If demographics is destiny, then America’s future looks bleak. You see, they’re not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”.When the numbers of the middle-aged big spenders are falling, risk markets plunge. Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

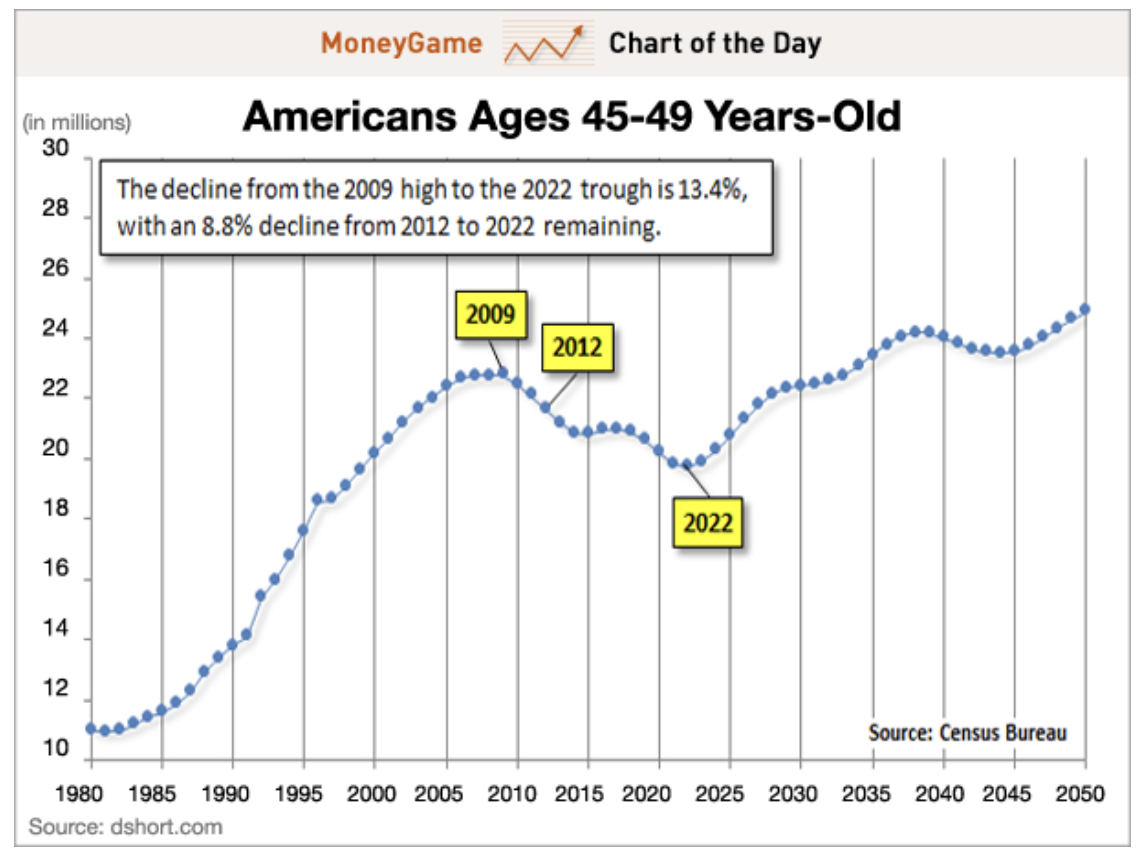

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth.That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, they also back-test with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country and you can develop a highly reliable timetable for when and where to invest.

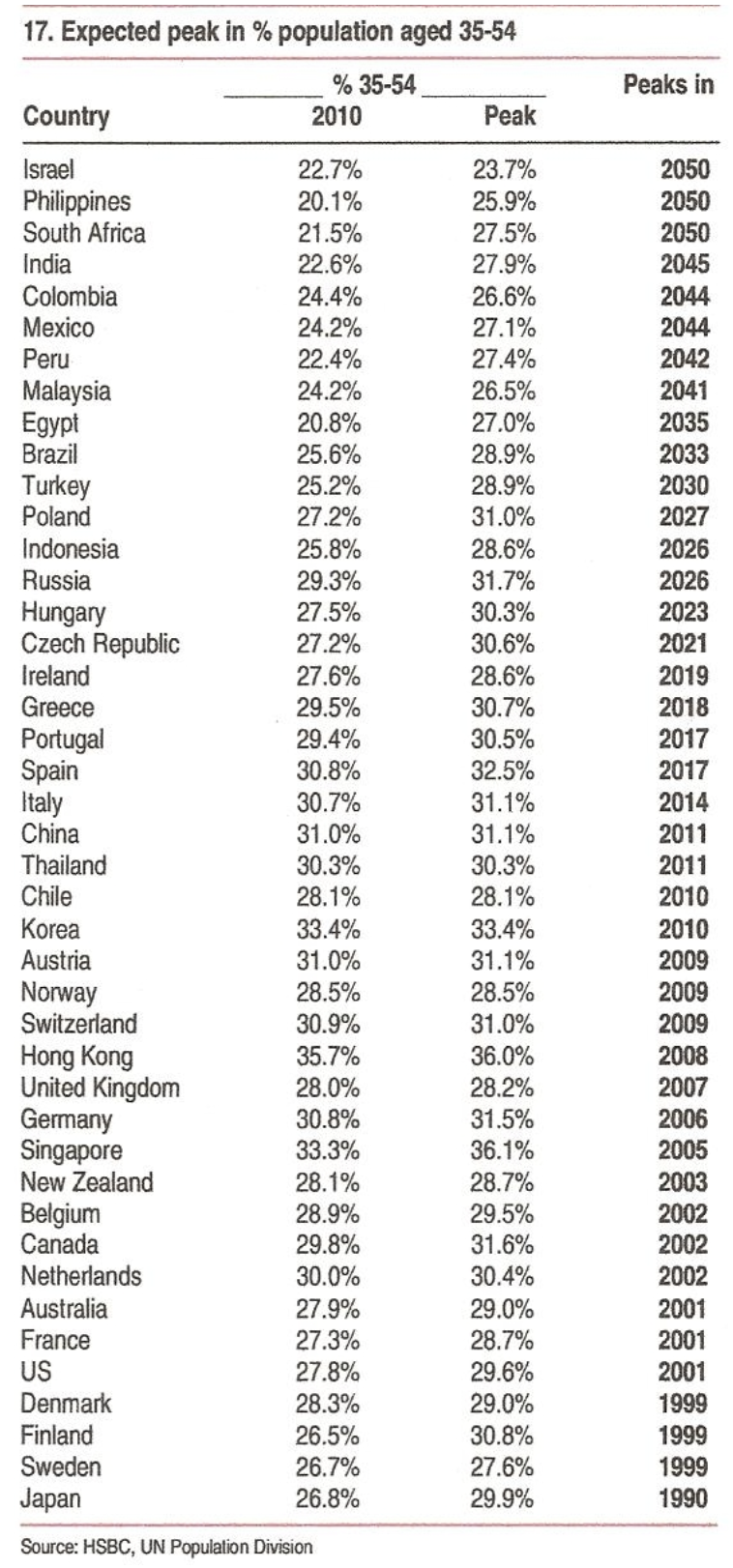

Instead of pouring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice backtest.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2000s and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle age not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan) while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

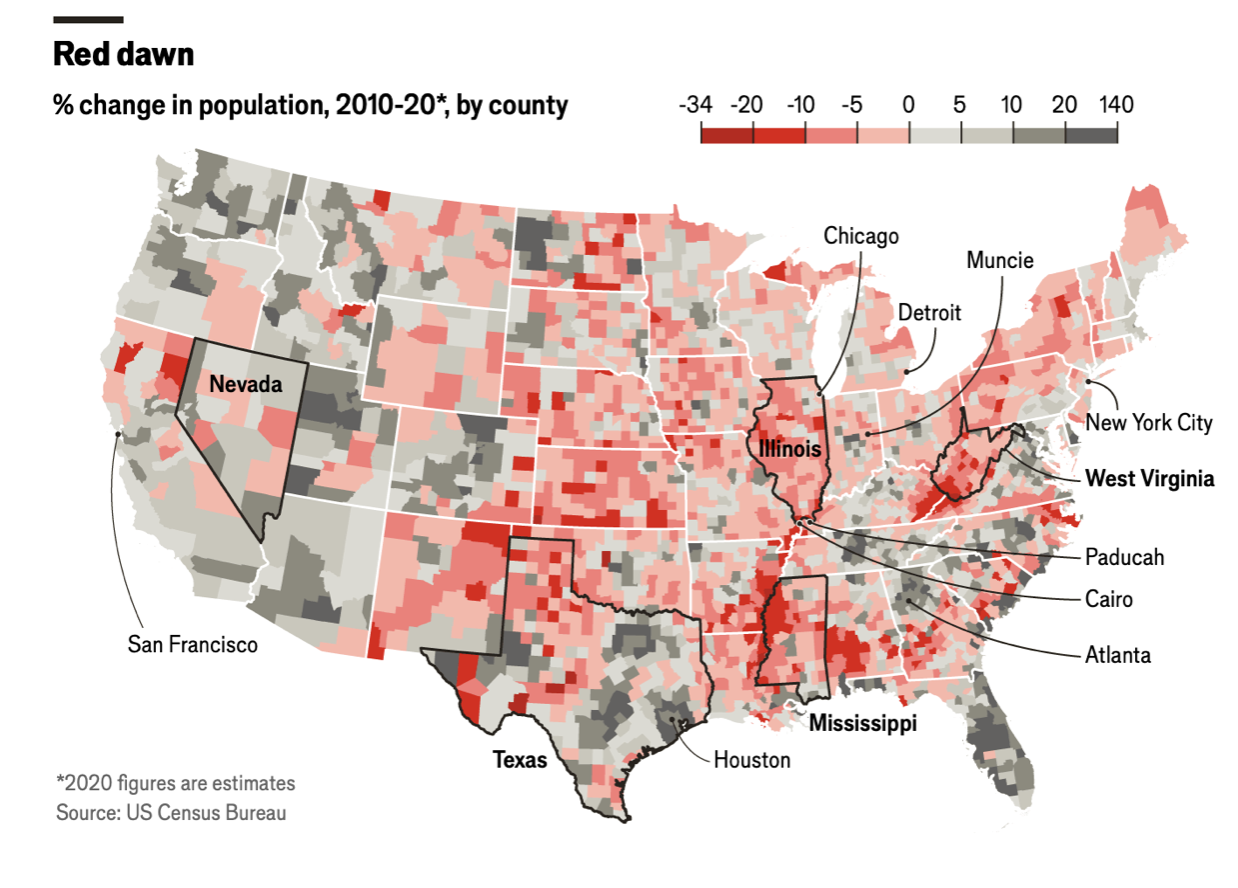

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills picking up speed, the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

https://www.madhedgefundtrader.com/wp-content/uploads/2022/04/manischewitz.png370364april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-24 09:02:502024-04-24 10:12:59They’re Not Making Americans Anymore

(MARKET OUTLOOK FOR THE WEEK AHEAD, or VOLATILITY IS BACK!)

(REMEMBERING TRINITY)

(TLT), (TSLA), (NVDA), (FCX),

(XOM), (WPM), (GLD), (FXI), (FXY), (USO), (GOOGL)

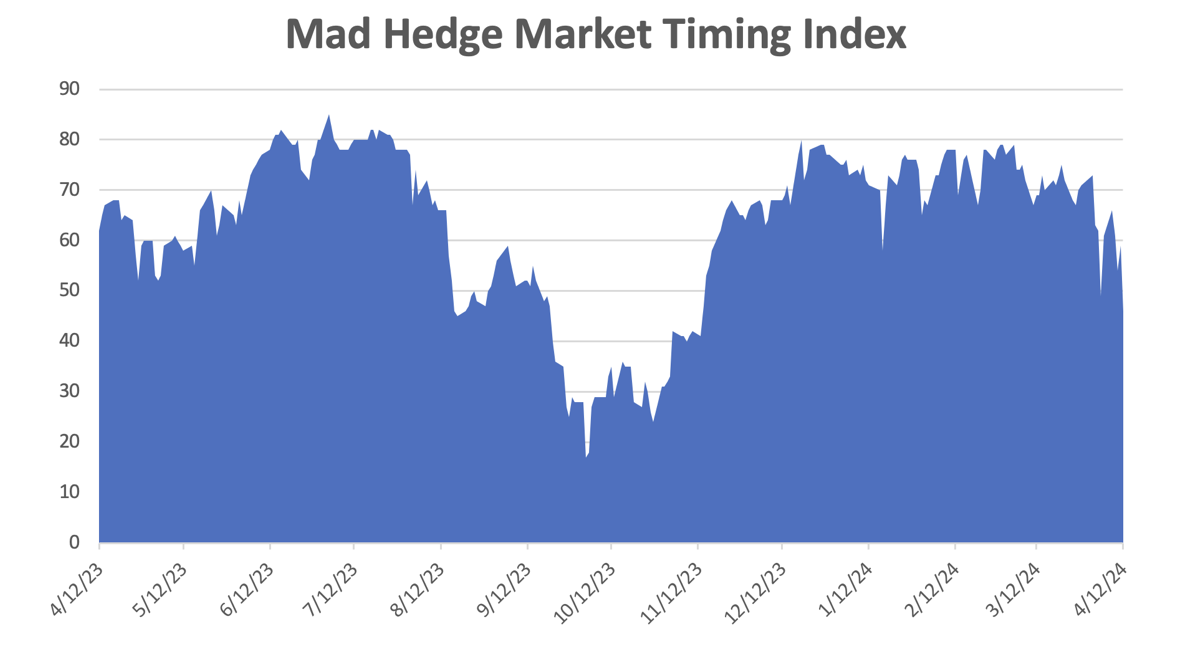

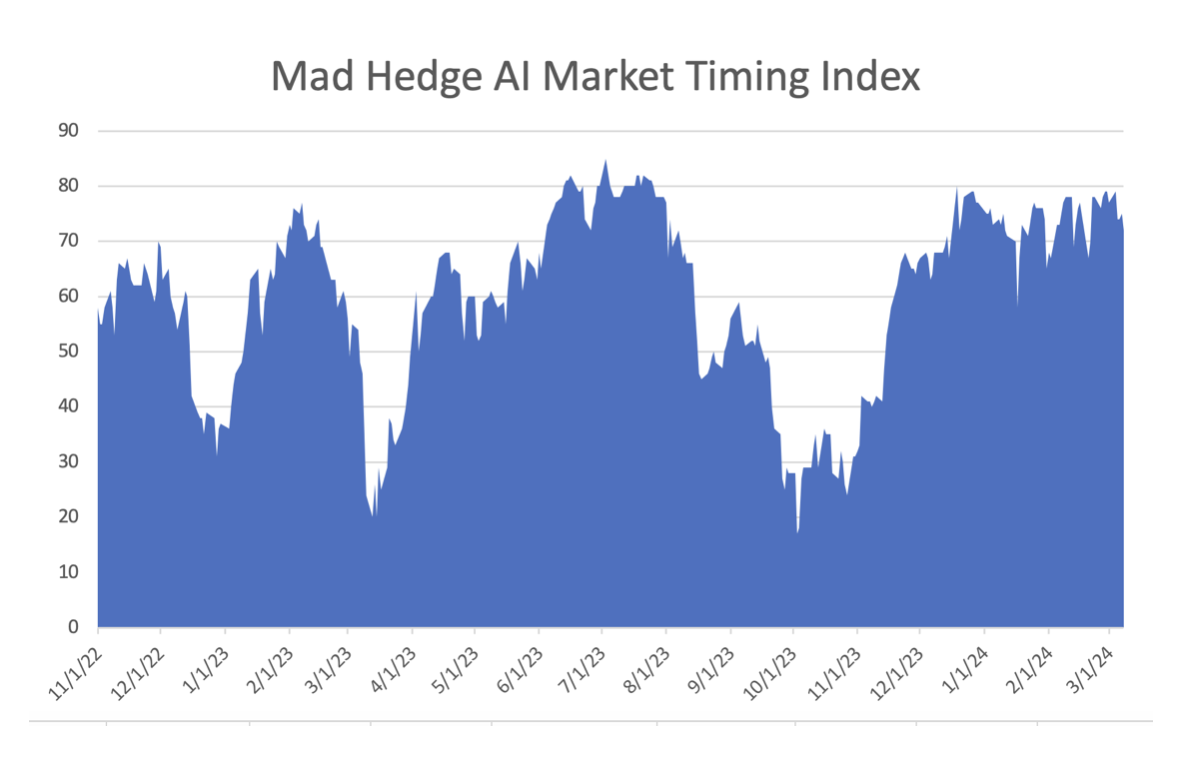

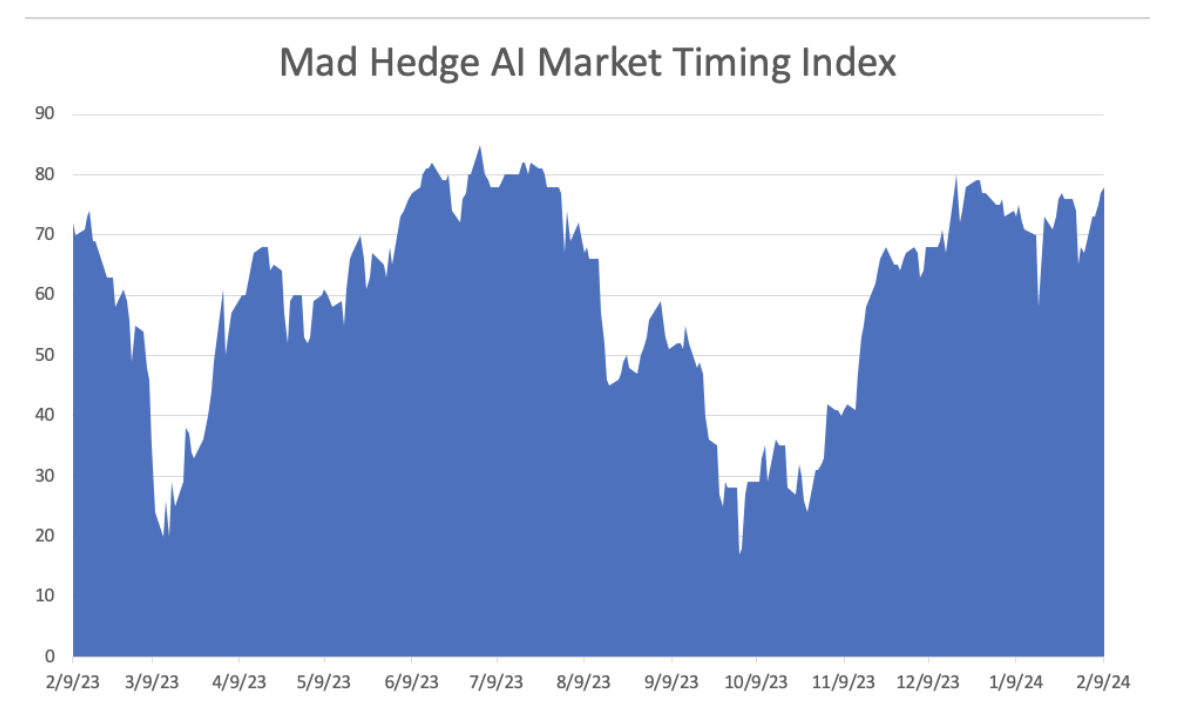

Those who expected markets to go up forever were given a rude awakening last week with a swift slap across the face with a wet kipper. The Volatility Index ($VIX) soared from $12 to $19 and higher highs will unfold this week. The Mad Hedge Market Timing Index dropped below 50 for the first time since October and lower lows beckon.

For those of us who earn our crust of bread off of volatility, its return is like a gift from the gods. The long desert has been crossed and the fresh mountain springs beckon just ahead.

What prompted this ($VIX) melt-up is that many traders and investors are finally throwing in the towel on ANY interest rate cuts in 2024. In a mere four months, we have gone from an expectation of six rate cuts to zero. Not helping matters is that the “May” thing, as in “Sell and Go away” is only two weeks away. After an overcooked Q1, we may be headed into a summer that is the next great Ice Age.

At least that is the assumption we have to make from a trading point of view for the short-term. While this represents a worst-case scenario, I don’t expect bonds to drop much from here, maybe a couple of points, as future interest rate cuts are a certainty. All that has happened is that our rate cuts have been moved out from two months to five months. The next move in interest rates is still down.

At some point, there will be a great bond trade out there, but definitely, not yet!

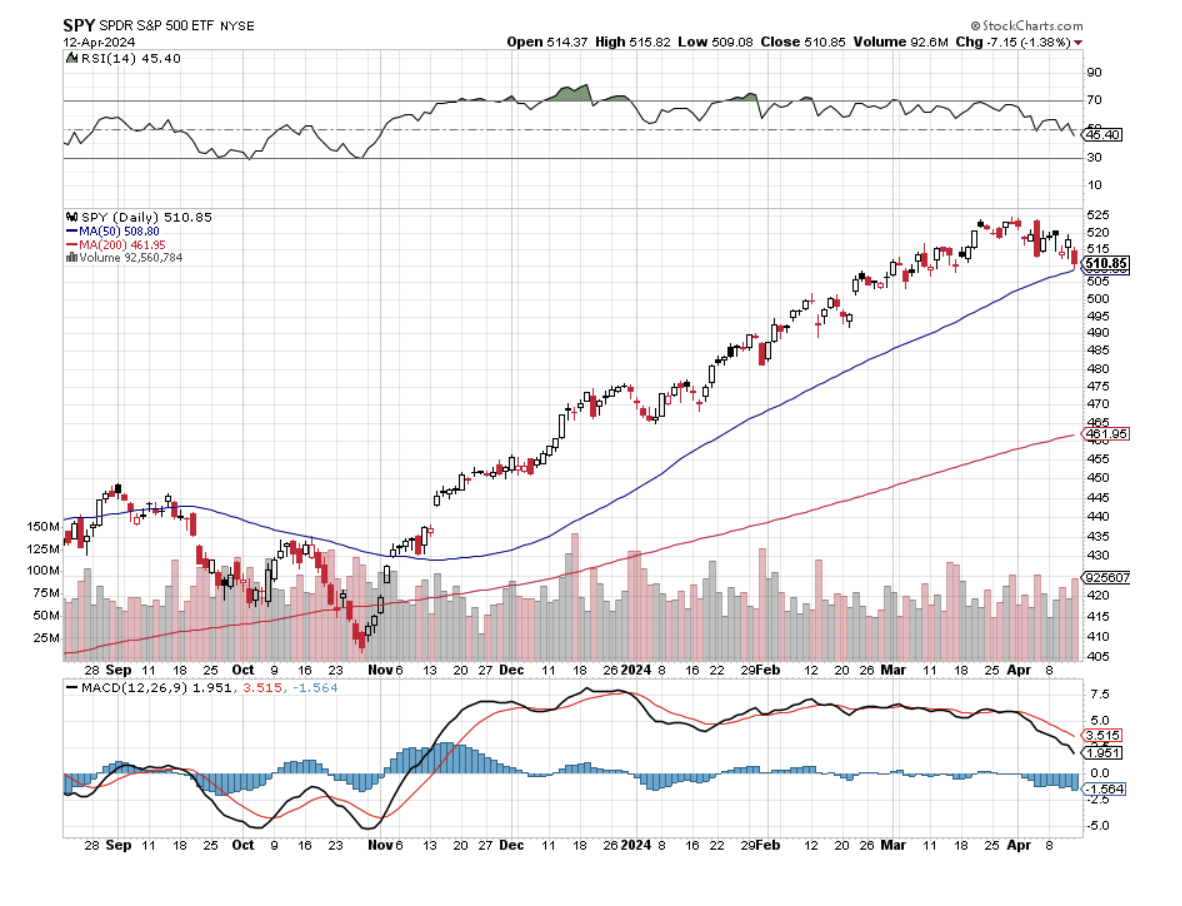

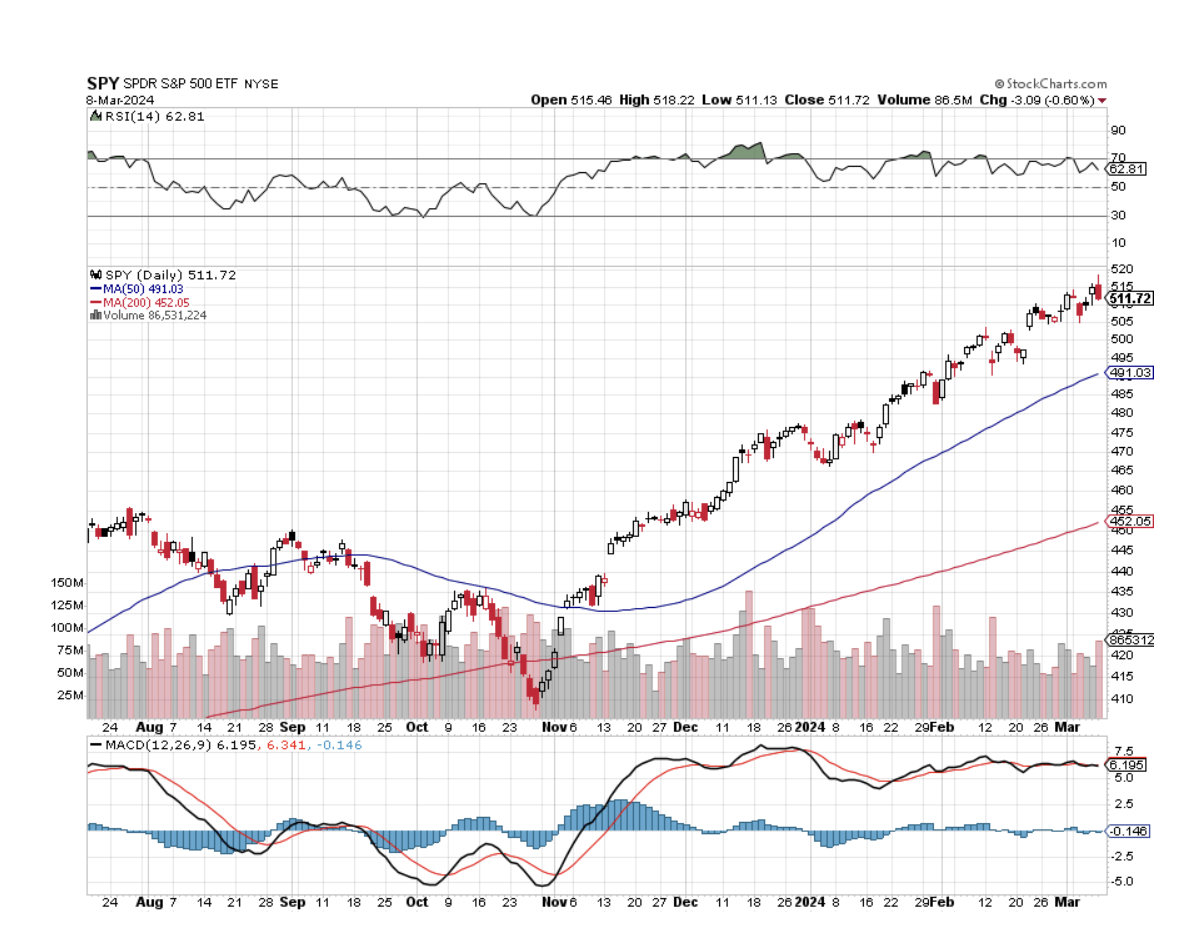

Watching the market action last week, it was especially impressive how well NVIDIA (NVDA) held up.

NVIDIA is so far ahead of the competition that no one will catch up for years. What the (NVDA) bears don’t get is that the company has a moat so wide it is impossible to cross. Their enormous lead in software is the result of crucial platform decisions made 20 years ago. The key staff are all locked up with ultra-cheap equity options with strike prices around $1-$2.

Virtually everyone has now raised their upside targets for the stock over $1,000/share and there are $1,400 figures out there. That’s because, with a price-earnings multiple of only 30X, it is still the cheapest Big Tech stock in the market. By comparison, its biggest customer, (META) is at 34X, AI Leader (MSFT) is at 38X, and (AMZN) is at a stratospheric 63X.

Efforts by Alphabet (GOOGL) to break into the AI chip business are feeble at best. This is a business that has a very long learning curve with very high capital costs.

Every 15% correction in (NVDA) over the last two years has been a strong “BUY”. It really owns the AI design business. It’s looking at $250-$500 BILLION in sales growth over the next several years.

Santa Clara-based NVIDIA designs and manufactures high-end, top-performing graphics cards or GPUs. There is probably one in your PC. They are essential in the artificial intelligence, automobile, PC, supercomputing, cybersecurity, and gaming industries. As a design company only company NVIDIA represents pure intellectual added value. Its chips are manufactured in Taiwan.

They are also crucial for national defense. The Biden administration recently banned NVIDIA from exporting high-end chips and their manufacturing equipment to China, which they were using to build sophisticated weapons to use against us. Last week China banned NVIDIA chips in a typical tit-for-tat gesture.

We have had a spectacular week here at Mad Hedge Fund Trader.

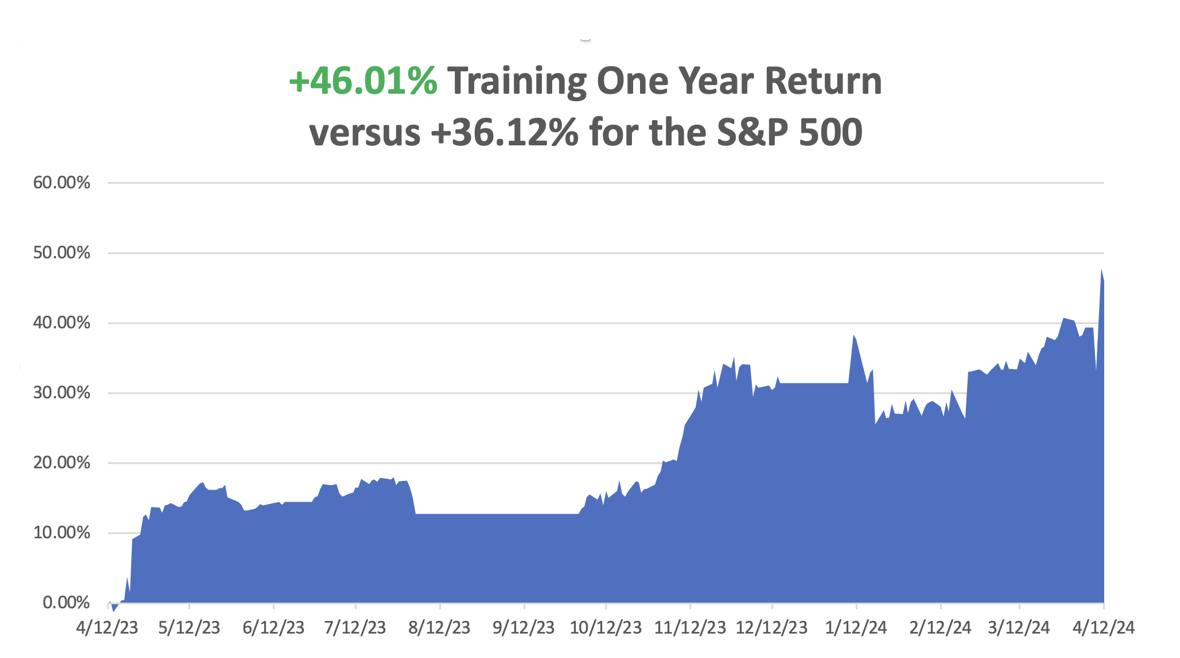

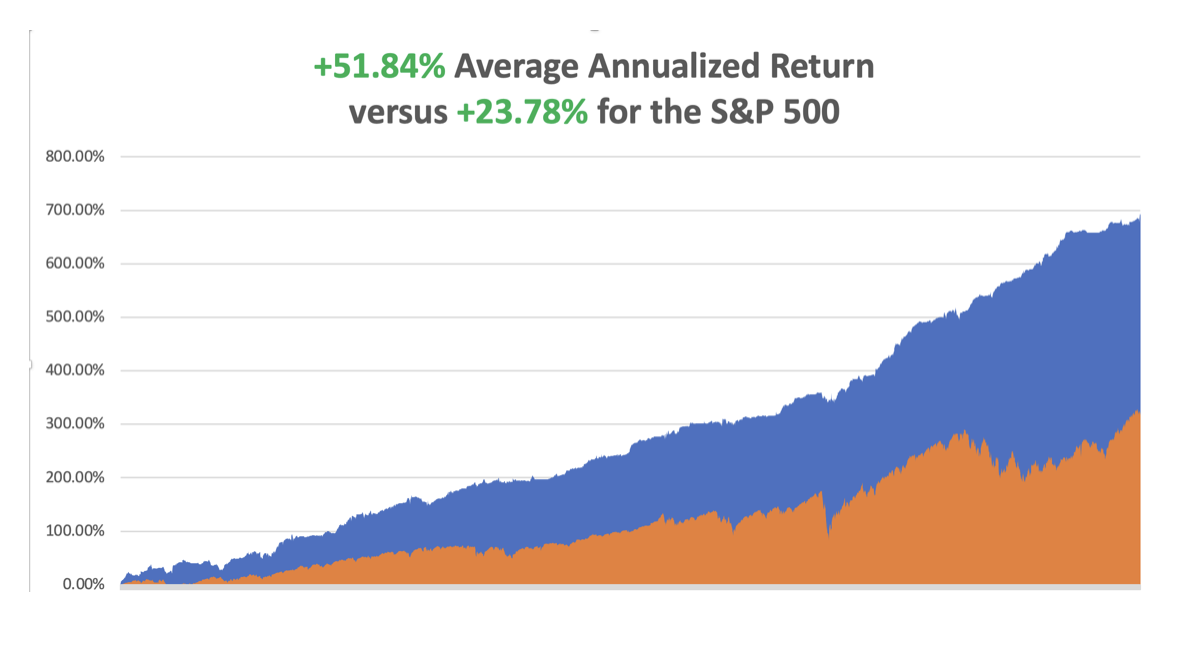

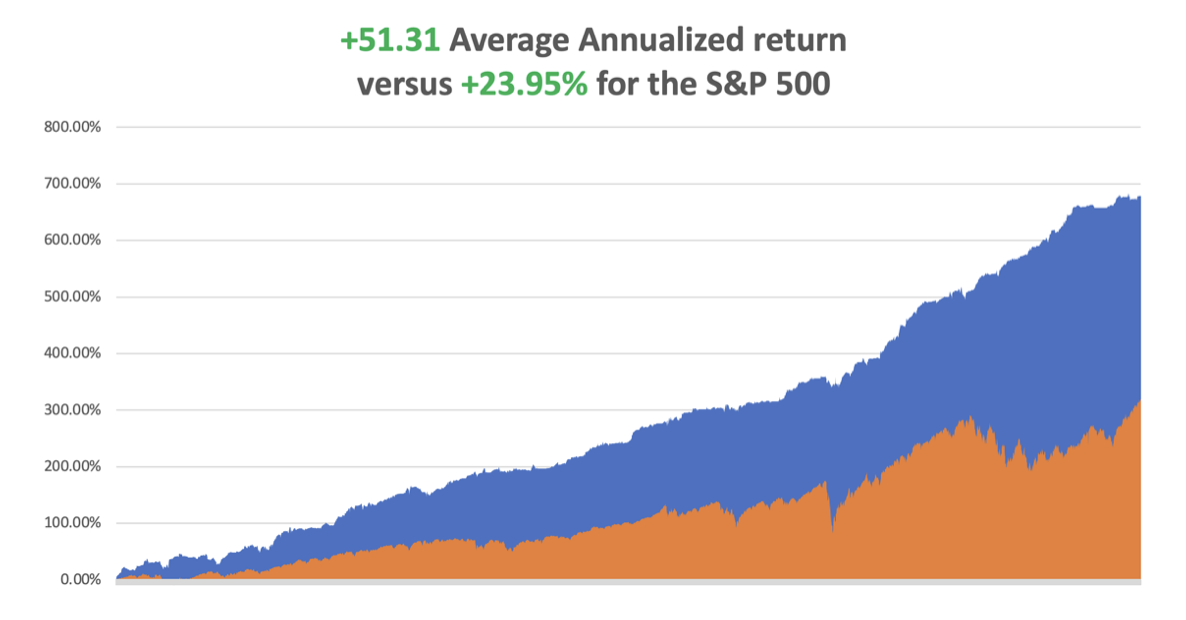

So far in April, we are up +5.20%. My 2024 year-to-date performance is at +14.47%.The S&P 500 (SPY) is up +7.22%so far in 2024. My trailing one-year return reached +46.01%versus +36.12% for the S&P 500. That brings my 16-year total return to +691.20%.My average annualized return has recovered to +51.84%.

Some 63 of my 70 round trips were profitable in 2023. Some 20 of 26 trades have been profitable so far in 2024.

We got a rare dip last week, which I used to rush into four new May positions, double positions in (NVDA) and additional ones in (FCX) and (TLT). I will let my existing April longs expire at a max profit in four days on April 19 in Freeport McMoRan (FCX), Occidental Petroleum (OXY), ExxonMobile (XOM), Wheaton Precious Metals (WPM), Tesla (TSLA), and Gold (GLD).

I am in a rare 100% invested position with no cash given the massive upside breakout in commodity, precious metals, and energy we have witnessed. This is going to be a great month.

Consumer Price Index Comes in Hot at 0.4% for March, the same rate as in February according to the Bureau of Labor Statistics, knocking stocks down 500 points. Housing and transportation were the big badges. Hopes of a June interest rate cut have been dashed. September is now the earliest. Avoid (TLT).

Producer Price Index Comes in Cold at 0.2% for March.On a 12-month basis, the PPI rose 2.1%, the biggest gain since April 2023, indicating pipeline pressures that could keep inflation elevated. Stocks rallied 200 points.

US Dollar Rockets on Hot CPI, hitting a new 34-year high against the Japanese yen at ¥151.55. Bank of Japan's intervention to support the yen is expected. Yen shorts in the futures market hit a five-month high. Avoid (FXY).

China Continues Record Gold Buying, soaking up record amounts. Central banks bought a record 1,082 metric tonnes of gold in 2023. The Bank of China bought a record 735 tonnes of gold in 2023, two-thirds of which were purchased through covert third-party middlemen. An additional 1,411 tonnes, likely to bypass a collapsing Yuan, and a whopping 228 tonnes in January 2024 alone. This is what delivered the barbarous relic’s decisive upside breakout from a three-year trading range. This dwarf’s the record 1,082 metric tonnes of gold global central banks bought in 2023. The world gold market has been taken short and prices will continue to rise.

Gold Derivatives are Now Wagging the Dog. There are 187,000 metric tonnes of gold above ground worth a mere $14.4 billion which price is 50 times that figure in paper derivatives, like ETFs, futures contracts, and options. A metric tonne of gold today is worth $77 million. That increases the barbarous relic’s volatility once it breaks out of long-term trading ranges, which it has just done. With new volatility eventually, some bodies have to float to the surface. The bad news is that this may also be a signal that China will invade Taiwan. Buy (GLD) on dips.

Oil (USO) Spikes on New Iran War Threats, sending Brent to $92, a new 2024 high. Gold (GOLD) and silver (WPM) have gone ballistic as well. Hang on for higher highs.

JP Morgan Misses on Earnings, tanking the shares by $10. The firm earned $23.1 billion in net interest income in the first three months of 2024, up 11% from a year earlier. The bank’s NII haul ended a streak of seven quarters where it posted record levels of the metric. The bank cited deposit margin compression — tightening of profits between what the bank earns on loans and pays out on deposits — and lower deposit balances in the consumer business for the sequential decline. Buy (JPM) on dips.

China’s International Trade Collapses. Exports from China slumped 7.5% year-on-year last month by value, the biggest fall since August last year. They had risen 7.1% in the January-February period.

Hong Kong's major indexes extended losses to more than 2%.

Chinese exporters are continuing to slash prices to maintain sales amid stubbornly weak domestic demand. Avoid (FXI).

Tesla Cancels Model 2, a key part of the bull story for (TSLA). Elon Musk says “Not so fast” and instead highlights the company’s move into robotic self-driving cars. Don’t be so dismissive, as Waymo completed an eye-popping 100,000 robotic taxi rides in San Francisco in December, many with thrilled first-time users. The stock held up incredibly well on awful news indicating that it believes Elon and not the media. Buy (TSLA) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 15, at 7:00 AM EST, the US Retail Sales are announced.

On Tuesday, April 16 at 8:30 AM, US Housing Starts are released.

On Wednesday, April 17 at 2:00 PM, the Beige Book notes from the previous Fed meeting are published

On Thursday, April 18 at 8:30 AM, the Weekly Jobless Claims are announced. At 10:00 AM, Existing Home Sales are out.

On Friday, April 19 at 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, with the spectacular popularity of the Oppenheimer movie, I thought I’d review my own nuclear past. When the Cold War ended in 1992, the United States judiciously stepped in and bought the collapsing Soviet Union’s entire uranium and plutonium supply.

For good measure, my client George Soros provided a $50 million grant to hire every Soviet nuclear engineer. The fear then was that starving homeless scientists would go to work for Libya, North Korea, or Pakistan, which all had active nuclear programs at the time.

They ended up here instead. I just might be that the guy standing next to you in line at Safeway with a foreign accent who knows how to design a state-of-the-art nuclear bomb.

That provided the fuel to run all US nuclear power plants and warships for 20 years. That fuel has now run out and chances of a resupply from Russia are zero. The Department of Defense attempted to reopen our last plutonium factory in Amarillo, Texas, a legacy of the Johnson administration.

But the facilities were deemed too old and out of date, and it is cheaper to build a new factory from scratch anyway. What better place to do so than Los Alamos, which has the greatest concentration of nuclear expertise in the world?

Los Alamos is a funny sort of place. It sits at 7,320 feet on a mesa on the edge of an ancient volcano so if things go wrong, they won’t blow up the rest of the state. The homes are mid-century modern built when defense budgets were essentially unlimited. As a prime target in a nuclear war, there are said to be miles of secret underground tunnels hacked out of solid rock.

You need to bring a Geiger counter to garage sales because sometimes interesting items are work castaways. A friend almost bought a cool coffee table which turned out to be a radioactive part of an old cyclotron. And for a town designing the instruments to bring on the possible end of the world, it seems to have an abnormal number of churches. They’re everywhere.

I have hundreds of stories from the old nuclear days passed down from those who worked for J. Robert Oppenheimer and General Leslie Groves, who ran the Manhattan Project in the early 1940s. They were young mathematicians, physicists, and engineers at the time, in their 20s and 30s, who later became my university professors. The A-bomb was the most important event of their lives.

Unfortunately, I couldn’t relay this precious unwritten history to anyone without a security clearance. So, it stayed buried with me for a half century, until now.

Some 1,200 engineers will be hired for the first phase of the new plutonium plant, which I got a chance to see. That will create challenges for a town of 13,000 where existing housing shortages already force interns and graduate students to live in tents. It gets cold at night and dropped to 13 degrees F when I was there.

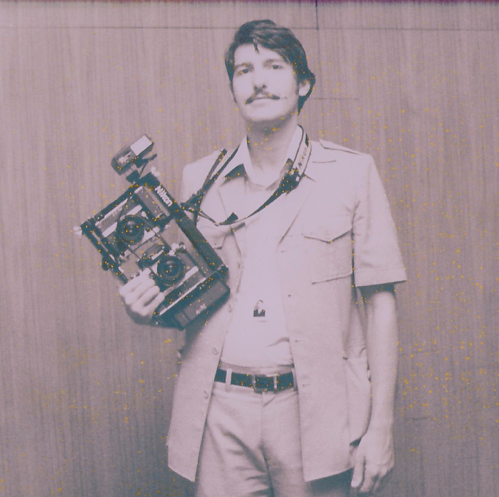

I actually started in the nuclear biz during the early 1970s when my math professor recommended me for a job there. In those days, mathematicians had only two choices. Teach or work for the Defense Department. As I was sick of school, I chose the latter.

That led me to drive down a bumpy dirt road in Mercury, Nevada to the Nuclear Test Site where underground testing was still underway. There were no signs. You could only find the road marked by four trailers occupied by hookers who did a brisk business with the nearly all-male staff. My fondest memory was the skinny dipping that took place after midnight in a small pool when the MPs were on break.

I was recently allowed to visit the Trinity site at the White Sands Missile Test Range, the first outsider to do so in many years. This is where the first atomic bomb was exploded on July 16, 1945. The 20-kiloton explosion set off burglar alarms for 200 miles and was double to ten times the expected yield.

Enormous steel targets hundreds of yards away were thrown about like toys (they are still there). Half the scientists thought the bomb might ignite the atmosphere and destroy the world but they went ahead anyway because so much money had been spent, 3% of US GDP for four years. Of the original 100-foot tower, only a tiny stump of concrete is left (picture below).

With the other visitors, there was a carnival atmosphere as people worked so hard to get there. My Army escort never left me out of their sight. Some 79 years after the explosion, the background radiation was ten times normal, so I couldn’t stay more than an hour.

Needless to say, that makes uranium plays like Cameco (CCJ), NextGen Energy (NXE), Uranium Energy (UEC), and Energy Fuels (UUUU) great long-term plays, as prices will almost certainly rise and all of which look cheap. US government demand for uranium and yellow cake, its commercial byproduct, is going to be huge. Uranium is also being touted as a carbon-free energy source needed to replace oil.

At Ground Zero in 1945

What’s Left of a Trinity Target 200 Yards Out

Playing With My Geiger Counter

Atomic Bomb No.3 Which was Never Used

What’s Left from the Original Test

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/03/ground-zero.png758584april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-15 09:02:482024-04-15 14:04:39The Market Outlook for the Week Ahead, or Volatility is Back!

(The Mad MARCH traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HIGHER HIGHS)

(NVDA), (META), (IWM), (AMZN), (RIVN), (SNOW), (GLD), (GOLD), (NEM), (FXI), DELL), (AAPL), (TSLA), (CCJ), ($NIKK), (USO), (GOLD)

I was all ready to write another hyper-bullish report for the week. That was at least until noon EST on Friday. That’s when NVIDIA (NVDA) Peaked at $955 and then free fell $100 to $855. New all-time and then a new intraday low on huge volume and that is the textbook definition of a market top.

Not that we should be complaining. At the high, (NVDA) was up an unimaginable 105% so far this year. I spent my week buying back short put options for 50 cents that I initially sold for $20. With a quarterly quadruple witching due this Friday, anything can happen.

By the end of February, more than half of all analyst 2024 yearend targets were met. The response was a rush to raise yearend targets, triggering the current melt-up.

It always ends in tears.

And I’m about to tell you something that you will absolutely love to hear. Lower interest rates dramatically increase corporate stock buybacks, already set at $1.25 trillion for 2024. That’s because of the lower cost of capital.

What do more share buybacks automatically bring? High stock prices, especially for large positive cash flow companies like big tech.

As much as the permabears hate to admit it, good news really is good news.

With all of the media obsession with NVIDIA (NVDA), my largest holding, and Meta (META), the fact is that the rally is broadening out. More than half of all industrial stocks are trading at all-time highs. Long-forgotten small caps (IWM) are also approaching 2021 all-time highs.

Going into this week managers were either overweight big tech and extremely nervous or out of big tech and kicking themselves. The urge to rotate is strong. But your standby rotation sectors, industrials, biotech, and banking have also seen big moves.

Which brings us to the subject of gold (GLD).

After a tedious one-year sideways consolidation, the barbarous relic blasted out to the upside above $2,200 an ounce, a new all-time high. After soaking up as much gold as they could over the past decade, China and Russia have finally taken the gold market net short, which is why we saw such dramatic price action.

With interest rates in the US soon to fall, the opportunity cost of owning non-yielding gold is about to shrink. That will cut the knees out from under the US dollar prompting a stampede into precious metals and Bitcoin.

Except this time, it’s different.

Gold miners usually outperform the yellow metal by four to one to the upside. Not so this time. Barrick Gold (GOLD) and Newmont Mining (NEM) were barely able to keep pace with the barbarous relic. That’s because inflation has boosted their costs and cut profit margins. After all, they are stock first and gold plays second.

Still, if gold reaches my $3,000 target in 2025 the LEAPS I sent out for (GOLD) last June should easily hit its maximum profit point of 298%.

That other weak dollar play, oil (USO) may not deliver the joys of past cycles and may in fact be trapped in a fairly narrow $60-$80 range. The futures markets are saying that the price of Texas tea will be lower in a year.

The US is now the world’s top oil producer at 13 million barrels/day and that is rising (thanks to enormously generous tax breaks), capping prices. Non-OPEC+ production is increasing, especially from Brazil and Canada. China, the world’s largest oil importer is missing in action. But low inventories, especially at the American Strategic Petroleum Reserve, are preventing a crash as well. Shale production is growing.

Still, even a $20 rally can have a dramatic impact on the share prices of the big US producers, like Exxon (XOM) and Occidental Petroleum (OXY), some 25% of which is now owned by Warren Buffet. Even without some sexy price action, this sector pays some of the highest dividend yields in the markets.

In February we closed up +7.42%. So far in March, we are up +0.70%. My 2024 year-to-date performance is at +3.21%. The S&P 500 (SPY) is up +7.11% so far in 2024. My trailing one-year return reached +54.28% versus +40.94% for the S&P 500.

That brings my 16-year total return to +689.74%. My average annualized return has recovered to +52.05%.

Some 63 of my 70 trades last year were profitable in 2023. Some 11 of 15 trades have been profitable so far in 2024.

I used the ballistic move in (NVDA) to take profits in my double long there. I am maintaining longs in (AMZN) and Snowflake (SNOW). I am both long and short the bond market (TLT) and I am 60% in cash given the elevated level of the stock markets.

Nonfarm Payroll Report Rose 275,000 in February. The Headline Unemployment Rate rose to 3.9%, a two-year high. The report illustrates a labor market that is gradually downshifting, with more moderate job and pay gains that suggest the economy will keep expanding without much risk of a reacceleration in inflation. These are very Fed friendly numbers.

JOLTS Job Openings Report Rises by 140,000 to 8,890,000, less than expected. Leisure and hospitality led with 41,000 new jobs, construction added 28,000 and trade, transportation and utilities contributed 24,000. Growth was concentrated among larger companies, as establishments with fewer than 50 employees contributed just 13,000 to the total.

Rivian Shares Soar, on news it is halting plans to build a new $2.25 billion factory in Georgia, an abrupt reversal aimed at cutting costs while the company prepares to launch a cheaper electric vehicle. Shifting planned production of the forthcoming R2 model to an existing facility in Illinois will allow Rivian to begin deliveries in the first half of 2026, earlier than expected. Buy (RIVN) on dips.

New York Community Bancorp Bailed Out, with a cash infusion led by former Treasury secretary Steve Mnuchin. The shares soared from $2 to $3.41. That takes the heat off the sector….until the next one. The US is shrinking from 4236 banks to only six banks. Who says politics doesn’t pay?

Europe Moves Towards Interest Rate Cuts, igniting a global bond market rally. Staff projections now see economic growth of 0.6% in 2024, from a previous forecast of 0.8%. They presented a more positive picture of inflation, with the forecast for the year brought to an average 2.3% from 2.7%. Market bets increased on rate cuts taking place as early as June, with the euro trading 0.35% lower against the British pound following the news.

Beige Book Comes in Moderate, saying "labor market tightness eased further," in February but noted "difficulties persisted attracting workers for highly skilled positions." The Beige Book is a review of economic conditions across all 12 Fed districts. Fed Chair Jerome Powell told Congress on Wednesday that the U.S central bank expected "inflation to come down, the economy to keep growing," but shied away from committing to any timetable for interest rate cuts.

China Targets 5% Growth for 2024, but nobody buys it for a second. A covid hangover, residential real estate crisis triggering a financial crisis, and constant invasion threats over Taiwan, make this target a pipe dream. Avoid (FXI) and all Middle Kingdom plays.

Gold Hits New All-Time High, at $2,141 an ounce on expectations of imminent rate cuts by the Fed. Gold, often used as a safe store of value during times of political and financial uncertainty, has climbed over $300 dollars since the start of the Israel-Hamas war. Buy (GLD), (GOLD), and (NEM) on dips.

Dell (DELL) Becomes an AI Stock, sending the shares up 47% in a Day. That’s been changing over the past year, as Dell has been reporting strong orders of servers designed to power generative AI workloads—many of which use chips supplied by AI kingmaker Nvidia. The company’s fourth quarter results convinced any doubters. Can Apple (AAPL) do the same?

Tesla Plunges on Poor China Sales, down $14.50 on sales data dimmed the outlook for Tesla's global deliveries, at a time when the top EV maker is battling a decline in demand and is weighed down by a lack of entry-level vehicles and the age of its product line-up. Not the time to be in EVs or solar. Buy (TSLA) on bigger dip.

US National Debt is Rising by $1 Trillion Every 100 Days. A trillion here, a trillion there, sooner or later that adds up to a lot of money. Eventually, someone is going to have to do something about this. The US national debt stands at $34.5 trillion, or $104,545 per person.

The Uranium Shortage is Getting Extreme, with yellow cake up 112% in a year. Owners of left-for-dead uranium mines are restarting operations to capitalize on rising demand for the nuclear fuel. Most of those American mines were idled in the aftermath of Fukushima when uranium prices crashed and countries like Germany and Japan initiated plans to phase out nuclear reactors. Now, with governments turning to nuclear power to meet emissions targets and top uranium producers struggling to satisfy demand, prices of the silvery-white metal are surging. Buy (Cameco (CCJ) on dips.

Japan’s Nikkei ($NIKK) Tops 40,000, a new 34-year high. The ultra-weak Japanese economy is giving the economy there a free lunch, but better hedge your currency exposure. Good thing I missed a dead market for 34 years.

NVIDIA Replaces Tesla as Top Traded Stock, with volumes migrating to the options market as well. Blockbuster profits are catnip for traders, while EV price wars aren’t. Tesla is down 52% from its all-time high two years ago and is one of the biggest percentage decliners in the Nasdaq 100 Index this year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 11 at 7:00 AM EST, the Consumer Inflation Expectations are announced.

On Tuesday, March 12 at 8:30 AM, Inflation Rate for February is released.

On Wednesday, March 13 at 2:00 PM, MBA Mortgage Applications are published

On Thursday, March 14 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index.

On Friday, March 15 at 2:30 PM, the University of Michigan Consumer Sentiment is published. At 2:00 PM the Baker Hughes Rig Count is printed.

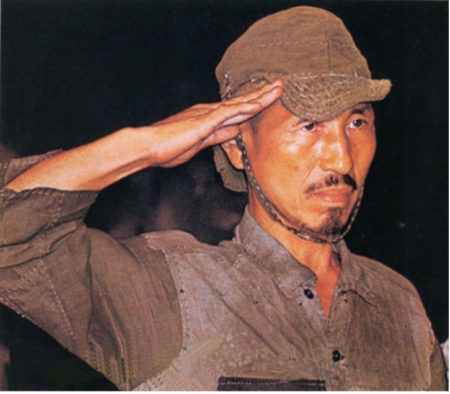

As for me, I have met many interesting people over a half-century of interviews, but it is tough to beat Corporal Hiroshi Onoda of the Japanese Army, the last man to surrender in WWII.

I had heard of Onoda while working as a foreign correspondent in Tokyo. So, I convinced my boss at The Economist magazine in London that it was time to do a special report on the Philippines and interview President Ferdinand Marcos. That accomplished, I headed for Lubang island where Onoda was said to be hiding, taking a launch from the main island of Luzon.

I hiked to the top of the island in the blazing heat, consuming two full army canteens of water (plastic bottles hadn’t been invented yet). No luck. But I had a strange feeling that someone was watching me.

When the Philippines fell in 1945, Onoda’s commanding officer ordered the remaining men to fight on to the last man. Four stayed behind, continuing a 30-year war.

As a massive American military presence and growing international trade raised Philippine standards of living, the locals eventually were able to buy their own guns and kill off Onoda’s companions one by one. By 1972 he was alone, but he kept fighting.

The Japanese government knew about Onoda from the 1950s onward and made every effort to bring him back. They hired search crews, tracking dogs, and even helicopters with loudspeakers, but to no avail. Frustrated, they left a one-year supply of the main Tokyo newspaper and a stockpile of food and returned to Japan. This continued for 20 years.

Onoda read the papers with great interest, believing some parts but distrusting others. His worldview became increasingly bizarre. He learned of the enormous exports of Japanese automobiles to the US, so he concluded that while still at war, the two countries were conducting trade.

But when he came to the classified ads, he found the salaries wildly out of touch with reality. Lowly secretaries were earning an incredible 50,000 yen a year, while a salesman could earn an obscene 200,000 yen.

Before the war, there was one Japanese yen to the US dollar. In the hyperinflation that followed the yen fell to 800, and then only recovered to 360. Onoda took this as proof that all the newspapers were faked by the clueless Americans who had no idea of true Japanese salary levels.

So he kept fighting. By 1974 he had killed 17 Philippino civilians.

After I left Lubang island, a Japanese hippy named Norio Suzuki with long hair, beads, and sandals followed me, also looking for Onoda. Onoda tracked him as he had me but was so shocked by his appearance that he decided not to kill him. The hippy spent two days with Onoda explaining the modern world.

Then Suzuki finally asked the obvious question: what would it take to get Onoda to surrender? Onoda said it was very simple, a direct order from his commanding officer. Suzuki made a beeline straight for the Japanese embassy in Manila and the wheels started turning.

A nationwide search was conducted to find Onoda’s last commanding officer and a doddering 80-year-old was turned up working in an obscure bookstore. Then the government custom-tailored a prewar Imperial Japanese Army uniform and flew him down to the Philippines.

The man gave the order and Onoda handed over his samurai sword and rifle, or at least what was left of it. Rats had eaten most of the wooden parts. You can watch the surrender ceremony by clicking here on YouTube.

When Onoda returned to Japan, he was a sensation. He displayed prewar mannerisms and values like filial piety and emperor worship that had been long forgotten. Emperor Hirohito was still alive.

When I finally interviewed him, Onoda was sympathetic. I had by then been trained in Bushido at karate school and displayed the appropriate level of humility, deference, mannerisms, and reference.

I asked why he didn’t shoot me. He said that after fighting for 30 years he only had a few shells left and wanted to save them for someone more important.

Onoda didn’t last long in the modern Japan, as he could no longer tolerate modern materialism and cold winters. He moved to Brazil to start a school to teach prewar values and survival skills where the weather was similar to that of the Philippines. Onoda died in 2014 at the age of 91. A diet of coconuts and rats had extended his life beyond that of most individuals.

Onoda wasn’t actually the last Japanese to surrender in WWII. I discovered an entire Japanese division in 1975 that had retreated from China into Laos and just blended in with the population. They were prized for their education and hard work and married well.

During the 1990’s a Japanese was discovered in Siberia. He was released locally at the end of the war, got a job, married a Russian woman, and forgot how to speak Japanese. But Onoda was the last to stop fighting.

The Onoda story reminds me of the fact that journalists learn very early in their careers. You can provide all the facts in the world to some people. But if they conflict with their own deeply held beliefs, they won’t buy them for a second.

Hiro Onoda Surrenders

Budding Journalist John Thomas

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-11 09:02:232024-03-11 12:13:02The Market Outlook for the Week Ahead, or Higher Highs

Below please find subscribers’ Q&A for the February 21 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: What do you think of the comments of Ray Dalio and Jamie Dimon of an imminent war with Russia and China?

A: I think the chances of that are almost zero. You’re talking about Russia with a $1 trillion economy going to war against a combined GDP of the US and Europe of $50 trillion. Even Switzerland is sending tanks to Ukraine now. Our military is so dominant compared to any other country in the world, that it would be an instant wipeout. Russia and China know that, so they can threaten all they want but will take no action. That really has been the course since the end of WWII; talk is cheap. However, it is not a zero risk—a person like Ray Dalio, especially, always has to consider the 1% risk (Jamie Dimon less so.) I don’t worry about that at all; a lot of that is media hype. Newspapers have to fill their space every day of the year, even when nothing is happening.

Q: What about Russia putting nuclear weapons in space?

A: The US actually looked at doing this in the 60s and 70s when I was with the Atomic Energy Commission, and this is the problem: Uranium weighs four times that of lead, and it’s very hard to get any serious weight into space. And Russia has never been able to actually hit anything it aims at, so other than destroying a bunch of nearby Starlink satellites, it wouldn’t really accomplish much. Plus, we do have a treaty with Russia not to put nuclear weapons in space—not that agreements between the US and Russia are particularly trustworthy these days.

Q: Would you sell naked Nvidia (NVDA) puts right now?

A: Dan, somehow you got into my personal trading account and looked at all my positions! You know, I never advise people to sell naked puts unless they're happy to own the stock at that level. That means, first of all, you cannot leverage at all—the way people go bust on short put strategies is they sell far more puts than they have the money to support the cash buy if they have to do it. But I can tell you, I looked at the numbers this morning: if you sell short an Nvidia put now at 600 you can get about $10 for it. And, if Nvidia goes below 600 by option expiration day, you own Nvidia stock at a cost of $590. And I'm happy to own Nvidia at $590 because I think it could be worth $1,000 by yearend. There may be better ways to use your money with Nvidia at $600, like doing an at-the-money LEAPS which will get you a 100% return in a year even on no move. If you want to go, say, $40 out of the money or $50, like a 650-$650 Nvidia LEAPS, then you're looking at it with a 150% return in a year. So that is the better way to do it, it just depends on how aggressive you want to be and how eager you are to go back to work at Taco Bell if you lose all your money.

Q: What would you do with Super Micro Computer Inc. (SMCI) right now?

A: I would sell it, but then I would’ve sold it on the first 23x move. (SMCI) is a no-touch right now—I think they have a 3% float in their shares, and that’s what’s causing the spectacular market volatility.

Q: Will continued weakness in China (FXI) bring down the US markets?

A: No. We have very few investors from China in the US stock market. They really have no impact on our market. And the fundamentals couldn't be more different. You know, the US economy is in great shape right now (and getting better, I might add), while China continues to go down the toilet and is saber-rattling and warmongering. So, it's not good for stock prices for sure. You could put that at the bottom of the list of worries.

Q: Will Tesla (TSLA) ever turn around?

A: Well what you don’t know if you don't follow the company on a daily basis like I do, is that Tesla is continuously cutting costs, and increasing performance, and that will lead to greater sales and greater profits. But when that happens, I have no idea. I think the Tesla 2 coming out next year—the $25,000 EV could be a big turning point for the company. And of course, Tesla stock may front-run that by six months. So eventually, Tesla will come back.

Q: Thanks for your advice. I have a ton of Nvidia (NVDA) and some Tesla (TSLA). Should I sell my Tesla and put it in Nvidia?

A: No, you should do the opposite. Buy low, sell high—it’s my revolutionary new stock trading system which I’m thinking of copywriting. Nvidia has had one of the biggest stock gains in history, and Tesla is down year-on-year. So, that is the trade, and that is what a lot of long-term investors are doing, is doing that swap.

Q: Can we do a LEAPS on Palo Alto Networks (PANW)?

A: Absolutely. Wait for this selloff to finish, then go in at the money one year out and you should get a 100% or a double on your return. And by the way, when I’m convinced that tech stocks have finished this selloff, I’ll be issuing a whole bunch of LEAPS trade alerts. I’ll do the numbers and do the heavy lifting for you.

Q: Can Ukraine win the war against Russia without US aid?

A: No, in fact, it needs aid from both the US and Europe. Right now, Europe is carrying 100% of the burden, as the US has stopped providing aid to Ukraine, thanks to the Republican-led House of Representatives. And Ukraine is now ceding cities to Russia because they don’t have the ammunition or the missiles to defend them. So, give as much ammo as we can. Otherwise, it’s just a matter of time before US soldiers get involved in a European war once again. How the Republicans see cutting off as in America’s benefit, I can’t imagine, nor do many Republicans. They must be reading different news sources. But I’m also prejudiced on this, having been shot by Russians in Ukraine in October. (Those injuries are all healed by the way thanks to a stem cell injection and I’m back to hiking as usual.)

Q: When you say buy on dips, do you have a rule of thumb on what percentage a stock has to drop in order to consider it a dip?

A: It’s different for every stock because every stock has a different volatility. “Buy on the dip” might be a 5% for Cleveland Cliffs but it might be 20% for Nvidia. It’s all over the map—you just have to look at the charts and judge where the next support level is, before considering risking your own money.

Q: What’s your favorite dividend stock?

A: Well my Number One favorite, of course, is Crown Castle International (CCI)—the cellphone tower REIT—and REITS of any kind are going to be very high-yield and very attractive. Just stay away from the commercial office REITS, which are having their own well-publicized problems. Beyond that, the only attractive high dividend stocks are in energy: you have Exxon Mobil (XOM) yielding 3.7% and Diamondback Energy with the lovely ticker symbol of (FANG) yielding 4.48%. On the oils, you get a shot for not only the dividend but a nice capital gain on any recovery in the oil market. So that could be an attractive play once we finish bombing the Houthis and wiping out all their Iran-supplied missiles.

Q: What happened to the Japanese yen rally?

A: Well as with all other foreign currencies, it died and went to Heaven, because of the delay in US interest rate cuts. As long as the US doesn't cut interest rates, it will continue to have the strongest currency in the world. And when we get to the currency charts, you'll see exactly how strong the dollar has been. That does make the currencies very attractive right around here.

Q: Will commercial real estate blow up the banks, and therefore the stock market?

A: No, first of all, for big banks (XLF), commercial real estate is only 5% of their loan portfolio and if they lose 20% of that, that’s only a 1% loss of their total loans year for them and that is totally acceptable by in their business model. Second, if interest rates fall, the commercial real estate problem goes away because they can refinance at lower rates than you get now. Third, as the economy recovers, demand for office space will also recover, though it may take 5 years to soak up all the excess inventory that we have right now. San Francisco has an empty office space rate of about 30%, which is higher than it’s ever been. That is why a lot of smart, long-term real estate money is buying up buildings in San Francisco— they're buying them up for pennies on the dollar, so that sounds like a great investment. I remember back in the early eighties, Morgan Stanley did exactly the same thing in Houston after an oil collapse. You know, they were giving away office buildings—paying you to take them away, literally—and Morgan Stanley set up an in-house partner fund (it was only open for the partners from Morgan Stanley to invest in) and we went in and bought 600 million dollar’s worth of cheap Houston real estate. I think we ended up getting a 10x return on that, but that's what being a Morgan Stanley partner is all about. That was about 45 years ago, and it’s what’s happening now in San Francisco.

Q: Are you worried about Amazon (AMZN) with Jeff Bezos selling 8 billion dollars worth of stock?

A: Well, if you've made a couple of $100 billion you're allowed to spend $8 billion on yourself. And Amazon is one of the early leaders in AI technology, so I'm buying that on every dip. In fact, we had a long position in Amazon that just expired on Friday.

Q: Why is Home Depot Inc. (HD) stagnating?

A: Well that's easy: during the pandemic, everyone was stuck at home 24 hours a day, 7 days a week, so they wanted to fix stuff. With the end of the pandemic, that has ended and has slowed down business at both Home Depot and Lowes (LOW).

Q: Do you like Advanced Micro Devices (AMD) and would you buy it on a dip?

A: Absolutely, it’s all part of the same AI trade, as are all the other big chip stocks.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

When I announced my year-end target for the S&P 500 on the first of January, I knew it was cautious. That provided for only a 15% gain for 2024. Yet here we are a mere six weeks into the New Year, and we only have 10.4% to go.

That is with the six lead stocks, which account for 30% of the entire stock market capitalization, seeing earnings grow up to 300% annually. With that kind of growth, even $6,000 is looking overly conservative, even allowing for no multiple expansion whatsoever.

The top six stocks are over 11% YTD, while half of all S&P 500 stocks are down. A few friends of mine who are still alive and have been in the market for as long as I have never seen a market this concentrated. They are amazed, befuddled, and aghast, as am I.

And if you do want to buy big tech, you’re going to have to compete with the big tech companies themselves to do so. The buyback machine continues full speed ahead, with Apple (AAPL) Hoovering up $20.5 billion of its own shares, Alphabet (GOOGL) $16.1 billion, Meta (META) 6.3 billion, and Microsoft (MSFT) $4 billion.

I am a firm believer that markets will do whatever they have to do to screw the most people. So far this year it has done an admirable job doing just that, going up in a straight line with everyone underinvested and with $8 trillion on the sideline.

This is how markets will continue screwing most people. It keeps going up a little bit more. The NVIDIA earnings announcement due out on February 21 could be the ideal turning point.

Then the market suffers a ferocious correction, maybe 10% in a short period. Traders panic and dump all their positions. Then the (SPX) turns around at about $4,800 on a dime and then rockets all the way up to $6,000, frustrating investors once again.

I just thought you’d like to know.

I am usually cautious about ultra bears, but I picked up an interesting view last week about how long it may take the Chinese economy to recover.

During the US house bust from 2007 to 2012, the United States had 3 million excess unwanted homes weighing on the market like a dead weight, or about a seven-month oversupply. That was enough excess to cause the Great Recession, a 52% crash in the S&P 500, and the demise of thousands of American companies, including Lehman Brothers and Bear Stearns.

Today, China has a staggering 50 million excess homes in a population only four times larger than ours. That is a 15-year oversupply for the market. That means China could suffer a decade and a half of subpar growth and lagging stock markets. Don’t touch Chinese stocks even though they offer attractive single-digit multiples.

Why do you care? Because China is the world’s largest consumer and importer of most commodities, food, and energy. The stocks that specialize in these areas could be facing a long-term drag from the Middle Kingdom unless it is offset somewhere else.

The Chinese are only now discovering that the principal driver of their economic growth for the past 30 years has been US investment. President Xi has managed to scare that away with a hostile attitude towards America and saber-rattling over Taiwan. Last year for the first time the US imported more from Mexico than from China, where many companies have re-shored.

Wonder why crude oil (USO), (XOM), (OXY) is at $68 a barrel when the US economy is growing at a 3.1% rate? This is the reason. It is also a strong argument in favor of investing in India, which I discussed last week. Buy the (INDA) and the (INDY), not the (FXI) or (BABA).

In the meantime, you’ve got to love ARM Holdings PLC, whose earnings announcement triggered a heroic 56% one-day move up in the stock. They execute sub-designs for almost every AI chip out there. That’s what a 3% float in the stock gets you. Anyone who has any doubts about the durability of the AI story should take a look at what happened to (ARM) last week.

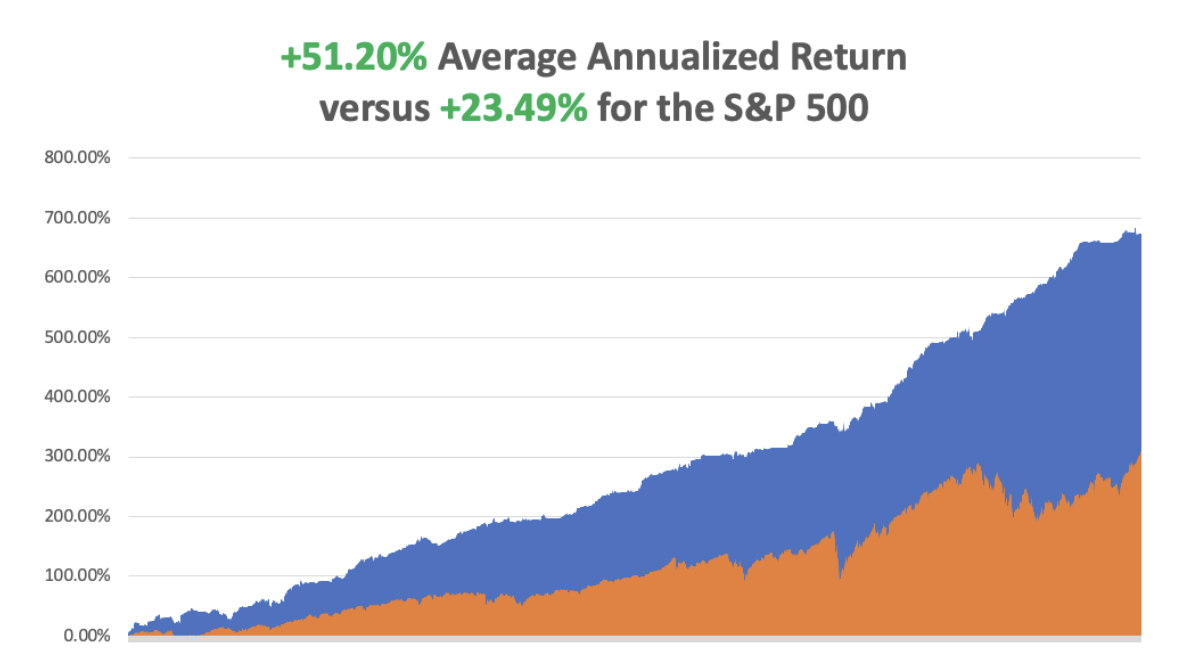

So far in February, we are up +1.78%. My 2024 year-to-date performance is also at -2.50%.The S&P 500 (SPY) is up +5.03%so far in 2024. My trailing one-year return reached +60.44% versus +33.13%for the S&P 500.

That brings my 16-year total return to +674.13%. My average annualized return has retreated to +51.20%.

Some 63 of my 70 trades last year were profitable in 2023.

I am maintaining longs in (MSFT), (AMZN), (V), (PANW), and (CCJ).

Reheating is Becoming an Issue, with a strong US economy and record-low unemployment rate possibly prompting the Fed to delay interest rate cuts. The stock market has been running on steroids on the expectation of imminent cuts. This is a new market risk and could unleash a thunderstorm on our parade.

CPI Revised Down, in December, from 0.3% to 0.2%. The deflationary economy is back! Stocks loved it, with the S&P 500 catapulting to $5,000. That’s why I revised my yearend target up to $6,000.

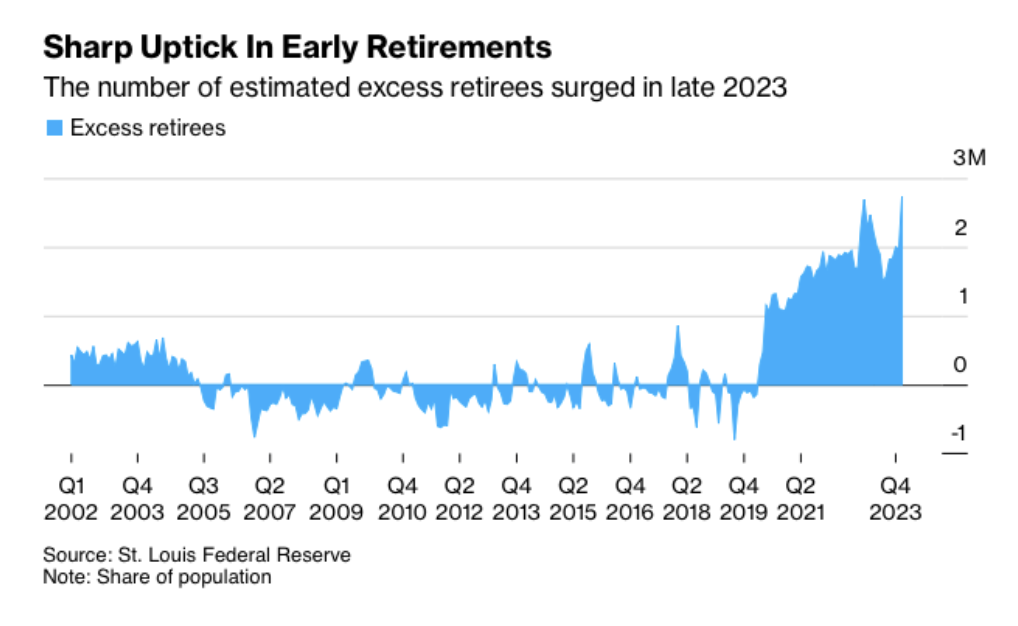

Early Retirements are Soaring, thanks to a stock market at new all-time highs. Baby boomers can now afford to “take this job and shove it.”

NVIDIA Enters New Custom Chip Market, potentially adding another $30 billion in revenues. The dominant global designer and supplier of AI chips aim to capture a portion of an exploding market for custom AI chips and to protect itself from the growing number of companies interested in finding alternatives to its products. Buy (NVDA) on dips.

Morgan Stanley Upgrades NVIDIA to an $800 Target. An exceptional supply-demand imbalance in the artificial intelligence-chip sector, as well as a massive shift in spending toward emerging technology, is likely to persist over the near term. Buy (NVDA) on dips.

ARM Holdings (ARM) Soars by 41%, off a spectacular forecast-based demand for designed-up AI chips. UK-based Arm makes money through royalties, when companies pay for access to build Arm-compatible chips, usually amounting to a small percentage of the final chip price. Arm said its customers shipped 7.7 billion Arm chips during the September quarter.

Tesla (TSLA) Looking to Cut Jobs, and reduce costs, as is the rest of Silicon Valley. The move could mark the bottom of the stock. Elon Musk is the master job cutter, axing 80% of the Twitter staff on takeover.

Meta (META) Gains $196 Billion in Market Cap in One Day, off the back of record sales, tripled earnings, and reduced costs.

Construction Spending Gains, up 0.9% in December, the best since October. Watch the industry reaccelerate as interest rates fall.

Royal Caribbean Beats, with record bookings in an industry I have recently become intensely interested in. (RCL) is grabbing market share from land-based vacations, as Millennials are finally discovering cheap cruise vacations, where it is often cheaper than to stay in a motel with all you can eat. Only a few cruises were lost to the Red Sea War. (RCL) just launched Icon of the Seas, the world’s largest cruise ship.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, February 12, the US Consumer Inflation Expectations are announced.

On Tuesday, February 13 at 8:30 AM EST,the Core Inflation Rate will be released.

On Wednesday, February 14 at 2:00 PM, the Producer Price Index is published. The Federal Reserve announces its interest rate decision.

On Thursday, February 15 at 8:30 AM, the Weekly Jobless Claims are announced. We also get Retail Sales.

On Friday, February 16 at 2:30 PM, the January Building Permits are published, along with the University of Michigan Consumer Sentiment. At 2:00 PM the Baker Hughes Rig Count is printed.

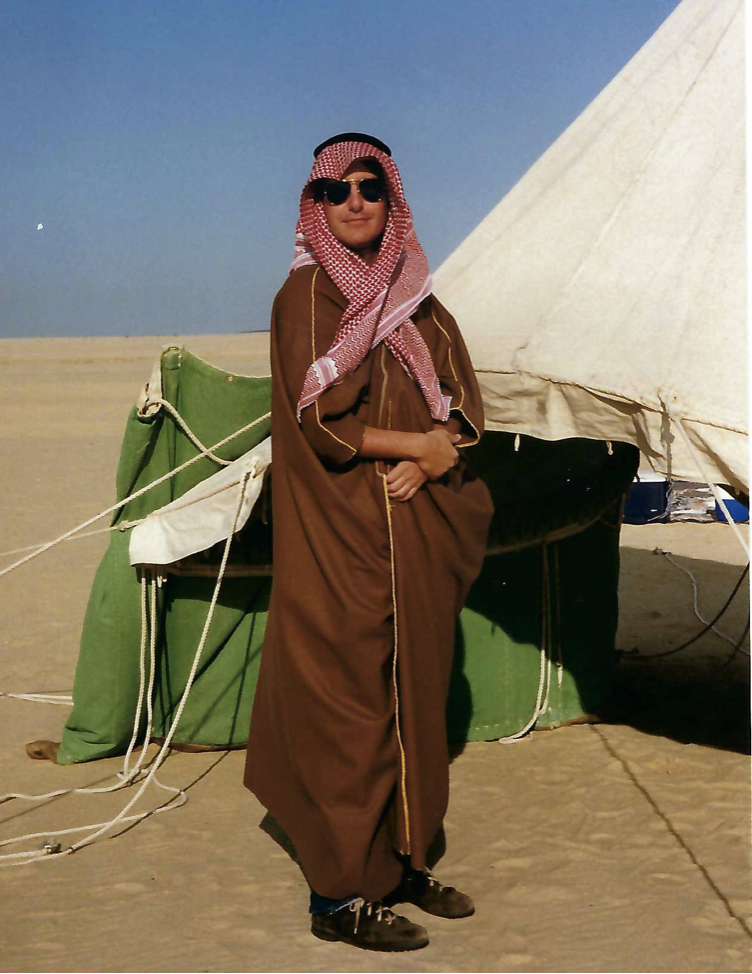

As for me,it was in 1986 when the call went out at the London office of Morgan Stanley for someone to undertake an unusual task. They needed someone who knew the Middle East well, spoke some Arabic, was comfortable in the desert, and was a good rider.

The higher-ups had obtained an impossible-to-get invitation from the Kuwaiti Royal family to take part in a camel caravan into the Dibdibah Desert. It was the social event of the year.

More importantly, the event was to be attended by the head of the Kuwait Investment Authority, who ran over $100 billion in assets. Kuwait had immense oil revenues, but almost no people, so the bulk of their oil revenues were invested in western stock markets. An investment of goodwill here could pay off big time down the road.

The problem was that the US had just launched air strikes against Libya, destroying the dictator, Muammar Gaddafi’s royal palace, our response to the bombing of a disco in West Berlin frequented by US soldiers. Terrorist attacks were imminently expected throughout Europe.

Of course, I was the only one who volunteered.

My managing director didn’t want me to go, as they couldn’t afford to lose me. I explained that in reviewing the range of risks I had taken in my life, this one didn’t even register. The following week found myself in a first-class seat on Kuwait Airways headed for a Middle East in turmoil.

A limo picked me up at the Kuwait Hilton, just across the street from the US embassy, where I occupied the presidential suite. We headed west into the desert.

In an hour, I came across the most amazing sight - a collection of large tents accompanied by about 100 camels. Everyone was wearing traditional Arab dress with a ceremonial dagger. I had been riding horses all my life, camels not so much. So, I asked for the gentlest camel they had.

The camel wranglers gave me a tall female, which was more docile and obedient than the males. Imagine that! Getting on a camel is weird, as you mount them while they are sitting down. My camel had no problem lifting my 180 pounds.

They were beautiful animals, highly groomed, and in the pink of health. Some were worth millions of dollars. A handler asked me if I had ever drunk fresh camel milk, and I answered no. They didn’t offer it at Safeway. He picked up a metal bowl, cleaned it out with his hand, and milked a nearby camel.

He then handed me the bowl with a big smile across his face. There were definitely green flecks of manure floating on the top, but I drank it anyway. I had to, lest my host would lose face. At least it was white. It was body temperature warm and much richer than cow’s milk.

The motion of a camel is completely different from a horse. You ride back and forth in a rocking motion. I hoped the trip was short, as this ride had repetitive motion injuries written all over it. I was using muscles I had never used before. Hit your camel with a stick and they take off at 40 miles per hour.

I learned that a camel is a super animal ideally suited for the desert. It can ride 100 miles a day, and 150 miles in emergencies, according to TE Lawrence, who made the epic 600-mile trek to Aquaba in only four weeks in the height of summer. It can live 15 days without water, converting the fat in its hump.

In ten miles, we reached our destination. The tents went up, clouds of dust rose, the camels were corralled, and the cooking began for an epic feast that night.

It was a sight to behold. Elaborately decorated huge three-by-five wide bronze platers were brought overflowing with rice and vegetables, and every part of a sheep you can imagine, none of which was wasted. In the center was a cooked sheep’s head with the top of the skull removed so the brains were easily accessible. We all ate with our right hands.

I learned that I was the first foreigner ever invited to such an event, and the Arabs delighted in feeding me every part of the sheep, the eyes, the brains, the intestines, and the gristle. I pretended to love everything and laid back and thought of England. When they asked how it tasted I said it was great. I lied.

As the evening progressed, the Johnny Walker Red came out of hiding. Alcohol is illegal in Kuwait, and formal events are marked by copious amounts of elaborate fruit juices. I was told that someone with a royal connection had smuggled in an entire container of whiskey and I could drink all I wanted.

The next morning I was awoken by a bellowing camel and the worst headache in the world. I threw a rock at him to get him to shut up and he sauntered over and peed all over me.

The things I did for Morgan Stanley!

Four years later, Iraq invaded Kuwait. Some of my friends were kidnapped and held for ransom, while others were never heard from again.

The Kuwaiti government said they would pay for the war if we provided the troops, tanks, and planes. So they sold their entire $100 million investment portfolio and gave the money to the US.

Morgan Stanley got the mandate to handle the liquidation, earning the biggest commission in the firm’s history. No doubt, the salesman who got the order was considered a genius, earned a promotion, and was paid a huge bonus.

I spent the year as a Marine Corps captain, flying around assorted American generals and doing the odd special opp. I got shot down and still set off airport metal detectors. No bonus here. But at least I gained an insight and an experience into a medieval Bedouin lifestyle that is long gone.

They say success has many fathers. This is a classic example.

You can’t just ride out into the Kuwait desert anymore. It is still filled with mines planted by the Iraqis. There are almost no camels left in the Middle East, long ago replaced by trucks. When I was in Egypt in 2019, I rode a few mangy, pitiful animals held over for the tourists.

When I passed through my London Club last summer, the Naval and Military Club on St. James Square, whose portrait was right at the front entrance?None other than that of Lawrence of Arabia.

It turns out we were members of the same club in more ways than one.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

John Thomas of Arabia

Checking Out the Local Camel Milk

This One Will Do

Traffic in Arabia

https://www.madhedgefundtrader.com/wp-content/uploads/2024/02/John-Thomas-of-Arabia.png974752april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-12 09:02:392024-02-12 11:11:57The Market Outlook for the Week Ahead, or Raising my Yearend Target to (SPX) $6,000

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.