Mad Hedge Technology Letter

May 5, 2025

Fiat Lux

Featured Trade:

(COST OF DIGITAL CONTENT ON THE RISE)

(NFLX), (DIS)

Mad Hedge Technology Letter

May 5, 2025

Fiat Lux

Featured Trade:

(COST OF DIGITAL CONTENT ON THE RISE)

(NFLX), (DIS)

A torpedo has just hit the world of digital content.

The cost of digital content is about to skyrocket as Washington D.C., plans to levy a 100% tariff on movies produced outside the states.

Actually, this is one of Hollywood’s dirty little secrets and a big way they cut costs by outsourcing film production to Eastern Europe or Southeast Asia.

Budapest, Hungary, has become a major hub for studios to geoarbitrage production, and a massive studio has sprouted up in this part of Europe.

Millions of expenses have been saved by not making movies in the United States, and so much has been outsourced that the administration has created a new tariff to get the movie business back in the United States.

I would not say this is anything like a national security threat, even to the point that I would say that Hollywood is more or less socially irrelevant in 2025.

However, corporate entertainment content still moves the needle even if people don’t watch it anymore.

It also keeps people employed, and this is a specific attempt to force whoever is making these movies to return to the United States instead of hiring cheaper Hungarians to make our movies.

Imposing a 100% tariff on all films produced abroad that are then sent into the United States will negate most of the cost savings.

A bombshell like this will hurt employment in the industry, causing companies to fire staff much like tech has been doing for the past few years.

Movie and TV production has been exiting Hollywood for years, heading to locations with tax incentives that make filming cheaper.

Governments around the world have increased credits and cash rebates to attract productions and capture a greater share of the $248 billion that will be spent globally in 2025 to produce content.

All major media companies, including Walt Disney (DIS), Netflix (NFLX), and Universal Pictures, film overseas to increase profits.

Film and television production has fallen by nearly 40% over the last decade in Hollywood’s home city of Los Angeles, because of the outrageous cost of doing business in the state of California.

The January wildfires accelerated concerns that producers may look outside Los Angeles, and that camera operators, costume designers, sound technicians, and other behind-the-scenes workers may move out of town rather than try to rebuild in their neighborhoods.

Ultimately, this tariff is devastating to digital content.

This is also on the heels of China limiting Hollywood to only 10 movie imports into China per year.

The city of Los Angeles is about to face a rash of job losses as digital content companies will turn to AI to fill out the rest of the production.

Much less content will be made if these large budget productions of over $20 million cannot be outsourced to cheaper global south employees.

In general, the cost of creating digital content will increase and be painful for the average content maker.

Who does this favor?

Those individual YouTubers who go around filming on a selfie stick while simultaneously editing their own content.

Any digital content company masquerading as a global Titanic will need to shrink accordingly and get leaner.

Americans will need to think twice whether to develop production outside of the United States with this new steep cost.

Companies that will be hurt from this are Netflix, Disney, Amazon, and Comcast.

If these executives don’t pay the tariffs, they could even find themselves locked up in Alcatraz.

Who would have thought that a few days ago?

Mad Hedge Technology Letter

January 6, 2025

Fiat Lux

Featured Trade:

(DIGITAL SPORTS CONTENT RISES TO THE TOP)

(FUBO), (DIS)

It isn’t a shocker that the first deal to go through in 2025 is in digital sports streaming.

This sub-sector is scorching hot.

It was only just a few days ago when Netflix rolled out its debut in streaming NFL during Christmas when they broadcasted 2 games.

Live American football – not the European variant - is the holy grail of digital content and the beefiest of marketers with the deepest of pockets will cough up to place their ads in these commercial slots.

Disney (DIS) will combine its Hulu + Live TV business with sports streamer FuboTV (FUBO) in the first major media dealmaking move of 2025.

Disney will control 70% of Fubo. Shareholders of the sports streamer will own the remaining 30% of the combined business, which will operate under the Fubo publicly traded company name.

Disney is struggling in many parts of their business, for example, is underperforming in their theme parks.

Their movies also suck.

Pro football is the last bastion of premium content and even the woke employees at Disney understand that.

Disney stock has essentially halved since 2021 with shareholders furious about their lack of strategic vision.

The acquisition of Fubo gives Disney a chance to restart in a sub-sector that has a glowing future.

Cord cutters are exploding and since last year’s Presidential election, the trust in legacy media has never been at such a low ebb, and rightly so with the poor level of content quality.

The combination of the two businesses will form one of the largest digital pay-TV providers as consumers search for cable alternatives amid increased cord-cutting.

Fubo, which offers users access to live TV channels over the internet, has primarily focused on sports.

Hulu + Live TV, categorized as a cable replacement option — similar to YouTube TV — allows users to stream from about 100 live TV channels across sports, news, and entertainment.

As a much smaller player, Fubo struggled with high content costs and the ability to curb subscriber churn and adequately compete in the marketplace — hence the lawsuit's inception.

The three companies first announced the joint venture last year, with an expected price point of $42.99 a month. The service will bring together their respective slates of sports rights and comes as media companies face pressure from investors to scale their streaming services and achieve profitability.

I’m not saying that digital streaming of pro sports is easy.

We aren’t in the early innings.

Content costs are astronomically high and subscriber churn can be a problem in the offseason.

The nightmare could end up like the NBA.

Look at sports like pro basketball (NBA, viewership is down 50% this season as subscribers flee the sinking ship.

The basketball commissioner created a model where most teams make the playoffs meaning the 82 game schedule has been deemed irrelevant causing their best stars to sit out games.

It’s just one example of the management of pro sports going down the drain and pro football isn’t immune to bad management too.

As it stands, I highly support Disney’s foray into Fubo and Fubo would be a great stock to pick up and hold at $4.80.

The stock is up from $1.44 this morning.

Live pro sports still fetches a premium and I don’t believe that will change any time soon.

Jump into tech stocks that have big investments planned in American football.

Much of the big growth opportunities have been saturated and I do believe the tech market will become more of a zig-zag trading market in 2025.

Global Market Comments

March 22, 2024

Fiat Lux

Featured Trade:

(MARCH 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(DIS), (GLD), (BITB), (UUP), (FXY), (F), (TSLA), (NVDA), (FCX), (UNG), (TLT), (MCD)

Below please find subscribers’ Q&A for the March 20 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley.

Q: Do you recommend a form of dollar-cost averaging, and what is it?

A: Absolutely, yes. It is impossible for anybody to get an absolute bottom when you're buying, so the best thing to do is time average. If you have a position you like, go in there every day and buy a little piece. I bought Nvidia (NVDA) practically every day for months and boy did that work! (NVDA) had already gone up a lot, but I just kept buying it and buying it, averaging up and up. So that is the way I dollar-cost average. It's really more of a time averaging than a price averaging. No one knows where tops and bottoms are, even if they promise you that they do.

Q: Are you still long the Yen (FXY) and shorting the Dollar (UUP) given current conditions?

A: I actually don’t have any positions in the currencies, because the volatility is so low compared to stocks. Suffice to say that over time when US interest rates go down, currencies should go up, especially the Yen, which has been depressed for such a long time.

Q: Can gold (GLD) and Bitcoin (BITB) go up at the same time?

A: Absolutely. They almost always go up at the same time, because they are liquidity-driven assets, and when liquidity is as rich as it is now, all liquidity-driven assets go up at the same time which includes gold, silver, and Bitcoin and other cryptos. The only difference this time is that the source of liquidity is not the Federal Reserve—in fact, the Fed is quite restrictive right now with their high-interest rate policy—the new source of liquidity is corporate profits, especially from technology stocks, and that is unlimited and not subject to political whims. It’s always there and it’s always growing; it's a much better form of liquidity than the old form from the US government.

Q: What are your thoughts on the Disney (DIS) and Peltz fight, and how should that affect the stock price?

A: Whenever Nelson Peltz gets involved in a company, it's almost always positive for the stock even if he makes boards uncomfortable. That's why he's going in—to force better management. He usually succeeds and then gets out at a higher price. And if it means forcing some things on management they don't like (and I'm not really sure in the case of Disney what it is he's pressuring them for), he gets his profit and he leaves, and that's what corporate raiders do.

Q: Should I buy the dip in the EV narrative?

A: Not yet. You need a global economic recovery for that to happen, especially in Europe and China. We forget how prosperous we are here, and how weak things are in pretty much the rest of the world—and that is where the EV sales have really collapsed. So let the burden of proof be on the EV companies to report better sales and better technology, and then I'll be back in. Tesla periodically has 80% corrections: we’re right at the tail end of one of those. We may have another 10% to go and that's it. I'm a fair-weather friend, I only like to be long stocks when they're going up. How about that?

Q: I am understanding correctly that you believe the transition from technology and semiconductors to commodities and elsewhere is actually showing long-term strength growth for the tech stocks since they are mostly going sideways from here and not crashing with the rotation.

A: What I see is a time correction in technology where after tremendous moves they go sideways for a period, and new money switches over to other sectors like commodities and energy. And then you'll have a rotation back into technology after they've had a rest, probably before the end of the year. This back-and-forth kind of action could go on for many years—I've seen this happen before. So that's what I'm trying to position for now. And you know, I'm not alone in saying I don't like buying stocks after they tripled in a year. It's almost a no-win trade if you're a professional manager.

Q: Are we heading towards $90 a barrel in oil (USO), and will we pass $100?

A: Yes, we’re definitely headed to $90. But I think the new range is sort of like $65 to $95 because when you get up to the high prices, all of a sudden supply starts coming out of the woodwork, especially from the United States, which is already the world's largest oil producer at 13 million barrels a day. As soon as you get a high price, money just starts pouring in to start new drilling, setting up the next price collapse. The United States is the cap on global oil prices and China is the floor. They come in as the buyer of last resort as the world's largest consumer whenever prices get super cheap, and that actually is a best-case scenario—not only for us but for OPEC. Because their investments do well in the US when oil is in a $65 to $95 range. Any higher than that, the stock market crashes, wiping out the value of their savings. And that is how the modern world has evolved.

Q: Will today's Fed meeting be a non-event?

A: Yes, no interest rate changes until June, maybe even later. And the market is basically telling us that—dead in the water as it is. Dow is nowhere, and there are no big moves. Everyone is just treading water here.

Q: Would you take profits on NVIDIA (NVDA)?

A: Yes, some profits. I structured my own personal portfolio so I have expiring front month short put positions, which are ringing the cash register every month, but my long-term LEAPS I'm keeping. Because I think you could have another 50% move up in a year in (NVDA) stock given their dominant position in the market, and the fact that the new Blackwell chip, the $40,000 Blackwell chip is taking over the world. It's essentially a computer on its own, and it writes its own software. Nobody else is close to that, nor will they be. So keep the long-term positions to LEAPS, and keep taking profits every month. And you have to keep in mind also that (NVDA) is almost every portfolio manager's larger single position through capital appreciation, or they're not in it at all, and they're looking for a job or driving an Uber cab somewhere.

Q: Should I buy Ford (F) or Tesla (TSLA) or both?

A: Wait for the market to start discounting the Tesla Model 2 when it comes out next year. Maybe you start buying the stock in 6 months or a year. Probably the better question is not Ford or Tesla, but Tesla or Rivian (RIVN), which seems to be making progress in their mass production. I just don't see any future for the legacy car companies at all. They're just so far behind in technology. I spent most of my life trying to tell them what to do, and if they had followed my advice, they would be much better off than now.

Q: How long can an employment number stay strong? I feel like we have been waiting for a recession for almost 5 years now.

A: Actually the last real recession was the pandemic in 2020, which only lasted a couple of quarters. We may not have another real recession for 5 or 10 years. Why? Because we're in the roaring twenties and we have 6 more years to go. We also are in the new American Golden Age, and who's been predicting that for the last 10 years? I have! It's all about demographics. We happen to have peak spenders, i.e. people in their thirties and forties, at all-time highs, and that is what drives the economy—that is what makes the golden ages predictable as they have been for hundreds of years.

Q: How are the stem cell injections working?

A: Fantastic. After I got shot in the hip last year in Ukraine, I got one and I literally was walking around in weeks and eliminated the pain completely. I went from talking about hip replacement to climbing Kilimanjaro in literally a matter of weeks. So yes, they work for me. I know they don't work for everyone, but I've used them on both my knees, my back, and my hip, and they've been wildly successful. I won't need any more stem cell injections until I go back to Ukraine and get shot again.

Q: Where are you traveling to this time?

A: I’ll be working out of Florida during April, and probably take the quickie trip to Cuba. After that, it's Ecuador and the Galapagos Islands where I want to challenge Darwin’s Theory of Evolution. It turns out that it is in the same time zone as New York, so it'll be easy to work there from a time zone point of view. The Space X Starlink has provided great Internet everywhere, the Galapagos and Ukraine.

Q: Our real estate commission is about to disappear. Will that benefit housing prices?

A: You get what you pay for. If you have commissions drop from 6% to 1%, you'll get 1% worth of the service out of your agent. So if you want your house sold and sold well, you’d better keep paying the commission. Otherwise, your agent will not work for it. You get what you pay for. However, I always thought real estate commissions were too high for too long, and that may be about to change. And if you don't believe me, try selling your house on the internet someday. It doesn't work.

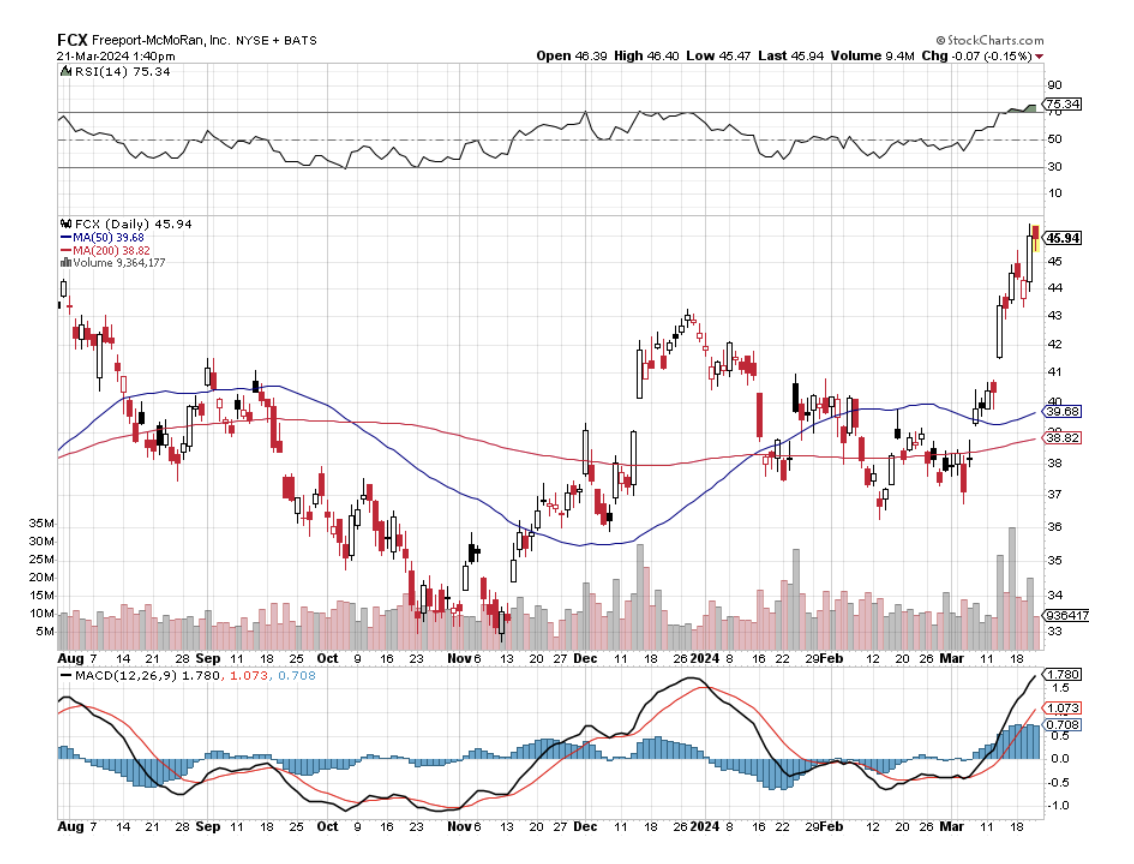

Q: Does the US have the infrastructure for electrification?

A: No, it does not. That means it has to be built out, and that is why we own Freeport McMoRan (FCX) and you should too! Anything involving electrification involves a lot of copper. The grid has to double in size to accommodate the needs of AI.

Q: Should I continue with natural gas (UNG)?

A: If you have a long-term position I would hang on because you're only one cold snap away from a major rally, and at some point, China will come back on stream as a major buyer. So long term I would hold it. Short term positions I would get rid of it before accelerated time decay wipes out your position.

Q: Will the US 10-year Treasury bond (TLT) go below 4% again?

A: Yes, when you get the Fed on an interest rate cutting cycle, 4% is easy; and by the way, home mortgages will be much cheaper in a year, so it's probably not a bad idea if you're buying a home now to take an adjustable-rate mortgage (ARM) then refinance after the Fed finishing cutting rates.

Q: Should I buy the dip in McDonald's (MCD)?

A: Probably not. The concern there is that the weight loss drugs are destroying American appetites and reducing their need for fast food. Eventually, some 100 million Americans could end up taking weight loss drugs. So that's why the stock is sold off. Fundamentally, (MCD) is a low-margin retail play so it's never interested me. The good news is that they're cutting jobs with computers. So that is the only reason to buy it, is the computerization effort. Walk into a new McDonald’s and you can only order by computer. The people there don’t even know how to take a verbal order. This is even more widespread in Europe where labor costs are higher.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Home Sweet Home

Global Market Comments

September 22, 2023

Fiat Lux

Featured Trade:

(SEPTEMBER 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(AMZN), (SPX), (TLT), (TSLA), (DIS), (LEN), (KBH), (PHM), (USO), (FXA), (UNG), (JPM), (C), (BAC)

Below please find subscribers’ Q&A for the September 20 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: How do we know when interest rates have peaked?

A: Well, that's easy—the Fed announces it and they start cutting interest rates. The first hint of that is they don’t raise interest rates when they have the opportunity to do so. That will be today as it was in July. So we’re at the top now, and they’ll probably go sideways for 6 months or even longer before they start cutting. Markets will start to discount this 6-9 months in advance, or about now.

Q: Year-end target for the S&P 500? What about Amazon (AMZN)?

A: 5,000. For the (SPX). For Amazon, I think we could easily tack on another 20-25%.

Q: Does the Mad Hedge Global Trading Dispatch include tech trade alerts?

A: It does, but only the higher quality, lower risk trades. Pure Tech traders are a much higher-risk bunch of people, and they want more aggressive trade alerts in smaller companies. As for me, with Global Trading Dispatch I try to stick to a 90% success rate, and the only way to do that is to avoid tech when it flatlines and not try to catch any falling knives.

Q: Any hope of recovery for the iShares 20 Plus Year Treasury Bond ETF (TLT)?

A: Yes; as I said, the Fed will start cutting interest rates next year, and markets discount 6-9 months in advance, so that gives us 3 months for our January 2024 $100/$105 call spreads to expire at max profit. So yes, it is entirely possible, if not likely, that we will see those numbers by January.

Q: Can you help me jump the line for a Cybertruck from Tesla (TSLA)?

A: Well, if I was going to help anyone get a Cybertruck, it would be me! And I can't get one. Back in the old days, Tesla people would fall down on their knees crying “thank you!” when you bought one of their cars. Now, I think I’m number 2 million on the waiting list. You’re on your own on that one.

Q: Is Disney (DIS) a good LEAP stock?

A: No, Disney has some major problems with their streaming business, and the parks have maxed out. That is why the stock seems immune to good news—unless you know something I don’t. So go for it if you’re ready for that risk.

Q: What is your fact-finding trip to Ukraine all about?

A: Nothing beats research on the ground for finding out what really happened. Second, Ukraine got a lot of aid from other countries when the war started, but it’s since run out and we know that hospitals and orphanages in Ukraine are in trouble and running out of money. So, nothing beats showing up with US dollar cash in that situation. So that is why I’m going. This’ll be my eighth war. I guess the war correspondent in me never left. I’ll also be escorting American doctors to Ukrainian hospitals who don’t know how to do this. There’s more to life than just making money.

Q: Should I buy the dip in homebuilders like Lennar Homes (LEN), D.R. Horton (DHI), and KB Homes (KBH)?

A: Absolutely, yes—with both hands. Who does better with a falling interest rate cycle than home builders who have to depend on falling mortgage rates for business to boom once again. So yes, any dip in this sector and I would be loading the boat. The next declining interest rate cycle could last 5 or 10 years.

Q: Will the United Auto Workers strikes cause inflation to rocket and feed into higher inflation figures?

A: No, not really. Union membership has declined by 75% over the last 40 years. The UAW itself has declined from 1.6 million members to 400,000, and they really have become too small to affect the general economy. What they will do is accelerate existing trends, like people dumping their ice cars and moving to Tesla and other EV manufacturers. This is sort of like a gift for Tesla, and that's why the stock was up 10% last week. Also, in the long, long run, if they force the car companies to move to Mexico and cut the same deals that Elon Musk got, then it reduces inflation.

Q: Does the recent increase in Chinese ships and warplanes near Taiwan change anything?

A: No, it just shows us how weak the economy in China is. It’s effectively in recession even though they refuse to admit it, and therefore they have to create more distractions. The Chinese have been bluffing on Taiwan for 70 years—why stop now?

Q: What is a good time to buy banks?

A: I would start scaling into (JPM), (BAC), and (C) now. They will be a major beneficiary of an economic recovery next year and falling interest rates; and the prices down here are good. They’re one of the worst performers so far this year—one of the few cheap sectors left in the market.

Q: Should I buy Tesla (TSLA) here?

A: The thing here that I’m telling my professional money managers is: scale in on a one-month basis. Figure out how much you want to buy, and then buy 1/30th of that amount every day for a month. Then, you’ll scale in, you won’t get the absolute bottom but you’ll get some kind of bottom, and when a turnaround happens, then it goes up 50% or 100%. That’s the way to play Tesla. A lot of the professional money managers and investment advisors who follow me have a problem; they’re getting tons of new customers based on their performance this year. So yes, what do you do when you get money after a great run? You can only scale in.

Q: Is oil (USO) topping and going back to 70 a barrel?

A: I think yes. We saw the run from $70 to $95; it looks like it’ll probably hit $100. After that, Saudi Arabia will start bringing supply back on. What they did is create an artificial short squeeze in oil by taking 5 million barrels off the market with Russia—that got prices up. Any higher than that, and high oil starts to adversely affect Saudi Arabia’s foreign investments. So yes, they do back off when we get over 100; they’re very happy with $100/barrel, as is the American oil industry. So, I’m inclined to take profits if you did the oil trade in June.

Q: Would you buy iShares 20 Plus Year Treasury Bond ETF (TLT) now?

A: No, I’ve been holding back because it seems to want to have a capitulation; that’s why it’s not rallying off the 93 level—it’s been bouncing on the bottom. Some piece of bad news, some kind of high inflation, could trigger a capitulation, which would take us down another 5 points—that's where you buy it. Then, all of a sudden something like a 2024 $85/$90 bull call spread is offering you 100% return one year out.

Q: Do you recommend 4-week T-bills?

A: No, I recommend 4-month T-bills. Those expire in January and take advantage of the cash squeeze in the financial system you always get in New Years. Returns on 4-month T-bills are much higher than 3 month, 2 month, or 1 month. I just bought some before this meeting because I’m not going to do a lot of trading this month, and I got a 5.48% yield. For me to do a trade now, it has to have a very low-risk 20% return. That’s what I need to beat T-bills at 5.48%, which have zero risk and a guaranteed return of money. You need the extra 15% return on a 1-month trade to justify the risk that individual stocks have.

Q: Will the Australian dollar (FXA) stay weak as long as China is weak?

A: Yes, and the flip side is also true: Will the Australian dollar be strong when China recovers? Absolutely. I still see 1 to 1 against the US dollar for the long term.

Q: Why is everyone pouring into short-term options?

A: They’re buying lottery tickets. A lot of people are in the markets not to invest, but to gamble. They have gambling addictions quite often, and nothing beats the instant gratification of a same-day win, even though 80% of the same-day options expire worthless. So, enter that market with caution.

Q: After artificial intelligence destroys 90% of jobs, won’t there be nobody left to buy stocks since stocks won’t go up solely on institutional buying?

A: While AI will destroy a lot of jobs, it’s creating even more jobs—that has always been the case with technology from day one. However, you do get mismatches from the time a job is destroyed to when a new one is created. There are also mismatches in skill levels and that can create turmoil in the economy. Look at the United Auto strike, which is hell-bent on stopping technology and automation—stopping any kind of technology they can. Technology in the long term always destroys jobs, but it also creates more jobs, just moving them from old economies into new industries. I’m sure the same thing went on with the hay and leather industries 120 years ago when we moved from horses to internal combustion cars.

Q: If companies go to a four-day workweek, how will that affect stocks?

A: It’ll probably make them go up. When people go to four-day work weeks, productivity goes up and companies get more output for their dollar of labor costs. That’s why it’s happening and why it’s so popular. People who work at home and get to play with their kids on weekends will work for less money—that is a proven fact.

Q: Any thoughts on when we will see the United States Natural Gas Fund (UNG) turn upward?

A: This winter. (UNG) is priced for perfection, sitting around here at the $7 level. The slightest surprise like a cold winter, for example, which we may get (at least in California we will), and then the thing will spike up.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2018 On the HMS Victory in Plymouth, England

Mad Hedge Technology Letter

September 11, 2023

Fiat Lux

Featured Trade:

(DEATH OF LEGACY MEDIA)

(CHTR), (DIS), (NFLX), (NXST), (DISH)

Negotiations between Spectrum’s parent company, Charter Communications (CHTR), and Walt Disney (DIS) finally got over the impasse and they struck a deal.

No deal for both would have been catastrophic for both.

Disney faced the potential loss of 14.7 million Charter pay TV subscribers, or 20% of ESPN's current linear subscriber base of 74 million.

That equates to linear revenue losses of roughly $5 billion, or 6% of overall revenue.

Cord-cutting has been occurring at a brisk pace in the last few years, but the lack of solidarity among the legacy media negotiators appears to turn the trickle into a breaking of the dam.

What am I talking about?

Disney decided to go nuclear by removing its channels from the cable provider. Charter (CHTR) proposed that Disney (DIS) offer its customers free access to Disney’s streaming services, especially ESPN; Disney rebuffed the offer, but CHTR finally agreed to add Disney+ Basic ad-supported offering being provided to Charter customers who purchase the Spectrum TV Select package at no additional cost, "as part of a wholesale arrangement."

This is really the beginning of the end for legacy media and this melee could trigger a swift bout of consolidation as disagreements become the norm and not the outlier.

It’s no surprise the cost of creating content is going up and these channels like DIS feel they can just pass the costs

Remember that many people pay for cable just to watch college football and the NFL.

Roughly 25% of Charter’s clients engage with Disney content, Charter said on a call last week.

DirecTV is also embroiled in its own content squabble with local broadcast network Nexstar (NXST), which recently pulled over 200 stations in more than 100 metro areas from DirecTV’s network over a similar price dispute.

While the cable TV business has been declining for years, there’s concern this is the last hurrah.

Down the road, the winners out of all of this may be internet TV operators, including YouTube TV, Hulu TV, FuboTV, and Dish’s DISH’s (DISH) Sling. Some of these have been gaining steady traction even before negotiations soured, with Hulu’s web traffic up 7.2% year-over-year in July and Sling’s traffic up 11.8%.

Web traffic may pick up as consumers look for ways to watch their regularly scheduled programming. Online search interest in five major live TV streaming services picked up Sept. 1 when news of Disney’s blackout became public, according to Google Trends data.

I believe that online momentum will translate to a long-term subscriber bump for these companies.

CEO of CHTR Christopher Winfrey and CEO of DIS had to make this deal.

The ongoing chaos in the legacy media markets signals that cord-cutting will supplant the legacy markets within the next 10 years.

Baby Boomers are the last stalwarts of the legacy media market and they are retiring in droves.

Netflix (NFLX) is another streamer that is in line to pick up some of the demand for streaming content.

With high rates, the era of excesses is rearing its ugly head.

Platforms are being careful with the type of agreements they make as less quality content is facing a bleak future.

Live professional sports are lynchpin to why many consumers don’t quit cable.

I believe the next contract cycle will see many pro sports leagues go all streaming much like the American soccer league MLS did with Apple TV.

When pro sports migrate 100% into digital, expect to be outsized winners and losers while distributors like SlingTV should sink like a rock.