Global Market Comments

July 22, 2021

Fiat Lux

Featured Trade:

(HOW DID THOSE TECH LEAPS WORK OUT?)

(AAPL), (AMZN), (MSFT)

Global Market Comments

July 22, 2021

Fiat Lux

Featured Trade:

(HOW DID THOSE TECH LEAPS WORK OUT?)

(AAPL), (AMZN), (MSFT)

A month ago, I sent you a research piece about the merits of long-term LEAPS in the major technology stocks (click here for the link).

They included:

Amazon (AMZN) January 2022 $3,200-$3,400 vertical bull call spread

Microsoft (MSFT) January 2022 $240-$270 vertical bull call spread

Apple (AAPL) January 2022 $120-$130 vertical bull call spread

So, how did those work out? Here is the stock performance and the LEAPS performance for each position:

Amazon (AMZN) stock +11.40% LEAPS +26.79%

Microsoft (MSFT) stock +7.69% LEAPS +35.38%

Apple (AAPL) stock +13.38% LEAPS +30.92%

In other words, the LEAPS outperformed the stock to the upside by anywhere from 2.5X to 5X. All three positions are now deep-in-the-money. As long as the stocks close at or above the upper strike prices by the January 16, 20222 option expiration day, they will all produce profits of 100% or more in only seven months!

It goes to confirm the strategy that I have been vociferously arguing in recent months, that LEAPS offer far and away the best risk/reward of any investment in current market conditions. Whenever I have a payday, I pour the money straight into my retirement funds and into the most attractive LEAPS.

The liquidity for long-dated options is not that great. That is why entering limit orders in LEAPS only, as opposed to market orders, is crucial.

These are really for your buy-and-forget investment portfolio, defined benefit plan, 401k, or IRA.

Like all options contracts, LEAPS give its owner the right to exercise the option to buy or sell 100 shares of stock at a set price for a given time.

LEAPS have been around since 1990, and trade on the Chicago Board Options Exchange (CBOE).

To participate, you need an options account with a brokerage house, an easy process that mainly involves acknowledging the risk disclosures that no one ever reads.

If LEAPS expire "out-of-the-money" on expiration day, you can lose all the money you spent on the premium to buy it. There's no toughing it out waiting for a recovery, as with actual shares of stock. Poof, and your money is gone.

Note that a LEAPS owner does not vote proxies or receive dividends because the underlying stock is owned by the seller, or "writer," of the LEAPS contract until the LEAPS owner exercises.

Despite the Wild West image of options, LEAPS are actually ideal for the right type of conservative investor.

They offer vastly more margin and more efficient use of capital than traditional broker margin accounts. And you don’t have to pay the usurious interest rates that margin accounts usually charge.

And for a moderate increase in risk, they present hugely outsized profit opportunities.

For the right investor, they are the ideal instrument.

So, let’s get on with my specific math for the (AMZN) LEAPS to discover its inner beauty.

By now, you should all know what vertical bull call spreads are. If you don’t, then please click this link for my quickie video tutorial (you must be logged in to your account). Warning: I have aged since I made this video.

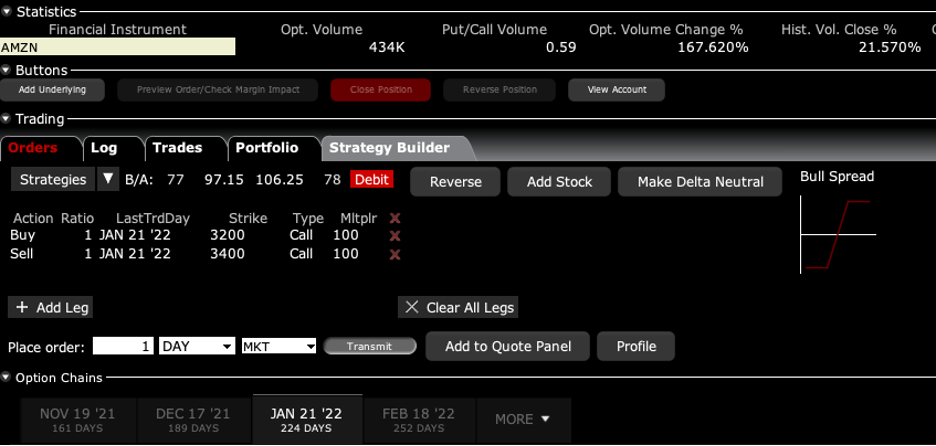

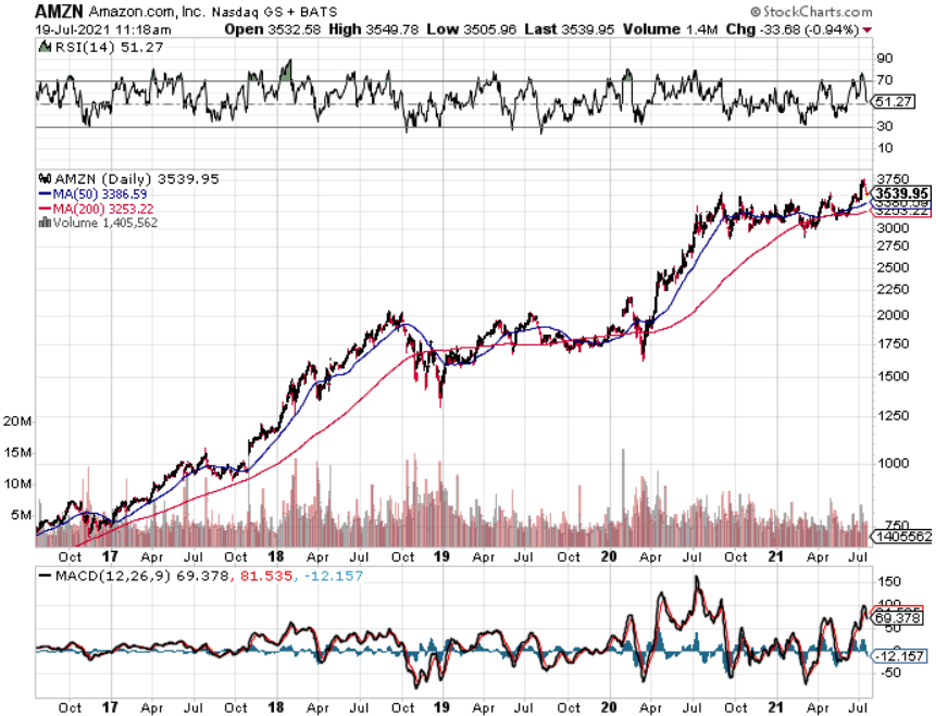

A month ago, Amazon closed at $3,346.83.

The cautious investor should have bought the (AMZN) January 2022 $3,200-$3,400 vertical bull call debit spread for $102. One contract gets you a $10,000 exposure. This is a bet that (AMZN) shares will close at $3,400 or higher by the January 22, 2022, option expiration, some 1.6% higher.

Sounds like a total no-brainer, doesn’t it?

Here are the specific trades you needed to execute this position:

expiration date: January 21, 2022

Portfolio weighting: 10%

Number of Contracts = 1 contract

Buy 1 January 2022 (AMZN) $3,200 call at………..….……$374.00

Sell short 1 January 2022 (AMZN) $3,400 call at…………$272.00

Net Cost:………………………….………..………….............….....$102.00

Potential Profit: $200.00 - $102.00 = $98.00

(1 X 100 X $98.00) = $9,800 or 96.07% in six months.

In other words, your $10,200 investment turned into $19,800 with an almost sure bet giving you a profit of 96.07%.

Why do a vertical bull call debit spread instead of just buying the January 2022 (AMZN) $3,400 calls outright?

You need a much bigger upside move to make money on this trade. (AMZN) would have to rise all the way to $3,674 to break even on the calls, and all the way up to $3,772 to match the profit of the call spread.

While I think it is possible that (AMZN) could rise that much by January, it is vastly more probable that (AMZN) will be over $3,400 by then. That is what hedge funds do all day long, and that is to find the most probable trade out there and then leverage up like crazy.

Remember, one call option gives you the right to buy 100 shares. That means over $3,400 your call spread that cost $10,200 will enable you to control 100 shares of Amazon worth $340,000. The potential upside leverage over $3,400 is 33.33X!

By paying only $102 for the spread instead of $274.00 for an outright call-only position, you can increase your size by 2.68 times, from 1 to 3 contracts for the same $10,200 commitment. That triples your upside leverage on the most probable move in (AMZN), the one above $3,400. That increases the upside leverage over $3,400 to an impressive 100X compared to the outright call buy.

How could this trade go wrong?

There is only one thing. We get a new variant on Covid-19 that overcomes the existing vaccines and brings a fourth wave in the pandemic.

In this case, (AMZN) doesn’t rise above $3,400 but crashes down to the $1,700 low we saw during the 2020 pandemic. We go back into recession. Both of the above positions go to zero. But if we get a fourth wave, you are going to have much bigger problems than your options positions.

So there it is. You pay your money and take your chances. That's why the potential returns on these simple trades are so incredibly high.

If you are interested in getting a more dedicated LEAPS service from the Mad Hedge Fund Trader, you might consider our Concierge service, which costs $10,000 a year and is by application only. If interested, please email support@madhedgefundtrader.com and put Concierge candidate in the subject line.

Enjoy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Tech LEAPS are the Way to Go

Mad Hedge Technology Letter

July 19, 2021

Fiat Lux

Featured Trade:

(THE LARGEST SHADOW BANKER AND U.S. TECH)

(BLK), (AMZN), (MSFT), (AAPL)

In the top-heavy global media landscape, there seems to be this notion that the U.S. and its capital is the primary alpha male swaying asset prices.

The close to $6 trillion in recent stimulus chasing too few services demonstrably has an outsized vote on the matter of asset pricing.

But the dirty little secret about this stimulus is that U.S. private equity is spilling into Nordic and Western European markets effectively forcing a rapid Americanization of asset prices across the Atlantic.

Shadow banks finance financial transactions that are too risky for banks.

In the US, they already grant half of all loans.

In times of low or even negative interest rates for credit, fewer and fewer investors bring their money to a normal bank, but rather to a so-called shadow bank.

This is a term that has become established to describe a phenomenon for financial participants who are not a bank.

What a shadow bank is is not exactly defined, because there are no shadow banking licenses; but tech companies and the U.S. wielding of this critical function have changed the financial world.

In some cases, a few large private families who now have the means to invest in such funds are also focused on funding through these shadow banks and most of the time to buy American tech stocks.

And they deliberately invest not just in a single fund, but across all countries in the world, and shadow banks make up around a third of the financial sector.

In Germany, it is more than a third and on the EU average, it is almost exactly a third.

Pension funds and pension funds work like small insurance companies: employees of a company pay part of their gross wages directly, free of tax and social security contributions. At the end of their working life, they will then be paid a supplementary pension from the income generated.

The fact that “their” money is mandated to be invested in the global financial markets - at least if people hope to receive a pension after their active working life.

These European pension funds are also turning to U.S. branded shadow banking.

According to the Financial Stability Board, shadow banks had a total of $80 trillion in business in 2021.

Compared to the previous year, this was an increase of 8.5%. The FSB information is based on data from 29 countries. These in turn represent 80% of global economic output.

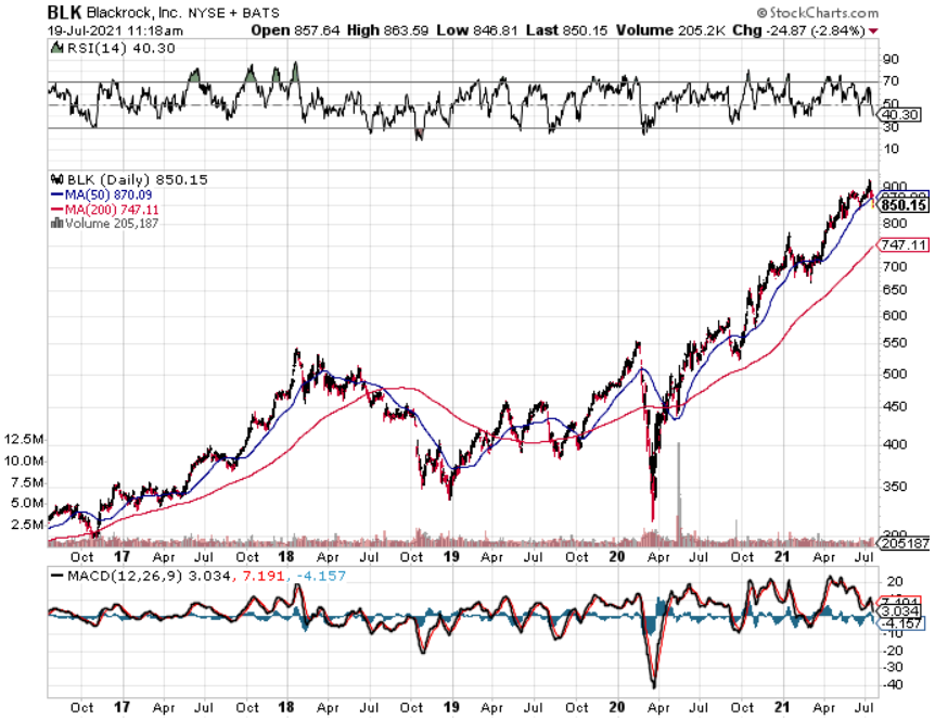

Many deals and transactions are outsourced from the banks now. That means: The financial business tries to circumvent the regulations and the largest shadow bank is BlackRock (BLK) - involved in 20,000 companies.

Many of these outsourced financial service providers are also nothing more than subsidiaries of BlackRock.

This outsourcing offers their customers the prospect of significantly higher interest rates.

BlackRock is an influential major shareholder in all listed global corporations from Europe and the USA.

Although it was founded in 1988, BlackRock was unknown to most people in Germany for decades.

That only changed in 2018, when the politician and lobbyist Friedrich Merz announced his candidacy for the CDU party chairmanship.

At this point in time, Friedrich Merz had been head of the supervisory board of the German offshoot of BlackRock for two years.

This is a company that currently manages a fortune of over nine trillion dollars which is far more than what is produced in Germany, every year, in terms of goods and services - considerably more.

At BlackRock, they harness the smorgasbord of mechanisms that define this new area of shadow banking: hedge funds, VC, real estate, index funds, and money market funds.

BlackRock holds considerable blocks of shares through various subsidiaries, including in normal commercial banks - such as Bank of America, Citigroup, and Deutsche Bank.

But that’s not all.

BlackRock is by far the largest owner in the German share index - with a share of 15 to 17%.

That means: every sixth share of the 30 largest German corporations is controlled by one of the BlackRock funds.

That BlackRock's ownership structure rotates in circles. The asset management companies control themselves, or are actually not subject to any control.

It’s an almost incestuous system where you pursue your own interests through a network of participation. While banks are systemically relevant, BlackRock is still uncontrolled, and they refuse to classify this company as systemically relevant.

But that is BlackRock and that is part of what made them highly successful.

It is extremely well connected. It has long-standing, important politicians in its ranks. Friedrich Merz is just one example in the big picture.

French President Emmanuel Macron recently said he wanted to see the creation of at least 10 tech companies in Europe worth over 100 billion euros each by 2030.

While Europe is now home to many unicorns — start-ups valued at over $1 billion — it is yet to produce a company with the scale of American and Chinese tech giants.

But I am ready to argue that Europeans no longer have control over their own narrative in their own financial system, it is now U.S. private equity.

Assuming that this holds true, even if President Macron’s wish bears fruit, the owners of these “European” tech companies will of course be Americans who are dressed up as European pension funds and maybe even perhaps somehow a company starting with a B and ending with ROCK?

The oversupply of capital from the U.S. that has overcharged U.S. tech shares will get any piece of the action that Europe creates if they are to create a tech renaissance, which I highly doubt.

And the real truth is that any unicorn created in Europe will most likely go public in New York anyway.

The pandemic has also supercharged the influence of Blackrock in Germany and Europe as a whole and that cannot be diminished.

According to Blackrock’s 13F, 10% of their portfolio is Apple (AAPL), Microsoft (MSFT), and Amazon (AMZN) - holding $128 billion in AAPL, $123 billion in MSFT, and only $87 billion in AMZN.

Their largest 7 holdings are in U.S. tech stocks.

This is just a 13F in their main fund, and it wouldn’t be shocking to find out some of their European subsidiaries are also doing the same thing even if not with the same amount of capital.

The European financial system has effectively been gamed by Blackrock and its copycats, so next time you hear of a large Nordic or German equity fund making a big splash in U.S. tech shares, the eventual originator of that decision could be Blackrock.

This is the type of sophistication we are dealing with at this point in global markets and essentially nothing beats the eye test anymore because we have no idea what is happening unless we follow the trail of money.

Global Market Comments

July 19, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE DELTA CORRECTION IS HERE)

(AMZN), (AAPL), (FB), (MSFT), (TAN), (FSLR)

Right now, the fate of your investment portfolio, and indeed your life, is in the hands of a minority of anti vaxers in the Midwest.

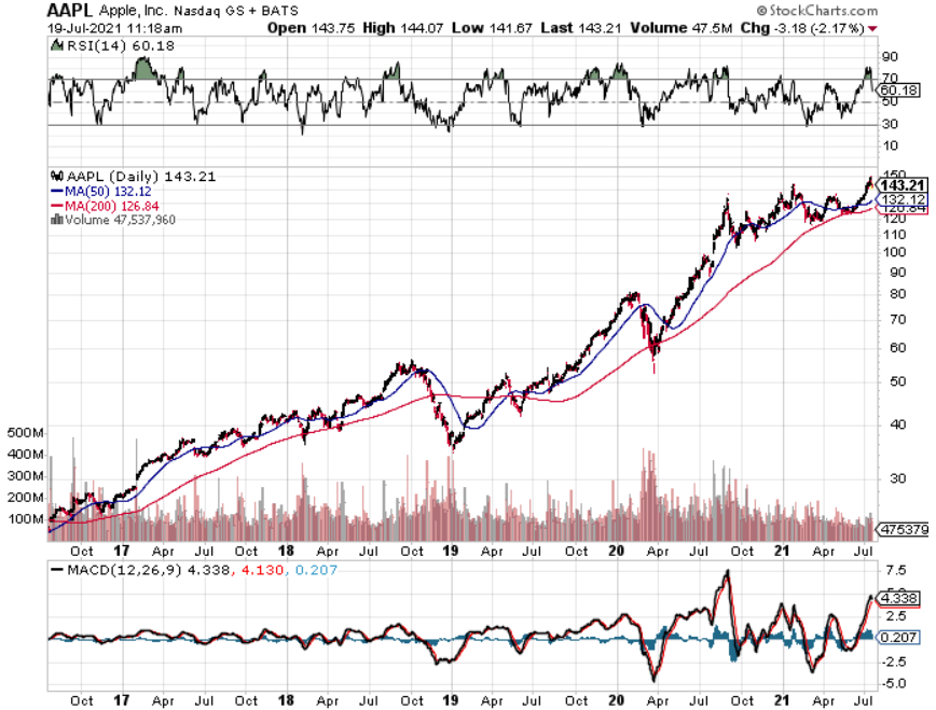

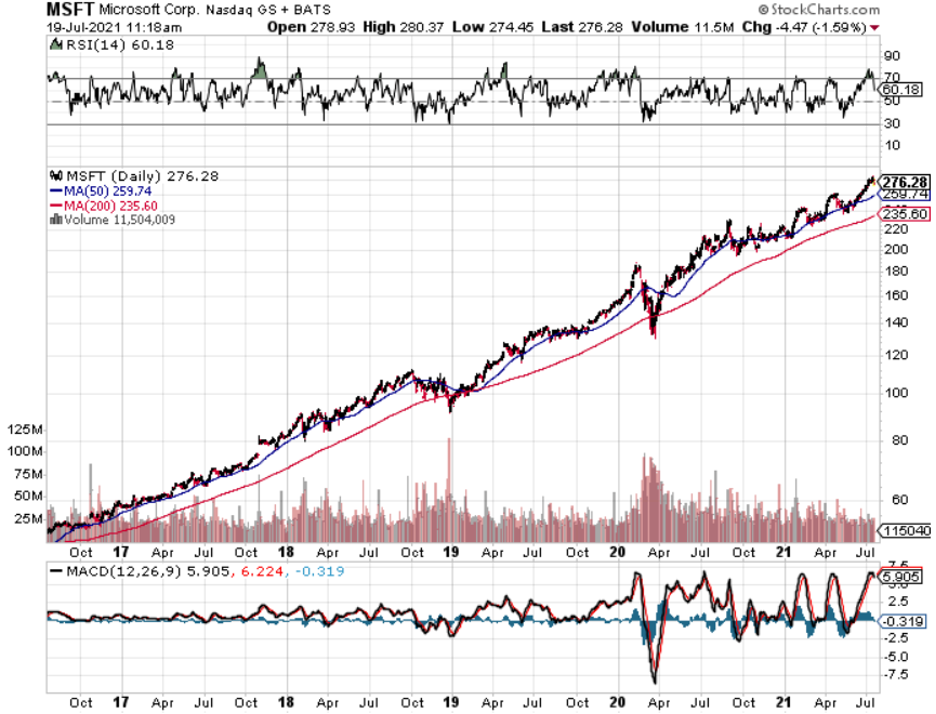

If the surge in the delta variant burns out in weeks or a month, the current market correction won’t extend any more than 5% and you should be loading the boat with big tech stocks like (AMZN), (AAPL), (FB), and (MSFT).

The delta variant is becoming a big deal, with unvaccinated states like Arkansas (35% vaccination rate) and Missouri (40% rate) driving the resurgence. It is essentially an epidemic of the unvaccinated.

Unless checked, it could lead to a broader stock market selloff in August. Los Angeles brought back the indoor mask mandate on Saturday, although compliance is near zero. San Francisco may be close behind.

Everyone in my company worldwide is now vaccinated, with Australia last to get one. I’ll be first in line for the Pfizer booster out in the fall. Delta is twice as contagious, more fatal, with more permanent side effects than earlier variants. And it’s killing more kids.

But it’s not the delta you have to worry about. If a future epsilon or zeta variant emerges, that can overcome our current vaccines, bred in the Midwest, the economy would shut down again and you can kiss your bull market goodbye. That would lead to a 1918 style finish to this pandemic, the fatality rate would go up to 50%, and millions more would die.

I’ll stick to the optimistic case….for now.

Even if we get a new variant, we now have the infrastructure in place to sequence the DNA of a new strain in a day and have 100 million doses in the freezer in two months. But it could be a close-run thing.

If you want to stick with your long portfolio in the face of millions dying here is the argument.

The Fed is unable to stimulate the economy any further through interest rate cuts or more QE. It is like pushing on a string. Companies can’t hire the labor they need to increase production or obtain the parts to make things.

This ends in August when workers get their free childcare back in the form of the public school system. The ending of Covid benefits will also light a fire under them. This will lead to a collapse in the unemployment rate and a further rise in GDP from the current ballistic 7.0% rate. This will allow the Fed to raise rates, but not enough to hurt stocks, especially techs.

This is your Goldilocks scenario for H2.

Driving down from Lake Tahoe to Long Beach to pick up my kids from Scout Camp, I passed two huge wildfires. Half the vehicles on the road (US 395) were fire trucks and crews moving in from other states. It’s like being at war.

So, you might ask the question of when will Climate Change affect the stock market? The answer is that Climate Change is actually great for stocks. Money gets spent to put fires out, then trillions of dollars get spent to rebuild with insurance claims.

The biggest impact of climate change is the decarbonization of our energy infrastructure, out of fossil fuels and into alternatives. Solar will soar from 20% to 70% of total electric power output in a decade while nuclear stays at 20% and hydroelectric at 10%. Coal and oil completely disappear. This will enable a large cut in our total energy bill.

Yes, I know oil has rallied lately. I’m sure American Leather had rallied on the way to zero, the only Dow stock to ever completely disappear. It was wiped out by the transition from horses to cars, eliminating 97% of the demand for leather. (The horse population went from 120 million to only 3.8 million today).

There are ways to play this today. Solar growth will be massive, so you have to look at the Invesco Solar ETF (TAN) and First Solar (FSLR).

Here is the next market top, at least for the short term. That’s because, for the last year, stocks have a nasty habit of selling off after quarterly earnings reports, which are just around the corner. Announcement dates for the FANGS are below. For the short term, you want to sell days before the reports. For the long term, you want to keep them, as I expect all to double or more in the next three years.

Facebook (FB) is July 28, 2021

Alphabet (GOOGL) - Jul 25, 2021

Apple (AAPL) Jul 27, 2021

Amazon (AMZN) Jul 26, 2021

Netflix (NFLX) Jul 20, 2021

Microsoft (MSFT) - Jul 28, 2021

China’s economy is slowing, with the post-Covid bounce over. It just provided $154 billion in stimulus for its economy and cut bank reserve requirements by 50 basis points. If they slow there, we could slow here, especially for big exporters to China in the ags.

Core CPI jumps to 5.4%, the biggest gain in 13 years. Excluding food and energy, it’s the biggest print since 1991. The Fed is holding its breath that these large numbers are temporary. Used car and truck prices accounted for a third of the gain for the second month in a row. That is certainly not sustainable, or I’m going into the used car business. Tech took off like a rocket on the news.

Producer prices show biggest gain since 2008, the is index up a hot 1.0% in June against 0.8% in May. PPI is up 7.3% YOY. Higher commodity and labor costs against shrinking inventories were the big issues. Inflationary pressures are here, but for how long?

Senate agrees to $3.5 trillion spending plan, providing great news for stocks and terrible news for bonds. No Republican support is required. This is in addition to the $579 billion infrastructure deal reach with opposition support. It’s enough dosh to keep this stock market percolating for years. Buy FANGS on dips.

Any tightening is a ways off, says Fed governor Jerome Powell in his congressional testimony, sending bonds soaring. The comment was in response to the superheated 5.4% CPI print on Tuesday. The $120 billion a month in Fed bond buying continues. Big tech loved it and continued with its non-stop rally. The rocket fuel for share prices continues unabated.

The four biggest US banks deliver spectacular earnings, posting a combined $33 billion in profits, triggering the predictable selloff. That is $9 billion above analyst forecasts, which seem to be a permanent lagging indicator. Consumer spending is exceeding pre-pandemic levels, credit quality is soaring, and credit card spending is through the roof. Buy (JPM), (BAC), and (V) on dips.

US retail sales come rocketing back, with customers spending those stimulus checks hand over fist. The 0.6% gain in June came on the heels of a 1.7% drop in May. Vaccinations are driving buyers back into the stores. Electronics stores, clothing, and restaurants saw the biggest increases.

Bank of America lowers US GDP from 7.0% to 6.5%, still the whitest hot numbers in history. 2022 is looking like 5.5%, still double the pre-pandemic rate. Personally, I think these numbers are low, and the stock market thinks so too. Keep buying dips in the good names.

Investors pouring out of bonds and into stocks, according to a survey of mutual fund flows last week. I couldn’t agree more. The Fed can’t keep holding on to zero rates forever, and when their turn comes, its will be brutal.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached a 1.84% gain so far in July. My 2021 year-to-date performance appreciated to 70.44%. The Dow Average is up 13.35% so far in 2021.

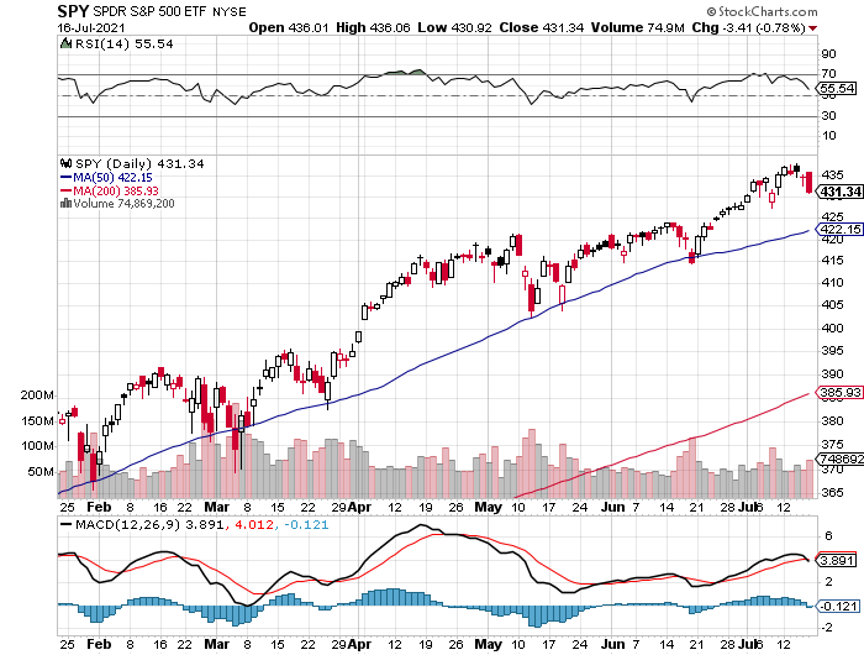

I spent the week running my two last positions, a long in (JPM) and a short in the (TLT) into the July 16 options expiration. Both expired at max profit. I then immediately strapped on a new short in the (SPY), my first since the pandemic began. That leaves me 90% in cash. I’m keeping positions small as long as we are at extreme overbought conditions.

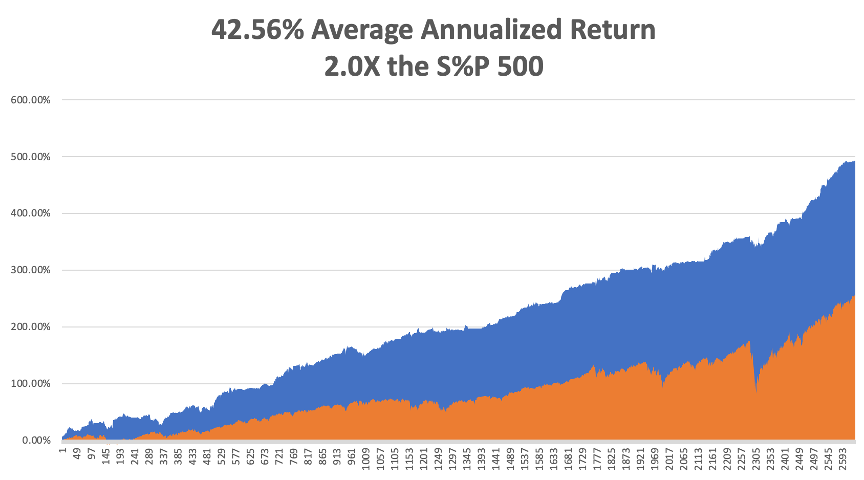

That brings my 11-year total return to 492.99%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.56%, easily the highest in the industry.

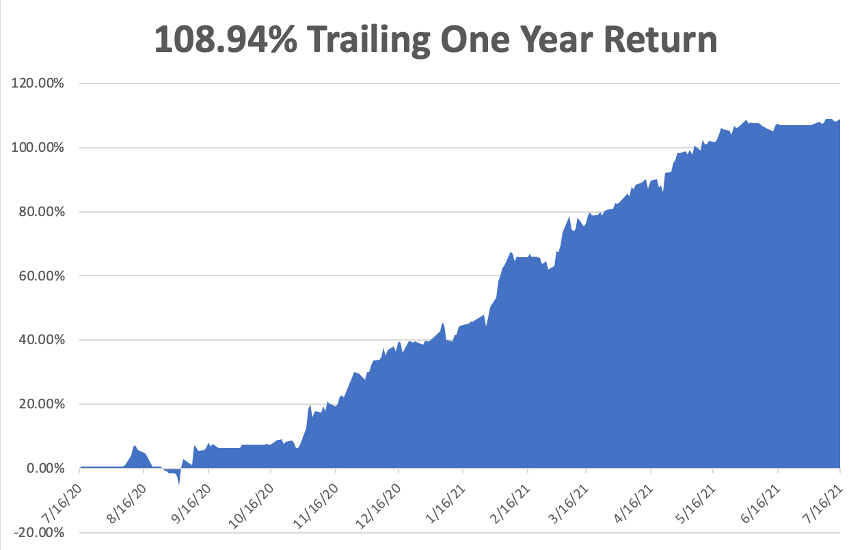

My trailing one-year return exploded to positively eye-popping 108.94%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 34.1 million and deaths topping 609,000, which you can find here.

The coming week will be a weak one on the data front.

On Monday, July 19 at 11:00 AM, the NAHB Housing Market Index for July is out. Johnson & Johnson (JNJ) and Verizon (VZ) report.

On Tuesday, July 20, at 8:30 AM, Housing Starts for June are printed. Haliburton (HAL) and United Airlines (UAL) report.

On Wednesday, July 21 at 11:30 AM, EIA Crude Oil Stocks are announced. Netgear (NTGR) reports.

On Thursday, July 22 at 8:30 AM, we learn the latest Weekly Jobless Claims. At 11:00 AM, we get Existing Home Sales for June. American Airlines (AAL) and Biogen (BIIB) report.

On Friday, July 23 at 2:00 PM, we learn the Baker-Hughes Rig Count. American Express (AXP) reports.

As for me, we all had to rearrange our budgets in the last year, dumping old spending habits and adopting new ones.

As for me, my electric scooter bill with Lime (click here for the site) has gone through the roof. They neatly fill the gap between walking and Uber in major tourist areas like Long Beach.

It’s a lot of fun, provided you don’t kill yourself on your first ride. The scooters go fast, some 20 miles an hour. Each one has a 13-mile range. When you’re done, you just drop it, take its picture, and then Lime picks it up and recharges it overnight.

I think I broke all seven of their mandatory rules (no driving on sidewalks, driving without a helmet, drinking while driving….). Hey, the great thing about being my age is that there are no long-term consequences to anything.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Check Out My New Wheels

Here is the Problem

Mad Hedge Technology Letter

July 12, 2021

Fiat Lux

Featured Trade:

(RIDE THE MOMENTUM)

(SHOP), (NFLX), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)

Just as millions of people in the United States are sensing that life has returned to something that resembles normalcy, the Coronavirus’ delta variant has emerged as American technology stocks biggest upcoming inflection point.

This certainly ups the ante in the struggle to grapple with the pandemic and has wide-reaching consequences for your technology portfolio.

Fresh data from the U.S. Centers for Disease Control and Prevention shows that more than half of all new cases in the U.S. were attributed to the delta variant, which is believed to be easily transmissible.

About 50% of Americans are fully unvaccinated meaning 50% are not, which could lead to hellacious autumn for the 175 million who are not.

The tech market has sniffed this out.

Data suggesting this variant is three times as infectious as the original coronavirus strain is the catalyst for a massive rotation into premium big tech who boast glamorous balance sheets.

It is still unclear if this virus is actually deadlier or leads to more severe illness, but the health of Facebook, Google, Apple, Microsoft, and Amazon aren’t reliant on the outcome of the delta variant or at least relative to companies that have physical storefronts.

I believe the momentum in these names will continue in the short term as more countries prepare to carve up new movement restrictions and quasi lockdowns to combat the new variant.

The recent tech rotation has been inconspicuous but powerful and the who’s who of big tech are enjoying a stellar run in the past month with FB up 6%, GOOGL up 4.5%, AAPL up 13%, MSFT up 8%, and AMZN up 11%.

These premium tech stocks are acting almost like U.S. treasuries and are increasingly defined as a perceived flight to safety because of

the net high quality of the assets.

Whether there is another virus that kills another 4 million globally again, investors are confident that these prioritized tech stocks are immune to any meaningful weaknesses.

On a granular level, pullbacks are becoming highly rare and mini pullbacks are becoming the only practical entry points into these stocks.

Readers waiting for a 5% drop are still waiting.

Reading waiting for 10% drops risk never getting in when the going is good.

Fresh news of Japan banning spectators for the upcoming and badly organized Tokyo Olympics took down GOOGL and FB 2% intraday only for shares to make up half the losses in one afternoon.

The delta variant has strengthened the “buy the dip” philosophy that is deeply entrenched in these 5 tech names.

The strength of tech can be seen further down the totem pole in inferior names.

Shopify (SHOP), Canada’s ecommerce crown jewel, is another winner with shares up 19% in the past 30 days.

If this rotation continues, I can realistically expect dips or sideways price action in Uber (UBER), Lyft (LYFT), and Airbnb (ABNB) because their investment case weakens relative to the big 5 in a delta variant world.

Netflix (NFLX) is another one that will harvest the low-hanging fruit with strong near-term action resulting in a 9% gain in the past 30 days.

It’s highly likely that in more than several regions around the world, the delta variant will re-silo consumers and hamstring businesses.

Crushing any green shoots that the reopening is supposed to deliver isn’t an ideal runway to growth.

Epidemiologists are starting to come out of the woodwork with Hungarian virologist Ferenc Jakab saying Hungary will be lucky to “get away with August” when referring to a possible 4th wave.

This hasn’t been fully priced into the U.S. tech market and tech will enjoy a full-scale rotation if the 4th wave arrives in full force.

However, I don’t believe we are on the cusp of another $12+ trillion bailout for the delta like last time go around, which does cap momentum to the upside.

There will also be a lack of meme stock profit-taking and bitcoin profit-taking that can be rolled into the big tech safety trade.

Sensibly, this could be a short-term boost for emerging growth tech as well with the likes of DocuSign (DOCU), Zoom Video (ZM), and Teladoc (TDOC) benefiting from investors dusting off the 2020 playbook again.

I forgot to mention that U.S. treasuries falling to $1.36% is the primary reason why at the balance sheet level, growth tech will also get the benefit of the doubt in the short term.

This won’t just be a big 5 momentum encore, others will enjoy the fruits of labor.

Loss-making tech is inordinately reliant on rates being low to subsidize losses and as the 10-year rate has gone from 1.72% to 1.36%, it’s no surprise that growth tech looks like eye candy now too.

Big tech is certainly more durable and has the capacity to navigate around rising rates which is the deal-clincher for me.

I am inclined to get back into the market with any delta scare that cheapens tech before the next leg up.

The embarrassing loss in the judicial system against FB by the Feds is the cherry on top.

I am bullish tech in the short term.

Global Market Comments

July 7, 2021

Fiat Lux

Featured Trade:

(JUNE 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (BRKB), (GOOG), (NVDA), (FB), (TSLA), (JPM), (BAC), (C), (GS), (MS), (NASD), ((X), (FCX), (AMZN), (MSFT), (AAPL), (FCX)

Global Market Comments

July 6, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ALL EYES ON THE FANGS)

(FB), (AAPL), (AMZN), (MSFT), (NFLX), (NVDA), (AMD), (MU)