Global Market Comments

February 16, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or A RETURN TO IRRATIONAL EXHUBERANCE)

(PLBY), (SPX), ($INDU), (NVDA), (AMD), (MU), (USO)

Global Market Comments

February 16, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or A RETURN TO IRRATIONAL EXHUBERANCE)

(PLBY), (SPX), ($INDU), (NVDA), (AMD), (MU), (USO)

Playboy is going public.

Its flagship magazine was wiped out by free internet porn last year after a storied 66-year run. During the 1970s, an invitation to a new club opening was the hottest ticket in town.

Of course, I bought the magazine only to read the articles.

Melania Trump as a centerfold? The business possibilities boggle the mind. Of course, it’s going public through a SPAC. Nobody else would touch this with a ten-foot pole. The ticker symbol will be (PLBY).

What this IPO does tell me is how overheated the markets are getting. In 1996, former Fed governor, saxophone player, and Ayn Rand acolyte, the gnomish Alan Greenspan warned the stock market of “irrational exuberance.” Since then, the Dow Average has risen by 5.2 times in 23 years, revisiting the 6,000 low once in 2009.

In fact, let me explain to you why stocks are so cheap.

At the 2000 Dotcom Bubble top, ten-year US Treasury yields stood at 6%. Stocks would have to rise five times more from today’s paltry 1.20% to reach the same relative valuation.

Dow 163,000 anyone?

Similarly, the big FANG stocks would have to triple in value to get us to the 100X price earnings multiple that prevailed in 2000. That gets us at least to Dow 94,500.

And this is what people don’t get about liquidity-driven bull markets. They go on far, far longer than anyone imagines possible. You had to be in Tokyo in 1989 to understand this.

If you’re really and truly worried about stocks, take a look at the chart below and how they reacted to the last catastrophic selloff that took place during 2007-2009.

After an initial, frenetic move, they rose by, you guessed it, 5.2 times.

The Global Chip Shortage is spreading beyond cars to phones and electronics. High prices beckon across the board. Could this be the black swan that heads off the recovery? It’s all a screaming BUY for (NVDA), (AMD), and (MU). I can’t believe these haven’t moved yet.

Biden created a Bull Market in Oil (USO) when he banned new leases on federal lands. The move took 3 million barrels a day off the market, taking a bite out of the 10 million barrels a day oversupply. And economic recovery should soak up the remaining 7 million barrels, 2021 forecasts for Texas tea are now reaching as high as $80.

Space X is taking pre-orders for Starlink, Elon Musk’s Global satellite WIFI network. Another industry disrupted. For a $99 deposit, you can access 500 megabytes a second, faster than available for most of the US. The goal is to launch 11,943 satellites by 2024. If it works, AT&T (T), Comcast (CMCSA), and Verizon (V) could be in big trouble. When you own your own rocket company, it’s easy to undercut the competition.

Weekly Jobless Claims are still weak, at 793,000, far higher than expected, but less than last week. Total jobless claims have it an unbelievable 20.44 million, just short of the 1930’s Great Depression high. Perhaps 20% of the country is living on government handouts.

The Pandemic Property Boom continues, posting the hottest numbers since 2005. The National Association of Realtors says the price of a single-family home rose by a staggering 14.9% in Q4. The Northeast was the leader at a 21% gain. The market keeps going from strength to strength.

Will the Dow double in a year? We only have 4,500 points to go for a 100% gain from the last March 20 low. We have already seen the sharpest gain in history, beginning when Biden took the lead in the primaries. Will passage of the $1.9 trillion rescue package take us over the finish line? And are we setting up for a “Buy the rumor, sell the news? We’ll know in a month. I bet you’ve just made more money in stocks than you’ve ever imagined possible. Take short-term profits in everything.

Bonds hit new lows, taking the ten-year US Treasury yield up to 1.20%. The Feds hit the markets for a massive $120 million in debt this week and buyers are obviously glutted. Keep selling those rallies in the (TLT). Maybe you should start selling dips, too. Use bond selloffs for your stock market timing. They’re about to become “certificates of confiscation” again.

No hint of rising rates soon, hints Fed governor Jay Powell. Recovery is the only goal, damn the inflation torpedoes.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned an amazing 16.48% so far in February after a blockbuster 10.21% in January. The Dow Average is up a trifling 2.80% so far in 2021.

This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 26.69%. There are only four trading days left until the February 19 option expiration, when I automatically go into 80% cash. That’s convenient!

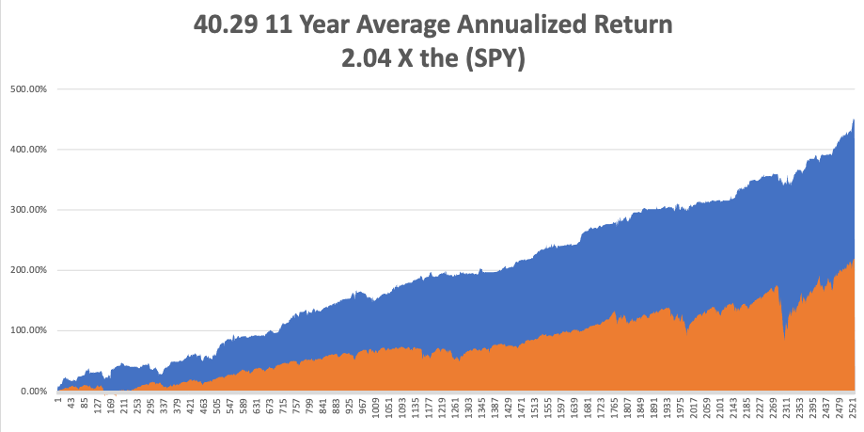

That brings my 11-year total return to 449.24%, some 2.04 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an Everest-like new high of 40.29%.

My trailing one-year return exploded to 90.96%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 108.63% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 27.7 million and deaths approaching 500,000, which you can find here. We are now running at a heartbreaking 3,000 deaths a day. But that is down 35% from the recent high.

The coming week will be a boring one on the data front.

On Monday, February 15, markets are closed for Presidents Day.

On Tuesday, February 16 at 8:30 AM EST, the NY Empire State Manufacturing Index is out. CVS (CVS) and Zoetis report.

On Wednesday, February 17 at 8:30 AM, US Retail Sales for January are published. At 2;00 PM, we learn the Fed Open Market Committee minutes from the last meeting. Shopify and Twilio report.

On Thursday, February 18 at 9:30 AM, Weekly Jobless Claims are printed. Barrick Gold (GOLD) and Roku (ROKU) report.

On Friday, February 19 at 10:00 AM, Existing Home Sales for January are released. We learn the Baker-Hughes Rig Count. As we have a three-day weekend following, option volatility should collapse. John Deere (DE) reports.

As for me, let me tell you what the last weeks of the great Japanese bull market were like at the end of 1989.

The big thing then was to eat sushi salted with flecks of pure gold. Any foreigner who could speak Japanese was worth hundreds of thousands of dollars a year.

The brokers would hire anyone. Kids went from running sandwich shops to trading desks at Morgan Stanley. Others upgraded from bicycles to Porsche Carrera’s and used to race on Tokyo’s abandoned freeway system in the middle of the night.

And you know what? Someone offered me a piece of gold-flecked sushi just the other day!

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 9, 2021

Fiat Lux

Featured Trade:

(ON EXECUTING MY TRADE ALERTS),

(TEN REASONS WHY STOCKS CAN’T SELL OFF BIG TIME),

(SPY), (INDU), ($COMPQ), (IWM), (TLT), (GME)

Global Market Comments

February 8, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE SWEET SPOT CONTINUES),

(INDU), (SPY), (SLV), (GME), (TLT), (JPM), (BAC), (C), (BLK)

We just completed the best week in the 13-year history of the Mad Hedge Fund Trader.

Kudos have been coming in from all over the world, with stories of retirements financed, mortgages paid off, and college educations paid for. Some Mad Hedge Concierge clients are reporting windfall profits of $1 million a day.

The key was calling the GameStop (GME) fiasco the one hit wonder that it was, and using it as an opportunity to go 100% long, pedal to the metal, and bet the ranch. When the market gives you a gift, you grab it with both hands as if your life depended on it and don’t let go.

It worked.

That’s what 50 years of practice gets you, the ability to spot the gold coins lying on the street ignored by everyone else and pocket them immediately.

A record $4.2 billion poured into technology stock funds last week as investors call the end of the six-month big tech correction. The barbell approach is working like a charm, with buying bouncing back and forth like a ping pong ball between domestics, technology, or both sectors go up at the same time. It’s better than owning a printing press for $100 bills.

The Mad Hedge Technology Letter also spotted which way the gale force winds were blowing and piled on the longs as well. (AMZN), (QCOM), and (CRWD), it’s all music to my ears. My old friend Jeff retired, paving the way for another doubling in his stock (AMZN).

We now are getting a clearer picture of how 2021 will play out in the stock market. Periods of sideways action will be followed by big gaps up, eventually taking us to a Dow Average of 40,000.

The sweet spot continues. As low as interest rates and inflation remain low and a tidal wave of new money is pouring into the economy, you have a rich uncle writing you a check every month from the stock market.

We have not had a correction of more than 4% since October. This could go on for years.

Where will the next surprise come from?

When Joe Biden gets his full $1.9 trillion in upfront rescue spending. With the grim tidings of three disastrous monthly jobs reports out, it couldn’t go any other way. The cost of waiting is just too high, especially for the 18 million U-6 unemployed and millions of small businesses hanging on by their fingernails.

The Nonfarm Payroll Report came in very weak, at 49,000 in January. The headline Unemployment Rate was at 6.3%, a decline as more people are leaving the workforce. The U-6 broader “discouraged worker” unemployment rate is still at 11%. December was revised down to an even bigger 227,000 loss. Construction was down 10,000, Retail down 37,000, and Government Jobs were up 43,000. It’s the third disappointing month in a row so a double-dip recession is still on the table. We have a very long road to recovery.

Weekly Jobless Claims improved, dropping to 779,000, the lowest since November. The correlation with falling Covid-19 cases is almost perfect, which have declined by 35% in two weeks. Is the stock market getting ready to roar?

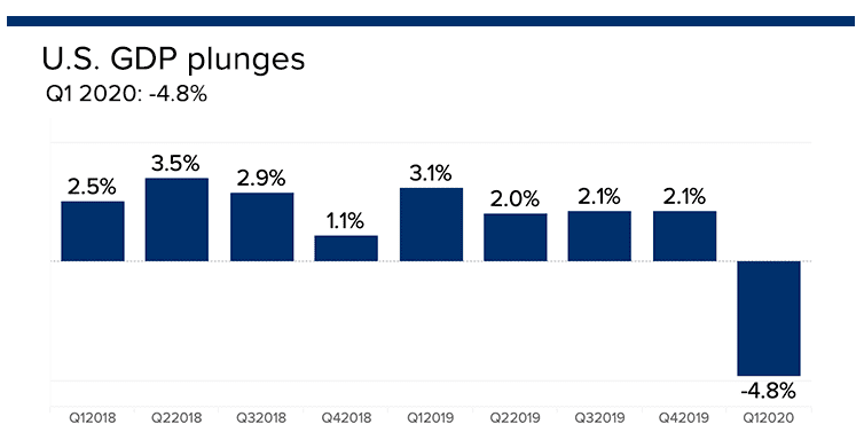

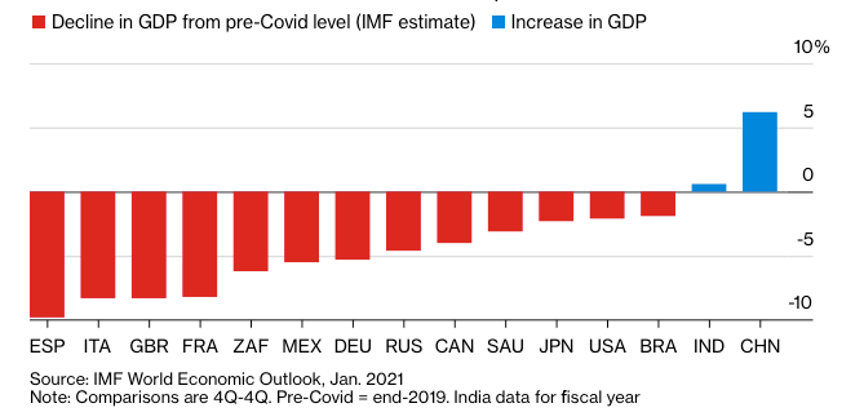

US GDP fell by 3.5% in 2020, wiping out all of 2019 and a good chunk of 2018 as well. The last quarter of 2020 came in at -4.8%, much worse than expected, and further downward revisions are coming, according to the Bureau of Economic Analysis. The economy won’t recover pre-pandemic levels until late 2022 or 2023. The biggest drags on the economy were dramatic falls in consumer spending, nonresidential fixed investment, and a trade war-induced plunge in exports.

Pending Home Sales fell, 0.3% in December, but are still up a staggering 21.4% YOY. It is the highest December reading on record, but the fourth straight month of declines. A historic shortage of supply is the main reason.

The short squeeze play moved to silver, with prices hitting an eight-year high. Many local dealers are seeing business rise tenfold over the weekend and are running out of inventory. The white metal was up 35% in two days. It’s the largest one-day volume every. This time, the kids may have got it wrong, since all short positions in the options market are fully hedged with long positions in silver futures or silver bars. The GameStop players only saw the short side. Long term, I love (SLV) for industrial demand from electric cars and solar panels and see it going from today’s $28 to $50, but not today.

Apple (AAPL) is boosting share buybacks and is borrowing to do it. It’s issuing $14 billion in bonds out to 40 years in maturity at 95 basis points above Treasuries. If Apple is so aggressive in buying its own stock, maybe you should too.

The Apple car is moving forward, as incredible as it may seem. The company is in talks with South Korea’s Hyundai to produce autonomous self-driving electric vehicles that will be available by 2024. I’ll believe it when I see it. I’ve seen Apple self-driving cars in the Bay Area for years. It’s an interesting combination: Apple software, a South Korean design, and non-union Georgian metal bashing combined. Sounds like a winner to me.

The GameStop (GME) game ends. Back to selling used video games in shopping malls. Millions were lost in the crash from $483 to $49. Back to buying real stocks with the systemic threat to the main market over.

Jeff Bezos retired, putting the operation of Amazon into the hands of Andy Jassy, the inventor and head of the cloud unit AWS. No move in the stock beyond the first few seconds. Jassy has been there since the beginning. If I were the second richest man in the world, after Elon Musk, I’d take some time off too. Now, maybe my former Morgan Stanley colleague will have drinks with me. Buy (AMZN) on dips. My two-year target is $5,000.

Bombs away for the bond market, as the (TLT) hits a new 2021 low, taking ten-year yields up to 1.13%. I’m taking profits on the last of my bond shorts and piling money into financials, which love higher interest rates. Buy (JPM), (BAC), (C), and (BLK) on dips. A 1.50% yield on the ten-year US Treasury bond here we come! This is the quality trade of 2021.

The ADP Private Employment recovered, up 174,000 in January after a 74,000 plunge in December. Leisure & Hospitality is the big variable.

PayPal transactions were up 25% in 2020, showing the incredible extent of the online migration of the economy. Keep going with Fintech. There’s another double in (PYPL).

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned an amazing 14.15% during the first week of February after a blockbuster 10.21% in January. The Dow Average is up 3.47% so far in 2021. This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 24.36%.

I absolutely nailed the market bottom created by the GameStop fiasco, which I didn’t expect to last any more than days. I went 100% leveraged long, which enabled me to achieve the astounding numbers I am reporting today.

Not only did I get the market right, I picked the perfect sectors as well. I jumped 60% into financials, 20% in Tesla, 10% for commodities, and 10% in chips. I used the bond market meltdown to cover the last of my bond shorts. But all of my financial longs are essentially bond shorts.

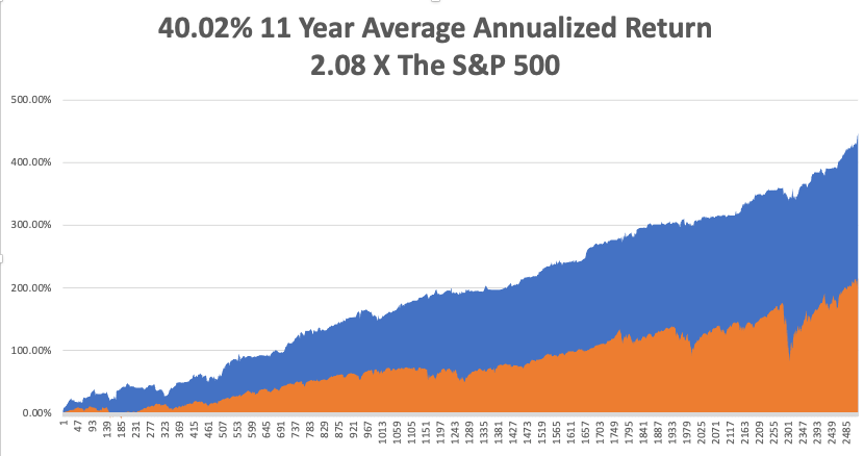

That brings my 11-year total return to 446.81%, some 2.08 times the S&P 500 over the same period. My 11-year average annualized return now stands at an Everest-like new high of 40.02%.

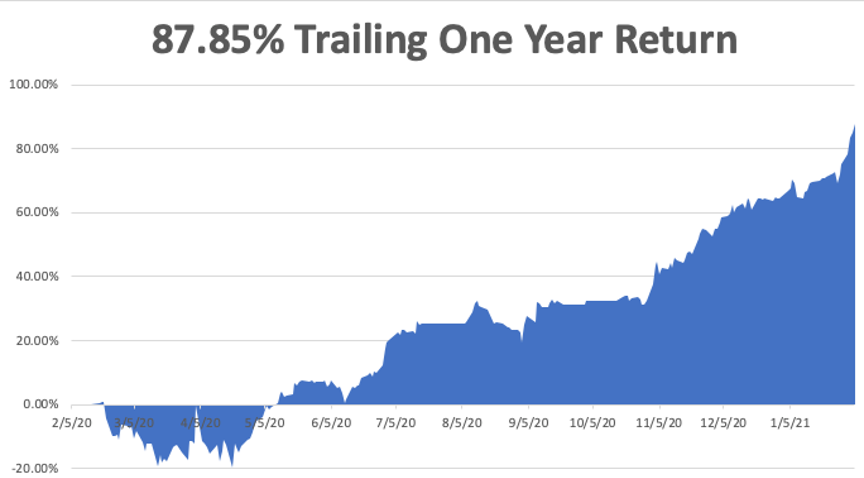

My trailing one-year return exploded to 87.85%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 105.58% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 27 million and deaths 465,000, which you can find here. We are now running at a heartbreaking 3,000 deaths a day. But that is down 35% from the recent high.

The coming week will be a boring one on the data front.

On Monday, February 8 at 11:00 AM EST, Consumer Inflation Expectations for January are out. Softbank (SFTBY) and KKR & Co. (KKR) report.

On Tuesday, February 9 at 6:00 AM, the NFIB Business Optimism Index is released. Cisco Systems (CSCO) and Twitter (TWTR) report.

On Wednesday, February 10 at 8:30 AM, the US Core Inflation Rate is announced. Coca-Cola (KO) and Uber (UBER) report.

On Thursday, February 11 at 9:30 AM, Weekly Jobless Claims are printed. Walt Disney (DIS) and AstraZeneca (AZN) report.

On Friday, February 12 at 2:00 PM, we learn the Baker-Hughes Rig Count. As we have a three day weekend following, option volatility should collapse. Moody’s (MCO) reports.

As for me, I went into Reno last week to replace the windshield on my Toyota Highlander, my Tahoe car, which below zero temperatures had cracked. One-third of the town was shut down and boarded up, while what remained was booming. A giant shopping mall near downtown has resumed construction, but with less retail and more residential. Reno is the third fastest-growing city in the US and has become a metaphor for the entire country.

Still waiting for my Covid-19 vaccination. I’m at the top of four lists. Even the military can’t get enough. With any luck, I’ll have it in weeks.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 1, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GAMBLERS HAVE ENTERED THE MARKET),

($INDU), (TSLA), (TLT), (BA), (JPM), (MS), (GME), (STBX), (GE), (MRNA)

At long last, the 10% correction I have been predicting is happening. No, it wasn’t caused by the usual reasons, like a bad economic data point, an earnings disappointment, or a geopolitical event.

The market delivered the worst week since October because gamblers have entered the stock market. Perish the thought!

It turns out that if a million kids buy ten shares each of a $4 stock, they can wipe out even the largest hedge funds on their short positions. It also turns out they can wipe out their brokers, with infinite capital calls triggered by massive order flows.

If Chicago’s Citadel had not stepped in with a $1 billion bailout, Robin Hood would have gone under last week. Citadel buys Robin Hood’s order flow and is their largest customer. That’s where systemic risk enters the picture.

And it’s not like there was really any systemic risk. Markets have an inordinate fear of the unknown, and no one has ever seen a bunch of kids in a chat room like Redditt wipe out major hedge funds.

Fortunately, there are only a dozen small illiquid stocks that could be subject to such ‘buyers raids”. So, the spillover to the main market is very limited, probably no more than a week or two.

And the regulations to reign in such a practice are already in place. Whenever a broker gets more business than it can handle, it will simply shut it down. Robin Hood did that on Friday when it has limited purchases in 20 stocks to a single share, including Starbucks (STBX), Moderna (MRNA), and General Electric (GE).

What all this does is set up an excellent buying opportunity for you and me, of which there have been precious few in recent months. By ramping up the Volatility Index to $38, it is almost impossible to lose money on front month call options spreads. We are the real winners of the (GME) squeeze.

Stocks would have to fall another 10%-20% on top of existing 10%-20% declines, and that is not going to happen in 13 trading days to the February 19 options expiration with $20 trillion about to hit the economy and the stock markets. That breaks down to $10 trillion in stimulus and $10 trillion worth of global quantitative easing.

My own long, hard-won experience is that a (VIX) at $38 earns you about 20% a month in profits. Options prices are so elevated that scoring winners now is like shooting fish in a barrel. So, join the party as fast as you can.

On Friday, I was taking profits on exiting positions and shipping out new trade alerts in the best quality names as fast as I could write them. Where is that easy, laid back retirement I was hoping for!

Keep at the barbell portfolio. The big tech names are finishing up a six-month sideways “time” corrections. Their earnings are catching up with valuations at a prolific rate. The domestic recovery names have just given back 10%-20% and are ripe for another leg up. All of these are good candidates for 2023 options LEAPS.

After all, if an insurrection and the sacking of the capitol can’t take the market down more than 1%, GameStop (GME) is certainly not going to take it down more than 10%.

GameStop (GME) posted record volatility, up from $4 a month ago to $483. Even the biggest hedge funds can’t stand up to a million kids buying ten shares each at market. All single name shorts in the market are getting covered by hedge funds in fear of getting “Gamestopped”, producing a 700-point Dow rally.

Several brokers banned trading in the name and the SEC is all over this like a wet blanket. Trading is halted due to an excess of sell orders. The problem is that funds are selling real stocks to cover the losses we own, like JP Morgan (JPM) and Tesla (TSLA) and short (TLT).

In the meantime, the action has moved over the American Airlines (AA), which has soared by 50%. AMC Entertainment Holdings (AMC) saw a 400% pop, but I haven’t seen anyone rushing back into theaters to watch Wonder Woman. Blame Jay Powell for flooding the financial system with mountains of cash seeking a home. There is so much money in circulation that traders are invented asset classes to put it into. This can’t last. Buy the dip.

Here are the best short squeeze targets with the greatest outstanding short interests. GameStop (GME) tops the list with an eye-popping 139% short interest, followed by Bed Bath & Beyond (BBBY) (67%) and Ligand Pharmaceutical (LGND) (64%). National Beverage (FIZZ), The Macerich Company (MAC), and Fubo TV (FUBO) bring up the rear. These are all failed companies in some form or another, which is why hedge funds had such large short positions.

New Home Sales disappointed in December, up only 1.6% to 842,000 units. This is on a signed contract basis only. Affordability is the big issue caused by high prices. Who buys a house at Christmas anyway?

Case Shiller soared by 9.5% in November, the fastest home price appreciation in history. Phoenix (13.8%), Seattle (12.7%), and San Diego (12.3) were the big movers. Blame a long-term structural housing shortage, a huge demographic push from Millennials, near-zero interest rates, and a flight from the cities to larger suburban homes. The Pandemic is keeping millions of homes off the market.

US GDP may reach pre-pandemic high by end of 2021, it the vaccine gets distributed to every corner of the nation and aggressive stimulus packages pass congress. Growth should come in at a minimum of 5% or higher this year, wiping out last year’s disaster. Keeping interest rates near zero will be a big help, as Treasury Secretary Yellen is determined to do. China and India are already there.

Share Buybacks have returned, the catnip of share prices. Q4 saw a jump to $116 billion from $102 billion in Q2, and this year, banks now have free reign to buy back their own shares. That’s still below the $182 billion seen in Q4 2019. It can only mean that share prices are rising further.

California lifts stay-at-home regulations, enabling restaurants to open after a nearly two-month shutdown. It’s the first ray of hope that the pandemic will end by summer. It will if Biden hits his 1.5 million vaccinations a day target.

Tesla posts sixth consecutive profit quarter, taking the stock down $60 in the aftermarket momentarily on a classic “buy the rumor, sell the news” move. The once cash-starved company now has an eye-popping $19.4 billion in reserves. Revenues reached a massive $10.7 billion, better than expected. Gross margins reached 19.2%. Looking for 50% annual growth for several years. Shanghai, Berlin, and Austin will make their first deliveries this year. Cash flow is at $19.4 billion, enough to build six more factories. No short sellers left here. It’s a perfect entry point for a LEAP. Buy the March 2023 $1,150-$1,200 call spread for a ten bagger.

Space X rocket carries 143 spacecraft into space. The Falcon 9 rocket set a new record with new satellites launched at once. Yes, you too can put 200kg into orbit for only $1 million. Many are from small tech startups selling various types of data. Elon Musk’s hobby, now worth $20 billion according to its government contracts, could be his next IPO. Don’t pass on this one!

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned a blockbuster 10.21% in January, versus a Dow Average that is now down in 2021. This is my third double-digit month in a row.

I used the market selloff to take substantial profits in my short (TLT) holdings and buy new longs in Boeing (BA) and Morgan Stanley (MS). I rolled the strikes down on my JP Morgan (JPM) long by $10.

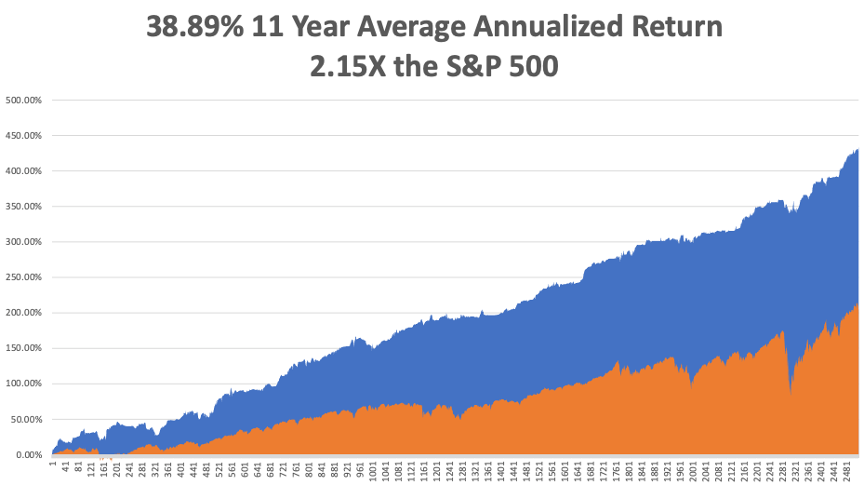

That brings my eleven-year total return to 432.76%, some 2.15 times the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.85%, a new high.

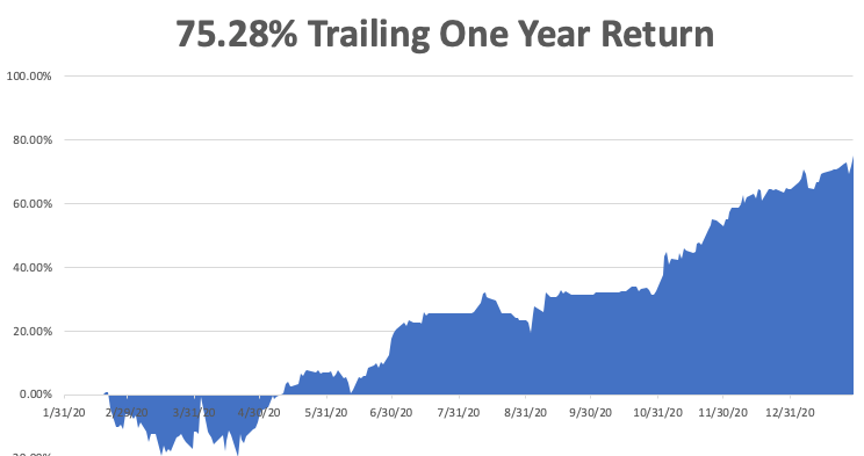

My trailing one-year return exploded to 75.28%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 91.43% since the March 20 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 26 million and deaths at 440,000, which you can find here. We are now running at a staggering 3,800 deaths a day.

The coming week will be all about the monthly jobs data.

On Monday, February 1 at 9:45 AM EST, the Markit Manufacturing PMI for January is out. Caterpillar (CAT) announces earnings.

On Tuesday, February 2 at 7:00 AM, Total Vehicle Sales for January are published. Alphabet (GOOG) and Amgen (AMGN) report.

On Wednesday, February 3 at 8:15 AM, the ADP Private Employment Report is published. QUALCOMM (QCOM) reports.

On Thursday, February 4 at 9:30 AM, Weekly Jobless Claims are printed. Gilead Sciences (GILD) reports.

On Friday, February 5 at 9:30 AM, the January Nonfarm Payroll Report is announced. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I am often kept awake at night by painful arthritis and a collection of combat injuries and I usually spend this time thinking up new trade alerts.

However, the other night, I saw a war movie just before I went to bed, so of course, I thought about the war. This prompted me to remember the two happiest people I have met in my life.

My first job out of college was to go to Hiroshima Japan for the Atomic Energy Commission and interview survivors of the first atomic bomb 29 years after the event. There, I met Kazuko, a woman in her late forties who was attending college in Fresno, California in 1941 and spoke a quaint form of English from the period. Her parents saw the war and the internment coming, so they brought her back to Hiroshima to be safe.

Her entire family was gazing skyward when a sole B-29 bomber flew overhead. One second before the bomb exploded, a dog barked and Kazuko looked to the right. Her family was permanently blinded, and Kazuko suffered severe burns on the left side of her neck, face, and forearms. A white summer yukata protected the rest of her, reflecting the nuclear flash. Despite the horrible scarring, she was the most cheerful person I had ever met and even asked me how things were getting on in Fresno.

Then there was Frenchie, a man I played cards with at lunch at the Foreign Correspondents Club of Japan every day for ten years. A French Jew, he had been rounded up by the Gestapo and sent to the Bergen-Belson concentration camp late in the war. A faded serial number was still tattooed on his left forearm. Frenchie never won at cards. Usually, I did because I was working the probabilities in my mind all the time, but he never ceased to be cheerful no matter how much it cost him.

The happiest people I ever met were atomic bomb and holocaust survivors. I guess, if those things can’t kill, you nothing can, and you’ll never have a reason to be afraid again. That is immensely liberating.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 25, 2021

Fiat LuxFeatured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE COMES THE SUPERHEATED ECONOMY),

(SPY), ($INDU), (TLT), (TBT), (TSLA)

The US economy is in the worst condition in a century. The U6 Unemployment rate stands at 20 million today. Main streets everywhere are boarded up. Millions of businesses have gone under. Some 4,500 people a day are dying from a dreaded virus.

All of this means that you should rush out and buy and stocks, as many as possible, with both hands, and by the bucket load. It’s time to take out that home equity loan and pour it into stocks, damn the torpedoes.

For things are about to get better for the US economy, a whole lot better, better beyond anyone’s wildest imagination, and for you individually.

Speaking to CEOs, fund managers, and hedge fund strategists, it is clear that most are wildly underestimating the strength of the 2021 recovery. People haven’t really added up all the stimulus and quantitative easing that is about the hit, which could reach $20 trillion. The total market value of US stock markets is only $51 trillion.

I hate to engage in some simplistic calculations here, but if you increase the amount of capital going into the economy by nearly 50% in two years, stocks just might go up by nearly 50% in two years. It’s no more complicated than that.

In fact, economic conditions are about to improve so fast that the Federal Reserve may have to break its promise about not raising interest rates for three years and instead start nudging them up by the end of 2021.

Needless to say, this is terrible news for the bond market (TLT), where I am lining up to go from a double to a triple short.

You are already starting to see other analysts ratchet up their overcautious yearend S&P 500 target. By November, they may reach my own outsized goal of 4,800, bringing in a total gain in stocks of 35%.

All of this explains why stocks just absolutely refuse to go down, even a little bit. Each one-day decline seems to be met with a wall of buying. The memo is out: you absolutely have to get into this market, whether you are an individual, hedge fund, institution, or outright bet the ranch gambler.

Of course, if you think I’m so bullish because I made 90% on my money since the April bottom, you’d be right.

Just keep your discipline and observe the basic rules of trading: 1) Don’t buy a position that is so big that it can’t handle a normal 10% correction, 2) Don’t accumulate a position that is so big that you can’t sleep at night, 3) No calling John Thomas in the middle of the night and asking “I have a 3X position in this and their trading down in Asia, what should I do?”

If you have to ask the question, your position is too big.

Biden’s economic plan boosts growth forecasts, according to Goldman Sachs. Prospects have jumped from 6.4% to 6.6%, the highest in a half-century, on the back of a massive Covid-19 package.

Treasury Secretary Janet Yellen says “GO BIG” or go home to the Senate Finance Committee. She was there to get confirmation and push for Biden’s $1.9 trillion stimulus package. Markets are underestimating the extent of the stimulus headed our way, which could reach $10 trillion in addition to another $10 trillion in quantitative easing. Buy dips.

Index Funds are getting trashed, substantially trailing the S&P 500, as single-story stocks dominate the market. It’s become a stock pickers market in the extreme, with no more obvious example that (TSLA), up 1,000% in 9 months. Small caps, IPOs, and cyclical are getting all the action, leaving the (SPX) in the dust.

Tesla delivered its first Chinese Model Y, which will add 250,000 units to sales in 2021. It’s all part of Elon’s quest to take over the global automobile market. He plans to boost sales from 500,000 last year to 20 million in a decade. If so, the stock today still looks cheap. But is the quality the same?

Tesla Q4 registrations soar by 63%, in California, its largest market. It’s due to the runaway success of the Model Y small SUV. The stock is taking a long-overdue rest with a sideways “time” correction. It’s still true that if you buy the stock, you get the car for free.

Weekly Jobless Claims are still sky-high at 900,000. It’s a decline on the week but still horrifically high. The stock market may be starting to notice, with stocks moving sideways for two weeks.

Existing Home Sales soared to a 15-year high, up an amazing 22% YOY in December to a seasonally adjusted 6.76 million units. In the meantime, inventories hit all-time lows at only 1.9 months as they can’t build them fast enough. Sales of $1 million-plus homes are up an incredible 94%. The hottest markets were in Austin, TX, Tampa, FL, and Phoenix, AZ. New York was the worst, followed by San Francisco. The market is on fire and could continue for another decade. Pending tax breaks from the new tax bill will give homeownership another big push.

US Housing Starts jump 5.8%, to 1.7 Million units. Single-family homes are up 12% YOY, driven by the pandemic. Notice the enormous supply/demand gap which assures that home prices will keep rising for years. Rising mortgage interest rates so far have had no effect.

US Manufacturing PMI hits 14-Year high, according to Markit, their index jumping from 57.1 to 59.1. The performance would have been better if it weren’t for rampant parts shortages nationwide. It’s another argument for the long-term bull case.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch shot out of the gate with an immediate 7.25%so far in January. That is net of a 4% loss on a Tesla short which I added one day too soon. Given the great heights of the market, I have trimmed my book to just a long in Tesla and a Short in US Treasury bonds.

That brings my eleven-year total return to 430.30% double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.80%. My trailing one-year return exploded to 74.44%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 90% since the March low.

The coming week will be a big one for big tech earnings.

We also need to keep an eye on the number of US Coronavirus cases at 25 million and deaths at 420,000, which you can find here. We are now running at a staggering 4,500 deaths a day.

When the market starts to focus on this, we may have a problem.

On Monday, January 25 at 9:30 AM EST, we get the Chicago Fed National Activity Index for December. Phillips (PSX) and Kimberly Clark (KMB) report.

On Tuesday, January 26 at 10:00 AM, we learned the new S&P Case Shiller National Home Price Index. Microsoft (MSFT), Johnson & Johnson (JNJ), and American Express (AMEX) report.

On Wednesday, January 27 at 10:00 AM, US Durable Goods for December are published. Apple (AAPL), Facebook (FB) and Tesla (TSLA) report.

On Thursday, January 28 at 9:30 AM, the first look at US GDP for Q4 is announced. McDonald’s (MCD), American Airlines (AA), and Visa (V) report.

On Friday, January 29 at 9:30 AM, US Personal Income and Spending for December is published. Ely Lilly (LLY) and Caterpillar (CAT) report. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I have never been big on the “meme” thing, but you have to love the one that has been circulating about Bernie Sanders. Suddenly, he showed up on every transit system in the country. Clearly, the country was dying for a laugh. I include several pictures below. Hopefully, I won’t end up like him someday.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 22, 2021

Fiat Lux

Featured Trade:

(JANUARY 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (IWM), (SPY), (ROM), (BRK/A), (AMZN), NVDA), (MU), (AMD), (UNG), (USO), (SLV), (GLD), ($SOX), CHIX), (BIDU), (BABA), (NFLX), (CHIX), ($INDU), (SPY), (TLT)