Global Market Comments

October 20, 2023

Fiat Lux

Featured Trade:

(TESTIMONIAL)

(OCTOBER 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(LMT), (MS), (GOOG), (NVDA), (TSLA), (MSFT), (AMZN), (APPL), (META), (FXI), (RIVN), (NFLX)

Global Market Comments

October 20, 2023

Fiat Lux

Featured Trade:

(TESTIMONIAL)

(OCTOBER 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(LMT), (MS), (GOOG), (NVDA), (TSLA), (MSFT), (AMZN), (APPL), (META), (FXI), (RIVN), (NFLX)

Below please find subscribers’ Q&A for the October 18 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from London England.

Q: Is Nvidia (NVDA) a buy at the current price?

A: Absolutely, if your view is more than, say, a month. This stock will easily be $1,000 in the next year or two. They have such a huge moat on their business, and the high-end chips that are banned in China are only a tiny fraction of their overall business—they’re still allowed to sell small and medium-sized chips.

Q: Where do you see bond yields peaking out?

A: My pet target is 5.2% on a spike. We may get there in a few weeks or months. The position we have breaks even at 5.15% in 21 trading days. So any kind of rally on that position becomes profitable—even a one-day rally.

Q: Are you hitting Israel next?

A: No, I covered the Middle Eastern wars for 10 years starting with the ‘73 Yom Kippur wars, and I got sick of it. They’re using the same arguments to justify their positions that they were 50 years ago. In fact, the disputes have been going on for hundreds of years. So, I moved on to other more interesting wars like Ukraine. There are plenty of newbies cutting their teeth as war correspondents in Gaza now—I'll leave it to them.

Q: Are the results for all of the newsletters or just for one?

A: Those alerts that I send out personally are the results for the Mad Hedge Global Trading Dispatch. All of the other services (we have six now) have their own trade histories which we don’t publish, as it’s too much of an account job effort to update six independent track records. People know whether they’re making money or not—that's good enough for me. That’s how we’re set up; we’re a staff-light operation so that we can keep the prices low.

Q: What do you expect for Tesla (TSLA) earnings today?

A: I never make same-day earnings calls, but I would expect they’d be good. They would be less than they were in the past because the price wars are cutting into margins, but they’re gaining market shares at everybody else’s expense, which makes (TSLA) a “BUY”. In fact, if you look at the charts, it seems to be moving sideways into an upside breakout.

Q: Is it too late to buy military?

A: No, I’d be buying any of the big military stocks like Lockheed Martin (LMT), because the increase in demand for weapons is not a short-term thing—it is a more or less permanent thing which will go out decades. Also, they all already have massive government contracts to rebuild our own weapons. Most people don't realize that almost every weapons system in the United States is more than 50 years old. The reason is we quit investing in conventional weapons because we all thought the next war would be cyber. Well, Russia got absolutely nowhere on cyber—they made a few weak attempts to shut down Ukraine and couldn't even break into Elon Musk’s Skylink system, which all of Ukraine is running on.

Q: Why is Morgan Stanley (MS) doing so poorly?

A: All the financials are getting hit because of the collapsing bond market. Once the bond market finds a bottom you want to be buying financials with both hands.

Q: When the market recovers, which sector will lead?

A: Technology. The Magnificent Seven will lead. There’s safety in size. Google/Alphabet (GOOG), Nvidia (NVDA), Tesla (TSLA), Microsoft (MSFT), Amazon (AMZN), Apple (APPL), Facebook/Meta (META). They’re already leading now, so if you have those positions, I’d keep them. If you don’t, you should start picking them up.

Q: Is Rivian (RIVN) a buy at this level?

A: Absolutely. Amazon, which owns 25% of the company, just hit 10,000 Rivian delivery vans. I’ve seen them in California, they’re completely silent—very interesting cars. It’s just a question of how quickly they can produce them.

Q: Why is there a market drop today?

A: It’s the bond market. The first thing you look at every day is the bond market—if it's doing crappy, everything sells off.

Q: Do you still suggest 90-day T-bills at this point?

A: We may end up getting a stock buying opportunity into the year-end. Even if we have to wait for a yearend rally, you get paid every day for 90-day T-bills, and you can sell them at any time and get interest up to the day you sell them because they’re discount bonds that appreciate every day to reflect the yield. It’s a great way to park money, and most brokers will let you buy stocks against your 90-day T-bill position. So say you want to go fully invested in stocks—you could do that while selling your 90-day T-bills the same day. Most brokers will let you do that, worst case charging you one day of margin.

Q: Do you think China is using the Hamas attack on Israel to distract the US?

A: No, China wouldn’t want to get involved in this. Iran has its fingerprints all over it. Iran supplied all the missiles used to attack Israel, and if the Israelis turn around and attack Iran by destroying all of their nuclear and missile-making facilities, I would not be surprised one bit. That may be what Biden is really doing over there—trying to convince the Israelis not to escalate the war.

Q: What are the chances of a US default on November 17 (TLT)?

A: So far on all of these government shutdowns, the US Treasury has been able to come up with magic tricks to keep from defaulting; but if the default is long enough, even they will have to stop paying interest to bondholders, which will increase the debt burden of the US government because a lower credit rating will cause it to pay higher interest rates. Why people think this is a great strategy is beyond me.

Q: Gasoline is down and oil is up—what’s going on?

A: That’s usually driven by the crack spread—the availability of gasoline from refineries in the US, so I wouldn’t use that as any kind of indicator.

Q: Do you think China (FXI) is shifting priorities away from economic growth to military strength?

A: No I don’t, they would love to have economic growth if they could, and in fact, their central bank has been stimulating their economy, and it's working; that’s how this morning’s report got back up to 5%. At the end of the day, they just want peace. All this military stuff—they’re just bluffing and posturing, which is really all they’ve ever done, at least since the Korean War. They weren’t even big participants in the Vietnam War, so China doesn’t worry me at all; there are bigger things to worry about. But they definitely have hit a wall in economic growth, and a big part of that is Covid, and a big part of that is a shrinking population—a shortage of workers, and a shortage of workers who can support older parents.

Q: Will there be an oil embargo against Israel? The US and Europe by OPEC countries?

A: No. The Middle Eastern governments know what's really going on here, even though what they may say in public is completely different. The fact is that Hamas started this war, and none of these other countries want Hamas in their countries because they know that the first thing they'll do is overthrow the local government. Effectively, Hamas doesn’t exist anymore either—they've really all been killed, so you just have to give some time for things to cool down out there, and of course, the US is working overtime to keep the situation from escalating, but we can only try—we can’t enforce this thing. One question I've been getting from a lot of people lately is: will the US send troops to Israel or to Gaza? The answer is no—we were in Iraq and Afghanistan for 20 years! We’re in no hurry to get back into a new war, especially a new 20-year war, and that would not be in our own interest. By the way, Israel can amply defend itself; they have the best military in the Middle East by far, largely supported by the United States. For me, the big mystery is how intelligence in Israel missed this attack. They were just completely asleep at the switch, and some day in the future there will be an investigation about this, but don’t expect it from the current government.

Q: Why won’t Egypt and Jordan take the Palestinian refugees?

A: They are both poor countries. Neither of them is oil-rich, and Egypt especially has a horrendous population problem—they are in fact the world's second largest food importer after China. They have 110 million people to feed and not enough production locally to do that, so it isn’t easy to take in 2 million Palestinians. If you don't believe me, go to Cairo—it's just incredibly crowded. With a population of 10 million you can't go anywhere, so where are they going to put 2 million more people? So this is a difficult problem, there's no easy fix depending on what side you’re on.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2021 Mount Rose Summit Nevada

Mad Hedge Technology Letter

October 9, 2023

Fiat Lux

Featured Trade:

(GLOBAL WAR THREATENS TECH RALLY)

(GOOGL), (MSFT), (LMT), (EV), (CHINA)

Hot wars play a central role in accelerating inflation and the world’s newest kinetic war in the Middle East could prove toxic to the Fed’s quest to quell high inflation.

First, condolences to the atrocities that have occurred in the past 72 hours, the damage to families, society, and communities are hurtful and long-lasting.

Conflict in the Middle East means higher energy prices because a higher risk premium will be attached to the cost of logistics and production.

The Middle East has some of the highest outputs of oil and natural gas in the world with supply from Qatar, Saudi Arabia, and Iran flooding the world with cheap energy.

What does that mean for technology stocks?

I can tell you nothing good.

Physical wars rotate demand to certain goods that will deliver the consumer the best outcomes and in this case food and shelter. Running a supermarket during the lockdowns was a small gold mine. That means there is a high chance that money rotates out of Google and Microsoft and goes into defense and military stocks like Raytheon and Lockheed Martin (LMT).

Unless products are critical to survival, goods like EVs and Tesla’s (TSLA) are placed on the backburner.

Few will have the money to charge their EVs with another wave of price increases coming down the pipeline. I already hear Norwegians complaining about the cost of fueling EVs after cheap Russian energy was shut off to them.

Forget about an iPhone upgrade cycle.

Kids will just have to deal with the iPhone 14 for longer.

High inflation plays a leading role in wars and conflicts. But that doesn’t mean that economic policy doesn’t matter anymore. Less wars result in bigger tailwinds to deflation.

China also owns the rare metals industry and policy might dictate to hold back supply and earmark it for national and military industries instead of selling to foreigners.

Tesla’s might not be able to be produced anymore because they can’t secure the right materials like cobalt from China.

If a full-fledged regional war intensifies, then the US economy is almost guaranteed to lock in 4% as the new CPI low for this inflationary cycle. The next move would be higher.

The US has already pledge financial and military aid to Israel and that bill will be footed by the US taxpayer.

If this war begins to get expensive and the US starts shipping off $200 billion every few months to the Middle East then this fiscal spending will bring forward more inflation.

Ultimately, if a third war in the shape of Taiwan rears its ugly head, we could experience high 20% inflation like we did in the 1970’s, but this time around, we would do it with close to $34 trillion in US federal debt and those onerous debt interest payments.

The technology sector better hope and pray for a quick resolution to the Middle East conflict in order to stave off the threat of destroying the Santa Claus rally in the Nasdaq.

A third concurrent war in Taiwan would mean instant recession, spiking bond yields, $150 per barrel oil, and technology stocks experiencing a wild pullback.

In the meantime, the newest stresses will guarantee the Eurozone plus UK into a deep recession because they aren’t self-sufficient.

It also adds even more stress to the US economy which is the last man standing at this point because US tech earnings are still in the green.

Certain stocks do very well in times of geopolitics, but these multinational globalized companies have a lot to sacrifice if the world goes pear-shaped.

We’ve just seen our last interest rate rise in the economic cycle. Yes, I know that our central bank took no action at their last meeting in September. The market has just done its work for it.

And the markets are no shrinking violet when it comes to taking bold action. The 50 basis points it took bond yields up over the last two weeks is far more than even the most aggressive, economy-wrecking, stock market-destroying Fed was even considering.

And that doesn’t even include the rate hikes no one can see, the deflationary effects of quantitative tightening, or QT. That is the $1 trillion a year the Fed is sucking out of the economy with its massive bond sales.

It really is a miracle that the US economy is growing as fast as it is. After a warm 2.4% growth rate in Q2, Q3 looks to come in at a blistering 4%-5%. That is definitely NOT what recessions are made of.

Where is all this growth coming from?

Some of the credit goes to the pandemic spending, the free handouts we call got to avoid starvation while Covid ravaged the country. You probably don’t know this, but nothing happens fast in Washington. Government spending is an extremely slow and tedious affair.

By the time that contracts are announced, bids awarded, permits obtained, men hired, and the money spent, years have passed. That means money approved by Congress way back in 2020 is just hitting the economy now.

But that is not the only reason. There is also the long-term structural push that is a constant tailwind for investors:

Hyper-accelerating technology.

Yes, I know, there goes John Thomas spouting off about technology again. But it is a really big deal.

I have noticed that the farther away you get from Silicon Valley, the more clueless money managers are about technology. You can pick up more stock tips waiting in line at a Starbucks in Palo Alto than you can read a year’s worth of research on Wall Street.

What this means is that most large money managers, who are based on the east coast are constantly chasing the train that is leaving the station when it comes to tech.

On the west coast, managers not only know about the new tech, but the tech that comes after that and another tech that comes after that, if they are not already insiders in the current hot deal. This is how artificial intelligence stole a march on almost everyone, until a year ago, unless you were on the west coast already working in the industry. Mad Hedge has been using AI for 11 years.

You may be asking, “What does all of this mean for my pocketbook?” a perfectly valid question. It means that there isn’t going to be a recession, just a recession scare. That technology will bail us out again, even though our old BFF, the Fed, has abandoned us completely.

Which brings me to the current level of interest rates. I have also noticed that the farther away you get from New York and Washington, the less people know about bonds. On the west coast mention the word “bond” and they stare at you cluelessly. Indeed, I spent much of this year explaining the magic of the discount 90-day T-bill, which no one had ever heard of before (What! They pay interest daily?).

In fact, most big technology companies have positive cash balances. Look no further than Apple’s $140 billion cash hoard, which is invested in, you guessed it, 90-day T-bills when it isn’t buying its own stock, and is earning a staggering $7.7 billion a year in interest.

The great commonality in the recent stock market correction is easy to see. Any company that borrows a lot of money saw its stock get slaughtered. Technology stocks held up surprisingly well. That sets up your 2024 portfolio.

Put half your money in the Magnificent Seven stocks of Apple (AAPL), Amazon (AMZN), Meta (META), Microsoft (MSFT), Tesla (TSLA), (NVIDIA), and Salesforce (CRM).

Put your other half into heavy borrowers that benefit from FALLING interest rates, including bonds (TLT), junk bonds (JNK), (HYG), Utilities (XLU), precious metals (GOLD), (WPM), copper (FCX), foreign currencies (FXA), (FXE), (FXY), emerging markets (EEM).

As for me, I never do anything by halves. I’m putting all my money into Tesla. If I want to diversify, I’ll buy NVIDIA. Diversification is only for people who don’t know what is going to happen.

I just thought you’d like to know.

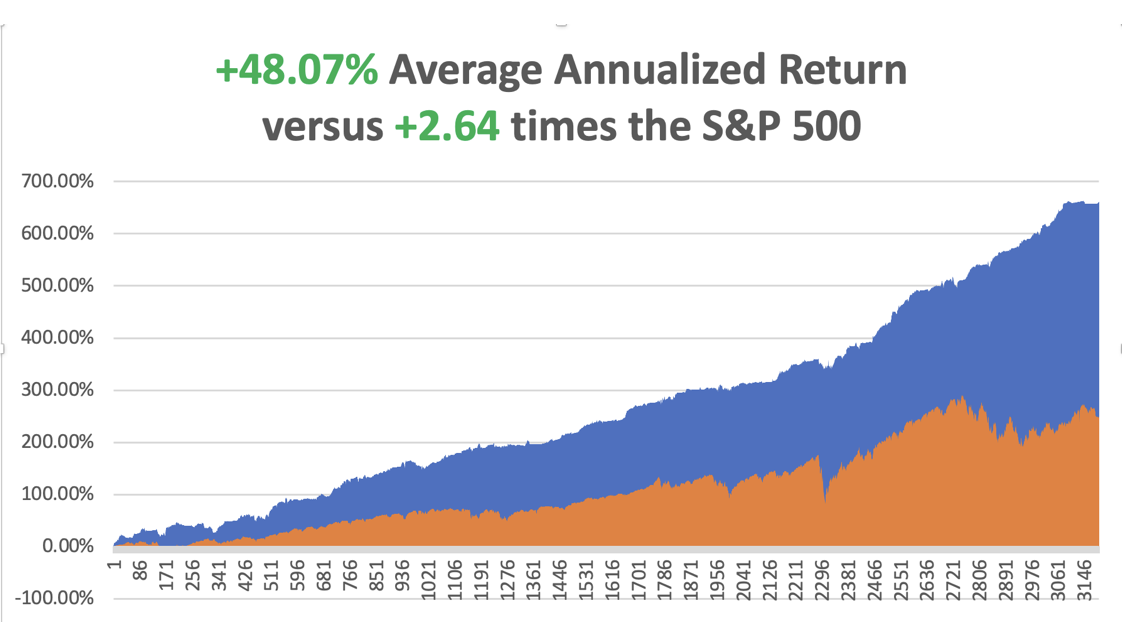

So far in October, we are up +2.96%. My 2023 year-to-date performance is still at an eye-popping +63.76%. The S&P 500 (SPY) is up +12.89% so far in 2023. My trailing one-year return reached +76.46% versus +22.57% for the S&P 500.

That brings my 15-year total return to +660.95%. My average annualized return has fallen back to +48.07%, another new high, some 2.64 times the S&P 500 over the same period.

Some 44 of my 49 trades this year have been profitable.

Chaos Reigns Supreme in Washington, with the firing of the first House speaker in history. Will the next budget agreement take place on November 17, or not until we get a new Congress in January 2025? Markets are discounting the worst-case scenario, with government debt in free fall. Definitely NOT good for stocks, which are reaching for a full 10% correction, half of 2023’s gains.

September Nonfarm Payroll Report Rockets, to 336,000, and August was bumped up another 50,000. The economy remains on fire. The headline Unemployment Rate remains steady at an unbelievable 3.8%. And that’s with the UAW strike sucking workers out of the system. This is supposed to by impossible with 5.5% interest rates. Throw out you economics books for this one!

JOLTS Comes in Hot at 9.61 million job openings in August, 700,000 more than the July report. The record labor shortage continues. Will the Friday Nonfarm Payroll Report deliver the same?

ADP Rises 89,000 in September, down sharply from previous months, showing that private job growth is growing slower than expected. August was revised down. It’s part of the trifecta of jobs data for the new month. The mild recession scenario is back on the table, at least stocks think so.

Weekly Jobless Claims Rise to 207,000, still unspeakably strong for this point in the economic cycle. Continuing claims were unchanged at 1.664%.

Traders Pile on to Strong Dollar, headed for new highs, propelled by rising interest rates. There is a heck of a short setting up for next year.

Yen Soars on suspected Bank of Japan intervention in the foreign exchange markets to defend the 150 line against the US dollar. The currency is down 35% in three years and could be the BUY of the century.

Kaiser Goes on Strike with 75,000 health care workers walking out on the west coast. The issue is money. The company has a long history of labor problems. This seems to be the year of the strike.

Oil (USO)Gets Slammed on Recession Fears, down 5% on the day to $85, in a clear demand destruction move and worsening macroeconomic picture. Europe and China are already in recession. It’s the biggest one-day drop in a year. Is the top in?

Tesla Delivers 435,059 Vehicles in September, down 5% from forecast, but the stock rose anyway. The Cybertruck launch is imminent, where the company has 2 million new orders. Keep buying (TSLA) on Dips. Technology is accelerating.

EVs have Captured an Amazing 8% of the New Car Market. They have been helped by a never-ending price war and generous government subsidies. EV sales are now up a miraculous 48% YOY and are projected to account for a stunning 23% of all California sales in Q3. Tesla is the overwhelming leader with a 52% share in a rapidly growing market, distantly followed by Ford (F) at 7% and Jeep at 5%. However, a slowdown may be at hand, with EV inventories running at 97 days, double that of conventional ICE cars. This could create a rare entry point for what will be the leading industry of this decade, if not the century. Buy more Tesla (TSLA) on bigger dips, if we get them.

Apple Upgrades New iPhone 15 to deal with overheating from third-party gaming. It will shut down some of its background activity, including some of the new AI functions, which were stressing the central processor. Third-party apps were adding to the problem, such as Uber and games from (META). This is really cutting-edge technology.

Moderna (MRNA) Bags a Nobel Prize in Chemistry. Katalin Kariko and Drew Weissman’s work helped pioneer the technology that enabled Moderna and the Pfizer Inc.-BioNTech SE partnership to swiftly develop shots. I got four and they saved my life when I caught Covid. I survived but lost 20 pounds in two weeks. It was worth it.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 9, there is no data of note released.

On Tuesday, October 10 at 8:30 AM EST, the Consumer Inflation Expectations is released.

On Wednesday, October 11 at 2:30 PM, the Producer Price Index is published.

On Thursday, October 12 at 8:30 AM, the Weekly Jobless Claims are announced. The Consumer Price Index is also released.

On Friday, October 13 at 1:00 PM the September University of Michigan Consumer Expectations is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, one of the many benefits of being married to a British Airways senior stewardess is that you get to visit some pretty obscure parts of the world. In the 1970s, that meant going first class for free with an open bar, and occasionally time in the cockpit jump seat.

To extend our 1977 honeymoon, Kyoko agreed to an extra round trip for BA from Hong Kong to Colombo in Sri Lanka. That left me on my own for a week in the former British crown colony of Ceylon.

I rented an antiquated left-hand drive stick shift Vauxhall and drove around the island nation counterclockwise. I only drove during the day in army convoys to avoid terrorist attacks from the Tamil Tigers. The scenery included endless verdant tea fields, pristine beaches, and wild elephants and monkeys.

My eventual destination was the 1,500-year-old Sigiriya Rock Fort in the middle of the island which stood 600 feet above the surrounding jungle. I was nearly at the top when I thought I found a shortcut. I jumped over a wall and suddenly found myself up to my armpits in fresh bat shit.

That cut my visit short, and I headed for a nearby river to wash off. But the smell stayed with me for weeks.

Before Kyoko took off for Hong Kong in her Vickers Viscount, she asked me if she should bring anything back. I heard that McDonald’s had just opened a stand there, so I asked her to bring back two Big Macs.

She dutifully showed up in the hotel restaurant the following week with the telltale paper bag in hand. I gave them to the waiter and asked him to heat them up for lunch. He returned shortly with the burgers on plates surrounded by some elaborate garnish and colorful vegetables. It was a real work of art.

Suddenly, every hand in the restaurant shot up. They all wanted to order the same thing, even though the nearest stand was 2,494 miles away.

We continued our round-the-world honeymoon to a beach vacation in the Seychelles where we just missed a coup d’état, a safari in Kenya, apartheid South Africa, London, San Francisco, and finally back to Tokyo. It was the honeymoon of a lifetime.

Kyoko passed away in 2002 from breast cancer at the age of 50, well before her time.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Sigiriya Rock Fort

Kyoko

Mad Hedge Technology Letter

September 25, 2023

Fiat Lux

Featured Trade:

(JOSTLING FOR THE FUTURE OF TECH)

(AMZN), (ANTHROPIC), (CRM), (MSFT)

Amazon AMZN will invest $4 billion in artificial intelligence company Anthropic.

This is a company competing with ChatGPT.

It’s just another chess move in what could symbolize as the beginning of the war in generative artificial intelligence.

I do believe this could be the last iteration of the internet as humans know it because the next big “upgrade” will be uploaded into the physical human itself.

That is what developments in companies like Neuralink are telling us.

It’s not surprising that many of the big tech firms are taking strategic bets on the future of artificial intelligence.

This trend mirrors the past seminal trends where the end game turns into a winner-takes-all sweepstakes.

I am not going to sit here and say this will be better for the consumer on the internet as a whole, it mostly won’t.

This next iteration of the internet will become cloudier because consumers won’t know who is a chatbot and who isn’t.

The critical takeaway here is that the internet will become less smooth for consumers, but absolutely great for the few technology firms that harness generative artificial intelligence to build revenue.

Even chatbots are on record for not knowing who is a chatbot or who is a human.

What does that mean?

Soon, we will see chatbots talking to chatbots for money.

No humans needed.

In this case, big tech earnings revenue for their chatbot capabilities will explode and the ones that do it best with harvest the most contracts.

That is terrible for certain platforms that rely on authentic human interaction like online dating.

For some subsectors like cybersecurity, computers will be fighting computers and whoever has the best AI software will win out.

Amazon now has real skin in the game and the deal includes Anthropic using its custom chips to build and deploy its AI software.

Amazon also agreed to incorporate Anthropic’s technology into products across its business.

People familiar with the deal said Amazon has committed to an initial $1.25 billion investment in two-year-old Anthropic, a number that could grow to $4 billion over time depending on certain conditions.

This is peanuts for a company as rich as Amazon.

Google invested more than $300 million in Anthropic in May. Salesforce (CRM) has also invested in a series of AI startups, including Anthropic and OpenAI rival Cohere.

Amazon, which runs the largest cloud-computing business, has been shifting its strategy somewhat in backing AI startups.

Large language models, the algorithms that power chatbots such as ChatGPT require huge amounts of capital to build and train, and startups spend that money largely on cloud-computing costs. Of the billions of dollars that OpenAI has raised from Microsoft (MSFT), much of it has been spent on the tech giant’s AI business Azure.

Despite the excitement and investment in AI, it still makes up only a fraction of the revenue flowing into cloud-computing businesses.

All this is right now is positioning as the real revenue payout is much later down the road and I am talking years.

Whoever acquires the best pieces of the AI infrastructure now and sets the rules of the road, will basically box out everyone else.

Amazon has now clearly thrown their hat in the ring.

Trade AMZN in the short-term and hold for the long-term.

Global Market Comments

September 25, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE SINGULARITY IS HERE!)

(SPY), (TLT), (MSFT), (TSLA), (USO), (AMZN)

While changing planes at Heathrow airport in London last week, my partners in artificial intelligence graciously came out to join me for lunch over some of the awful food there. I can’t tell you who they are, but if I did you would fall out of your chair.

Whenever someone gets a lead in AI applications these days, mum’s the word. There’s no point in giving the competition a leg up, let alone a commanding lead. What they told me was incredibly exciting, but also terrifying. Suffice it to say that you ain’t seen nothing yet.

2023 is probably the last year when mere humans will be able to identify what’s real and what isn’t. The Turing Test, by which machines become indistinguishable from man, laid out by Dr. Alan Turing in 1950, has been conquered. Dr. Ray Kurzweil got it all wrong. We are not going to have to wait until 2040 for the Singularity to take place, whereby man and machine become one (click here for the link).

It’s happening right now.

It seems that these days. you spend half of your day proving to robots that you’re not a robot. Let me tell you that it’s about to get a lot worse. Lately, I have been irritatingly failing these tests more often because I can’t see the part of a bicycle hiding in a corner of the box next door. It won’t be long before we are working for these robots.

That could be a good thing because robots lack human flaws, like abusing their employees, getting drunk, failing to show up for work, and demanding more pay. What they WILL do is make you work FASTER, as the employees at Amazon (AMZN) found out, where workplace accidents and exhaustion at distribution centers are running rampant. Some workers can only handle six weeks of employment at a time.

It turns out that Elon Musk was the initial founding investor in ChatGBT, pumping in $1 billion in seed capital. When you’re the richest man in the world, you can do that sort of thing.

But Musk had a great falling out in 2021 when management refused to accept his absolute control of their AI in exchange for more money. That led to ChatGPT’s sale to Microsoft (MSFT) for $13 billion, a figure which, in retrospect, seems a pittance given the $1 trillion in value it is expected to create (so buy (MSFT).

By the way, ChatGPT refers to Generalized Preprogrammed Transformers in a homage to the cartoon series. That’s how nerdy these people are.

In any case, a huge conflict of interest had arisen with Tesla’s own AI efforts. One proof of this is that my own monthly insurance rates with Tesla keep going down, now at an unbelievably low $204 a month for a $165,000 vehicle.

It’s not that I’m a better driver. At my age, I’m probably getting worse. It's because the CAR keeps getting smarter, reducing the chance of an accident and therefore the risk to Tesla’s insurance division. By the way, notice how well Tesla shares have been outperforming the market lately.

Insurance industry watch out! You are about to get disrupted.

What is especially scary is that a presidential election will take place next year just when AI is hitting its stride. In 2016, many thought that the Access Hollywood videotape would make Donald Trump unelectable.

Everyone believed the video was real, but while half the voters were outraged, the other half said that’s just Trump being Trump and he got elected. If that video were released today, only half would believe it’s real while the other half would think it’s a deep fake produced by the opposition.

The possibilities boggle the mind, with multiple deep fakes already gaining airtime for next year’s primaries.

There isn’t much to say about stocks these days except that the grand finale for the current correction is fast approaching.

The UAW strike won’t cause the stock market to crash. But add it in with a prolonged government shutdown, sharply rising interest rates, and recessions in our biggest export markets in Europe and China, and suddenly the short-term downside argument becomes a lot more persuasive.

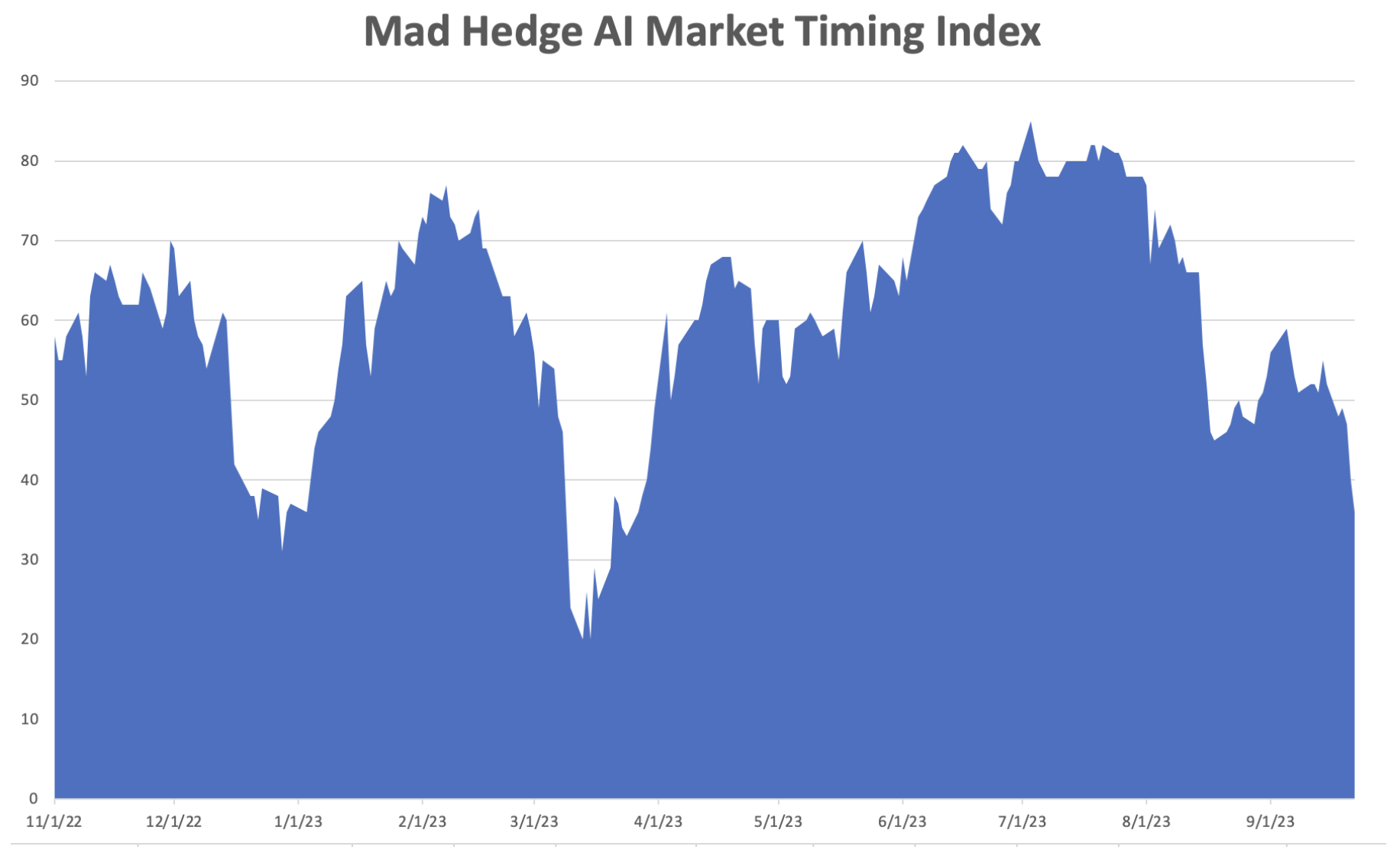

If you DO need convincing, look no further than my Mad Hedge AI Market Timing Index. It decisively broke 50 on Friday and plunged all the way down to 36. Finally, after a tortuous six months of doing nothing, we are starting to see some value in the market.

Whenever I go through periods of issuing no trade alerts for a prolonged period because the risk/reward is terrible, I get a lot of complaints from customers. After all, who wouldn’t want more trade alerts with a 90% success rate? The only way you achieve that success rate is to stay out of markets when they suck, as in now. Lately, I have noticed on down days, I get absolutely no complaints AT ALL.

I will end this dissertation by telling you a funny story. The last time I landed at San Francisco Airport, I grabbed an Uber cab home. As we departed the airport, I noticed a rolled set of plans on the floor forgotten by the previous passenger. I pointed this out to the driver, but he was from China and didn’t speak English.

So I opened up the plans and called the phone numbers listed in the key. First, I tried the University of California at San Francisco, whose name was clearly marked at the top. No luck there. The university is just too big.

Then I tried the printing company in Berkeley that produced the plans. I asked for the customer’s cell phone number, but the printer said they never released confidential client information. After some prodding, I convinced him to call his own customer and tell him I was headed back to the gate where he debarked with the plans (I can be very convincing).

By now, I was 20 minutes away from the airport, so I had ample time to examine what I had chanced on. It turns out I had blueprints of the human brain showing 100 sites where it can be connected directly to the Internet, ranking them by transmission efficiency. The owner was headed to Los Angeles to make a presentation to fellow scientists and some venture capital investors.

Yikes, I thought!

When we pulled up to the gate, there was a man looking like he had come out of central casting for the role of “scientist”, beard, glasses, and all. He was very grateful and then disappeared into the crowd running for his plane. Yes, I know it sounds like the beginning of a science fiction thriller.

I just thought you’d like to know. Yes, it’s just another day in the life for me.

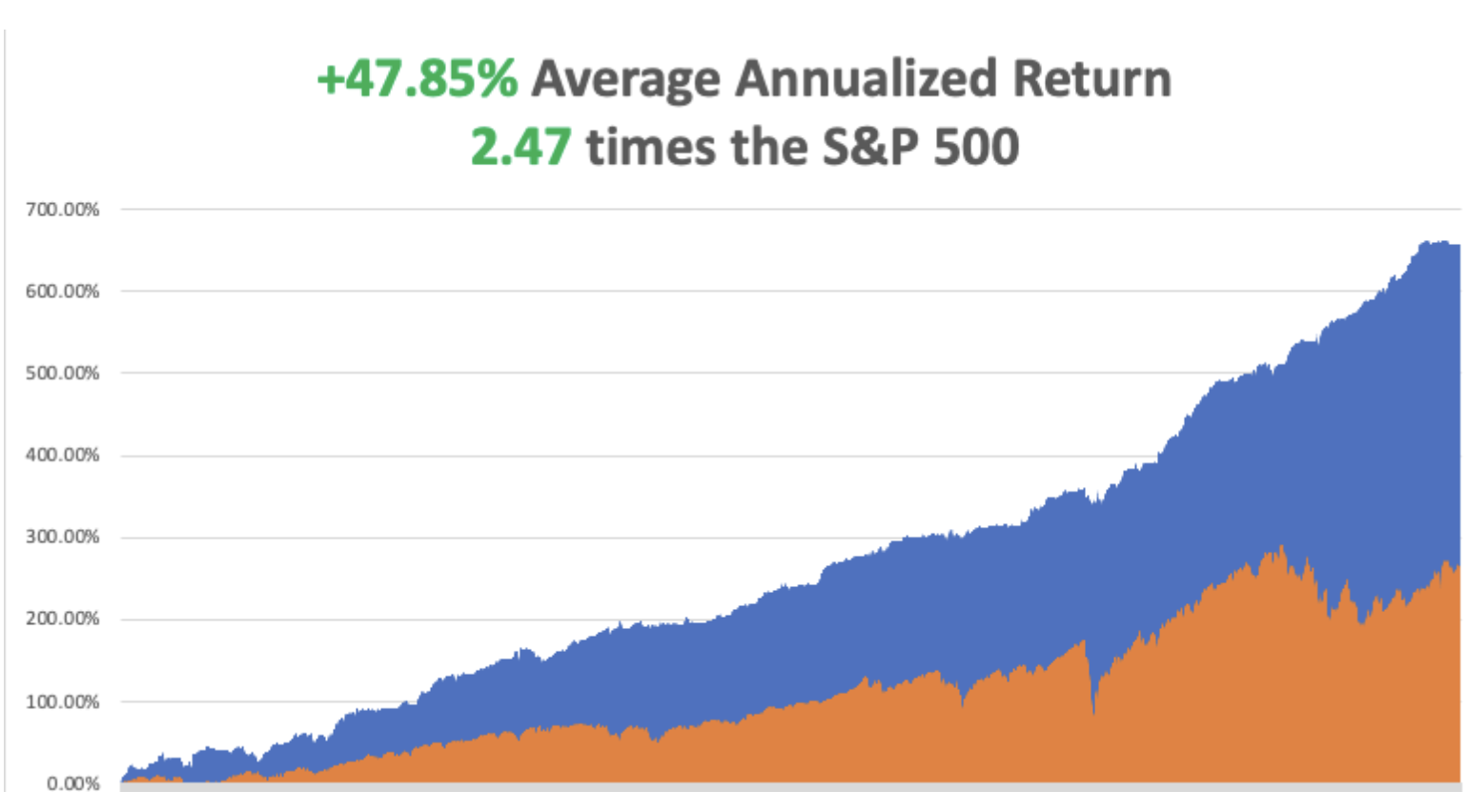

So far in August, we are down -4.70%. My 2023 year-to-date performance is still at an eye-popping +60.80%. The S&P 500 (SPY) is up +17.10% so far in 2023. My trailing one-year return reached +92.45% versus +8.45% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%, some 2.50 times the S&P 500 over the same period.

Some 41 of my 46 trades this year have been profitable.

The Most Important Thing That Powell Didn’t Say in Fed press conference is that quantitative tightening, or QT, continues. That drains $1 trillion a year from the financial system through bond sales until 2031 to get the Fed balance sheet down to zero. It is a negative for bonds….and the economy. The market is fixated on the 0.25% he did raise on interest rates.

UAW Strike Expanded on Friday, adding 38 new plants to the work stoppage. It’s death by a thousand cuts. The Big Three may respond with lockouts to drain union funds. Factories in Mexico are looking better every day. Elon Musk is laughing.

Industrial Production Jumps 0.4% in August, in another sign that the US has dodged the recession bullet. It’s one of the strongest numbers of the year. Capacity Utilization also rose to a high 79.7%.

Will a Government Shutdown Finally Drive Stocks Downward? Chaos rules supreme in the House of Representatives where there is a major effort to shut down the US government. Speaker Kevin McCarthy risks getting fired if he allows a spending bill to go through with Democratic support. It’s the result of a devil’s bargain made with his right wing to land the job in January. Will an impeachment inquiry into Biden be enough to placate them?

Cathie Woods’ New Take on Tesla (TSLA). As one of the earliest investors in Tesla, along with myself, it pays to listen to Cathie Woods talk about the stock. The company is headed from a current market valuation of $845 billion to $5 trillion, with two-thirds of the growth coming from its autonomous driving technology, a $15,000 upgrade. AI sold as software-as-a-service has an 80% profit margin compared to only 20%-30% for the EV business. Cathie’s bull case is $2,000 in five to ten years and her bear case is that the stock only reached $1,400. Teslas have a 40% lower accident rate than ICE cars, thanks to AI, so take the human out of the driving formula.

Oil (USO) Hits New 2023 High, with gasoline topping $5.00 a gallon in many states. There is no oil shortage or supply disruptions. This is pure price gouging, with Saudi Arabia and Russia cutting supplies by 5 million barrels/day since June and American oil companies riding on their coattails. The move coincided with a sudden and unexpected improvement in the US economic outlook, increasing demand. Too late to play on the long side here, with prices up 40% from the May lows.

National Debt (TLT) Tops $33 Trillion, or $100,000 per man, woman, and child. Not great news for bonds, as new issuance is swamping the markets. The debt has risen by 50% since 2019. Republicans want Democrats to spend less, while Democrats want Republicans to cut their spending.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 25, the Chicago Fed National Activity Index is out.

On Tuesday, September 26 at 3:00 PM EST, the S&P Case Shiller National Home Price Index is released. We also get New Home Sales.

On Wednesday, September 27 at 2:30 PM, the US Durable Goods is published.

On Thursday, September 28 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the final print for Q2 GDP.

On Friday, September 29 at 2:30 PM, the Personal Income & Spending is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, this is not my first Russian invasion.

Early in the morning of August 20, 1968, I was dead asleep at my budget hotel off of Prague’s Wenceslas Square when I was suddenly awoken by a burst of machine gun fire. I looked out the window and found the square filled with T-54 Russian tanks, trucks, and troops.

The Soviet Union was not happy with the liberal, pro-western leaning of the Alexander Dubcek government so they invaded Czechoslovakia with 500,000 troops and overthrew the government.

I ran downstairs and joined a protest demonstration that was rapidly forming in front of Radio Prague trying to prevent the Russians from seizing the national broadcast radio station. At one point, I was interviewed by a reporter from the BBC carrying this hulking great tape recorder over his shoulder, as I was the only one who spoke English.

It seemed wise to hightail it out of the country, post haste, as it was just a matter of time before I would be arrested. The US ambassador to Czechoslovakia, Shirley Temple Black (yes, THE Shirley Temple), organized a train to get all of the Americans out of the country.

I heard about it too late and missed the train.

All borders with the west were closed and domestic trains shut down, so the only way to get out of the country was to hitchhike to Hungary where the border was still open.

This proved amazingly easy as I placed a small American flag on my backpack. I was in Bratislava just across the Danube from Austria in no time. I figured worst case, I could always swim it, as I had earned both, the Boy Scout Swimming, and Lifesaving merit badges.

Then I was picked up by a guy driving a 1949 Plymouth who loved Americans because he had a brother living in New York City. He insisted on taking me out to dinner. As we dined, he introduced me to an old Czech custom, drinking an entire bottle of vodka before an important event, like crossing an international border.

Being 16 years old, I was not used to this amount of high-octane 40-proof rocket fuel and I was shortly drunk out of my mind. After that, my memory is somewhat hazy.

My driver, also wildly drunk, raced up to the border and screeched to a halt. I staggered through Czech passport control which duly stamped my passport. I then lurched another 50 yards to Hungary, which amazingly, let me in. Apparently, there is no restriction on entering the country drunk out of your mind. Such is Eastern Europe.

I walked another 100 yards into Hungary and started to feel woozy. So, I stumbled into a wheat field and passed out.

Sometime in the middle of the night, I felt someone kicking me. Two Hungarian border guards had discovered me. They demanded my documents. I said I had no idea what they were talking about. Finally, after their third demand, they loaded their machine guns, pointed them at my forehead, and demanded my documents for the third time.

I said, “Oh, you want my documents!”

I produced my passport, and when they got to the page that showed my age, they both started laughing.

They picked me and my backpack up and dragged me back to the road. While crossing some railroad tracks, they dropped me, and my knee hit a rail. But since I was numb, I didn’t feel a thing.

When we got to the road, I saw an endless stream of Russian army trucks pouring into Czechoslovakia. They flagged down one of them. I was grabbed by two Russian soldiers and hauled into the truck with my pack thrown on top of me. The truck made a U-turn and drove back into Hungary.

I contemplated my surroundings. There were 16 Russian Army soldiers in full battle dress holding AK-47s between their legs and two German Shepherds all looking at me quizzically. Then I suddenly felt the urge to throw up. As I assessed that this was a life-and-death situation, I made every effort to restrain myself.

We drove five miles into the country and stopped at a small church. They carried me out of the truck and dumped me and my pack behind the building. Then they drove off.

The next morning, I woke up with the worst headache of my life. My knee bled throughout the night and hurt like hell. I still have the scar. Even so, in my enfeebled condition, I realized that I just had one close call.

I hitchhiked on to Budapest, then to Romania, where I heard that the beaches were filled with beautiful women. My Italian let me get by passably in the local language.

It all turned out to be true.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

September 20, 2023

Fiat Lux

Featured Trade:

(THE BOND KING IS WRONG ABOUT TECH STOCKS)

($COMPQ), (UUP), (MSFT)