Mad Hedge Technology Letter

January 24, 2022

Fiat Lux

Featured Trade:

(BEST OF THE REST GETS SLAUGHTERED)

(MSFT), (SNAP), (GOOGL), (AAPL), (AMZN), (FB), (TIKTOK)

Mad Hedge Technology Letter

January 24, 2022

Fiat Lux

Featured Trade:

(BEST OF THE REST GETS SLAUGHTERED)

(MSFT), (SNAP), (GOOGL), (AAPL), (AMZN), (FB), (TIKTOK)

Popular nostrum has it that earnings will save the stock market.

The strength of corporate America time and time again is on display to show investors how high short-term growth follows through.

Anytime the Nasdaq enters a little rut, earnings bail us out and the next move is usually higher for tech shares.

Well, wait a second, things are different this time.

The bad news now is that confirmation of solid fundamentals during the upcoming earnings season, won’t make the Nasdaq index go higher.

The market is pricing in business as usually for the largest 5 tech stocks which are really the only ones that matter.

Internally, the rest of tech has been deeply damaged by this January sell-off and we are talking about 8-9% one-day sell-offs for the small cap tech growth and I haven’t even mentioned the peak to trough underperformance which is much worse.

Larger cap Enterprise and Cyber Security stocks still boast solid foundations and are going down less than the meme stocks, shelter-at-home stocks, and the best of the rest tech stocks.

Basically, we need to get through earnings because there is minimal upside for tech stocks as investors peruse through a lack of short-term catalysts.

We are stuck in a ditch where monetary and fiscal policy has been set dead straight against an environment of potentially appreciating tech stocks.

Until that changes, I don’t envision a snappy reversal apart from a dead cat bounce to sell into.

Chasing growth in a low-interest rate environment gave us an overshoot to the upside and now that is all working in reverse.

And for the big FANG stocks outperforming small cap, it just means shares are performing better than tech growth because they command lower volatility due to stronger balance sheets.

Resilience to indiscriminate selling is currency in today’s trading world.

Nothing wrong with growth, but they are what they are, so much so that if you cannot generate profitability now, sell-offs are indicative of their poor strategic position among bigger tech.

The carnage under the hood is stark today with Snap stock cratering after the social media company’s shares were downgraded amid risks to revenue growth and tough competition from rival TikTok.

Snap’s headwinds result from a weakening business profile stemming from IDFA headwinds, difficult [year-over-year comparisons] from stellar growth in 2020-21, and increasing competition from TikTok.

IDFA is a serious thorn in the side for the android-based systems of Google as well as for Facebook.

IDFA is Apple minimizing the reach of data harvesting platforms by turning off their data reach and these modifications by Apple (AAPL) to rules for advertising on mobile apps have forced companies like Snap to lower guidance.

When it reported quarterly earnings last October, Snap revealed that the impact on its advertising business could be long lasting and now we are experiencing that.

The IDFA issues could cut growth rates by half as these social media firms have been unable to remedy its loss of reach in digital advertising.

Snap has the unenviable position to not only be behind Google and Facebook, but they are also the next company to be upended by TikTok that has really come on the last few years.

TikTok has supplanted Snap as the go-to social media platform for teens and young adults.

In a rising interest rate environment, the best of the rest like Snap gets punished for not being the best of class.

Snap shares are down over 200% from its peak and threatening to close in on 300% in the red.

Snap represents the fortunes for the marginal tech stocks that rely on growth and that is not working in 2022.

Although not as loss-making as other tech growth, SNAP has been fairly pigeonholed as the tech you don’t want to own now.

It’s a dangerous position to fill in times of the VIX spiking to 30.

The problems don’t stop there with TikTok really threatening Snap’s position and the momentum signaling that Snap is prepared for a deeper slowdown than initially expected.

Snap’s foothold is strongest in the 13-34-year-old range in the U.S., Canada, the U.K., France, Australia, and the Netherlands, but TikTok’s audience is the most similar to Snap’s which means it puts both Snap’s user face time spent and ad dollars at risk.

From a monetary standpoint, digital advertisers will start to play off ad competition between TikTok and Snap, resulting in discounted ad revenue per unit which will narrow margins moving forward.

Not being able to command the prior ad premium is a stinging blow to Snap who thought they were in the driving seat to the third position behind Google and Facebook, but it shows that being a tech minnow is a harrowing experience and fending off toxicity is part of the playbook just to survive.

Head to higher waters in this volatile environment.

Global Market Comments

January 24, 2022

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or PARACHUTING WITHOUT A PARACHUTE),

(AAPL), (SPY), (MSFT), (TLT), (TBT), (TDOC), (NFLX), (DIS), (VALE), (FCX), (USO), (JPM), (WFC), (BAC), (TSLA), (AMZN), (NVDA)

It has been the worst New Year stock market opening in history.

After a two-day fake-out to the upside, stocks rolled over like the Bismarck and never looked up. NASDAQ did its best interpretation of flunking parachute school without a parachute, posting the worst month since 2008.

Markets can’t hold on to any rally longer than nanoseconds, and the last hour of the day has turned into one from hell.

What is even more confusing is that stocks are now trading like commodities, with massive one-way moves, while commodities, like oil (USO), copper( FCX), and iron ore (VALE) have resumed a steady grind up.

We had a lovefest going on here at Incline Village, Nevada for Technology and Bitcoin researcher Arthur Henry has been staying with me for the week to plot market strategy.

Once the market showed its hand, I sold short Microsoft (MSFT), which elicited torrents of complaints from readers. Then Arthur sold short Netflix (NFLX), inviting refund demands. Then I sold short Apple (AAPL), prompting accusations of high treason. Then Arthur sold short Teledoc (TDOC). There wasn’t a lot of talking, but frenetic writing and emailing instead.

Followers cried all the way to the bank.

In a mere two weeks, the price earnings multiple for the S&P 500 plunged from 22X to 20X. A lot of traders were only buying stock because they were going up. Take out the “up” and Houston we have a problem.

The entire streaming industry seems to have gone up in smoke and ex-growth practically overnight. Netflix (NFLX) delivered a gob smacking 29.5% swan dive in the wake of disappointing subscriber growth forecasts. Walt Disney (DIS), which ate the Netflix lunch, was dragged down 10% through guilt by association.

It is often said that the stock market has discounted 12 of the last six recessions. It is currently pricing in one of those non-recessions. What we are seeing is a sudden growth scare of the first order.

Despite last week’s carnage, stocks are still the most attractive asset class in the world, offering a potential 10% return in 2022. The problem is that they may make that 10% profit starting from 10% lower than here.

Despite all the red ink, big tech stocks are still on track to see a 30% earnings growth this year, and they account for a hefty 28% of the market.

Let’s look at Apple’s past declines for guidance on this meltdown.

Steve Jobs’ creation gave back 60% in the 2008 Great Recession, 34% during the 2015 growth scare, 48% during the great 2018 Christmas collapse, and 28% in the 2020 pandemic crash. So, the good news is that you won’t get killed by this selloff, you’ll just lose an arm and a leg. But they’ll grow back.

Remember, it’s always darkest just before it goes completely black. This correction is survivable, although it may not seem so at the moment.

It does vindicate my 2022 view that the first half will be about survival and that big money can be had in the second half.

So far, so good.

The Market is De-Grossing Big Time. That means cutting total market exposure and selling everything, regardless of stock or sector. The market is discounting a recession and bear market that isn’t going to happen, which occurs often. When it ends in a few weeks, interest rate sensitives, especially the banks, will bounce back hard, but tech won’t. Buy (JPM), (WFC), and (BAC) on bigger dips.

The Bond Collapse Goes Global, with German 10-year bunds going positive for the first time in three years, up 40 basis points in a month. Yes, inflation is finally hitting the Fatherland, home of post-WWI billion percent inflation. Eurozone inflation just topped 5%, well above its 2% target. British inflation hit a 30-year high. The move has lit a fire under all Euro currencies. Methinks the down move in (TLT) has more to go.

Fed to Raise Rates Eight Times, says Marathon Asset Management. That’s what will be needed to curb the current runaway inflation now at 7.0% and still rising. Personally, I think it will be 12 quarter-point increments to peak out at a 3 ¼% overnight rate. Any more and Powell might bring on a recession.

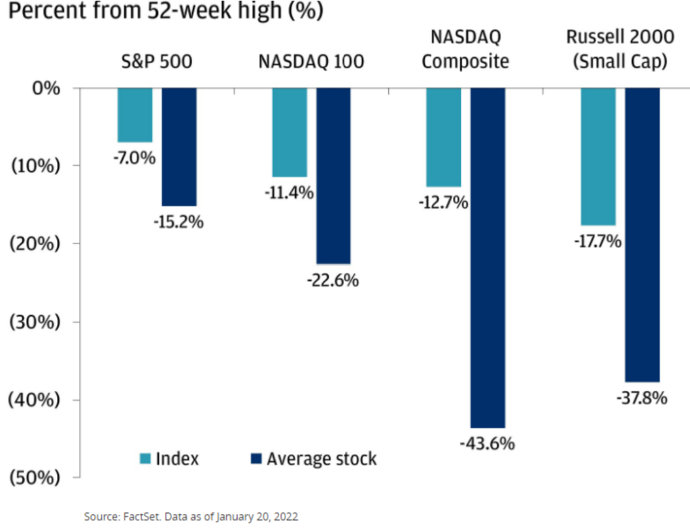

NASDAQ is Officially in Correction, down 10%, in the wake of poor performance this month. It’s the fourth one since the pandemic began two years ago. Tesla (TSLA), Amazon (AMZN), and NVIDIA (NVDA) have been leading the swan dive, all felled by rapidly rising interest rates. This could go on for months.

Weekly Jobless Claims Hit 286,000, a four-month high, as omicron sends workers fleeing home.

Goldman Sachs (GS) Gets Crushed, down 8%, on disappointing earnings. Tough market conditions are fading trading volumes while 2021 bonuses were through the roof. The move is particularly harsh in that buyers were flooding in right at support at the 200-day moving average.

China GDP (FXI) Grows 8.1% YOY but is rapidly slowing now, thanks to Omicron. China was first in and first out with the pandemic but is getting hit much harder in this round. That has prompted new mass lockdowns which will make out own supply chain problems worse for longer. In Chinese, “lockdown” means they weld your door shut, unlike here. Harsh, but it works.

Oil (USO) Hits Seven-Year High, as inventories hit a 21-year low. No new capital is entering the industry, crimping supplies as old fields play out. The threat of a Russian invasion of the Ukraine is prompting advance stockpiling. Russia is the world’s second-largest oil exporter.

Existing Homes Sales Hit a 15-Year High, at 6.12 million, the best since 2006. December fell 4.6%. Extreme inventory shortage is the issue, with only 910,000 homes for sale at the end of the year, an incredibly low 1.8-month supply. You can’t find anything on the market now, to buy or rent. The median price of a home sold in December was $358,000, a 15.8% gain YOY.

Bitcoin (BITO) Crashes, decisively breaking key support at $40,000. Non-yielding assets of every description are getting wiped. Bail on all crypto options plays asap.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my January month-to-date performance bounced back hard to 5.05%. My 2022 year-to-date performance also ended at 5.05%. The Dow Average is down -6.12% so far in 2022.

Once stocks went into free fall, I piled on the short positions as fast as I could write the trade alerts, including in Microsoft (MSFT), Apple (AAPL), and a double short in the S&P 500 (SPY). I also increased my shorts in the bond market (TLT) to a triple position. When prices became the most extreme, when the Volatility Index (VIX) hit $30, I bought both (SPY) and (TLT).

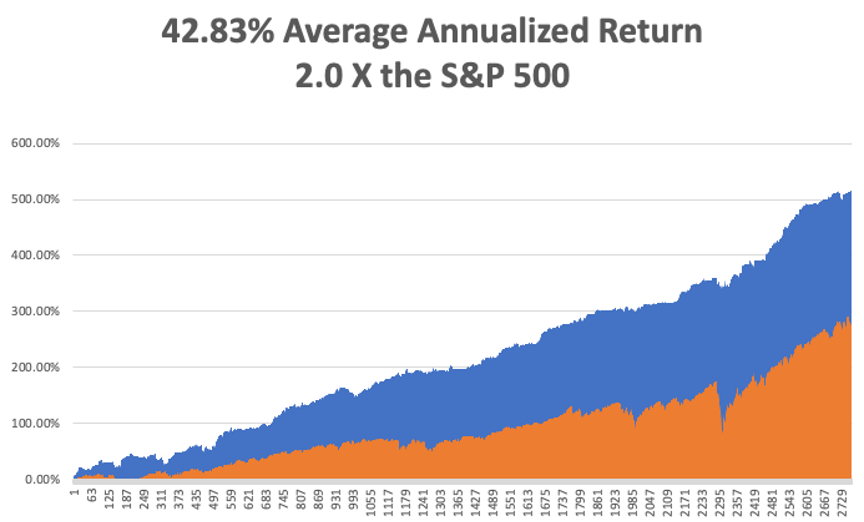

If everything goes our way, we should be up 14.26% by the February 18 options expiration.

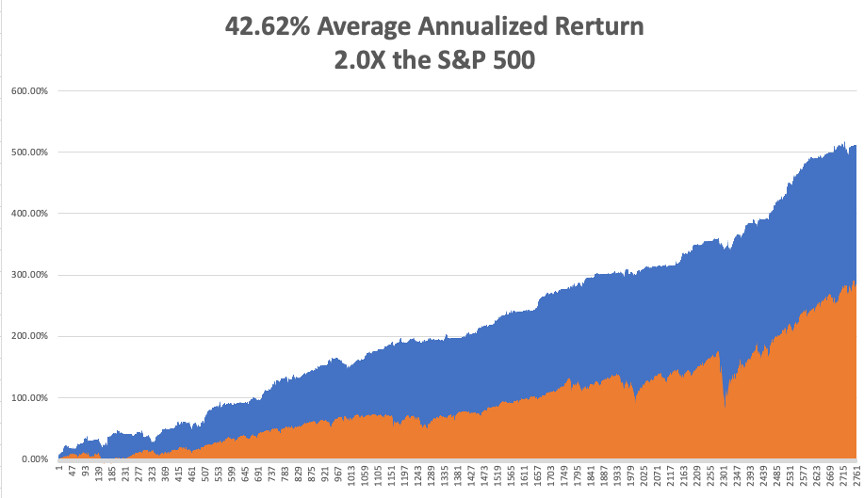

That brings my 12-year total return to 517.61%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 42.82% easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 71 million and rising quickly and deaths topping 866,000, which you can find here.

On Monday, January 24 at 6:45 AM, The Market Composite Flash PMI for January is out. Haliburton (HAL) reports.

On Tuesday, January 25 at 6:00 AM, the S&P Case Shiller National Home Price Index for November is released. American Express (AXP) reports.

On Wednesday, January 26 at 7:00 AM, the New Home Sales for December are published. At 11:00 AM The Federal Reserve interest rate decision is announced. Tesla (TSLA), Boeing (BA), and Freeport McMoRan (FCX) report.

On Thursday, January 27 at 8:30 AM the Weekly Jobless Claims are disclosed. We also get the first look at US Q4 GDP. Alaska Air (ALK) and US Steel (X) report.

On Friday, January 28 at 5:30 AM EST US Personal Income & Spending is printed. Caterpillar (CAT) reports. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, when I drove up to visit my pharmacist in Incline Village, Nevada, I warned him in advance that I had a question he never heard before: How good is 80-year-old morphine?

He stood back and eyed me suspiciously. Then I explained in detail.

Two years ago, I led an expedition to the South Pacific Solomon Island of Guadalcanal for the US Marine Corps Historical Division (click here for the link). My mission was to recover physical remains and dog tags from the missing-in-action there from the epic 1942 battle.

Between 1942 and 1944, nearly four hundred Marines vanished in the jungles, seas, and skies of Guadalcanal. They were the victims of enemy ambushes and friendly fire, hard fighting, malaria, dysentery, and poor planning.

They were buried in field graves, in cemeteries as unknowns, if not at all left out in the open where they fell. They were classified as “missing,” as “not recovered,” as “presumed dead.”

I managed to accomplish this by hiring an army of kids who knew where the most productive battlefields were, offering a reward of $10 a dog tag, a king's ransom in one of the poorest countries in the world. I recovered about 30 rusted, barely legible oval steel tags.

They also brought me unexploded Japanese hand grenades (please don’t drop), live mortar shells, lots of US 50 caliber and Japanese 7.7 mm Arisaka ammo, and the odd human jawbone, nationality undetermined.

I also chased down a lot of rumors.

There was said to be a fully intact Japanese zero fighter in flying condition hidden in a container at the port for sale to the highest bidder. No luck there.

There was also a just discovered intact B-17 Flying Fortress bomber that crash-landed on a mountain peak with a crew of 11. But that required a four-hour mosquito-infested jungle climb and I figured it wasn’t worth the malaria.

Then, one kid said he knows the location of a Japanese hospital. He led me down a steep, crumbling coral ravine, up a canyon and into a dark cave. And there it was, a Japanese field hospital untouched since the day it was abandoned in 1943.

The skeletons of Japanese soldiers in decayed but full uniform laid in cots where they died. There was a pile of skeletons in the back of the cave. Rusted bottles of Japanese drugs were strewn about, and yellowed glass sachets of morphine were scattered everywhere. I slowly backed out, fearing a cave-in.

It was creepy.

I sent my finds to the Marine Corps at Quantico, Virginia, who traced and returned them to the families. Often the survivors were the children or even grandchildren of the MIAs. What came back were stories of pain and loss that had finally reached closure after eight decades.

Wandering about the island, I often ran into Japanese groups with the same goals as mine. My Japanese is still fluent enough to carry on a decent friendly conversation with the grandchildren of their veterans. It turned out I knew far more about their loved ones than they. After all, it was our side that wrote the history. They were very grateful.

How many MIAs were they looking for? 30,000! Every year, they found hundreds of skeletons, cremated in a ceremony, one of which I was invited to. The ashes were returned to giant bronze urns at Yasakuni Ginja in Tokyo, the final resting place of hundreds of thousands of their own.

My pharmacist friend thought the morphine I discovered had lost half of its potency. Would he take it himself? No way!

As for me, I was a lucky one. My dad made it back from Guadalcanal, although the malaria and post-traumatic stress bothered him for years. And you never wanted to get in a fight with him….ever.

I can work here and make money in the stock market all day long. But my efforts on Guadalcanal were infinitely more rewarding. I’ll be going back as soon as the pandemic ends, now that I know where to look.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

True MIAs, the Ultimate Sacrifice

My Collection of Dog Tags and Morphine

My Army of Scavengers

Dad on Guadalcanal (lower right)

Mad Hedge Technology Letter

January 21, 2022

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO LAP UP AT THE BOTTOM)

(MSFT), (TSLA), (GOOGL), (AAPL), (AMZN)

Tech has led the way to the downside as the macro picture sours in the short term.

Valuations have come down from the nosebleed levels and now is the time to pick and choose where to allocate capital for the next leg up in tech.

Avoiding growth tech is something that should be stapled to your bedpost, loss-making companies won’t be able to compete with more established revenue models.

You don’t want to catch a falling knife, but at the same time, diligently prepare yourself to buy the best discounts of the year.

Here are the names of five of the best stocks to slip into your portfolio in no particular order when we find a bottom.

Remember, tech ALWAYS comes back.

Apple

Steve Job’s creation is weathering the gale-force storm quite well. Apple has been on a tear reconfirming its smooth pivot to a software service tilted tech company. The timing is perfect as China has enhanced its smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality.

That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has their supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and will gobble up a total of $200 billion in shares by the end of 2021. Get into this stock while you can, as entry points are few and far between.

Oh, and their 5G phone is selling like hotcakes. Some one billion need to be replaced to bring consumers into the new high speed 5G world.

Amazon (AMZN)

This is the best company in America, hands down, and commands 5% of total American retail sales or 49% of American e-commerce sales. The pandemic has vastly accelerated the growth of their business.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then, oozing innovation, and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart doorbell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft (MSFT)

The optics in 2021 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter -- and that is a good thing.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies, especially retailers.

Microsoft is also on the vanguard of the gaming industry and deals like the $86 billion purchase of Activision (ATVI) mean that it will be difficult for another company to loosen MSFTs stranglehold at the top of the gaming ladder.

Alphabet (GOOGL)

Alphabet and Facebook boast a strong duopoly of ad technology. Alphabet generated 80% of its revenue from Google's advertising services in 2020. Google's non-advertising businesses (including subscriptions and hardware) accounted for 12%, while another 7% came from Google Cloud.

Alphabet's total revenue rose 13% in 2020, even as the pandemic throttled the growth of Google's advertising business in the first half of the year. The growth of Google Cloud throughout the year also cushioned that blow.

Google's advertising business recovered in the second half of the year, and Alphabet's operating margin expanded from 21% in 2019 to 23% in 2020. Its diluted earnings per share (EPS) also grew 19%.

In the first nine months of 2021, Alphabet's revenue rose 45% year over year as Google's advertising and cloud business grew in tandem.

Its array of different businesses like LinkedIn, YouTube, and Google Maps means this revenue pipeline is as fertile as can be.

Google’s robust balance sheet will protect itself from any downtrend in business that they might ever suffer.

Tesla (TSLA)

The influential EV leader has really surged ahead of the competition during the pandemic.

Demand for its product is off the charts as they delivered 184,800 Model 3 and Model Y cars in the first quarter, beating expectations and setting a record for Tesla.

However, the company also said it produced none of its higher-end Model S sedans or Model X SUVs for the period ending March. It delivered 2,020 older Model S sedans and Model X SUVs from inventory.

Supply chain issues are likely to remain a challenge for Tesla this year as many EV makers are having a hard time sourcing semiconductor chips.

Tesla is now aiming to produce 2,000 Model S and X vehicles per week later this year.

The company said Monday it expects more than 50% vehicle delivery growth in 2021 overall, which implies minimum deliveries of around 750,000 vehicles this year.

This stock is a must-buy when tech reverses.

Mad Hedge Technology Letter

January 19, 2022

Fiat Lux

Featured Trade:

(MICROSOFT TAKES A GIANT LEAP FORWARD)

(MSFT), (ATVI), (PINS), (GOOGL), (AAPL), (AMZN)

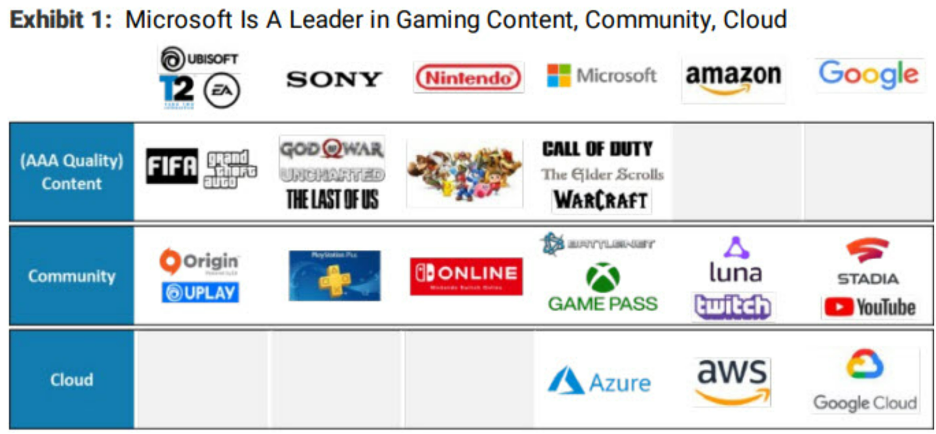

CEO of Microsoft (MSFT), Satya Nadella, and his management team have made an aggressive step towards making inroads to the metaverse.

Gaming will be the launching pad to the metaverse that will first start as digital communities and later evolve into interoperable and integrated digital worlds.

The rest of the metaverse will germinate via these gaming communities and Microsoft knows that which is why they purchased Activision (ATVI) in cash for $68 billion and change.

The price was 3X higher than what they paid for LinkedIn but equally as strategic as many tech behemoths look forward to the next “big thing.”

The deal will mean MSFT will be one of the biggest gaming companies in the world just nudging out China’s Tencent and Japan’s Sony.

In the U.S., they will be by far the biggest gaming company and Nadella has made it a point of emphasis to navigate the gaming world by tapping M&A.

Remember, it was Nadella who built the MSFT cloud from scratch and Microsoft possessing its own stand-alone cloud asset dovetails nicely with their deep dive into gaming.

There are intrinsic synergies resulting from owning both.

The lack of native cloud infrastructure was a critical reason why ATVI gave up, as Chief Executive Officer Bobby Kotick said in an interview, “You look at companies like Facebook and Google and Amazon and Apple, and especially companies like Tencent — they're enormous and we realized that we needed a partner in order to be able to realize the dreams and aspirations we have,” he said.

This was the best Kotick could have wished for and I’ve mentioned this overarching trend of the best Silicon Valley companies getting stronger and now it’s even more pronounced as we are on the verge of exiting this pandemic this year.

In a higher interest rate environment, cash hoarders like Microsoft, Apple (AAPL), and Amazon (AMZN) simply have more ammunition than these smaller outfits who get penalized because of a harder route to access cheap capital making future cash flows costlier.

Now many of these smaller companies are realizing that they need to stand on their own two feet and that’s a scary thought for many CEOs who have been accustomed to tapping the capital markets to paper over the cracks.

What’s good about ATVI?

Activision owns mobile-gaming studio King, maker of Candy Crush, one of the most popular mobile games of all time.

Microsoft has almost zero presence in mobile gaming.

Nadella wants his gaming empire to facilitate direct payment like Apple’s App Store.

That’s effectively the holy grail of today’s gaming.

Microsoft has been at war with Apple and Google, over the fees the app stores charge for games.

It’s no surprise that Microsoft wants complete control over its ability to distribute games and content.

The deal also allows Microsoft an access point to secure an influential pool of gamers creating their own gaming content and worlds.

After adding Minecraft, LinkedIn, and GitHub, Nadella has been on the hunt for a game-changing asset that will drive the bottom line of MSFT via a large community of creators.

He failed to land social video service TikTok, while negotiations with Pinterest (PINS) and Discord were rebuffed.

ATVI is really a feather in the cap for Nadella, who won’t stop there and knows it’s just one battle of a greater war for tech supremacy.

These high-quality assets don’t get cheaper over time either.

Simply put, Microsoft loves subscription businesses, and gaming is among the best of them, and they are the stickiest around with recurring revenue that makes predicting future cash flows that much easier.

The ATVI pickup will raise the price of buying gaming assets across the board as I foresee a rush into these types of assets where not only can a company purchase the content, licenses, and gaming platform, but they can also add top-notch gaming developers which are equally as important as Microsoft tries to outmuscle Apple and Google.

This move is highly bullish for MSFT, so much so, that anti-trust regulators might cast a suspicious eye on this deal.

Global Market Comments

January 18, 2022

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SOARING WITH THE EAGLES)

(SPY), (TLT), (MSFT), (JPM), (AAPL)

Here I am, locked up again. Another day, another pandemic. There is nothing left for me to do but think.

When I turned negative on technology stocks at the end of November, many readers protested, accusing me of high treason, sedition, perfidy, and insisted I be hung from the nearest lamppost.

After last week’s drubbing on technology stocks, those claims are fading fast.

As a math graduate from UCLA, I can tell you it’s not about incompetence, delusion, or dementia, it’s simply all about the numbers.

Over the last five years, the S&P 500 (SPY) rose by 2X, while NASDAQ jumped by 3X, a 50% premium to the main market.

Most of this outperformance was due to multiple expansions. As interest rates fell further and further, investors were willing to pay ever more for tech stocks. As a result, 30% of tech stocks lose money and 30% trade for a nosebleed 10X sales or more.

Roll the interest rate move in reverse, and the tech premium disappears in a puff of smoke. And that has been happening with a vengeance since early December, with yields on the ten-year US Treasury bond soaring an eye-popping 58 basis points, from 1.34% to 1.82%.

Tech stocks are also coming off a pandemic tailwind of hurricane force. Now that every home in the country is equipped with four home offices and the hardware and software to support them, the turbocharger is failing.

Apple (AAPL) is a perfect example. From 2015 to 2019, Steve Jobs creation grew earnings by an average of 4% a year. Then the perfect storm hit, and earnings grew by an astonishing 60% in 2021. That delivered a gobsmacking 58% gain in the share price since March.

Tech momentum is now dead. In two-thirds of the tech market, a Dotcom bust has already played out, with non-earning pandemic darlings like Peloton (PTON) and Zoom (ZM) falling by 60%-70%.

It is not, however, the end of the world (usually, the world doesn’t end). If you are a long-term investor, big (earning) tech won’t fall enough to make it worth selling out and buying back lower. Non-earning small tech has already fallen so much it's no longer worth selling down here.

Back to the numbers, me the mathematician.

It’s all about margins, which are still expanding, and will be up by another 40-basis point in 2022 for the S&P 500 as a whole. For big tech, it’s just a matter of time before earnings catch up with valuations and it's off to the races again. It will take longer for small tech, possibly a lot longer.

The Economy is the Strongest in Decades, according to JP Morgan CEO Jamie Diamond. I agree. That’s because banks prosper most early in an interest-raising cycle. The Fed could raise rates four times this year. Keep buying financials on dips.

Quantitative Tightening to Start in July, says Goldman Sachs. That’s when the Fed starts selling its vast holdings of US Treasury bonds, about $8.5 trillion worth. They will continue QT until the pain becomes too great. Four rate hikes in 2022 are in the bag. It’s not a stock market-friendly scenario.

This is Not the Year to Own Money-Losing Tech, says my friend Goldman’s David Kostin. For investors, the glass has gone from half full to half empty. The big ones will be OK but are still due for a pullback. NASDAQ price-earnings are still at a 20 year high at 38X. Rising interest rates were the stick that broke the camel’s back. Don’t buy the dip too soon.

What is the Cheapest Sector in the Market? Biotech and Healthcare, which are at valuation lows not seen since the 2009 and 2000 lows. It also has the best decade-long growth outlook after technology. The problem is that no one wants to buy them on the back nine of a global pandemic. They will rally hard….someday.

Inflation Hits 7.0%, with the Consumer Price Index hitting a 39-year high. Bonds ended a $3.00 rally and resumed a downtrend. Rents and used cars led the gains. I remember 1982 well. My first home mortgage had an 18% interest rate. Expect worse to come.

S&P 500 Profits Jump 22.4% in Q4, possibly taking the full-year figure up an incredible 49%. It makes stocks look like a bargain, which were up only 27% in 2021. Expect cooler numbers and a quieter stock market in 2022.

Wholesale Prices Soar 9.7% YOY, the most in 11 years. It augers for more interest rate hikes sooner, with overnight rates targeting 1.25% by yearend.

Weekly Jobless Claims Hit Two-Month High at 230,000. No doubt it is due to the omicron surge. A million cases a day is certainly going to make a dent in the workforce. Some people are afraid to get sick, while others know they can get away with it.

Auto Stocks Will Be Top Performers in 2022, says value legend Mario Gabelli. Dealers are extremely short of inventory and demanding more production. Used car prices are soaring. Average industry sales prices have soared from $40,000 to $45,000 in a year. Buy (F) on a dip. (TSLA) has topped out for now with the rest of the tech stocks.

Bitcoin Breaks $40,000, as the flight from all interest-bearing securities continues. Don’t buy the dip yet.

China Posts Record Trade Surplus in 2021 at $676 billion on global economic recovery. The US ran a massive deficit with the Middle Kingdom last year, which is clearly dollar negative. None of the trade deals negotiated by Trump were honored. Exports were up 21% YOY in December.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With a new year at hand, it’s off to the races once again. I exploded out of the gate with a hardy 2.5% profit last week. I used fleeting rallies to sell short the S&P 500, Microsoft (MSFT), and the bond market (TLT). The Friday collapse in JP Morgan (JPM) tempted me into a long position there.

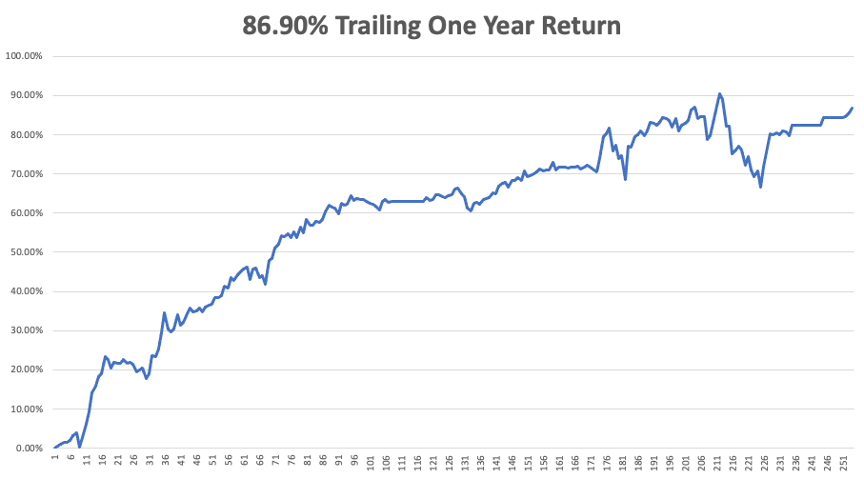

Yes, last year’s mighty 90.02% performance is a lot to top. But even the highest mountain is climbed with the first step (been there, done that).

That brings my 12-year total return to a record 515.11%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to a record 42.62%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 66 million and rising quickly and deaths topping 851,000, which you can find here.

On Monday, January 17 markets are closed for Martin Luther King Day.

On Tuesday, January 18 at 7:00 AM, the NAHB Housing Index for January is released.

On Wednesday, January 19 at 8:30 AM, Housing Starts for December are announced.

On Thursday, January 20 at 7:00 AM, the Existing Homes Sales for December are printed. At 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, January 21 at 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, during the 1980s, my late wife and I embarked on a National Geographic Expedition to the remote Greek islands, including Santorini, which in those days didn’t have an airport.

At dinner, we sat at our assigned table and I noticed that the elderly gentleman next to me spoke the same unique form of High German as I. I asked his name and he replied “Adolph.”

And what did Adolph do for a living? He was a pilot. And what kind of plane did he fly?

A Messerschmitt 262, the world’s first jet fighter.

What was his last name? Galland. Adolph Galland.

I couldn’t believe my luck. Adolph Galland was the most senior Luftwaffe general to survive WWII. He was one of Germany’s top aces and is credited with 109 kills. He only survived the war because he was shot down during the final weeks and ended up in a military hospital.

And that was the end of the cruise for the rest of the table, as Galland and I spent the rest of the week discussing the finer points of aviation history.

It was made especially interesting by the fact that I had already flown most of the allied planes that Galland went up against, including the P51 Mustang and the Spitfire.

Galland started life as a Versailles Treaty glider pilot and joined the civilian airline Lufthansa in 1932. He transferred to the Luftwaffe in 1937 to fight with Franco in the Spanish Civil War and participated in the invasion of Poland in 1939.

He flew a Messerschmitt 109 as cover for German bombers during the Battle of Britain. In 1941, he was promoted to the general in charge of Germany’s fighter force until 1945 when he was sidelined due to his opposition to Goring and Hitler.

It was a fascinating opportunity for me to learn many undisclosed historical anecdotes. Germany actually had a functioning jet fighter in 1939. But Hitler, with a WWI mindset, diverted development money to twin-engine bombers and artillery.

The army eventually produced a canon that fired a monster one-meter-wide shell but was so heavy that it needed double railroad tracks to move anywhere. The canon was virtually useless in a modern war and was a colossal waste of money. Galland believed the decision cost Germany the war.

The ME 262 was a fabulous plane. But it was too little too late. Of the 1,000 produced, 500 were destroyed on the ground and most of the rest during takeoff and landing.

A big problem with the plane was that its jet engines were made out of steel and would only last ten hours. Turkish titanium needed for longer-lived engines was embargoed by the allies.

Today, a beautiful example hangs from the ceiling of the Deutsches Museum in Munich.

Galland negotiated the handover of his jet fighter wing to the Americans from a hospital bed so they could be used in an imminent war against the Russians. The atomic bomb ended that idea.

Galland was one of the few German generals never subjected to a war crimes trial. Pilots on both sides saw themselves as modern knights of the air with their own code of conduct. Parachuting pilots were never attacked and lowering your landing gear was a respected sign of surrender.

After the war, Galland emigrated to Argentina to train Juan Peron’s Air Force. He also test flew Gloster Meteor jets for the Royal Air Force. He participated in the 1972 film, The Battle of Britain and many WWII memorials. By the time I met him, his eyesight was failing. He died in 1996 at 84 of natural causes.

I give thanks to the good luck I had in meeting him, and that I had the history behind me to understand the historical figure I was sitting next to. It isn’t everyone that gets six dinners with Germany’s top fighter ace.

A year later saw me on a top-secret mission flying from Cyprus back to the American airbase at Ramstein. I plotted my course directly over Santorini.

When I approached the volcanic island, I put my Cessna 340 into a steep descent, dove straight into the mouth of the volcano, and leveled out at 100 feet above the water, no doubt terrifying the many yachts at anchor.

Greek Military Air Control gave me hell, but it was my own private way of honoring the principlals of Adolph Galland.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader