Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEW MAN IN TOWN) (TSLA), (GOOGL), (AMZN), (NVDA),(SPY), (USO), (XLK), (SOXX), (NVDA), (IGV), (DELL), (IBM), (AAPL), (SPCX), (TSLA), (DAL), (BRK/B), (XLY), (XLF), (GS), (MS), (IWM), (KRE), (XRT), (XLF), (WMT), (XLC), (SLV)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or IRAN WAR SETS MARKETS ON FIRE),

(USO), (GLD), (SLV), (TLT), (GS), (FCX),(XOM), (PFE), (BMY), (PFE),(XLF), (IWM), (TAB), (NVDA), (DGE.L), (IBM), (DHI), (AMD)

Below please find subscribers’ Q&A for the September 11 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe Nevada.

Q: Will the Fed cut by 50 basis points at their next meeting?

A: The probability of that happening actually dropped by about half with the warm CPI report this morning with core CPI at 0.3%. That may have pushed the Fed from a 50% basis point rate cut back down to only 25%. I think if we only get 25%, the market will sell off. So that’s Wednesday next week. Mark that on your calendars—the market may well be on hold until then.

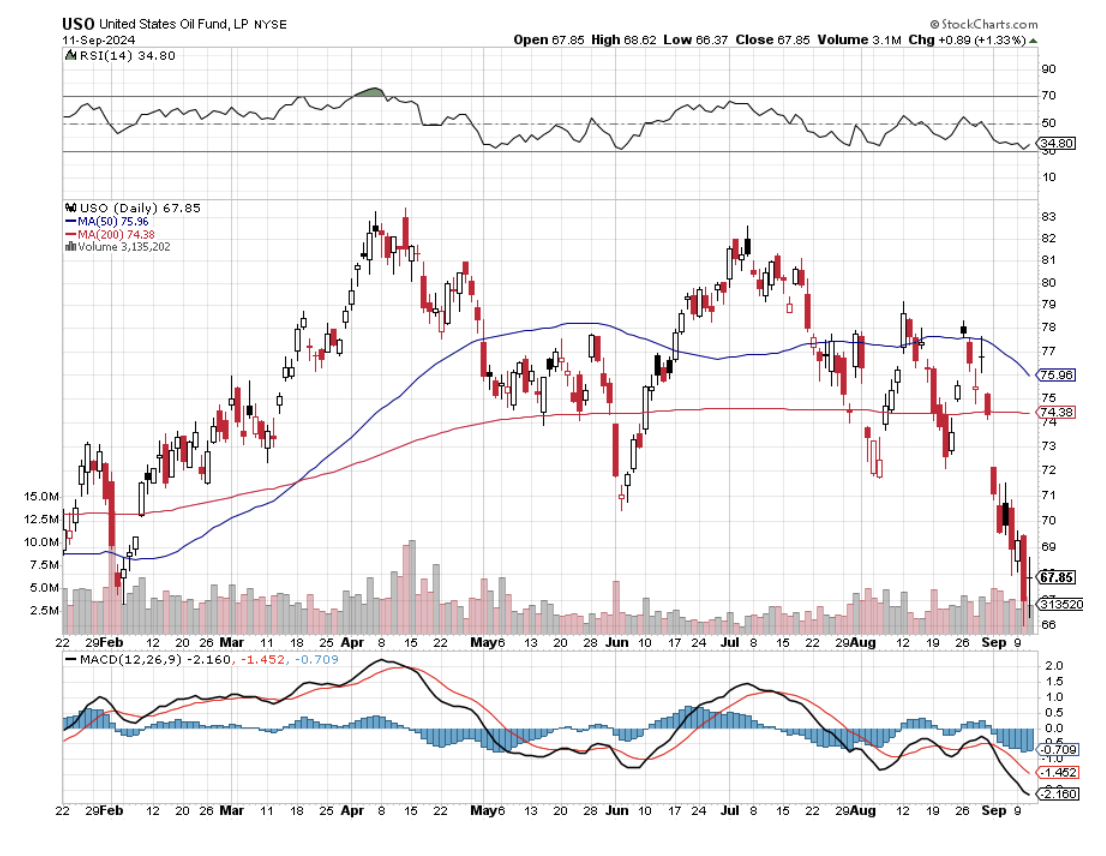

Q: Is $50/barrel oil (USO) coming by the end of this year?

A: No, but I think $60 is in the works. And that may be the bottom of this cycle because after that we expect an economic recovery, greater demand for oil, and rising prices in 2025. Until then, overproduction both in the US and in the Middle East is knocking prices down.

Q: Will the US dollar (UUP) continue its terrible performance through the end of the year?

A: Yes, and in fact, it may be for the next 10 years that the US dollar is weak—certainly 5—so any rally or dips you get in the currencies (FXA), (FXE), (FXC), and (FXB) I’d be buying with both hands.

Q: Where are you hiding at the moment?

A: 90-day T-bills, which are yielding 4.97%. You can buy and sell them any time you want, and the interest is only payable when you sell them.

Q: Is September 18th the selloff?

A: It depends on how much we do before then. Obviously, we’re making good progress today with the Dow ($INDU) down 700 points, so we shall see. However, the market is flip-flopping every other day, making it untradable—you can’t get any position and hold on to it long enough to make money, so it’s better just to stay out. There’s no law that says you have to be in the market every day of the year, and this is a day not to be in the market for sure.

Q: How will the presidential debate reaction affect the market?

A: There’s only one stock you have to follow for that and that’s the (DJT) SPAC, and that’s Trump’s own personal ETF, and it is down 13% today to a new all-time low. I believe that’s well below its IPO price, so anyone who’s touched that stock is losing money unless they got out at the top. That is a good signal.

Q: JP Morgan (JPM) stock had a steep pullback to $200/share—is it a buy here?

A: No, but we’re getting close. If we can get (JPM) close to its 200-day moving average at $188 on high volatility, that would be a fantastic buy, because (JPM) will benefit enormously from falling interest rates, and it is the world's quality banking play.

Q: Is it too soon on Berkshire Hathaway (BRK) and Tesla (TSLA)?

A: Yes on both. It’s too soon for anything right now. I wouldn’t touch anything before the interest rate cut unless you have a really special situation, and there are some out there.

Q: Do you think Nvidia (NVDA) could test $90 again?

A: It could very easily; it got within $10 of that last week. So, it just depends on how bad the news is and how scared people get in September.

Q: Is the end of carry trade affecting the market?

A: No, we had a big deleveraging there. Although people are going back in again now, it’s not enough to hurt the market.

Q: I heard Putin is threatening over raw materials. What do we get from Russia, and what stocks or ETFs would be impacted?

A: We get nothing from Russia anymore. We used to get a lot of commodities and oil from them, and that has ceased. Russia has essentially exited the global economy because of the sanctions and the war in Ukraine, so they can’t really hurt anyone at this point.

Q: What about Russia doing an end-run around with direct trade? BRICS block is going to make the dollar even more worthless in the future.

A:I don’t buy that at all. I’ve been covering sanctions for 50 years; they always work, but they always take a long time. You could always do black market trade through the back door, but the volumes are way down, and the profits are much less because people only buy sanctioned goods at big discounts. The oil that China is buying from Russia is something like a 30% discount to the market. They execute a high cost of doing business, and nobody wants to be in sanctions if they can possibly do avoid. That said, when the war ends, the sanctions may end. That could be some time next year when Russia completely runs out of tanks and airplanes.

Q: Should I buy Nvidia (NVDA) call options now?

A: It's not just a matter of Nvidia. It's what the general market is doing, and tech is doing. And tech is not doing that well—even on the up days. So I would hold off a bit on Nvidia.

Q: Why is Warren Buffet (BRK/B) unloading so much of his equity portfolio?

A: He thinks the market is expensive, and he has thought it has been expensive for years and he's been unloading stocks for years. He has something like $250 billion in cash now so he can buy whole companies in the next recession. Whether he'll live long enough to see that recession is another question, but his replacement staff is already at work and running the fund, so Berkshire will continue running on autopilot even after he’s gone.

Q: Is IBM an AI play?

A: (IBM) wants to think that it’s an AI play. They haven’t disclosed enough to the public to make the stock a real AI investment, so I would say it probably is, but we don’t know enough at this point, and there are probably too many other candidates to buy in the meantime.

Q: How do I invest in green energy stocks, and do you have any names for me?

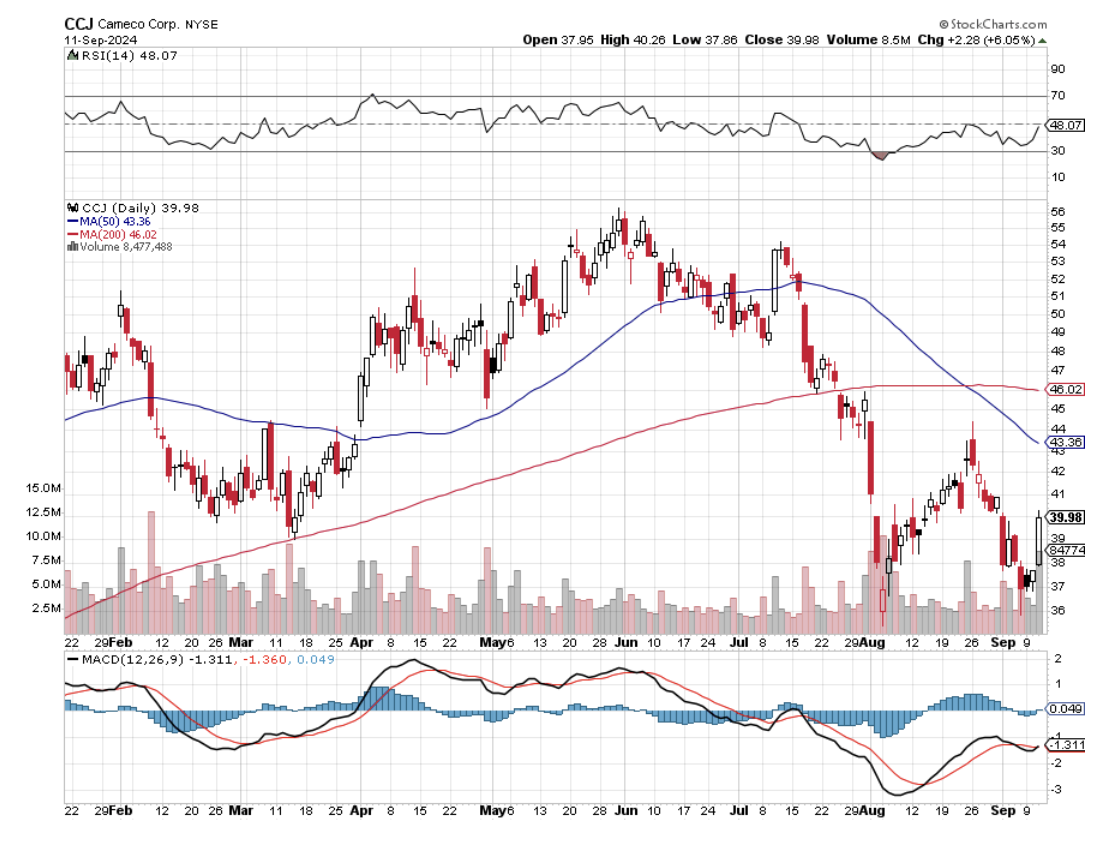

A: Well here’s one right here and that’s the Canadian uranium producer Cameco (CCJ). There is a nuclear renaissance going on. China just announced an increase in their plants under construction from 100 to 115. You have the new modular technology ready to take off in the US, and it uses uranium alloys, or uranium aggregates, so it’s impossible for a plant to go supercritical. You also have other countries reactivating nuclear plants that have been closed, and California even delayed its Diablo Canyon shutdown by 5 years. So Nuclear is back in play, and we have an absolute bottom in the stock here and it just dropped 37%, in case you needed any more temptation. So this would be a very attractive alternative energy play for the long term right here.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Remember the last time you had to pop a pill that felt like a one-size-fits-all solution? I sure do. It was for a nagging cough, and while it did the trick, the side effects left me feeling like I'd been hit by a truck.

Turns out, Big Pharma is facing its own kind of side effects. They spend an average of $2.6 billion and over a decade to bring a new drug to market. That's like betting on a long shot at the Kentucky Derby, but with way worse odds.

But what if we could change the game entirely? What if drug discovery wouldn’t solely be about blindly mixing chemicals and hoping for the best.

Instead, picture a super-smart robot scientist, capable of reading millions of pages of medical research in seconds, understanding how different molecules interact, and even predicting which ones might be effective against a disease.

This AI-powered scientist could then design experiments to test those molecules, analyze the results, and even create new molecules from scratch, tailored to specific diseases and individual patients.

That's the promise of autonomous drug discovery.

While we've already seen robots and miniaturization speed up the drug discovery process, AI is taking it to the next level. I’m talking about AI agents running the entire show, from brainstorming biological theories to designing and running experiments, all with barely a human finger lift.

This isn't just about efficiency. It's a veritable gold mine of benefits: costs slashed, development times cut down, success rates skyrocketing, and a productivity boost that could revolutionize personalized medicine. And why does that matter?

Because it means treatments that are more effective, safer, and tailored to your unique genetic makeup, medical history, and lifestyle. Imagine popping a pill that's not just designed to treat your disease, but designed specifically for you. That's the kind of future autonomous drug discovery could deliver.

Imagine a world where your next prescription is fine-tuned to your genetic makeup, your medical history, your lifestyle. Sounds like bespoke tailoring, but for your health.

And this isn't just hype – it's backed by hard numbers. A recent study by McKinsey & Company found that AI-enabled drug discovery could potentially generate up to $50 billion in annual value by 2026.

The study also highlighted that AI could reduce the time required for drug discovery by up to 50%, while also improving the success rate of clinical trials.

These aren’t merely some abstract predictions either. In fact, some companies are already making waves in this new world of drug discovery.

Recursion Pharmaceuticals (RXRX), for example, is at the forefront of these innovations. They've developed a radical new drug discovery platform that combines advanced robotics, experimental biology, and machine learning to rapidly identify potential new treatments for a wide range of diseases.

Forget dusty labs and slow, painstaking research. Recursion's approach is like giving Sherlock Holmes a supercomputer to solve medical mysteries, and the results speak for themselves: over 2,000 novel biological relationships discovered and a mind-boggling 150 terabytes of relatable biological data generated.

That's the equivalent of roughly 30 million songs, all focused on cracking the code of human biology and disease.

Recursion isn't the only player here. A slew of innovative companies are riding the AI wave, reimagining the drug discovery landscape.

Schrödinger (SDGR) is turbocharging the process with AI and computational wizardry, using algorithms to predict how potential drugs will behave in the body before even stepping foot in a lab.

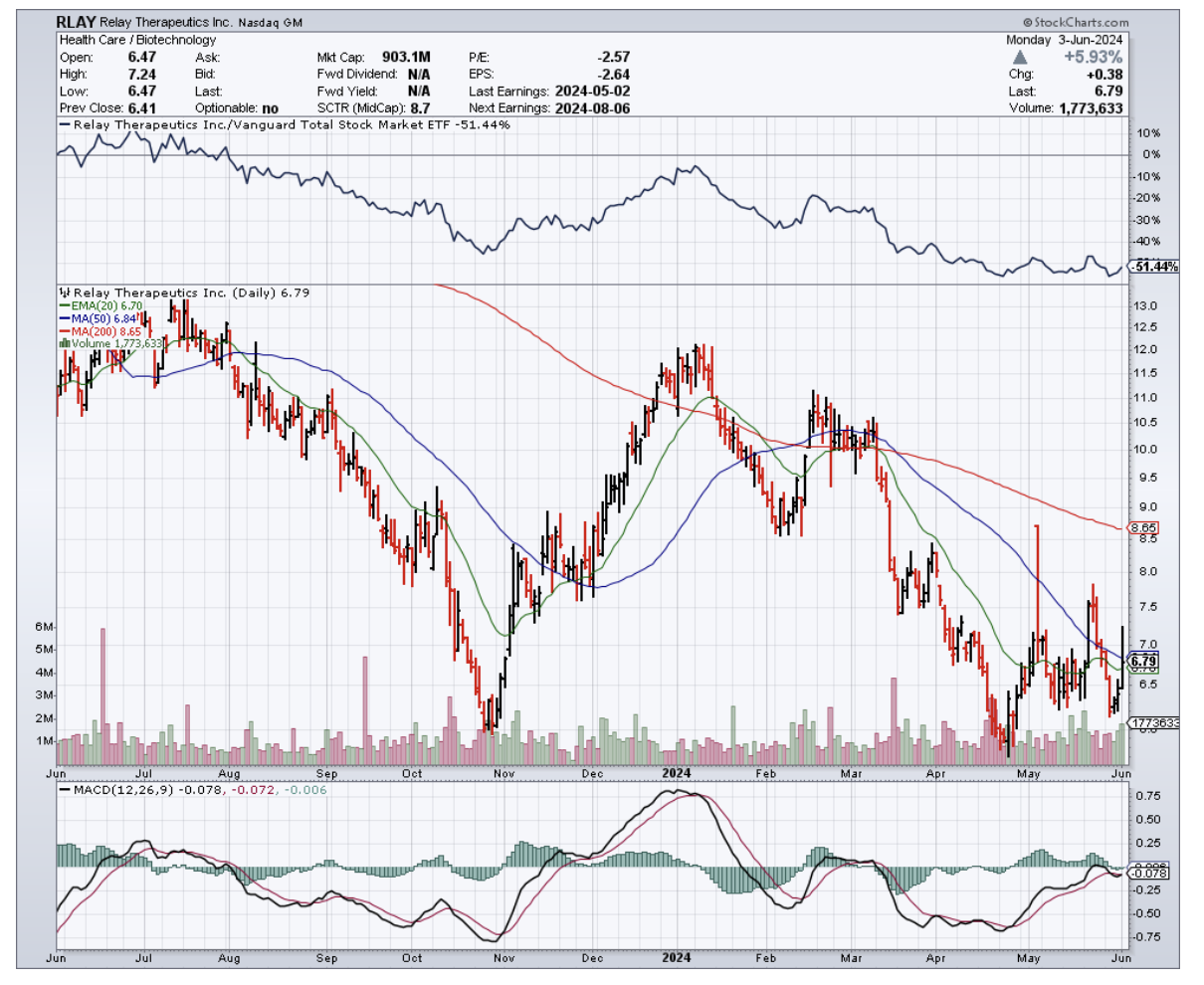

Relay Therapeutics (RLAY) is forging new paths by marrying cutting-edge computation with experimental techniques, focusing on how cancer cells move and change shape to develop targeted therapies.

Exscientia (EXAI), the AI-driven pharmatech company, is designing and discovering new drugs with unprecedented speed, while AbCellera Biologics (ABCL) is harnessing the power of AI and machine learning to decode the secrets of our immune systems, hunting for antibodies that could be developed into life-saving drugs. It’s basically like having a crack team of digital detectives scouring your immune system for clues to fight off diseases.

Meanwhile, BenevolentAI (AMS: BAI) is the top name when it comes to clinical-stage AI drug discovery, using a potent combination of AI, machine learning, and cutting-edge science to unravel the complexities of disease biology and unearth novel treatments. They're not simply content with throwing darts at a target. This company is using AI to pinpoint the bullseye.

But, this AI-powered revolution of the healthcare world isn't happening in a vacuum. It's being supercharged by a tag team of tech titans who are bringing their AI firepower to the table.

Think of it as the Avengers assembling to fight disease, but instead of superpowers, they're armed with algorithms and cloud computing.

Nvidia Corporation (NVDA), IBM Corporation (IBM), and Microsoft Corporation (MSFT) are leading the charge, providing the AI muscle needed to accelerate drug discovery.

Nvidia's Clara Discovery platform, IBM Watson Health, and Microsoft Azure's AI and machine learning services are all being harnessed to build, train, and deploy AI models for a wide range of applications in the biotech and healthcare sectors. It's like having Tony Stark, Bruce Banner, and Thor all working together to create the next medical breakthrough.

And this isn't some wishful thinking. The use of AI in biopharma R&D is projected to skyrocket, growing at a compound annual growth rate of 30% to 40% over the next five years.

Plus, the impact could be huge: AI could potentially boost clinical trial efficiency by 15% to 20% and slash the overall cost of drug development by 10% to 15%. Talk about a win-win situation.

All in all, it’s clear that this AI drug discovery thing isn't just a fad. It's a full-blown revolution that's shaking up the healthcare world as we know it. And while it's still in the early innings, it would be wise to keep a close eye on it. I'm not saying you should throw all your money in right this second, but seriously, put the companies above on your radar.

These are the trailblazers leading the charge into the future of personalized medicine. Who knows, they might just be the ticket to a healthier portfolio—and a healthier you.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-04 12:00:562024-06-04 12:21:21From Petri Dish To Personalized Prescriptions

This earnings season is chugging along exactly like I thought it would play out.

The haves are covering for the have-nots.

Sadly, the pixie dust isn’t encompassing all tech stocks, but just enough sprinkles so investors don’t start selling.

That is what matters most and sure, investors can knit-pick all they want, but there have been just enough positive numbers to be repackaged as a win for AI and the advancement of tech even if the proverbial goalposts are widening.

Competition has reared its ugly head as tech services fight for the extra consumer and enterprise dollar in a global economy where demand is being squeezed by sticky inflation.

That’s not good news for many of the smaller companies that are unproven and tap debt by delivering a promising story to prospective investors.

Remember that Mr. Market is undefeated and price will always find its natural equilibrium.

The question is how long will it take to find that natural equilibrium?

Since 2020, many would say that the irresponsible monetary policy in many areas of the world has contributed to markets unable to match up buyers and sellers at a reasonable price.

There is some truth to that but let’s see who that benefits.

My belief is that strong tech companies have overly benefited from this type of fiscal backdrop because they can always fall back on a strong balance sheet like in Google’s case where it suddenly issued a dividend.

View it as a rainy day fund if you will where they can wield when need be.

The extra buffer zone of safety has allowed a company like Microsoft to focus on Azure growth, of which 7% was related to AI, up from 6% of impact in the previous quarter.

Microsoft provides cloud services for the ChatGPT chatbot from startup OpenAI, and companies have been increasingly adopting Azure AI services to develop their capabilities for summarizing information and writing documents.

It’s a good problem to have when capacity bottleneck cuts into the AI portion of Azure growth.

Companies tapping that AI story are the only tech companies in 2024 that Mr. Market is keeping safe and that must scare or enthrall you depending on who you are.

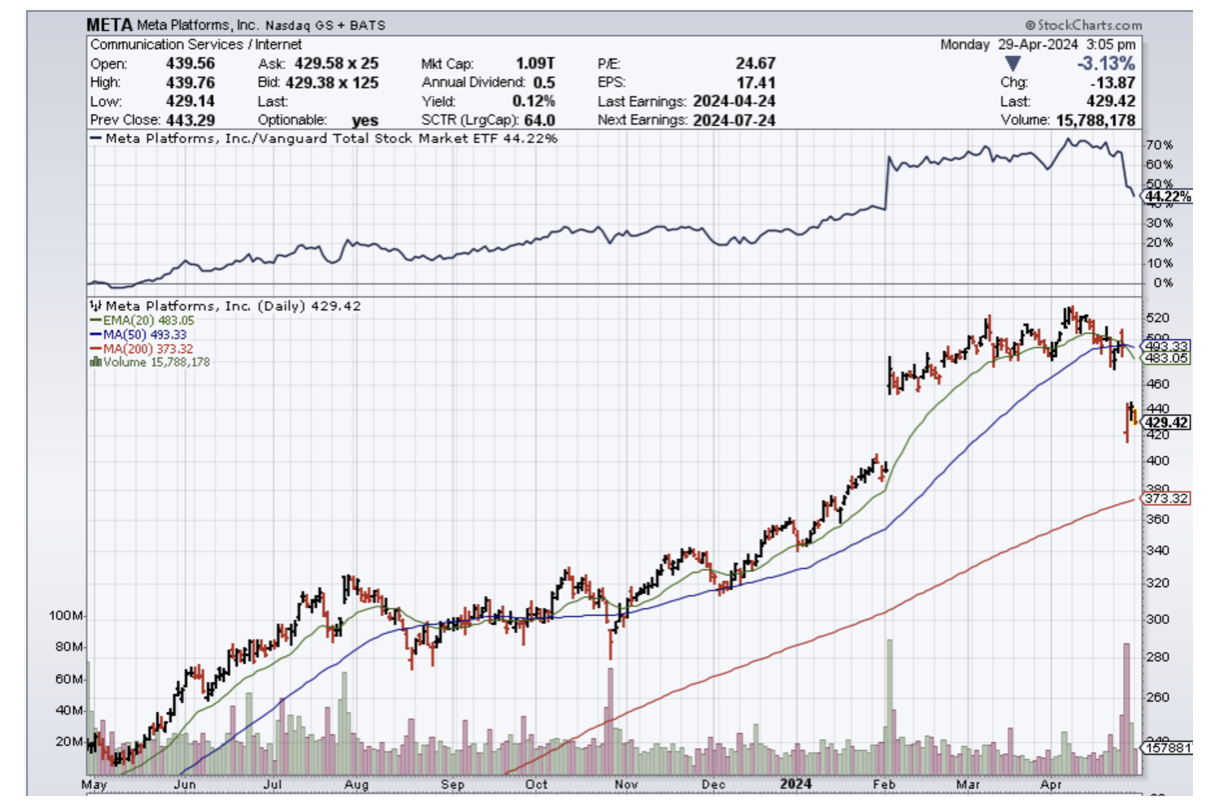

Meta (META) materially lifted its full-year capital expenditures guidance and signaled even bigger spending in 2025 — all because of unknown AI projects. Running tech businesses isn’t getting cheaper so imagine how small companies feel about that.

It’s Ford (F) losing lots of money on EVs because of higher-than-expected costs.

Meanwhile, IBM (IBM) CFO Jim Kavanaugh struck a more cautious note when asked about soft sales at its lucrative consulting business blaming the macroeconomic backdrop.

It’s not all smooth sailing in tech land and readers need to be vigilant.

It’s not the time to take some speculative Hail Mary on some far reach.

Don’t draft a 7th-round prospect in the 1st round.

Price action has been unkind to tech firms with poor balance sheets in 2024 and I believe that trend to continue until the Fed can finally tamper inflation back to reasonable levels.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-29 14:02:562024-04-29 16:12:26Just Good Enough

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

How high are we talking? How about a Dow Average of 240,000 by 2035, up another 515% from here? That is a 40-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion or more in corporate stock buybacks for the past decade.

I’m not talking pie-in-the-sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th-century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000, the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my dad’s generation that meant loading your portfolio with US Steel (X), IBM (IBM), and General Motors (GM).

For my generation, that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on NVIDIA (NVDA), Netflix (NFLX), Amazon (AMZN), Meta (META), and Alphabet (GOOGL). Oh, and they like Bitcoin too (BITO).

That’s why the Magnificent Seven account for all of the past year’s monster gains.

There is another gale force tailwind pushing stocks up. The enormous profits created by artificial intelligence are essentially replacing the Federal Reserve as an unlimited source of liquidity. If you missed the quantitative easing and the free money of the 2010s, you get another pass at the brass ring. But you have heard me talk about this before so I won’t bore you.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 240,000, we need to squeeze in a recession. Bear markets in stocks historically precede recessions by an average of seven months. But for the time being, it looks like smooth sailing.

When I get a better read on precise dates and market levels, you’ll be the first to know.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/03/john-thomas-snow.jpg285259april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-06 09:02:172024-03-06 10:09:22Why the Dow is Going to 240,000

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.