Global Market Comments

May 20, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DOW 40,000 AND HANGING WITH THE AMAZON HEADHUNTERS)

(TLT), (JNK), (WES), (ET), (GLD), (SLV), (MSFT),

(NVDA), (AAPL), (SPY), (FXI), (COPX), (FCX)

Global Market Comments

May 20, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DOW 40,000 AND HANGING WITH THE AMAZON HEADHUNTERS)

(TLT), (JNK), (WES), (ET), (GLD), (SLV), (MSFT),

(NVDA), (AAPL), (SPY), (FXI), (COPX), (FCX)

Global Market Comments

May 16, 2024

Fiat Lux

Featured Trade:

(THE COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

May 13, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT AMERICAN GOLDEN AGE HAS ONLY JUST BEGUN and SWIMMING WITH THE SHARKS)

(AAPL), (NVDA), (META), (GLD), (GOLD), (SLV), (WPM), (MSFT), (NVDA), (TLT), (FCX), (FXI), (BRK/B)

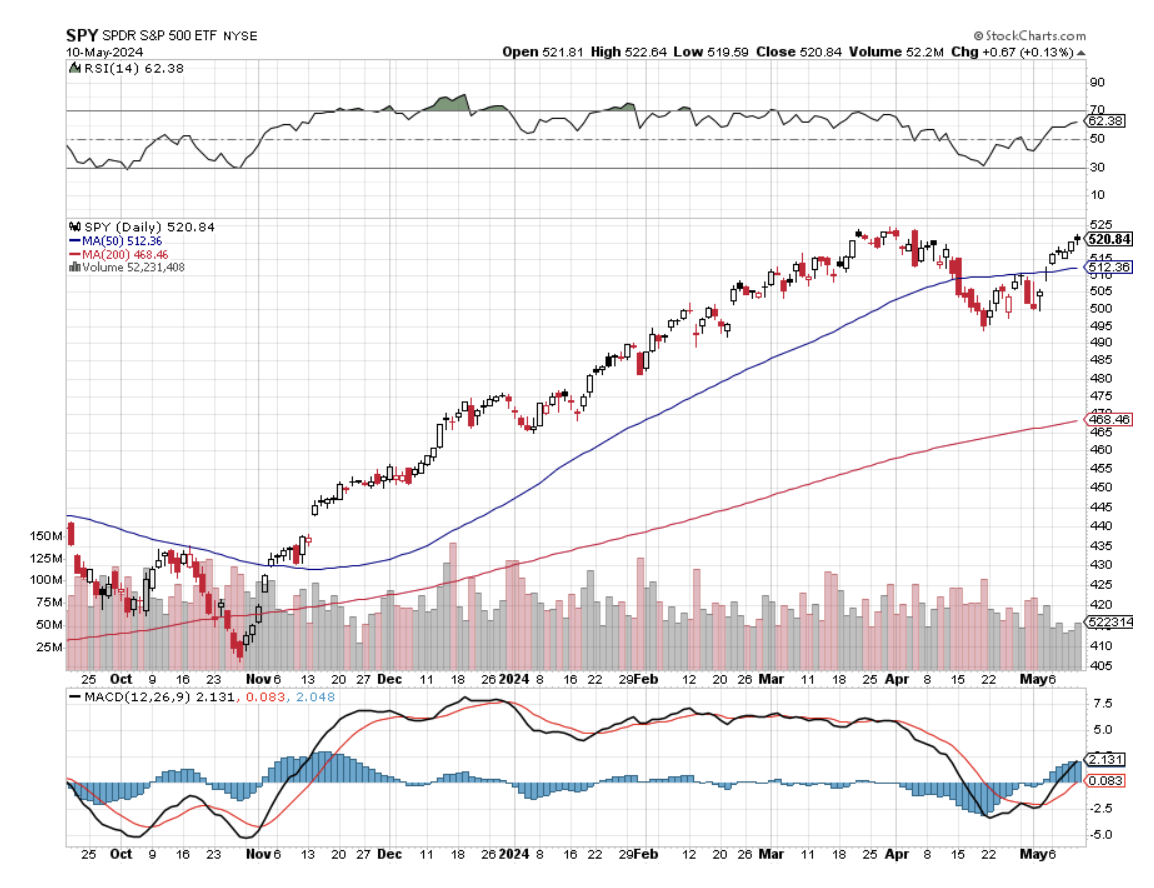

The Bull Market has Five More Years to Run, with S&P 500 growing earnings at 10% a year for the foreseeable future. Last year brought in $222 per share, 2024 will see $250, 2025 $270, and $300 for 2026. The Great American Golden Age has only just begun.

Profit margins will expand to all-time record highs. Falling interest rates and a weak dollar will boost exports to a recovering Europe and Japan. Inflation should hit the Fed’s 2% in 2025 as AI chatbots replace workers at a breakneck rate, cutting costs dramatically as they already have at some firms. The future is happening fast. Buy everything on dips, even bonds.

The stock market couldn’t even manage a 10% correction in April. We got a measly 6.10% instead. It’s all about the economy, stupid. Leftover massive Covid spending and the $280 billion CHIPS Act have created a tidal wave of cash surging through the system with much of it ending up in stocks.

The top eight tech companies (the Magnificent Seven plus Netflix (NFLX)) accounting for 30% of the entire market cap are only getting stronger. The (SPY) has a current price-earnings multiple of 20X with the Big 8 and 17X without them going forward. It’s not cheap but better than a poke in the eye with a sharp stick.

Boring old high-yielding utilities will become a big play as the electric power grid has to triple in size to accommodate the voracious appetites of EV’s and AI. And as we have already seen in California and much of the country, utilities have no reservations about raising prices.

We are back to normal with interest rates, returning to pre-financial crisis levels. Certainly, a stock market at all-time highs is happy with rates. The real concern here is that the Fed DOES cut rates too fast to bail out the loan-dependent half of the economy and the US Treasury as well. That could trigger a melt-up in stocks that would make the last six months pale in comparison and make my own $6,000 target for the (SPX) look ridiculously conservative.

There is also a major generational change in demographics underway. Previous retiring generations, having experienced the Great Depression, hoarded savings and were a drag on the economy. The Baby Boomers are spending like there is no tomorrow because after going through COVID-19, there might not BE a tomorrow. The Boomers have thus turned into the greatest job creators of all time through their spending.

I’ve seen them everywhere in recent weeks in Florida, Cuba, Ecuador, the Galapagos Islands, Panama, and of course, San Francisco where a Big Mac Happy Meal costs $11. What they don’t spend is being passed on to Gen Xers and Millennials, creating a $75 trillion wealth transfer, the largest in history. A lot of this is going into stocks as well. Wonder where all that “meme stock” money is coming from?

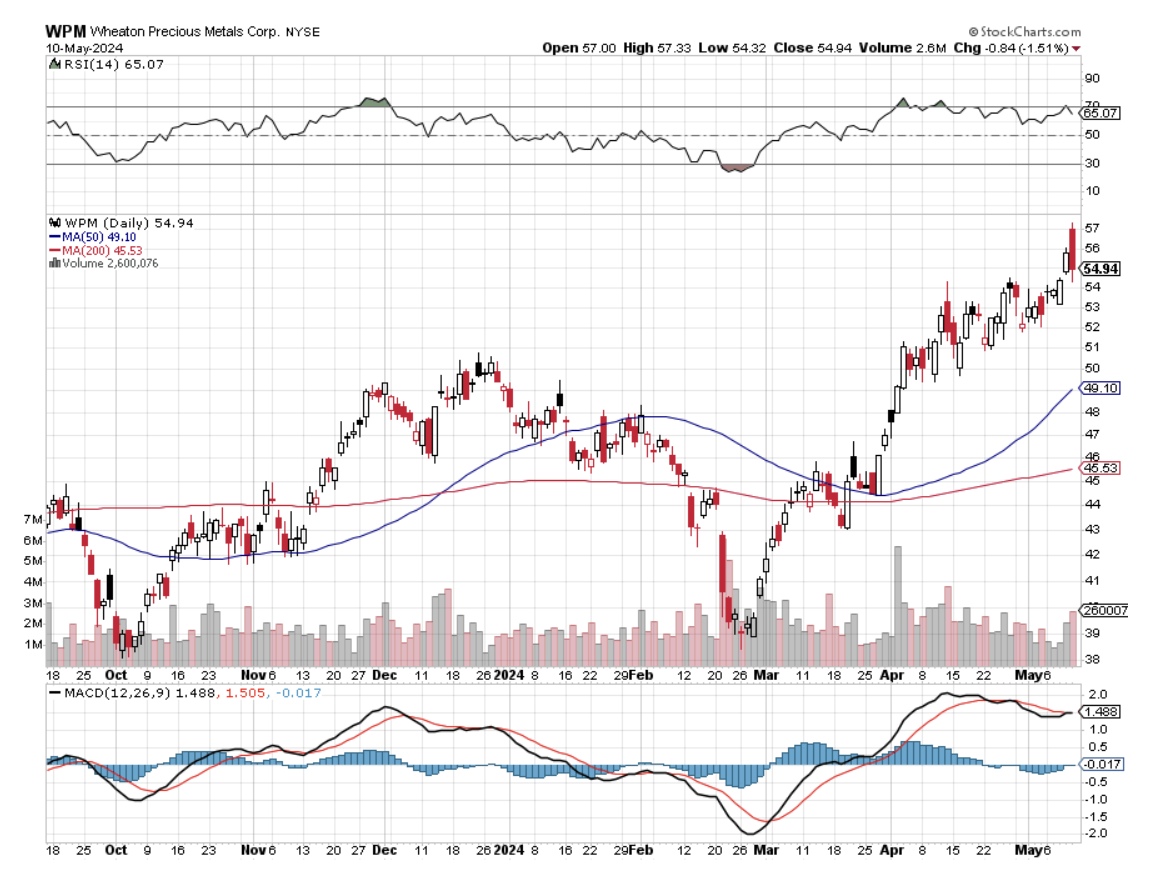

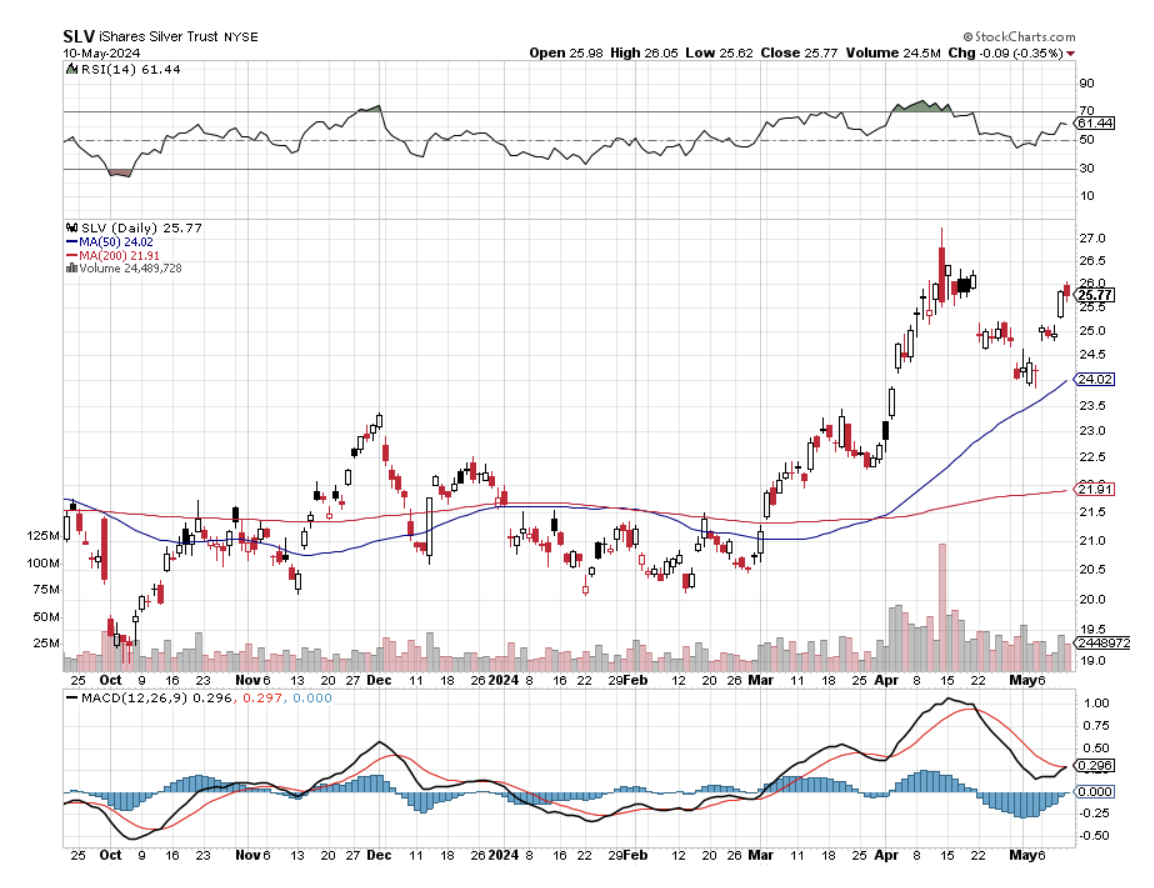

And from the “Department of I Told You So”, notice that precious metals were on an absolute tear last week, with gold (GLD) up 4.78% and silver posting a gob-smacking 7.40%. The new demand that I was aware of but had no hard data on finally became public. Solar Panels are Driving Global Silver Demand in an unprecedented fashion. Global investment in solar PV manufacturing more than doubled last year to around $80 billion.

Miners are expanding their operations and ramping up production as prices for the precious metal climb to decade highs, sending gross revenues to the moon. Demand for silver from the makers of solar PV panels, particularly those in China, is forecast to increase by almost 170% by 2030, to roughly 273 million ounces—or about one-fifth of total silver demand.

That’s a lot of silver. Buy (SLV) and (WPM) on dips.

So far in May, we are up +4.14%. My 2024 year-to-date performance is at +18.75%, a new all-time high. The S&P 500 (SPY) is up +10.48% so far in 2024. My trailing one-year return reached +35.79% versus +30.58% for the S&P 500.

That brings my 16-year total return to +695.38%. My average annualized return has recovered to +51.83%.

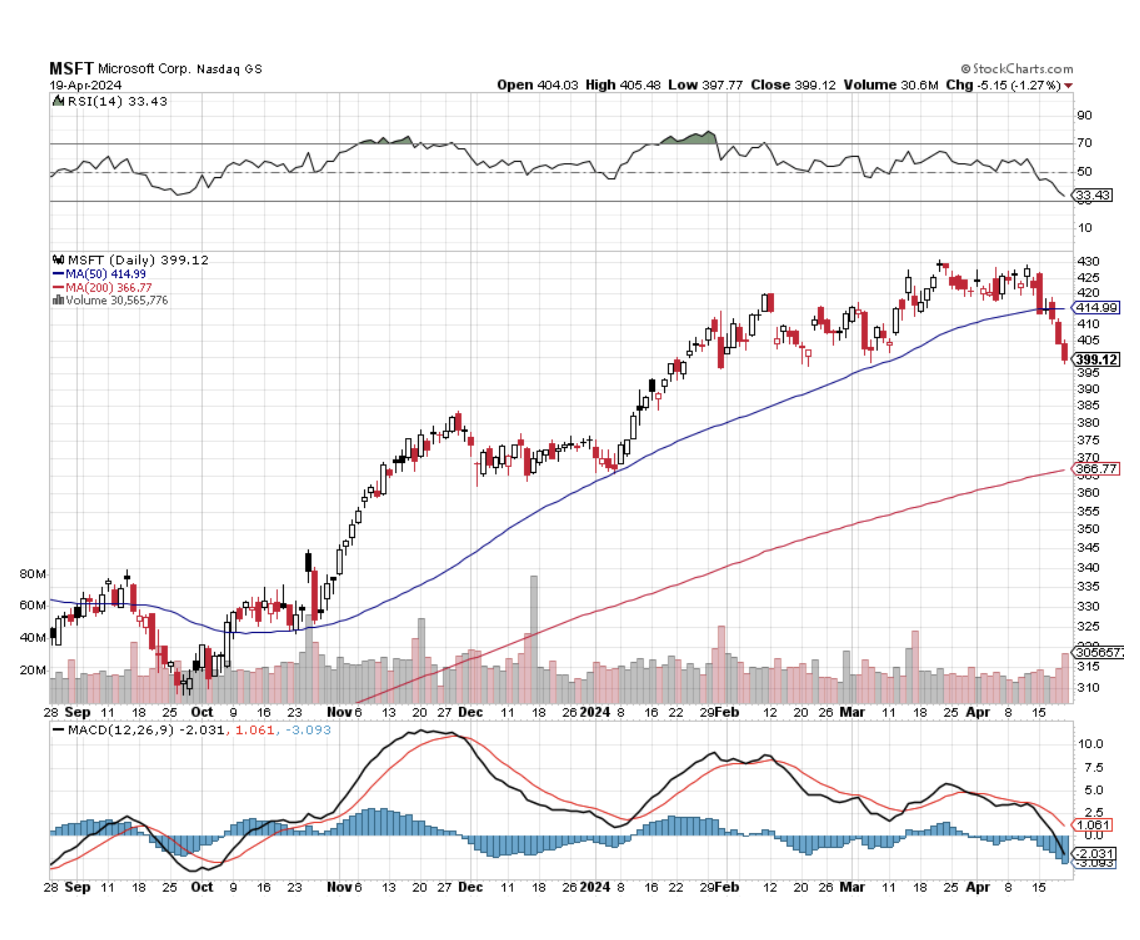

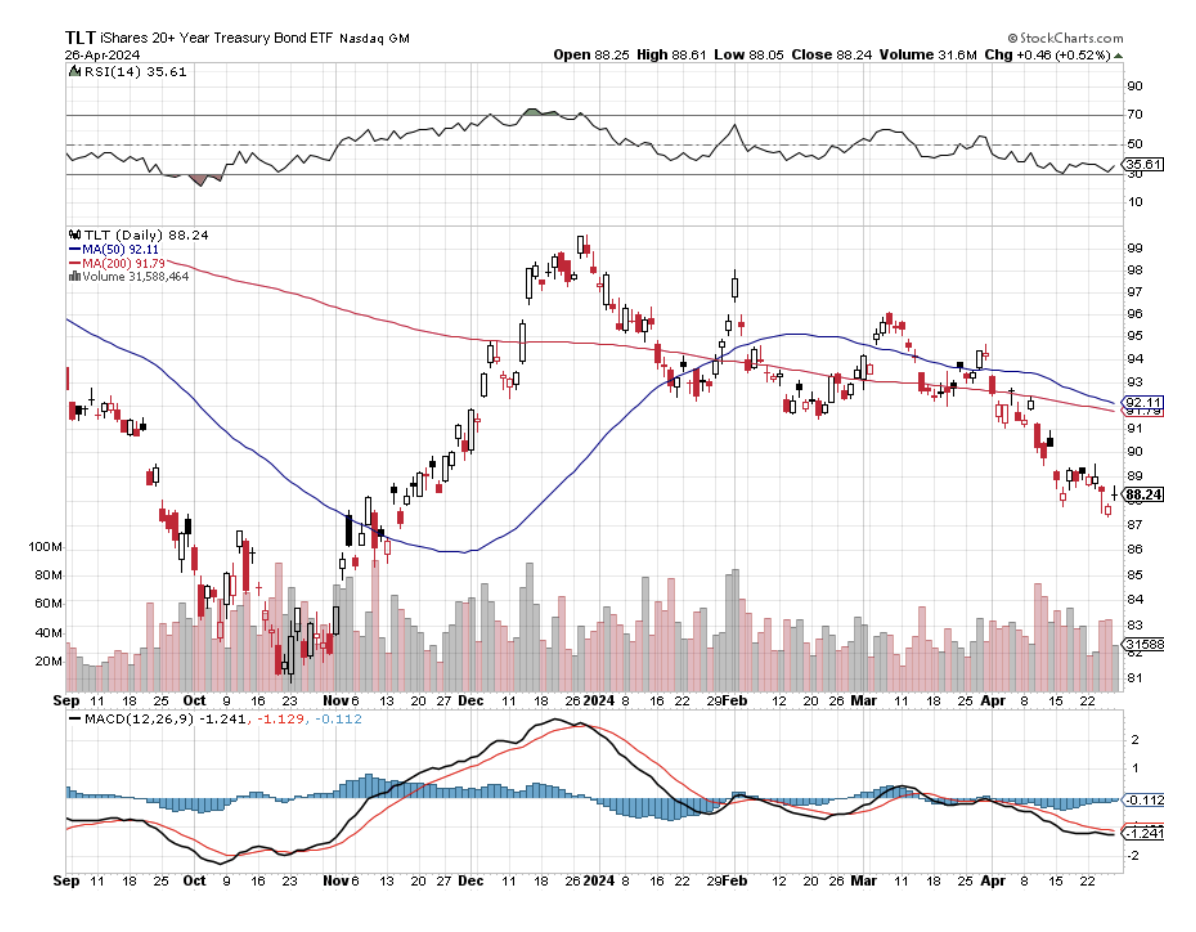

I stopped out of short positions for small losses in (AAPL) and (NVDA) last week. I took profits on my long in (META). I am running my longs in (GLD) and (SLV) and my shorts in (MSFT) and (NVDA) into the Friday, May 17 options expiration. The only new position I added last week was a short in the (TLT).

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

Weekly Jobless Claims Hit a Nine Month High at 233,000, the bitter fruit of persistently high interest rates. New York City public school workers such as bus drivers are allowed to apply for benefits during winter and spring breaks, which tend to boost weekly claims numbers. Claims also picked up in California, Indiana, and Illinois.

Underwater Home Mortgages are Soaring, with the South taking the biggest hit. Roughly one in 37 homes are now considered seriously underwater in the US and that share is much higher across a swath of southern states. Nationally, 2.7% of homes carried loan balances at least 25% more than their market value in the first few months of the year. That’s up from 2.6% in the previous quarter. It’s another cost of high rates.

Online Retail Spending Up 7%, during the January-April period YOY. Cheaper items are seeing the fastest growth. Consumer discretionary spending has been in focus over the past several months, as sticky inflation has forced shoppers in various categories to trade down to more affordable products. It’s another sign of a modest slow, 1.6% growing economy.

Morgan Stanley (MS) Pushes Back Rate Cut Expectations to September. I couldn’t agree more. You see this in the $4 rally in bonds since last week. Sell short (TLT) for the very short term.

TikTok Sues the US Government, claiming its first amendment rights have been violated in a ban imposed on Congress. They will probably win. The national security threat posed by millions of dancing teenagers has never been showed. It’s just another talking point for technology-ignorant politicians egged on by Facebook (META) and other competitors. No one ever said the people in Silicon Valley were nice.

Social Security Trust Fund to Go Broke by 2035, according to US Treasury estimates. I knew they wouldn’t pay me after 55 years of contributions. Medicare is in less bad shape, not running out until 2036, a five-year extension. Retirees, the baby boomers, and exceeding new contributors, the Gen Xers. Expect your taxes to go up to fill the gap.

Berkshire Hathaway Delivers Blockbuster Earnings in Q1, thanks to a $9 billion pop in (AAPL) stock last year. Buffet just cut his massive position by 13% and will cut more. Total 2023 profits came in at a mind-numbing $93 billion. The company — whose divisions include insurance, the BNSF railroad, an expansive power utility, Brooks running shoes, Dairy Queen and See’s delivered a sharp swing from its $22 billion loss in 2022 because of the bear market. Its vast insurance operations that include Geico car insurance and reinsurance reported $5.3 billion in after-tax earnings for 2023, thanks to steep premium increases which we have all felt. Sell (AAPL), buy (BRK/B).

Bond Investors are Making a Killing, with the US Treasury paying out $900 billion in interest in 2023. That’s double the annual cost of the past decade. Remember those coupons? That’s another reason for the Fed to cut rates soon, to lessen this backbreaking burden on the government. After being held hostage by zero-rate policies for almost two decades, US Treasuries are finally reverting to their traditional role in the economy. Bonds are becoming respectable again after a long winter. Buy (TLT) on dips.

China Home Sales Plunge by 47%, as the real estate crisis deepened, indicating that a recovery may be far off. But when it does bounce back, expect all commodities to hit record highs. Buy (FCX) on dips.

Biden Piles on the Foreign Tariffs, announcing new China tariffs aimed at the EV Industry that is currently decimating Europe. Europe is in danger of giving away its edge in cars to the Chinese and a proactive response would ensure American car manufacturers can stand up to the low-priced onslaught.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 13, at 10:30 AM EST, the Consumer Inflation Expectations are announced.

On Tuesday, May 14 at 8:30 AM EST, Producer Price Index for April is released.

On Wednesday, May 15 at 8:30 AM EST, the Consumer Price Index is published

On Thursday, May 16 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, May 17 at 8:30 AM the Monthly Options Expiration takes place at the close.

At 2:00 PM the Baker Hughes Rig Count is printed.

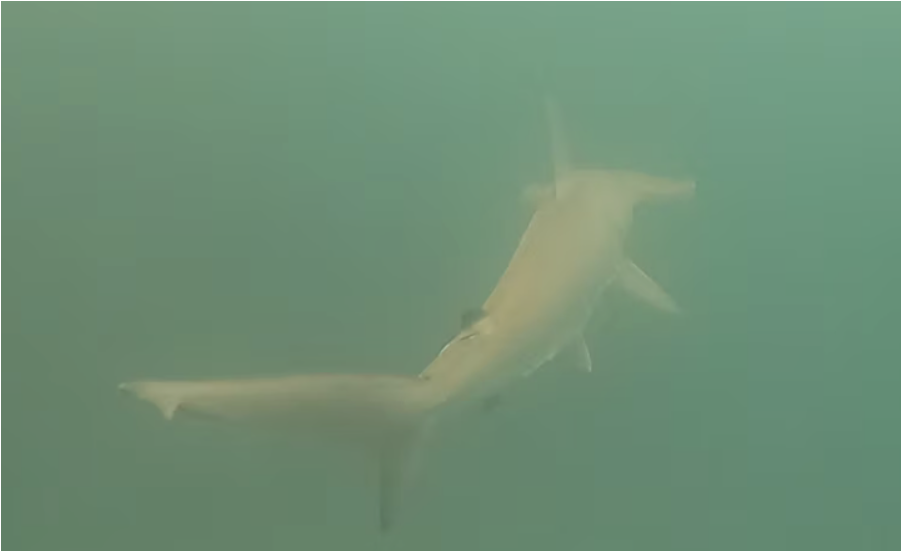

As for me, I will never forget the words from my underwater guide: “Stay where you are and the current will bring the sharks to you.”

Is that something we want, I queried in my fractured Spanish. “Don’t worry”, he answered, “The sharks are vegetarians.” Yes, but did anyone tell the sharks that they were vegetarians?

Sure enough, two six-foot-long hammerhead sharks hungrily swam by me within feet in the green murk, not even pausing to give me the time of day. They swam so close that one almost slapped me in the Face with his tailfin. I guess I wasn’t on the menu that day, not even as a special.

Fortunately, I brought a GoPro underwater video with me and filmed the whole thing. Otherwise, you wouldn’t believe me for a second (click here for the link.)

Such was the high point of my week in the Galapagos Islands last week, a remote archipelago of 13 volcanic islands some 600 miles west of Ecuador, 2 degrees South Latitude in the Pacific Ocean. Sitting in my beachfront house in San Cristobal, I worked all morning, knocking out some eight trade alerts on the week, and explored every afternoon.

It was bliss.

You scientists out there will already know the Galapagos Islands as the place where Charles Darwin landed in 1835 on the HMS Beagle and collected the data that led to the Theory of Evolution and the concept of the Survival of the Fittest. (It was all about black Finches, now known as Darwin’s finches, of which I saw hundreds).

Darwin was at first widely ridiculed, as are the creators of all new revolutionary advances. Critics highlighted his close relationship with monkeys. Now it’s required reading for all high school students. While I was there a reproduction of the Beagle sailed in from Holland to celebrate the 200th anniversary of Darwin’s discoveries….11 years early.

The Galapagos Islands are not an easy place to get to. It was a four-hour flight from Miami to Quito in Ecuador, the worlds third highest airport at 9,500 feet. A lot of transients get altitude sickness. Then an hour's flight to Guayaquil on the coast where the Ecuadorian drug trade is run and another hour to San Cristobal. When I tried to visit here in the 1970’s there was only one ship a week and no planes.

Galapagos connected to the outside world just last year when Space X’s Starlink service initiated a 200mb/sec service. With that, I can trade stocks as if I were in downtown Manhattan. This is true for virtually every remote location in the world now, the consequences of which we have yet to imagine. I set up a Starlink in Ukraine last October while under fire and the Russians never were able to jam it.

The Ecuadorian government has gone through great lengths to keep the Galapagos Islands a pristine eco-tourism destination and they have largely succeeded. I counted only one Cessna G5 jet at the airport. Incoming luggage is X-Rayed for foreign fruit and sniffed for drugs by German Shepherds. Residents are limited to a tiny southwestern sliver of San Cristobal island and the rest is a national park.

A friend charitably turned down a $20 million offer from the Four Seasons international hotel chain for his 120 acres of land there. There are not a lot of places in the world left where you can walk out of your front door to a deserted beach unscarred by footprints. Yet, it offers Ecuadorian prices, about one-third of those found in the US.

I think you should visit there.

HMS Beagle, kind of

55 Years of Trading and Finally my Own Beach!

Let the Current Bring the Sharks to You

Chillin with the Crew

My New Office

The View from Home

My New Neighbors

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 29, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DIGESTION TIME)

(NVDA), (FCX), (META), (MSFT), (TLT), (TSLA), (AAPL), (VISA), (FCX), (COPX), (GOOGL),

(A TRIP TO CUBA)

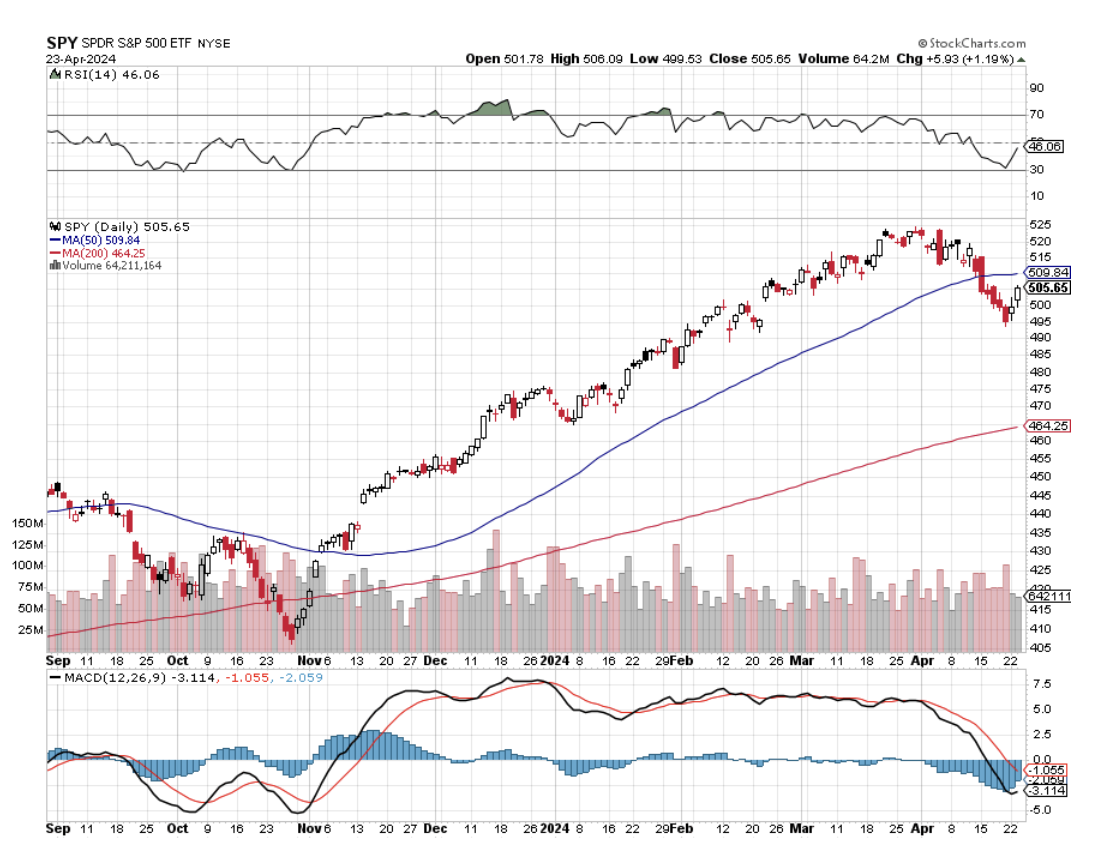

Before you even ask, I’ll give you the answer you’ve all been waiting for: It’s too late to sell and too early to buy.

Stocks may still have some digesting to do having soared by 27% in six months. Nobody wants to look like an idiot by buying a market top. As I have learned over the decades, investors fear looking stupid more than they fear losing money, especially if they are professionals.

Everyone knows the market is eventually going higher so they are not selling in any meaningful way unless they are short-term, algos, or day traders.

This means we may have a whole lot of nothing going on in the coming weeks or months.

That leaves us time to examine the most interesting trends going on in the markets right now, especially the new bull market in commodities. Believe it or not, we are still unwinding the long-term effects of Covid 19 and commodities have only recently come to the fore.

Remember Covid?

Since October, copper prices have risen by 22%, oil by 23%, gold by 34%, and uranium by a gobsmacking 83%. What’s causing this sudden new interest? It’s not a recovering Chinese economy, that’s for sure. Investors have been waiting for a bounce back in the Middle Kingdom seemingly forever. But China remains hobbled by the bitter fruit of a 40-year one-child policy and an ineffective government. History tells us that the United States does not make a great enemy.

So what’s driving the new demand? Remember Covid? Believe it or not, we are still unwinding the long-term effects of Covid 19 and commodities have only recently started to play catch up.

Commodities are unique in that they have such a long lead time to add new supply. It can take 5-10 years, to map out new sites, get government approvals, deliver heavy equipment, and mine, process, refine, and ship the final product.

In the meantime, enormous new demand has arisen. There have been 10 million EVs manufactured in recent years and each one needs 200 pounds of copper. AI means the electric power grid has to double in size quickly. Commodity markets are unable to meet the supply. Therefore, prices can only go up.

That enabled Freeport McMoRan (FCX), the world’s largest copper producer, to handily beat its earnings expectations, helped by higher production and easing costs. The mining giant said its quarterly production of copper rose to 1.1 billion pounds from 965 million pounds a year earlier, helped by a 49% jump in output from its Indonesia operations. (FCX) said it was working with the Indonesian government, which has put a ban on raw material exports, to obtain approvals to continue shipping copper concentrates and anode slimes. Its current license is set to expire in May. Buy (FCX) and (COPX) on dips.

Corporate raiders have taken notice.

Activist Elliot is taking a Run at Mining Giant Anglo American, accumulating a $1 billion stake. BHP, the largest iron ore miner, is also making a takeover bid here on the coattails of which Elliot is trying to ride. It just highlights the global interest in mining shares.

Anglo American plc is a British multinational mining company that is the world's largest producer of platinum, with around 40% of world output, as well as being a major producer of diamonds, copper, nickel, iron ore, polyhalite, and steelmaking coal. On a side note, copper hit a two-year high above $10,000 per metric tonne in the London Market last week.

Needless to say, the commodity boom could continue for another decade.

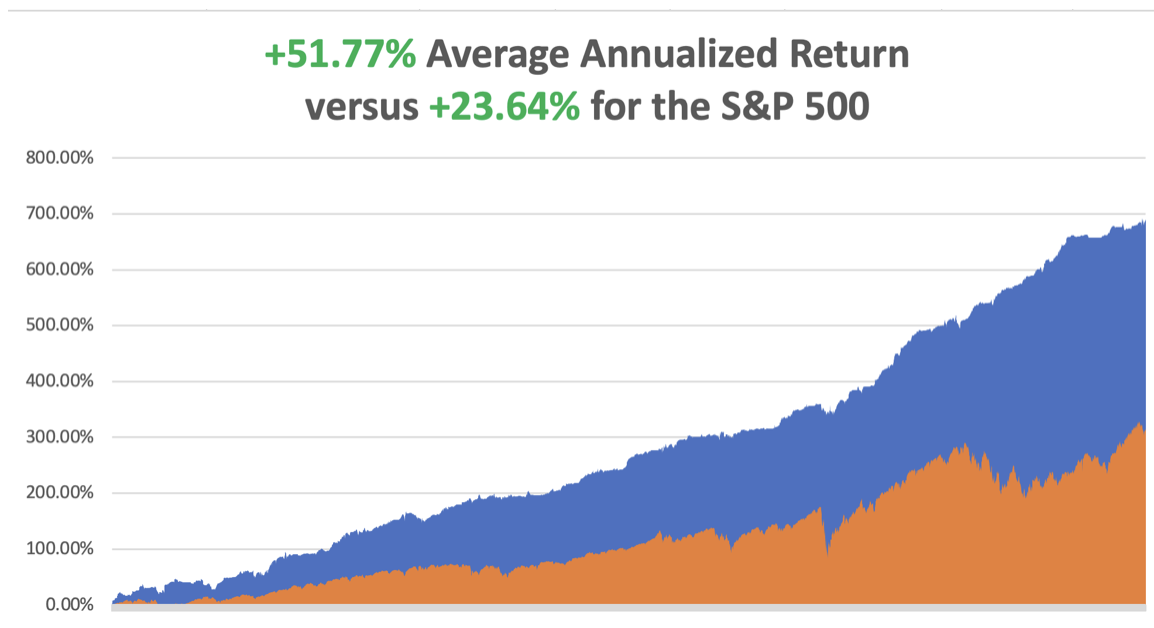

So far in April, we are up +4.24%. My 2024 year-to-date performance is at +13.61%. The S&P 500 (SPY) is up +6.50% so far in 2024. My trailing one-year return reached +32.40% versus +23.14% for the S&P 500.

That brings my 16-year total return to +690.24%. My average annualized return has recovered to +51.77%.

Some 63 of my 70 round trips were profitable in 2023. Some 25 of 33 trades have been profitable so far in 2024.

Tesla Delivers Worst Earnings in 12 Years, with a 9% revenue drop, but the stock rallies big as the disappointment was well telegraphed. Revenue declined from $23.33 billion a year earlier and from $25.17 billion in the fourth quarter. Net income dropped 55% to $1.13 billion, or 34 cents a share, from $2.51 billion, or 73 cents a share, a year ago. The drop in sales was even steeper than the company’s last decline in 2020, which was due to disrupted production during the Covid-19 pandemic. Tesla’s automotive revenue declined 13% year over year to $17.38 billion in the first three months of 2024. I’ll watch (TSLA) from the sidelines from now.

Personal Consumption Expenditures (PCE) Comes in Warm for March, up 2.8% YOY, the same as for February. Service prices led. But the numbers were not as hot as feared so both bonds and stocks rose.

Big Tech Crashes, with all of the Magnificent Seven breaking 50-day moving averages. (NVDA) alone gave up 10% on Friday. The next stop is the 200-day moving averages, which are far, far away. If those hold this is just a correction. If they don’t the bear market is back.

Biggest Treasury Bill Auction in History is a Huge Success, at $69 billion for a two-year paper with a 4.898% yield. That is almost a risk-free government-guaranteed 10% yield in two years. Another $70 billion of five-year notes go on sale today. Half of this is going to foreign investors and central banks. Faith in America and the US dollar remains strong. Who else’s bonds would you rather buy? Passage of the Ukraine aid bill was probably a help. Wait for (TLT) to bottom.

Visa Pops on Earnings Beat, continuing as the powerhouse that it has been for years. Reported at $4.7 billion, showing a 10% increase year-over-year, slightly above the estimate of $4.943 billion. Visa is a call option on the growth of the Internet. Buy (V) on dips.

Apple China Sales Dive, by 19% as Chinese switch to cheaper Huawei phones for nationalism reasons. It’s also another sign of a slow Chinese economy. China remains one of the company’s biggest markets, but business there has grown harder after Beijing escalated a ban on foreign devices in state-backed firms and government agencies. Avoid (AAPL) until the turnaround.

Alphabet Earnings Beat Delivers Monster 10% Move, recovering a $2 trillion market cap. It also announced its first-ever dividend and a $70 billion share back, the second largest after Apple. Buy (GOOGL) on dips.

March New Home Sales Jump, by 8.1% when only 1.1% is expected, to 693,000. The median price of a home sold fell to $430,700 as builders pulled back on incentives like those cherry cabinets. It’s an uphill slog with those 7.0% mortgage rates.

CDC Birth Data Fall to Lowest Level Since the Great Depression, 1.1 births per 1,000 people. That is well below the Great Depression levels. Only 3,664,292 new Americans were born in 2021. It means there will be a shortage of consumers in 20 years so be out of stock by then. The good news is that Covid deaths have fallen from 4,000 per day to only 19 a day since January 2020.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 29, at 10:30 AM EST, the Dallas Fed Manufacturing Index is announced.

On Tuesday, April 30 at 9:00 AM, S&P Case Shiller National Home Price Index is released.

On Wednesday, May 1 at 2:00 PM, the ADP Private Employment Change report will be published

On Thursday, May 2 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, May 3 at 8:30 AM, the April Nonfarm Payroll Report is announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I have wanted to visit Cuba for decades. But relations with the US have run hot and cold over the years and whenever I had the time and money to go, the was a chill on, sometimes an extreme one.

So when I arrived in Key West and learned they were offering Cuba tour packages, I jumped at the chance. Unfortunately, you need to book three months in advance so that option was out.

Then I thought, “Why not fly there myself?” After payment of some hefty fees, commissions, and some outright bribes, I scored a Cuban visa and an aging Britten-Norman Islander twin built in the UK some 40 years ago. It was perhaps the smallest twin I have ever flown, with two minuscule 270 horsepower engines.

Although it was only 90 miles to Cuba, I had to load up with full tanks. Cuban aviation fuel is often contaminated with sludge or water and is unsafe to use. Losing both engines over shark-infested waters doesn’t fit in with my retirement plan. So I needed enough 100LL avgas to make the round drip, which meant skipping breakfast to stay within my weight limitations.

It was a clear and balmy morning when I received my clearance for takeoff, the sky dotted with fluffy white cumulus clouds. Of course, I had to skirt the Bermuda Triangle to get there, but no worries.

Amazingly Cuban air traffic control spoke English. Soon, the green hills of Cuba appeared on the horizon, and I received the words I will never forget: “N686KW you are cleared for landing in Havana.” I haven’t felt like that since I last landed in Moscow.

Much to my surprise, I found other US aircraft there as I was parked near jets from Southwest and American Airlines. I was greeted by an immigration officer who escorted me into the country, putting my Spanish skills to the test.

I had some concerns that I might be arrested in case Russia put me on a wanted list due to my recent work in Ukraine. But my fears proved unwarranted. You see, you get paranoid in your old age. A private car, a French Citroen van, a driver, and a government guide were waiting for me outside the airport.

Suddenly, I found myself in a strange new world. A darkly tanned people wore tired polyester clothes. Everyone was rail thin and the only obese people I saw were foreign tourists. There was an incredible variety of vehicles on the road, including ancient cars from Russia, China, Poland, and Japan. Apparently, Chevrolet had a great year in Cuba in 1956 because no American cars have entered the country since then and they are everywhere.

We headed straight for Earnest Hemingway’s Cuban home, known as Finca Vigia, or “Lookout Farm” built in 1886 on a hilltop overlooking Havana. The building was falling apart and showed large cracks, but going inside I was transported in time back to 1960, when Hemingway left the property ahead of the Cuban Revolution.

Finca Vigia has been untouched since. The walls are covered with an assortment of hunting trophies from Africa, including springboks, cape buffalo, lions, and leopards. They were collections of African spears and gun cases. Mounted on the walls were paintings of bullfights in Spain, cartoons about Hemingway, and family photos.

Magazine racks were stuffed with the 1960 issues of Life, Look, and The Saturday Evening Post. The National Geographic issues looked positively prehistoric. And there were thousands of books. Anyone who read his books would recognize all of this.

Hem, as his friends called him, bought the property in 1940 for $8,000, living there with wife three for five years, the famed war correspondent Martha Gellhorn, and wife four, Time magazine reporter Mary Welsch, who became his widow.

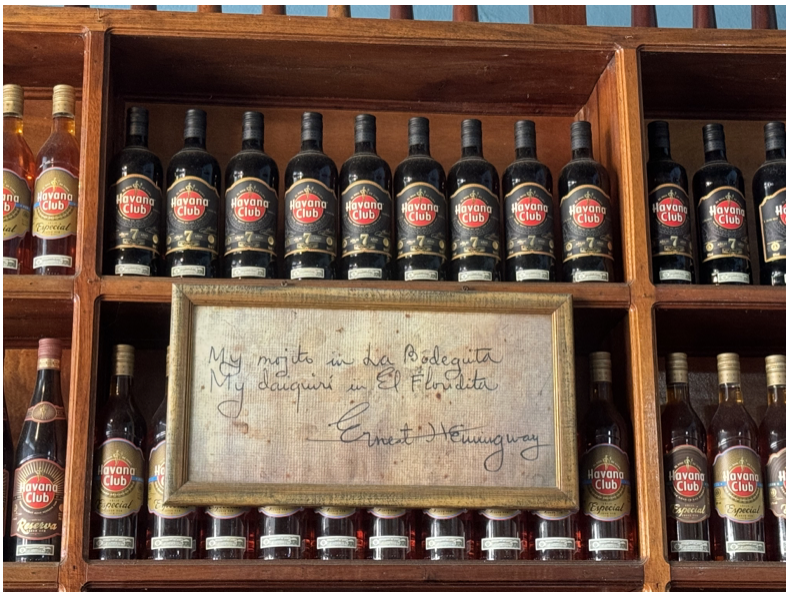

After passing on a Che Guevara T-shirt in the gift shop, I enjoyed a glass of freshly squeezed sugar cane juice. Then I headed into Havana, escorted by my guide, Eliar. The trip turned into a Hemingway bar crawl. I visited the well-known La Floridita, which made Hem’s favorite Daiquiri, La Bodegita, which mixed the best mojito and had lunch at his favorite roof terrace restaurant.

Cuba has long been one of the worst-managed countries in the world, second only to North Korea, and I learned why after grilling my guide all day about economic conditions. It’s 11.2 million people earn a per capita of $11,255, with 71% living below the poverty line. The real figure is a third of that as there are now 300 pesos to the US dollar, not the fictitious 120 that the government pretends.

When the Soviet Union collapsed in 1992, generous subsidies ended and Cuba quickly lost 33% of its GDP. With some of the richest farmland in the world, it imports 80% of its food and is currently suffering a food crisis. Even the bottled water I drank came from Panama.

Oil accounts for 100% of its energy supply which mostly comes from Russia and is paid for with raw sugar. Cuba’s largest exports are tobacco, nickel, and zinc most of which are exported to China. China also provided $11 billion in loans which Cuba promptly defaulted on.

The country would have been much better off if only Fidel Castro had accepted an offer from the Washington Senators to play US major league baseball in the early 1950s. Cuba is officially one of the last communist countries in the world, with Russia and China abandoning it years ago. After reforms in the 1990s, what they now practice is an odd mixture of communism and capitalism, with the government and the private sector competing side by side.

With thousands fleeing the country every year the real estate market has collapsed. You can buy a two-bedroom apartment in Havana for $30,000. Flying over the countryside at low altitude you fund vast expanses of agricultural land undeveloped for want of machinery and parts. There is unused labor everywhere. Cuba should be one of the richest countries in the world with all those beaches. The tourism possibilities are enormous. But with a 60-year trade and investment ban from the US, nothing can happen.

American credit cards and cell phones don’t work, so I brought in $200 in ones. You can’t bring back to the US the country’s only two worthy exports, rum and cigars. But there are buskers everywhere and by the end of the trip, I ended up giving it all away in tips. I did OK with the food, but only ate overcooked meals in high-end restaurants. Salads were out of the question but drink all the local beer and rum you can.

I ended my trip with a tour of the enormous Revolution Square where Fidel Castro used to give four-hour speeches to one million. One area the government did not skimp on spending was on the massive ministry buildings that surround the square. It seems the image of a strong government, especially the police, is essential in a workers’ socialist paradise.

Then it was back to the airport where surprisingly I obtained immediate clearance for takeoff. No passport stamps, as the government wanted to leave no evidence of my visit in an American passport. I returned to Key West just in time to catch a magnificent sunset over the Gulf of Mexico. US customs recognized my face and waved me right through.

Damn! Should have picked up some of those $5 bottles of rum.

It's all just another day in the life of John Thomas.

At Hemingway’s Cuban Home

A Look Back into 1960

Where Hem Wrote “Old Man and the Sea”, Standing

Hemingway’s Office

I passed on Che

Meeting an Old Friend for a Round at Floridita

Mixing it up with the Locals

One of Cuba’s Only Exports

Looks Like Chevy had a Great Year in 1956

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 25, 2024

Fiat Lux

Featured Trade:

(RISK CONTROL FOR DUMMIES) or (THE HEADS I WIN, TAILS YOU LOSE STRATEGY),

(SPY), (FCX), (NVDA), (TLT)

Whenever I change my positions, the market makes a major move, suffers a “black swan” or reaches a key level, I stress test my portfolio by inflicting various scenarios upon it and analyzing the outcome.

This is common practice and second nature for most hedge fund managers.

In fact, the larger ones will use top-of-the-line mainframes powered by $100 million worth of in-house custom programs to produce a real-time snapshot of their positions in hundreds of imaginable scenarios at all times. This is the sort of thing Ray Dalio used to do.

If you want to invest with these guys feel free to do so.

They require a $10-$25 million initial slug of capital, a one-year lock-up, charge a fixed management fee of 2%, and a performance bonus of 20% or more.

You have to show minimum liquid assets of $2 million and sign 100 pages of disclosure documents.

If you have ever sued a previous manager, forget it.

And, oh yes, the best-performing funds have a ten-year waiting list to get in, as with my friend David Tepper. Unless you are a major pension fund like the State of California, they don’t want to hear from you.

Individual investors are not so sophisticated and it clearly shows in their performance, which usually mirrors the indexes with less of a large haircut.

So, I am going to let you in on my own, vastly simplified, dumbed down, the seat of the pants, down-and-dirty style of scenario analysis and stress testing that replicates 95% of the results of my vastly more expensive competitors.

There is no management fee, performance bonus, disclosure document, lock up, or upfront cash requirement. There’s just my token $3,500 a year subscription and that’s it.

To make this even easier for you, you can perform your own analysis in the Excel spreadsheet I post every day in the paid-up members section of Global Trading Dispatch.

You can just download it and play around with it whenever you want, constructing your own best-case and worst-case scenarios. To make this easy, please log into your Mad Hedge Fund Trader, click on “MY ACCOUNT”, then click on Global Trading Dispatch, then Current Positions, and download the Excel spreadsheet for April 25, 2024.

There you will find my current trading portfolio showing:

Current Capital at Risk

Risk On

(NVDA) 5/$710-$720 call spread 10.00%

(TLT) 5/$82-$85 call spread 10.00%

(FCX) 5/$42-$45 call spread 10.00%

Risk Off

(NVDA) 5/$960-$970 put spread -10%

Total Net Position 30.00%

Total Aggregate Position 40.00%

Since this is a “for dummies” explanation, I’ll keep this as simple as possible.

No offense, we all started out as dummies, even me.

I’ll the returns in three possible scenarios: (1) The (SPY) is unchanged at $505 by the May 17 expiration of my front month option positions, which is 15 trading days away, (2) The S&P 500 rises 5.0% to $530 by then, and (3) The S&P 500 falls 5.0% to $480.

Scenario 1 – No Change

The value of the portfolio rises from a 5.07% profit to a 13.00% Profit. My existing longs in (FCX), (TLT), and (NVDA) expire at their maximum profits. So does my one short in (NVDA).

Scenario 2 – S&P 500 rises to $530

You can easily forget about the long positions in (FCX), (TLT), and (NVDA) as they will expire well in the money. If they go up fast enough, I might even take an early profit and roll into a June or July position. Our short in (NVDA) might take some heat. But in the current environment of going into the summer doldrums, there is no way (NVDA) shoots up to a new all-time high, right where our strike prices were set at on purpose. The net of all this is that our portfolio should expire at a maximum profit for the year at up 13.00%.

Scenario 3 – S&P 500 falls to $480

All three of my stocks fall, but not enough for my three call spreads to go out of the money. (FCX) will stay above my stop-out level at $45, (TLT) at $85, and (NVDA) at $720. Obviously, the short in (NVDA) becomes a chipshot. Again, we expire at a maximum profit for the year at up 13.00%.

Up we make money, down we make money, sideways we make money, I like it! This is why I run long/short baskets of options spreads whenever the market allows me. It’s a “Heads I win, tails you lose strategy”.

If the market goes up, I’m looking for stocks to sell. If the market goes down, I'm looking for securities to buy. Boy low, sell high, I’m thinking of patenting the idea.

This is the type of extremely asymmetric risk/reward ratio hedge funds are always attempting to engineer to achieve outsized returns. It is also the one you want after the stock market has risen by 25% a year since the 2020 pandemic.

All that’s really happened is that the world has gone from slightly good to better this year. I can rejigger this balance anytime I want. If I think that a change in the economy or the Fed’s interest rate policy is in the works.

Keep in mind that these are only estimates, not guarantees, nor are they set in stone. Future levels of securities, like index ETF’s are easy to estimate. For other positions, it is more of an educated guess. This analysis is only as good as its assumptions. As we used to do in the computer world, garbage in equals garbage out.

Professionals who may want to take this out a few iterations can make further assumptions about market volatility, options implied volatility or the future course of interest rates. Keep the number of positions small to keep your workload under control. I never have more than ten. Imagine being at Goldman Sachs and doing this for several thousand positions a day across all asset classes.

Once you get the hang of this, you can start projecting the effect on your portfolio of all kinds of outlying events. What if a major world leader is assassinated? Piece of cake. How about another 9/11? No problem. Oil at $150 a barrel? That’s a gimme. What if there is an Israeli attack on Iranian nuclear facilities? That might take you all of two minutes to figure out. The Federal Reserve launches a surprise interest rate rise? I think you already know the answer.

The bottom line here is that the harder I work, the luckier I get.

Global Market Comments

April 22, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or FACING HARSH REALITY)

($VIX), (FCX), (XOM), (WPM), (GLD), (TLT), (FCX), (NVDA), (JNK), (META), (MSFT), (TSLA), (HYG), (NFLX), (OXY), (XOM), (USO)

There comes a time in every trader’s life when it’s time to face harsh reality and admit that you’re just dead wrong.

As much as I thought a I had strong case for the best stocks to move sideways before continuing their upward drive, the markets decided otherwise. One thing I have learned over my half-century of trading is that you never argue with Mr. Market. He is always right.

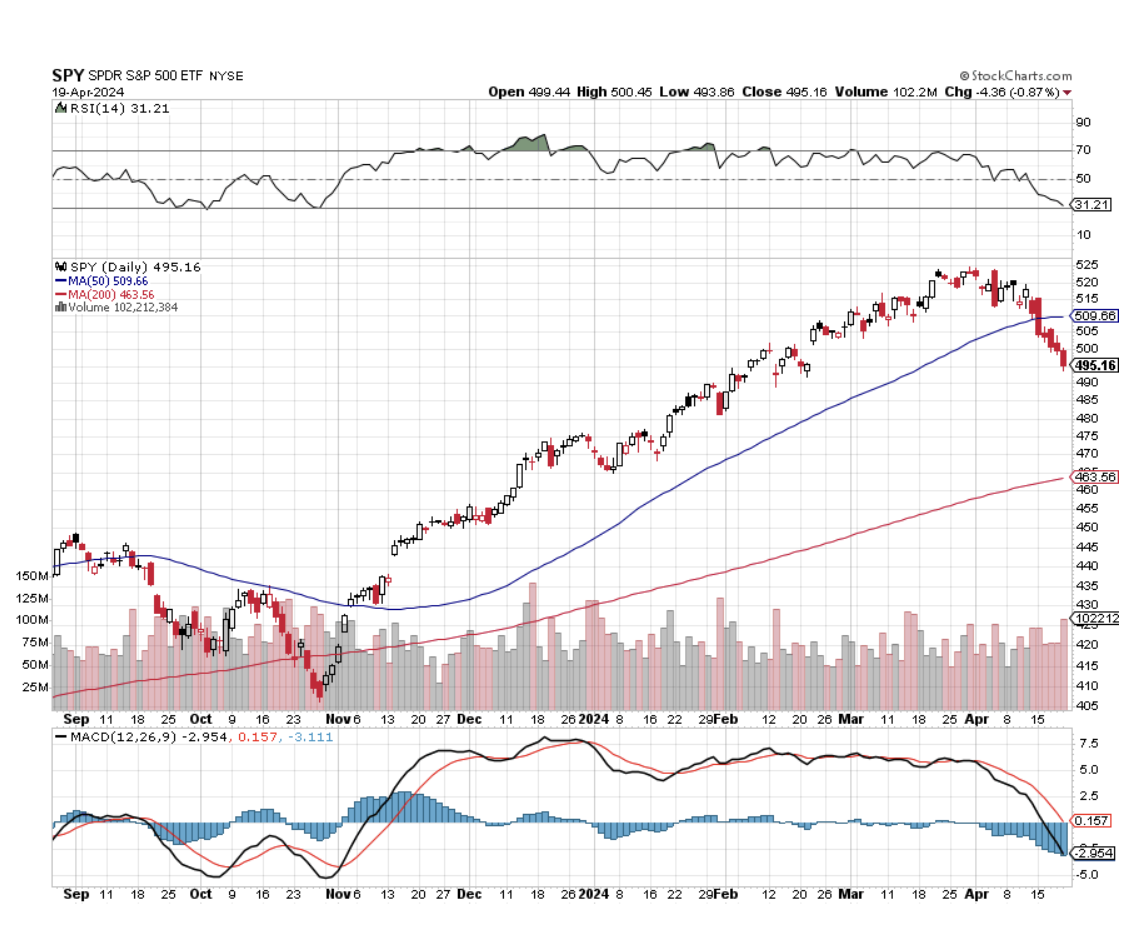

So it was with some dismay that on Friday, I watched NVIDIA (NVDA) shares slice through its 50-day moving average at $840 like a hot knife through butter putting the shares into a free-fall. Virtually the next print was the low of the day at $760, down 10% on the day.

There was no new news about (NVDA). Its prospects look as bright as ever, and there are a series of conferences of earnings reports over the coming month to remind us of that. But sometimes, the market just doesn’t care.

(NVDA) has had a great run, up some 144% since October. During this time, I executed a dozen profitable long-side trades. But when you’re that aggressive you know in advance that the last trade is going to kill you and that is the case today. (NVDA) is falling because of the sheer weight of its price.

New flash: while (NVDA) is still the cheapest big tech stock in the market, cheap stocks can get cheaper as we all know.

With the advantage of 20/20 hindsight, I should have been paying more attention to the Magnificent Seven 50-day moving averages which have been falling like dominoes. First went Tesla (TSLA) in February and Apple in March. The S&P 500 (SPY) gave it up on Monday and Microsoft (MSFT) on Wednesday. Amazon (AMZN), (META), and (NVDA) were the last to go on Friday.

Sure you can blame the April 19 option expiration when traders were loaded to the hilt with expiring longs with all these stocks they had to dump. The dreaded month of May, when traders go to die, and the summer doldrums are just two weeks away. Algorithms poured gasoline on the fire exaggerating the moves, as they always do. But still, wrong is wrong.

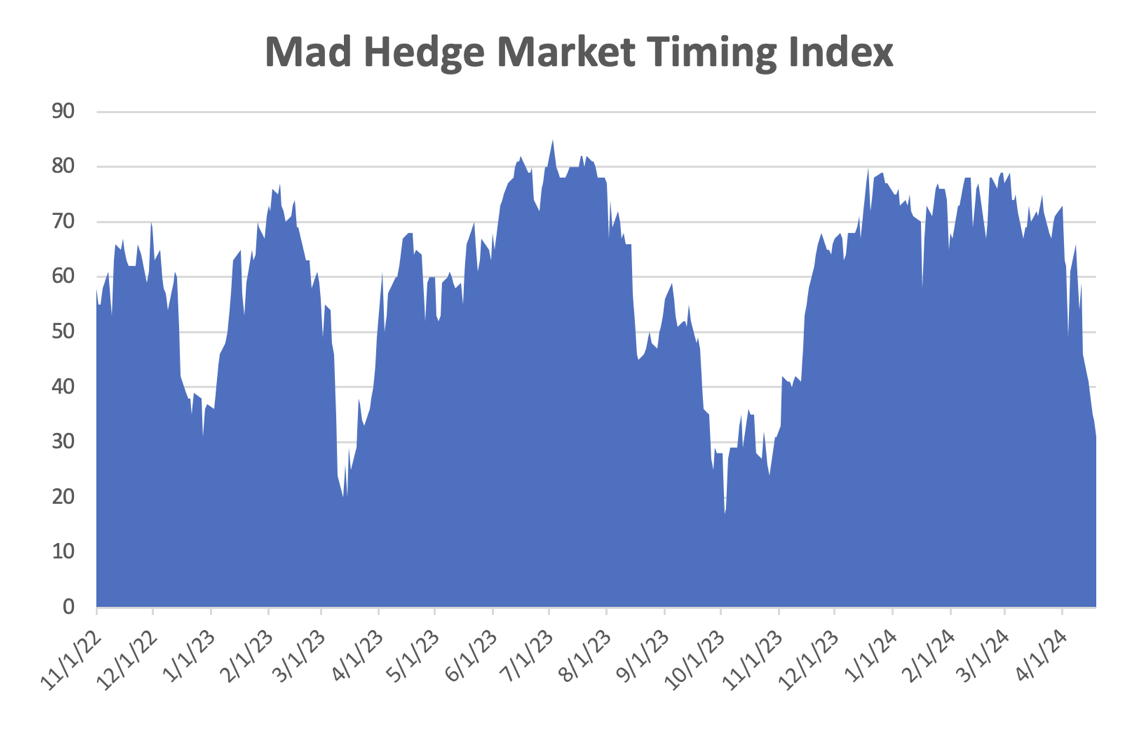

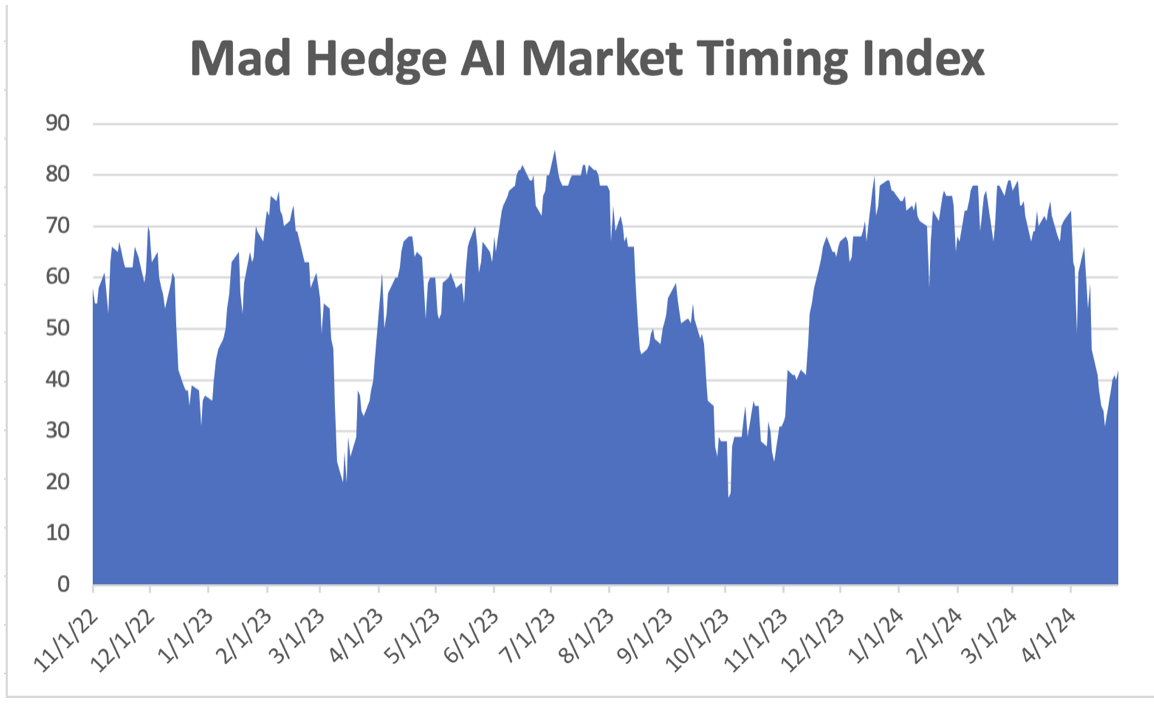

And there’s my mea culpa for 2024. I am human after all. I’m not right all the time, I just act like it. If the horrific market action last week has one silver lining, it’s that it sets up the next great trades, for which there will be many. With my Mad Hedge AI Market Timing Index down to a lowly 31 that may not be far off.

Your next question is “How far down is down?” In the worst-case scenario, the 200-day moving average is in play for all of these. That is pegged at $463 for the S&P 500, $569 for (NVDA), $377 for (MSFT), $150 for (AMZN), and $308 for (META). (AAPL) and (TSLA) already lost their 200-days a long time ago. In other words, the market is in the process of giving up all its 2024 gains and then some.

Sure, the 200 days are all rising sharply so it's unlikely we’ll hit these dire numbers. Still, it's best to prepare your boss for the worst and then let serendipity work its magic.

Remarkably, my commodity and precious metal stocks, where I had eight of ten long positions, stuck to the script and moved sideways instead of down. If you throw bad news on a stock and it refuses to fall, you buy the hell out of it. So that will be my next move in the market, once I clean all the mud off my face and pull the arrows out of my rear.

Those of us who have been trading gold for a long time, I’ve been doing it for 50 years and 60 if you count the Kennedy silver dollars I collected, will tell you that this new bull market in the barbarous relic is a very strange one.

None of the traditional factors that drive gold up are present. Interest rates have lately been rising, not falling. ETF financial demand fell all last year, and much of that money was diverted to Bitcoin. Retail demand, especially from Asia, has also been falling off a cliff. Gold miners have in no way been leading the price of the yellow metal because of their excess leverage as they usually do. But gold has seen a 34% rally off the October low.

Go figure.

It turns out that central bank buying has increased dramatically, especially from China, enough to offset all the other no-shows. The conflict in the Middle East is also drawing in more flight to safety demand. The good news is that the Chinese buying will continue. The bad news is that this might be a precursor to the invasion of Taiwan as it flees the Western financial system.

What does all this mean? When the traditional demand for gold returns, interest rates, ETFs, and retail, the price of gold will move a lot higher. The barbarous relic can easily reach $2,800 this year and possibly $3,000. The miners will play catch up. Buy (GLD) on dips and silver (SLV) as well, which has a lot of catching up to do.

I just thought you’d like to know.

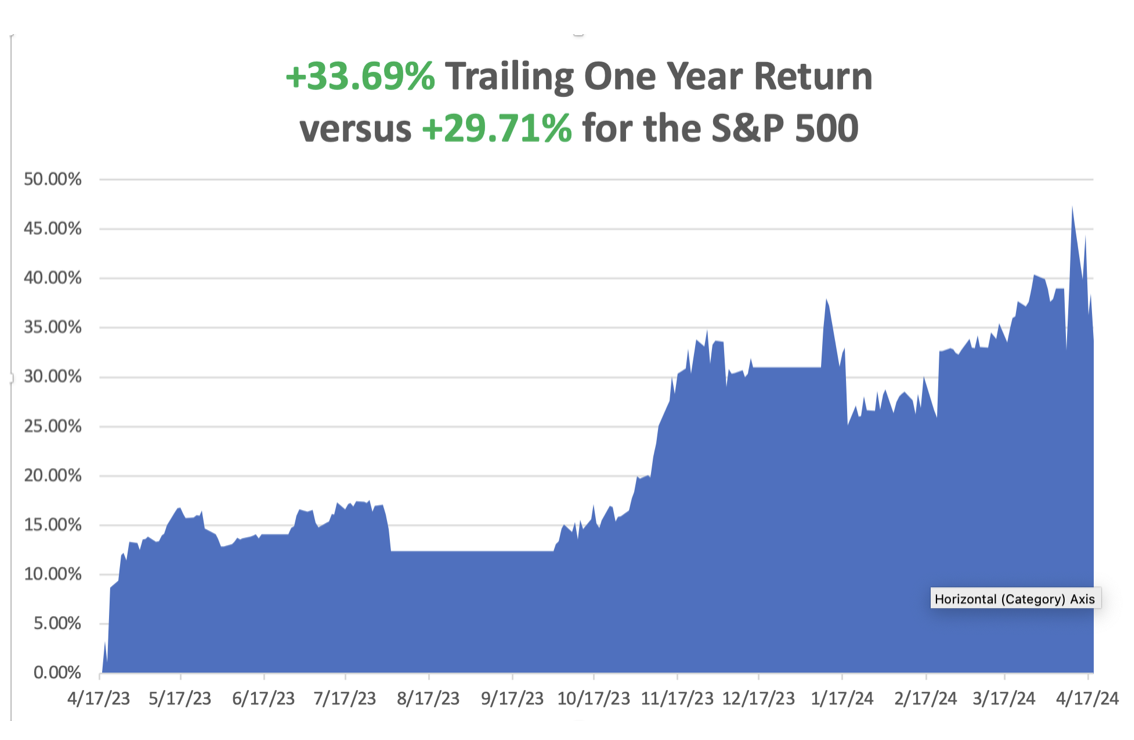

So far in April, we are down a heartbreaking -6.69%. My 2024 year-to-date performance is at +14.47%. The S&P 500 (SPY) is up +2.68% so far in 2024. My trailing one-year return reached +33.69% versus +29.71% for the S&P 500.

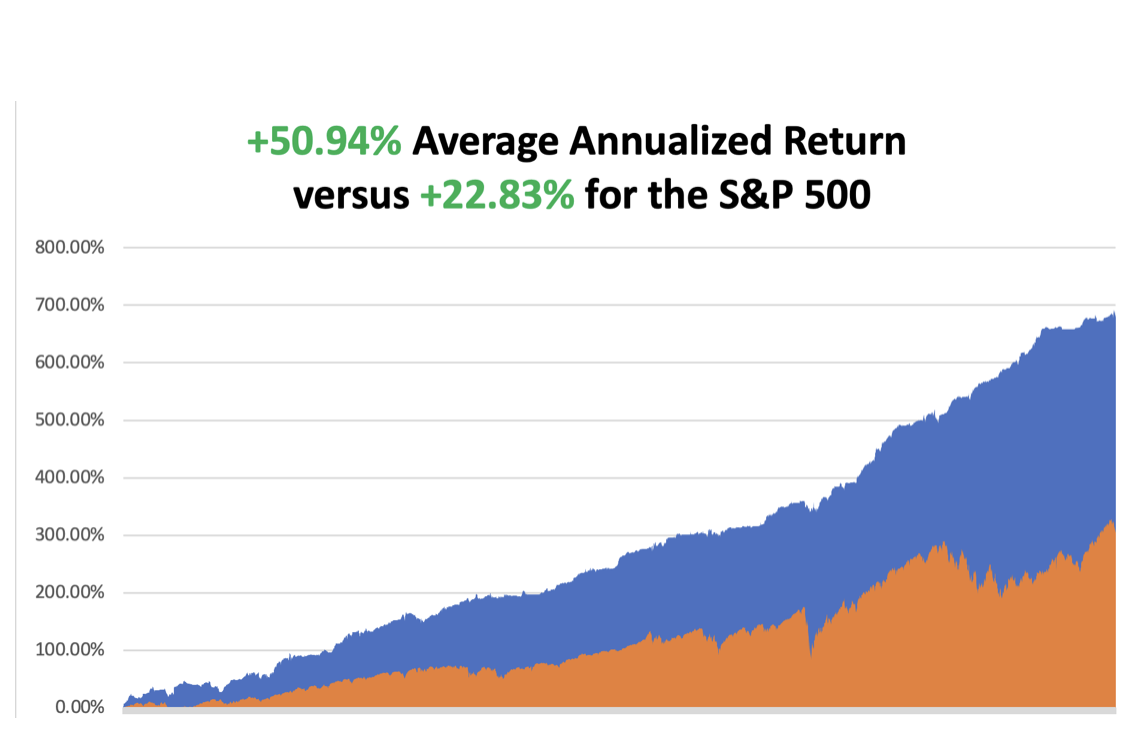

That brings my 16-year total return to +676.63%. My average annualized return has recovered to +50.94.

Some 63 of my 70 round trips were profitable in 2023. Some 20 of 28 trades have been profitable so far in 2024.

I stopped out of my long in Tesla last week at cost, expecting further downside, which happened. A week early the position had been at max profit. I let my April longs expire at a max profit on April 19 in Freeport McMoRan (FCX), Occidental Petroleum, ExxonMobile (XOM), Wheaton Precious Metals (WPM), and Gold (GLD).

That leaves me with my remaining May longs in (TLT) and (FCX) a double long in (NVDA) and 60% in cash.

Volatility Index ($VIX) Hits Six-Month High, on threats of a New Iran War, Oil Supply Cut-offs, and topping stocks. It’s been a long and dry desert crossing, but we are finally back to reach the $20 handle. The volatility trade is back. For a double bonus, the Mad Hedge Market Timing Index also dropped below 50 for the first time since October. Options traders will love it!

Junk Bonds See Biggest Outflows in a Year, as the Federal Reserve’s hawkish approach to inflation makes investors wary, sending yields soaring to 6.33%. Yields won’t peak until the Fed actually cuts rates. Buy (JNK) and (HYG) on dips.

Netflix (NFLX) Adds 9.33 Million New Subscribers, nearly double analyst forecasts, including my five kids who aren’t allowed to share my password anymore. But the shares dropped on weak Q2 guidance. Netflix has rebounded from a slowdown in 2021 and 2022 to grow at its fastest rate since the early days of the coronavirus pandemic. That is due in large part to its crackdown on people who were using someone else’s account. The company estimated more than 100 million people were using an account for which they didn’t pay.

Mortgage Rates Top 7.0% for the first time in 2024, adding dead weight to the housing market. Most borrowers are now taking out adjustable 5/1 ARMS and then praying for a Fed rate cut later this year.

Existing Home Sales Dive by 4.3% in March to 4.19 million units on a sign-contract basis. Inventories rose 4.47% to a 3.2-month supply, up 14% YOY. The median price of an existing home sold in March was $393,500, up 4.8% from the year before. Regionally, sales fell everywhere except in the North, where they rose 4.2% month-to-month. Sales fell hardest in the West, down 8.2%. Prices are highest in the West.

Housing Starts Plunge, down 14.5% in March. Permits for future construction of single-family houses fell to a five-month low. Residential investment rebounded in the second half of 2023 after contracting for nine straight quarters, the longest such stretch since the housing market collapse in 2006. But the recovery appears to be losing steam.

China Surprises with Q1 GDP Growth at 5.3%, but who knows how real these numbers really are? They don’t line up with individual data like international trade. Peak China is behind us. Avoid (FXI).

Tariff Wars Heat Up, US President Joe Biden is threatening China again, and this time he wants to triple the China tariff rate on steel and aluminum imports. On Wednesday, the president will visit the United Steelworkers headquarters in Pittsburgh and has vowed his saber-rattling is not just empty threats. His rhetoric on China could make relations between the US and the Middle Kingdom that much frostier as we enter into the heart of the US election race.

Biden Boosts the Cost of Alaska Oil Drilling Leases, from $10,000 to $160,000, the first increase since 1920. There is also a bump in the royalty on extracted oil, from 12.25% to 16.27%. The government is no longer giving away oil found on its land for free. Coddling of the oil companies is over. Oil companies will no longer bid for cheap oil leases with the intention of sitting on them for decades. The US is currently the largest oil (USO) producing country in history at 13 million barrels/day and hardly needs any subsidies, which date back to the Great Depression. Buy energy stocks on dips, like (XOM) and (OXY), which are posting record profits.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 22, at 7:00 AM EST, the Chicago Fed National Activity Index is announced.

On Tuesday, April 23 at 8:30 AM, New Home Sales are released.

On Wednesday, April 24 at 2:00 PM, Mortgage applications come out.

On Thursday, April 25 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, April 26 at 8:30 AM, Consumer Expectations. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I spent a decade flying planes without a license in various remote war zones because nobody cared.

So, when I finally obtained my British Private Pilot’s License at the Elstree Aerodrome, home of the WWII Mosquito twin-engine bomber, in 1987, it was cause for celebration.

I decided to take on a great challenge to test my newly acquired skills. So, I looked at an aviation chart of Europe, researched the availability of 100LL aviation gasoline in Southern Europe, and concluded that the farthest I could go was the island nation of Malta.

Caution: new pilots with only 50 hours of flying time are the most dangerous people in the world!

Malta looms large in the history of aviation. At the onset of the Second World War, Malta was the only place that could interfere with the resupply of Rommel’s Africa Corps, situated halfway between Sicily and Tunisia. It was also crucial for the British defense of the Suez Canal.

So, Malta was mercilessly bombed, at first by Mussolini’s Regia Aeronautica, and later by the Luftwaffe. By April 1942, the port at Valletta became the single most bombed place on earth.

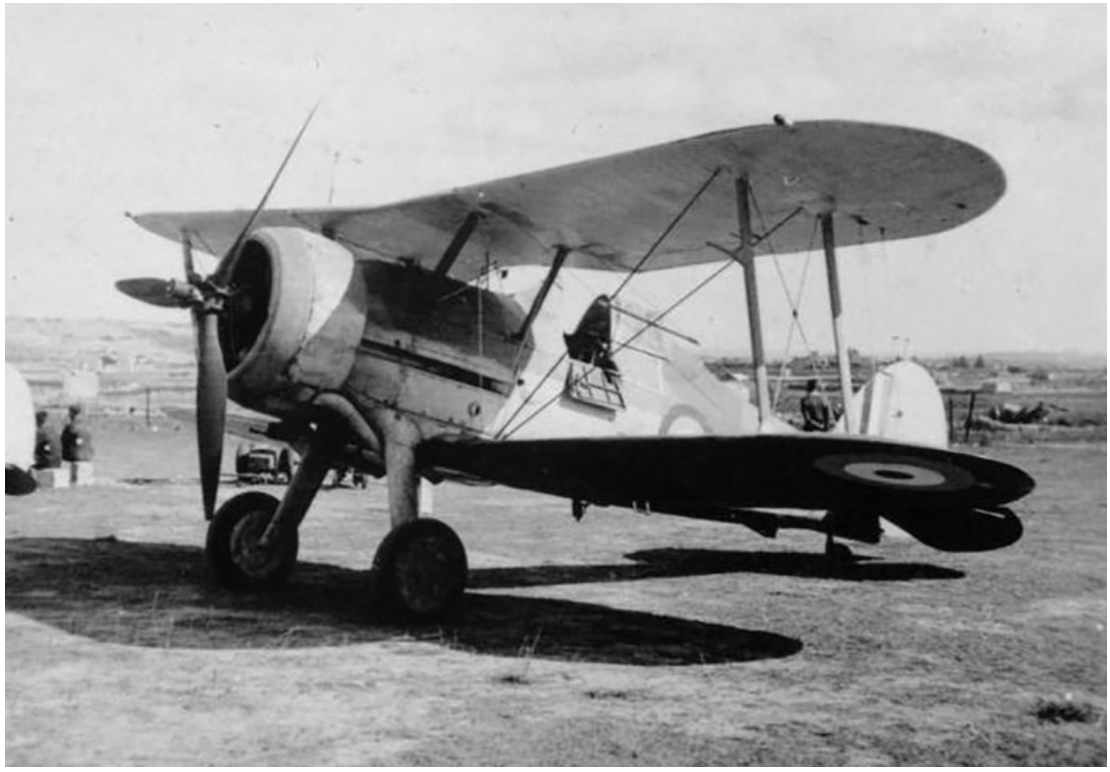

Initially, Malta had only three obsolete 1934 Gloster Gladiator biplanes to mount a defense, still in their original packing crates. Flown by volunteer pilots, they came to be known as “Faith, Hope, and Charity.”

The three planes held the Italians at bay, shooting down the slower bombers in droves. As my Italian grandmother constantly reminded me, “Italians are better lovers than fighters.” By the time the Germans showed up, the RAF had been able to resupply Malta with as many as 50 infinitely more powerful Spitfires a month, and the battle was won.

So Malta it was.

The flight school only had one plane they could lend me for ten days, a clapped-out, underpowered single-engine Grumman Tiger, which offered a cruising speed of only 160 miles per hour. I paid extra for an inflatable life raft.

Flying over the length of France in good weather at 500 feet was a piece of cake, taking in endless views of castles, vineyards, and bright yellow rapeseed fields. Italy was a little trickier because only four airports offered avgas, Milan, Rome, Naples, and Palermo. Since Italy had lost the war, they never experienced a postwar aviation boom as we did.

I figured that if I filled up in Naples, I could make it all the way to Malta nonstop, a distance of 450 miles, and still have a modest reserve.

Flying the entire length of Italy at 500 feet along the east coast was grand. Genoa, Cinque Terra, the Vatican, and Mount Vesuvius gently passed by. There was a 1,000-foot-high cable connecting Sicily with the mainland that could have been a problem, as it wasn’t marked on the charts. But my US Air Force charts were pretty old, printed just after WWII. But I spotted them in time and flew over.

When I passed Cape Passero, the southeast corner of Sicily, I should have been able to see Malta, but I didn’t. I flew on, figuring a heading of 190 degrees would eventually get me there.

It didn’t.

My fuel was showing only a quarter tank left and my concern was rising. There was now no avgas anywhere within range. I tried triangulating VORs (very high-frequency omnidirectional radar ranging).

No luck.

I tried dead reckoning. No luck there either.

Then I remembered my WWII history. I recalled that returning American bombers with their instruments shot out used to tune in to the BBC AM frequency to find their way back to London. Picking up the Andrews Sisters was confirmation they had the right frequency.

It just so happened that buried in my pilot’s case was a handbook of all European broadcast frequencies. I looked up Malta, and sure enough, there was a high-powered BBC repeater station broadcasting on AM.

I excitedly tuned in to my Automatic Direction Finder.

Nothing. And now my fuel was down to one-eighth tanks and it was getting dark!

In an act of desperation, I kept playing with the ADF dial and eventually picked up a faint signal.

As I got closer, the signal got louder, and I recognized that old familiar clipped English accent. It was the BBC (I did work there for ten years as their Tokyo correspondent).

But the only thing I could see were the shadows of clouds on the Mediterranean below. Eventually, I noticed that one of the shadows wasn’t moving.

It was Malta.

As I was flying at 10,000 feet to extend my range, I cut my engines to conserve fuel and coasted the rest of the way. I landed right as the sun set over Africa.

While on the island, I set myself up in the historic Excelsior Grand Hotel. Malta is bone dry and has almost no beaches. It is surrounded by 100-foot cliffs. I paid homage to Faith, the last of the three historic biplanes, in the National War Museum in Valetta.

The other thing I remember about Malta is that CIA agents were everywhere. Muammar Khadafy’s Libya was a major investor in Malta, recycling their oil riches, and by the late 1980s owned practically everything. How do you spot a CIA agent? Crewcut and pressed, creased blue jeans. It’s like a uniform. What they were doing in Malta I can only imagine.

Before heading back to London, I had to refuel the plane. A truck from air services drove up and dropped a 50-gallon drum of avgas on the tarmac along with a pump. Then they drove off. It took me an hour to hand pump the plane full.

My route home took me directly to Palermo, Sicily to visit my ancestral origins. On takeoff to Sardinia, wind shear flipped my plane over, caused me to crash, and I lost a disk in my back.

But that is a story for another day.

Who says history doesn’t pay!

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

“Faith”

The Andrews Sisters

Spitfire

Grumman Tiger