Mad Hedge Technology Letter

February 6, 2019

Fiat Lux

Featured Trade:

(ALPHABET WOWS THEM AGAIN),

(GOOGL), (AMZN), (AAPL), (MSFT)

Mad Hedge Technology Letter

February 6, 2019

Fiat Lux

Featured Trade:

(ALPHABET WOWS THEM AGAIN),

(GOOGL), (AMZN), (AAPL), (MSFT)

Alphabet (GOOGL) is entangled in the same imbroglio as Apple (AAPL), that is why I have held back on issuing any trade alerts on this name.

The stalwart is still grinding out a respectable 20% of revenue growth in their core business but the underlying conundrum is that their hyper-growth segments are 5 times or more diminutive than their bread and butter of digital ads.

Apple is addressing the same type of strain in attempting to flip high octane revenue drivers into a bigger piece of the pie – the services business trails the hardware business by a large margin.

This phenomenon highlights how investors demand tech companies to grow at elevated rates and a maturing business model isn’t given any free passes.

Investors simply migrate towards higher growth names period.

That being said, Alphabet’s digital ad business is one of the premier tech divisions in all of technology and the American economy.

How powerful is it?

They did $32.6 billion in sales last quarter.

If you look at that number without context, it is quite impressive, but there are several lurking impediments.

This 20% QOQ growth is flatter than a pancake offering evidence that the best days are behind them.

No investors like to hear the dreaded “P word” thrown into a company’s business trajectory – peak.

In respect to revenue growth rates, I expect Google’s digital ad business to gradually decline relative to competition.

This segment also battles with the law of large numbers.

It’s simply difficult to accelerate revenue rates at a 25% YOY clip when revenues are already over $30 billion per quarter. Again, this is another Apple problem and a side effect of being overly successful in one part of the business model.

If investors' tepid reaction about these aspects of the core business telegraph dissatisfaction, then discovering further ancillary problems might be the final dagger in the heart.

Google search’s price per click cratered 29% YOY indicating that variables in the current marketing environment have significantly blunted Google’s pricing power.

Traffic Acquisition Cost (TAC) represents the cost for a company to acquire internet traffic onto their assets.

Alphabet faced a 15% YOY rise in TAC costs last quarter to $7.44 billion illustrating the difficulty in keeping these high costs down.

The bulk of the $7.44 billion stems from a widely known agreement with Apple contracting Google search as its default search engine on Apple devices.

This TAC expense has been surging the past few years and Alphabet has little negotiating power.

Expect an annual 15-20% rise in TAC expenses as long as Alphabet’s digital ads are expanding the standard vanilla 20% most investors expect them to grow.

As a whole, TAC costs soaked up 23% of the digital ad revenue which was in line with analysts’ expectations.

However, I expect this number to surpass 25% before winter because I believe Google search’s ad business will confront ceaseless growth problems.

Amazon’s (AMZN) new-found digital ad business is an influential factor in this story.

New marketing dollars aren’t being showered on Google as they once were, over 50% of product searches populate from Amazon.com today boding poorly for the future of Google search.

This optionality could be a large reason in driving the cost per click downwards.

CEO of Amazon Jeff Bezos refused to enter the digital ad game for years but his recent change of heart will correlate to subduing Google digital ad model.

Consumers are finding less incentive to search on Google for products when they just can smartly and efficiently search on Amazon directly.

Clearly, this only affects product searches and not searches on other informative content such as widely popular searches including “top 10 places to travel in Europe” or “best Thanksgiving recipes.”

Google’s “other revenues” is chugging along nicely with 31% YOY growth headed by Google’s cloud business and hardware division.

This is what Alphabet needs to focus on going forward similar to Microsoft and Amazon web services.

Yes, Google is the 3rd biggest cloud player but miles behind the top two.

Being in catch-up mode is no fun and is part of the reason capital expenditures exploded and came in $1.38 billion higher than expected.

Alphabet simply isn’t doing a good job at executing relative to Amazon and Microsoft frittering away more capital in the name of growth but not curating the type of growth that current expenses justify.

Higher costs damaged operating margins coming down 2% YOY to 21%.

Even more worrisome is that there has been no material progress on the Waymo business.

This is the year that Alphabet expected the technology to roll out to the masses.

However, this broad-based integration will not happen as fast as they would like.

I blame regulation and consumers' hesitation to quickly adopt this new technology.

Alphabet is reliant on this business to carry them to the next level of growth and I believe it can become a $100 billion per year business in a $2 trillion addressable market.

But when you peruse through the “Other Bets” category which houses Alphabet’s other companies such as health venture Verily, the $154 million in revenue was a huge miss against the $187.4 million expected.

Estimates aside, the pitiful fact that Waymo only brings in revenue of less than 1% of total revenue is disappointing.

Summing things up, Alphabet is a great company and is a long-term buy and hold stock even with short term transitory headaches.

In the near term, there is uneasiness about the decreasing profitability, exploding expense factors, a heavy reliance on weakening core business revenue, and a lack of top-line contribution of “other revenues” relative to their core business.

Long term, Alphabet’s game-changing investments have yet to show signs of life in terms of real revenue expansion even though Alphabet is the global leader of artificial intelligence and self-driving technology.

Investors would like to see actionable steps to incorporate this best of breed technology that funnels down to the top and bottom line.

Investors are stuck with a stale digital ads business that has locked the stock into a holding pattern essentially trading sideways for the past year until they prove they are ready to take the next step up.

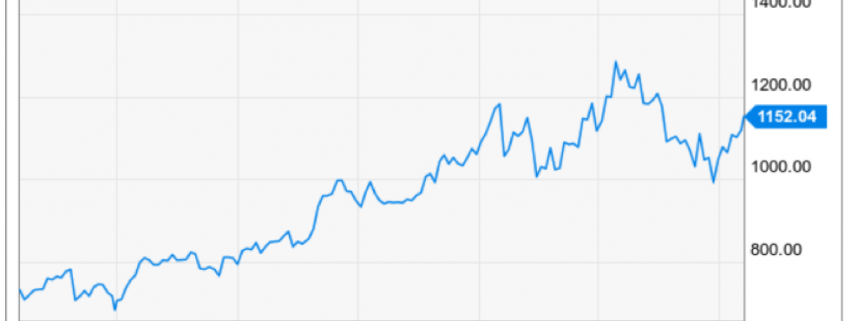

Looking at Alphabet’s chart, the stock has iron-clad support at $1,000 which it tested in April 2018 and December 2018.

Using this entry point as the lower range would be sensible as I don’t foresee any demonstrably negative news blindsiding the stock, and I surmise that investors will start receiving positive news on Waymo’s roll out towards the middle of the year.

Mad Hedge Technology Letter

January 29, 2019

Fiat Lux

Featured Trade:

(WHATS BEHIND THE NVIDIA MELTDOWN),

(QRVO), (MU), (SWKS), (NVDA), (AMD), (INTC), (AAPL), (AMZN), (GOOGL), (MSFT), (FB)

Great company – lousy time to be this great company.

That is the least I can say for GPU chip company Nvidia (NVDA) who issued a cataclysmic earnings alert figuring it was better to spill the negative news now to start the healing process earlier.

This stock is a great long-term hold because they are the best of breed in an industry fueled by a secular tailwind in GPUs.

But this doesn’t mean they will be gifted any freebies in the short term and, sad to say, they have been dragged, kicking and screaming, into the heart of the trade skirmish along with Apple (AAPL) and buddy Intel (INTC) amongst others.

The best thing a tech company can have going for them right now is to have no China exposure, that is why I am bullish on software companies such as PayPal, Twilio, and Microsoft.

I called the chip disaster back in summer of 2018 recommending to stay away like the plague.

The climate has worsened since then and like I recently said – don’t buy the dead cat bounce in chips because the bad news isn’t baked into the story yet or at least not fully baked.

It’s actually a blessing in disguise if banned in China if you are firms such as Facebook (FB), Google (GOOGL), and Amazon (AMZN).

I recently noted that a material end to this trade war could be decades away and the tech world is already being reconfigured around the monopoly board as we speak with this in mind.

Where do things stand?

The US administration took a scalp when Chinese communist backed DRAM chip maker Fujian Jinhua effectively shuttered its doors.

Victory in a minor battle will likely embolden the US administration into continuing its aggressive stance if it is working.

If you forgot who Fujian Jinhua was… they are the Chinese chip company who were indicted by the U.S. Justice Department for stealing intellectual property (IP) from Boise-based chip behemoth Micron (MU).

The way they allegedly stole the information was by poaching Taiwanese chip engineers who would divulge the secrets to the Chinese company buttressing China in pursuing their hellbent goal of being able to domestically supply enough quality chips in order to stop buying American chips in the future.

Officially, China hopes to ramp up its self-sufficiency ratio in the semiconductor industry to at least 70% by 2025 which dovetails nicely with the broader goal of Chinese tech hegemony.

Fujian Jinhua was classified as a strategically important firm to the Chinese state and knocking the wind out of their sails will have a reverberating effect around the Chinese tech sector and will deter Taiwanese chip engineers to act as a go-between.

According to a research note by Zhongtai Securities, Jinhua’s new plant was expected to have flooded the market with 60,000 chips per month and generate annual revenue of $1.2 billion directly competing with Micron with their own technology borrowed from Micron themselves.

Jinhua’s overall goal was to support a monthly manufacturing target of 240,000 chips spoiling Chinese tech companies with a healthy new stream of state-subsidized allotment of chips needed to keep costs down and build the gadgets and gizmos of the future.

For the most part, it was unforeseen that the US administration had the gall and calculative nous to combat the nurtured Chinese state tech sector.

However, I will say, it makes sense to pick off the Chinese tech space now before they stop needing American chips at all in 5-7 years and when all remnants of leverage disappear.

The short-term pain will be felt in the American chip tech sector which is evident with the horrid news Nvidia reported and the aftermath seen in the price action of the stock.

Nvidia expects top line revenue to shrink by $500 million or half a billion – it’s been a while since I saw such a massive cut in forecasts.

Half of revenue comes from the Middle Kingdom and expect huge downgrades from Apple on its earnings report too.

If this didn’t scare you, what will?

These short-term headwinds are worth it to the American tech sector as a whole.

To eventually ward off a future existential crisis when Chinese GPU companies start offering outside business actionable high quality chips curated with borrowed technology, funded by artificially low debt, and for half the price is worth its weight in gold.

The same story is playing out with Huawei around the globe but at the largest scale possible.

This is what happens when the foreign tech sector is up against companies who have access to unlimited state loans and is part of wider communist state policy to take over foundational technology globally.

I will also emphasize that the Chinese communist party has a seat on every board at any notable Chinese tech company influencing decisions at the top even more than the upper management.

If upper management stopped paying heed to the communist voice at the table, they would be out of business in a jiffy.

Therefore, Huawei founder Ren Zhengfei standing at a podium promulgating a scenario where Huawei is operating freely from the government is what dreams are made of.

It’s not a prognosis rooted in reality.

The communist party are overlords breathing down the neck of Huawei after any material decisions that can affect the company and subsequently the government’s position in the interconnected world.

The China blue print essentially entails a pan-Amazon strategy emphasizing large volume – low cost strategy.

Amazon was successful because investors would throw money at the company until it scaled up and wiped the competition away in one fell swoop.

Amazon is on a destructive path bludgeoning every American second-tier mall reshaping the economic world.

The unintended consequences have been profound with the ultimate spoils falling at the feet of CEO and Founder of Amazon Jeff Bezos, his phalanx of employees as well as Amazon stockholders which are mostly comprised of wealthy investors.

Well, Chairman Xi Jinping and the Chinese communist party are attempting to Amazon the American tech sector and the broader American economy.

The American economy could potentially become the second-tier mall in this analogy and the game playing out is an existential crisis for the likes of Advanced Micro Devices (AMD), Nvidia, Micron, Intel and the who’s who of semiconductor chips.

If stocks reacted on a 30-year timeframe, Nvidia would be up 15% today instead of reaching a trading day nadir of 17%.

What is happening behind the scenes?

American tech companies are moving supply chains or planning to move supply chains out of China.

This is an epochal manifestation of the larger trade war and a decisive development in the eyes of the American administration.

In fact, many industry analysts understand a logjam of failed trade solutions as a bonus to the Chinese.

However, I would argue the complete opposite.

Yes, the Chinese are waiting out the current administration to deal with a new one that might be more lenient.

But that will take another two years and publicly listed companies grappling with the performance of quarterly earnings don’t have two years like the Chinese communist party.

And who knows, the next administration might even seize the baton from the current administration and clamp down even more.

Be careful what you wish for.

Taiwanese company and biggest iPhone assembler Foxconn Technology Group is discussing plans to move production away from China to India.

India is a democratic country, the biggest democracy in Asia, and is a staunch ally of the United States.

CEOs of Google (GOOGL) and Microsoft (MSFT), some of Silicon Valley heavyweights, are from India and American tech companies have been making generational tech investments in India recently.

Warren Buffet even invested $300 million in an Indian FinTech company Paytm.

When you read stories about India being the new China, well it’s happening faster than anyone thought and on a scale that nobody thought, and the underlying catalyst is the overarching trade war fueling this quick migration.

Apple is already constructing low grade iPhones in India in the state of Karnataka since 2017, and these were the first iPhones made in India.

They won’t be the last either.

Wistron, major Taiwanese original design manufacturer, has since started producing the iPhone 6S model there as well.

And it is no surprise that China and its artificially priced smartphones have undercut Samsung and Apple in India grabbing the market share lead.

This is happening all over the emerging world.

And don’t forget if U.S. President Donald Trump revisits banning American chip companies supply channels to Chinese telecom company ZTE. That would be 70,000 Chinese jobs out the window in a nanosecond.

The current administration has drier powder than you think and this would hasten the deceleration of the Chinese economy and also move forward the American recession into 2019 boding negative for tech shares.

Therefore, I would recommend balancing out a trading portfolio with overweights and underweights because it is obvious that tech stocks won’t be coupled to a gondola trajectory to the peak of the summit this year.

It’s a stockpickers market this year with visible losers and winners.

And if China does get their way in the tech war, American chip companies will eventually become worthless squeezed out by mainland competition brought down by their own technology full circle.

They are first on the chopping board because their overreliance on Chinese revenue streams for the bulk of sales.

Among these companies that could go bust are Broadcom (AVGO), Qualcomm (QCOM), Qorvo (QRVO), Skyworks Solutions (SWKS) and as you expected Micron and Nvidia who are one of the main protagonists in this story.

Global Market Comments

January 28, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or IT’S FINALLY OVER)

(SPY), (TLT), (FXE), (MSFT), (AAPL),

(PG), (F), (LRCX), (AMD), (XLNX)

Last week, I was too busy to cook dinner for my brood, so I ordered a pizza delivery. When an older man showed up with our dinner, I told the kids to tip him double. After all, he might be an unpaid federal air traffic controller.

It is a good thing I work late on Friday afternoon because that's when the government shutdown ended after 35 days. The bad news? The government stops getting paid again in only 18 more days. If you have to travel, you better do it quick as the open window may be short.

The most valuable thing we learned from all of this is that the weak point in America is the airline transportation system which relies on 4,000 flights to get the country’s business done.

Having once owned a European air charter company, I could have told you as much was coming. Every nut, bolt, and screw that goes into a US registered aircraft has to be inspected by the federal government. They are painted yellow when viewed which is called “yellow tagging”. No inspection, no screw. No screw, no airplane. No airplane, no flight. No flight, no economy. I can’t tell you how many times I have seen a $30 million aircraft grounded by a failed 50-cent part.

And here’s what most investors don’t get. We lost 75 basis points in GDP growth from the shutdown. We may lose another 75 basis points restarting. And if you lose 1.50% from a post-Christmas period that is normally weak anyway, Q1 GDP may well come in negative. Hello recession!

We won’t know for sure until the first advanced estimate of Q1 GDP from the US Department of Commerce’s Bureau of Economic Analysis is published on April 26. That’s when the sushi will hit the fan. That, by the way, is perilously close for the May 10 prediction of the end of the entire ten-year bull market.

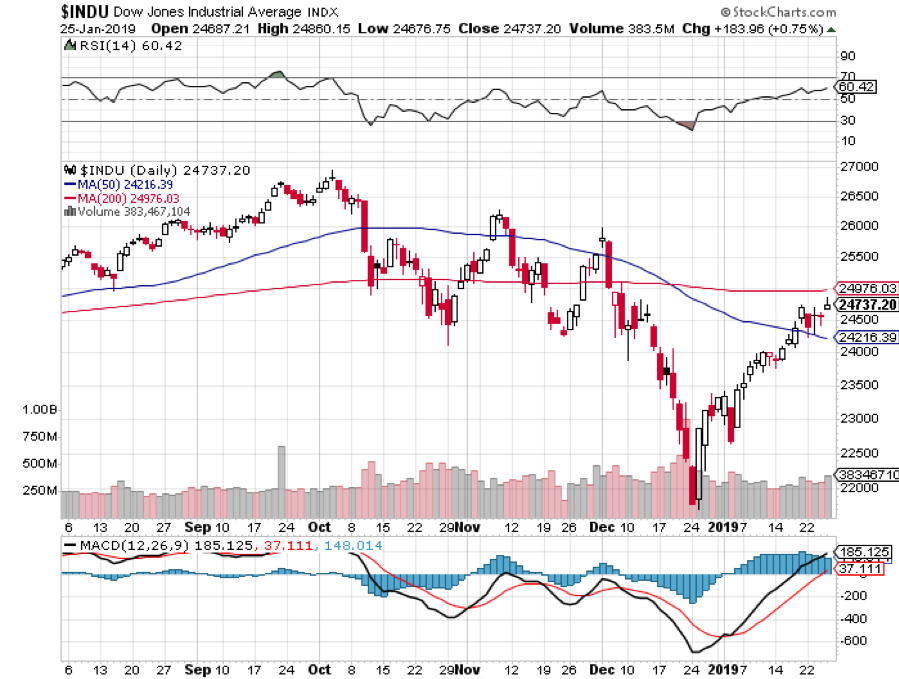

How did investors fare during the shutdown? We clocked the best January in 32 years with the Dow Average up 7.55%. Maybe the government should stay closed all the time!

It is not like the government shutdown, the fading Chinese trade talks, and the arrest of the president’s pal were the only things happening last week.

A slowing China is freaking out investors everywhere. Even if a trade deal is cut tomorrow, it may not be enough to pull the economy out of a downward death spiral. Look out below! A 6.6% growth rate for 2018 is the slowest in 30 years.

Existing Home Sales were down a disastrous 6.4%, in December and 10% YOY, the worst read since 2012. The government shutdown is made closings nearly impossible.

The EC’s Mario Draghi said there would be no euro rate rises until 2020 and the US bond market took off like a rocket. Another point or two and we’ll be in short selling territory again. Don’t count on Europe to pull us out of the next recession. Whoever came up with the idea of putting an Italian in charge of Europe’s finances anyway? Like that was such a great idea.

Procter & Gamble (PG) beat with an upside earnings surprise. It must be all those people buying soap to wash their hands of our political system. But Ford (F) disappointed, dragged down by weak foreign earnings. The weakest big car company to get into electric cars is really starting to suffer. The last of the buggy whip makers is taking a swan dive

The semis have bottomed in the wake of spectacular earnings reports from (LRCX), (AMD), and (XLNX). The great artificial intelligence play is back in action after a severe spanking. I never had any doubt they would come back. Now for an entry point.

Farmers are leaving crops to rot in the field as the trade war with China destroys prices and the Mexicans needed to harvest them are trapped at the border. There’s got to be an easier way to earn a living. Avoid the ags and all ag plays. Short tofu stocks!

Investors are now sitting on pins and needles wondering if we get a repeat of the horrific February of 2018, or whether so far great earnings reports will drive us to higher highs. Earnings tail off right when the next government shutdown is supposed to start so our lives will be interesting, to say the least.

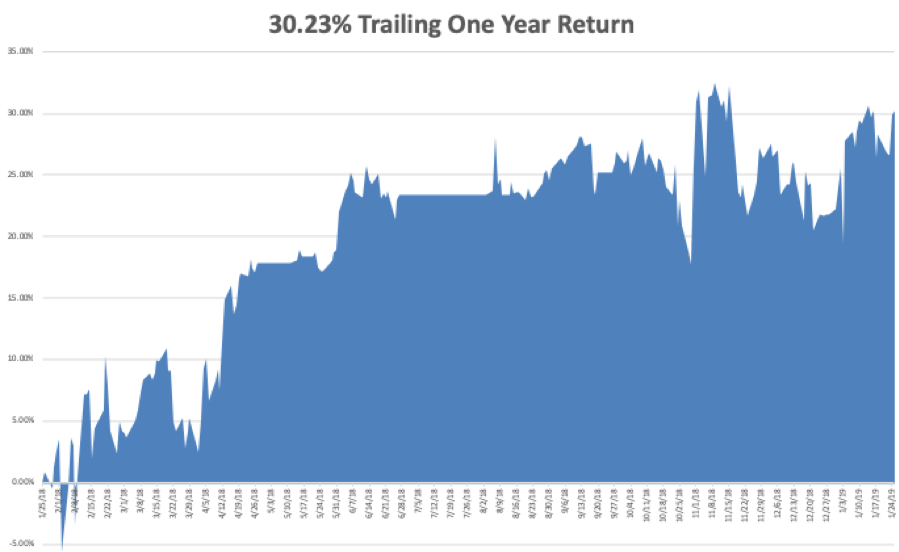

My January and 2019 year to date return soared to +7.24%, boosting my trailing one-year return back up to +30.23%.

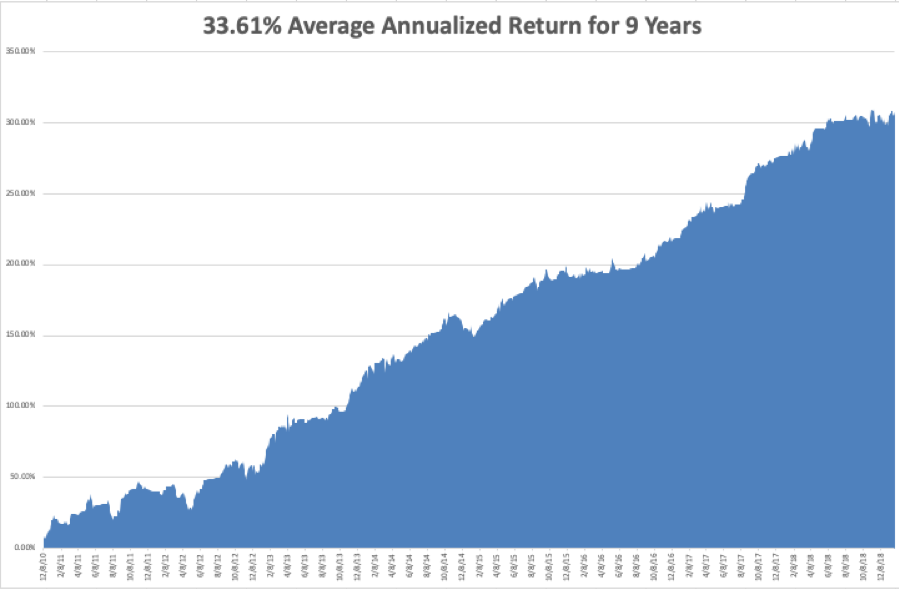

My nine-year return climbed up to +308.14%, a mere 1.72% short of a new all time high. The average annualized return revived to +33.61%.

I have been dancing in between the raindrops using rallies to take profits on longs and big dips to cover shorts.

I started out the week using the 4 1/2 point plunge in the bond market (TLT) to cover the last of my shorts there, bring in a whopper of a $1,680 profit in only 13 trading days. To quote the Terminator (whose girlfriend I once dated, the Terminatrix), I’ll be back.”

I used the big 500-point swoon in the Dow on Monday to come out of my (SPY) short at cost. An unfortunate comment on interest rates by the European Central Bank forced me to stop out of my long in the Euro (FXE), also at cost.

That has whittled my portfolio down to only two positions, a long in Microsoft (MSFT) and a short in Apple (AAPL). As a pairs trade you could probably run this position for years. I am now 80% in cash.

The goal is to go 100% into cash into the February option expiration in 14 trading days, wait for a big breakout, and then fade it. Essentially, I am waiting for the market to tell me what to do. That will enable me to bank double-digit profits for the start of 2019, the best in a decade.

The upcoming week is very iffy on the data front because of the government shutdown. Some government data may be delayed and other completely missing. Private sources will continue reporting on schedule. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

Jobs data will be the big events over the coming five days along with some important housing numbers. We also have several heavies reporting earnings.

On Monday, January 28 at 8:30 AM EST, we get the Chicago Fed National Activity Index.

On Tuesday, January 29, 9:00 AM EST, the Case Shiller National Home Price Index for November is released. The ever important Apple (AAPL) earnings are out after the close, along with Juniper Networks (JNPR).

On Wednesday, January 30 at 8:15 AM EST, the ADP Private Employment Report is announced. Pending Home Sales for December follows. Boeing Aircraft (BA) and Facebook (FB), and PayPal (PYPL) announce.

Thursday, January 31 at 8:30 AM EST, we get Weekly Jobless Claims. We also get the all-important Consumer Spending Index for December. Amazon (AMZN) and General Electric (GE) announce.

On Friday, February 1 at 8:30 AM EST, the January NonFarm Payroll Report hits the tape.

The Baker-Hughes Rig Count follows at 1:00 PM. Schlumberger (SLB) announces earnings. Home Sales is released. AbbVie Inc (ABBV) and DR Horton (DHI) report.

As for me, I will be celebrating my birthday. Believe me, lighting 67 candles creates a real bonfire. I received the best birthday card ever from my daughter which I have copied below

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 24, 2019

Fiat Lux

Featured Trade:

(FROM THE FRONT LINES OF THE TRADE WAR),

(AAPL), (AVGO), (QCOM), (TLT),

(HOW THE MAD HEDGE MARKET TIMING ALGORITHM TRIPLED MY PERFORMANCE),

Mad Hedge Technology Letter

January 23, 2019

Fiat Lux

Featured Trade:

(WHY TECH IS FLEEING SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

When did Marc Benioff become a real estate agent?

That is the main takeaway from the interview he gave to the world from the annual powerful people conference in Davos, Switzerland.

During the interview, he cut straight to the chase and described the cocktail of negative unintended consequences that the tsunami of tech profits has spawned.

His thesis, though not new, parlayed admirably with Bridgewater Associates Founder Ray Dalio interview in chronicling an economic landscape in which geopolitical turmoil finally catches up meaningfully with the movement of tech shares because of the underlying threat to influence concrete economic policy moving forward.

Why is he a real estate seller?

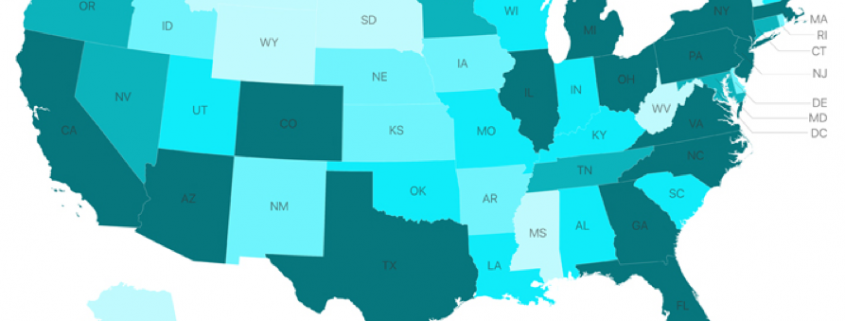

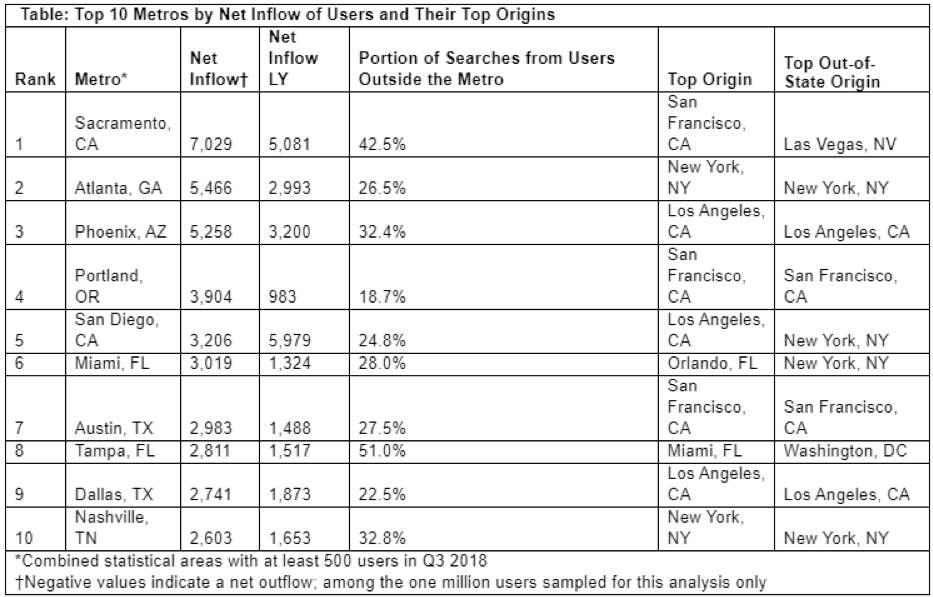

Well, he might as well be one in second-tier cities with copious amounts of tech talent such as Austin, Nashville, Sacramento, Atlanta, and Portland because these metro areas are about to experience a wild ride in the property market rollercoaster.

Benioff just added fuel to this fire.

The robust housing demand, lack of housing supply, mixed with the avalanche of inquisitive tech money will propel these housing markets to new heights and this phenomenon is happening as we speak.

Benioff lamented that San Francisco, where ironically he is from, is a diabolical “train wreck” and urged fellow tech CEOs to “walk down the street” and see it with their own eyes to observe the numerous homeless encampments dotted around the city limits.

The leader of Salesforce doesn’t mince his words when he talks and beelines to the heart of the issues.

After relinquishing some of his CEO duties to newly anointed Co-CEO Keith Block, Benioff will have the operational time and a wealth of resources to get on top of the pulse of not only tech issues but bigger picture stuff and he now has a mouthpiece for it with Time magazine which he and his wife recently bought.

In condemning large swaths of the beneficiaries of the Silicon Valley ethos, he has signaled that it won’t be smooth sailing for the rest of the year in tech wonderland, and he urged companies to transform their business model if they are irresponsible with user data.

The tech lash could get messier this year because companies that go rogue with personal data will face a cringeworthy reckoning as the tech lash fury seeps into government policy and the social stigma worsens.

I have walked around the streets of San Francisco myself. Places around Powell Bart station close to the Tenderloin district are eyesores. South of Market Street isn’t a place I would want to barbecue on a terrace either.

Summing it up, the unlimited tech talent reservoir that Silicon Valley gorged on isn’t flowing anymore because people don’t want to live there now.

This tech talent, equipped with heart-tugging stories from siblings and anecdotes from classmates getting shafted by the San Francisco dream, has recently put the Bay Area in the rear-view mirror for many who would have stayed if it were 20 years ago.

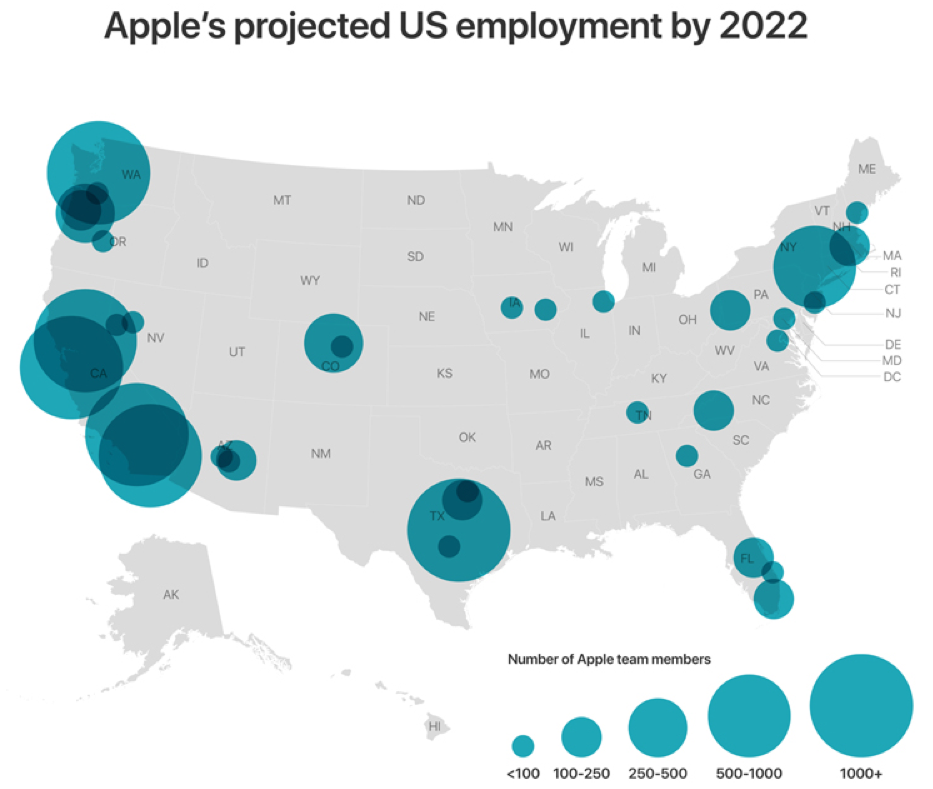

This is exactly what Apple’s $1 billion investment into a new tech campus in Austin, Texas and Amazon adding 500 employees in Nashville, Tennessee are all about. Apple also added numbers in San Diego, Atlanta, Culver City, and Boulder just to name a few.

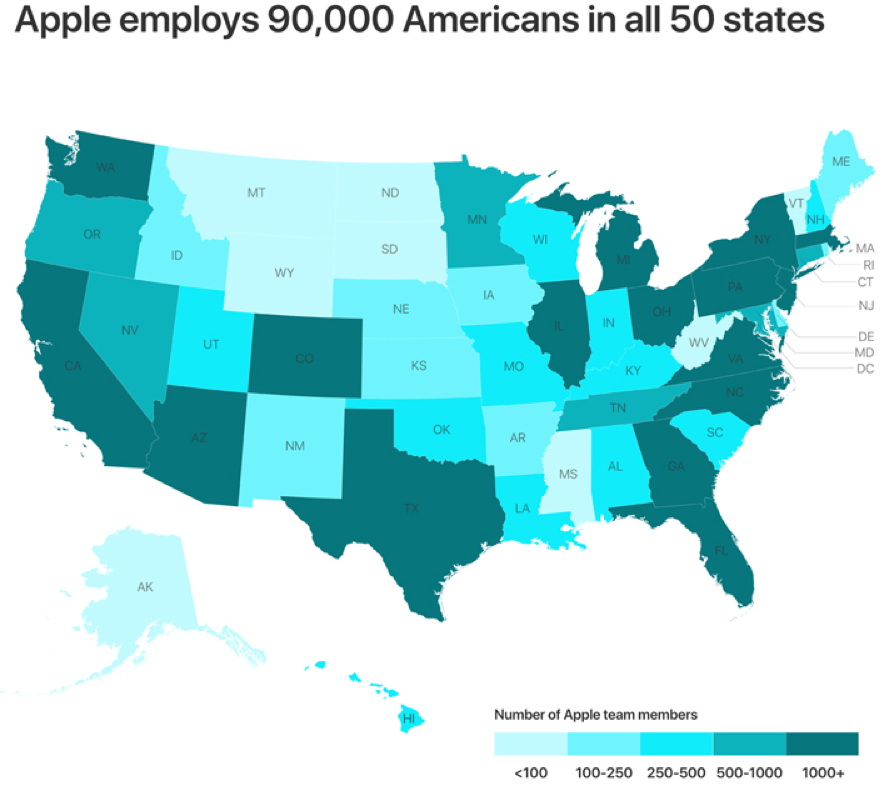

Apple currently employs 90,000 people in 50 states and is in the works to create 20,000 more jobs in the US by 2023.

Most of these new jobs won’t be in Silicon Valley.

Since the tech talent isn’t giddy-upping into Silicon Valley anymore, tech firms must get off their saddle and go find them.

The tables have turned but that is what happens when the heart of western tech becomes unlivable to the average tech worker earning $150,000 per year.

I also mind you that these external forces have nothing to do with pure technology, pure technology improves with each iteration and gaps up with each revolutionary idea.

That will not change.

Driving out young people who envision a long-term future elsewhere than the San Francisco Bay Area forces Silicon Valley to adapt to the new patterns revealing themselves.

Sacramento has experienced a dizzying rise of newcomers from the Bay Area itself.

Some are even commuting, making that 60-mile jaunt past Davis, but that will give way to entire tech operations moving to the state capitol.

Millennials are reaching that age of family formation and they are fleeing to places that are affordable and possible to become a new home buyer.

These are some of the practical issues that tech has failed to embrace and to maintain the furious pace of growth that investors' capricious expectations harbor.

Silicon Valley will have to become more practical adding a dash of empathy as well instead of just going by the raw and heartless data.

We aren’t robots yet, and much of the world still augurs to emotional decisions and disregards the empirical data.

My favorite tech companies are not only saying the right things but are doing the right things as well.

Microsoft (MSFT) just laid down a marker promising $500 million to build more affordable housing in Seattle.

Sustainability does not only mean building a sustainable business model on the balance sheet, but this definition is growing to be inclusive of upholding the stability and long-term prospects of a local area.

Microsoft has put the trust in its products at the fore of their business model.

Each time CEO of Microsoft Satya Nadella interviews, he preaches about the universal trust that consumers possess in Microsoft.

He is not off on his claims and Microsoft is riding this mantra all the way to the bank while sidestepping regulatory scrutiny.

Nadella is always smartly one step ahead.

All this screams going long Microsoft by buying the dips.

Sell the rallies in the names that have a crisis of trust such as Facebook (FB) and Google (GOOGL).

I was recently gouged $250 on my monthly phone bill by Google because of a technicality from cell phone service Google Fi.

All a specialist said was that according to the data, I should be charged almost as if I should be shamed for even questioning their business model.

Not only that, the best and brightest from Stanford, University of California at Berkeley, and Ivy league schools do not want to work for Facebook and Google anymore.

These brands have been tainted.

The result will be needing to overpay to secure the able forces needed to pursue growth and success.

Not only that, upper management has left in droves “pursuing new opportunities.”

Google is also grappling with an Apple problem - no new innovative products and it’s yet to be seen if Waymo, the autonomous driving business, can be that solid growth driver going forward.

As the economy creeps closer and closer to the end of the cycle, investors won’t be willing to drain money down some loss-making outfit in the name of growth.

Therefore, software companies based on innovation fused with stable profits will be the go-to formula in tech investing in 2019 and Amazon (AMZN), Salesforce (CRM), and Microsoft (MSFT) are ahead of the curve.

Don’t get me wrong - Silicon Valley is still alive and kicking.

But, instead of physical offices being planted in the Bay Area, the tech industry will give way to the “spirit” of Silicon Valley with offices in far-flung places.

And remember that all of these new tech talent strongholds will need housing, and housing that an IT worker making $150,000 per year desires.

Global Market Comments

January 23, 2018

Fiat Lux

Featured Trade:

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT SPREADS), (TLT)

(WHY TECHNICAL ANALYSIS DOESN’T WORK)

(FB), (AAPL), (AMZN), (GOOG), (MSFT), (VIX)