Global Market Comments

July 18, 2025

Fiat Lux

Featured Trade:

(JULY 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (SLV), (DHI), (LEN), (CCI), (KRE), (META), (NFLX), (AMZN), (SLB), (PPL), (XOM), (OXY), (AGQ), (WFC), (DXJ), (FXE)

Global Market Comments

July 18, 2025

Fiat Lux

Featured Trade:

(JULY 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (SLV), (DHI), (LEN), (CCI), (KRE), (META), (NFLX), (AMZN), (SLB), (PPL), (XOM), (OXY), (AGQ), (WFC), (DXJ), (FXE)

Global Market Comments

October 17, 2019

Fiat Lux

Featured Trade:

(UPDATING THE MAD HEDGE LONG TERM MODEL PORTFOLIO),

(USO), (XLV), (CI), (CELG), (BIIB), (AMGN), (CRSP), (IBM), (PYPL), (SQ), (JPM), (BAC), (EEM), (DXJ), (FCX), (GLD)

When I first arrived in Japan in 1974, international investors widely expected the country to collapse, a casualty of the overnight quadrupling of oil prices from $3 per barrel to $12, and the global recession that followed.

Japanese borrowers were only able to tap foreign debt markets by paying a 200 basis point premium to the market, a condition that came to be known as ?Japan Rates.?

Hedge fund manager, Kyle Bass, says that the despised Japan rates are about to return. There is nothing less than one quadrillion yen of public debt in Japan today.

A perennial trade surplus powered high corporate and personal savings rates during the eighties and nineties, allowing these agencies to sell their debt entirely to domestic, mostly captive investors.

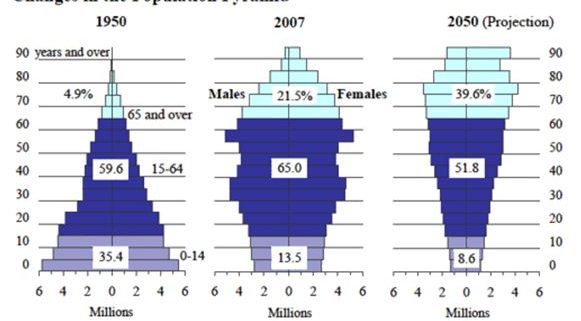

Those days are coming to a close. The problem is that the working age population in Japan has peakedd, and the country is entering a long demographic nightmare (see population pyramids below).

This year, the Ministry of Finance will see ?40 trillion in receivables, the same figure seen in 1985, against ?97 trillion in spending. Interest expense, debt service, and social security spending alone exceed receivables.

The tipping point is close, and when it hits, Japan will have to borrow from abroad in size. Foreign investors all too aware of this distressed income statement will almost certainly demand big risk premiums, possibly several hundred basis points. That?s when the sushi hits the fan.

To top it all, no one in living memory in Japan has ever lost money in the JGB market, so expectations are unsustainably high.

Both the JGB market and the yen can only collapse in the face of these developments. I know that the short JGB trade has killed off more hedge fund managers than all the irate former investors and divorce lawyers in the world combined.

But what Kyle says makes too much sense and the day of reckoning for this long despised financial instrument may be upon us. How much downside risk can there be in shorting a ten-year coupon of negative -0.11%?

Is Kyle trying to show us the writing on the wall?

I was just about to don my backpack and head out for my evening hike when I caught a phone call from Tokyo.

The Bank of Japan had just announced they were implementing negative interest rates for the first time in history. The Japanese yen (FXE), (YCS) was in free fall and the stock market (DXJ) was soaring.

Note to self: don?t ever answer the phone just as I?m heading out the door. Good-bye hike, hello another inch on my waistline.

However, bank stocks were getting destroyed, as they would now have to pay money to the central bank to accept deposits, as they already do in Europe and Switzerland.

The overnight trading in S&P 500 (SPY) futures jumped from unchanged to up 100 points. It looked like January was going to go out with a bang. This could be the mother of all month end window dressings.

It really was a day for moves that made no sense. Bonds (TLT) rose with stocks on the hopes that any Fed interest rate hikes for this year will be cancelled. That?s like dogs and cats laying together.

Gold (GLD) rose modestly, even though the prospect of more quantitative easing anywhere in the world should have caused it to crater.

The US dollar was robust (UUP), just when you?d think that lower for longer interest rates should weaken it. I guess it?s a case of being the best house in a bad neighborhood.

Oil (USO), the main driver of all process for the past six months, was strangely unchanged for a change.

It was really one of those days when you wanted to hurl your empty beer cans at the TV, throw up your hands, and cry.

Personally, I don?t think US risk markets are out of the woods yet. We can?t escape the reality that earning multiples for American companies are falling.

You have to ask the question of what do negative interest rates really mean for the global economy? Hint: none of the answers are good.

Blame it on a Fed tightening cycle, which has just been shifted from second gear back to first. Blame it on a decade long GDP growth rate, which is stuck at 2%. That is caused by demographic headwinds that we can do nothing about.

Whatever the reason, stocks are not headed straight up from here. I think we are just squeezing out the shorts for the umpteenth time. They could all be cleaned out by the time the (SPY) hits $195.

Then it will be back to the low end of our new, violent range, probably just above $182.

You wanted clarity in understanding the current state of play in the global financial markets? Here?s your #$%&*#!! clarity.

You should expect nothing less for this ridiculously expensive service of mine.

But maybe that is the cabin fever talking, now that I have been cooped up in my Tahoe lakefront estate for a week, engaging in deep research and grinding out the Trade Alerts, devoid of any human contact whatsoever.

Or, maybe it?s the high altitude.

I did have one visitor.

A black bear broke into my trash cans last light and spread garbage all over the back yard. He then left his calling card, a giant poop, in my parking space.

Judging by the size of the turds, I would say he was at least 600 pounds. This is why you never take out the trash at night in the High Sierras.

Ah, the delights of Mother Nature!

We certainly live in a confusing, topsy-turvy, tear your hair out world this year. Good news is bad news, bad news worse, and no news the worst of all.

The biggest under performing week of the year for stocks is then followed by the best. Net net, we are absolutely at a zero movement, and lots of clients complaining about poor returns on their investment.

I tallied the year-on-year performance of every major assets class and this is what I found.

+16% - Hedged Japanese Stocks (DXJ)

+15% - Hedged European stocks (HEDJ)

+13% - US dollar basket (UUP)

+10% - My house

0% - Stocks (SPY)

0% -? bonds (TLT)

-5% - Japanese Yen (FXY)

-11% - Euro (FXE)

-12% - Gold (GLD)

-18% -? Oil (USO)

-27% -? Commodities (CU)

-27% - Natural Gas (UNG)

There are some sobering conclusions to be drawn from these numbers.

There were very few opportunities to make money this year. If you were short energy, commodities, and foreign currencies, you did very well.

Followers of the Mad hedge Fund Trader can?t help but know and love these ticker symbols. They?ll notice that our long plays were found among the asset classes with the best performance, while our short bets populated the losers.

The problem with that is most financial advisors are not permitted to place client funds in the sort of inverse or leveraged ETF?s that most benefit from these kinds of moves (like the (YCS), (EUO), and (DUG)).

That left them reading about the success of others in the newspapers, even when they knew these trends were unfolding (through reading this letter).

How frustrating is that?

What was one of my best investments of 2015?

My San Francisco home, which has the additional benefit in that I get to live in it, have a place to stash all my junk, and claim big tax deductions (depreciated home office space, business use of phone, blah, blah, blah).

Of course, I do have the advantage of living in the middle of one of the greatest technology and IPO booms of all time. Every time one of these ?sharing? companies goes public, the value of my home rises by a few hundred grand.

The real problem here is that investing since the end of the Federal Reserve?s quantitative easing program ended a year ago has become a real uphill battle.

While the government was adding $3.9 trillion in funds to the economy we traders enjoyed one of the greatest free lunches of all time. It made us all look like freakin? geniuses!

Just maintaining their present $3.9 trillion balance sheet, not adding to it, has left almost every asset class dead in the water.

Heaven help us if they ever try to unwind some of that debt!

Janet has promised me that she isn?t going to engage in such monetary suicide.

The Fed is continuing with Ben Bernanke?s plan to run all of their Treasury bond holdings into expiration, even if it takes a decade to achieve this. And with deflation accelerating (see charts below), the need for such a desperate action is remote.

Still, one has to ponder the potential implications.

It all kind of makes my own 43% Trade Alert gain in 2015 look pretty good. But I don?t want to boast too much. That tends to invite bad luck and losses, which I would much rather avoid.

Nearly two years ago, the Japanese government introduced the Individual Retirement Account for individual investors in Japan for the first time.

The move was part of Prime Minister Shinzo Abe?s multifaceted efforts to revive Japan?s economy, and could unleash as much as $690 billion in net buying into Japanese equities by 2018.

The move was inspired by American IRA?s, which were first introduced in 1981. After that, the Dow average soared by 25 times. It is amazing to what lengths people will go to avoid the taxman.

Starting October 1, 2013 individuals have been permitted to contribute up to ?1 million a year into Nippon Individual Savings Accounts (NISA) or some $8,000, while married couples can chip in ?2 million.

These funds are exempt from capital gains and dividend taxes for five years. At the same time, capital gains taxes will rise from 10% to 20%.

Thanks to a 22-year long bear market, only 7.9% of personal assets in Japan are currently invested in stocks, compared to 34% in the US. Individuals account for only 28% of the daily trading volume in Tokyo, while foreigners take up 63%. Still, that?s up from only 21% a year earlier.

Over the past 10 years, individuals sold a net $214 billion in equities, keeping their eyes firmly on the rear view mirror. Almost all of the funds were deposited into bank accounts yielding near zero.

Even 10 year Japanese Government Bonds are yielding only 0.41% as of today. That doesn?t buy you much sushi in your retirement.

Over the past three years, Japan has enjoyed having the world?s fastest growing industrialized economy. The latest data show that it is expanding at a white hot 3.5%, versus a far more modest 2% rate in the US, and only 0.5% in Europe.

Early indications are that the NISA?s are hugely popular. Japanese brokers have launched a massive advertising effort to promote the program, which promises to substantially boost their own earnings. Firms have had to lay on extra customer support staff to assist with online applications, where clueless investors have spent two decades in hiding. That certainly makes Japanese brokers, like Nomura (NMR), a buy. Another of my favorites is Sony (SNE).

To get some idea of the potential, take a look at how Merrill Lynch?s stock performed after 1981, which rose by many multiples. The bear market has lasted for so long that many applicants confess to investing in equities for the first time in their lives.

Since Shinzo Abe announced his candidacy for prime minister and his revolutionary economic and monetary program nearly four years ago, the Japanese stock market (DXJ) has soared by an amazing 176% in US dollar terms. The short Japanese yen 2X ETF (YCS) has similarly rocketed by a huge 232%.

Regular readers of the Mad Hedge Fund Trader have been mercilessly pounded to buy Japanese stocks and sell short the Japanese yen for the best of three years. I can almost hear ?Oh no, here comes another yen bashing piece!?

The need to bolster Japan?s retirement finances is overwhelming. It has the world?s oldest population, with some 26% of their 127.6 million over the age of 65.

The average life span in Japan is 82.6 years. That is a lot of people to support for a $6 trillion GDP. Thanks to plummeting fertility rates, the population is expected to decline to 106 million by 2055.

By yanking $690 billion out of the banks and moving out the risk spectrum, Abe?s new IRA?s provide additional means through which the economy can permanently return to health.

Higher stock prices will provide cheap equity financing for public companies, which can then reinvest in the domestic economy and create jobs.

I have written endlessly on the fundamental case for a strong Japanese stock market this year (to read my previous articles on yen, please click the following links: ??Rumblings in Tokyo?, ?New BOJ Governor Craters Yen??and ?New BOJ Governor Crushes the Yen?).

While driving back from Lake Tahoe last weekend, I received a call from a dear friend who was in a very foul mood. He had bailed on all his equity holdings at the end of last year, fully expecting a market crash in the New Year.

Despite market volatility doubling, multinationals getting crushed by the weak euro and the Federal Reserve now signaling its first interest rate rise in a decade, here we are with the major stock indexes sitting at all time highs.

Why the hell are stocks still going up?

I paused for a moment as a kid driving a souped up Honda weaved into my lane of Interstate 80, cutting me off. Then I gave him my response, which I summarize below:

1) There is nothing else to buy. Complain all you want, but US equities are now one of the world?s highest yielding securities, with a lofty 2% dividend. That compares to one third of European debt offering negative rates and US Treasuries at 1.90%.

2) Oil prices have yet to bottom and the windfall cost savings are only just being felt around the world.

3) While the weak euro is definitely eating into large multinational earnings, we are probably approaching the end of the move. The cure for a weak euro is a weak euro. The worst may be behind for US exporters.

4) What follows a collapse in European economic growth? A European recovery, powered by a weak currency. This is why China has been on fire, which exports more to Europe than anywhere else.

5) What follows a Japanese economic collapse? A recovery there too, as hyper accelerating QE feeds into the main economy. Japanese stocks are now among the worlds cheapest. This is why the Nikkei Average hit a new 15-year high over the weekend, giving me yet another winning Trade Alert.

6) While the next move in interest rates will certainly be up, it is not going to move the needle on corporate P&L?s for a long time. We might see a ?% hike and then done, and that probably won?t happen until 2016. In a deflationary world, there is no room for more. At least, that?s what Janet tells me.

This will make absolutely no difference to the large number of corporates, like Apple (AAPL), that don?t borrow at all.

7) Technology everywhere is accelerating at an immeasurable pace, causing profits to do likewise. You see this in biotech, where blockbuster new drugs are being announced almost weekly.

See the new Alzheimer?s cure announced last week? It involves extracting the cells from the brains of alert 95 year olds, cloning them and then injecting them into early stage Alzheimer?s patients. The success rate has been 70%. That one alone could be worth $5 billion.

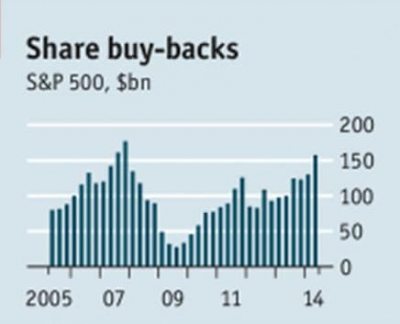

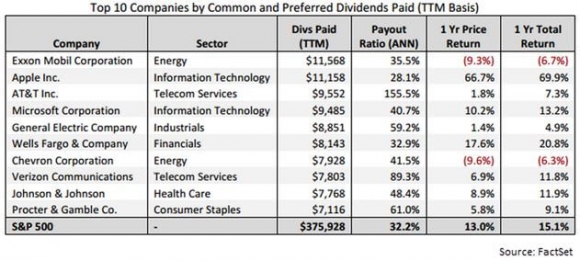

8) US companies are still massive buyers of their own stock, over $170 billion worth in 2014. This has created a free put option for investors for the most aggressive companies, like Apple (AAPL), IBM (IBM), Exxon (XOM), Wells Fargo (WFC), and Intel (INTC), the top five repurchasers. They have nothing else to buy either.

They are jacking up dividend payouts at a frenetic pace as well and are expected to return more than $430 billion in payouts this year (see chart below).

9) Oil will bottom in the coming quarter, if it hasn?t done so already. This will make the entire energy sector the ?BUY? of the century, dragging the indexes up as well. Have you noticed that Conoco Phillips (COP), Warren Buffets favorite oil company, now sports a stunning 4.70% dividend?

10) Ditto for the banks, which were dragged down by falling interest for most of 2015. Reverse that trade this year, and you have another major impetus to drive stock indexes higher.

My friend was somewhat set back, dazzled, and non-plussed by my long-term overt bullishness. He asked me if I could think on anything that might trigger a new bear market, or at least a major correction.

I told him to forget anything international. There is no foreign development that could damage the US economy in any meaningful way. No one cares.

On he other hand, I could think of a lot of possible scenarios that could be hugely beneficial for US stocks, like a peace deal with Iran, which would chop oil prices by another half.

The traditional causes of recessions, oil price and interest rate spikes, are nowhere on the horizon. In fact, the prices for these two commodities, energy and money, are headed lower and not higher, another deflationary symptom.

Then something occurred to me. Share prices have been going up for too long and need some kind of rest, weeks or possibly months. At a 17 multiple American stocks are not the bargain they were 6 years ago when they sold for 10X earnings. Those were the only thing I could think of.

But then those are the arguments for shifting money out of the US and into Europe, Japan, and China, which is what the entire world seems to be doing right now.

I have joined them as well, which is why my Trade Alert followers are long the Wisdom Tree Japan Hedged Equity ETF (DXJ) (click here for ?The Bull Case for Japanese Stocks?).

With that, I told my friend I had to hang up, as another kid driving a souped up Shelby Cobra GT 500, obviously stolen, was weaving back an forth in front of me requiring my attention.

Whatever happened to driver?s ed?

If you live long enough, you see everything.

After a 25-year hiatus, here I am finally back making money in the Japanese stock market once again.

Any sentient being couldn?t help but notice the specular results the Japanese stock market has produced so far in 2015.

The Nikkei Average is up a robust 11.7%, while the Wisdom Tree Japan Hedged Equity Fund (DXJ), which eliminates all of the underlying yen currency risk, has tacked on an impressive 13.2%. This compares to a US Dow average return for the same period of essentially zero.

So, is it too late to get in? Are we joining the tag ends of a party that is winding down? Or is the bull market just getting started?

To answer that question, you have to go to a 30 year chart for the Nikkei average which chronicles all of the violence, heartbreak and drama of the great Japanese stock market crash, and the budding recovery that has since ensued.

The bulls see a crucial triple bottom at ?7,500 that has spread out over ten years, from 2003 to 2013. The initial resistance for the bull market was at ?18,000. That level was decisively broken last week.

And as any long in the tooth technical analyst will tell you, the longer the base building, the longer the recovery.

It is no accident that this sea changing technical action is happening now. Last year rumors abounded that the Japanese government would mandate higher equity weighting by Japanese pension fund managers.

That is exactly what happened at the end of February. The government required pension fund managers to increase equity weightings from 8% to 25%, at the expense of their Japanese government bond holdings. I guess the 0.33% yield on the ten-year wasn?t exactly tickling their fancy.

To meet the new guidelines, managers have to buy $120 billion worth of stocks over the next two years.

That is a lot of stock.

Japanese pension fund managers are the world?s most conservative. Since they can no longer buy all the domestic bonds they want, they are investing in stocks that are essentially bond equivalents.

These include relatively high dividend yielding domestic defensive sectors, like pharmaceuticals, railroads, services, chemicals and foods. With the program only just starting, the Nikkei will be underpinned by local Japanese institutional buying, possibly for years. That eliminates your downside.

Enter the foreign investor. Gaijin mutual fund and hedge fund managers alike were net sellers of Japanese stock for all of 2014. They turned to net buyers only three weeks ago.

Guess what kind of stocks foreigners like to buy? The same kind they buy at home: technology stocks. Take a look at the charts below for Sony (SNE) and Canon (CAJ) and the breakouts there exactly match up with the timeline I described above.

Sony, in particular deserves special mention. Sony was the Apple of Japan during the 1980?s, and should have been the Apple of today. But the company lost its way after 1990, when the founder, my friend Akio Morita, passed away.

Succeeding management was dull, sluggish, and unimaginative. The world quit buying its top of the line stereo systems. As a result, its market capitalization plunged from $150 billion to only $10 billion.

The final indignity came when North Korean hackers almost wiped out the company last year when it released The Interview, a spoof on dictator Kim Jong-un.

These days, Sony is leading the resurgence of the Japanese stock market. Management modernized and westernized. It launched a range of new high tech products. It is selling at a dirt cheap 12X multiple. I also think it is safe to say that their hacking defenses are now state of the art.

It doesn?t hurt that when foreign investors think of buying Japan, picking up Sony is the first thing that comes to mind.

So the technicals and the supply/demand picture lines up, how about the fundamentals?

Go into Japan now, and you are betting that Prime Minister Shinzo Abe (I knew his dad), will succeed in his ?three arrows? plan for economic and financial reform. Insiders believe he can pull this off.

The December election gave him a continued mandate from the Japanese people. The Bank of Japan is also in his corner, implementing a monetary policy that is so aggressive that it was once thought unimaginable. Doubling the money supply in two years?

This is why the Japanese yen will continue to depreciate, which is also highly reflationary for the economy, and is the subject of my Trade Alert below to sell yen.

If all of this lines up, then the next target for the Nikkei is for it to add another ?10,000, up nearly 50% from here. Beyond that, the Japanese stock average is likely to take a run at its old 1989 high of ?39,000.

I remember the day it hit that level all too well.

The rock group Chicago was leading the charts with Look Away. The office at Morgan Stanley was packed with women wearing these big shoulder pads that made them look like football players. Huge sunglasses, neon colors and big hair were everywhere.

Like I said, if you live long enough, you see everything, even another Japanese bull market.

Yes, that is the shocking truth that Fed chairman Janet Yellen told us today with the release of the central bank?s minutes.

Of course, she didn?t exactly say that she would raise interest rates for the first time in a decade in so many words. To discern that, you had to be fluent in Janetspeak.

Very few people have the slightest idea what comprises Janetspeak. It just so happens that I am quite knowledgeable in this arcane argot. In fact I can even negotiate a menu written entirely in Janetspeak and receive a meal reasonably close to what I thought I ordered.

I learned this esoteric language through private tutoring from none other than Janet Yellen herself. These I obtained while having lunch with her at the San Francisco Fed every quarter for five years.

It was a courtesy Janet extended not just to me, but to all San Francisco Bay area financial journalists. But fewer than a half dozen of us ever showed up, as monetary policy is so inherently boring, and government supplied food is never all that great. Ask any Marine.

So let me parse the words for you, the uninitiated. The Fed removed the crucial word ?patient? from its discussion. In the same breath, it says it is unlikely that rates will rise at the April meeting.

She said that any future rate rise would be conditional on continued improvement in the labor market. As the US economy is now approaching full employment, there seems to be little room for improvement there.

Now comes the vital part. Janet also said that an increase in interest rates would also be conditional on inflation returning to the Fed?s 2% inflation target!

Here?s a news flash for sports fans. Inflation is not rising. It is falling. Look no further than the price of oil, which kissed the $42 a barrel handle only this morning.

Inflation is at negative numbers in Europe and in Japan. Even the Fed?s own inflation calculation has price rises limited to 1% in 2015. Their best-case scenario does not have inflation rising to 2% until 2017 at the earliest.

Furthermore, things on the deflation front are going to get worse before they get better. Some one third of all the debt is Europe now carries negative interest rates.

Tell me about inflation when oil hits $20, which it could do in coming months, and will have a massive deflationary impact on the entire US economy, especially in Texas.

That?s the key to understanding Janet. When she says that she won?t raise rates until she sees the whites of inflations eyes, she means it.

I love the way that Janet came to this indirect decision, worthy of King Salomon himself. By taking ?patient? out of the Fed statement, she is throwing a bone to the growing number of hawks among the Fed governors.

At the same time she shatters any impact this action might have. The end result is a monetary policy that is even more dovish than if ?patient? has stayed in.

That is so Janet. No wonder she did so well as a professor at UC Berkeley, the most political institution in the world. I feel like I?m back at college.

You all might think I?m smoking something up here in the High Sierra, or that maybe a rock fell down and hit me on the head. But look at the market action. I?ll go to the video tapes.

Every asset class delivered a kneejerk reaction as if the Fed had just CUT interest rates. Stocks (IWM), bonds (TLT), the euro (FXE), the yen (FXY), OIL (USO), and gold (GLD) all rocketed. The dollar and yields dove.

This is the exact opposite of what every market participant expected, which is why the moves were so big. It is also why I went into this with a 100% cash position in my model trading portfolio.

We lost the word ?patient? we got the ?patient? result.

I had a batch of Trade Alerts cued up and ready to go expecting a dovish outcome. But it was delivered in such a left-handed fashion that I held back on the news flash. It was only when I heard the words from Janet herself that I understood exactly what was happening.

Out went the Trade Alert to buy the Russell 2000 (IWM)! Out went the Trade Alert to pick up some Wisdom Tree Japan Hedged Equity ETF (DXJ)!

Why the (IWM)? Because small caps are the American stocks least affected by a weak Euro.

Why the (DXJ)? Because the Fed action is an overwhelmingly ?RISK ON?, pro stock action. Unlike the rest if the world, the Japanese stock market has to double before it reaches new all time highs. It is just getting started.

Won?t today?s strong yen hurt the (DXJ)? Only momentarily. The Nikkei has yet to discount the breakdown from Y100 to Y120 that has already occurred, let alone the depreciation from Y120 to Y125 that is about to unfold.

Banzai!

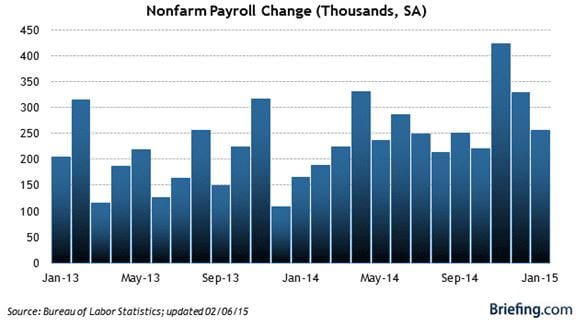

Economists were blown away by the January nonfarm payroll numbers, announced on Friday.

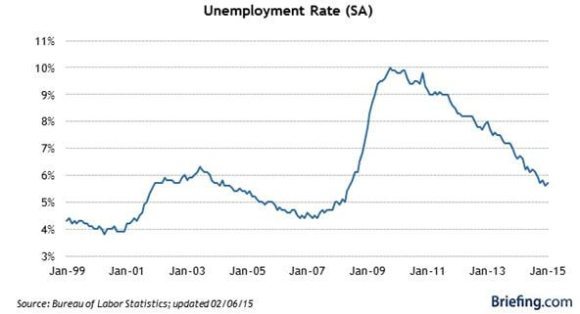

Some 257,000 jobs were added the previous month, holding the headline unemployment figure at 5.7%. Far more important were the revisions for earlier months, which saw December increased to a robust 329,000 and November bumped up to a breathtaking 423,000.

These numbers are almost back to ?normal.? Are ?normal? interest rates to follow?

All told, the January report, the revisions and the additions to the work force means that 703,000 jobs were added to the economy, taking the year on year increase to a positively boom time 3 million. The last quarter has seen the fastest jobs growth rate since 1997. Yikes!

A major part of the new jobs were in retail, proof that our windfall tax cut in the form of falling gasoline prices is finally kicking in.

Needless to say, this is all a bit of a game changer.

It totally vindicates the high-end forecasts for the US economy of 3% plus I made in my New Year forecasts (click here for my ?2015 Annual Asset Class Review?).

The data confirms my thesis that investors are substantially underestimating the strength of the US economy. Furthermore, they have yet to understand the enormously positive impact of cheap energy prices.

It also means that the bull market in stocks is alive and well. It is only resting.

To understand why, let me highlight the major points brought to the fore by the Bureau of Labor Statistics report.

1) The US Economy Has Entered a Self Sustaining Recovery

The trend line for many economic data points are now moving so convincingly upward that they can no longer be treated as statistical anomalies. Nor can they be ascribed to temporary artificial overstimulation by the Federal Reserve in the form of quantitative easing.

Count on Treasury Secretary, Jack Lew, to announce ?mission accomplished? when he address congress later on this week (click here for my one-on-one with Jack, ?Riding With the Treasury Secretary?).

My bet is that this is not our last blockbuster revision. Next to come will be the Q4 GDP, from the just reported flaccid 2.6% annual rate back towards the red hot 5% seen in Q3.

2) The Date for the Next Fed Rate Hike has Been Moved Up

The bond market certainly believed this last week, giving up 9 full points in a couple of days, taking yields from 2.62% to 2.92% in a heartbeat.

I still think this is a 2016 story. The pernicious effects of deflation are still advancing, not retreating, and are not exactly an argument for raising interest rates. But there is no doubt that the desire among the Fed governors to return rates to normal levels is growing, especially if the impact on the economy will be minimal. So call the next rate rise an early, rather than a later, 2016 eventuality.

3) The Strong Dollar is Becoming a Factor With Earnings

The Euro (FXE) has depreciated 31% against the dollar from its 2008 peak, and the yen (FXY) 38% from its 2011 apex. Yet the impact on corporate earnings so far has been marginal at best.

Where will it really start to hurt?

When these currencies approach my final targets of 87 cents and 150, or down another 22% and 18%. It is safe to say that a strong dollar will command an increasing amount of our attention going forward.

This is the argument for investing in small cap US stocks (IWM), where the currency exposure is minimal. Hedge European (HEDJ) and Japanese (DXJ) stocks start to look pretty good too.

4) Wages May Finally Be Rising

The biggest structural impediment facing the US economy has been wage inequality, where virtually all of the benefits of growth accrue to the risk investors of the 1% at the expense of the working class. Hyper accelerating technology and dreadfully imbalanced tax policies are to blame.

January brought us an increase in wages that was miniscule, incremental and modest at best, but it was an increase nonetheless. Average hourly earnings fell by 5 cents in December and then rose by 12 cents the following month.

If this continues, consumer spending will see a big revival, giving us yet another leg to a rising stock market, and creating a win-win situation for all.

One can only hope.

5) More Americans Are Looking for Work

The really amazing thing about the January numbers that they occurred in the face of a large increase in the work force. The participation rate, which has been plummeting for a decade, rose smartly. Long-term U-6 unemployment stayed high, but is down a quarter from peak levels.

To me, this is all a warm up for my ?Golden Age? in the 2020?s. The best is yet to come.