Mad Hedge Technology Letter

March 18, 2019

Fiat Lux

Featured Trade:

(WHY ALPHABET IS THE BEST FANG TO BUY NOW),

(GOOGL), (NFLX), (FB), (TWTR), (DIS)

Mad Hedge Technology Letter

March 18, 2019

Fiat Lux

Featured Trade:

(WHY ALPHABET IS THE BEST FANG TO BUY NOW),

(GOOGL), (NFLX), (FB), (TWTR), (DIS)

Why am I bullish on Alphabet (GOOGL) short-term?

Video has muscled its way to the peak of the digital content value chain.

If you don't have video streaming, then you are significantly depriving yourself of the necessary ammunition capable of battling against legitimate content originators.

The optimal type of content is short form yet engaging.

Interesting enough, the format method integrated into systems of Facebook (FB) and Twitter (TWTR) has experienced unrivaled success.

They have been leaning on this model as growth levers that will take them to the next stage of revenue acceleration and rightly so.

This has seen smartphone apps such as Instagram become game-changing revenue machines destroying all types of competition.

The x-factor that stands out in Instagram's, Facebook’s, YouTube’s model is that it's free and they do not absorb heavy expenses from content creation.

It’s certainly cheap when the user is the product.

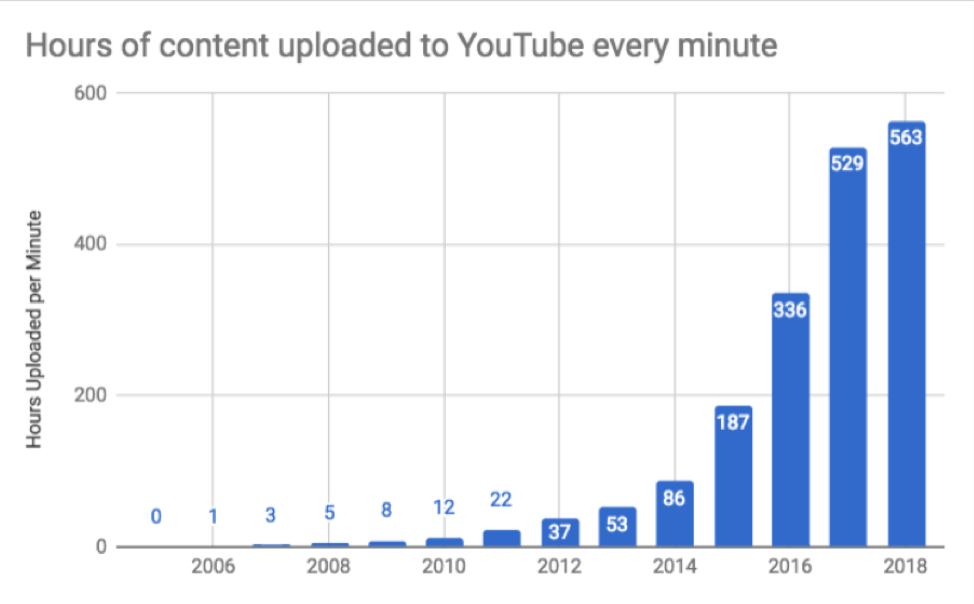

Google’s YouTube service has morphed into something of a phenomenon.

Its interface is easy to use, and followers have a simple time navigating around its platform.

Familiar news outlets such as Sky News, Bloomberg News, and even CNBC news have recently installed their live feeds on YouTube's main platform scared of losing aggregate eyeballs.

And even more intriguing is that YouTube has become a legitimate competitor to Netflix's (NFLX) online video streaming platform.

YouTube has sensed the outsized pivot to their free platform and has double down hard by installing 5-second ads at the front end and middle of videos.

Of Alphabet’s total $39.3 billion revenue pocketed in Q4 2018, ads constituted 83% or an astounding $32.6 billion.

I feel that Alphabet shares are currently undervalued, and I believe that we will see outperformance from Alphabet shares for the rest of 2019 based on YouTube's performance relative to expectation.

YouTube’s ever-growing presence showing up in the top line will offer the growth investors desire to pile into these shares as the company wrestles with future projects such as Waymo.

That's not to say that their traditional advertisement business of Google Search is failing.

Investors can expect continuous 20% to 25% growth in this cash cow business, but the reason why Alphabet share has not been able to break out is that investors have baked this into the pie.

Therefore, YouTube is really the X Factor and will take them to this new promised land with shares surging past the $1,250 mark and more importantly, staying at that level.

YouTube brought in about $15 billion in 2018 and that consisted of about 10% of Alphabet’s total annual revenue.

However, the company is just scratching its surface of what it can accomplish with this fast-growing revenue driver and I can extrapolate this growth segment turning into 20% or 25% of the company’s annual revenue in the next few years.

Google does not strip out YouTube revenue in its reporting, therefore, it's difficult to put my finger on exactly how much YouTube is carving out in terms of revenue.

I can also assume that if Netflix continues to raise the cost of monthly subscription, this strategy will directly hurt its revenue acceleration ability as it relates to competing with Google's YouTube because YouTube's free service is demonstrably attractive to viewers hoping to discover high-quality content relative to a $20 per month Netflix subscription.

I do agree that Netflix is a great company and a great stock, but as they slowly raise the price of content, this will gift YouTube a huge chunk of Netflix’s marginal audience freeing itself from the shackles of Netflix’s price rises.

At some point, online video streaming will become as expensive as the cable bundles now, and at that point, we know that saturation is imminent boding negative for Netflix.

What I do envision in the short-term future are consumers in America will pay into several unique bundles such as Netflix, maybe Disney (DIS), ESPN and merely stick with these as their base content generators as more consumers cut their cord and hard pivot from traditional cable packages that are becoming less appealing by the day.

And don't forget that at some point, Netflix will have to demonstrate profitability and the huge cash burn that permeates throughout the business will be exposed when subscription growth starts to fade away.

In every possible variant, YouTube will become an outsized winner in the media wars because the quality of the free content keeps improving, the cost for consumers stays at 0, and their best of breed ad tech migrating from their Google search into YouTube just keeps getting more surgical and efficient.

Not only are the positive synergies from the best of breed ad tech aiding YouTube’s model, but just think about YouTube having access to the Google cloud and saving expenses by accessing this function to store data onto the Google Cloud.

If this was a standalone service, they would have to subcontract cloud storage functions to third-party cloud company causing the content service to spend millions and millions of dollars per year in expenses.

This would have the potential of crushing the bottom line.

That is just one example of the synergies that Google can take advantage of with YouTube under its umbrella of assets.

And think about self-driving vehicles, Google could potentially equip YouTube as a pre-programmed application inside of autonomous vehicle platform tech with YouTube popping up on the multiple screens.

I assume that there will be multiple screens inside of cars with self-phone driving technology because of the lack of driving required.

The worst maneuver that Alphabet could do right now is spinoff YouTube into its own company, and if that happens, YouTube won't be able to take advantage of the various synergies and benefits of being an Alphabet asset.

We are just scratching the surface of what YouTube can accomplish, and I believe this upcoming overperformance isn’t in the price of the stock yet.

If the Fed continues its “patient” strategy towards interest rates at a macro level, Alphabet will easily soar past $1,250 and it can easily gain another 10% in 2019.

If any “regulation” risk as a result of extremist content rears its ugly head, buy shares on the dips because the algorithms are in place to eradicate this material and any fine will be manageable.

Mad Hedge Technology Letter

March 12, 2019

Fiat Lux

Featured Trade:

(FIREEYE’S LAST LINE OF DEFENSE),

(FEYE), (MSFT), (AMZN), (GOOGL), (ORCL), (EFX), (IBM)

A potential cataclysmic threat potentially wreaking havoc to our financial system is no other than cybercrime – that is one of the few gems that Fed Chair Jerome Powell delivered to the American public in a historic interview with 60 Minutes this past weekend.

Powell has even gone on record before claiming that Congress should do “as much as possible (against cybercrime), and then double it.”

The Fed Chair clearly has intelligence that retail investors wish they could get their hands on.

Digital nefarious attacks have been all the rage resulting in public blowups at Equifax (EFX) and North Korea’s state-sponsored hack on International Business Machines Corporation (IBM) just to name a few.

At the bare minimum, this means that cybersecurity solution companies will be the recipients of a gloriously expanding addressable market.

Powell’s testimony to the public was timely as it provides the impetus for investors to look at cybersecurity firms that will actively forge ahead and protect domestic business from these lurking threats.

Considering a long-term investment in FireEye Inc. (FEYE) at these beaten down prices could unearth value.

For all the digital novices, FireEye offers cybersecurity solutions allowing organizations to pre-emptively plan, prevent, respond to, and remediate cyber-attacks.

It offers vector-specific appliance, virtual appliance, and a smorgasbord of cloud-based solutions to detect and thwart indistinguishable cyber-attacks.

The company deploys threat detection and preventative methods including network security products, email security solutions, and endpoint security solutions.

And when you marry this up with my 2019 underlying thesis of the year of the enterprise software subscription, this company is on the verge of a breakout.

Last year was a year full of milestones for the company with the firm achieving non-GAAP profitability for the full year for the first time and generating positive operating and free cash flow for the full year.

The company was able to attract new business by adding over 1,100 new customers.

The cloud is where the company is betting all their chips and crafting the optimal subscription-as-a-service (SaaS) product is the engine that will propel the company’s shares higher.

The heart of their cloud initiative relies on Helix - a comprehensive detection and response platform designed to simplify, integrate and automate security operations.

This intelligence-led approach fuses innovative security technologies, nation-grade FireEye Threat Intelligence and world-renowned expertise from FireEye Mandiant into FireEye Helix.

By enhancing the endpoint products and email protection, sales of both products exploded higher by double digits YOY as FireEye successfully displaced incumbent vendors and legacy technology to the delight of shareholders.

As a result, the firm’s pipeline of opportunities continues to build.

As for network security, FireEye plans to extend the reach of their market-leading advanced threat protection capabilities further into the cloud with protection specifically aimed for cloud heavyweights Microsoft (MSFT) Azure, Amazon Web Services (AWS), Google (GOOGL) and Oracle (ORCL) Cloud.

They are collaborating with these major cloud providers on hybrid solutions that integrate seamlessly with their technologies so FireEye solutions will easily snap into a customer's cloud deployments.

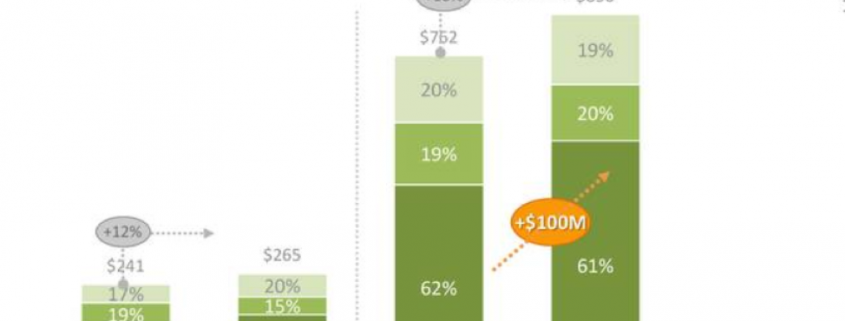

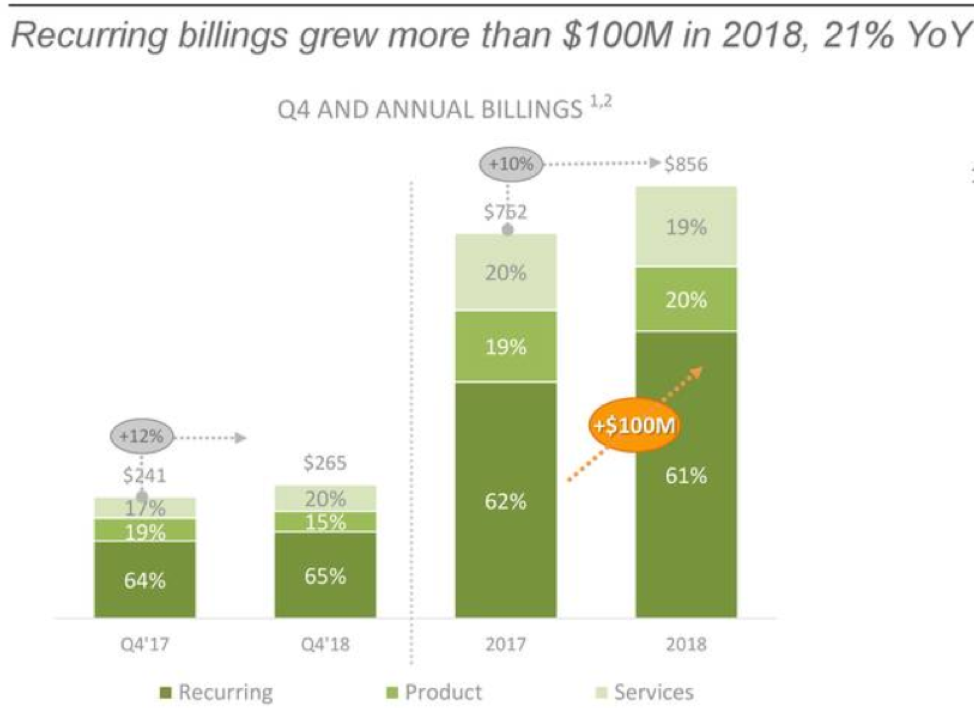

Cloud subscriptions and managed services were the ultimate breakout performer highlighting the successful outsized pivot to (SaaS) revenue.

This segment increased 31% sequentially and 12% YOY, highlighting underlined strength in the segments of managed defense, standalone threat intelligence, Helix subscriptions, and cloud email solution.

The furious growth was achieved even though Q4 2017 billings included a $10 million plus transaction and if this deal is excluded, cloud subscriptions and managed services would have grown more than 30% YOY in Q4 2017 demonstrating the hard bias to the cloud has been highly instrumental to its success.

Recurring billings expanded 12% YOY, a small bump in acceleration from 11% in Q3, but if you remove that big deal in Q4 '17, recurring billings grew over 20% YOY in Q4 2018.

The growing chorus of product satisfaction can be found in the customer retention rate of 90%.

Transaction volume was at record levels for both deals greater than $1 million and transactions less than $1 million, signaling not only that customer renewals are expanding, but also explosion of new revenue streams captured by FireEye is aiding the top line.

This story is all about the recurring revenue and I expect that narrative to perpetuate throughout 2019 as an overarching theme to the strength of the firm’s revenue drivers.

The 10% billings growth last quarter paints a more honest trajectory of the true growth proposition for FireEye.

I believe the 6%-to-7% revenue guide for fiscal 2019 is down to the accounting technicals manifesting in the appliance revenue that is fading from the overall story.

The solid billings growth underpinning the overall business meshing with diligent expense control is conjuring up a massive amount of operating leverage.

Shares are undervalued and offer an attractive risk versus reward proposition.

If the company delivers on its core growth outlook, which I fully expect them to do plus more, shares should climb over $20 barring any broad-based market meltdowns.

I am bullish FireEye and urge readers to wait for shares to settle before putting new money to work.

Mad Hedge Technology Letter

March 11, 2019

Fiat Lux

Featured Trade:

(THE BEST TECH PLAY IN HEALTHCARE),

(ISRG), (GOOGL), (JNJ)

Seeking for a great long-term buy and hold tech name?

Then look no further than Intuitive Surgical, Inc. (ISRG).

Intuitive Surgical develops and produces robotic products designed to enhance clinical outcomes for patients through minimally invasive surgery, its most well-known product is the da Vinci surgical system.

Healthcare is one sector that I have rarely touched on, but not only will this cross-pollination with tech serve a social good, investors have a chance to rake in future profits.

The da Vinci systems and Intuitive Surgical are the best of breed and have had almost zero competition in the past 20 years.

The systems are placed in operating room used for invasive surgery for various types of ailments from cancer to hernia, and the systems were successfully used over one million times for surgery last year.

The da Vinci systems aren’t cheap – they cost $1.5 million and the customers, usually the hospitals, buy the add-ons of extra parts and supplies that inflate the price another $1,900.

As you would expect, net profit margins are compelling, being over 30% which e-commerce companies would give a left leg for translating into numbers that make the company incredibly profitable.

The story of the da Vinci systems starts way back in the 80s with the Defense Advanced Research Projects Agency (DARPA) hoping it could figure out how to offer surgeons the ability to operate remotely on soldiers wounded on the battlefield.

SRI International (SRI), an American nonprofit scientific research institute and organization took the painstaking time to develop the technology.

SRI's intellectual property was eventually acquired in 1994 and incorporated a new company named Intuitive Surgical Devices by the founders.

It took another 4 years for the FDA (Food and Drug Administration) to finally approve usage of the da Vinci Surgical System.

The first available surgery was for general laparoscopic surgery used to address gallbladder disease and gastroesophageal disease.

The next year saw another harvest of approvals with the FDA giving the green light to use the system for prostate surgery.

The approvals started to flow like a waterfall with thoracoscopic surgery, cardiac procedures performed with adjunctive incisions, and gynecologic procedures also approved by the FDA.

Fast forward to 2019 and the company couldn’t be financially healthier looking back at the year of 2018 in review.

Instruments & Accessories revenues came in at $1.96 billion comprising 52.7% of total revenue.

System sales crushed it with $1.13 billion, growth of 30.3% YOY and service sales amounted to $635.1 million up 17% YOY.

And in the latest quarter, Intuitive Surgical reported 19% YOY growth in worldwide da Vinci procedure volumes which contributed to bumping up revenue 18% YOY in the instruments and accessories segment.

The company is seeing the same type of success abroad with foreign revenues totaling $307 million, up 24% YOY.

Intuitive Surgical installed 115 systems in the previous quarter outside of America compared with 86 in the quarter before last.

55 of these new systems were installed in Europe, 31 in Japan, and nine in Brazil.

Procedure growth is forecasted to expand between 13-17%, fueled by U.S. general surgery and procedures.

Unfortunately, the stock sold off after earnings because adjusted operating expenses are expected to rise 20-28% reminding investors that the stock can’t always move up in a straight line.

The harm to operating margins is a tough pill to swallow in the short-term, but that does not take away the gloss from this leading tech company.

Intuitive Surgical plans to branch out from the da Vinci systems with its new Ion system, a robotic-assisted bronchoscope awaiting FDA clearance, a revolutionary way to kill cancer cells inside the lung.

After decades of unbridled market leadership, there are a few icebergs ahead in the distance in the form of competition.

Verb Surgical, a collaboration between Johnson & Johnson (JNJ) and Alphabet (GOOGL), will enter the healthcare robot surgery market in 2020.

Johnson & Johnson recently indicated it will splurge $3.4 billion in cash for Auris Health, a robotics startup with a device to perform lung biopsies that could compete with Intuitive Surgical’s Ion system.

Auris Health was approved by the FDA in March 2018 for this device that performs lung biopsies and Intuitive Surgical promptly sued citing patent infringement.

Auris Health was established by the co-founder of Intuitive Surgical Dr. Frederic Moll who pioneered the field of surgical robotics but left Intuitive in 2003 after 8 years there.

Intuitive could rub up on some more competition in the future, that is a stark possibility, but the pathway to profits are still open as the company rolls out different systems, services, and has the capital to fund new directions.

Hospitals that already have existing relationships with Intuitive will be less inclined to switch over to competing services if they are satisfied with the quality, service, and price points of the equipment.

This will help Intuitive build on the current strong momentum and ensure their products are in the pipeline to be adopted by the next batch of future demand.

Shares of the company are sky-high and expensive with a PE multiple of 55.

The big investment into R&D is in no doubt to fend off the potential competition around the corner, but I view that as a net positive.

It would be logical to wait for a pullback to buy shares, this one is a keeper.

Mad Hedge Technology Letter

February 27, 2019

Fiat Lux

Featured Trade:

(HOW AUTONOMOUS DRIVING WILL CHANGE THE WORLD),

(TSLA), (GM), (GOOGL)

The car insurance industry will grapple with a massive existential crisis of epic proportions unless they evolve.

The looming threat is caused by technology and autonomous driving.

This is why parents usher their children into industries that won’t be blown up by technological disruption.

Removing the driver from the automobile industry could be the single most societal shift in our lifetimes.

This technology is getting ramped up as we speak and Waymo is the clear leader that is already collecting money for commercial rides in the state of Arizona.

Car insurers must wonder if they will be able to charge the same amount if there are no drivers?

The answer is that the liability will head from the driver to the manufacturer with companies like General Motors (GM) Tesla (TSLA) likely footing the bill while the passenger is likely to pay minimally.

We are headed towards another data war with insurers incentivized to dismiss the relevance of data in self-driving cars and devaluing it will cause the car companies’ bills to go higher.

Car insurance companies are also heavily investing in data analytics teams to see which part of the pie and how big of it they can get from self-driving technology.

This is uncharted territory.

Consensus has it that by 2035, 23 million autonomous vehicles or around 10 percent of today’s total will grace our roads and highways.

But I believe this number is understating the underlying series of generational factors at play.

It’s no secret that the majority of Millennials and Generation Z want to live in coastal urban cores participating in the heart of downtown activities mainly because of the chance to find a high-paying job.

This has exacerbated the migration from rural to metro areas around the country and sapping the need to drive or buy a car when Uber can become an almost perfect substitute.

And don’t forget that according to the latest data, cars are stationary 92% of the time signaling consumers’ intentions to stop purchasing and instead rent cars by the minute, hour, and day.

That is the beauty of the sharing economy and how self-driving cars will fit in.

This avant-garde model will emerge between 2035 and 2050 effectively reducing the value of owning a car, the self-driving car that will be bought, probably by the self-driving tech company itself, could constitute 50% of all vehicles sold globally.

The sum of the parts could mushroom into a $3 trillion addressable market, not only made up of the physical cars but the assortment of ancillary technology needed to fuel these cutting-edge machines.

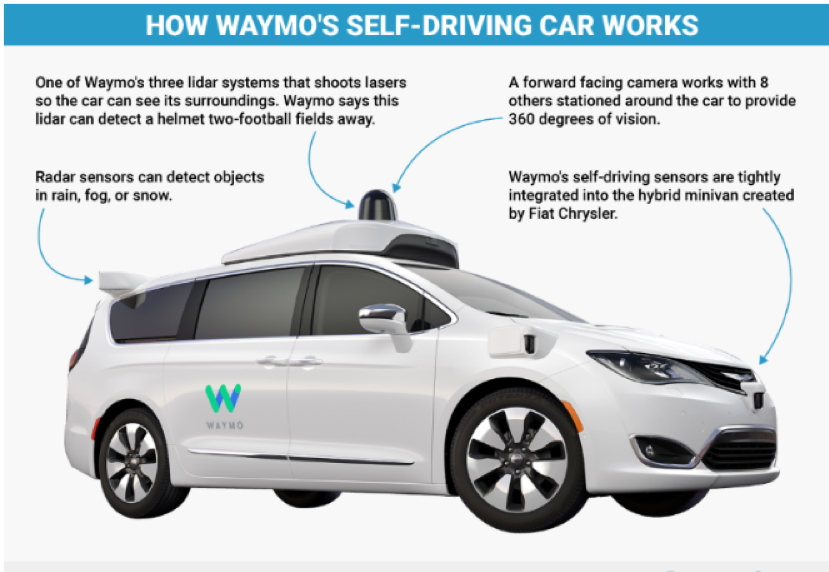

Alphabet’s (GOOGL) self-driving unit named Waymo run an onboard computer that processes images in real time using its machine learnings algorithm built by the industries’ best machine learning engineers.

However, not only do these firms need an army of artificial intelligence engineers to build the algorithms that are at the fulcrum of what they do, they also need other parts that fit into the puzzle such as lidar radar technology.

Lidar is an acronym for light detection and ranging, and the physical manifestation of this technology has so far been a cone-shaped object on top of the car's roof emitting laser pulses that bounce off objects allowing the car to recreate a 3D image of its surroundings.

The advancement of this technology and the potential production of scale will cut the cost of manufacturing this technology to less than $10 per sensor.

A full-blown lidar unit costs $75,000 at current market prices, but luckily the phenomenon of deflationary technology always drives the prices down to bare bones.

Cameras, sensors, cooling systems, and GPU chips are other products that must be heavily developed to accommodate self-driving technology.

GM is another prominent player in this field, and they have already outfitted close to 200 cars for testing.

The firm transformed its Orion Assembly plant in Michigan to accommodate cameras, lidar, and other sensors to its Chevrolet Bolt.

Whoever masters the lidar technology the quickest will have an inside edge to grab market share once this industry explodes and a lower insurance bill.

Waymo won’t be the only player usurping market share even though they are the brightest name out there, and there is room for others to crash the party.

GM invested $500 million into Lyft which could act as a gateway path into outfitting Lyft cars with GM’s proprietary technology.

Whoever specializes in the art of licensing self-driving technology to companies will ring in the register as well and the opportunities abroad are endless because emerging economies aren’t players in this industry.

GM’s Cruise AV has opened eyes with GM removing pedals or a steering wheel for this electric car.

It’s under testing in select cities and GM plans to integrate it into its ride-sharing program.

Investors are still waiting for companies to telegraph meaningful revenue to the top line, and this teething phase could cause the impatient to bolt for greener pastures.

Waymo has claimed it will be able to deliver up to 1 million trips per day by 2022 signaling that real top line revenue appears a few years off at the earliest.

This trade isn’t for the smash-and-grab type, but this is the future and it will be a slow crawl to broad-based adoption and material revenue.

The death of the car insurance industry is still years away and insurers still have time to save their bacon.

Data at the Association for Safe International Road Travel (ASIRT) shows that nearly 1.25 million people die in road crashes each year, on average 3,287 deaths a day and another 20-50 million are injured or disabled.

Technology is on the move and will try to correct this awful trend in road safety and human fatalities.

These years could be the high-water mark for car insurance and as self-driving technology continues to seep deeper into the public consciousness, it could snatch revenue from the coffers of the insurance companies.

But if these legacy companies become nimble and embrace the changes, they could potentially be at the vanguard of a highly lucrative industry charging the likes of GM and Tesla to ferry around humans.

Mad Hedge Technology Letter

February 14, 2019

Fiat Lux

Featured Trade:

(FACEBOOK’S NEW PROBLEM),

(FB), (GOOGL), (TRIP), (EXPE)

A major catalyst exacerbating recent tech layoffs has been a decline in referral traffic to news publishers from Facebook (FB).

Blame the algos!

Referral traffic is a way of reporting visits coming from a site from sources outside of the original site.

When someone clicks on a hyperlink leading to a different website, data analytics classified this as a referral visit to the second site by tracking mechanisms.

The truth is that news publishers have a painfully smaller window to monetize content than ever before and this opinion is echoed by some of big media’s stalwarts such as Rupert Murdoch, the chairman of News Corp.

Facebook decided to give preference to content in the news feed that is shared between Facebook users over those by news organizations, ironically, the news is being stripped out of the news feed whether that seems logical or not.

Under the guise of protecting the platform, Facebook is applying this ploy to further cut off users from escaping its walled garden trapping them inside for the purpose of clicking around the Facebook website even more.

As the technology evolves, companies are becoming increasingly pedantic in finding any practical method of allowing users to escape to another part of the internet.

Diminishing user time equals fewer clicks followed by reduced digital advertising revenue.

Another shift in Facebook rules entails elevating and demoting media outlets by trust levels and credible content that ultimately Facebook makes the decision on.

The algorithms in this case would prop up the more renowned institutions and essentially cut out minnow news organization.

Algorithms are inherently biased, and sources of revenue are cut off or opened up by these algorithmic shifts.

The monopolistic status of Facebook has made it near impossible for stand-alone firms to develop organically and ramping up digitally means leveraging Facebook ads to lure new customers.

What does this all mean?

News publications are bracing themselves for an atrocious year.

The side effect from recent changes mean that Facebook will ultimately become the God of the news cycle choosing which news populates where on the news feed or if it shows up at all.

Being a left-leaning company, Facebook is likely to anoint left-leaning news organizations as “trustworthy” while demoting more right-wing news feeds pushing them further down the pecking order.

And for marginal start-up news companies praying for any exposure, this is effectively a death sentence because of the lack of footprint inside of Facebook’s current database.

Machine learning cannot account for new developments in the system, let alone system altering shifts causing this technology to be defective.

The technology handsomely rewards the entrenched that have cultivated a big footprint inside the database that decisions hinge on.

Its backward-looking nature to carry out a business that is forward-looking is utter nonsense.

Many third-party businesses attempt to stimulate Facebook users’ appetite in order to bridge them over and act as a stepping stone to their own website.

Small businesses should prepare for an era where this type of digital reach is stunted and at some point, completely disengaged.

Effectively, Facebook and the rest of the FANGs will do its best to cut off outside activity preferring to keep usership in-house.

News organizations are feeling the full brunt of these ripple effects with online media firms such as Vox Media and BuzzFeed cutting staff in response to these Facebook algorithm changes.

Which industry will get chopped down next?

Online travel aggregators.

TripAdvisor (TRIP) had a great winter quarter in 2018, but looking down the line, the business model could get bogged down by the algorithm problem.

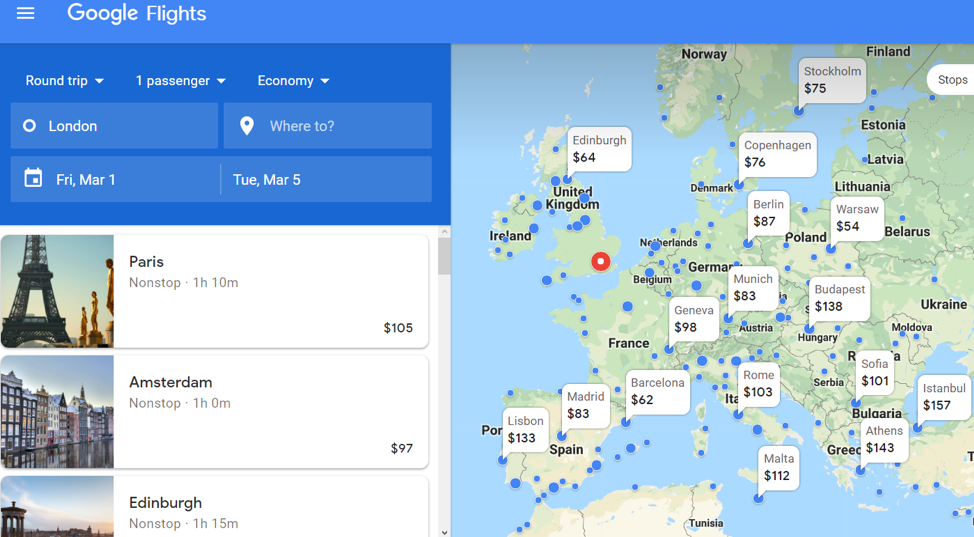

For instance, take the best flight purchase algorithm in the world Google Flights.

The United States Department of Justice Antitrust Division approved Google's $700 million purchase of ITA Software in 2011.

Within a few months, Google bent its algorithm into shape and reformulated it as Google Flights.

How does it stack up?

Easy to use, lack of digital ads, best of breed, and innovative are all ways I would describe this service.

That is why consumers prefer Google Flights over any other service.

It offers open-ended searches making the traditional flight search software seem pathetic.

Simply input the departure location and Google Flights will show the user every price to every location in the world on a visual map.

It’s travel transparency at its brightest and users can change trips in an instant if something attractive catches their eye.

The user can mix and match different destinations and dates until an optimal time and place can be calibrated along with a suitable price.

This gives the power back to the consumers.

Once in a while, dispersion between the Google Flight price and the official airline site price can be irritating, but the accuracy has improved over time.

Truth be told, it’s a waste of time to use a different flight search engine now after the existence of Google Flights.

Google is able to do this because they are masters at building algorithms and have an army of engineers at their disposal.

Online flight brokers such as Expedia (EXPE) and TripAdvisor are on a collision course for the beast that is the Google algorithm division.

This dovetails astutely with my overarching theme of technology destroying every broker industry because FANG algorithm teams do a way better job enhancing this segment of business than anyone else.

As you correctly guessed, I am bearish Expedia and TripAdvisor long term.

Travel fare aggregators can’t compete with Google and former CEO of Expedia Dara Khosrowshahi was smart to take the head job at Uber saving him from the future carnage.