The next time there is a Fed interest rate announcement, earnings from all the big tech companies, and a Nonfarm Payroll Report all within five days, I am going to call in sick, volunteer at the Oakland Food Bank, or explore some remote Pacific island!

For good measure, a top-secret Chinese spy balloon passed overhead before it was shot down, which I was able to read all about in USA Today.

Still, when you live life in the front trenches and on the cutting edge and use the kind of leverage that I do, you are going to take hits. It’s all a cost of doing business. If you can’t stand the heat, get out of the kitchen.

The last month in the markets have seen one of the greatest whipsaws of all time. Many leading stocks are up 40%-100%, while the Volatility Index ($VIX) plunged to a two-year low. Stocks have gone from zero bid to zero offered. The bulls are back in charge, for now.

Go figure.

This year has proved full of flocks of black swans so far, with February setting me back -5.70%. My 2023 year-to-date performance is still at the top at +16.65%. The S&P 500 (SPY) is up +9.92% so far in 2023. My trailing one-year return maintains a sky-high +84.10%.

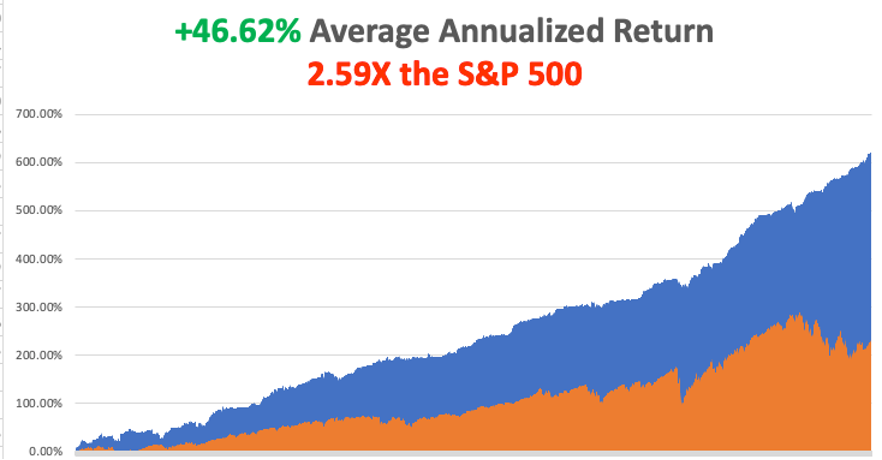

That brings my 15-year total return to +613.84%, some 2.59 times the S&P 500 (SPX) over the same period. My average annualized return has retreated to +46.62%, still the highest in the industry.

Last week, I got stopped out of my short position in the (QQQ), in what will hopefully be my biggest loss of the year, but not the last. Once or twice a year, you get a major gap opening that takes you through one, and sometimes two full strike prices, taking you to the cleaners, and this was one of those times. It takes three more winning trades to make up for these.

I also took small profits on my remaining long in Apple (AAPL). That leaves me 80% in cash, with a double short in Tesla (TSLA). Markets are wildly overextended here with my own Mad Hedge Market Timing Index well into “SELL” territory at 76. Tread at your own peril. Cash is king right here.

Growth stocks are on fire and small caps have been prospering, all classic bull market indicators. This has triggered panic short covering by hedge funds which have seen their worst start to a New Year in decades. The old pros are getting carried out on stretchers.

Maybe this is a good time to hire some kid to do your trading, like one who has never seen markets go down before, one who started his career only on January 1? Or maybe one who retired on December 31 2021, and took a year off?

So, what are markets trying to tell us? That in an hour, the view of the economy has flipped from a mild recession to a soft landing? That interest rates don’t matter anymore? That big chunks of the economy can operate without outside money? That big tech will always make money, it will just rotate from large profits to small ones and back to outrageous ones again?

Those who instead bet on a severe recession are currently filling out their applications as Uber drivers. Warning: it’s harder than it used to be, no more fake IDs or salvage title cars. Next, they’ll want your DNA sample.

If it is any consolation, Fed governor Jay Powell hasn’t a clue about what’s happening either, and that’s with 100 PhD's in economics on his staff. He was just as flummoxed as we over a January Nonfarm Payroll Report that came in 2.5 X expectations on top of 4.5% in interest rate hikes.

Clearly, a new economy has emerged from the wreckage of the pandemic, and no one, not anyone, has quite figured out what it is yet.

Some ten years’ worth of economic evolution has been pulled forward. Everything is digitizing at an astonishing rate. What do I do after slaving away in front of a computer all day? Go back to my computer to have fun. Lots of “zeros” and “ones” there.

It looks like we get a new stock market too.

All of this frenetic market action does fit one theory that I spelled out for you in great detail last week. It is that technology stocks are about to spin off such immense profits that it is about to replace the Fed as a new immense supply of free money.

META up 20% in a day? That’s what it says to me. Notice that Mark Zuckerberg mentioned “AI” 16 times in his earnings call.

Is it possible that I nailed this one….again?

On another related topic, the last three months have just given us a wonderful illustration of how well the Mad Hedge Market Timing Index works (see chart below). We got a strong BUY at an Index reading of 30 on December 22, when the (SPY) began a robust 12% move up. We are now at the top end of an upward trend with my Index at 76. You’d be Mad to add a long position here, at least for the short term.

Someone asked me the other day if the algorithm has gotten smarter in the seven years I have been using it. The answer is absolutely “yes,” and you can see it in my performance. During this time, my average annualized return has jumped from 31% to 46%. That’s because the algorithm gets smarter with the hundreds of new data points that are added every day. Believe it or not, this is how much of the economy is run now.

But there is another factor. I get smarter every year. Believe it or not, when you go from year 54 to 55, you actually learn quite a lot about the markets. Of course, markets are evolving all the time and the rate of change is accelerating. When I saw the market moving towards algorithms, I wrote an algorithm. The challenge is to solve each new problem the market throws at you every year, which I love doing.

Nonfarm Payroll Report at 513,000 Blows Away Estimates, more than double expectations. The Headline Unemployment Rate fell to a new 53-year low at 3.4%.Leisure & Hospitality gained an incredible 128,000, Professional & Business Services 82,000, and Government 74,000. You can kiss that interest rate cut goodbye. Bonds believe it, down 3 points, but stocks are still in Lalaland, reversing a 300-point reversal in the (QQQ)s.

Fed Raises Rates 25 basis points, but Powell talks hawkish, smashing stocks for an hour. He needs more evidence that inflation is finally headed down. He might as well have said he’ll burn the place down. One or two more rate rises to go before the pivot.

Weekly Jobless Claims Hit New 9 Month Low, at 183,000, down 3,000, and is close to a multi-generational low. A recession is rapidly moving off the table as today’s move in tech stocks indicates.

JOLTS Surges Past 11 Million Job Openings in December to a five-month high. The Fed’s assault on labor clearly isn’t working. The million who died from Covid certainly aren’t coming back to work, nor are the 500,000 long Covid cases. That’s 1% of the US workforce.

Ukraine War is Accelerating Move to Green Energy, or so thinks British Petroleum, cutting its ten-year energy demand forecast. Russian energy has proven unreliable at best, and the key pipelines have been blown up anyway. Massive subsidies have been unleashed in Europe and the US for solar, wind, EVs, hydro, and even nuclear. The war gave coal a respite from oblivion, but only a temporary one.

S&P Case Shiller Drops to an 8.6% Annual Gain, the National Home Price Index falling for five consecutive months. No green shoots here. The deeply lagging indicator may not turn positive until yearend. Miami, Tampa, and Atlanta showed the biggest gains, with San Francisco the biggest loser.

Office Occupancy Recovers to 50%, according to a private research firm. New York, San Jose, and San Francisco are still lagging. With the work-from-home trend and high interest rates, commercial properties have entered a perfect storm. Austin, TX was the highest at 68%.

Europe Delivers Surprising Q4 Growth, despite WWIII playing out on its doorstep. GDP increased by 0.1% when a decline was expected. European stocks should outperform American ones in 2023.

IMF Upgrades Global Growth Forecast for 2023 to 2.9% and sees a modest recovery in 2024. The figures are an improvement from the last report, thanks to falling inflation and energy prices. China ending lockdowns is another plus.

General Motors to Invest $650 Million in Lithium Americas, pouring money into a Nevada mine at Thacker Pass, the largest such US investment so far. (GM) says it will raise EV production to 400,000 this year versus 120,000 for all of 2022. Good luck because local environmental opposition to the new mine has been enormous. Goodbye China.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, February 6, no data of note is announced.

On Tuesday, February 7 January 31 at 5:30 AM EST, the Balance of Trade is out.

On Wednesday, February 8 at 7:30 AM, the Crude Oil Stocks are published. On Thursday, February 9 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, February 10 at 8:30 AM, the University of Michigan Consumer Sentiment is printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, the telephone call went out amongst the family with lightning speed, and this was back in 1962 when long-distance calls cost a fortune. President Dwight D. Eisenhower was going to visit my grandfather’s cactus garden in Indio the next day, said to be the largest in the country, and family members were invited.

I spent much of my childhood in the 1950s and 1960s helping grandpa look for rare cactus in California’s lower Colorado Desert, where General Patton trained before invading Africa. That involved a lot of digging out a GM pickup truck from deep sand in the remorseless heat. SUVs hadn’t been invented yet, and a Willys Jeep (click here) was the only four-wheel drive then available in the US.

I have met nine of the last 13 presidents, but Eisenhower was my favorite. He certainly made an impression on me as a ten-year-old boy, who I remember as a kindly old man.

I walked with Eisenhower and my grandfather plant by plant, me giving him the Latin name for its genus and species, and citing unique characteristics and uses by the Indians. The former president showed great interest and in two hours we covered the entire garden. I still make my kids learn the Latin names of plants.

Eisenhower lived on a remote farm at the famous Gettysburg, PA battlefield given to him by a grateful nation. But the winters there were harsh so he often visited the Palm Springs mansion of TV Guide publisher Walter Annenberg, a major campaign donor.

Eisenhower was one of the kind of brilliant men that America always comes up with when it needs them the most. He learned the ropes serving as Douglas MacArthur’s Chief of Staff during the 1930s. Franklin Roosevelt picked him out of 100 possible generals to head the allied invasion of Europe, even though he had no combat experience.

After the war, both the Democratic and Republican parties recruited him as a candidate for the 1952 election. The latter prevailed, and “Ike” served two terms, defeating the governor of Illinois Adlai Stevenson twice. During his time, he ended the Korean War, started the battle over civil rights at Little Rock, began the Interstate Highway System, and admitted Hawaii as the 50th state.

As my dad was very senior in the Republican Party in Southern California during the 1950s, I got to meet many of the bigwigs of the day. New York prosecutor Thomas Dewy ran for president twice, against Roosevelt and Truman, and was a cold fish and aloof. Barry Goldwater was friends with everyone and a decorated bomber pilot during the war.

Richard Nixon would do anything to get ahead, and it was said that even his friends despised him. He let the Vietnam War drag out five years too long when it was clear we were leaving. Some 21 guys I went to high school with died in Vietnam during this time. I missed Kennedy and Johnson. Wrong party and they died too soon. Ford was a decent man and I even went to church with him once, but the Nixon pardon ended his political future.

Peanut farmer Carter was characterized as an idealistic wimp. But the last time I checked, the Navy didn’t hire wimps as nuclear submarine commanders. He did offer to appoint me Deputy Assistant Secretary of the Treasury for International Affairs, but I turned him down because I thought the $15,000 salary was too low. There were not a lot of Japanese-speaking experts on the Japanese steel industry around in those days. Biggest mistake I ever made.

Ronald Reagan’s economic policies drove me nuts and led to today’s giant deficits, which was a big deal if you worked for The Economist. But he always had a clever dirty joke at hand which he delivered to great effect….always off camera. The tough guy Reagan you saw on TV was all acting. His big accomplishment was to not drop the ball when it was handed to him to end the Cold War.

I saw quite a lot of George Bush, Sr. who I met with my Medal of Honor Uncle Mitch Paige at WWII anniversaries, who was a gentleman and fellow pilot. Clinton was definitely a “good old boy” from Arkansas, a glad-hander, and an incredible campaigner, but was also a Rhodes Scholar. His networking skills were incredible. George Bush, Jr. I missed as he never came to California. And 22 years later we are still fighting in the Middle East.

Obama was a very smart man and his wife Michelle even smarter. Stocks went up 400% on his watch and Mad Hedge Fund Trader prospered mightily. But I thought a black president of the United States was 50 years early. How wrong was I. Trump I already knew too much about from when I was a New York banker.

As for Biden, I have no opinion. I never met the man. He lives on the other side of the country. When I covered the Senate for The Economist, he was a junior member.

Still, it’s pretty amazing that I met 9 out of the last 13 presidents. That’s 20% of all the presidents since George Washington. I bet only a handful of people have done that and the rest all live in Washington DC. And I’m a nobody, just an ordinary guy. It just makes you think about the possibilities.

Really.

It’s Been a Long Road

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/john-thomas-white-house.jpg500665Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-06 14:02:382023-02-06 16:24:09The Market Outlook for the Week Ahead, or Welcome to the Whipsaw

They are and will continue to be the largest influencer in tech share price action in the short-term and the last 2 days has proved it.

Whatever you think or say about the equity market, we can’t hide from the truth that liquidity will either wreak havoc on short-term price action or shoot it to the moon like we saw post-Fed announcement about the latest rate hike.

Tech shares lifted off like an Elon Musk spaceship to Mars and the Mad Hedge Technology Letter was tactical enough to take profits on a DocuSign (DOCU) put spread and stomp out in Meta (META) before the earnings report.

I was able to add some additional long tech as Friday is proving to benefit from the spillover effect.

No matter how we view it, volatility isn’t going anywhere any time soon.

Why?

Since January 2020, the US has printed nearly 80% of all US dollars in existence.

Lots of fiat paper sloshing around in the system has many unintended consequences.

When pushed into certain asset classes, the hot money polarizes price action. That’s how we got all the meme stock craziness.

This phenomenon won’t be going away anytime soon and the Fed slowly reducing their asset sheet pales in comparison to the liquidity hanging around on the sidelines.

The Fed hike means short-term rates now stand at between 4.5%-4.75%, the highest since October 2007.

The move marked the eighth increase in a process that began in March 2022. By itself, the fund's rate sets what banks charge each other for overnight borrowing, but it also spills through to many consumer debt products.

Tech shares took off because Chairman Powell acknowledged that “the disinflationary process” had started.

In a blink of an eye, the Nasdaq was up 2% and growth stocks were up 5%.

Powell intentionally didn’t pour cold water on the rally when he had a chance to smash it down with more hawkish rhetoric or a 50 basis point hike.

It appears highly likely that Powell isn’t interested in tech stocks or any equities for that matter experiencing another bloodbath like 2022.

There might be pitchforks out for him if there is a 30% loss in major indexes this year and perhaps he is scared that Washington would bring the heat. He likes his cushy job and the benefits that come with it.

I do believe this is only the first of a series of Powell Houdini acts where he is willing to disappear behind any sort of opportunity to smash down the markets and let them run wild.

Tech stocks will be a natural buy-the-dip opportunity during this deflation narrative.

We have a clear runway from 6.5% inflation to around 4% and during this 2.5% deflation drop, I can easily see the Nasdaq lurching higher.

I used Friday to add a bullish position in Lyft (LYFT) and Amazon (AMZN) after their terrible earnings while I took almost maximum profit in our Netflix (NFLX) call spread.

It was almost as if Powell announced a new round of QE or, well, sort of.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-03 16:02:302023-03-02 00:24:52Hi Beta Is Suddenly Hot

America will never achieve a “super app,” and what does that mean for Silicon Valley?

These “killer apps” thrive in other places but not in America.

WeChat is the super app in China, while there is Careem in the Middle East, Rappi in Latin America, and Grab in Southeast Asia.

Any attempt to move in on that territory has been stymied by Washington.

A Super app is roughly a place where ecommerce, daily and monthly payments, financial management, social chats, social media, and daily services like ride-hailing co-exist in harmony on one app.

American tech companies are getting blocked from incorporating new payments into their apps while legacy payment systems remain.

Facebook’s attempts to build out standalone payment capabilities through the Libra/Diem blockchain project failed, but other apps in its family such as Instagram and WhatsApp are bolting on payment and e-commerce functionality.

As Zuckerberg and his team seem to have noticed, payments are critical to any would-be super app.

Half of US smartphone users are expected to adopt mobile payments as late as 2025, according to eMarketer research.

By contrast, 64% of China's population had made a payment on their phone by the end of 2021, according to a report from China UnionPay, the state-owned financial services firm.

Companies will struggle to generate the volume needed to make a super app work the way WeChat does, which has accumulated more than 1 billion users thanks to its mix of services and payments that ensure people don't have to look elsewhere.

In emerging market countries, payments skipped cards altogether because the infrastructure was weak.

Instead of bank cards, citizens went from cash to paying by phones using their local super app.

This could never happen in America because card payment options are diverse and trustworthy.

America has a reliable network of fragmented services and regulators have become so emboldened that they would never allow a financial payment system on a super app to ever develop.

There's another clear reason why the most successful super app has emerged in China.

Beijing has shut out foreign competitors from offering Chinese consumers any alternative.

Under Lina Khan, the FTC is becoming more sharply focused on competition and user privacy. Creating super apps would almost certainly require aggressive consolidation through acquisitions — a surefire way of attracting scrutiny.

As it stands, American regulators are now hawkish against American tech.

There's also the issue of Apple.

With the iOS system, Apple doesn’t allow the type of access needed to be able to build a super app on an iPhone.

Even if Apple wants to build a super app, there are still plentiful Android users in America that wouldn’t be captured either.

Apple would also need to backtrack on its pledge to safeguard personal data which is very unlikely to happen.

The best bet is probably Elon Musk’s Tesla, Twitter, and Space X combo.

He has two strong elements needed for a super app, but he doesn’t have a payment system and there is almost no chance in this regulatory climate of getting that approved.

The best way forward is tech firms with strong balance sheet picking up the best of breed in tech sub-sectors and eventually, they will all merge together.

However, that’s proved difficult as well with Microsoft’s blocked acquisition of video game firm Activision.

In a high interest rate world, profitable tech firms with strong balance sheets will be rewarded the most if they buy smaller tech companies which will be additive to their profit model.

The cash burners have a tough time competing in a high rate world and zero chance of achieving that super app status.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-16 14:02:392023-01-02 16:33:59American Super App

It is almost guaranteed that the 2023 tech playbook will be quite different from 2022.

That’s not to say it will be easy.

But backward-facing data shows us that market leaders of a certain time period in history almost never recreate the same kind of success moving forward.

Domination emerges from elsewhere and is usually a place we would have never imagined.

Looking at some of the biggest tech companies in 2022, many were wrong-footed.

Micro examples are plentiful such as Apple’s reliance on Chinese factories for iPhone manufacturing.

Also, there is the failure of Meta (META) to have pivoted to the metaverse, and look at Netflix suddenly thinking it was a genius idea to enter the American culture wars with their content.

There were early signs that a shift is already underway.

Even more concerning is that these big companies are out of ideas for the moment.

Will Apple (AAPL) keep making the iPhone with no material improvement?

Probably yes since they can get away with it for the moment.

I believe that a company will come along and finally knock the stuffing out of these big tech giants.

Some of them have gotten too comfortable and instead of investing deeply into their creative divisions, they have chosen to increase share buybacks and bolster dividends.

The percentage of capital spent on research and development keeps dwindling as a percentage of total revenue.

Next year’s tech consensus is 8% revenue growth which is hardly what you would expect for this traditional growth sector.

While it is true that it is hard to move the needle much for a $2 trillion company, I still feel they aren’t doing enough to rewrite the rules of the game while they still have the clout and resources.

The example of past stock market greats is a reminder that things can change quickly. Cisco (CSCO) and Intel (INTC) were leaders in the dot-com boom of the late 1990s, but have never climbed back to the highs they reached in 2000, while it took the Nasdaq 100 Index 15 years to surpass its 2000 peak.

Not only is revenue growth projected to shrink next year, but profitability is supposed to slow by 2%.

Faced with higher cost of borrowing and rising inflation, investors are becoming choosier in terms of which companies they are willing to back.

The last few weeks have been incredibly slow in not only the volume of tech trading but the velocity of price movement in tech stocks.

The Santa Claus rally was effectively extinguished when China’s protest smothered the loosening of interest rate momentum.

Since then, we have received mixed reports in China which have been difficult to decode because the country is like a black box.

Tomorrow we will finally get more direction to tech stocks with the CPI report that everybody has been waiting for.

Expectations are for a 7.3% increase year over year in the face of rising producers purchasing data.

Either way, a big move is expected tomorrow upon the news of the inflation data.

It will either confirm that inflation is headed lower, which is bullish for tech stocks, or a high data point will trigger a sharp selloff.

Expect some new tech trade alerts short following the CPI report tomorrow.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-12 16:02:072022-12-28 19:01:48A Different Playbook

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TOP FIVE TECHNOLOGY STOCKS OF 2023),

(RIVN), (ROM), (ARKK), (PANW), (CRM), (FXE), (FXY), (FXA), (LEN), (KBH), (DHI), (TLT), (UUP), (META), (TSLA), (BA), (JNK), (HYG), (BRKB), (USO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-14 10:04:422022-11-14 11:24:00November 14, 2022

The year 2022 has been driven by rising interest rates, a strong dollar, a weak economy, a bear market in stocks.

A massive reversal is about to take place. 2023 will gain the benefit of gale force macroeconomic tailwinds for the right stocks.

So far this year, Mad Hedge earned an astounding 77.20% profit cashing in on this year’s trends. We could earn the same return taking advantage of next year’s trends.

If you want to ride along on my coattails next year, that is fine with me. But it requires you to take a leap of faith.

I refer you to the motto of Britain’s Special Air Service: “Qui audet adipiscitur,” or “Who dares wins.”

For it only makes sense that the worst stocks of 2022 will be the best performers of 2023.

I have no doubt that tech stocks will bottom out sometime in 2023. Those who get in early will build some of the largest fortunes of this century. Those who miss the boat will spend their retirement years working at Taco Bell.

The reasons are very simple.

*Ultra-high interest rates will force a mild recession in early 2023. Then suddenly, inflation will plummet. We know this has already started because the largest element in the inflation calculation is housing costs, which are in free fall.

*The Fed will panic and deliver 2023 the sharpest DECLINE in interest rates in American history.

*Plunging interest rates will bring a crash in the US dollar.

*Foreign currencies like the Euro (FXE), the Japanese Yen (FXY), and the Australian dollar (FXA) will soar.

*And guess who gets the bulk of their earnings from abroad, sometimes up to two-thirds? The technology industry.

Kaching!

If you think I’m out of my mind, just look at the top performers of the historic stock market rally last week.

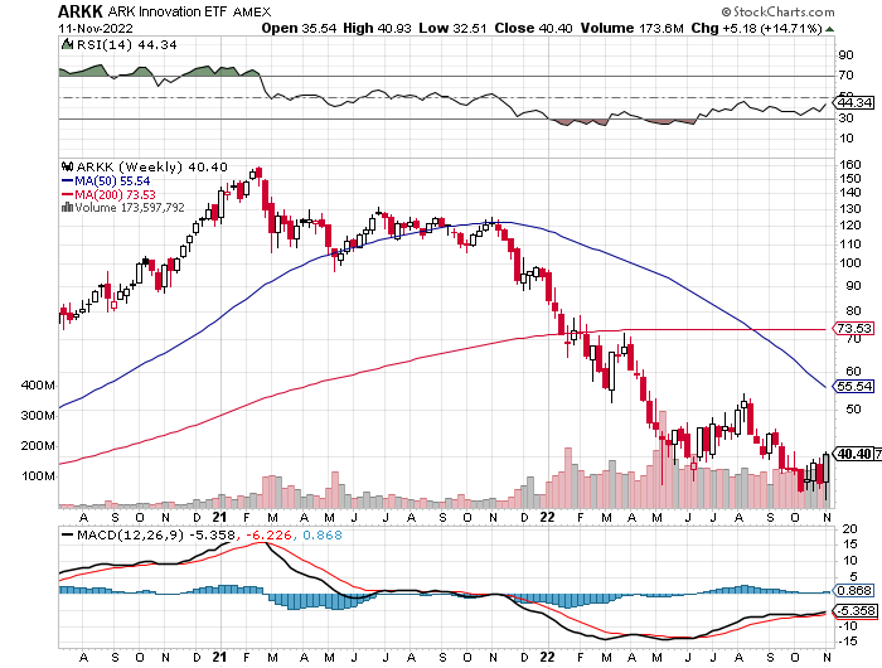

All the interest rate-sensitive sectors caught on fire. Technology stocks took off like a scalded cat, with Cathie Woods’ Ark Innovation Fund (ARKK) up an astounding 14% in a single day.

Bank shares soared. Homebuilders (LEN), (KBH), (DHI) caught a strong bid for the first time in ages. Junk bonds went bid only. US Treasury Bonds had their best day in 20 years (TLT), while the greenback (UUP) had its worst.

The bottom line here is so clear that I’ll write it on a wall for you. Falling interest rates will be the primary driver of stock prices for 2023 and 2024.

Of course, there is a better way to play this than buying the first technology index you stumble across.

So, let me boil this strategy down to just five names, close your eyes, and buy them.

Rivian (RIVN)– ($34) - Rivian is widely believed to be the next Tesla (TSLA). Some 25% owned by its largest customer, Amazon (AMZN), Rivian produces three types of EVs: the R1T pickup truck, the R1S SUV, and Amazon's EDV (electric delivery van). Its R1 vehicles start at under $70,000 and can travel more than 300 miles on a single charge. To learn more about Rivian, please click here.

To say that Rivian is the hot car of the day would be a vast understatement. New cars are trading for double list on the grey market. Owners complain of getting mobbed with gawkers whenever they hit the beach or the ski slopes. The buzz has led to an outstanding order book of an impressive 98,000, or four years of current production. The obvious cool factor allows enormous pricing power.

And here is the key to buying Rivian at this time. At 25,000, it is right at the mass production point where Tesla shares went ballistic all those years ago. And it already has an 80% decline in the price, in the rear-view mirror.

In 2024, Rivian plans to open its second plant in Georgia. After it fully expands its Illinois plant, it expects its annual production capacity to reach 600,000 vehicles.

Inflation Reduction Act passed this summer greatly accelerated rollout of the entire EV industry, which created a $7,500 per vehicle tax credit on top of state benefits.

Yes, this company offers venture capital-type risks. But it offers venture capital-type returns as well, up 10X-50X from here.

Ark Innovation Fund (ARKK) – ($40) – Cathie Woods’ high-tech fund was the proverbial red-headed stepchild of this bear market. It fell a gut-punching 80% from the 2021 top until last week. Just to get back to its old high, likely over the next five years, it has to rise by 400%. Its largest holdings are a real rollcall of the severely abused, Tesla (TSLA), Roku (ROKU), Exact Sciences (EXAS), Intellia (INTL), and Teladoc Health (TDOC), which Woods actively trades. But they are also a valuable insight into the future, EVs, CRISPR technology, robotic surgery, and molecular diagnostics. To learn more about the Ark Innovation Fund, please click here.

ProShares Ultra Technology ETF (ROM) – ($27) – This is a 2X long technology ETF that gives you an extremely aggressive position across the tech sector. It has 19% of its holdings in Apple (AAPL), 16% in Microsoft (MSFT), 10% in Alphabet (GOOGL) and Google (GOOG), at 3.5% in NVIDIA (NVDA), and 120 other smaller names. (ROM) shares are down a breathtaking 67% just in the past year. To learn more about the (ROM), please click here.

Palo Alto Networks (PANW) - $165 – Hacking is one of the fastest-growing sectors in technology, it is recession-proof and immune to the economic cycle. As a result, spending on the defense against hacking is absolutely exploding. Palo Alto Networks, Inc. is an American multinational cybersecurity company with headquarters in Santa Clara, California. Its core products are a platform that includes advanced firewalls and cloud-based offerings that extend those firewalls to cover other aspects of security. I have already earned a tenfold return over the past decade and expect to make another 10X in the coming years. You won’t find any dips in this stock as too many people are trying to get into it. To learn more about the Palo Alto Networks, please click here.

Salesforce (CRM) - $157 – The baby of tech genius Mark Benioff, this company is the dominant player in customer relationship management. If you want to do any business in the cloud, and almost all big companies do, you are up to your eyeballs in customer relationship management. Salesforce is the largest San Francisco-based cloud-oriented software company with virtually all of the Fortune 500 as its customer list. It provides customer relationship management software and applications focused on sales, customer service, marketing automation, analytics, and application development. Salesforce shares have been the target of a haymaker, down 55% in a year. To learn more about Salesforce, please click here.

You know what? I can do better than this.

I can create customized options LEAPS for you that will deliver a tenfold return on whatever performance these ultra-high beta stocks deliver. If the shares of one of my picks rise by 100%, you will make 1,000%.

This is an investment strategy that will enable you to retire early, real early. Tired of punching a time clock or logging into the next Zoom meeting on time?

Those will become a distant memory if you pursue my Mad Hedge Investment strategy for 2023.

As a result, my November month-to-date performance went off to the races, already achieving a hot +2.20%.

That leaves me with a very rare 100% cash position. With midterm election results out on Wednesday and the next report on the Consumer Price Index on Thursday, that sounds like a prudent place to be.

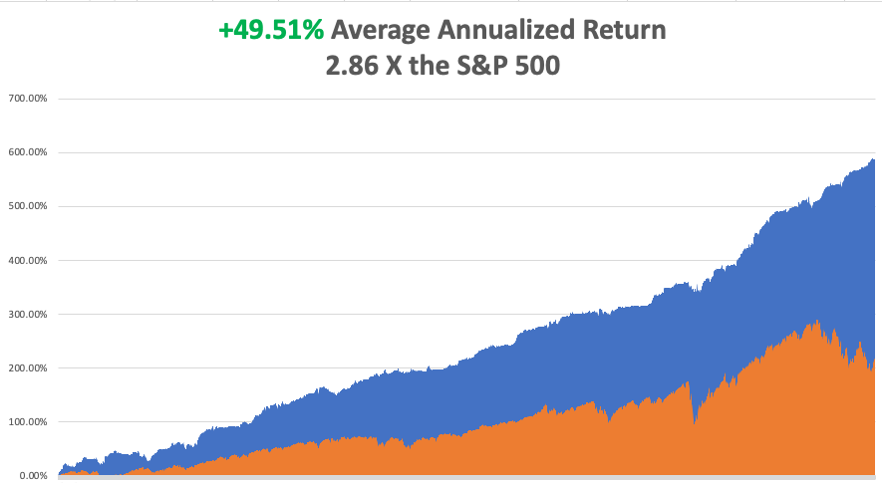

My 2022 year-to-date performance ballooned to +77.57%, a new high. The Dow Average is down -11.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +75.53%.

That brings my 14-year total return to +590.13%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +49.51%, easily the highest in the industry.

Bonds Clock Best Day in Years, taking the ten-year US Treasury bond fund up $3.64. All low interest rate plays had monster days. Junk bond ETFs (JNK) and (HYG) were up two points. 30-year fixed rate mortgages dropped 60 basis points to 6.60%, the biggest drop in history. Long bonds will be THE big trade of 2023.

US Dollar has Worst Day in 20 Years, driven by plunging interest rates. Big tech, which gets a major share from overseas sales, rocketed. Apple alone was up $12. Cathy Wood’s Ark Innovation Fund (ARKK) was up an incredible 14%. It vindicates my view that tech will turn when interest rates and the dollar fall.

Oil Companies (USO) Book Record $200 Million Profit this year, using the Ukraine War to double your cost of gasoline. If we have a recession next year, or the war ends, energy share prices should be peaking around here. Even if they don’t, the risk-reward here is terrible. It means we will have to pay a much higher price to decarbonize the economy at a later date.

Wells Fargo Gets Hit with $1 Billion Fine for its many regulatory transgressions over the last decade. Looting of customer accounts with bogus fees has been a recurring problem. Use any selloffs to buy (WFC) on dips.

Berkshire Hathaway's 20% Profit Increase YOY and buys back another $1 billion worth of stock. However, they did take a $10 billion loss on stocks in Q3 during the market meltdown. Keep buying (BRKB) stock and LEAPS on dips.

$1.5 trillion in Homeowners Equity Lost Since May, thanks to interest rates at 20-year high and a shrinking money supply. Since July, the median home price has dropped by $11,560. The average borrower has lost $30,000 in equity. It’s not a great time to rent either as prices there are soaring. Residential housing could remain weak for another 12-24 months, compared to the six-year drawdown we had from 2006.

Boeing Orders Rise in October, but deliveries fall. The company is finally out of the penalty box, up 40% since October 1. Don’t buy (BA) up here.

The Red Wave Fails to Show, with control of congress still too close to call. Republican House control has shrunk from an expected 60 seats six months ago to maybe two today. Donald Trump threw the election for his party, picking unelectable extremist candidates and campaigning where he wasn’t wanted. A pro-life Supreme Court brought out millions of women voters across the country. If the Republicans can’t win with inflation at 8.7%, they are toast in 2024 when it drops back down to 2%.

Market Dives 646 Points on Democratic Win, with technology stocks taking the biggest hit. The red wave no-show was a black swan traders were not looking for. Energy was the worst performing sector because they aren’t getting the air cover they paid for with a red wave. The result was much as I expected, which is why I went into November 8 with a rare 100% cash position waiting to buy the next low. It turns out that rights are more important than prices.

Elon Musk Sells More Tesla Shares and Warns of a Twitter Bankruptcy, some $3.9 billion worth, bringing this year’s total to $36 billion. Musk is raising money to head off a bankruptcy of Twitter now that major advertisers are fleeing en masse. This certainly is a distress sale. If Musk was looking to build a real business, re-tweeting fringe conspiracy theories was the worst thing he could have done. Endorsing the Republican party will cost him half of his customers. Is this Musk’s Waterloo, or his Dien Bien Phu?

Facebook to Lay Off 11,000, about 13% of its total employees. Zuckerberg admits the error of pushing the company into the metaverse too far too fast. With the stock down 77%, there are not a lot of happy campers at One Hacker Way. Avoid (META) for now, but it may be a 2023 play when we get closer to a new final product.

FTX Becomes an Epic Bankruptcy, with $9.5 billion missing from its balance sheet, in one of the biggest blowups of the crypto age. Losses are expected to reach $50-$60 billion, with the bankruptcy of 130 affiliated companies. It is also a potential Dept of Justice target. All affiliated tokens and coins have gone to zero. So, placing your money with a fresh-faced kid in the Bahamas wearing baggy shorts and with no financial background was not such a great idea after all. It’s amazing how many serious people were sucked in on this one. At least Sam Bankman-Fried said he was sorry.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 14 at 8:00 AM, the Consumer Inflation Expectations for October are released.

On Tuesday, November 15 at 8:30 AM, the Producer Price Index for October is released.

On Wednesday, November 16 at 8:30 AM, Retail Sales for October are published.

On Thursday, November 17 at 8:30 AM, Weekly Jobless Claims are announced. Housing Starts and Permits for October are also out.

On Friday, November 18 at 10:00 AM, the Housing Starts for October are printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I am often told that I am the most interesting man people ever met, sometimes daily. I had the good fortune to know someone far more interesting than myself.

When I was 14, I decided to start earning merit badges if I was ever going to become an Eagle Scout. I decided to start with an easy one, Reading Merit Badge, where you only had to read four books and write one review.

I was directed to Kent Cullers, a high school kid who had been blind since birth. During the late 1940s, the medical community thought it would be a great idea to give newborns pure oxygen. It was months before it was discovered that the procedure caused the clouding of corneas and total blindness. Kent was one of these kids.

It turned out that everyone in the troop already had Reading Merit Badge and that Kent had exhausted our supply of readers. Fresh meat was needed.

So, I rode my bicycle over to Kent’s house and started reading. It was all science fiction. America’s Space Program had ignited a science fiction boom and writers like Isaac Asimov, Jules Verne, Arthur C. Clark, and H.G. Welles were in huge demand. Star Trek came out the following year, in 1966. That was the year I became an Eagle Scout.

It only took a week for me to blow through the first four books. In the end, I read hundreds to Kent. Kent didn’t just listen to me read. He explained the implications of what I was reading (got to watch out for those non-carbon-based life forms).

Having listened to thousands of books on the subject, Kent gave me a first class education and I credit him with moving me towards a career in science. Kent is also the reason why I got an 800 SAT score in math.

When we got tired of reading, we played around with Kent’s radio. His dad was a physicist and had bought him a state-of-the-art high-powered short-wave radio. I always found Kent’s house from the 50-foot-tall radio antenna.

That led to another merit badge, one for Radio, where I had to transmit in Morse Code at five words a minute. Kent could do 50. On the badge below the Morse Code says “BSA.” In those days, when you made a new contact, you traded addresses and sent each other postcards.

Kent had postcards with colorful call signs from more than 100 countries plastered all over his wall. One of our regular correspondents was the president of the Palo Alto High School Radio Club, Steve Wozniak, who later went on to co-found Apple (AAPL) with Steve Jobs.

It was a sad day in 1999 when the US Navy retired Morse Code and replaced it with satellites. However, it is still used as beacon identifiers at US airfields.

Kent’s great ambition was to become an astronomer. I asked how he would become an astronomer when he couldn’t see anything. He responded that Galileo, the inventor of the telescope, was blind in his later years.

I replied, “good point”.

Kent went on to get a PhD in Physics from UC Berkely, no mean accomplishment. He lobbied heavily for the creation of SETI, or the Search for Extra Terrestrial Intelligence, once an arm of NASA. He became its first director in 1985 and worked there for 20 years.

In the 1987 movie Contact written by Carl Sagan and starring Jodie Foster, Kent’s character is played by Matthew McConaughey. The movie was filmed at the Very Large Array in western New Mexico. The algorithms Kent developed there are still in widespread use today.

Out here in the west aliens are a big deal, ever since that weather balloon crashed in Roswell, New Mexico in 1947. In fact, it was a spy balloon meant to overfly and photograph Russia, but it blew back on the US, thus its top secret status.

When people learn I used to work at Area 51, I am constantly asked if I have seen any spaceships. The road there, Nevada State Route 375, is called the Extra Terrestrial Highway. Who says we don’t have a sense of humor in Nevada?

After devoting his entire life to searching, Kent gave me the inside story on searching for aliens. We will never meet them but we will talk to them. That’s because the acceleration needed to get to a high enough speed to reach outer space would tear apart a human body. On the other hand, radio waves travel effortlessly at the speed of light.

Sadly, Kent passed away in 2021 at the age of 72. Kent, ever the optimist, had his body cryogenically frozen in Hawaii where he will remain until the technology evolves to wake him up. Minor planet 35056 Cullers is named in his honor.

There are no movies being made about my life…. yet. But there are a couple of scripts out there under development.

Watch this space.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/11/boy-scouts.png625418Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-14 10:02:212022-11-14 11:26:31The Market Outlook for the Week Ahead, or The Top Five Technology Stocks of 2023

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.