Global Market Comments

November 14, 2023

Fiat Lux

Featured Trade:

(WHY YOU WILL LOSE YOU JOB IN THE NEXT FIVE YEARS, AND WHAT TO DO ABOUT IT),

(INTU), (AMZN), (GOOGL), (TSLA), (BLK), (HRB)

Global Market Comments

November 14, 2023

Fiat Lux

Featured Trade:

(WHY YOU WILL LOSE YOU JOB IN THE NEXT FIVE YEARS, AND WHAT TO DO ABOUT IT),

(INTU), (AMZN), (GOOGL), (TSLA), (BLK), (HRB)

Yes, it’s happening.

And if you lose your job to AI in five years you will be one of the lucky ones.

It’s possible that your job is already gone, they just haven’t told you yet.

The shocking conclusion I am getting from dozens of research fronts is that artificial intelligence and automation are accelerating far faster than anyone realizes.

It is all extraordinarily disruptive.

This will cause corporate profits to rocket and share prices to soar but at the price of higher nationwide political instability.

A big leap took place at the beginning of the year when suddenly it appeared that everything got a lot smarter.

My local Safeway has started using self-checkout scanners to enable customers to avoid the long lines still operated by humans.

I hate them because I can never get them to scan pineapples correctly.

Soon, Amazon (AMZN) opened a supermarket in Seattle where there is no checkout stand at all. You simply just pick up whatever products you want, and it will scan them all on the way out to the parking lot.

Once the software is perfected (it is self-learning), and the consumers are educated, 5 million checkout clerks will be joining the unemployment lines.

Uber has been testing self-driving taxis in Phoenix, AZ, with sometimes humorous results. It seems that other human-driven cars like crashing into them. There has been one fatality so far when the human safety driver was caught texting.

When they figure this out, probably in two years, 180,000 taxi drivers and 600,000 Uber and Lyft drivers will have to hit the road.

Some 3 million truck drivers will be right behind them.

Notice that I am only a couple of paragraphs into this peace and already 8,780,000 jobs are about to imminently disappear out of a total of 150 million in the US.

Two decades from now, only vintage car collectors or the very poor will be driving their cars if Tesla (TSLA) has anything to do with it.

I let my Model X drive me around most of the time. It has reaction time, night vision, and a 360-degree radar system that are far better than my 71-year-old senses.

However, all new Teslas now come equipped with the hardware to use it. They are all only one surprise overnight software upgrade away from the future.

And it's not just the low-end high school dropout jobs that are being thrown in the dustbin of history.

Automation is now rapidly moving up the value chain.

A rising share of online news is machine-generated and is targeting you based on your browsing history. You just didn’t know it.

It was a major influence in the last election.

Blackrock (BLK), the largest fund manager in the country, has announced that it is laying off dozens of stock analysts and turning to algorithms to manage its vast $8.6 trillion in assets under management.

As the April 15 tax deadline relentlessly approaches, you are probably totally unaware that an algorithm prepared your return, particularly if you use a low-end service like H & R Block (HRB) or Intuit’s (INTU) TurboTax.

Because of the simultaneous convergence of multiple technologies, half of all current jobs will likely disappear over the next 20 years.

If this sounds alarming, don’t worry.

We’ve been through all of this before.

From 1900 to 1950 farmers fell from 40% to 2% of the labor force. The food output of that 2% has tripled over the last 60 years, thanks to improved seed varieties and farming methods.

The remaining 38% didn’t starve.

They retrained for the emerging growth industries of the day, automobiles, aircraft, and radio.

But there had to be a lot of pain along the way.

More recently, some 30% of all job descriptions listed on the Department of Labor website today didn’t exist 20 years ago.

Yes, disruption happens fast.

And here’s where it gets personal.

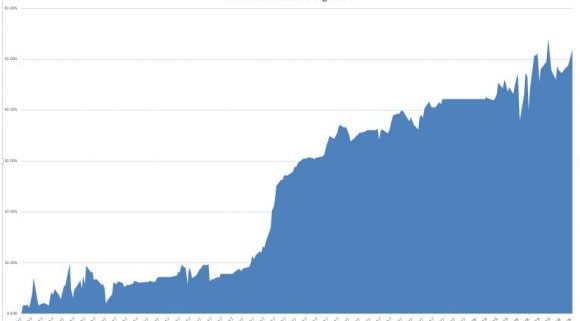

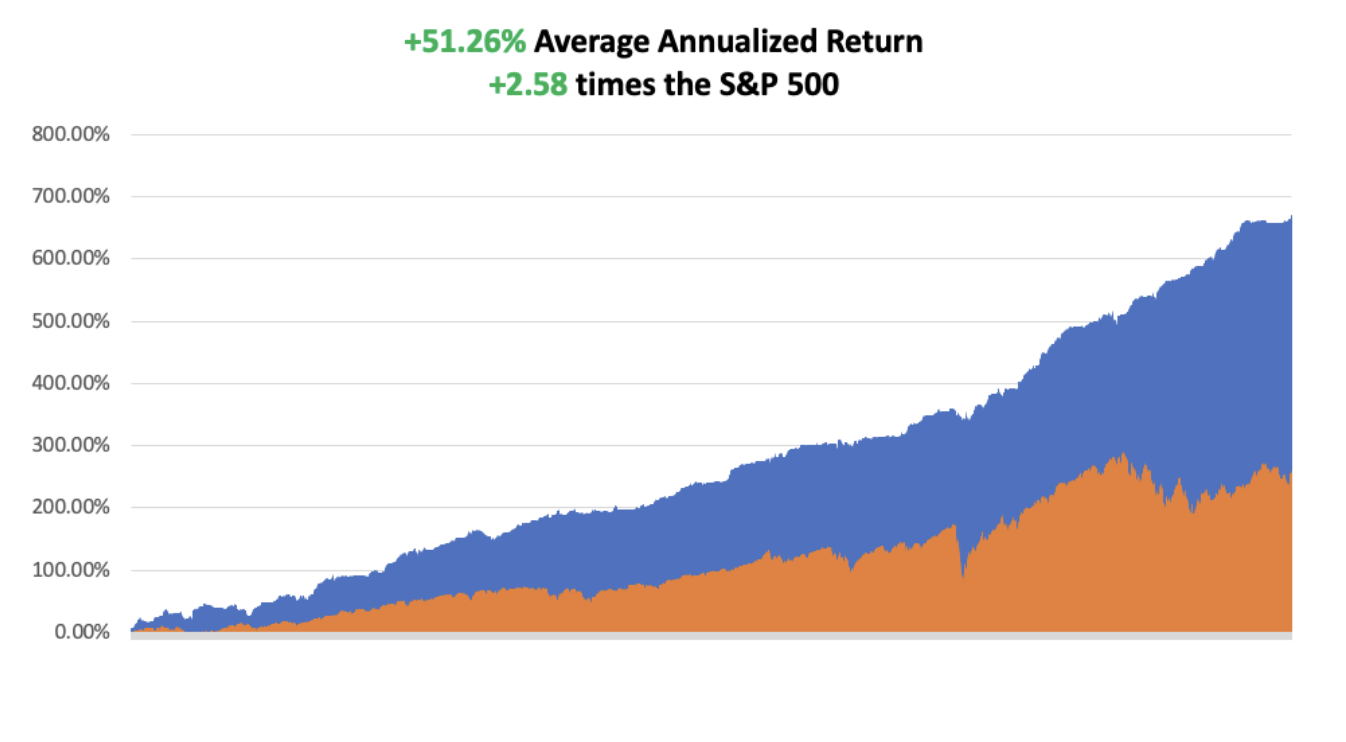

Since I implemented an AI-driven, self-learning Mad Hedge Market Timing algorithm to assist me in my own Trade Alert service six months ago, MY PERFORMANCE HAS ROCKETED, FROM A 21% ANNUAL RATE TO 51%!

As a result, YOU have been crying all the way to the bank!

The proof is all in the numbers (see chart below).

Those trading without the tailwind of algorithms today suddenly find the world a very surprising and confusing place.

They lose money too.

The investment implications of all of this are nothing less than mind-boggling.

Wages are almost always the largest cost for any business, especially the labor-intensive ones like retailing, fast food, and restaurants.

Reduce your largest expense by 90% or more, and the drop through to the bottom line will be enormous.

Stock markets have already noticed.

Maybe this is why price-earnings multiples are trading at a multi-decade high of 19.5X.

Perhaps, the markets know something that we mere humans don’t?

It also is the largest budgetary item in any government-supplied service.

I bet that half of the country’s 7 million teaching jobs will be gone in a decade, taken over by much cheaper online programs.

Today, my kids do their homework on their iPhones, complete class projects on Google Docs, and get a report card that is updated and emailed to me daily.

They’re probably to last generation to ever go to a physical school.

(That’s life. Just as the cost of driving them to school every day becomes free, they don’t have to go anymore).

You can always adopt a “King Canute” strategy and order the tide not to rise.

Or, you can rapidly adapt, as I did.

The choice is yours.

Global Market Comments

February 17, 2021

Fiat Lux

Featured Trade:

(HOW TO HANDLE THE FRIDAY, FEBRUARY 19 OPTIONS EXPIRATION),

(TSLA), (MS), (BA), (BLK), (GS), (AMD), (KO), (BAC), (NFLX), (AMZN), (AAPL), (INTU), (QCOM), (CRWD), (AZN), (GILD)

Followers of the Mad Hedge Fund Trader Alert Services have the good fortune to own no less than 16 deep in-the-money options positions, all of which are profitable. All but one of these expire in two trading days on Friday, February 19, and I just want to explain to the newbies how to best maximize their profits.

It was time to be aggressive. I was aggressive beyond the pale.

These involve the:

Global Trading Dispatch

Mad Hedge Technology Letter

Mad Hedge Biotech & Healthcare Letter

Provided that we don’t have a huge selloff in the markets or monster rallies in bonds, all 15 of these positions will expire at their maximum profit point.

So far, so good.

I’ll do the math for you on our oldest and least liquid position, the Tesla February 19 $650-$700 vertical bull call spread, which I initiated on January 25, 2021 and will definitely run into expiration. At the Friday high, Tesla shares were at a lowly $816, some $53 lower than the $869.70 that prevailed when I strapped on this trade.

Provided that Tesla doesn’t trade below $700 in two days, we will capture the maximum potential profit in the trade. That’s why I love call spreads. They pay you even when you are wrong on the direction of the stock. All of the money we made was due to time decay and the decline in volatility in Tesla stock.

Your profit can be calculated as follows:

Profit: $50.00 expiration value - $44.00 cost = $6.00 net profit

(4 contracts X 100 contracts per option X $6.00 profit per options)

= $2,400 or 20% in 18 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning February 22 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and find it.

Although the expiration process is now supposed to be fully automated, occasionally machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears, and the spreads substantially widen, when security has only hours, or minutes until expiration on Friday, February 19. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

If for some reason, your short position in your spread gets “called away,” don’t worry. Just call your broker and instruct them to exercise your long option position to cover your short option position. That gets you out of your position a few days early at your maximum profit point.

If your broker tells you to sell your remaining long and cover your short separately in the market, don’t. That makes money for your broker, but not you. Do what I say, and then fire your broker and close your account because they are giving you terrible advice. I’ve seen this happen many times among my followers.

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next month-end.

Take your winnings and go out and buy yourself a well-earned dinner. Just make sure it’s take-out. I want you to stick around.

Well done, and on to the next trade.

Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

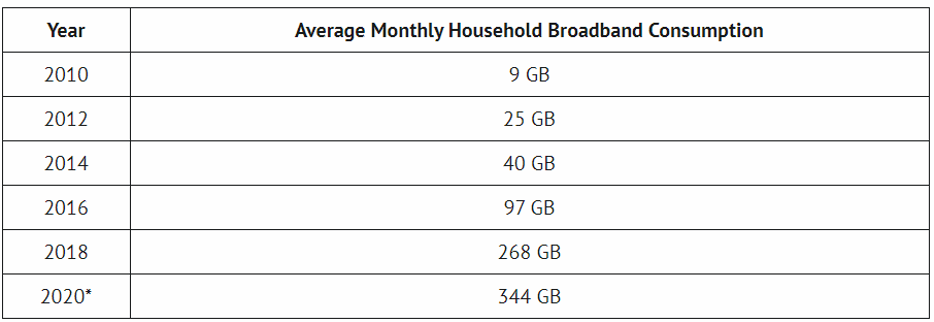

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

Global Market Comments

October 9, 2019

Fiat Lux

Featured Trade:

(HOW FINTECH IS EATING THE BANKS’ LUNCH),

(BAC), (C), (WFC), (SQ), (PYPL),

(WCAGY), (FISV), (INTU), (BABA),

Mad Hedge Technology Letter

August 26, 2019

Fiat Lux

Featured Trade:

(INTUIT’S WAKE UP CALL)

(INTU)

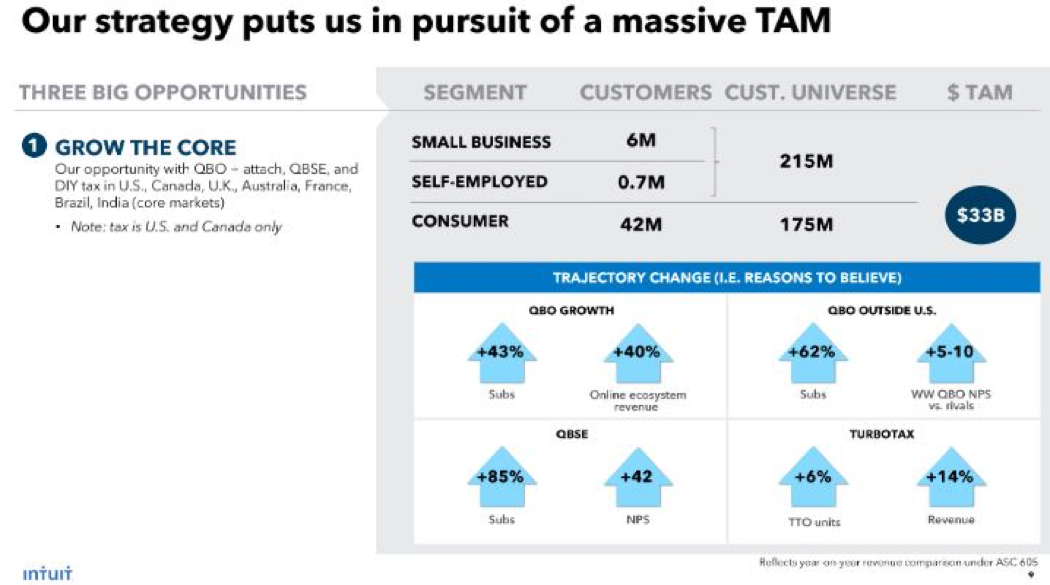

Intuit Inc. (INTU), one of my favorite domestic cloud plays came to life Friday morning by posting earnings and revenue surpassing estimates.

Cha-Ching!

Intuit provides financial management and compliance products and services for small businesses, consumers, self-employed, and accounting professionals.

It’s not the sexiest company, but it does the job.

This is the perfect late economy cycle software stock to hide out while the two largest economies in the world battle it out on the geopolitical level.

And don’t worry, Chinese haven’t found a use case to rip off the software, insulating the products from any international exposure.

The stock responded in kind shooting up 7% and I have been keen on this name for quite a while.

Its non-GAAP loss was 9 cents per share slimmer than the expected loss of 14 cents.

Profit has improved 800% on a year-over-year basis on revenue grossing $994 million, up 15% from the year-ago quarter’s adjusted revenues.

Total revenue crushed estimates of $961 million by displaying robust momentum in online ecosystem revenues and growth in the consumer business.

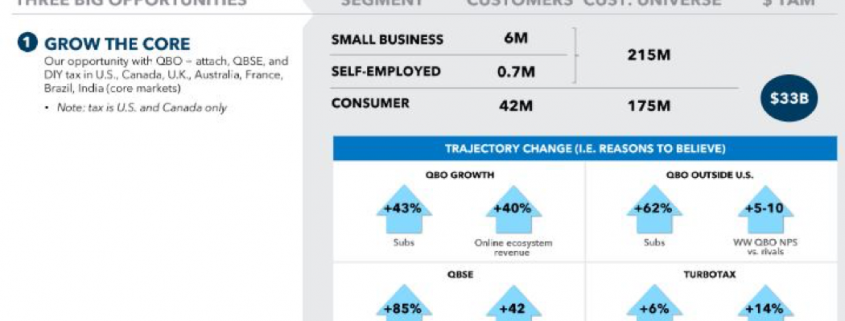

We can attribute the startling outperformance to the 33% subscriber surge for QuickBooks Online, which tallied up more than 4.5 million at the end of the fiscal fourth quarter.

The Online ecosystem revenues jumped 35% to $459 million.

The U.S.-based subscribers of QuickBooks Online expanded 25% to more than 3.2 million while international subscribers rose 58% on a year-over-year basis to more than 1.3 million.

Can Intuit squeeze more juice out of the lemon for 2020?

Revenues are expected to register in the range of $7.44-$7.54 billion.

For the full fiscal year, Small Business and Self-Employed group is expected to grow 12-14% year-over-year.

The Consumer Group is expected to increase by 9-10%.

Intuit predicts revenue growth of 10-12% in the range of $1.12-$1.13 billion for the first quarter of fiscal 2020.

Intuit expects Online Ecosystem revenues to grow more than 30%.

There are some parts of this business that are supercharged with more than 30% expansion, hallmarks of a solid growth cloud company.

The reality is that in total, this is a company that is growing around 10% and the 8-10% projected for 2019 was eclipsed with growth of 13%.

Investors cannot expect growth that typifies Amazon Web Services or Microsoft Azure, but this stock remains a reliable yet unspectacular bet on the cloud names to advance.

Accountant software is not a fashionable business, but this software has to be classified as best in show.

If investors are keen on “buy the dip” strategies, this candidate should give one no pause in jumping in headfirst.

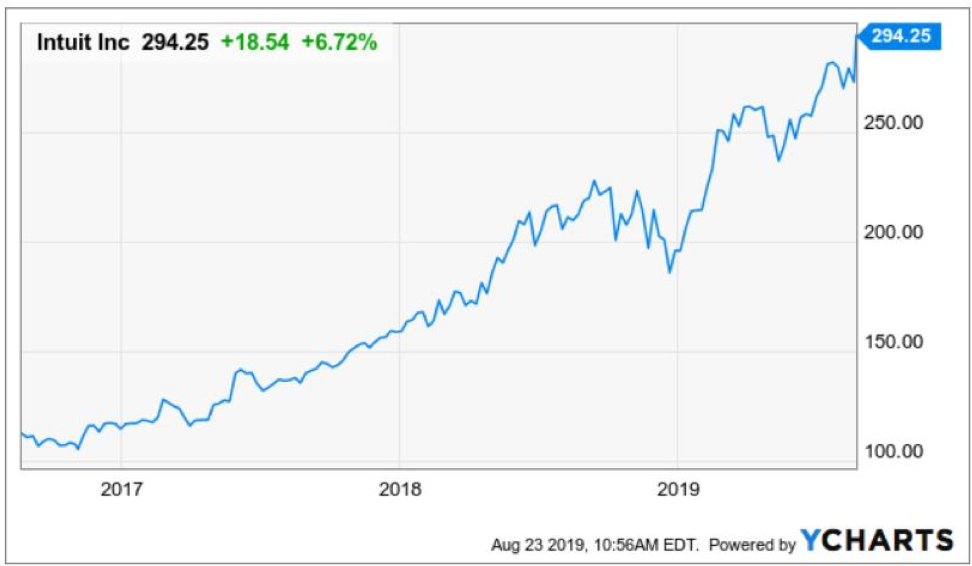

This stable cloud stock has tickled the fancy of investors already up 35% year to date and is resilient in times of stress.

The dips are shallow and the up moves impressive, hard not to like this stock.

Global Market Comments

May 20, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR I’LL TAKE SOME OF THAT!)

(FXI), (CYB), (TSLA), (AAPL), (BA), (WMT), (TLT), (INTU), (GOOGL)