Mad Hedge Biotech & Healthcare Letter

June 4, 2020

Fiat Lux

Featured Trade:

(MERCK’S BIG COVID-19 EXPANSION)

(MRK), (PFE), (GSK), (AZN), (MRNA)

Mad Hedge Biotech & Healthcare Letter

June 4, 2020

Fiat Lux

Featured Trade:

(MERCK’S BIG COVID-19 EXPANSION)

(MRK), (PFE), (GSK), (AZN), (MRNA)

Leading biotechnology and healthcare giant Merck (MRK), with a market capitalization of $203.75 billion, has been a low-key player during the pandemic.

Now, it finally reveals its grand plans via three major initiatives that aim to create a vaccine and design a novel antiviral against the coronavirus disease (COVID-19).

While Merck has been slow to take part in the COVID-19 war, it’s definitely making up for the lost time by announcing a promising acquisition and two collaborative projects in the works.

The first of the three deals is Merck’s acquisition of Vienna-based biotechnology company called Themis Bioscience. This small-cap biotech develops a range of vaccines and other therapies for infectious diseases.

One of Themis Bioscience’s pipeline candidates is a COVID-19 vaccine, which is a collaborative effort with the Institut Pasteur. Another promising candidate in Themis Bioscience’s pipeline is its late-stage work on a Chikungunya.

Through the acquisition, Merck will be able to access these works and hasten the development of the vaccine.

The second deal is Merck’s collaboration with a nonprofit scientific research group called International AIDS Vaccine Initiative (IAVI). This partnership aims to create a COVID-19 vaccine as well.

This will be a powerful collaboration since IAVI also received $38 million in funding from the US Health Department’s Biomedical Advanced Research and Development Authority (BARDA) to help them with their vaccine development initiatives.

Apart from IAVI, BARDA also awarded over $2 billion in funding to other vaccine developers like AstraZeneca (AZN), Phlow, and Moderna (MRNA).

Together, IAVI and Merck aim to optimize the latter’s recombinant vesicular stomatitis virus (rVSV) technology which has been used for Merck’s Ebola vaccine called Ervebo.

The third deal is Merck’s partnership with privately held Ridgeback Biotherapeutics, a Miami-based biotechnology company founded in 2018.

The collaboration intends to develop an oral antiviral treatment, dubbed as EIDD-2801, which can be used for COVID-19.

So far, this developmental drug had been proven safe in a trial with healthy volunteers. Clinical testing for COVID-19 patients has already commenced.

Under the terms of the deal, Merck will own exclusive global rights to EIDD-2801.

The giant biopharma will take charge of the clinical development, manufacturing, and regulatory procedures. In exchange, Ridgeback received an undisclosed amount in upfront payment and milestones. The smaller biotechnology company will also be entitled to a share of net proceeds from the COVID-19 treatment.

Prior to these deals, investors have been curious as to why Merck was missing in action amid the government’s “Operation Warp Speed” for COVID-19 treatments and vaccines.

With this triple play, Merck has signaled that it’s also going all-in on this pandemic and will pull out all the stops to be on the same level as the efforts from other major biotechnology and healthcare players like GlaxoSmithKline (GSK), Pfizer (PFE), and AstraZeneca (AZN).

The strategic moves from this healthcare giant clearly underscore the incredible demand for any vaccine that actually survives the R&D gamut, as every nation across the globe frantically looks for a vaccine to boost their people’s immunity.

While companies such as CanSino (HKG:6185) and Moderna go neck to neck to take the lead in the clinical race, we all know that two companies cannot handle the production of a vaccine for the entire world -- offering Merck a slot at a place in these chosen group of companies.

Outside its COVID-19 efforts, Merck recently chalked up another win for its blockbuster melanoma drug Keytruda. This time, the top-selling medication expanded its use to advanced colon cancers.

Based on key findings, Keytruda lowered the risk of the disease’s progression or even death by 40% compared to chemotherapy.

Results show that the tumors of patients given Keytruda did not grow for 16.5 months. In comparison, chemotherapy patients experienced tumor growth in 8.2 months.

Even prior to the expansion of its indications, Keytruda sales have continued to make headway.

In the first quarter of 2020, sales of this cancer drug reached $3.3 billion, showing off a whopping 45% year-over-year jump.

With this new addition to Keytruda’s indications, sales of this drug is expected to climb even higher this year.

Apart from that, Merck’s HPV vaccines, called Gardasil and Gardasil 9, performed well in the first quarter as well as sales of both HPV vaccines increased by 31% to reach $1.1 billion.

Another strategic effort for Merck is delving into drug development focused on neurodegenerative diseases like Alzheimer’s, Parkinson’s, and Huntington’s disease.

This initiative was kicked off by Merck’s move to buy a GSK startup, called Calporta Therapeutics, for $576 million in 2019.

It was followed by forging a two-year partnership with Almac Discovery this year. Apart from neuro-related diseases, the two companies are looking into developing therapies for cancer and viral diseases as well.

To further boost its pipeline, Merck completed a deal with Taiho Pharmaceuticals and Astex Pharmaceuticals worth $50 million in upfront payment plus incentive payments of up to $2.5 billion.

The company is also working on spinning off its "Women's Health, Trusted Legacy Brands, and Biosimilars” products into a brand new company with a focus on oncology and vaccines as well as animal health. If things go smoothly, the spinoff should be done by the first half of 2021.

Overall, Merck has proven itself as a stable dividend stock that investors can simply buy and hold for years.

The biotechnology company has managed to post a profit every year for the past decade, actually hitting double-digits most of the time within that period.

This is a trend observed in Merck’s first quarter report as well. The company posted $3.2 billion in profit on sales worth $12.1 billion. This represents a respectable 27% profit margin.

Mad Hedge Biotech & Healthcare Letter

May 12, 2020

Fiat Lux

Featured Trade:

(GLAXOSMITHKLINE’S ENTRY INTO THE COVID-19 VACCINE RACE)

(GSK), (VIR), (AZN)

It’s all-hands-on-deck for the biotech sector as the world battles the deadly coronavirus disease COVID-19.

As the US coronavirus-related deaths mount to over 80,000 and reported cases hitting over 1.3 million, the need to find a cure and vaccines increases in urgency every passing minute.

Joining the biotech companies throwing their hats into the ring is GlaxoSmithKline (GSK), which recently announced its decision to work hand in hand with Vir Biotechnology (VIR) in the search for a coronavirus cure.

On top of the collaboration efforts, the partnership will also involve GSK investing $250 million in Vir. According to these terms, each Vir share will be worth $37.73.

The collaboration announcement also pushed Vir shares to rise by as much as 34% and trading more than doubled. Meanwhile, (GSK) went up by roughly 2%.

The partnership will explore several platforms to come up with a treatment for COVID-19.

So far, the most promising candidates involve two antibodies presently dubbed as VIR-7831 and VIR-7832. Both were developed by Vir as treatments for SARS, which is also caused by a coronavirus.

Actually, these antibodies were developed using samples from a patient who recovered from SARS. However, these could also be produced artificially.

(GSK) and Vir estimate that Phase 2 clinical trials will commence in three to five months.

Apart from these antibody treatments, the two companies are also looking into utilizing CRISPR screening technology to figure out which proteins are used by the coronavirus to infect the healthy cells.

Once they identify these, (GSK) and Vir could come up with drugs that block viral infection. That is, they can use the information to create a vaccine to be used not only for COVID-19 but also for other types of coronaviruses.

According to (GSK), the Vir proteins had been identified as “highly potent” when targeted at the coronavirus in the laboratory.

If all goes well, a coronavirus vaccine could be on its way in 12 to 18 months.

Aside from (GSK), Vir also has an ongoing collaboration with another bigwig biotech, Biogen (BIIB).

This isn’t the first venture of (GSK) in looking for a COVID-19 cure though.

The British biotech giant is also working with China’s Xiamen Innovex on another potential coronavirus vaccine.

In addition, (GSK) is looking into forming a joint laboratory with AstraZeneca (AZN) to assist the UK government in stretching and expanding its supplies for COVID-19 diagnostic tests.

Although diagnostics are not part of their primary efforts, the goal is for the two big biotechs to determine the best ways to help in detecting the spread of COVID-19.

While these efforts to help find a solution to the pandemic are at the forefront of the biotech world today, GSK has a lot more to offer.

(GSK) manufactures products that people need to take on a regular basis.

The need is so great that the company actually allocates 80% of its research efforts focused on drug development for various issues like oncology, immuno-inflammation, and HIV. These treatments are vital to the daily existence of so many patients across the globe.

Meanwhile, (GSK) also aims to streamline its business and focus on the research and development of products and services. Hence, it decided to split its businesses into two.

One will be geared towards pharmaceutical efforts. The second will be focused on consumer health.

This is an excellent move in ensuring that (GSK) maximizes its potential to dominate its chosen markets.

Throughout the years, (GSK) has demonstrated its capacity to grow while delivering a strong bottom line. From 2015 until 2019, the biotech giant’s sales increased by over 40% with its operating margin rising as well.

While it’s undeniable that this global biotech stock has gotten itself caught up in the COVID-19 whirlwind that managed to hurt virtually every sector, its downside alternative makes absolutely no sense.

No one has the ability to predict and control when they get sick or what type of illness they get afflicted with, which makes the biotech sector and specifically drug developers particularly safe bet whatever the financial climate is.

So, investors looking for a stable stock can now afford to buy (GSK) shares at approximately 10 times worth of next year’s per-share profit potential. As if that’s not enough, the company also offers a mouthwatering 7.5% dividend yield.

Keep in mind that a wise way to insulate your portfolio amid the fears of a market crash is through investing in stable businesses that offer products and services needed on a daily basis.

If the companies provide essential items in both good and bad times, it’s a good sign the stocks will be able to survive any market crash.

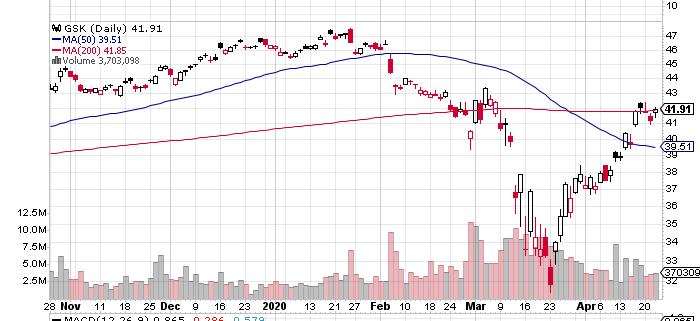

(GSK), which is currently at an 11-year low due to the pandemic and economic crisis, is worth considering.

![]()

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but take advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

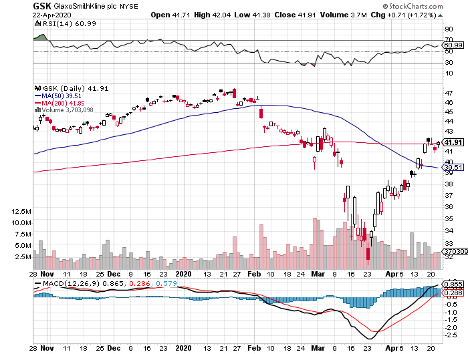

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but takes advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

Mad Hedge Biotech & Healthcare Letter

April 14, 2020

Fiat Lux

Featured Trade:

(ELI LILLY’S CORONA LEAP FORWARD)

(LLY), (GSK)

Eli Lilly (LLY) is one of the major biotechnology companies that have been working double-time to develop a coronavirus disease (COVID-19) cure, and the company shared its progress in this field.

According to this top biotech company, its partnership with the National Institute of Allergy and Infectious Diseases will explore the potential of Olumiant as a COVID-19 treatment.

This drug was first approved in June 2018 as a rheumatoid arthritis medication. Health experts believe that its anti-inflammatory effects on the immune system could be effective as a COVID-19 cure.

The clinical trial for Olumiant will involve COVID-19 patients in the US, with results available within two months.

Other than this Olumiant trial, Eli Lilly has another potential COVID-19 clinical trial already in Phase 2 for an experimental antibody treatment currently dubbed LY3127804.

This trial will involve pneumonia patients diagnosed with COVID-19. These patients are at a higher risk of acquiring acute respiratory distress syndrome (ARDS). The antibody treatment trial is slated to begin by late April at several US centers.

Apart from these experimental treatments, Eli Lilly is also taking an active part in providing testing centers to frontliners in its home state Indiana.

In March, Eli Lilly launched drive-through testing centers for active healthcare workers. This initiative was in partnership with the Indiana State Department of Health and backed by the U.S. Food and Drug Administration.

Eli Lilly’s centers test for the SARS-CoV-2 virus, which is the type that caused COVID-19. This service is offered free of charge to frontliners.

Outside its COVID-19 efforts, Eli Lilly has been active in developing its pipeline.

The latest deal towards this end is with privately held company Sitryx, which focuses on creating drugs for cancer and inflammatory diseases.

The partnership involves a five-year collaboration culminating in the development of four drugs. Eli Lilly has already selected two lead projects from Sitryx’s pipeline to be the first drugs they’ll submit for licensing.

Founded in 2018, all projects in Sitryx’s pipeline are still in the preclinical phase. The company is also comprised of widely known immunology experts, with another biotech heavyweight GlaxoSmithKline (GSK) contributing to its technology.

According to the terms of the collaboration, Sitryx will handle drug discovery while Eli Lilly will fund the clinical development as well as the marketing efforts.

Sitryx will get $50 million from Eli Lilly upfront, with the Indianapolis biotech company making an additional $10 million equity investment.

Meanwhile, the smaller biotech is eligible to almost $820 million if the development milestones are reached. Sytrix is also entitled for royalties.

Amid the pandemic, Eli Lilly is riding the momentum of its previous quarters and is still aiming to deliver a promising growth this year.

Coming off a strong 2019 fourth quarter, the company saw an 8% year over year growth in its top line. The entire year’s sales also went up by a modest 4% from how much they earned in 2018.

As for earnings per share (EPS), the said quarter showed off an impressive 49% year over year jump to reach $1.64. Meanwhile, the entirety of 2019 recorded an EPS of $8.89 which is more than twice 2018’s $3.13 total.

For Eli Lilly’s 2020 performance, the company is anticipating more growth, especially after the completion of its $1.1 billion all-cash acquisition of Dermira.

This acquisition opens a plethora of opportunities for Eli Lilly, particularly in the dermatology medicines sector.

A prime example to illustrate potential growth is Dermira’s top-selling product Qbrexza, which is used to treat excessive underarm sweating. This bestselling item boosted Eli Lilly’s quarterly sales by 27%, increasing the revenue from $8.1 million to $10.2 million.

Even without the collaborations, Eli Lilly can stand on its own as a solid buy.

The company has shown a strong operating margin, staying over 20% in all the previous 10 quarters. Moreover, its free cash flow of $3.5 billion and consistent revenue generation platforms through the years, Eli Lilly is in a good position to take on more acquisitions down the road.

Basically, Eli Lilly is ideal for investors on the lookout for a biotech stock that you can buy and just forget.

Only a handful of sectors managed to escape the coronavirus pandemic unscathed as practically every stock suffered a 20% drop over the course of the past months. I believe there’s one group that merits our attention even in the midst of this pandemonium: the biotech sector.

I think biotech stocks will roar back soon enough, and buying shares of solid and well-managed biotech companies that pride themselves with promising product lineups and solid pipelines should be rewarded in the long run.

Among these biotech stocks, Eli Lilly is one of the best-positioned growth stories. Investors searching for a port in this coronavirus storm might want to take a good look at this biotech stock.

Global Market Comments

March 31, 2020

Fiat Lux

Featured Trade:

(MORE PLAYERS ENTER THE RACE FOR A CORONA CURE)

(MRNA), (ARCT), (JNJ), (SNY), (GOVX), (ALT), (NVAX), (GSK), (GNBT), (VXL.V), (INO), (APDN), (CADILAHC)