Imagine you're the CEO of a major pharmaceutical company. You've got blockbuster drugs that are raking in billions, a cushy corner office, and a corporate jet at your disposal. Life is good.

But then, you look at the calendar and realize that your patents are about to expire. Suddenly, that jet feels more like a crop duster, and your corner office starts to feel like a broom closet.

That's the reality facing Big Pharma right now. These pharma big shots are sweating bullets over losing their golden geese like AbbVie's (ABBV) Humira and Merck's (MRK) Keytruda.

That’s roughly $300 billion in products about to get kicked to the curb.

But these guys didn't get to the top by sitting on their hands. They've got a war chest of $1 trillion, and they're not afraid to use it.

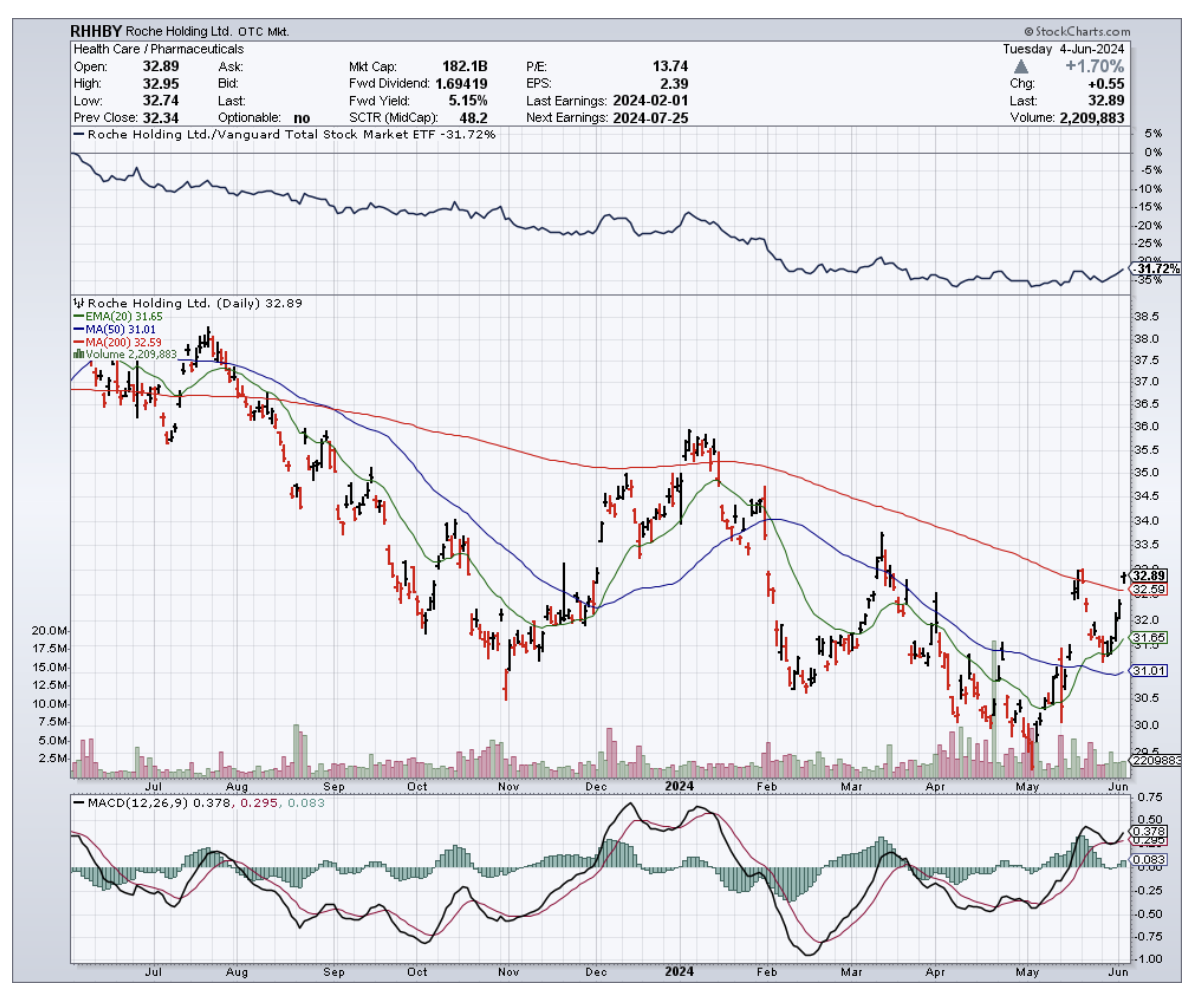

Major pharmaceutical giants like Pfizer (PFE), Roche (RHHBY), Johnson & Johnson (JNJ), AstraZeneca (AZN), and GlaxoSmithKline (GSK) are about to go on the mother of all shopping sprees.

Why the rush? Because they're staring down the barrel of a patent cliff that's going to make the Grand Canyon look like a pothole.

We're talking $198 billion worth of branded drugs going off the patent cliff between 2021 and 2025. That's a gut-wrenching 56% jump from the last five years.

But don't think for a second that they're just going to sit back and watch their profits go up in smoke. No sir, they're on the hunt for the next big thing, and they've got their sights set on some juicy targets – and biotech is at the top of their list.

Leading the biotech charge are mRNA pioneers Moderna (MRNA) and BioNTech (BNTX), each sitting on a gold mine of potential blockbusters taking on everything from flu to cancer vaccines.

Underdogs like CRISPR (CRSP) biotech stars Intellia (NTLA) and Beam Therapeutics (BEAM) are also squarely in Big Pharma's acquisition crosshairs for their cutting-edge work in genetic disease treatments.

But beyond the headliners, don't overlook the sleeper hits that could catalyze the next big boom.

Oncology, in particular, is a prime hunting ground, accounting for 37% of pharma M&A deal value in 2023 as the $392 billion global cancer drug market continues to boom.

Companies like Turning Point Therapeutics (TPTX) and Zentalis Pharmaceuticals (ZNTL), with their promising targeted therapies for various solid tumors, are particularly attractive prospects.

Mirati Therapeutics (MRTX), focused on KRAS inhibitors, and Blueprint Medicines (BPMC), specializing in precision therapies, have also caught the eye of big pharma with their innovative approaches.

Additionally, companies with late-stage assets like MacroGenics (MGNX), Mereo BioPharma (MREO), and Tyra Biosciences (TYRA) could offer promising near-term revenue opportunities for acquiring companies looking to bolster their oncology portfolios.

Close behind are rare disease treatments, snagging 16% of new drug approvals and 9 of the top 100 deals last year in this $262 billion market ripe for more growth.

This lucrative sector has captivated pharma giants, who see potential in companies like Sarepta Therapeutics (SRPT) and Vertex Pharmaceuticals (VRTX), leaders in rare disease therapies with strong financial performance and consistent growth.

Aside from these, smaller biotechs like Amicus Therapeutics (FOLD) and Ultragenyx Pharmaceutical (RARE), focused on developing innovative therapies for a range of rare diseases, are attracting attention for their potential to address unmet medical needs and deliver substantial returns on investment.

But the real wild card everyone wants a piece of is cell and gene therapies. This medical Wild West is projected to explode to $66.8 billion by 2030, with the FDA already greenlighting 6 cutting-edge therapies like next-gen CAR-T treatments from Caribou Biosciences (CRBU) in 2023 alone.

Notably, the buying frenzy is very much already underway. In fact, 2023 saw the biggest biotech M&A spree in a decade, with a staggering $122.2 billion changing hands as the FDA approved 50% more new therapies.

Pharma mega-mergers also hit $135.5 billion as firms raced to reload pipelines.

Interestingly, these deals are only the tip of the iceberg. As Wall Street predicts, with record-smashing deals, sky-high demand, and new approvals surging, "biotech's got plenty of reasons to be cautiously optimistic."

Especially if interest rates finally cooperate, throwing gasoline on the M&A bonfire and making biotech the belle of the ball as soon as late 2024.

So keep your eyes peeled and your powder dry. I suggest you add these innovative biotech names to your watchlist, and you might just discover the next blockbuster drug or breakthrough therapy that could reshape medicine – and deliver explosive returns in the process.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-11 12:00:012024-06-11 12:03:04The Capital Cure

Well, well, well, look who's decided to crash the obesity-drug party. Roche (RHHBY), the Swiss pharmaceutical giant, has just unveiled some pretty impressive early-stage results for its weight-loss drug, CT-388. And let me tell you, this could be the start of something big.

Now, I know what you're thinking: "Another weight-loss drug? Yawn." But trust me, this is no ordinary contender.

In a small trial, patients who received CT-388 saw an average placebo-adjusted weight loss of 18.8% after just 24 weeks. That's right, 18.8%.

While it's hard to compare trials, experts are saying these numbers might even give Eli Lilly's (LLY) Zepbound, the current king of the market, a run for its money.

Let's take a step back and look at the bigger picture. The obesity drug market has been on fire lately, with everyone going gaga over these miracle pills.

Lilly and Novo Nordisk (NVO) have been dominating the scene with their drugs, Zepbound and Wegovy, but that hasn't stopped a whole host of other companies from trying to get a piece of the pie.

Merck (MRK), Sanofi (SNY), Abbott Labs (ABT), and Eisai have all tried their hand at weight-loss drugs and ultimately thrown in the towel.

More recently, Pfizer's (PFE) daily oral pill, danuglipron, has faced hurdles due to side effects. Amgen's (AMGN) drug, MariTide, is in Phase 2 studies and showing promise. And let's not forget Viking Therapeutics' (VKTX) VK2735, which has earned the nickname "twincretin" for its dual targeting of GLP-1 and GIP receptors.

So, what makes Roche's CT-388 so special?

Well, for starters, it's a GLP-1/GIP receptor agonist, which is similar to Lilly's Zepbound. In the Phase 1 trial, all participants achieved more than 5% weight loss, with 85% losing more than 10%, 70% shedding more than 15%, and a whopping 45% dropping more than 20% of their body weight. That's some serious weight loss.

Of course, there were some side effects, mainly mild to moderate gastrointestinal issues, but hey, that's the price you pay for looking fabulous, right? Roche is also testing CT-388 in patients with Type 2 diabetes, so stay tuned for updates on that front.

Now, I know you're all dying to know how CT-388 stacks up against the competition.

Notably, the drug's data looks strong compared to earlier studies of Zepbound. In fact, CT-388's efficacy results appeared "numerically higher" than Zepbound's.

But let's not get ahead of ourselves. Lilly still has a multi-year lead on Roche, so CT-388 isn't an immediate threat. However, it does suggest that the future of this rapidly growing market is up for grabs.

Now, let's talk about Roche. It’s the world's seventh-largest pharma company by market cap, sitting at around $205 billion. They pulled in $65 billion in revenue in 2023, second only to Johnson & Johnson (JNJ).

But here's the kicker—they've been struggling with growth, and their share price has taken a hit, down more than 25% over the past three years.

Contrast that with Eli Lilly and Novo Nordisk. Lilly's share price shot up 290% in three years, and Novo's climbed 226%.

Even though their revenues were less than half of Roche's in 2023, their market caps are sky-high. Why? Because of their blockbuster GLP-1 agonist drugs, Zepbound and Wegovy, which have shown jaw-dropping weight-loss results.

But could CT-388 be the underdog story Roche needs?

With the obesity market estimated to reach a staggering $100 billion by 2030, and over 1 billion people worldwide suffering from obesity, the potential is enormous.

Of course, there's still a long way to go for CT-388. Cross-trial comparisons can be tricky, and Roche's Phase 1 trial was much smaller than Lilly's pivotal study of Zepbound.

Plus, we don't have all the juicy details on patient characteristics, dose titration, and long-term weight loss just yet.

But here's the thing: Roche has scale and infrastructure on its side. It could potentially outmuscle smaller players like Viking and Boehringer Ingelheim.

And if CT-388 can match or even surpass the performance of current and future GLP-1 agonists? Well, let's just say those peak revenue forecasts might be in for a surprise.

So, is Roche the dark horse you should bet on in the obesity-drug race? If you're looking to get in on the action without paying the premium commanded by Lilly and Novo, or taking on the higher risk of smaller players, Roche might just be the ticket.

With promising mid-single-digit revenue growth on the horizon and a strong position in other areas like oncology and autoimmune disorders, Roche could be a smart play for anyone keen on the obesity drug market.

As for me? Well, you know I love an underdog story. And CT-388 might just be the Cinderella story of the year. I suggest you buy the dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-05-21 12:00:422024-05-21 12:21:44The Fat's In The Fire

Big pharma usually makes investors smile - fat profits, juicy dividends, and stocks that crush the market.

Lately, though, some of these giants are looking more like grumpy old men. Sure, there are exceptions like Novo Nordisk (NVO) and Eli Lilly (LLY) printing money with their obesity blockbusters.

But what about the rest? Even with Washington breathing down their necks, patent cliffs, and a shaky economy, you'd think these drug titans wouldn't be lagging the market, right? Wrong.

Check out the "Big Eight" top dogs - Johnson & Johnson (JNJ), Merck (MRK), AbbVie (ABBV), Pfizer (PFE), and the rest. Only a few have really delivered the goods in the past five years. AbbVie and Merck have been alright, but the others? They make me want to take a nap.

Now, I'm not saying give up on pharma entirely - there's still money to be made. But you've got to do your homework. Today, let's take a look at Merck.

They raked in $60.1 billion in 2023, making them a heavy hitter. But without their COVID cash machine Lagevrio, growth is...less impressive. Still up, but not setting the world on fire.

The real story is spending - Merck went on a spree, burning through cash on R&D. Why? Their golden goose Keytruda, that $25 billion cancer blockbuster, is facing generic competition soon.

Merck isn't just sitting around waiting for the Keytruda patent cliff either. They're furiously throwing money at new drugs, acquisitions, cancer, heart disease, immune disorders - hoping to find the next Keytruda before the current one fades away. It's like an aging rockstar desperately trying to write another big hit.

But let's be real, finding billion-dollar breakthroughs is a gamble, even for giants like Merck. They've got potential in the pipeline for sure, but it's a long road from the lab to pharmacy shelves. Plenty of drugs flame out along the way.

Looking back, 2023 wasn't a victory parade for Merck. It was more like a mad dash to spend their way out of the looming Keytruda patent cliff.But hey, sometimes you've gotta break a few eggs to make an omelet, right?

Speaking of potential winners, let's talk about those newly approved lung drugs – sotatercept could be a major player.

Merck's vaccine department is looking strong too, with potential blockbusters targeting lung infections and RSV in the pipeline.

Of course, it hasn't all been smooth sailing. That new cough drug, gefapixant, getting rejected by the FDA again? Merck took a hit on that. Still, this biotech’s not giving up. This is a company buying time to build up a whole new arsenal, and the Keytruda cliff might hurt, but they'll come out swinging.

So, let’s forget about that 2023 earnings dip. Merck's forecasting a serious jump in 2024 profits as they dial back the crazy spending. Yes, their balance sheet took a hit, but look at what they're building. They're hunting big deals to bolster that pipeline, and that's a good thing in my book.

Speaking of big moves, Merck's been on a shopping spree. Wall Street might get nervous if they drop another bombshell, but I trust their judgment. These aren't just random buys; this is how they protect their future cash flows. Besides, any short-term drama from a big deal could be a sweet buying opportunity.

And while Merck’s still figuring out which one could be the next big thing, the true star of the show, until that patent cliff arrives, is still Keytruda.

That beast is still growing and could keep going strong for years, especially in early-stage treatments. Plus, that new subcutaneous version of this blockbuster treatment? Talk about extending the gravy train well past the generic competition.

Let's also check out the other horses in this race: sotatercept's early sales numbers, a potential FDA approval for that HER2 drug, the saga of gefapixant's third shot (or not), and the cash potential of V116 and Welireg. Not to mention, juicy updates on that Moderna (MRNA) partnership…Merck’s next months could be packed with surprises.

As for this company’s dividend? Decent track record, but don't expect fireworks after the recent hike. As for buybacks, Merck seems to have...other priorities right now. Those profits are pouring straight into the growth pipeline.

The bottom line: While some of Big Pharma looks pale lately, Merck is still bringing it, share price gains and all. Sure, that gefapixant rejection stings. But Keytruda keeps roaring, and Merck's pipeline is buzzing with potential. I'm not sweating earnings.

Merck's got contingencies lined up for the Keytruda patent apocalypse - new drugs, deals, maybe even extending Keytruda itself. They're playing for the long game here. I suggest you buy the dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-25 12:00:432024-04-25 13:36:39Racing To Swap A Golden Goose For A New Flock

It looks like Merck (MRK) just scored a major touchdown in the drug wars, which might make the looming Keytruda patent expiration sting a little less.

Remember when Merck dropped $11.5 billion on Acceleron back in 2021 to get their hands on Winrevair (then known as Sotatercept)? That was a seriously gutsy move to soften the blow when their Keytruda goldmine started drying up.

Talk about a gamble. Acceleron didn't even have their Phase 3 trial results in hand yet. A lot of people were scratching their heads at the time, thinking maybe Merck had lost their marbles.

But fast-forward to today, those Phase 3 results drop, and here we are. Turns out Merck knows a thing or two about playing the long game.

Their new drug, Winrevair, which just got the FDA thumbs up for a rare heart condition, tackles a serious heart condition called pulmonary arterial hypertension (PAH).

PAH is no joke – it basically strangles your lungs and heart, drastically shortening your lifespan. Unlike those old PAH drugs like Uptravi from Johnson & Johnson (JNJ), Winrevair's got a completely different way of fighting back. That could be huge for patients who aren't getting enough relief with current options.

Winrevair targets that messed-up TGF-beta pathway, trying to reverse some of the damage caused by this disease.

Although PAH might be rare, affecting an estimated 15 to 50 people per million in the United States and Europe, those who suffer from it are often desperate for effective treatments.

The global PAH market is already worth a staggering $7.3 billion annually and is projected to hit $12.18 billion by 2032.

Merck's timing couldn't be better. Not only did Winrevair sail through approval, but it also dodged all those nasty black box warnings and extra safety hoops some drugs have to jump through.

Translation: this drug is about to hit the market full speed ahead.

Given the promise of this new drug, Merck must be popping champagne corks right about now. No restrictions mean doctors can prescribe this stuff far and wide – that's a probable goldmine, especially for a serious disease like PAH.

Let's not forget why all this matters. Keytruda was a $25 billion cash cow for Merck in 2023, making up a huge chunk of their revenue.Those cheap knock-offs are coming in 2028, ready to eat into that sweet slice of the pie.

But thanks to Wenrevair, that future doesn’t seem too daunting anymore.

Merck has set a price of $14,000 per vial for Winrevair, translating to an average annual cost of $212,000 per patient. While this may seem steep, it reflects the drug's potential to improve the lives of PAH sufferers and secure Merck's financial future.

Actually, analysts are predicting peak sales of a mind-boggling $11 billion – maybe even $8 billion at the low end.Either way, that's a massive lifeline for Merck as they brace for the dreaded Keytruda patent cliff in 2028.

In fact, Winrevair could pull in $500 million this year alone, jumping to $3 billion by 2027. Talk about a growth spurt.

With Winrevair set to change the PAH treatment landscape, investors can breathe easy knowing that Merck has a new ace up its sleeve.

After all, this drug is practically guaranteed to be another blockbuster, which is great news considering the looming Keytruda patent expiration in 2028.

Merck's audacious $11 billion bet on Acceleron seems to be paying off – Winrevair could easily bring in $30 billion over its lifespan.

But let's not get too carried away – Winrevair won't single-handedly save Merck in the long run.They'll need more hits to keep outperforming the competition.

For now, Merck seems like a decent hold. It's got reasonable growth potential, and you might even want to nab some shares if the price dips.

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.