Global Market Comments

November 2, 2018

Fiat Lux

Featured Trade:

(OCTOBER 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(EDIT), (TMO), (OVAS), (GE), (GLD), (AMZN), (SQ), (VIX), (VXX), (GS), (MSFT), (PIN), (UUP), (XRT), (AMD), (TLT)

Global Market Comments

November 2, 2018

Fiat Lux

Featured Trade:

(OCTOBER 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(EDIT), (TMO), (OVAS), (GE), (GLD), (AMZN), (SQ), (VIX), (VXX), (GS), (MSFT), (PIN), (UUP), (XRT), (AMD), (TLT)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 31 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: I would like to keep CRISPR stocks as a one or two-year-old, or even longer if it is prudent. What do you think?

A: Yes, there is a CRISPR revolution going on in biotech—I’m extremely bullish on all these stocks, like Editas Medicine (EDIT), Thermo Fisher Scientific (TMO), and Ovascience Inc. (OVAS). If any of these individual companies don’t move forward with their own technology, they will get taken over. The principal asset of these companies is not the patents or the products, it’s the staff, and there is an extreme shortage in CRISPR specialists (and anybody who knows anything about monoclonal antibodies).

Q: Could you explain how to manage LEAPs? For example, the Gold (GLD) and the General Electric (GE) LEAPs. Sit and leave them or trade them short term?

A: You make a lot of money trading long-term LEAPs. Just because you own a year and a half LEAP doesn’t mean that you keep it for a year and a half. You sell it on the first big profit, and I happen to know that on both the Gold (GLD) and the (GE) LEAPs we sent out, people made a 50% profit in the first week. So, I told them: sell it, take the profit. The market always gives you another chance to get in and buy them cheap. You make the money on the turnover, on the volume—not hanging out trying to hit a home run.

Q: Why did you only close the Amazon (AMZN) November $1,550-$1,600 vertical bull call spread and not roll the strike prices down and out?

A: Well I actually did do the down and out strike roll out first, which is the super aggressive approach. By adding the November $1,350-$1,400 vertical bull call spread position on Monday at the market lows and doubling the size—we took a huge 30% position in Amazon and that position alone should bring in about $3600 in profits in two weeks, at expiration. And when I put on that second position I told myself that on the next big rally I would get out of the high-risk trouble making position, which was the November $1,550-$1,600 vertical bull call spread. So that’s how you trade your way out of a 30% drop in three weeks in one of the best tech stocks in the market.

Q: Is AT&T (T) no longer a good buy at these prices?

A: All of the telephone companies have legacy technology, meaning they are all dying. Basically, AT&T is about owning a bunch of rusting copper wire spread around the country. They haven’t been able to innovate new technologies fast enough to keep up with others who have. The only reason to own this is for the very high 6.56% dividend. That said, dividends can be cut. Look at General Electric which cut its dividend earlier this year. Whatever you make of the dividend can get lost in the principal.

Q: Do you think Square (SQ) is a good buy at this level?

A: Absolutely, it’s a screaming buy. It’s one of the favorite companies of the Mad Hedge Technology Letter and one of the preeminent disruptors of the banks. We think there’s another 400% gain in Square from here. It’s dominating FinTech now.

Q: When do you expect to close the short position in the iPath S&P 500 VIX Short-Term Futures ETN (VXX)?

A: If we can get the Volatility Index (VIX) down to $15, the (VXX) should crater. We’ll take a hit on the time decay and that’s why I say we may be able to sell it for 20 cents in the future when this happens. We’ll still take a 50% hit on the position, but half is better than none.

Q: What happened to Microsoft (MSFT) last week?

A: People sold their winners. They had a great earnings report and great long-term earnings prospects, but everyone in the world owned it. Buy the long-term LEAP on this one.

Q: If we want to double up on the iPath S&P 500 VIX Short-Term Futures ETN (VXX), how do you plan to do it?

A: Go out to further with your expiration date. When you go long the (VXX) you only buy the most distant expiration date. I would buy the February 15 expiration as soon as it becomes available.

Q: How do you see Goldman Sachs (GS) from here to the end of the year?

A: It may go up a little bit as we get some index money coming into play for year-end, but not much; I expect banks to continue to underperform. They are no longer a rising interest rate play. They are a destruction by FinTech play.

Q: Is it too soon for emerging markets in India (PIN)?

A: As long as the dollar (UUP) is strong, which is going to be at least another year, you want to avoid emerging markets like the plague. As long as the Federal Reserve keeps raising interest rates, increasing the yield differential with other currencies, the buck keeps going up.

Q: What are your thoughts on retail ETFs like the SPDR S&P Retail ETF (XRT)?

A: You may get lucky and catch a rally on that but the medium term move for retail anything is down. They are all getting Amazoned.

Q: Is it better to increase long exposure the day before the election?

A: No, what we saw starting on Tuesday was the pre-election move. That said, I expect it to continue after the election and into yearend.

Q: Any opinions on Advanced Micro Devices (AMD)?

A: Yes, this is a great level. It was extremely overbought two months ago but has now dropped 50%. It is a great long-term LEAP candidate.

Q: What about the W bottom in the stock market that everyone thinks will happen?

A: I’m one of those people. So far, the bottom for the move in the S&P 500 is looking pretty convincing, but we will test the faith sometime in the next week I’m sure. We got close enough to the February $252 low to make this a very convincing move. It sets up range trading for the market for the next year.

Q: How do you figure the inflation rate is 3.1%?

A: The year-on-year Consumer Price Index for September printed at 2.3%, and the most recent months have been running at an annualized 2.9% rate. Given that this data is months old we are probably seeing 3.1% on a monthly annualized basis now given all the anecdotal evidence of rising prices and wages that are out there. That is certainly what the bond market believes with its recent sharp selloff and why I will continue to be a fantastic short. Sell every United States US Treasury Bond Fund ETF (TLT) rally. Like hockey great Wayne Gretzky said, you have to aim not where the hockey puck is, but where it's going to be.

Q: Will rising interest rates kill the housing market?

A: It already has. A 5% 30-year mortgage rate shuts a lot of first time Millennial buyers out of the market. We are seeing real estate slowing all over the country. Los Angeles is getting the worst hit.

Q: How do you see the Christmas selling season going?

A: It’s going to be great, but this may be the last good one for a while. And Amazon is getting half the business.

Q: October was terrible. How do you see November playing out?

A: It could well be a mirror image of October to the upside. We are already $1,000 Dow points off the bottom. So far, so good. Throw fundamentals out the window and buy whatever has fallen the most….like Amazon.

Did I mention you should buy Amazon?

Good luck and good trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

October 17, 2018

Fiat Lux

Featured Trade:

(THE SPOTIFY REGIME),

(SPOT), (AAPL), (NFLX), (MSFT), (AMZN), (GS)

It’s not earth-shattering to concede that our attention spans have shrunk and as a result, there are unintended consequences.

The various smart devices and other technology vying for a slice of your precious attention have been accepted as the new normal.

Whether it’s binging on Netflix (NFLX) or gaming on a Microsoft Xbox (MSFT), consumers are absorbed obsessively staring into a screen most of the day.

As tech penetrates the core of our existence, the music industry has been the recipient of changes that were hard to fathom just a few years ago.

And as all businesses morph into pseudo-tech enterprises supported by data analytic teams, management is able to unearth some compelling data and utilize it to commercialize the audience.

Spotify (SPOT), the world’s leading music streaming platform, doesn’t monetarily reward music artists unless a stream surpasses a minimum of 30 seconds.

This is just one way that Spotify’s founder and CEO Daniel Ek has changed the music industry.

Think about the implications.

Gone are the elaborate instrumentals to warm listeners up before a catchy chorus hooks you forever.

Songs are entirely front loaded now with the end goal of persuading listeners to not swipe until the 30-second barrier is passed.

Whatever happens after that doesn’t matter – the song might as well go silent because Spotify will pay the artist.

According to Spotify data, Ed Sheeran’s “The Shape of You” is Spotify’s most-streamed song with 1.94 billion listens.

This is just one scant nugget of data in Spotify’s treasure trove of global music data that finely chronicles the state of the music industry and how consumers devour music.

Spotify CFO Barry McCarthy promptly explained the Spotify’s relationship with data and music at the Goldman Sachs’ (GS) Communacopia conference by saying, “The company with the most data wins. The company with the most data insights wins. The company with the engineering culture, software-driven business wins. And that’s the play we’re making.”

In the current tech climate, I will take software over hardware any day of the week.

Hardware sales are a one-off event until the next cycles bring an upgraded iteration which could take years to execute.

Software sales are an annual recurring revenue stream that is as sticky as the software's quality giving hope to company CFO’s of a perpetual income stream.

It doesn’t matter that Spotify isn’t profitable. The end goal isn’t to make money in an industry that is notoriously difficult to combat the royalty expenses eroding 70% of every $1 of revenue.

What has happened is that Spotify is too big to fail and it loves every second of it.

The music industry needs Spotify just as much as Spotify needs the music industry and this awkward partnership is far from a match made in heaven, but it works for the foreseeable future.

It helps that artists, for the most part, have bought into the data-based streaming model.

Music artists have turned into tech-like firms themselves.

Their new goal is to compile an audience then monetize like Spotify itself.

It speaks volumes of how the tech model has penetrated every corner of the world.

Apple (AAPL) is acutely aware of the potency a music streaming service offers and has been investing in Apple Music, its music streaming arm.

Rumors have been swirling that Apple absorbed the entire staff of a music analytics firm called Asaii including the owners, for a tad under $100 million.

This talent grab on the heels of the Shazam purchase indicates that Apple seeks a better understanding of how to curate music playlists and better serve music fans who own Apple devices.

Even though Apple has the second leading music streaming service, they have ceded the battle to Spotify.

CEO of Apple Time Cook is on record saying, “We’re not in it for the money.”

Indirectly, Cook means Apple Music is a loss-making division and he doesn’t care because it is just a small fragment of what makes Apple one of the best companies in the world.

Apple has also commissioned 24 television shows and 2 films costing them $1 billion.

A single billion is peanuts considering the eye-popping amount of Apple’s cash hoard. They can afford to take the long-term view and slowly enhance the ecosystem instead of Spotify whose eggs are all in one basket.

Apple is more concerned about offering iOS users the best experience possible and in return Cook hopes to count on them to use iOS devices for a lifetime.

Apple Music’s biggest weakness is its biggest strength.

In short, Apple music is tailored to the iOS operating system.

If you sign up, the app directs users to sign up for an Apple ID if you do not already have one.

Android lovers have little interest in signing up for Apple Music considering they do not have an Apple device and then must pay $9.99 per month after the introductory 3-month offer expires when Spotify is free. It’s not worth the extra hassle.

It is almost certain that Spotify will enact an Android operating system pivot to build a moat around its business and that is something Apple cannot do.

Spotify will start partnering with Samsung, Microsoft, and the Android-based Asian manufacturers to focus on monetizing the Android audience and make it even more inconvenient for listeners to access Apple Music.

Signing up for Spotify and listening to its ad-free subscription without creating an Apple ID is more appealing.

And after three months, users have the option to continue a free version of Spotify, albeit with digital ads popping up.

This leads me to the belief that there is definitely space for more than one player in the music streaming industry.

Amazon is another tech firm who has a music streaming service but are more concerned if they convert users into prime memberships.

If compiling the most music data wins out, then Spotify is in the lead with its 83 million paid users and 101 million free users.

Apple trails in second place with 50 million users which is still an extraordinary number of listeners and easily monetizable.

The way music streaming platforms works is that users are more likely to listen to the most popular artists and songs and not look for an adventure.

The app is merely there to locate the songs they already like or click on a recommendation produced by an algorithm.

It’s not like going out on a Friday night to experience some unknown singer in a grunge basement and becoming a new fan. Users know what they want, and they desire to access it. Such is the nature of internet search.

Spotify’s data shows that out of 3 million artists on the platform, 200,000 artists receive 70% of the music streams, clearly segmenting the haves and have-nots.

The rest of the 2.8 million are struggling to be discovered and cannot cut a wage off of Spotify’s platform.

Online music streaming products also align perfectly well with artificial intelligence-based voice activation technology.

These services will deeply integrate this technology into its services as they desire to ramp up the quality of services.

As for the music streaming business hopefuls, it's game over as the three major players have the leverage to put out any fires that crop up.

When you break it down, Spotify has a 180 million user audience growing at 30% YOY and is hellbent on becoming profitable.

As they enhance the platform’s tools and services, gradually expect more subscription-based products to entertain users.

And even if Spotify doesn’t become profitable as soon as they would like, the aggregate hoard of data will multiply in value.

Spotify is already the most prized music asset in the world with a market cap of $26 billion, about $10 billion higher than all global music revenues.

Yes, Spotify destroyed album artwork and its audio quality of 320 kilobits per second is no match for CD-quality audio. But this is the world we live in today and Daniel Ek’s Spotify is the 800-pound gorilla in the room.

Spotify is a great long-term buy-and-hold asset. Take the latest weakness to add to your position.

Mad Hedge Technology Letter

October 4, 2018

Fiat Lux

Featured Trade:

(HOW SOFTBANK IS TAKING OVER THE US VENTURE CAPITAL BUSINESS),

(SFTBY), (BABA), (GRUB), (WMT), (GM), (GS)

One of the few people who can magnify pressure on the venture capitalists of Silicon Valley is none other than Masayoshi Son.

What a ride it has been so far. At least for him.

His $100 billion SoftBank Vision Fund has put the Sand Hill Road faithful in a tizzy – utterly revolutionizing an industry and showing who the true power broker is in Silicon Valley.

He has even gone so far as doubling down his prospects by claiming that he will raise a $100 billion fund every few years and spend $50 billion per year.

This capital logically would flow into what he knows best – technology and the best technology money can buy.

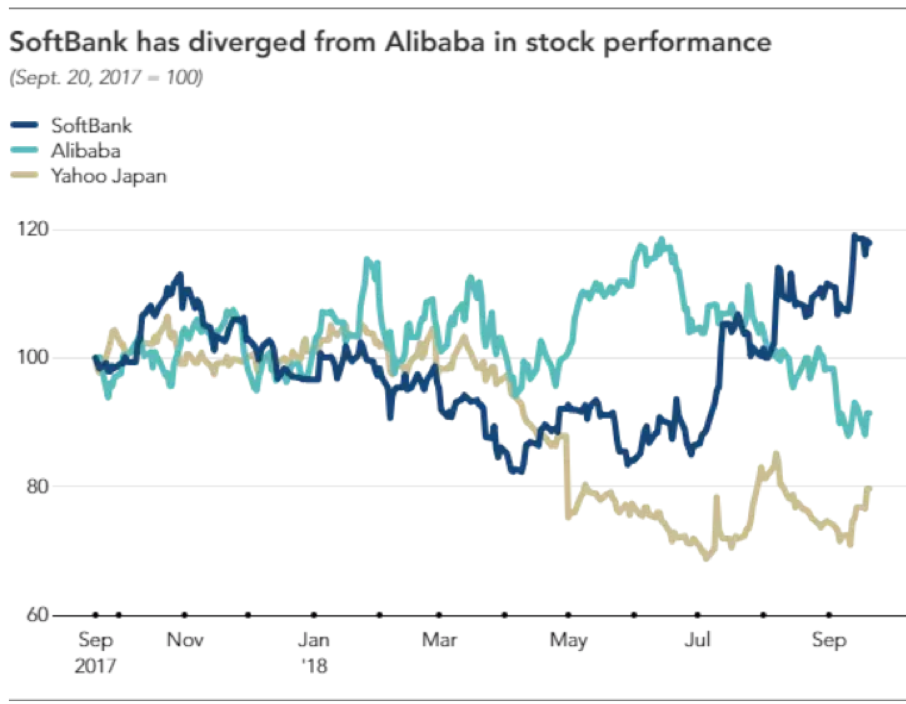

As Yahoo Japan and Alibaba (BABA) shares have floundered, SoftBank’s stock has decoupled from the duo displaying explosive brawn.

SoftBank’s stock is up 30% in the past few months and I can tell you it’s not because of his Japanese telecommunications business which has served him well until now as his cash cow.

Yahoo Japan, in which SoftBank owns a 48.17% stake, has existing synergies with SoftBank’s Japanese business, but has experienced a tumble in share price as Son turns his laser-like focus to his epic Vision Fund.

His tech investments are bearing fruit and not only that, Son revealed his Alibaba investment is about to clean up shop to the tune of $11.7 billion next year shooting SoftBank shares into orbit.

A good portion of the lucrative windfall will arrive from derivatives connected to the sale of Alibaba, and the other 60% comes from the paper profits finally realized in this shrewd piece of business.

Equally paramount, SoftBank’s Vision Fund hauled in $2.13 billion in operating profits from the April-June quarter underscoring the effectiveness of Masayoshi Son’s tech ardor.

Son said it best of the performance of the Vision Fund saying, “Results have actually been too good.”

So good that after this June, Son changed his schedule to spend 3% of his time on his telecom business down from 97% before June.

His telecommunications business in Japan has turned into a footnote.

It was the first quarter that Son’s tech investments eclipsed his legacy communications company.

Son vies to rinse and repeat this strategy to the horror of other venture capitalists.

The bottomless pit of capital he brings to the table predictably raises the prices for everyone in the tech investment world.

Son’s capital warfare strategy revolves around one main trope – Artificial Intelligence.

He also strictly selects industry leaders which have a high chance of dominating their field of expertise.

Geographically speaking, the fund has pinpointed America and China as the best sources of companies. India takes in the bronze medal.

Unsurprisingly, these two heavyweights are the unequivocal leaders in artificial intelligence spearheading this movement with the utmost zeal.

His eyes have been squarely set on Silicon Valley for quite some time and his record speaks for himself scooping up stakes in power players such as Uber, WeWork, Slack, and GM (GM) Cruise.

Other stakes in Chinese firms he’s picked up are China’s Uber Didi Chuxing, China’s GrubHub (GRUB) Ele.me and the first digital insurer in China named Zhongan International costing him $500 million.

Other notable deals done are its sale of Flipkart to Walmart (WMT) for $4 billion giving SoftBank a $1.5 billion or 60% profit on the $2.5 billion position.

In 2016, the entire venture capitalist industry registered $75.3 billion in capital allocation according to the National Venture Capital Association.

This one company is rivalling that same spending power by itself.

Its smallest deal isn’t even small at $100 million, baffling the local players forcing them to scurry back to the drawing board.

The reverberation has been intense and far-reaching in Silicon Valley with former stalwarts such as Kleiner Perkins Caufield & Byers breaking up, outmaneuvered by this fresh newcomer with unlimited capital.

Let me remind you that it was considered standard to cautiously wade into investment with several millions.

Venture capitalists would take stock of the progress and reassess if they wanted to delve in some more.

There was no bazooka strategy then.

SoftBank has thrown this tactic out the window by offering aspiring firms showing promise boatloads of capital up front even overpaying in some cases.

Conveniently, Son stations himself nearby at a nine-acre estate in Woodside, California complete with an Italianate mansion he bought for $117.5 million in 2012.

It was one of the most expensive properties ever purchased in the state of California even topping Hostess Brands owner Daren Metropoulos, who bought the Playboy Mansion from Hugh Hefner in 2016 for $100 million.

If you think Son is posh – he is not. He only fits himself out in the Japanese budget clothing brand Uniqlo. He just needed a comfortable place to stay and he hates hotels.

In August, SoftBank decided to top off the $4.4 billion investment in WeWork, an American office space-share company, with another $1 billion leading Son to proclaim that WeWork would be his “next Alibaba.”

Son continued to say that WeWork is “something completely new that uses technology to build and network communities.”

The rise of remote workers is taking the world by storm and this bet clearly follows this trend.

The unlimited coffee and beer found in the new Japanese Roppongi WeWork office that opened earlier this year was a nice touch.

WeWork plans to open 10-12 offices in Japan by the end of 2018.

Thus far, WeWork is operating in over 300 locations in over 20 countries.

Revenue is growing rapidly with the $900 million in 2017 a 12-fold improvement from 2014.

The newest addition to SoftBank’s dazzling array of unicorns is Bytedance, a start-up whose algorithms have fueled news-stream app Jinri Toutiao’s meteoric rise in China.

The deal values the company at $75 billion.

It also runs video sharing app Douyin, and overseas version TikTok.

Bytedance’s proprietary algorithm, serving to personalize streams for users, is the best in China.

They have been able to insulate themselves from local industry giants Tencent and Alibaba.

TikTok has piled up over 500 million users and brilliant investment like these is why Son revealed that the Vision Fund’s annual rate of return has been 44%.

SoftBank’s ceaseless ambition has them in the news again with whispers of investing in a Chinese online education space with a company called Zuoyebang.

China’s online education market is massive. In 2017, this industry pulled down over $33 billion in revenue, and 2018 is poised to break $55 billion.

Zuoyebang has lured in Goldman Sach’s (GS) as an investor.

This platform allows users to upload homework questions for third party assistance – the name of the app literally translates into “homework help.”

Cherry-picking off the top of the heap from the best artificial intelligence companies in the world is the secret recipe to outperforming your competitors.

At the same time, aggressively throwing money at these companies has effectively frozen out any resemblance of competition. Once the competition is frozen out, the value of these investments explodes, swiftly super-charged by rapidly expanding growth drivers.

How can you compete with a man who is willing to pay $300 million for a dog walking app?

Venture capitalist funds have been scrambling to reload and mimic a Vision Fund-like business of their own, but its not easy raising $100 billion quickly.

This genius strategy has made the founder of SoftBank the most powerful businessman in the world.

Son owns the future and will have the largest say on how the world and economies evolve going forward.

Global Market Comments

September 27, 2018

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL),

(TUESDAY, OCTOBER 16, 2018, MIAMI, FL,

GLOBAL STRATEGY LUNCHEON)

Global Market Comments

September 24, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or IT’S FED WEEK),

(SPY), (XLI), (XLV), (XLP), (XLY), (HD), (LOW), (GS), (MS), (TLT),

(UUP), (FXE), (FCX), (EEM), (VIX), (VXX), (UPS), (TGT)

(TEN TIPS FOR SURVIVING A DAY OFF WITH ME)

20/20 hindsight is a wonderful thing, especially when all of your predictions come true.

In February, I announced that markets would trade in broad ranges until the run-up to the midterm elections. That is what has happened to a tee, with the decisive upside breakout taking place last week. From here on. You’re trying to buy dips for a year-end run-up to higher highs.

For many months I was the sole voice in the darkness crying out that the bull market was still alive, it was just resting. Now quality laggards are taking the lead, such as in Industrials (XLI), Health Care (XLV), Consumer Staples (XLP), and Consumer Discretionary (XLY).

Home Depot (HD), which I recommended a month ago has taken off for the races, as has competitor Lowes (LOW), thanks to a twin hurricane boost. Even the long dead banks have recently showed a pulse (MS), (GS).

Technology stocks are taking a long-needed rest after a torrid two-and-a-half-year run. But they’ll be back. They always come back.

It’s not only stocks that have broken out of ranges, so has the bond market (TLT), the U.S. dollar (UUP), and foreign currencies (FXE). Will commodity companies like Freeport-McMoRan (FCX) and emerging markets (EEM) be the last to pick themselves off the mat, or do they really need to see the end of the trade wars first?

Markets are essentially acting like the trade war is over and we won. Why would traders believe this? That’s what a Volatility Index touching $11 tells you and is why I have been telling them to avoid buying it all week. Because the president told them so.

Another not insignificant positive is that multinationals have been slow to repatriate foreign funds, so there is a lot more still abroad to buy back their own stocks.

Weekly jobless claims hit another half century low at 201,000. Major U.S. companies such as UPS (UPS) and Target (TGT) are planning record levels of Christmas hiring. By the way, this is what economic peaks look like.

The Senate passes a mini spending bill that keeps the government from shutting down until December 7. The budget deficit keeps on soaring, but apparently, I am the only one who cares. Live through a debt crisis like we had during the early 1980s and you’d feel the same way.

The data for housing continues to be terrible, and we saw our first increase in inventories in three years.

Finally, with people camping out overnight and lines around the block, Apple’s CEO Tim Cook opens the doors to the Palo Alto, CA, store at 9:00 AM sharp on Friday to three new phones. But did the stock peak at $230, as it has in past release cycles?

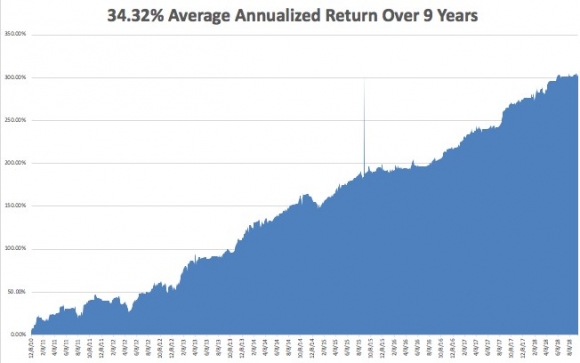

Last week, the performance of the Mad Hedge Fund Trader Alert Service forged a new all-time high and then gave it up on one bad trade. September is now unchanged at -0.32%. My 2018 year-to-date performance has retreated to 26.69%, and my trailing one-year return stands at 38.23%.

My nine-year return appreciated to 303.16%. The average annualized Return stands at 34.32%. I hope you all feel like you’re getting your money’s worth.

This coming week is all about the Fed, plus a plethora of housing data.

On Monday, September 24, at 10:30 AM, we learn the August Dallas Fed Manufacturing Survey.

On Tuesday, September 25, at 9:00 AM, the new S&P Corelogic Case-Shiller National Home Price Index for July, a three-month lagging indicator.

On Wednesday September 26, at 10:00 AM, the August New Home Sales is published. At 2:00 the Fed Open Market Committee announced its decision to raise interest rates by 25 basis points.

Thursday, September 27 leads with the Weekly Jobless Claims at 8:30 AM EST, which dropped 3,000 last week to 201,000, a new 43-year low. At the same time an update on Q2 GDP is published.

On Friday, September 28, at 9:45 AM, we learn the August Chicago Purchasing Managers Index. The Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me,

Good luck and good trading.

Global Market Comments

September 21, 2018

Fiat Lux

Featured Trade:

(SEPTEMBER 19 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (VIX), (VXX), (GS), (BABA), (BIDU), (TLT), (TBT),

(TSLA), (NVDA), (MU), (XLP), (AAPL), (EEM),

(MONDAY, OCTOBER 15, 2018, ATLANTA, GA,

GLOBAL STRATEGY LUNCHEON)