Mad Hedge Technology Letter

February 2, 2022

Fiat Lux

Featured Trade:

(GOOGLE IS STILL ON SALE)

(GOOGL), (ARKK), (MSFT), (AAPL)

Mad Hedge Technology Letter

February 2, 2022

Fiat Lux

Featured Trade:

(GOOGLE IS STILL ON SALE)

(GOOGL), (ARKK), (MSFT), (AAPL)

Google (GOOGL) shares were up 65% last year and I would still call the name cheap in 2022.

It’s interesting for me to see ARK (ARKK) Funds CEO Cathy Woods claim that growth is on sale now.

I take the other side of the argument and would pontificate that quality is for sale, like Google, who has carved out an unrivaled position in the digital ad space.

Their cash cow business is so effective that they are set to achieve $100 billion in free cash flow by 2023.

It’s mind-boggling that a company of this magnitude still trades at a discount even though generating more free cash flow than Apple (AAPL) and Microsoft (MSFT).

Google’s ad revenue was up to $61 billion which was up from $46 billion last year.

These numbers are staggering because of the sheer math it takes to jump to 33% when we are talking about over $50 billion.

Google is so big that the law of large numbers works against them, but they still shrug that off and register these outlandish numbers.

This company is one of the sure-fire bets in tech along with Microsoft and it’s no surprise that the best companies are taking the rest of the market on their back to diffuse this recent volatility.

The plaudits don’t stop there with their critical cloud division growing 45% year over year to $5.5 billion.

The cloud and ad revenue serve as the structural stabilizers to a healthy business and all signs point to Google having tremendous value as a stock.

Google also announced a 20:1 stock split which should allow investors with smaller bank accounts access to the stock.

Apple and Tesla saw huge inflows after they announced stock splits and I see no reason why this should be different for Google.

Fortunately, it appears that supply chain bottlenecks aren’t materially damaging Google’s ad demand.

Now Google is on the verge of cruising by $2 trillion in market cap.

Since we are in a market where outperformers are rewarded, Google is in great shape for 2022 when supply chain problems are set to improve.

I have repeatedly said to stay away from those companies that cannot meet expectations and aren’t cash flow-positive.

There is no more free money to subsidize poor management or a poor product or both.

When we analyze Google’s ad business from a microeconomic level, then it’s easy to understand that businesses cannot get rid of their services because of its deep application for consumers.

People also want deals.

They're looking for value.

For shoppers, Google made it possible to browse and discover the hottest deals for major moments like Black Friday and Cyber Monday on Google Search.

For merchants, Google made it even easier to list promotions via automated imports from third-party integrations like Shopify and WooCommerce.

Google is easily selling ad inventory, attracting new customers, and building brand loyalty.

In the holiday season, the number of merchants using promo features jumped 280% year over year.

Retailers are also turning to Google to help them transform and accelerate growth such as Warby Parker, who drove a 32% year-over-year increase.

They accomplished this by not only opening stores and expanding their contact lens business but also by tapping into Google across services.

Omnichannel bidding, smart shopping campaigns and an expanded presence in Google Maps to promote in-store eye exams contributed to Warby Parkers’ success.

Google is making it easier for viewers to buy what they see and simpler for advertisers to drive action with innovative solutions like product feeds and video action campaigns and emerging formats like live commerce.

Backcountry.com generated a 12-1 return on ad spend with product feeds in 2021 and plans to double its investment in 2022, while Samsung, Walmart, and Verizon partnered with creators to host shoppable holiday live stream events in the U.S.

In short, Google has pricing power, and its strategic position is such that it’s hard not to see rampant growth ahead in the short and long term.

Its cash position is enviable to any tech or non-tech company and at some point a dividend is inevitable.

Even with its success, Google is still investing aggressively for the future and is part of every cutting-edge technology from artificial intelligence to self-driving and even the metaverse.

Mad Hedge Technology Letter

January 28, 2022

Fiat Lux

Featured Trade:

(APPLE PUSHES THE ENVELOPE)

(MSFT), (AAPL), (GOOGL), (FB)

We can flip through the thesaurus to look for superlatives that would describe how Apple (AAPL) is performing versus the rest of the market or tech sector, yet it really doesn’t matter who we compare them to, because no matter what we do, somebody would need to be clinically insane to bet against this well-oiled machine.

To give credit where credit is due, Apple CEO Tim Cook parlayed his friendship with co-founder Steve Jobs into the top job at Apple precisely because he was and still very much is an operational specialist.

In times of pandemic, climate change, supply chain problems, hyperinflation, and geopolitical volatility, this is the man you want at the helm to make those operational decisions that benefit shareholders.

Cook even pulled off China and is the only person in Silicon Valley that can claim that level of tech success in the Middle Kingdom.

Not many US tech companies can outdo the Chinese in China, but that is what Cook has managed to achieve and that sometimes gets overlooked.

I have undeniably been a major skeptic about China, but he has managed to penetrate so deeply into Chinese culture that the Chinese can’t root him and his products out without massive disruption and possible social unrest.

Cook, being the operations guy that he is, told the media that he expects supply bottlenecks to ease, which is a major bullish signal to the rest of tech and the semiconductor industry.

That comment alone will mean that the Nasdaq will finish the year at least 7-10% higher than if he didn’t make that comment and to nobody’s surprise, Apple is trending higher by over 6% today and rightly so.

The market trusts Tim Cook and what he says, and I can’t say the same for Tesla’s Elon Musk who loves to overpromise and underdeliver.

This is also good news for the EV sector such as Lucid (LCID) and Rivian (RIVN) which I highlight as two stocks with massive potential even if they can’t ramp up to Tesla levels right away.

Optimizing the supply chain has never been more important today because of the de-globalized elements that have filtered through to corporate America.

Part of streamlining the operations helps when you are Apple and you are Tim Cook and you can negotiate contracts down to the fractional cent.

Other companies simply don’t have that negotiating leverage.

They have curried together that type of goodwill that Apple has with their brand name and footprint.

Moving forward, the best way to decode the content of Apple’s earnings report is by viewing it as an equivalent to an implicit guarantee that margins and operations will be running smoothly for the rest of the year.

That in itself carries more weight than the Fed supplying capital for zombie companies.

I keep mentioning that this is the era in which the balance sheet matters; and wow, Apple has a crystal clean sheet that almost doesn’t need balancing.

Apple’s optionality is just mind-boggling from unlimited buybacks, to possibly raising their dividend from 22 cents, to hiring and expanding their workforce, adding more data centers, and so on.

They literally have any tool in the tool kit to respond to any possible headwind.

That is a luxury that most tech companies cannot claim to possess aside from a handful.

As Microsoft reported stellar earnings, this is just another feather in the cap for big tech.

Big tech is protected from the carnage that smaller tech companies must face, and who have less options to remediate possible devastating internal or external threats.

Not only is Apple riding high on their horse at the vanguard, but they possess products and software that simply can’t be substituted out, which easily creates an overwhelming strong hand when it comes to pricing power.

Next in the queue with earnings is Alphabet (GOOGL), where I fully expect them to reveal record earnings. Facebook (FB) too should do well, but not as good as GOOGL.

Don’t bet against Goliath.

Mad Hedge Technology Letter

January 26, 2022

Fiat Lux

Featured Trade:

(MSFT DIGS US OUT OF A HOLE)

(MSFT), (AMZN), (GOOGL), (AAPL)

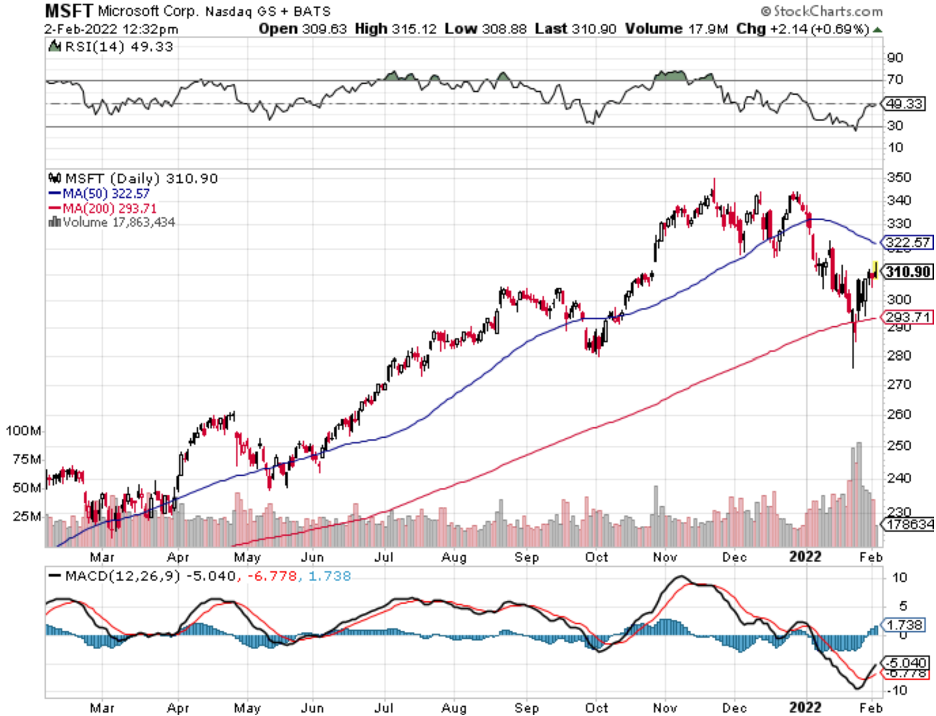

The 14% selloff year to date in tech shares finally met its match when Microsoft (MSFT) soothed us with its most recent quarterly performance.

It’s starting to feel like a broken record, but this world belongs to 5 large Silicon Valley tech companies and for the rest of the other few hundred publicly listed companies, we are just living in their world.

And it just so happens that if anybody or anyone is anointed as the savior to save this market from capitulating, it has to be the heavy lifters and we are getting validation from the strongest of cloud/enterprise companies.

Just as resonating, MSFTs positive quarter draws yet one more line in the sand for Mr. Market, offering us support and offering us evidence this could morph into a short-term bottom.

Even more salient, this is even deeper evidence that the software sector is the cream of the crop in tech and their strategic position is only getting stronger.

The thing that these guys have that is critical in today’s economic environment is tinged with inflation headwinds — pricing power.

Starting in March, Microsoft is pushing through an MSFT 365 price hike and consumers and businesses will see their monthly bill go up a few bucks.

According to Microsoft, those increases will apply globally with local market adjustments for certain regions.

And it’s not that 365 is MSFT's cutting edge division, it’s just another example of how MSFT can raise prices and consumers have no other choice but to comply because, at this point, 365 is a utility.

Sure, you can find a substitute, but it wouldn’t be as good of a product.

It was a record quarter, driven by the continued strength of the Microsoft Cloud, which surpassed $22 billion in revenue, up 32% year over year. We are living through a generational shift in our economy and society. Digital technology is the most malleable resource at the world's disposal to overcome constraints and reimagine everyday work and life.

Anyone who bet the ranch on the cloud and enterprise is happy they bet the ranch on it.

MSFT's earnings were just a giant confirmation of how tech won’t be knocked off its perch as the apex warrior, not only in the Nasdaq index but the broader market.

The stock market has been a tech market for quite a few years and that can’t be ignored or discounted.

Fundamentally, the foundations of profitable tech stocks have never been healthier, and they are extracting more of the pie than ever.

Then as we hear nonstop about the upcoming metaverse project and its entryways through gaming, MSFT is so on top of that new development that they will put all other companies to shame.

Granted, there are other heavyweights like Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL) that MSFT must take measures of to see if they are pushing ahead with something they are unaware of, but all is good is Redmond, Washington.

As data volumes and transactions increased over 100% year over year, MSFT has a grip on what’s going on and can quickly pivot to anything that’s worth it with its army of high-quality developers.

MSFT’s ubiquitous fingerprints are everywhere with even over 90% of Fortune 500 companies using Teams Phone this past quarter highlighting the deep penetration into the richest corners of corporate America.

My overarching point is that MSFTs products aren’t just a one-trick pony ala Facebook.

More than half of customers have four or more MSFT workloads, up 75% year over year, underscoring MSFTs end-to-end differentiation.

On a short-term trading basis, traders must adopt tech winners with robust balance sheets, and this must be looked at as a dealbreaker or deal winner of sorts.

In a world that is clamoring for quality tech names, it’s no time to allocate your hard-earned savings into Podunk technology.

Once the macro washout fades, pile into MSFT!

What I am saying is that there is a great deal of the market to plain out avoid, and don’t get caught up in those lemons.

Mad Hedge Technology Letter

January 24, 2022

Fiat Lux

Featured Trade:

(BEST OF THE REST GETS SLAUGHTERED)

(MSFT), (SNAP), (GOOGL), (AAPL), (AMZN), (FB), (TIKTOK)

Popular nostrum has it that earnings will save the stock market.

The strength of corporate America time and time again is on display to show investors how high short-term growth follows through.

Anytime the Nasdaq enters a little rut, earnings bail us out and the next move is usually higher for tech shares.

Well, wait a second, things are different this time.

The bad news now is that confirmation of solid fundamentals during the upcoming earnings season, won’t make the Nasdaq index go higher.

The market is pricing in business as usually for the largest 5 tech stocks which are really the only ones that matter.

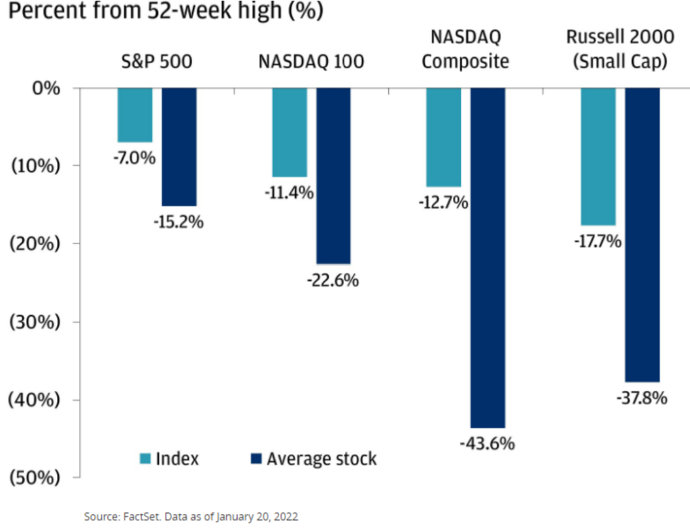

Internally, the rest of tech has been deeply damaged by this January sell-off and we are talking about 8-9% one-day sell-offs for the small cap tech growth and I haven’t even mentioned the peak to trough underperformance which is much worse.

Larger cap Enterprise and Cyber Security stocks still boast solid foundations and are going down less than the meme stocks, shelter-at-home stocks, and the best of the rest tech stocks.

Basically, we need to get through earnings because there is minimal upside for tech stocks as investors peruse through a lack of short-term catalysts.

We are stuck in a ditch where monetary and fiscal policy has been set dead straight against an environment of potentially appreciating tech stocks.

Until that changes, I don’t envision a snappy reversal apart from a dead cat bounce to sell into.

Chasing growth in a low-interest rate environment gave us an overshoot to the upside and now that is all working in reverse.

And for the big FANG stocks outperforming small cap, it just means shares are performing better than tech growth because they command lower volatility due to stronger balance sheets.

Resilience to indiscriminate selling is currency in today’s trading world.

Nothing wrong with growth, but they are what they are, so much so that if you cannot generate profitability now, sell-offs are indicative of their poor strategic position among bigger tech.

The carnage under the hood is stark today with Snap stock cratering after the social media company’s shares were downgraded amid risks to revenue growth and tough competition from rival TikTok.

Snap’s headwinds result from a weakening business profile stemming from IDFA headwinds, difficult [year-over-year comparisons] from stellar growth in 2020-21, and increasing competition from TikTok.

IDFA is a serious thorn in the side for the android-based systems of Google as well as for Facebook.

IDFA is Apple minimizing the reach of data harvesting platforms by turning off their data reach and these modifications by Apple (AAPL) to rules for advertising on mobile apps have forced companies like Snap to lower guidance.

When it reported quarterly earnings last October, Snap revealed that the impact on its advertising business could be long lasting and now we are experiencing that.

The IDFA issues could cut growth rates by half as these social media firms have been unable to remedy its loss of reach in digital advertising.

Snap has the unenviable position to not only be behind Google and Facebook, but they are also the next company to be upended by TikTok that has really come on the last few years.

TikTok has supplanted Snap as the go-to social media platform for teens and young adults.

In a rising interest rate environment, the best of the rest like Snap gets punished for not being the best of class.

Snap shares are down over 200% from its peak and threatening to close in on 300% in the red.

Snap represents the fortunes for the marginal tech stocks that rely on growth and that is not working in 2022.

Although not as loss-making as other tech growth, SNAP has been fairly pigeonholed as the tech you don’t want to own now.

It’s a dangerous position to fill in times of the VIX spiking to 30.

The problems don’t stop there with TikTok really threatening Snap’s position and the momentum signaling that Snap is prepared for a deeper slowdown than initially expected.

Snap’s foothold is strongest in the 13-34-year-old range in the U.S., Canada, the U.K., France, Australia, and the Netherlands, but TikTok’s audience is the most similar to Snap’s which means it puts both Snap’s user face time spent and ad dollars at risk.

From a monetary standpoint, digital advertisers will start to play off ad competition between TikTok and Snap, resulting in discounted ad revenue per unit which will narrow margins moving forward.

Not being able to command the prior ad premium is a stinging blow to Snap who thought they were in the driving seat to the third position behind Google and Facebook, but it shows that being a tech minnow is a harrowing experience and fending off toxicity is part of the playbook just to survive.

Head to higher waters in this volatile environment.

Mad Hedge Technology Letter

January 21, 2022

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO LAP UP AT THE BOTTOM)

(MSFT), (TSLA), (GOOGL), (AAPL), (AMZN)

Tech has led the way to the downside as the macro picture sours in the short term.

Valuations have come down from the nosebleed levels and now is the time to pick and choose where to allocate capital for the next leg up in tech.

Avoiding growth tech is something that should be stapled to your bedpost, loss-making companies won’t be able to compete with more established revenue models.

You don’t want to catch a falling knife, but at the same time, diligently prepare yourself to buy the best discounts of the year.

Here are the names of five of the best stocks to slip into your portfolio in no particular order when we find a bottom.

Remember, tech ALWAYS comes back.

Apple

Steve Job’s creation is weathering the gale-force storm quite well. Apple has been on a tear reconfirming its smooth pivot to a software service tilted tech company. The timing is perfect as China has enhanced its smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality.

That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has their supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and will gobble up a total of $200 billion in shares by the end of 2021. Get into this stock while you can, as entry points are few and far between.

Oh, and their 5G phone is selling like hotcakes. Some one billion need to be replaced to bring consumers into the new high speed 5G world.

Amazon (AMZN)

This is the best company in America, hands down, and commands 5% of total American retail sales or 49% of American e-commerce sales. The pandemic has vastly accelerated the growth of their business.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then, oozing innovation, and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart doorbell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft (MSFT)

The optics in 2021 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter -- and that is a good thing.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies, especially retailers.

Microsoft is also on the vanguard of the gaming industry and deals like the $86 billion purchase of Activision (ATVI) mean that it will be difficult for another company to loosen MSFTs stranglehold at the top of the gaming ladder.

Alphabet (GOOGL)

Alphabet and Facebook boast a strong duopoly of ad technology. Alphabet generated 80% of its revenue from Google's advertising services in 2020. Google's non-advertising businesses (including subscriptions and hardware) accounted for 12%, while another 7% came from Google Cloud.

Alphabet's total revenue rose 13% in 2020, even as the pandemic throttled the growth of Google's advertising business in the first half of the year. The growth of Google Cloud throughout the year also cushioned that blow.

Google's advertising business recovered in the second half of the year, and Alphabet's operating margin expanded from 21% in 2019 to 23% in 2020. Its diluted earnings per share (EPS) also grew 19%.

In the first nine months of 2021, Alphabet's revenue rose 45% year over year as Google's advertising and cloud business grew in tandem.

Its array of different businesses like LinkedIn, YouTube, and Google Maps means this revenue pipeline is as fertile as can be.

Google’s robust balance sheet will protect itself from any downtrend in business that they might ever suffer.

Tesla (TSLA)

The influential EV leader has really surged ahead of the competition during the pandemic.

Demand for its product is off the charts as they delivered 184,800 Model 3 and Model Y cars in the first quarter, beating expectations and setting a record for Tesla.

However, the company also said it produced none of its higher-end Model S sedans or Model X SUVs for the period ending March. It delivered 2,020 older Model S sedans and Model X SUVs from inventory.

Supply chain issues are likely to remain a challenge for Tesla this year as many EV makers are having a hard time sourcing semiconductor chips.

Tesla is now aiming to produce 2,000 Model S and X vehicles per week later this year.

The company said Monday it expects more than 50% vehicle delivery growth in 2021 overall, which implies minimum deliveries of around 750,000 vehicles this year.

This stock is a must-buy when tech reverses.