February. At 2:00 PM we get the Federal Reserve interest rate decision and press conference.

On Thursday, March 18 at 8:30 AM, Weekly Jobless Claims are out. We also obtain the Philadelphia Fed Manufacturing Index.

On Friday, March 19 at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I was saddened to learn of the death of George Schultz, Treasury Secretary and Secretary of State under president Ronald Reagan. He was 101.

George graduated from Yale at the outbreak of WWII and immediately joined the US Marine Corps (Semper Fi) where he used his ample math background to become an anti-aircraft officer. He issued my dad’s unit the useful advice to always lead an attacking Zero fighter by four plane lengths to hit the engine with a machine gun. It’s simple ballistics.

After the war, he used the GI bill to get a PhD from MIT, and later worked for President Eisenhower. He then became the Dean of the Chicago Business School.

I first met George when The Economist magazine sent me to interview him in San Francisco as the CEO of Bechtel Corp, a major engineering and construction company in 1982. The following week, he was drafted by the incoming Reagan administration, where he stayed for eight years. We kept in touch ever since.

When the Soviet Union collapsed in 1991, Schultz as Secretary of State was instrumental in managing the event so that it stayed peaceful….and moved forward. I later flew to Berlin to watch the Russian Army pull its troops out of my former home.

In his later years, George was very active in the Marines Memorial Association where I got to know him very well, he often was wearing his full-dress blues looking as new as if they came out of the factory that day, bringing a fascinating series of military speakers.

As Schultz got older, he couldn’t remember what he knew was top-secret or classified, and what wasn’t. I benefited greatly from that, but kept my mouth shut. However, I learned some amazing things.

He was also very active in arms control and flew to Moscow as recently as 2019. In recent years, I help him to the podium, George grasping my arm and walking his slow shuffle.

George Schultz was a great example of the best leaders that American can produce. He will be missed.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 8, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HISTORY IS REPEATING),

(SPY), (INDU), (TLT), (TBT) (TSLA), (DAL), (BA)

When I was 13 years old in 1965, the week-long Watts Riots broke out in impoverished South Los Angles, killing 34. It was sparked by a police arrest for reckless driving.

While the ruins were still smoking, my dad drove me downtown to view the wreckage. Prudently, he kept his loaded Marine 1911 Browning .45 caliber automatic under a newspaper on the front seat. It looked like a war zone, with some 256 buildings burned to the ground and another 200 looted.

I have been running towards the sound of guns ever since.

Some 55 years later, we are seeing history repeat itself. However, instead of seeing the riots occur in major cities one at a time, as they did in the 1960s, we saw demonstrations and riots in 356 US cities all at the same time!

The impact on the economy, and eventually the stock market, will be immense.

As a long term follower of the structure of the US economy, what is going on now is utterly fascinating. A million connections within the economy have been severed forever and a million new ones created, which few understand.

The end result will be a far more efficient and profitable form of American capitalism. Companies are rebuilding time-tested business models in weeks. Those who can discern these new connections early will make fortunes. Those who don’t will dry up and blow away like so much dust into the ashcan of history.

Of course, the defining announcement of the week came on Friday morning with the Headline Unemployment Rate, which delivered a blockbuster FALL, from 14.7% to 13.3%, sending stock up 1,000 points. It’s proof that the stimulus is largely going into the stock market.

Economist forecasts were off by a whopping 10 million jobs, delivering the biggest miss in history. Leisure and Hospitality accounted for 1.2 million job gains, half the total.

Something doesn’t smell right here. How do you miss 10 million jobs? The streets and traffic levels tell me the real jobless rate is more like 20%. I can’t even get into my bank to deposit a check.

I believe the streets.

Look for big downward revisions, which may pose another threat to the market, and possibly a secondary crash, but not for another month.

A client told me last week that he wishes there were major market crashes more often where he could load the boat with deep out-of-the-money LEAPS which then double or triple in weeks.

He may get his wish. The faster we rise now, the greater the risk of a secondary crash which could wipe out half the recent gains.

I managed to catch the bottom of the biggest stock market rally of all time with dozens of LEAPS like with (TSLA), (DAL), (UAL), (BRKB), and (BA). I took profits all the way up and went into last week modestly “Risk On.” But the 1,000-point rally on Friday caught me totally by surprise, as it did everyone else.

I’m sorry, but I guess I’m lousy at trading those once in hundred-year events.

My saving grace has been the most aggressive, in-your-face short positions in the bond market (TLT), (TBT) in the 13-year history of this letter at the same time. It’s still a great trade. Selling short US Treasury bonds now with a 0.90% yield is the same as buying the Dow Average at 20,000….again.

Pending Home Sales collapsed 21.8% in April and off 33.8% YOY on a signed contract basis. These are the worst numbers since the data series started. The West was hardest hit, down 50%. No wonder I’ve seen so many real estate agents at the beach. We already know that a sharp rebound is underway as Millennials move to the burbs and flee Corona-infested cities. Home prices will be up this year.

Mortgage Demand is soaring as ultra-low rates spur demand. Housing will lead the recovery of the bricks and mortar economy. It will take another year before jumbo loan rates start to decline as banks avoid risk like the plague. Buy (LEN) and (KHB) on dips.

Stocks are the most overbought in 20 years since the top of the Dotcom bubble. Risk is extreme for new longs. Almost all S&P 500 stocks are trading above 50 day moving average. The technical indicators are screaming “SELL”.

Consumer Confidence is recovering as even the slightest bit of reopening looks like a lot coming off of zero. The Conference Board’s consumer confidence index rose to 86.6 this month from 85.7 in April, well up from an expected 82. Call it “green shoots”.

Used Car Prices have crashed with Hertz going bankrupt and defaults on new car loans reaching record levels. Surviving rental companies have cancelled all new car orders. Vacation travel has vaporized. Wells Fargo has ceased lending to car dealers. Time to upgrade that second car?

The greatest 50-day rally in the S&P 500 is now over, up 40% since March 23. Buyers are getting nervous and exhausted and are overdue for a pullback. But the historical six-month gain after a move like this is another 10.2% up, followed by a one-year gain of 17.3%. Over $14 Trillion in Fed and fiscal stimulus can go a long way.

US Factory Orders collapsed further, down 13% in May after a 14% crash in April. Don’t expect these numbers to decline any time soon. The stock market will never notice.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil at a cheap $34 a barrel, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

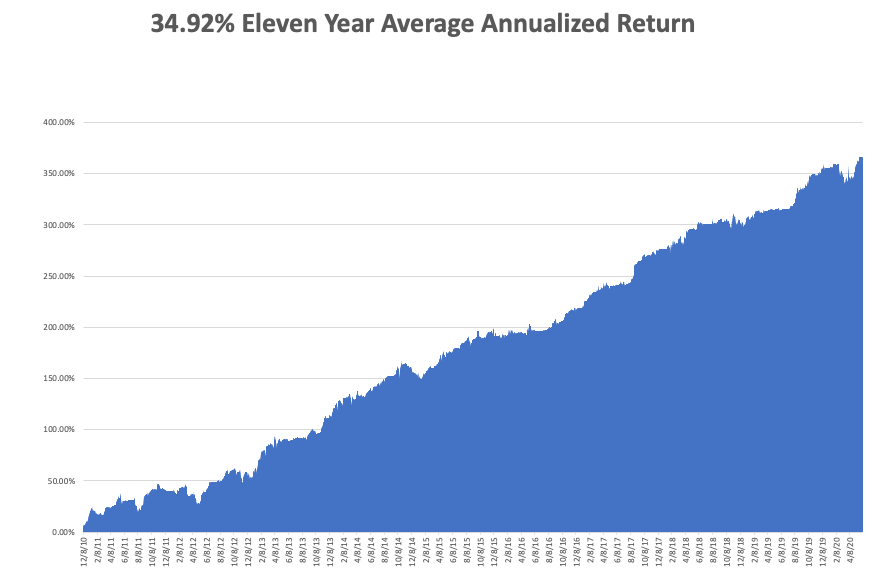

My Global Trading Dispatch performance was up modestly on the week, my downside hedges costing me money in a steadily rising but wildly overbought market. We stand at an eleven-year performance all-time high of 366.68%.

My huge short bond positions, which I have been adding to all the way down, are still delivering big profits. That’s because time decay is really starting to kick in with nine trading days left until the June expiration.

That takes my 2020 YTD return up to a lofty +10.77%. This compares to a loss for the Dow Average of -4.9%, up from -37%. My trailing one-year return exploded to a near-record 52.27%. My eleven-year average annualized profit ballooned to +34.92%.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, June 8 at 8:00 AM EST, Consumer Inflation Expectations for May are announced.

On Tuesday, June 9 at 10:30 AM EST, we learn the NFIB Small Business Optimism Index for May.

On Wednesday, June 10 at 8:15 AM EST, the US Core Inflation Rate for May is printed. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are published.

On Thursday, June 11 at 8:30 AM EST, Weekly Jobless Claims are announced.

On Friday, June 5, at 10:00 AM EST, the University of Michigan Consumer Sentiment figures are out. The Baker Hughes Rig Count follows at 2:00 PM EST.

As for me, I traveled to the local shopping mall to see how real this 2.5 million gain in jobs really exists. More than 50% of the shops were closed, several had already gone bankrupt and traffic was easily below 10% of pre-pandemic levels. Restaurants had maybe 5% of peak traffic sitting at outside tables. Mall police were there to enforce facemask rules.

Nope, not seeing any recovery here. Caveat Emptor.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 11, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEXT GOLDEN AGE HAS ALREADY STARTED)

(TLT), (TBT), (SPY), (INDU), (VIX),

(DAL), (BRK/A), (LUV), (AA), (UAL)

I always get my best ideas when hiking up a steep mountain carrying a heavy backpack.

Yesterday, I was just passing through the 9,000-foot level on the Tahoe Rim Trail when suddenly, the fog lifted and the skies cleared. I was hit with an epiphany.

It was my “AHA” moment.

The next American Golden Age, the next Roaring Twenties, started on March 23.

However, you have to dive deep into investor psychology to reach that astonishing conclusion.

The conundrum of the day is why stocks are trading at a plus 30X multiple two months into a Great Depression. The economic data has been so horrific that the mainstream news has been reporting them.

Some 30 million unemployed on the way to 51 million? Those are Fed numbers, not mine (click here for the link ). Over 52% of small businesses going bankrupt in the next six months? A GDP that is shrinking at an amazing -40% annualized rate?

Yet, we have a Dow Average that has risen a breathtaking 38% in six weeks. The market has essentially dropped 38% and risen 38% over three months, with the Volatility Index (VIX) making a brief visit to the $80 handle.

To understand these massive contradictions, you have to understand what investors think they are buying. They are not hoovering up stocks that are cheap, offer value, or at the bottom of an economic cycle.

Instead, they are investing in a hope, a vision, an expectation that the coming decade will bring a major economic boom. Yes, they are buying my coming American Golden Age.

Only 10% of the value of a stock is reflected in current year earnings, according to Dr. Jeremy Siegal at the Wharton School of Economics (click here to go to the site). The other 90% is in the following nine years. Investors have written off this year’s earnings and are paying up for the following nine.

Long term followers of this newsletter are well aware of my approaching forecast of the next Roaring Twenties (click here for the link).

Except that this time we have a catapult, the pump-priming effects of the pandemic. The government has stepped in with $14 trillion worth of fiscal and monetary stimulus. Creative destruction is taking place at an exponential rate. Companies have to become hyper-efficient overnight or die.

It’s not rocket science. More than 85 million millennials are aging into their peak spending years, buying homes, cars, and all the luxuries of life. Every time this has happened for the past century, US economic growth leaped to 4%.

It happened in the 1920s, the 1960s, the 1990s, and is about to take place in the 2020s. And with each pop in growth, the stock market rises about 400%. Look at your long-term charts and you’ll see I’m dead right.

That takes us from the March 23 Dow Average low at 18,000 up to 72,000 by 2030, except that it’s a low number. Throw in the hyper-acceleration of innovation by the technology and biotech sectors, a Dow 120,000 is within reach.

You may recall that number from my marketing pitches, except that this time it’s happening. In a decade you are going to look like an absolute genius by following the recommendation of the Mad Hedge Fund Trader.

It also means that we may not see market corrections of any more than 10% this year. That would take us down to a Dow Average of 22,500, and an (SPX) of 2,600 in the coming months. That’s where you should jump in and buy with both hands. The only way I would be wrong is if the US epidemic explodes to unimaginable levels, which is not impossible.

Last week, U-6 unemployment rates exploding to a stratospheric 22.8%. The rate was far higher among high school graduates, but only 8% for college grads. Some 20.2 million lost jobs, ten times the previous record, and more than seen during the Great Depression. The BLS (click here) said the true figure was probably 5% higher due to counting anomalies and a huge backlog of data. And this is just the beginning. The good news is that next month, only 10 million jobs will be lost.

NASDAQ (QQQ) turned positive for 2020, and the followers who piled into tech LEAPS at the March bottom are eternally grateful. Tech and biotech are the only places to be. Everywhere else is a waste of time and money. The entire country is turning into a tech economy or going out of business. Buy tech on dips.

Warren Buffet sold all his airline shares, taking a major loss, including Delta (DAL), Southwest (LUV), American (AA) and United (UAL). The Fed’s $50 billion airline bailout blocked him from making a real killing. His Berkshire Hathaway (BRK/A) (click here) owned close to 10% of all of them. The complete collapse of tourism and business travel are the issues. He sees no recovery in the foreseeable future. They don’t call him the “Oracle of Omaha” for nothing.

US Auto Sales are down a mind-blowing -48% in April, the worst on record. Only 8.6 million cars were sold in the US against last year’s annual rate of 17 million. Toyota and Honda saw the biggest falls as their ships can’t unload due to lack of storage space.

The US Treasury will borrow $3 Trillion this Quarter to fund the massive bailout programs. Announced programs amount to 20 times the $789 billion 2009 rescue package, which Republicans opposed. I’m increasing my bond shorts. Sell short (TLT) again, even if we don’t get a decent rally. Oh, and Trump is threatening a default too. He doesn’t see the connection.

Bonds crashed on massive issuance, with the Treasury announcing a record 20-year bond floatation. Yields hit a one-month high. With the (TLT) down $18 from its recent high, I am taking profits on my bond shorts. I’ll be selling the next rally….again. This could be my core trade for the next decade.

Consumer Debt soared to $14.3 trillion in Q1, a new all-time high. A lot of people are living on their credit cards right now.

Trump threatens to cancel China trade deal, blaming them for Covid-19, sending stocks into a 400-point dive. The last time he did this, shares plunged 20%. It’s all part of an effort to divert attention from the administration’s disastrous handling of the pandemic. America’s Corona deaths are now 20 times China’s, and they are still an emerging nation. Just what we needed, a renewed trade war on top of a pandemic-caused Great Depression, as if the market needed more uncertainty. Sell rallies in the (SPY)

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years again, up a gob-smacking +6.46%. We are now only 0.65% short of a new all-time high.

My aggressive short bond positions came in big time on the back of theannounced $3 trillion in new debt issuance in Q2. Short bonds are far and away the better quality trade of buying stocks at these elevated levels.

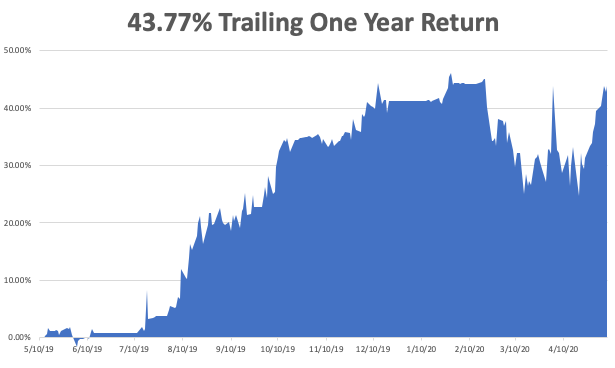

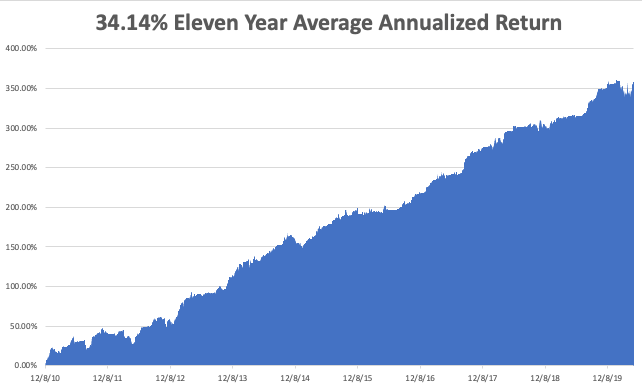

May is up +6.46%, taking my 2020 YTD return up to 2.59%. That compares to a loss for the Dow Average of -13.43% from the February top. My trailing one-year return exploded to 43.77%. My ten-year average annualized profit returned to +34.14%.

This week, Q1 earnings reports continue, and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 11 at 10:00 AM, the April US Inflation Expectations are out. Caesar’s Entertainment (CZR) and Marriot International (MAR) report earnings.

On Tuesday, May 12 at 5:00 PM, the NFIB Small Business Optimism Index for April is released. Toyota Motors (TM) reports earnings.

On Wednesday, May 13 at 9:30 AM, the ever fascinating weekly Cushing Crude Oil Stocks is announced. Cisco Systems (CSCO) reports earnings.

On Thursday, May 14 at 8:30 AM, we get another blockbuster Weekly Jobless Claims. Advanced Micro Devices (AMD) reports earnings.

On Friday, May 15 at 7:30, AM the Empire State Manufacturing Index is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll continue my solo circumlocution of the 160 mile Tahoe Rim Trail every afternoon in ten-mile segments. Why solo? Do you know anyone else who wants to hike 160 miles at 10,000 feet in two weeks?

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 8, 2020

Fiat Lux

Featured Trade:

(MAY 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(UNG), (UAL), (DAL), (INDU), (SPY), (SDS),

(P), (BA), (TWTR), (GLD), (TLT), (TBT)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 6 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What broker do you use? The last four bond trades I couldn’t get done.

A: That is purely a function of selling into a falling market. The bond market started to collapse 2 weeks ago. We got into the very beginning of that. We put out seven trade alerts to sell bonds, we’re out of five of them now. And whenever you hit the market with a sell, everyone just automatically drops their bids among the market makers. It’s hard to get an accurate, executable price when a market is falling that fast. The important point is that you were given the right asset class with a ticker symbol and the right direction and that is golden. People who have been with my service for a long time learn how to work around these trade alerts.

Q: Is there any specific catalyst apart from the second wave that will trigger the expected selloff?

A: First of all, if corona deaths go from 2 to 3, 4, 5 thousand a day, that could take us back down to the lows. Also, the market is currently expecting a V-shaped recovery in the economy which is not going to happen. The best we can get is a U-shape and the worst is an L-shape, which is no recovery at all. What if everything opens up and no customers show? This is almost certain to happen in the beginning.

Q: How long will the depression last?

A: Initially, I thought we could get out of this in 3-6 months. As more data comes in and the damage to the economy becomes known, I would say more like 6-9, or even 9-12 months.

Q: In natural gas, the (UNG) chart looks like a bullish breakout. Does it seem like a good trade?

A: No, the energy disaster is far from over. We still have a massive supply/demand gap. And with (UNG), you want to be especially careful because there is an enormous contango—up to 50 or 100% a year—between the spot price and the one-year contract price, which (UNG) owns. Once I saw the spot price of natural gas rise by 40% and the (UNG) fell by 40%. So, you could have a chart on the (UNG) which looks bullish, but the actual spot prices in front month could be bearish. That's almost certainly what’s going to happen. In fact, a lot of people are predicting negative prices again on the June oil contract futures expiration, which comes in a couple of weeks.

Q: What about LEAPS on United (UAL) and Delta (DAL)?

A: I am withdrawing all of my recommendations for LEAPS on the airlines. When Warren Buffet sells a sector for an enormous loss, I'm not inclined to argue with him. It’s really hard to visualize the airlines coming out of this without a complete government takeover and wipeout of all existing equity investors. Airlines have only enough cash to survive, at best, 6-8 months of zero sales, and when they do start up, they will have more virus-related costs, so I would just rather invest in tech stocks. If you’re in, I would get out even if it means taking a loss. They don’t call him the Oracle of Omaha for nothing.

Q: Any reason not to do bullish LEAPS on a selloff?

A: None at all, that is the best thing you can do. And I’m not doing LEAPS right now, I’m putting out lists of LEAPS to buy on a selloff, but I wouldn't be buying any right now. You’d be much better off waiting. Firstly, you get a longer expiration, and secondly, you get a much better price if you could buy a LEAP on a 2,000 or 3,000 point selloff in the Dow Average (INDU).

Q: Would you add the 2X ProShares Ultra Short S&P 500 (SDS) position here if you did not get on the original alert?

A: I would, I would just do a single 10% weighting. But don’t expect too much out of it, maybe you'll get a couple of points. And it’s also a good hedge for any longs you have.

Q: What happens if the second wave in the epidemic is smaller?

A: Second waves are always bigger because they’re starting off with a much larger base. There isn't a scientist out there expecting a smaller second wave than the first one. So, I wouldn't be making any investment bets on that.

Q: Pfizer (P) and others seem close to having a vaccine, moving on to human trials. Does that play into your view?

A: No, because no one has a vaccine that works yet. They may be getting tons of P.R. from the administration about potential vaccines, but the actual fact is that these are much more difficult to develop than most people understand. They have been trying to find an AIDS vaccine for 40 years and a cancer vaccine for 100 years. And it takes a year of testing just to see if they work at all. A bad vaccine could kill off a sizeable chunk of the US population. We’ve been taking flu shots for 30 years and they haven’t eliminated the flu because it keeps evolving, and it looks like coronavirus may be one of those. You may get better antivirals for treatment once you get the disease, but a vaccine is a good time off, if ever.

Q: Is this a good time to buy Boeing (BA)?

A: No, it’s too risky. The administration keeps pushing off the approval date for the 737 MAX because the planes are made in a blue state, Washington. The main customers of (BA), the airlines, are all going broke. I would imagine that their 1,000-plane order book has shrunk considerably. Go buy more tech instead, or a hotel or a home builder if you really want to roll the dice.

Q: How can the market actually drop to the lows, taking massive support from the Fed and further injections into account?

A: I don’t think we will get to new lows, I think we may test the lows. And my argument has been that we give half of the recent gains, which would take us down to 21,000 in the Dow and 2400 in the (SPX). But I've been waiting for a month for that to happen and it's not happening, which is why I've also developed my sideways scenario. That said, a lot of single stocks will go to new all-time lows, such as in retailers (RTF) and airlines (JETS).

Q: Would you stay in a Twitter (TWTR) LEAP?

A: If you have a profit, I would take it.

Q: What about Walt Disney (DIS)?

A: There are so many things wrong with Disney right now. Even though it's a great company for the long term, I'm waiting for more of a selloff, at least another $10. It’s actually rallying today on the earnings report. Around the low $90s I would really love to get into LEAPS on this. I think more bad news has to hit the stock for it to get lower.

Q: Are you continuing to play the (TLT)?

A: Absolutely yes, however, we’re at a level now where I want to take a break, let the market digest its recent fall, see if we can get any kind of a rally to sell into. I’ll sell into the next five-point rally.

Q: Any reason not to do calls outright versus spreads on LEAPS?

A: With LEAPS, because you are long and short, you could take a much larger position and therefore get a much bigger profit on a rise in the stock. Outright calls right now are some of the most expensive they’ve ever been. So, you really need to get something like a $10 or $15 rise in the stock just to break even on the premium that you’re paying. Calls are only good if you expect a very immediate short term move up in the stop in a matter of days. LEAPS you can run for two years.

Q: Is gold (GLD) still a buy?

A: Yes, the fundamental argument for gold is stronger than ever. However, it has been tracking one for one with the stock market lately. That's why I'm staying out of gold—I’d rather wait for a selloff in stocks to take gold down; then I’ll be in there as a buyer.

Q: Should I take profits on what I bought in April and reestablish on a correction?

A: Absolutely. If you have monster profits on a lot of these tech LEAPS you bought in the March/early April lows, then yes, I would take them. I think you will get another shot to buy these cheaper, and by coming out now and coming in later, you get to extend your maturity, which is always good in the LEAPS world.

Q: Would you buy casinos, or is it the same risk as the airlines?

A: I would buy casinos and hotels—they have a greater probability of survival than the airlines and a lot less debt, although they’re going to be losing money for years. I don’t know exactly how the casinos plan on getting out of this.

Q: Should we exit ProShares ultra short 20+ year Treasury Bond Fund (TBT) now?

A: No, that’s more of a longer-term trade. I would hang on to that—you could get from $16 to $20 or $25 in the foreseeable future if our down move in bond continues.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 28, 2020

Fiat Lux

Featured Trade:

(EIGHT "REOPENING" STOCKS TO BUY AT THE MARKET BOTTOM)

(UAL), (DAL), (UNP), (CSX), (WYNN), (MGM), (BRK/A), (BA)

With the massive technology rally off the March 23 market bottom, the risk/reward for entering new trades has dramatically shifted.

Back then. I was begging followers to load the boat with the best big tech and biotech & healthcare names with call options and two-year LEAPS (Long Term Equity Participation Securities).

One reader told me he bought Humana (HUM) call options for 70 cents and sold them for a breathtaking $30 for a profit of 4,280%! FedEx showed up with a bottle of single malt Glenfiddich Scotch whiskey the next day.

The times have changed. Many tech stocks are now only a few dollars short of new all-time highs, like Microsoft (MSFT) and Apple (AAPL), or are at all tie highs, such as Amazon (AMZN), Teledoc (TDOC), and Zoom (ZM).

What a difference 6,000 Dow points make!

As a result, it is far more interesting now to pick up stocks that currently look like potential chapter 11 candidates, but will likely prosper once the American economy starts to reopen. Call it my “Reopening Portfolio.”

You can buy any of the stocks below outright, sit on them, and probably reap a double over the next two years. However, if you are a much more aggressive kind of trader like me, then you might consider LEAPS, where 500%-%1,000% profits are possible.

The advantage of a stock or a two-year LEAPS is that if we get a second Coronavirus wave in the fall, which is highly likely, you can outlast any short term pain and still come out a huge winner.

Some of these names we sold short at the market top and made a killing. It is now time to flip to the other side.

I am often asked how professional hedge fund traders invest their personal money. They all do the exact same thing. They wait for a market crash like we are seeing now and buy the longest-term LEAPS (Long Term Equity Participation Securities) possible for their favorite names.

The reasons are very simple. The risk on LEAPS is limited. You can’t lose any more than you put in. At the same time, they permit enormous amounts of leverage.

Two years out, the longest maturity available for most LEAPS, allow plenty of time for the world and the markets to get back on an even keel. Recessions, pandemics, hurricanes, oil shocks, interest rate spikes, and political instability all go away within two years and pave the way for dramatic stock market recoveries.

You just put them away and forget about them. Wake me up when it is 2022.

I put together this portfolio using the following parameters. I set the strike prices just short of the all-time highs set two weeks ago. I went for the maximum maturity. I used today’s prices. And of course, I picked the names that have the best long-term outlooks.

You should only buy LEAPS of the best quality companies with the rosiest growth prospects and rock-solid balance sheets to be certain they will still be around in two years. I’m talking about picking up Cadillacs, Rolls Royces, and even Ferraris at fire-sale prices. Don’t waste your money on speculative low-quality stocks that may never come back.

If you buy LEAPS at these prices and the stocks all go to new highs, then you should earn an average 131.8% profit from an average stock price increase of only 17.6%.

That is a staggering return 7.7 times greater than the underlying stock gain. And let’s face it. None of the companies below are going to zero, ever. Now you know why hedge fund traders only employ this strategy.

There is a smarter way to execute this portfolio. Put in throw away crash bids at levels so low they will only get executed on the next cataclysmic 1,000-point down day in the Dow Average.

You can play around with the strike prices all you want. Going farther out of the money increases your returns, but raises your risk as well. Going closer to the money reduces risk and returns, but the gains are still a multiple of the underlying stock.

Buying when everyone else is throwing up on their shoes is always the best policy. That way, your return will rise to ten times the move in the underlying stock.

If you are unable or unwilling to trade options, then you will do well buying the underlying shares outright.

Enjoy.

United Airlines (UAL) just raised $1 billion in a new equity issue to tide it over hard times. That is just a drop in the bucket for what it needs. It’s hard to imagine the company coming through the crisis without any government involvement. The most likely is for the feds to offer a big chunk of cash in exchange for a minority ownership. Around 35% might work, which is the portion the US Treasury of General Motors (GM) during the 2008-09 crash. Still, if you’re looking for a double in the shares, that just water off a duck’s back.

LEAPS: the January 21 2022 $45-$50 vertical bull call spread at a price of 83 cents delivers a 525% gain with the stock at $50, up 94.5% from the current level.

Delta Airlines (DAL) is Warren Buffet’s favorite airline, although he has been selling lately. All of the arguments above apply for this best run of US Airlines.

LEAPS: January 21 2022 $40-$45 vertical bull call spread at a price of 83 cents delivers a 502% gain with the stock at $45, up 98.8% from the current level.

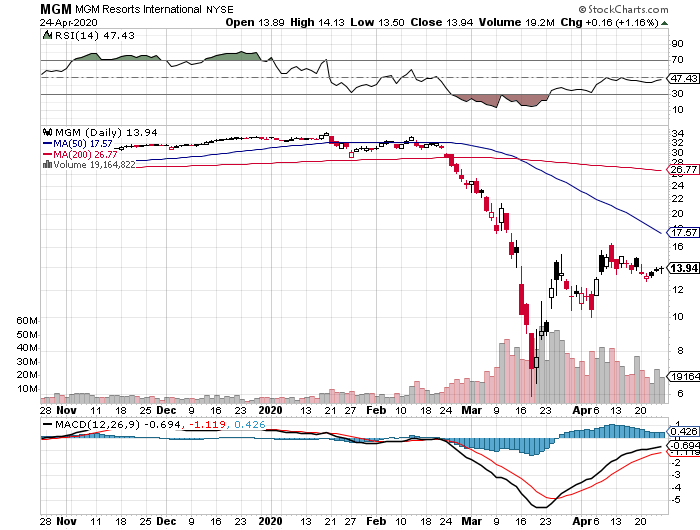

MGM Resorts (MGM)

Yes, Las Vegas is reopening soon, but it certainly won’t resemble the old Vegas. (MGM) is the dominant hotel owner of the strip, owning the Bellagio, Mandalay Bay, Aria Resort, and MGM Grand hotels. It also has a China presence.

LEAPS: the January 21 2022 $25-$30 vertical bull call spread at 75 cents delivers 566% gain with the stock at $30, up 95.6% from the current level.

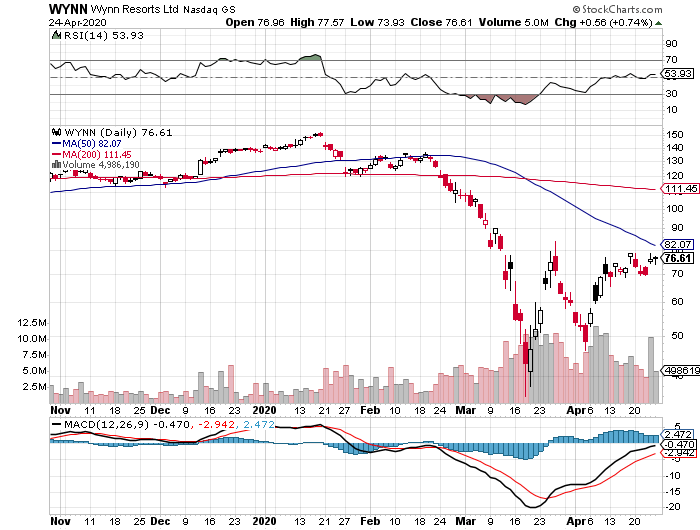

Wynn Hotels (WYNN)

We killed it on the short side with (WYNN), capturing an eye-popping 90% decline. (WYNN) is poised to lead the upturn. It has a major exposure in Macao, where China will lead any economic recovery.

LEAPS: the January 21 2022 $140-$150 vertical bull call spread at 90 cents delivers a 455% gain with the stock at $150, up 81% from the current level.

Union Pacific (UNP)

The reopening of industrial American means a resurgence of railroad traffic. These are not your father’s railroads. Over the last 30 years, they have evolved into highly efficient operators that offer the cheapest way far to over heavy good and bulk commodities, virtually turning into closet high-tech companies. (UNP) had the additional advantage in that as the country’s dominant East/West road, it stands to benefit the most from a recovery in trade with China. That is a likely outcome of any future administration.

LEAPS: the January 21 2022 $180-$185 vertical bull call spread at $1.40 delivers a 257% gain with the stock at $185, up 15.00% from the current level.

CSX Corp. (CSX)

Same arguments here, except that (CSX) wins on North/South trade, especially with Mexico. With a NAFTA 2 new trade agreement in place, this company benefits from an extra turbocharger.

LEAPS: the January 21 2022 $75.00-$77.50 bull call spread at 84 cents delivers a 495% gain with the stock at $77.50, up 16.27% from the current level.

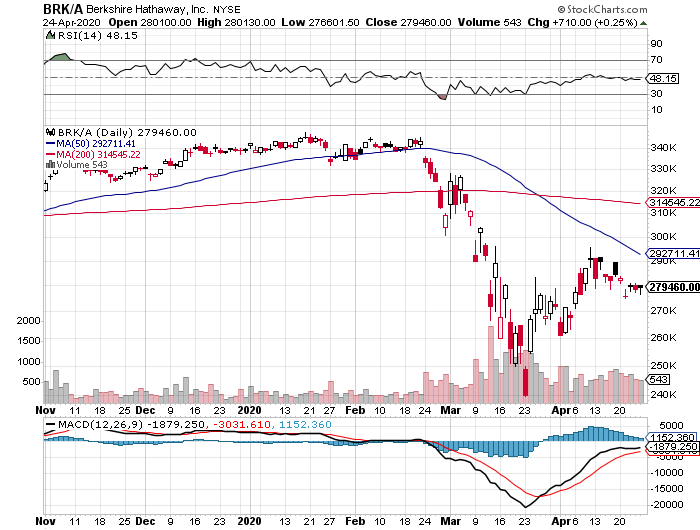

Berkshire Hathaway (BRK/A)

Yes, they make more than sheets these days. Warren Buffet’s flagship holding company is the poster bot for industrial American. The shares are high priced, but after this 32% pullback, you may finally have a chance to get in.

LEAPS: the June 17 2022 $225-$230 vertical bull call spread at $2.61 delivers a 91.5% gain with the stock at $230, up 22.7% from the current level.

Boeing Co. (BA)

This has been the worst falling knife situation in the market for the last two years, cratering from $450 to $85, or down 81%. The decertification of the 737 MAX started the rot, and the grounding of its major airline customers was the coup de grace. This is another company that may require a government bailout and stock ownership, as it is a strategic national value. You may have to wait until the next administration as its Washington State location is currently politically incorrect.

LEAPS: the June 17 2022 $185-$190 bull call spread at $1.25 delivers a 400% gain with the stock at $190, up 47.8% from the current level.

Buy all eight of these and if they all work, your average return will be 411.4%.

Enjoy!