Expect this type of showmanship to be the new normal as the U.S. government goes pedal to the medal hoping to extract better trade terms.

In the short term, expect wild swings in the prices of US tech stocks.

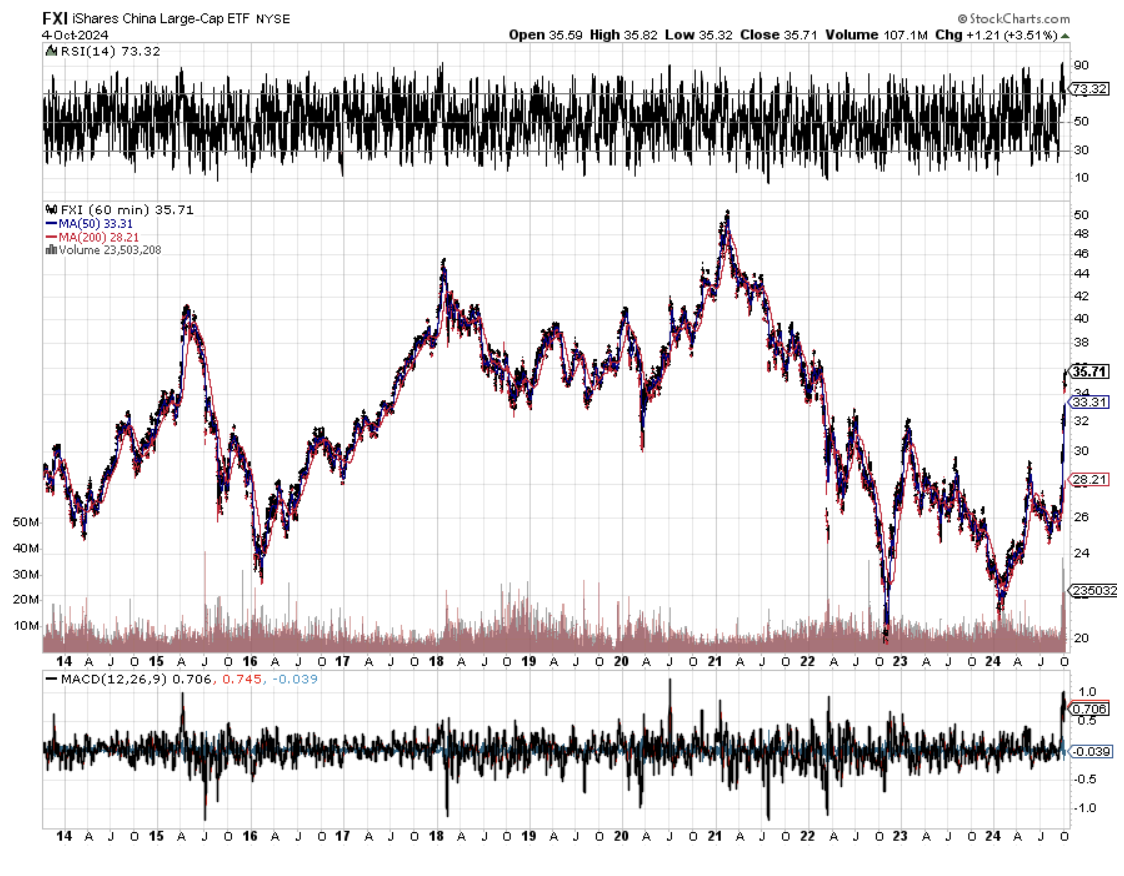

U.S. President Trump unilaterally raised the US tariff rate on China (FXI) to 125% and instituted a 90-day pause on steep 'reciprocal' tariffs.

The Nasdaq shot up by an intraday 10% - an unprecedented type of market reaction stemming from short-covering.

The entire tech index was heavily weighted for lower Nasdaq ($COMPQ) share prices and this one announcement torpedoed the short-term momentum to the downside.

2025 is presenting itself to be one of the hardest environments to trade in the last two decades plus as tech shares are the trajectory of them are reliant on the whims of an aggressive new federal government.

People are scared – scared more about the uncertainty this presents.

Uncertainty creates an environment to sell stock resulting in meaningful lower-tech shares.

Additionally, it is very obvious the federal government will target China and the way it does business to reign them in. They are the big fish.

Remember that China has a massive youth unemployment rate problem inching towards 30% and the Chinese Communist Party (CCP) knows they are playing with fire if Trump’s tariffs result in millions of new job layoffs.

Trump on Tuesday claimed that China, as well as other countries, are keen to negotiate. Those talks have reportedly begun with Japan and South Korea. But he has remained defiant as members of his own party and Wall Street billionaires start to push back.

On the negotiations front, both markets and trading partners still seem to be searching for what exactly Trump is seeking.

The president’s approach has prompted retaliation from China and caused other countries to draw up their own plans to hit American exports. As a result, economists have raised their expectations for a recession in the United States, and many now consider the odds to be a coin flip.

During the trade fight with China in Mr. Trump’s first term, U.S. agricultural exports plummeted after China imposed high retaliatory duties on soybean, corn, wheat, and other American imports, and the United States spent about $23 billion to support American farmers.

The Retail Industry Leaders Association, which represents major companies like Walmart, Target, and Best Buy, said this could drive up prices for the American consumer.

In the short term, this should first alleviate the pressure on the U.S. dollar and the price hikes for tech products.

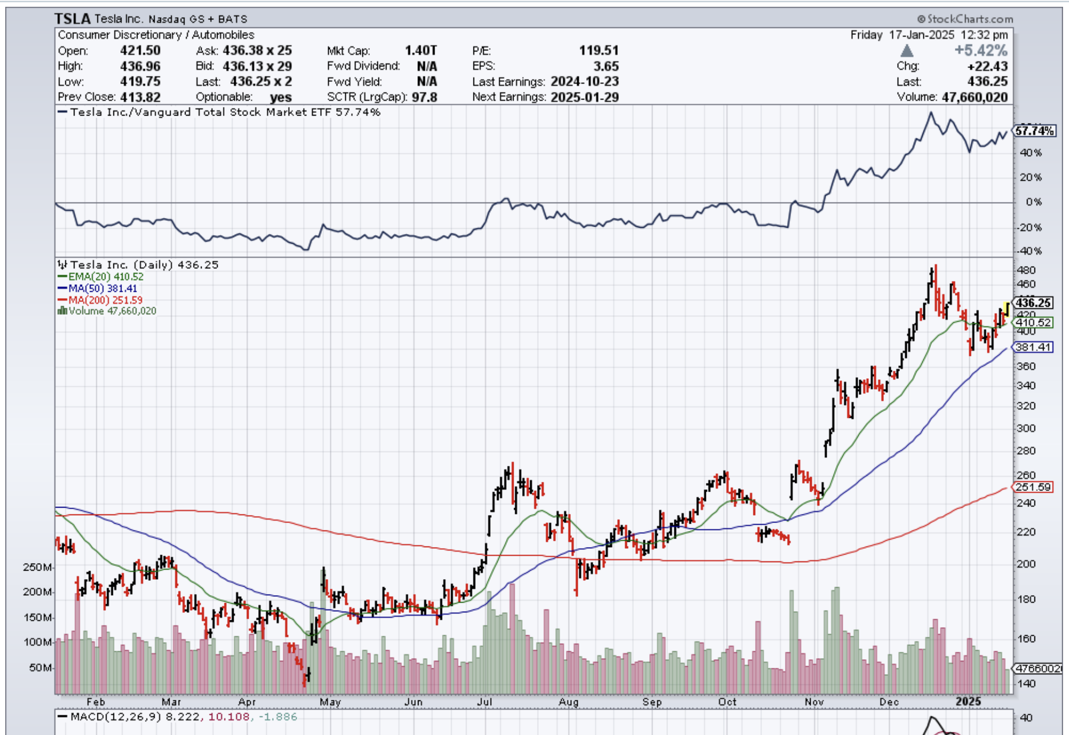

I would stay away from companies that have exposure to China like Tesla and Micron.

Gradually, we will see countries come to the table and if this gets through, even in diluted form, it would be considered a victory for US tech stocks.

Sure, the Federal Government could again jump back on its horse and go insane with the tariffs, but I do believe this pause highlights the fact that they aren’t willing to nuke the economy and tech sector just yet.

I also believe there is a roadmap to claim victory in all of this.

It starts with East Asian countries like Japan and South Korea which will take a “bad deal” in exchange for stability.

We have seen this a few times with Japan and I don’t believe they will reject America’s approach when Japan’s economy, society, and direction are even worse than Europe and America combined.

Once we get a little bit more settled and predictable, it should be a great buy-the-dip opportunity in tech shares.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-04-09 14:02:402025-04-09 16:34:57Tech Shares Recover on Macro News

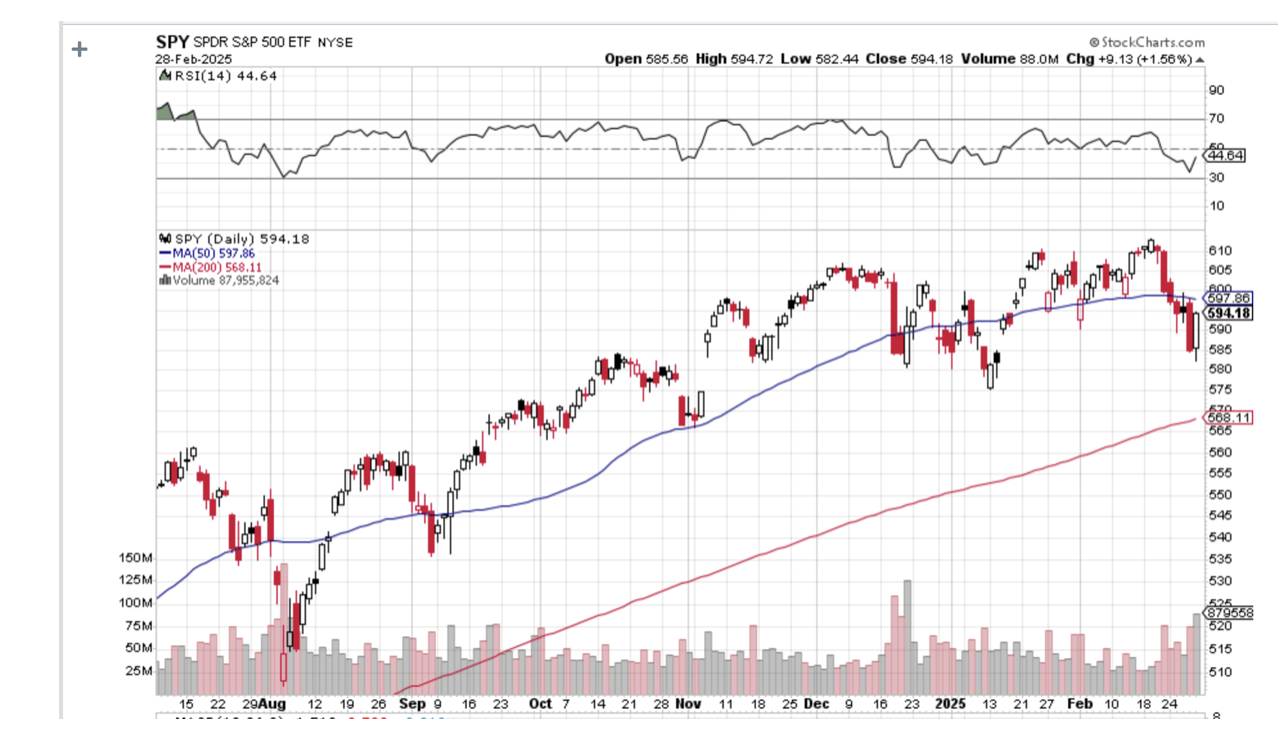

Armageddon is not a word I use lightly. But this weekend, every technical service I subscribed to warned that the recent damage to the market was immense. It’s time to raise cash, hedge your positions, or otherwise position for a bear market.

I have noticed over the past half-century that the best technicians spend a lot of time reading up on fundamentals, and the best fundamentalists spend a lot of time looking at charts. When both go to hell in a handbasket, as they are now, it’s time to head for the hills.

The only way Armageddon can be avoided, or at least postponed, is if the trade war, which is about to cut S&P 500 (SPY) earnings by half, suddenly ends. Only one person knows if that is going to happen, and he isn’t sharing any of his cards with me.

If the trade war continues or expands, the math here becomes very simple. The shares of companies that earn less money are worth less.

You learn in flight school that accidents aren’t usually the result of a single problem but several compounding ones. I know this too well because I have crashed three planes, in the Austrian Alps, in Sicily, and in Paris. First, the gyroscope blows up, then the radio goes out, and then you lose an engine when the weather turns bad. It doesn’t help when someone is shooting at you, either.

The problem for stock owners now is that there isn’t just one thing going wrong with the investment landscape right now; there are several compounding ones, like inflation, immigration, taxes, the deficit, the Ukraine War, and the end of American leadership of the West.

Loss of confidence in the top, which took a quantum leap downward in the wake of the dumpster fire at a White House Zelinski meeting, has consequences. At this point, every businessman in America is asking himself if he can survive the current regime.

With a scant one-seat majority in Congress, a budget can’t pass by March 14, when a government shutdown begins. It means that there will be no new tax cuts by year-end. Chaos ratchets up. Businessmen hate chaos.

It also means that the 2017 tax cuts extension isn’t going to happen, which adds $5 trillion in new taxes on the country just when the economy is slowing dramatically. Uncertainty runs rampant.

Here's the problem for investors with that. Confident markets trade at big premiums, as we saw for the last three years. Uncertain markets trade at big discounts. If I’m right, that discount will be 20%. If I’m wrong, it's 50%.

Ceding America’s leadership of the West comes at a heavy price. It started 80 years ago with the end of WWII. American stock markets have done pretty well during this time, rising by 435 times.Why anyone would want to give up such a system is beyond me.

For example, the US dollar would lose its reserve currency status. There is no way the national debt could have risen to $36 trillion, half of which was bought by foreigners, and all of which was used to stimulate the economy, without reserve currency status. Take that away, and economic growth goes elsewhere. So do higher stock prices, which we have already seen this year in China and Europe.

There is a fundamental repricing of the market taking place, and we are only just at the beginning.

About that economy thing. On Friday, the Atlanta Fed predicted that the US economy SHRANK by -1.5% in Q1. It would be easy to say, “There goes the Atlanta Fed again,” whose model is always prone to extreme predictions. But it is safe to say that the economy is either not growing or growing at a dramatically slowing rate.

The problem for investors? Reliable growing economies, which we have had since the Pandemic five years ago, support high stock multiples. Non-growing or shrinking economies can only support low earnings multiple. Remember back in 2009, the S&P 500 traded at a lowly multiple of only 9X, against today’s 25X.

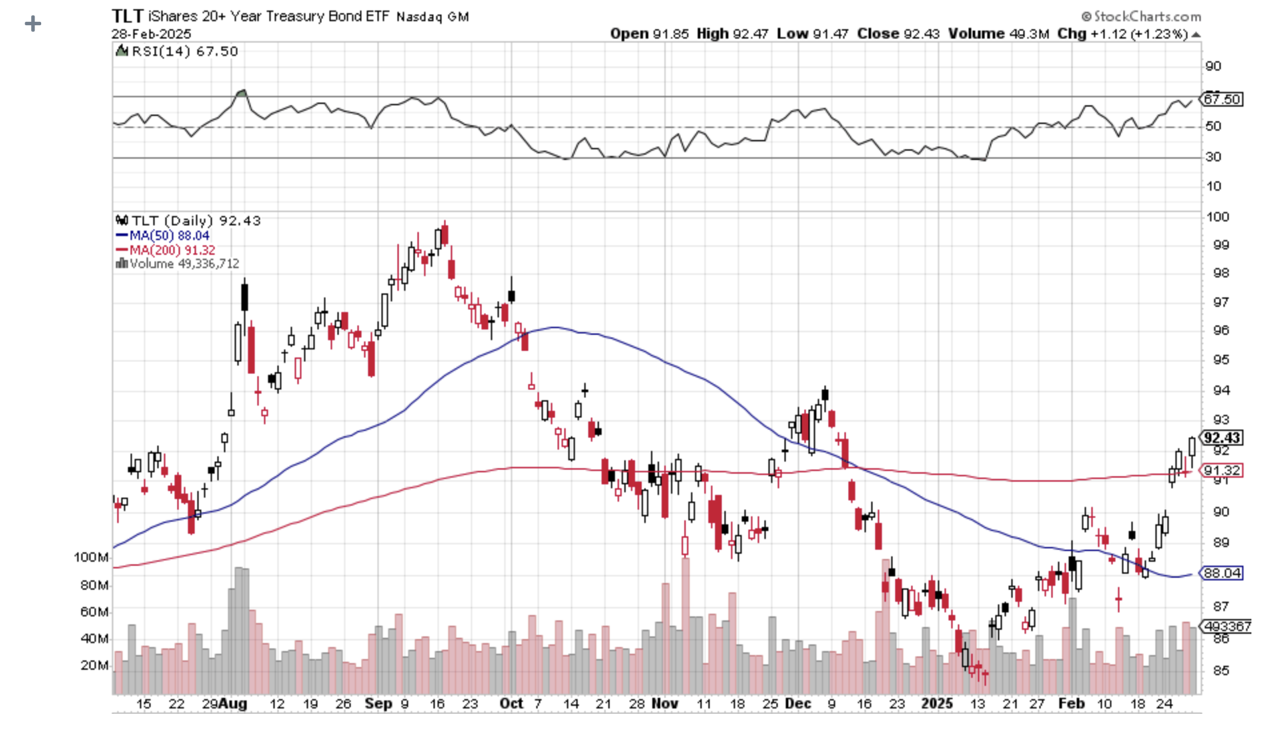

This isn’t just me howling at the moon. With a meteoric $10 rally this year, the bond market is starting to warn of a coming recession. Ten-year US Treasury bond yields have cratered from 4.80% to 4.20%. This is in the face of massive bond issuance in 2025, some $1.7 trillion worth, the product of the 2017 Trump tax cuts. Almost all new government policies are anti-economy and anti-growth.

The DOGE campaign is sucking massive amounts of money out of the economy. The yield curve has inverted, meaning that short-term interest rates are higher than long-term ones, indicating that the recession risk is real.

The dividend yield on the S&P 500 is at 1.2%. It was 2% only a couple of years ago. That is not much yield competition.

As I have been warning my Concierge members for weeks, get rid of all the stocks and asset classes you have been dating and only keep the ones you are married to. And what you keep should be hedged, such as through selling short call options against your longs, buying the (SDS), the 2X short S&P 500 ETF. And then there are 90-day US Treasury bills yield 4.2%, where nobody has ever lost money.

I learned something interesting the other day about your largest holding.

Some 70% of Nvidia is now held by indexes like the S&P 500. That’s because it has become an index proxy. It means that the shares have become an index hedge for hedge funds against which they can trade a myriad of options. This is why the (NVDA) options have implied volatilities four times those of the (SPY). It is a great arbitrage.

I watch closely the launch of new ETFs and write about the most interesting ones. I have been inundated by requests for private credit investments, which, by definition, are not available to the public.

The fund will launch with an initial $50 million, and the minimum investment is $100,000. The fund essentially offers daily liquidity for illiquid long-duration loans. The yield should be in line with private illiquid debt, or about 10%-12%.

How they pull this off is anybody’s guess. Past funds that tried to do this closed their doorsduring times of economic distress, known as “gating, “so beware of gating when market conditions turn less than ideal. The fund promises to hold up to 35% of its funds in private credit and the rest in a mix of junk bonds. No word yet on the yield, but it will be much higher than the leading junk bond fund (JNK), which is offering 6.48%.

February has started with a respectable +2.25% return so far. That takes us to a year-to-date profit of +9.46%so far in 2025. My trailing one-year return stands at a spectacular +81.87% as a bad trade a year ago fell off the one-year record. That takes my average annualized return to +49.83%and my performance since inception to +761.36%.

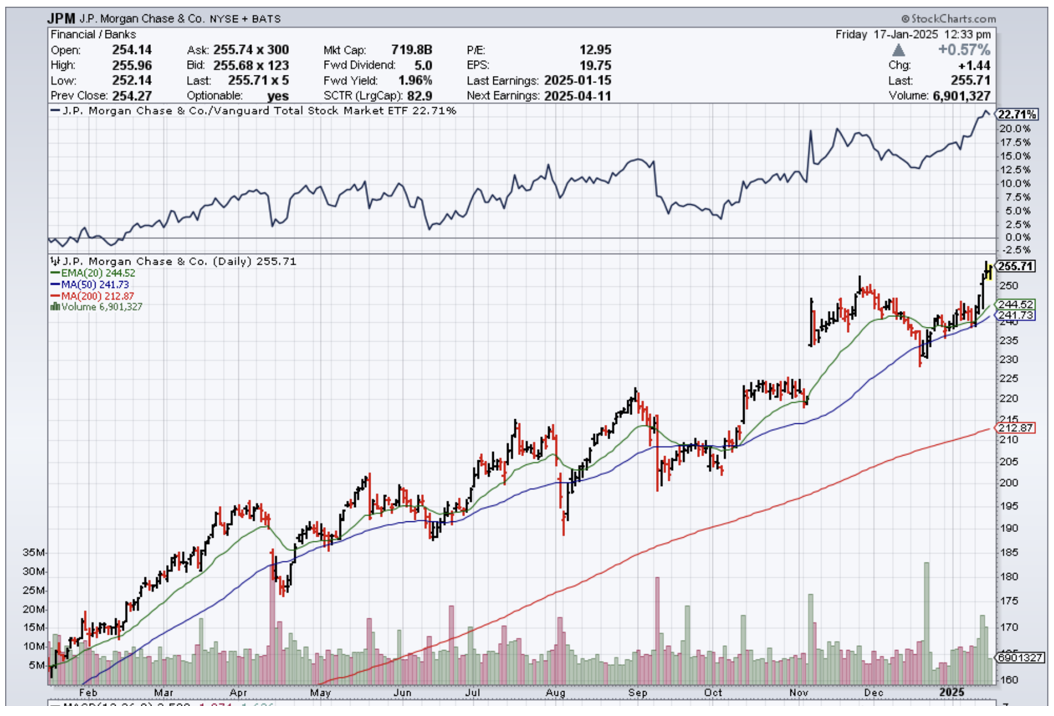

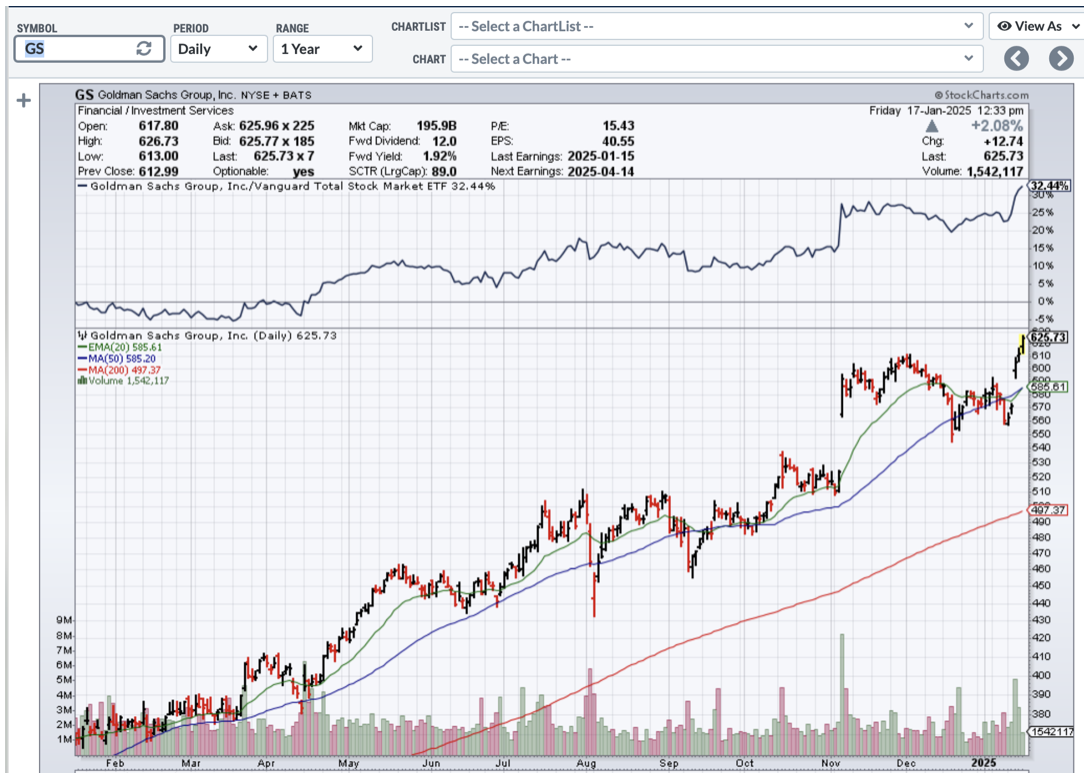

I saw the market breakdown coming a mile off and used my 90% cash to pile into new very short-term longs in JP Morgan (JPM), Interactive Brokers (IBKR), Tesla (TSLA), and Gold (GLD). I poured into new short positions with Tesla (TSLA), Nvidia (NVDA), and the United States US Treasury Bond Fund (TLT). This is in addition to an existing long in Goldman Sachs (GS). Last week, I leapt from 90% cash to 40% long, 40% short, and 20% cash.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades have been profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

Try beating that anywhere.

Core PCE Price Index Comes in Line. The personal consumption expenditures price index, the Federal Reserve’s preferred inflation measure, increased 0.3% for the month and showed a 2.5% annual rate. Excluding food and energy, core PCE also rose 0.3% for the month and was at 2.6% annually. Fed officials more closely follow the core measure as a better indicator of longer-term trends. Personal income posted rose 0.9% against expectations for a 0.4% increase. However, the higher incomes did not translate into spending, which decreased by 0.2%, versus the forecast for a 0.1% gain.

Retail Investors Market Sentiment Hit All-Time Bearish Highs. Options activity has also taken a big swing towards put buying. Dump all the stocks you were dating. Both Nvidia (NVDA) and Tesla (TSLA), the two most widely traded stocks in the market, broke their 200-day moving averages today. This is a very negative medium-term indicator. Only keep the ones you’re married to, not the ones you’re dating. This is not the rose garden we were promised.

US Margin Debt Hits All-Time High, at $937 billion as of January. That’s up 33% from $701 billion in January 2024. Over the same period, the S&P 500 gained 24.7%. Speculation on credit is running rampant. Margin trading, in which investors borrow funds from their brokerage firms in order to buy stocks, can amplify returns.

Weekly Jobless Claims Jump to 242,000, up 22,000, as the government firings kick in. In Washington, D.C., new claims totaled 2,047, an increase of 421, or 26%, the largest number for the city since March 25, 2023.

Nvidia Beats (NVDA) even the most optimistic expectations. The company forecasted higher first-quarter revenue, signaling continued strong demand for artificial intelligence chips, and said orders for its new Blackwell semiconductors were "amazing." The forecast helps allay doubts around a slowdown in spending on its hardware that emerged last month, following DeepSeek's claims that it had developed AI models rivaling Western counterparts at a fraction of their cost. Nvidia's outlook for gross margin in the current quarter was slightly lower than expected, though, as the company's Blackwell chip ramp-up weighs on Nvidia's profit. Nvidia forecast first-quarter gross margins will sink to 71%, below the 72.2% forecast by Wall Street, according to data compiled by LSEG.

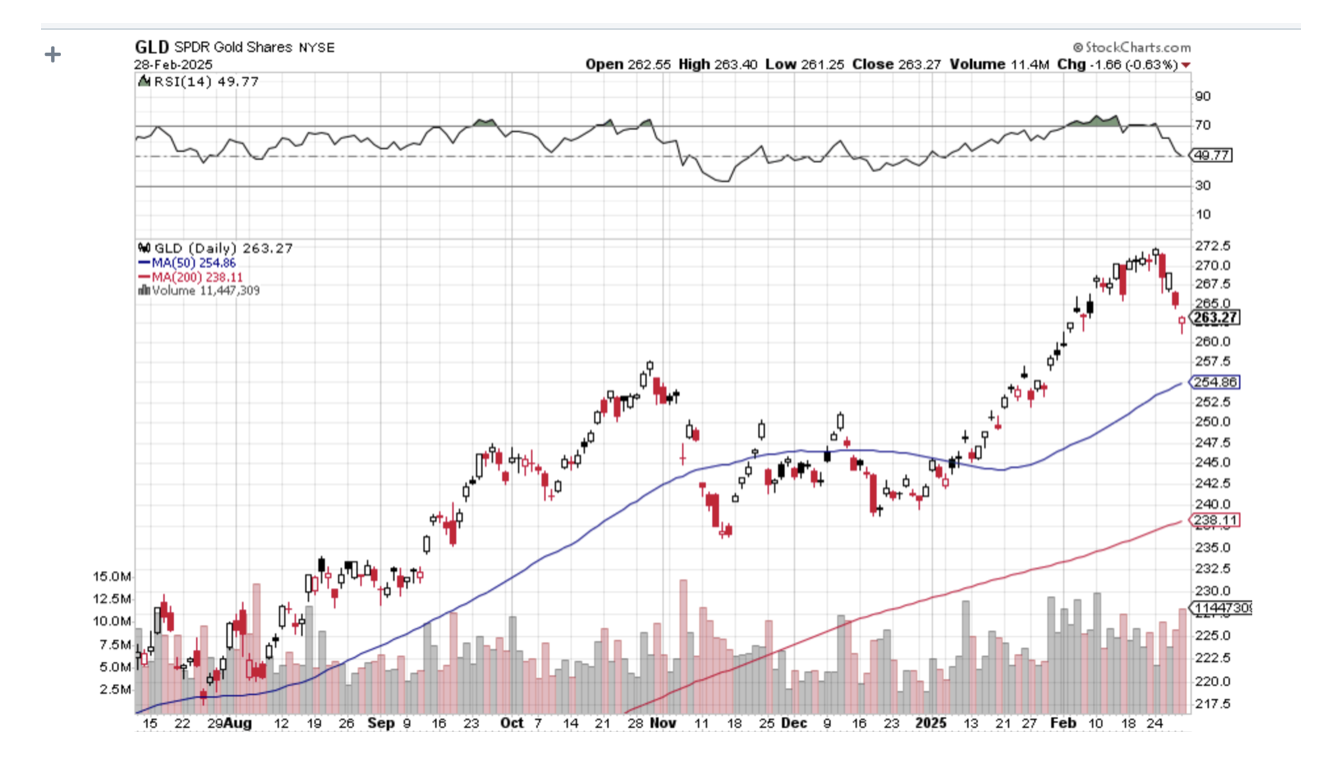

Gold ETFs (GLD) Have Become a Hot Commodity, with $4.5 billion pouring into (GLD) — with around half of that inflow occurring during Friday’s stock market selloff. The flight to safety bid is on. Those moves come as gold prices are at all-time highs in early 2025, boosted by trade uncertainty and inflation concerns. Buy (GLD) on dips.

Chinese Inflation (FXI) Hits 20-Year Lows, as the economy continues in free fall. Beijing is also expected to release its plans for spending on defense and technological development in the year ahead, along with details on private sector support. Last year, the inflation rate came in at only 0.2%.

Pending Homes Sales Hit All-Time Low, in January down 4.6% MOM and 5.2% YOY. Inventories are rising, but affordability is at record lows. Exceptionally cold weather was a factor. Homebuilder Sentiment plummeted to 42, a two-year low, and tariff concerns. Our drywall comes from Mexico, and our lumber comes from Canada. Avoid all real estate plays like the plague.

Home Prices are Still Rising, according to the S&P Case Shiller National Home Price Index. House prices rose 0.4%. They increased 4.7% in the 12 months through December. The strong increase in prices was despite rising housing supply, which is being driven by ebbing demand amid higher mortgage rates. New York showed the biggest gain at 7.2% YOY, followed by Chicago at 6.6% and Boston at 6.35%. Washington, DC, was the only city showing a loss at -1.1%.

Consumer Confidence Collapses to a Four-Year Low, down 7 points from 105 to 98, as tariff-driven inflation fears ramp up. The Conference Board’s Consumer Confidence Index for February, released Tuesday morning, fell to 98.3, falling for the third-straight month and marking the largest monthly decline since August 2021. Technology stocks sold off hard. Bonds are starting to discount a recession.

Berkshire Hathaway (BRK/B) Builds Record Cash, at $334 billion, up $9 billion in December alone. The Oracle of Omaha has been selling huge chunks of Apple (AAPL) and Bank of America (BAC) and putting the money into US Treasury Bills. Warren earned an eye-popping $47 billion in 2024, up 27% YOY. A price earnings multiple at a record 25X for the S&P 500. If Warren Buffet is selling, should you be buying?

Jamie Dimon Sells 30% of JP Morgan Stock, yet another indicator of a market top. Jamie is famous for loading up on (JPM) at the absolute market bottom in 2009. Does he know something we don’t? Banks have been the lead sector in the market since the summer.

Existing Homes Sales Crater, on a closing contract basis, down 4.9% in January to 4.09 million units. Terrible weather was a factor. Inventories are up 17% YOY and 3.5% for the month. Al cash sales hit 29%. The average price of a home is at an all-time high at $396,800, up 4.5% YOY.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at multiple gale force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

My Dow 240,000 target has been pushed back to 2035.

On Monday, March 3 at 8:30 AM EST, the ISM Manufacturing PMI is announced.

On Tuesday, March 4 at 8:30 AM, the API Crude Oil Stocks isreleased.

On Wednesday, March 5 at 8:30 AM, the ADP Employment Index is printed.

On Thursday, March 6 at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, March 7 at 8:30 AM, the Nonfarm Payroll Report for February is announced, as well as the headline Unemployment Rate. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I’ll never forget when my friend Don Kagin, one of the world’s top dealers in rare coins, walked into my gym one day and announced that he had made $1 million that morning.I enquired. “How is that, pray tell?”

He told me that he was an investor and technical consultant to a venture hoping to discover the long-lost USS Central America, which sunk in a storm off the Atlantic Coast in 1857, heavily laden with gold from the California gold fields. He just received an excited call that the wreck had been found in deep water off the US east coast.

I learned the other day that Don had scored another bonanza in the rare coins business. He had sold his 1787 Brasher Doubloon for $7.4 million. The price was slightly short of the $7.6 million that a 1933 American $20 gold eagle sold for in 2002.

The Brasher $15 doubloon has long been considered the rarest coin in the United States. Ephraim Brasher, a New York City neighbor of George Washington, was hired to mint the first dollar-denominated coins issued by the new republic.

Treasury Secretary Alexander Hamilton was so impressed with his work that he appointed Brasher as the official American assayer. The coin is now so famous that it is featured in a Raymond Chandler novel where the tough private detective, Phillip Marlowe, attempts to recover the stolen coin. The book was made into a 1947 movie, “The Brasher Doubloon,” starring George Montgomery.

This is not the first time that Don has had a profitable experience with this numismatic treasure. He originally bought it in 1989 for under $1 million and has made several round trips since then. The real mystery is who bought it last. Don wouldn’t say, only hinting that it was a big New York hedge fund manager who adores the barbarous relic. He hopes the coin will eventually be placed in a public museum.

Mad Hedge followers should start paying more attention to gold, which I believe just entered another decade-long bull market, thanks to falling US interest rates. You can’t go wrong buying LEAPS in the top two miners, Barrack Gold (GOLD) and Newmont Mining (NEM).

Who says the rich aren’t getting richer?

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2025/03/gold.png584622april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-03 09:02:412025-03-03 11:05:33The Market Outlook for the Week Ahead, or Armageddon

Below please find subscribers’ Q&A for the January 15 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Sarasota, Florida.

Q:What would I recommend right now for my top five stocks?

A: That’s easy. Goldman Sachs (GS), Morgan Stanley (MS), JP Morgan (JPM), Citibank (C), and Bank of America (BAC). There's five right there—the top five financials that are coming out of a decade-long undervaluation. A lot of the regional banks, which are also viable, are still trading to discount the book value, which all the financials used to trade out only a couple of years ago. Of course, JP Morgan's reaching a two-year return of around double, but the news just keeps getting better and better, so buy the dips. Buy every sell-off in financials and you will be a happy camper for the year.

Q: What do you think about Robin Hood (HOOD)?

A: Well, the trouble with Robinhood is it’s very highly dependent on crypto volumes. If you think crypto is going to go higher and volumes will increase, this is a great play. However, you get another 95%, out-of-the-blue selloff in crypto like we had three years ago and Coinbase (COIN) will follow it right back down again. On the last downturn, there were concerns that Coinbase would go under, so if you can hack the volatility, take a shot, but not with my money. I have the largest banks in the country that are about to double again; I would much rather be buying LEAPS in that area and getting anywhere from 100% to 1000% percent returns on a 2-year view—much more attractive risk-reward for me. And they pay a dividend.

Q: How do you define a 5% correction?

A: Well, if you have a $100 stock and it drops $5, that is a 5% correction.

Q: Can you please explain what Tesla 2X leverage actually means and is it a way to trade Tesla as an alternative?

A: I steer people away from the 2Xs because the tracking error is really quite poor. You only get 1.5% of the upside, but 2.5 times the downside over time. These are more day trading vehicles. They take out huge fees, and huge dealing spreads—it's a very expensive way to trade. Far cheaper is just to buy Tesla (TSLA) stock on margin at 2 to 1, and there your tracking error is perfect, your fees are much lower, and you just have the margin interest rate to pay on the position, which is 6% a year or 50 basis points a month. No reason to make the ETF people richer than they already are. They keep coining these products—1x, 2x, 3x long shorts on every one of the high volume stocks, and it sucks a lot of people in, but it's higher risk, lower returns for the amount of money you're risking as far as I'm concerned. So that's the way to do it.

Q: What are your projections for Nvidia (NVDA)?

A: I think not just Nvidia, but all of the big tech is going to be kind of trading in a sideways range for a while, maybe 6 months, and then we get an upside breakout if you get the earnings breakout, which we are all expecting. AI is still in business, and still growing gangbusters. There are always a lot of Cassandra's out there saying that we're going to crash anytime, and I just don't see it. I know a lot of these people, I'm in touch with a lot of the companies, I see Beta releases of all products, the consumer products, and…the slowdown just ain't happening, I'm sorry. And I've been through a lot of these tech booms over the last 40 years, and this is only showing signs of just getting started.

Q: How come Tesla (TSLA) is up and down $30 every couple of days?

A: Number one, it is the most actively traded stock in the market right now. It has implied volatility on the options of 70%, which is really the highest in the market of any individual stock. That just creates immense amounts of trading by options traders, volatility traders, by call writing, and 2x and 3x ETF long and short players. All of the financial engineering and new products that we see all gravitate toward the high volume stocks like Nvidia, Tesla, and Apple because that's where the money is being made. Some days Tesla accounts for 25% of all the market trading. Financial engineers go where the action is, where the volume is, where the customer demand is.

Q: Why do you expect only 5% to 10% corrections if the Fed rate cuts get completely priced out?

A: I don't expect the Fed to keep cutting interest rates. We should get another rate cut this year, and that may be it for the year. If inflation comes back (and of course, all of the new administration’s policies are highly inflationary) it’s just a question of how long it takes for it to hit the system.

Q: Do you believe I should hold all of my municipal bonds (MUB) with 10-year call protection at 4.75%?

A: On a tax-adjusted basis, I would say yes. You know, stock markets may peak and deliver a zero return, and in that situation, muni bonds are very attractive. The nice thing about bonds is that you hold on to maturity—you get 100% of your money back. With stocks, that is not always the case. Stocks you have to trade because the volatility can be tremendous. And in fact, what I do is I keep all of my money in one year Treasury bills. Last time I did this, which was in September, I locked in a one-year return for 5%.

Q: Would you prefer to buy deep in the money and put spreads on top of any rally?

A: Absolutely yes. If this is a real trading year, you not only buy the dips, you sell the rallies. We did almost no real selling last year. We really only did it in June and July because the market essentially went straight up, except for two hickeys. This could be the year of not only call sprints but put spreads as well. You just have to remember to sit down when the music stops playing.

Q: You say buy the dips; what would your dip be in JP Morgan (JPM)?

A: Well lower volatility stocks by definition have smaller drawdowns. JP Morgan (JPM) is one of those, so I'd be very happy to buy a 5% dip in JP Morgan. If it drops more, you double the position on a 10% pullback. Higher volatility stocks like Tesla—I'm really waiting for 10% or 20% corrections. You saw I just bought a 22% correction twice in Tesla with it down 110 points. One of those trades is at max profit right now and the other one has probably made half its money since yesterday. That is the game. The amount of dip you buy is directly related to the volatility of the stock.

Q: Should you let your cash go uninvested?

A: Yes, never let your cash go uninvested just sitting as cash. Your broker will take that money and put it in 90-day T-bills and keep the money for himself. So buy 90-day T-bills as a cash management tool—they're paying about 4.21% right now— and you can always use those as collateral under my positions on margin.

Q: Is Home Depot (HD) a buy on the LA reconstruction story?

A: I would say no, Los Angeles is probably no more than 5% of Home Depot's business—the same with Lowe's (LOW). A single city disaster is not enough to move the stock for more than a few days, and the fact is: Home Depot is mostly dependent on home renovation, which tends not to happen during dead real estate markets because, you know, it takes the flippers out of the market. It really needs lower interest rates to get Home Depot back up to new highs.

Q: Do you expect a big market move at the end of the day when the Fed makes its announcement?

A: The market has basically fully discounted the move on January 28, and if anything happens, there'll probably be a “sell on the news.” So, I expect we could give up a piece of the recent performance on the announcement of the Fed news.

Q: Should we expect trade alerts for LEAPS coming from you?

A: Absolutely, yes. However, LEAPS are something you really only want to do on down moves. If we don't get any, we'll just do the front-month call spreads. You can still make 10%, 20% a month just concentrating on financial call spreads.

Q: What would have happened to our accounts if we kept the (TLT) $82-$85 iShares 20+ Year Treasury Bond ETF (TLT) call spread and it went all the way down to $82?

A: The value of your investment goes to zero. Of course, it was declining at a very slow rate, and the $80: you might have gotten a bounce off the $85 level. But if the inflation number had come in hot, as had all other economic data of the last month, then you could have easily gotten a gap down to $82 and lost your entire investment, because two days is not enough time to expiration to recover that 3-point loss. And that's why I stopped out yesterday.

Q: Didn't David Tepper buy China (FXI)?

A: With both hands last September, yes he did. And my bet is he got out before he got killed. I mean, that's what hedge funds do. He probably got out close to cost, and you likely won't see him promoting China again anytime in the near future.

Q: I have June 530 puts on the S&P 500, should I get rid of them?

A: Yes, I don't see a big crash coming. You probably paid a lot going all the way out to June, and it's probably not worth hanging on to. Put spreads are the better way to go—that cuts your cost by two-thirds and those you only want to put on at market tops.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There was so much enthusiasm for China only a month ago.

A stimulus package was announced, a massive short-covering rally ensured, and finally, after a three-year hiatus, China was back in play. Several hedge funds announced major commitments to the Middle Kingdom.

Here we are only three weeks after the US presidential election, and China now looks so much rubble. Asst prices returned to their starting points. The hedge funds have so much mud on their faces. It’s back to a long wait.

Which gives us all plenty of time to think about what China is really all about.

I ran into Minxin Pei, a scholar at the Carnegie Endowment for International Peace, who imparted to me some iconoclastic, out-of-consensus views on China’s position in the world today.

He thinks that power is not shifting from West to East; Asia is just lifting itself off the mat, with per capita GDP at $12,969, compared to $81,695 in the US.

We are simply moving from a unipolar to a multipolar world. China is not going to dominate the world, or even Asia, where there is a long history of regional rivalries and wars.

China can’t even control China, where recessions lead to revolutions, and 30% of the country, Tibet and the Uighurs want to secede.

China’s military is almost entirely devoted to controlling its own people, which makes US concerns about their recent military build-up laughable.

All of Asia’s progress, to date, has been built on selling to the US market. Take us out, and they’re nowhere.

With enormous resource, environmental, and demographic challenges constraining growth, Asia is not replacing the US anytime soon.

There is no miracle form of Asian capitalism; impoverished, younger populations are simply forced to save more because there is no social safety net.

Try filing a Chinese individual tax return, where a maximum rate of 40% kicks in at an income of $35,000 a year, with no deductions, and there is no social security or Medicare in return.

Ever heard of a Chinese unemployment office or jobs program?

Nor are benevolent dictatorships the answer, with the despots in Burma, Cambodia, North Korea, and Laos thoroughly trashing their countries.

The press often touts the 600,000 engineers that China graduates, joined by 350,000 in India. In fact, 90% of these are only educated to a trade school standard. Asia has just one world-class school, the University of Tokyo.

As much as we Americans despise ourselves and wallow in our failures, Asians see us as a bright, shining example for the world.

After all, it was our open trade policies and innovation that lifted them out of poverty and destitution. Walk the streets of China, as I have done for four decades, and you feel this vibrating from everything around you.

I’ll consider what Minxin Pei said next time I contemplate going back into the (FXI) and (EEM).

China: Not All Its Cracked Up to Be

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/China-Parade.jpg266401Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-11-29 09:02:432024-11-29 11:36:58China's View of China

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GOLDILOCKS ON STEROIDS, plus A KERFFUFLE IN PARIS),

(SPY), (FXI), ($COMPQ), (CCJ), (SLB), (OXY), (TSLA),

(TLT), (DHI), (NEM), (GLD), (TSLA)

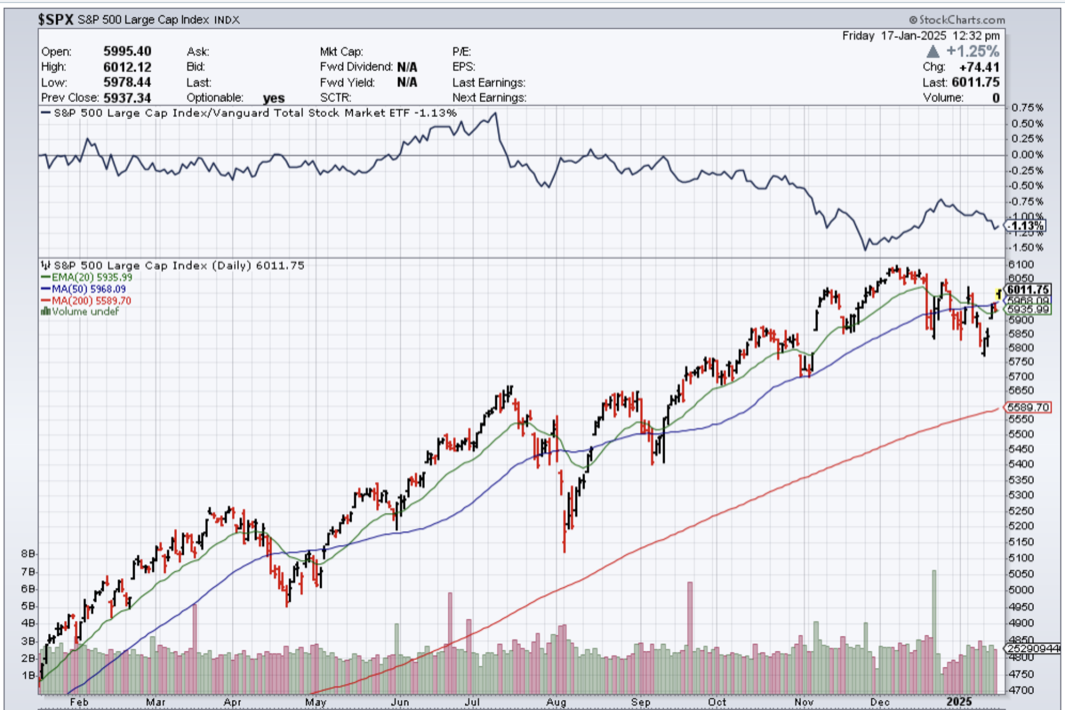

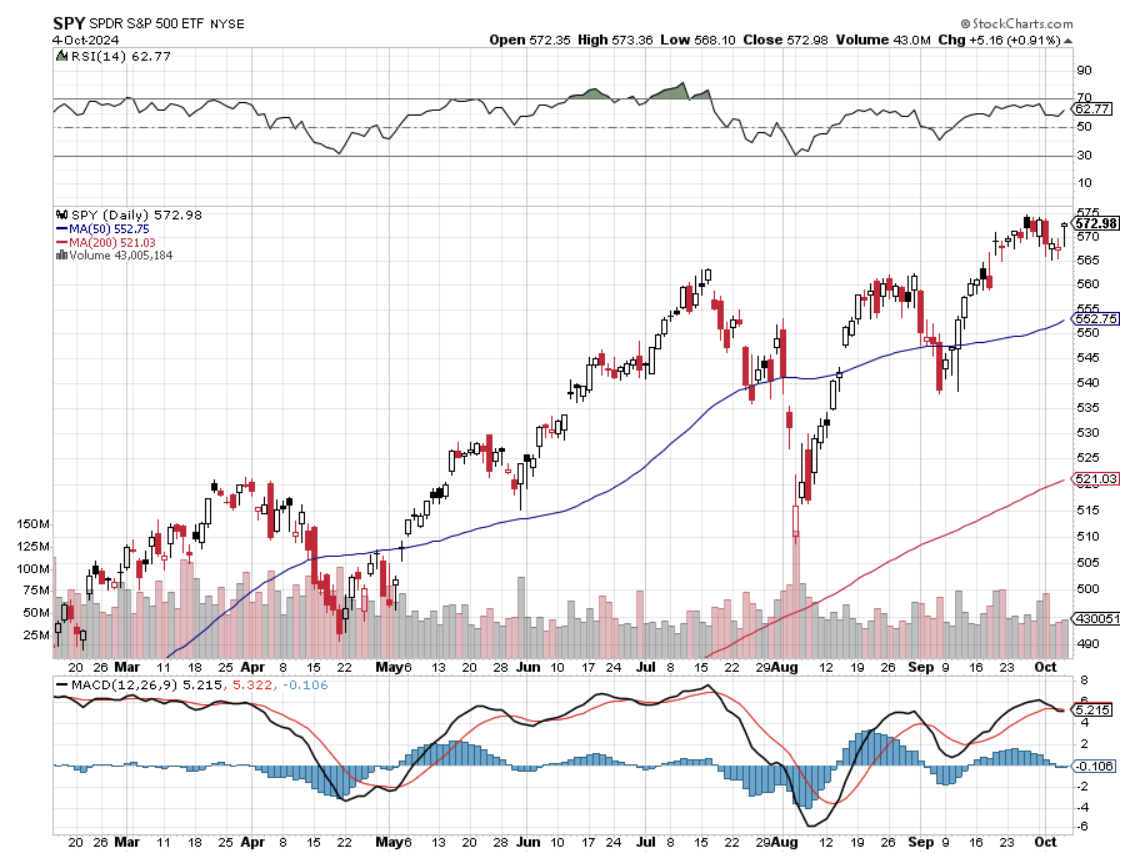

The 6,000 targets for the S&P 500 are starting to go mainstream.

That was my forecast on January 1, back when everyone said I was nuts. The inflation rate is 2.2%, GDP growth is 3.0%, and interest rates are falling sharply, on their way to 3.0% by next summer.

Goldilocks is back, but this time she’s on steroids.

Also helping is that we are in the midst of a global interest rate decline. The US, Europe, China, and Australia are all cutting interest rates at the same time. Japan is the sole exception, which is on the verge of raising rates from 0.25%. All of this has a compounding effect on the health of the global economy.

Long-term market veterans like myself are amazed, astounded, and astonished that here we are on October 7, and instead of testing new lows for the year, we are punching through to new all-time highs. It’s proof that if you live long enough, you see everything.

Some five seconds after Jay Powell cut interest rates by a shocking 0.50%, everyone in the world suddenly realized they had way too much cash and not enough stocks. This is the kind of market you get from that realization, one that doesn’t breathe, take a break, have a correction, nor let in outsiders.

Further confusing matters is that we are witnessing the most contentious presidential elections in history. One party is proclaiming how great the US economy is, while the other is claiming it is the worst ever.

Those who believed the former description are having a great year. Those who bought the latter are having an awful one, with many owning no stocks at all. Fortunately, election concerns will disappear in four weeks not to return for four years. This is hugely positive for stocks.

But as all steroid users eventually find out, they cause impotence, sterility, and cancer, so enjoy while it lasts. That may be a mid-2025 or 2026 event.

China (FXI) came back with a vengeance. A 25% rise in a stock market in a week is not to be taken lightly, although a lot of this was short covering. Pouring gasoline on the fire is a government promise to buy $1 billion worth of stocks.

The question bedeviling all investors is whether China is a one-hit wonder or is it reborn again. I know that if this stimulus package doesn’t work, they have the resources to follow up with many more. But there is a bigger problem.

Chinese stock markets have not exactly done well since Xi Jinping came into power in 2013. In fact, they are exactly unchanged. During the same period, the (SPY) was up 308%, and the NASDAQ ($COMPQ) was up 525%. Many investors, like my old friend hedge fund legend Paul Tudor Jones, don’t want to touch China until Xi vacates the scene.

In any case, if you want to play China, the best risk-adjusted plays are not there but here in the US. Any US blue chip oil play (OXY) (SLB) would be a great choice, as China is the world’s largest oil consumer. Oil happens to be the cheapest and worst-performing sector in the stock market. And you don’t have to worry about a CEO getting rolled up in a carpet and disappearing for a few years, as has happened in the Middle Kingdom. At least here, you get all the US investor protections.

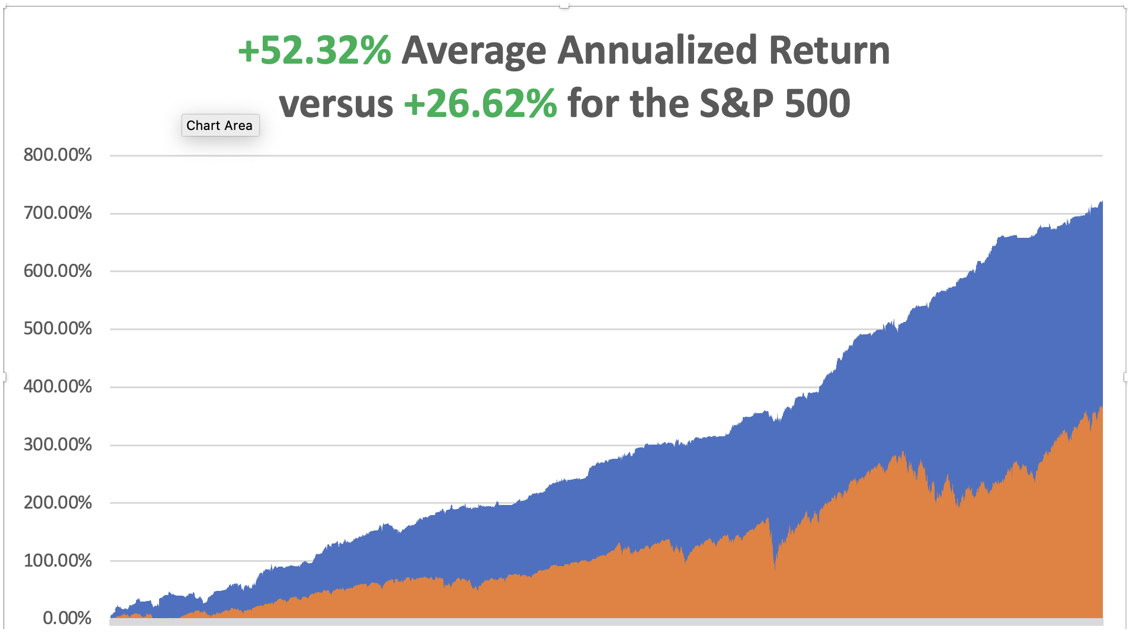

We closed out September with a blockbuster +10.28% profit. My 2024 year-to-date performance is at +44.97%.The S&P 500 (SPY) is up +19.92%so far in 2024. My trailing one-year return reached a nosebleed +62.77. That brings my 16-year total return to +721.60.My average annualized return has recovered to +52.32%.

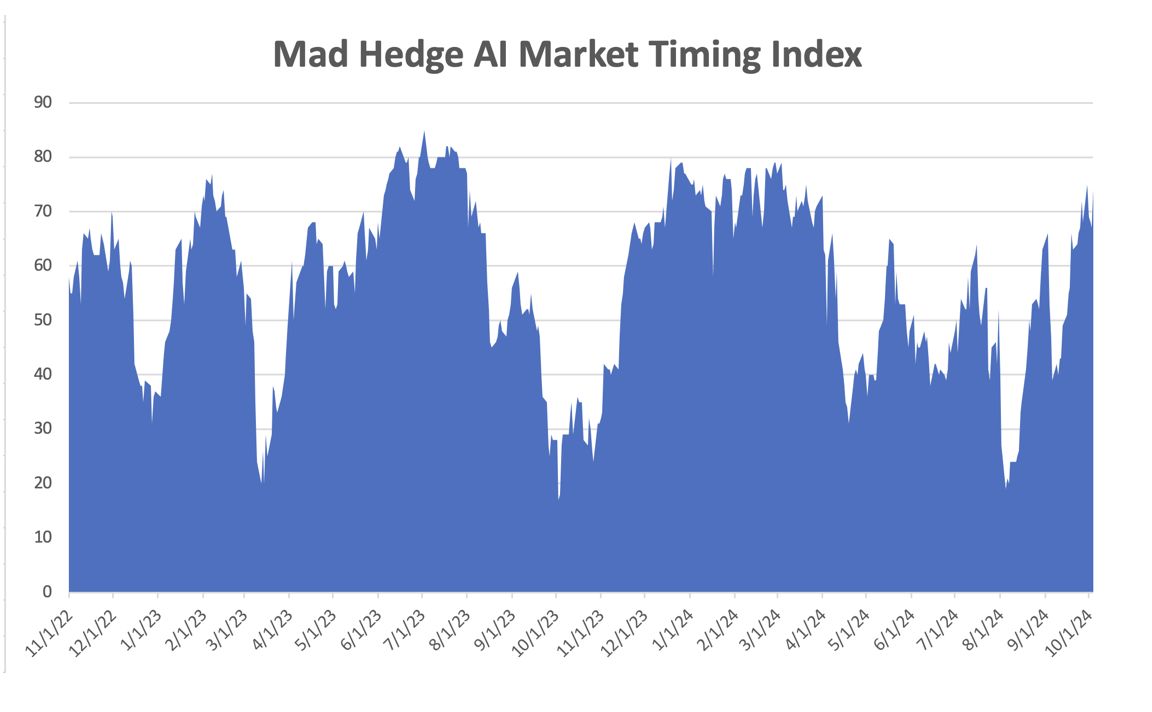

With my Mad Hedge Market Timing Index at the 70 handles for the first time in five months, it was a good week to take profits. I sold longs in (CCJ) and (TSLA) and covered a short in (TLT). I stopped out of my long in (TLT) because of the blowout September Nonfarm Payroll Report on Friday.

This is what we’ve got left:

Risk On

(NEM) 10/$47-$50 call spread 10.00%

(TSLA) 10/$200-$210 call spread 10.00%

(DHI) 10/$165-$175 call spread 10.00%

Risk Off

NO POSITIONS 0.00%

Total Net Position 30.00%

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 58 of 77 trades have been profitable so far in 2024, and several of those losses were really break evens. Some 16 out of the last 17 trade alerts were profitable. That is a success rate of +75.32%.

Try beating that anywhere.

September was Great, butOctober is Looking Tough, right on the doorstep of the November 5 election and the market waiting for another interest rate cut on November 6. I think I’ll run out the positions I have into the October 18 options expirations, then wait for the market to come to me. I am up too much this year to take on needless risk.

Nonfarm Payroll Report Comes in Hot, as US employers added 254,000 jobs in September, topping economists’ estimates. The payroll gain, the biggest advance since March, was led by leisure and health care. The headline Unemployment Rate fell to a three-month low of 4.1%.

Interactive Brokers Starts US Election Forecast Trading on the heels of a federal court ruling in their favor. The following Forecast Contracts on US election results will be available:

*Will Kamala Harris win the US Presidential Election in 2024?

*Will Donald Trump win the US Presidential Election in 2024?

Plus a dozen other election outcomes. The opening bids were 49% for Harris and 50% for Trump. The port Strike is Settled with a 62% six-year settlement. The bananas were rotting. 54 container ships queued outside ports, risking shortages. The Strike cost the U.S. economy $5 billion/day. Shipping stocks tumble across Asia and Europe. Expect the US to move to full automation, where Europe went 30 years ago. EC Imposes 45% Tariffs on Chinese EVs in a desperate bid to save the local car industry. The Commission, which oversees the bloc's trade policy, has said it would counter what it sees as unfair Chinese subsidies after a year-long anti-subsidy investigation, but it also said on Friday it would continue talks with Beijing. Expect the same to follow in the US.

A possible compromise could be to set minimum sales prices. Hedge Funds Stampede into China on news that government agencies promised to pour $1 billion into local stock markets. Chinese equities saw the largest net buying ever from hedge funds last week, marking the most powerful weekly purchase on record, according to Goldman Sachs prime brokerage data.

Weekly Jobless Claims Climb to 225,000, not straying too far from a four-month low touched in the prior week. That is an increase from an upwardly-revised mark of 219,000 last week, data from the Labor Department showed on Thursday. Economists had anticipated 222,000. Will This Crisis Take Gold to $3,000? Almost certainly, yes, given the way the barbarous relic traded yesterday. Buy all gold (GLD), plays on dips, the metal, ETFs, futures, and miners. Tesla Bombs, with Q3 deliveries down flat, but the shares fell only 5%. Total deliveries came in at 462,890, while total production was 469,796. YOY Tesla is facing increased competitive pressure, especially in China, from companies like BYD and Geely, along with a new generation of automakers, including Li Auto and Nio. US Car Makers Get Slaughtered, with Stellantis stock falling by double digits after the Jeep maker cut its 2024 financial guidance, citing deteriorating industry dynamics and Chinese competition. The warning, amid similarly negative news from other car makers, also dragged down shares of (F) and (GM). Avoid the auto industry except for (TSLA). Nvidia Still has more to Run, so says Samantha McLemore, the founder and Chief Investment Officer of Patient Capital Management. Nvidia has been crushing every quarter for a year. CEOs want to make the decision to invest more [in AI] rather than getting caught behind. She doesn’t see the bull market ending soon. Current operating profit margins are 65%. Buy (NVDA) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy is decarbonizing, and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 7 at 8:30 AM EST, Used Car Prices are out On Tuesday, October 8 at 6:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, October 9 at 11:00 PM, the Fed Minutes from the last meetingis printed.

On Thursday, October 10 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Consumer Price Index.

On Friday, October 11 at 8:30 AM EST, the Producer Price Index and the University of Michigan Consumer Price Index are announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

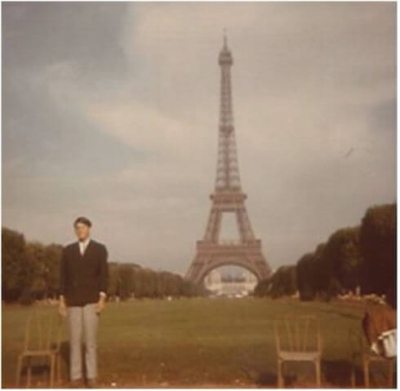

As for me, dentists find my mouth fascinating as it is like a tour of the world. I have gold inlays from Japan, cheap ceramic fillings from Britain’s National Health, and loads of American silver amalgam, which are now going out of style because of their mercury content.

But my front teeth are the most interesting as they were knocked out in a riot in Paris in 1968.

France was on fire that year. Riots on the city’s South Bank near Sorbonne University were a daily occurrence. A dozen blue police buses packed with riot police were permanently parked in front of the Notre Dame Cathedral, ready for a rapid response across the river. They did not pull their punches.

President Charles de Gaulle was in hiding at a French air base in Germany. Many compared the chaos to the modern-day equivalent of the French Revolution.

So, of course, I had to go.

This was back when there were five French francs to the US dollar, and you could live on a loaf of bread, a hunk of cheese, and a bottle of wine for a dollar a day. I was 16 years old.

The Paris Metro cost one franc. To save money, I camped out every night in the Parc des Buttes Chaumont, which had nice bridges to sleep under. When it rained, I visited the Louvre, taking advantage of my free student access. I got to know every corner. The French are great at castles….and museums.

To wash, I would jump in the Seine River every once in a while. But in those days, not many people in France took baths anyway.

I joined a massive protest one night, which originally began over the right of men to visit the women’s dorms at night. Then the police attacked. Demonstrators came equipped with crowbars and shovels to dig up heavy cobblestones dating to the 17th century to throw at the police, who then threw them back.

I got hit squarely in the mouth with an airborne projectile. My front teeth went flying, and I never found them. I managed to get temporary crowns, which lasted me until I got home. I carry a scar across my mouth to this day.

I visited the Left Bank again just before the pandemic hit in 2019. The streets were all paved with asphalt to make the cobblestones underneath inaccessible. I showed my kids the bridges I used to sleep under, but they were unimpressed.

But when I showed them the Mona Lisa at the Louvre, she was as enigmatic as ever. The kids couldn’t understand what the fuss was all about.

Everyone should have at least one Paris in 1968 in their lifetime. I’ve had many and am richer for it.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

1968 in Paris

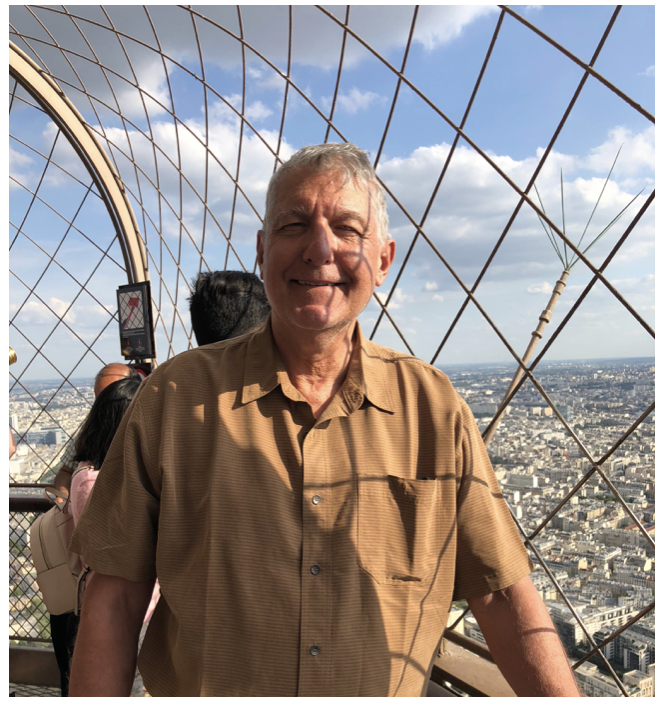

2019 in Paris on Top of the Eiffel Tower

https://www.madhedgefundtrader.com/wp-content/uploads/2024/10/John-thomas-in-Paris.png706658april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-07 09:02:262024-10-07 10:26:01The Market Outlook for the Week Ahead, or Goldilocks on Steroids

Global Market Comments

September 30, 2024 Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or CHINA IS BACK! plus MY ENCOUNTER WITH ALIENS),

(GLD), (CCJ), (NEM), (TSLA), TLT), (DHI), (FXI), (BIDU), (TNE)

(USO), (BTU), (UNG), (CORN), (WEAT), (SOYB), (LVS), (WYNN) (LVUY) (HESAF)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.