Mad Hedge Technology Letter

February 12, 2020

Fiat Lux

Featured Trade:

(UBER’S DARK FUTURE)

(UBER), (LYFT), (FB), (AMZN), (NFLX), (GOOGL)

Mad Hedge Technology Letter

February 12, 2020

Fiat Lux

Featured Trade:

(UBER’S DARK FUTURE)

(UBER), (LYFT), (FB), (AMZN), (NFLX), (GOOGL)

Autonomous or bankrupt; that is the ultimate fate of Uber (UBER).

In the short-term, Uber is a master at moving the goalposts in order to breathe life in the stock.

CEO of Uber Dara Khosrowshahi can only pray that the Fed will continue to pump cheap money into the market because without artificially low-interest loans, tech firms like Uber would implode.

Is it really time to give Uber the benefit of the doubt?

No more hype, just profits? Is the calculus to profits legitimate?

That's what we call a bubble. Bubbles always burst. Here's the scary part.

Many people are counting on the continued existence of Uber and Lyft to provide "cheap transportation."

Commuters will have to get suddenly unused to it.

There are many companies today that are running the same scheme as Uber in the “gig economy.”

It’s true that management loves to use a lot of flowery language to disguise a lack of profitability.

But as the conditions are ripe for a leg up in tech, the tide rises, and even Uber’s boat rises with it.

I have yet to see even one realistic analysis of how Uber or Lyft is going to become profitable - not even basic math!

I have met a plethora of drivers for both companies, and hope they do well, but there is only so long that one can put lipstick on a pig.

So here we are, Uber in the green everyday because they moved the goalposts yet again and promise us earlier than expected profitability but still losing billions of dollars.

Lyft and Uber have apparently increased revenues somewhat by reducing promotional discounts to riders, but that does not project to even a breakeven point and the unit economics tell me no even if my heart says yes.

The only trick up their sleeve seems to be fare increases, but where is the roadmap detailing this treacherous path?

Once we get to the point in time when Uber is supposed to be profitable, I bet that management will call in another trick play and move the goal posts yet again.

It is quite laughable when so called “tech experts” want Uber to join the ranks of Facebook Inc. (FB), Amazon.com Inc. (AMZN), Netflix Inc. (NFLX), and Alphabet Inc.’s Google (GOOGL) as part of a FANGU acronym.

Reasons for this new bundle is thought to be because of the ability to take advantage of its massive scale while working toward profitability.

Uber is the global ridesharing leader and is becoming the global food delivery leader, but do they really add value?

What if the local government finally got their finger out and built a proper transport system?

They are merely taking advantage of a broken system and passing on the costs of paying drivers to the drivers themselves by designating them as hourly workers.

Are we supposed to celebrate when Uber becomes more “rational?”

Meaning that players have limited their attempts to undercut one another with the sorts of pricing and big discounts that had at one time suggested the business might be a race to the bottom.

Uber projected a lower loss than analysts were expecting for 2020, does less loss mean profits in 2020?

And I do agree that it is encouraging that the company is finally disclosing more data, but shouldn’t they be doing that in the first place?

Love it or hate it, there is a “war” going on between profitability and growth at Uber as the company manages the trade-offs.

Uber had previously talked up that it would become Ebitda profitability by the end of 2021, but Khosrowshahi now forecasts profitability for the fourth quarter of this year.

He says it is possible because Uber initiated a “belt-tightening program” in the last half of 2019, exiting unprofitable ventures and laying off about 1,000 employees.

For instance, Uber sold its food-delivery business in India to a local startup, Zomato, in return for a 9.9% stake in that company.

I do believe that they haven’t done enough to build credibility with investors and the stock’s price action is behaving as we should trust Uber’s management with whatever comes out of their mouths.

The lack of visibility and uncertainty around trends in ridesharing and Eats outside the U.S. continue to be hard to quantify.

So that sounds great! Uber is more serious than ever about becoming profitable and investors have backed them up with the stock flying to the moon.

The trend is your friend and I would suggest readers to get out of the way of this one because you could get trampled on just like the Tesla bears.

And I do support Uber in making steps in the right direction and it also can be said that stocks appreciate the fastest when they transform from a horrible company to a less horrible company.

But there is no way that I am giving Khosrowshahi a pass for Uber’s current situation and no chance I am praising him to the hills.

It is what it is, and Uber is less bad than before, and if they don’t meet their targets, I don’t think investors will believe Khosrowshahi version of a spin doctor forecast anymore.

Uber will rise in the foreseeable future and if they fail to become profitable by 4th quarter, expect a massive drawdown.

If they succeed, expect a vigorous wave of new players to buy into Uber shares.

The stakes have never been higher for Uber and Khosrowshahi.

Mad Hedge Technology Letter

January 15, 2020

Fiat Lux

Featured Trade:

(THE TRADE ALERT DROUGHT EXPLAINED)

(GOOGL), (AMZN), (MSFT), (FB), (JPM)

Why has there been a dearth of Mad Hedge Tech trade alerts to start the year?

Let me explain.

Love it or hate it – earnings' season is about to kick off.

And now, this is the part where it starts to get ugly with consensus of a 2% year-over-year decline in fourth-quarter S&P 500 earnings.

Banks are expected to be a rare bright spot and JPMorgan (JPM) delivered us stable results as one of the first to report.

The unfortunate part of the equation is that a lot has to go right for tech shares to go unimpeded for the rest of the year.

What we have seen in the first 2 weeks of the year is a FOMO (fear-of-missing-out) environment in which valuations have lurched forward to 20 times forward earnings.

Tech is overwhelmingly carrying the load and I have banged on the drums about this thread advising readers to be acutely aware of a heavy positive bias towards the FANGs in 2020.

Well, that is already panning out in the first two weeks.

Examples are widespread with Facebook (FB) up over 8% and Apple (AAPL) already topping 6% to start the year.

It would be farfetched to believe that the tech sector can keep pilfering itself higher in the face of negative earnings growth.

However, behind the scenes, relations between China and America are improving, the threat of war with Iran is subsiding, and the Fed continues strong support tempering down risk to tech shares.

The situation we find ourselves in is that of an expensive tech sector that will again guide down on upcoming earnings’ reports telegraphing softness moving into the middle part of the year.

The ensuing post-earnings sell-off in specific software stocks will offer optimal short-term entry points.

The current risk-reward of chasing FANGs at these levels is unfavorable.

Another glaring example of the FANG outperformance is Alphabet who rose 26% last year.

They are on the brink of joining the $1 trillion club that Apple and Microsoft (MSFT) have joined.

Its market value currently sits idling at $985 billion and its surge towards the vaunted trillion-dollar mark is more of a case of when than if.

Alphabet (GOOGL), more or less, still expands at the same rate of low-20% annually that it did 10 years ago.

Sales have ballooned to $160 billion annually and they sit at the forefront of every cutting-edge sub-sector in technology from artificial intelligence, autonomous driving, and augmented reality.

The engine that drives Google is still its core advertising business and strategic premium acquisitions like YouTube and penetration into other fast-growing areas such as cloud computing.

It has rounded out into a broad-based revenue accumulator.

Apple was the first public company to surpass a $1 trillion market cap and ended the year up 86% in 2019, and it has only gone up since then currently checking in at a $1.36 trillion market cap.

Microsoft followed Apple, hitting the $1 trillion mark during the first half of 2019, and it is now worth $1.23 trillion.

Amazon fell back after surging past the $1 trillion mark but inevitably will achieve it on the next heave up.

Amazon shares have been quickly heating up since its capitulation from $2,000 in July 2019 and round out the group of overperforming tech behemoths.

Although the rush into big-cap tech stocks in the first two weeks has been a bullish signal, it still doesn’t marry up with the lack of earnings growth in the overall tech sector.

Companies beating meager expectations will experience strong share appreciation although not at the pace of last year and will still serve investors pockets of overperformance.

We will find our spots to trade shortly, but better to keep our gunpowder dry at the moment.

Mad Hedge Technology Letter

January 8, 2020

Fiat Lux

Featured Trade:

(THE TOP IS NOT IN FOR TECH STOCKS))

(AAPL), (FB), (GOOGL)

Tech shares are pricey, but that doesn’t mean they can’t get more expensive.

Strength often begets strength.

Let’s take for instance Apple (AAPL) – it delivered investors 86% in 2019 and that was their best performance in the past 10 years.

This was on the heels of a tumultuous 2018 where Apple sank 6%.

Many of the best of brightest of the tech industry beat the S&P last year, which itself gained 29%.

And as Apple leapfrogged into the software as a service business, they find themselves shunning China hardware revenue that got themselves into the 2018 mess.

Apple is betting that the confines of stateside consumer culture will offer greener pastures.

Overall, the market is pricing in a lukewarm 2020 for tech earnings boding well for the elite tech stocks that celebrated touchdown after touchdown in 2019.

Surpassing low expectations could be another rewind back to Q4 2019 which was a time that offered tech shares a platform to surge to all-time highs.

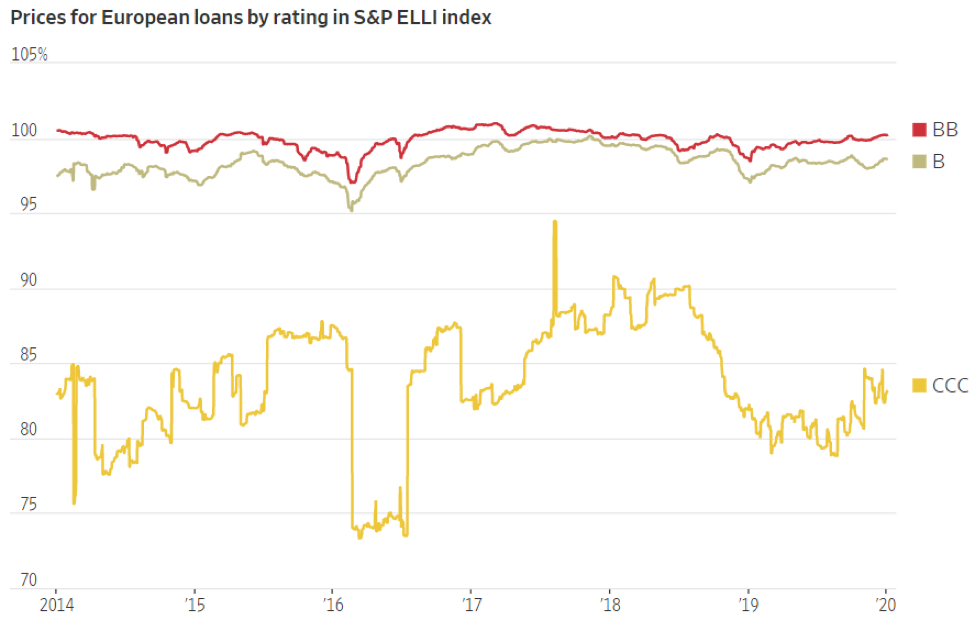

The worrying development for 2020 is that poorer-rated tech corporations won’t have the same access to cheap debt as they did in 2018 or even 2019.

The chapter of loose credit is about to close stymying loss-making tech companies who thought they could use subsidies to achieve success.

The prices of CCC-rated European bonds have declined immensely in the past year showing investors' lack of appetite for the riskier part of the corporate debt market.

Venture capitalists aren’t going to foot the bill for the next big thing in Silicon Valley at this point in the economic cycle unless the unit economics are too good to be true.

The story of 2020 will be the intensification between the haves and have nots in tech.

This is the case of the market putting a premium on time-honored tech brands and bulletproof balance sheets that they have cultivated.

On a broader level, the Fed who has presided over a $600 billion expansion in their balance sheet in the last four months offers yet another tailwind to tech shares in the short-term.

The Fed’s decision in the last few months to re-start large-scale asset purchases will help keep a foot under tech shares in early 2020 and responds like a de facto QE.

If you thought 2019 was a bad year for Uber and Lyft, then wait until this year plays itself out.

The gig economy stocks are in the direct firing line with nowhere to run and other non-sensical profit models will find it costly to search for debt alternatives in which to service their visions.

If the tech sector does become a war of attrition between the FANGs staving off one another by acquiring inorganic growth, then marginal tech players will get squeezed because they don’t have the capital bazookas to compete with the likes of Facebook (FB) and Google (GOOGL).

This is the year that we could see a slew of fringe tech companies go bust as debt markets sour on false narratives of future profits and equity markets turn against them.

The feast versus famine theme is also aligned with 5G, with many of the same cast of characters such as Apple, Alphabet posed to usurp revenue when this new technology finally becomes pervasive in consumer culture.

The Apple refresh cycle will dust off its playbook for another blockbuster rollout later this year when Apple debuts its much-awaited 5G phone.

Much of the share appreciate in Apple of late can be attributed to the anticipation of the new iPhone and the fresh infusion of revenue that branches off from it.

The applications that result from the new 5G Apple phone is seen as a luscious force multiplier to many 3rd party companies as well.

Chip stocks will be counted on as the ones lifting the tech foundations and just looking at shares in China, demonstrations of frothiness are running wild throughout their markets.

The Chinese government, to counteract the trade war, has been on a mission to flood its tech sector with unlimited capital as a catchup mechanism to overcome its inferior domestic chip industry.

Will Semiconductor, a supplier of integrated circuit products for telecommunications and electronics for cars, delivered a 390% performance in 2019 ranking it as the best performer in the Chinese stock market.

Luxshare Precision Industry and GoerTek, suppliers of consumer electronics products supplying Apple, and GigaDevice Semiconductor, producing flash chips, weren’t too shabby either each eclipsing at least 193% last year.

Even though 5G construction isn’t fully operational, I can attest that revenue creation for the companies involved are in full swing.

Investors must narrow their pickings to the biggest and financially resilient; this is not the time to expose oneself to the ugly trepidations of the mood-sensitive tech market.

For investors who can balance the delicate relationship of risk and surgical maneuvering, this year will end positive.

Mad Hedge Technology Letter

December 20, 2019

Fiat Lux

Featured Trade:

(THE BIG TECH TRENDS OF 2020)

(AAPL), (GOOGL), (FB), (AMZN), (NFLX)

The year is almost in the rear-view mirror – I’ll make a few meaningful predictions for technology in 2020.

Although iPhones won’t go obsolete in 2020, next year is shaping up as another force multiplier in the world of technology.

Or is it?

A trope that I would like to tap on is the severe shortage of innovation going on in most corners of Silicon Valley.

Many of the incumbents are busy milking the current status quo for what it’s worth instead of targeting the next big development.

Your home screen will still look the same and you will still use the 25 most popular apps

This almost definitely means the interface that we access as a point of contact will most likely be unchanged from 2019.

It will be almost impossible for outside apps to break into the top 25 app rankings and this is why the notorious “first-mover advantage” has legs.

The likes of Google search, Gmail, Instagram, Uber, Amazon, Netflix and the original list of tech disruptors will become even more entrenched, barring the single inclusion of Chinese short-form video app TikTok.

The FANGs are just too good at acquiring, cloning or bludgeoning upstart competitors.

It’s the worst time to be a consumer software company that hasn’t made it yet.

Advertising will find itself migrating to smart speakers

Amazon and Google have blazed a trail in the smart speaker market but ultimately, what’s the point of these devices in homes?

Exaggerated discounting means hardware profits have been sacrificed, and the lack of paid services means that they aren’t pocketing a juicy 30% cut of revenue either.

These companies might come to the conclusion that the only way to move the needle on smart speaker revenue is to infuse a major dose of audio ads to the user.

So if you are sick to your stomach of digital ads like I am, you might consider dumping your smart speaker before you are forced to sit through boring ads.

Amazon’s Alexa will lose momentum

In a way to triple down on Alexa, Amazon has installed it into everything, and this is alienating a broad swath of customers.

Not everyone is on the Amazon Alexa bandwagon, and some would like Amazon’s best in class products and services without involving a voice assistant.

Privacy suspicion has gone through the roof and smart speakers like Alexa could get caught up in the personal data malaise dampening demand to buy one.

Your voice is yours and 2020 could be the first stage of a full onslaught of cyber-attacks on audio data.

Don’t let hackers steal your oral secrets!

Cyber Warfare and AI

Hackers have long been experimenting with automatic tools for breaking into and exploiting corporate and government networks, and AI is about to supercharge this trend.

If you don’t know about deep fakes, then that is another thorny issue that could turn into an existential threat to the internet.

Not only could 2020 be the year of the cloud, but it could turn into the year of cloud security.

That is how bad things could get.

A survey conducted by Cyber Security Hub showed 85% of executives view the weaponization of AI as the largest cybersecurity threat.

On the other side of the coin, these same companies will need to use AI to defend themselves as fears of data breaches grow.

AI tools can be used to detect fraud such as business email compromise, in which companies are sent multiple invoices for the same work or workers duped into releasing financial information.

As AI defenses protect themselves, the sophistication of AI attacks grows.

It really is an arms race at this point with governments and private business having skin in the game.

Facebook gets out of the hardware game because consumers don’t trust them

Remember Facebook Portal – it’s a copy of the Amazon Echo Show.

The only motive to build this was to bring it to market and expect Facebook users to adopt it which backfired.

Facebook will find it difficult convincing users to use more than Facebook and Instagram software apps.

Don’t wait on Facebook to roll out some other ridiculous contraption aimed at stealing more of your data because there probably won’t be another one.

This again goes back to the lack of innovation permeating around Silicon Valley, Facebook’s only new ideas is to copy other products or try to financially destroy them.

China continues to out-innovate Silicon Valley.

The rise of short-form video app TikTok is cementing a perception of China as the home of modern tech innovation, partly because Silicon Valley has become stale and stagnated.

China has also bolted ahead in 5G technology, fintech payment technology, unmanned aerial vehicle (UAV) and is giving America a run for their money in AI.

China’s semiconductor industry is rapidly catching up to the US after billions of government subsidies pouring into the sector.

Silicon Valley needs to decide whether they want to live in a tech world dominated by Chinese rules or not.

Augmented Reality: Is this finally the real deal?

Augmented reality (AR) is still mainly used for games but could develop some meaningful applications in 2020.

Virtual Reality (VR) and AR will play a big role in sectors such as education, navigation systems, advertising and communication, but the hype hasn’t caught up with reality.

One use case is training programs that companies use to prepare new workers.

However, AR applications aren't universally easy or cheap to deploy and lack sophistication.

AR adoption will see a slight uptick, but I doubt it will captivate the public in 2020 and it will most likely be another year on the backburner.

Apple’s New Projects

Apple has two audacious experimental projects: a pair of augmented-reality glasses and a self-driving car.

The car, for now, has no existence outside of a few offices in California and some hires from companies like Tesla.

And, at the earliest, the glasses won’t hit shelves until 2021,

The car is likely to fizzle out and Apple will be forced to double down on digital content and services to keep shareholders happy which is typical Tim Cook.

The 5G Puzzle

Semiconductor stocks have been on fire as investors front-run the revenue windfall of 5G and the applications that will result in profits.

Select American cities will onboard 5G throughout 2020, but we won’t see widespread adoption until later in the year.

5G promises speeds that are five times faster than peak-performance 4G capabilities, allowing users to download movies in five seconds.

With pitiful penetration rates at the start, the technology will need to grow into what it could become.

The force multiplier that is 5G and the high speeds it will grace us with probably won’t materialize in full effect until 2021.

Each of the nine tech developments in 2020 I listed above negatively affects US tech margins and that will follow through to management’s commentary in next year’s earnings and guidance.

Tech shares are closer to the peak and the bull market in tech is closer to the end.

Innovation has ground to a halt or is at best incremental; companies need to stop cloning each other to death to grab the extra penny in front of the steamroller.

Profit margins will be crushed because of heightened regulation, transparency issues, monitoring costs, and the unfortunate weaponizing of tech has been a brutal social cost to society.

Tech is saturated and waiting for a fresh catalyst to take it to the next level, but that being said, tech earnings will still be in better shape than most other industries and have revenue growth that many companies would cherish.

Mad Hedge Technology Letter

December 6, 2019

Fiat Lux

Featured Trade:

(AUGMENTED REALITY IS HEATING UP),

(AAPL), (LITE), (QCOM), (NVDA), (ADSK), (FB), (MSFT), (SNAP)

First, what is augmented reality for all the newbies?

Augmented reality is an interactive experience of a real-world environment where the objects that reside in the real world are enhanced by computer-generated perceptual information, sometimes across multiple sensory modalities.

Augmented reality (AR) went rival in 2016 when the Pokemon Go mania captivated everyone from children to adults.

No sooner than 2021, the AR addressable market is poised to mushroom to $83 billion - a sizeable increase from the $350 million in 2018.

Much like machine learning, corporations are learning to marry up this technology with their existing products supercharging the performance.

Ulta Beauty, for example, has acquired AR and artificial intelligence start-ups to help customers digitally test the final appearance of makeup before users purchase the product.

That is just one micro example of what can and will be achieved.

Looking deeper into the guts, Qualcomm (QCOM) is hellbent on making their chips a critical part of the puzzle.

The company is better known for a telecom and a semiconductor play, not often lumped in with a list of AR stocks.

Qualcomm is strategically positioned to capitalize on the integration of augmented reality in mainstream corporate business embedding their chips into the devices.

Maximizing Qualcomm’s future role in the industry, the company announced in 2018 that it would be developing a chipset specifically for AR and VR applications.

This broad-based solution will make it easier for other developers to bring new glasses to the marketplace.

Autodesk (ADSK) is one of my favorite software stocks and a best of breed of industry design.

They sell 3D rendering software to designers and creators by offering a platform in which they can transform 2D designs into digital models that are both interactive and immersive, creating compelling experiences for end-users.

Autodesk has an array of powerful software suites to augment virtually any application, such as 3ds Max, a 3D modeling program; Maya LT game development software; its automotive modeling program VRED; and Forge, a development platform for cloud-based design.

Facebook (FB) has been piling capital into AR for years.

CEO Mark Zuckerberg wants to create an alternative profit-driver and is desperate to wean his brainchild from the digital ad circus.

One example is Facebook’s Portal TV and its Spark AR which is the platform responsible for mobile augmented reality experiences on Facebook, Messenger, and Instagram.

It supplies the virtual effects for consumers to play around with, but it is yet to be seen if consumers gravitate towards this product.

Lumentum (LITE) is the leader in 3D-sensing markets developing cloud and 5G wireless network deployments.

They manufacture 3D sensor lasers that can be used with smartphones to turn handsets into a sort of radar. Sensors are clearly a huge input in how AR functions along with the chips.

CEO of Apple (AAPL) Tim Cook put it best when he earlier said, “I do think that a significant portion of the population of developed countries, and eventually all countries, will have AR experiences every day, almost like eating three meals a day, it will become that much a part of you.”

He said that in 2016 and AR has yet to mushroom into the game-changing sector initially thought partly because the roll-out of 5G is taking longer than first expected.

Apple consumers will need to then adopt a 5G device or phone to really get the AR party started and that won’t happen until the backend of next year.

My initial channel checks hint that the Cupertino firm is planning a 5.4-inch model, two 6.1-inch devices, and one 6.7-inch phone, all of which will support 5G connectivity.

I surmise that Apple’s two premium devices will feature “world-facing” 3D sensing, a technology that could help Apple boost its augmented-reality capabilities and support other feature improvements on its priciest devices.

Apple has had a big hand in Lumentum's growth and will continue to buy their sensors, but other key component suppliers will get contracts such as Finisar, a manufacturer of optical communication components and subsystems.

Apple planned to debut AR glasses by 2020, but the rollout is now delayed until 2022.

They are clearly on the back foot with Microsoft (MSFT) further along in the process.

Microsoft already has a second iteration of its AR headset, HoloLens, and is compatible with several apps and has integration with Azure as well.

The head start of 2 years could really make a meaningful impact and might be hard for Apple to recover.

Facebook isn’t the only social media company going full steam into AR, Snap (SNAP) recently unveiled its newest spectacles, which feature AR elements.

Another application of AR is autonomous driving with Nvidia working on improving the driving experience by fusing AR with artificial intelligence.

Nvidia (NVDA) is already thinking about the next generation of AR technologies with varifocal displays, which improve the clarity of an object for a user.

It will take time to transform our relationship with AR, the infrastructure is still getting built out and many people just don’t have a device that will allow us to tap into the technology.

Investors must know that AR-related stocks will start to appreciate from the anticipation of full sale adoption and there could be a killer app that forces the mainstream user to take notice.

Until then, companies jockey for position and hope to be the ones that take the lion’s share of the revenue once the technology goes into overdrive.