Mad Hedge Technology Letter

October 31, 2018

Fiat Lux

Featured Trade:

(IBM’S PUTS ON A RED HAT)

(RHT), (IBM), (AMZN), (MSFT), (GOOGL), (ORCL)

Mad Hedge Technology Letter

October 31, 2018

Fiat Lux

Featured Trade:

(IBM’S PUTS ON A RED HAT)

(RHT), (IBM), (AMZN), (MSFT), (GOOGL), (ORCL)

What took you so long, Ginni?

That was my first reaction when I heard International Business Machines Corporation (IBM) was making a big strategic shift by purchasing open source cloud company Red Hat (RHT) in a landmark $34 billion deal.

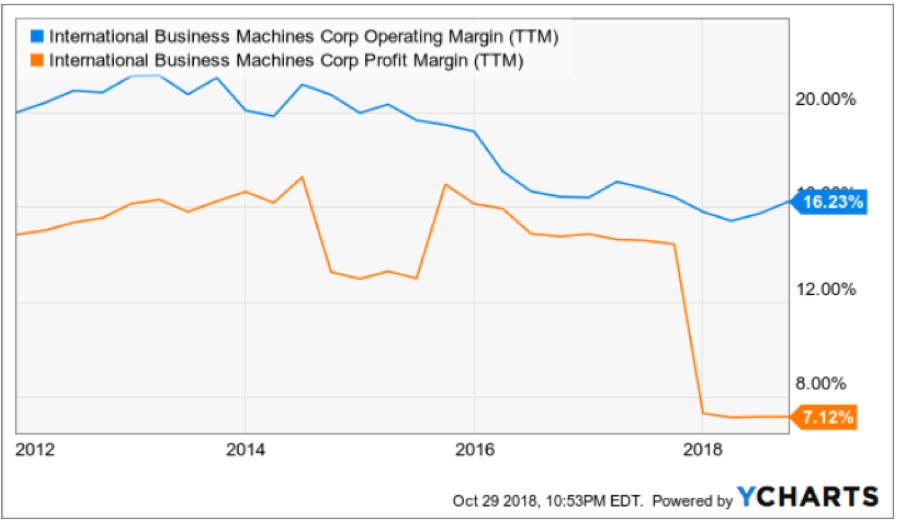

Ginni Rometty, IBM’s CEO since 2012, has presided over persistent negative sales growth and has done zilch for investors to conjure up some type of lasting hope for this company.

Not only has Rometty failed to grow the top line, but with an underwhelming 3-year EPS growth rate of -2%, the execution and performance haven’t been there as well.

Somehow and someway, she has maintained an iron-clad grip on her job at the helm of IBM and her legacy at IBM will be wholly determined by the failure or success of this Red Hat acquisition.

IBM shares sold off on the news as shareholders digested this bombshell.

Rometty took a hatchet to share buybacks and suspended them for 2020 and 2021 alienating a segment of their loyal shareholder base.

I can tell you one thing about this move – it smells of desperation and it won’t vault IBM into the conversation of Amazon (AMZN) Web Services or the Microsoft (MSFT) Azure.

The biggest winner of this deal is Red Hat’s CEO Jim Whitehurst who has been dangling the company for sale for a while.

Alphabet (GOOGL) was in the mix and had the opportunity to snag a last-second deal, but it never came to fruition.

The 63% premium IBM must pay for a company who only grew quarterly sales 14% YOY and quarterly EPS by 10% is expensive, but that is where we are with IBM.

Clearly overpaying was better than doing nothing at all.

IBM continues to hemorrhage sales and stopping the blood flow is the first step.

Rometty was responsible for the utter failure of artificial intelligence initiative Watson whose terrible management was a key reason for its implosion.

Analyzing this historic company gave me insight into the pitiful causing me to write a bearish story on IBM last month. To read that story, please click here.

Not only was the agreed price exorbitant, but Red Hat’s stock was trending south even before the interest rate induced sell-off rocked the tech sector of late.

Red Hat missed on sales revenue forecasts and offered weak guidance.

It could be the case that Whitehurst was actively seeking a buyer because he felt that Red Hat would go ex-growth in the next few years.

Red Hat was rumored to be on the market for quite a while looking to fetch a premium price for a company starting to stagnate with its visions of grandeur growth.

Rometty’s career-defining moment is high-risk and high-reward and is born out of being cornered by leading tech companies leaving IBM in their dust.

The deal finally allows IBM to return back to sales growth which will occur two years later, and Rometty will finally have that monkey off her back for now.

But the bigger question is will Rometty still have her job in two years if this experiment becomes toxic.

My guess is that Red Hat CEO Jim Whitehurst is automatically the next in line for the IBM throne if Rometty missteps, and piling on pressure will force IBM to evolve or die out.

And even though they will return back to growth, 2% growth is no reason to do cartwheels over.

The real work starts now and it will take years to turn around this dinosaur.

On the brighter side, the massive deals instantly improve sentiment that was flagging for years and puts IBM back on the map.

The synergies between IBM and Red Hat could be robust.

Red Hat can surely help IBM become a higher-quality hybrid cloud solutions company.

Models like this are the industry standard as luring a company into your cloud is one thing, but being able to cross-sell a plethora of extra add-on software services in the cloud is the necessary path to raising profitability.

IBM also inherits a slew of talented software engineers that it can mobilize for innovative cloud products. Red Hat’s products such as JBoss middleware and the OpenShift software for deploying applications in virtual containers could make IBM’s hybrid cloud more appealing and could help retain customers with the additional offerings.

Doubling down on the software side of the business was a strategy I pinpointed at the Mad Hedge Lake Tahoe conference and deals like this highlight the value of this type of assets.

There is a hoard of legacy tech companies like Oracle (ORCL) that is in dire need of such strategic injections and fresh ideas.

This won’t be the last deal of 2018, other cloud deals could shortly follow.

On the other side of the coin, hardware deals have turned rotten quickly with stark examples such as Hewlett-Packard’s (HPQ) $25 billion acquisition of Compaq, Microsoft’s $7.2 billion disastrous buy of Nokia’s mobile handset business and Google’s unimpressive $12.5 billion deal for Motorola Mobility that they later unloaded to Chinese PC company Lenovo.

Investors must be patient if IBM has any chance of completing this turnaround.

Listening to Rometty talk about this deal clearly reveals that she is hyping it up for something way bigger than it actually is.

Let’s not forget that Rometty’s tenure as CEO began in 2012 when IBM shares were trading north of $200 and she has presided over the company while the stock got pulverized by almost 30%.

It pains me that she is the one given the chance to turn the company around after years of underperformance.

Let’s not forget that at the end of 2017, IBM only had a 1.9% share of the cloud infrastructure, about 25 times smaller than Amazon Web Services.

The costly nature of the deal could also put a dent into IBM’s dividend, alienating another swath of its hardcore shareholder base.

Historically, IBM has had minimal success with transformative M&A and the industry competitors dominating IBM magnify the poor management performance headed by Rometty.

Rometty declaring that this deal means IBM will be “no. 1 in hybrid cloud” is overly optimistic, but this is a move in the right direction and could keep IBM spiralling out of control.

A return to sales growth might help stem the bleeding of its downtrodden share price, but Amazon and Microsoft are too far ahead to catch.

Investors will need to wait and see if the synergies between IBM’s and Red Hat’s products are meaningful or not.

Global Market Comments

October 23, 2018

Fiat Lux

Featured Trade:

(WATCH OUT FOR THE UNICORN STAMPEDE IN 2019),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

(A NOTE ON OPTIONS CALLED AWAY), (MSFT)

Mad Hedge Technology Letter

October 23, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

With stock market volatility greatly elevated and trading volumes through the roof, there is a heightened probability that your short options position gets called away.

If it does, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money call option spread, it contains two elements: a long call and a short call. The short called can get assigned, or called away at any time.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it.

The 5:30 AM phone call was as shrill as it was urgent.

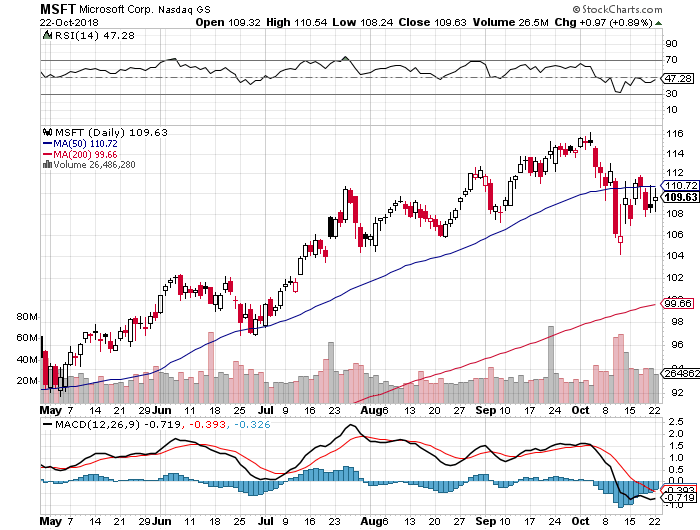

A reader had employed one of my favorite strategies, buying the Microsoft (MSFT) November 2018 $90-$95 in-the-money vertical call spread at $4.50.

He had just received an email from his broker informing him that his short position in the (MSFT) November $95 calls was assigned and exercised against him.

He asked me what to do.

I said, “Nothing.”

For what the broker had done in effect is allow him to get out of his call spread position at the maximum profit point 20 days before the November 16 expiration date.

All he had to do was call his broker and instruct him to exercise his long position in his November $90 calls to close out his short position in the $95 calls.

Calls are a right to buy shares at a fixed price before a fixed date, and one option contract is exercisable into 100 shares.

In other words, he bought (MSFT) at $90 and sold it at $95, paid $4.50 cents for the right to do so, his profit is 50 cents, or ($0.50 X 100 shares X 22 contracts) = $1,100. Not bad for a nine-day limited risk play.

Sounds like a good trade to me.

Weird stuff like this happens in the run-up to options expirations.

A call owner may need to sell a long stock position right at the close, and exercising his long November $95 calls is the only way to execute it.

Ordinary shares may not be available in the market, or maybe a limit order didn’t get done by the stock market close.

There are thousands of algorithms out there which may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, calls even get exercised by accident. There are still a few humans left in this market to blow it.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it.

This generates tons of commissions for the broker but is a terrible thing for the trader to do from a risk point of view, such as generating a loss by the time everything is closed and netted out.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many ways to steal money legally that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Global Market Comments

October 22, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or HEADING FOR LAKE TAHOE),

(SPY), (TLT), (VIX), (MSFT), (AMZN), (CRM), (ROKU),

(BRING BACK THE UPTICK RULE!)

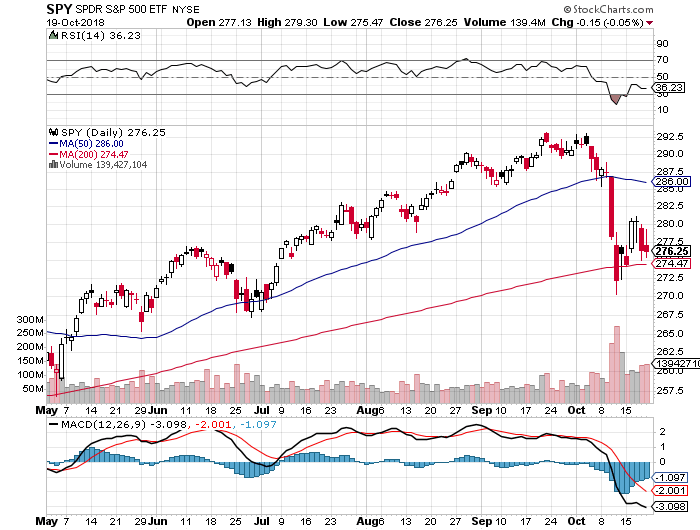

There’s nothing like a quickie five-day tour of the Southeast to give one an instant snapshot of the US economy. The economy is definitely overheating and could blow up sometime in 2019 or 2020.

Traffic everywhere is horrendous as drivers struggle to cope with a road system built to handle half the current US population. Service has gotten terrible as workers vacate the lower paid sectors of the economy. Everyone you talk to tells you business is great, from the CEOs down to the Uber drivers.

I managed to miss Hurricane Michael by two days. Hartsfield Jackson Atlanta International Airport was busy with exhausted transiting Red Cross workers. The Interstate from Savanna to Atlanta, Georgia was lined with thousands of downed trees. In Houston mountains of debris were evident everywhere, the rotting, soggy remnants of last year’s Hurricane Harvey.

I managed to score all day parking in downtown Atlanta for only $8. I kept the receipt to show my disbelieving friends at home.

Bull markets climb a wall of worry and this one has been no exception. However, the higher we get the greater the demands on the faithful.

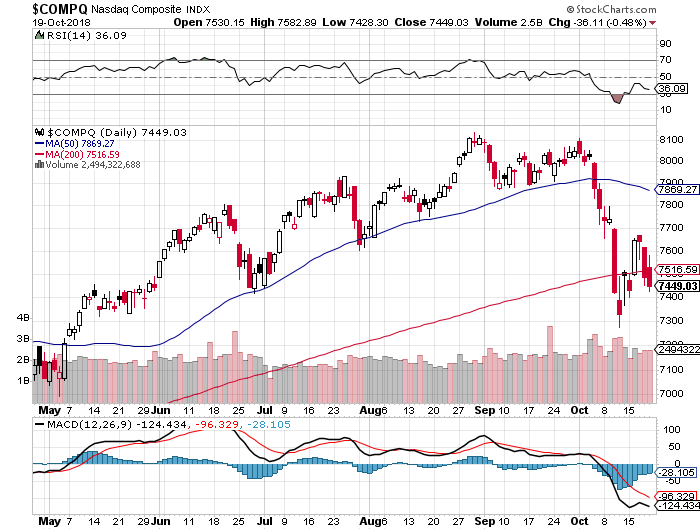

Last week saw my Mad Hedge Market Timing Index plunge to an all-time low reading of 4. I back-tested the data and was stunned to discover that October saw the steepest selloff since the 1987 crash, which saw the average crater 21% in one day.

And while evidence of a coming bear market is everywhere, the reality is that stocks can keep rising for another year. Market bottoms are easy to quantify based on traditional valuation measure, but tops are notoriously difficult to call. Look for one more high volume melt up like we saw in January and that should be it.

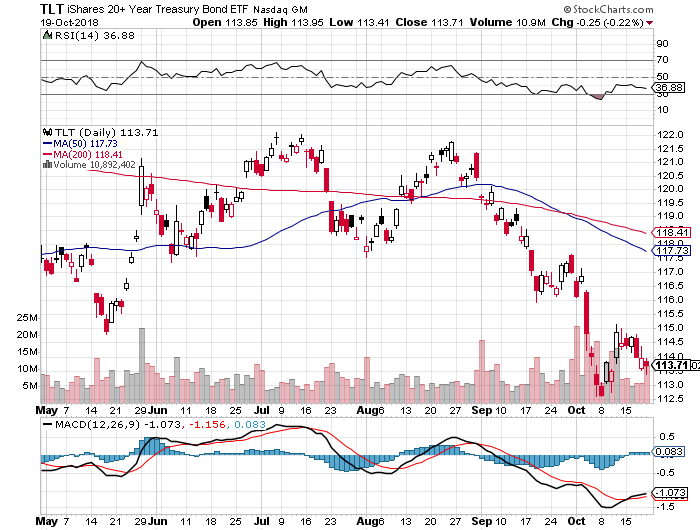

Real interest rates are still zero (3.2% bond yields – 3.2% inflation), so there is no way this is any more than a short-term correction in a bull market.

The world is still awash in liquidity

The Fed says they’re still raising rates four times in a year no matter what the president says. Look for a 3.25% overnight rate in a year, and 4% for three months funds. If inflation rises to 4% at the same time, real rates will still be at zero.

There certainly has not been a shortage of things to worry about on the geopolitical front. After Saudi Arabia was caught red-handed with video and audio proof of torturing and killing a Washington Post reporter, it threatened to cut off our oil supply and dump their substantial holding of technology stocks.

Tesla made another move towards the mass market by accelerating its release of the $35,000 Tesla 3. Production is now well over 6,000 units a month.

If you had any doubts that housing was now in recession, look no further than the September Existing Home Sales which were down a disastrous 3.5%. In the meantime, the auto industry continues to plumb new depths. In some industries, the recession has already started.

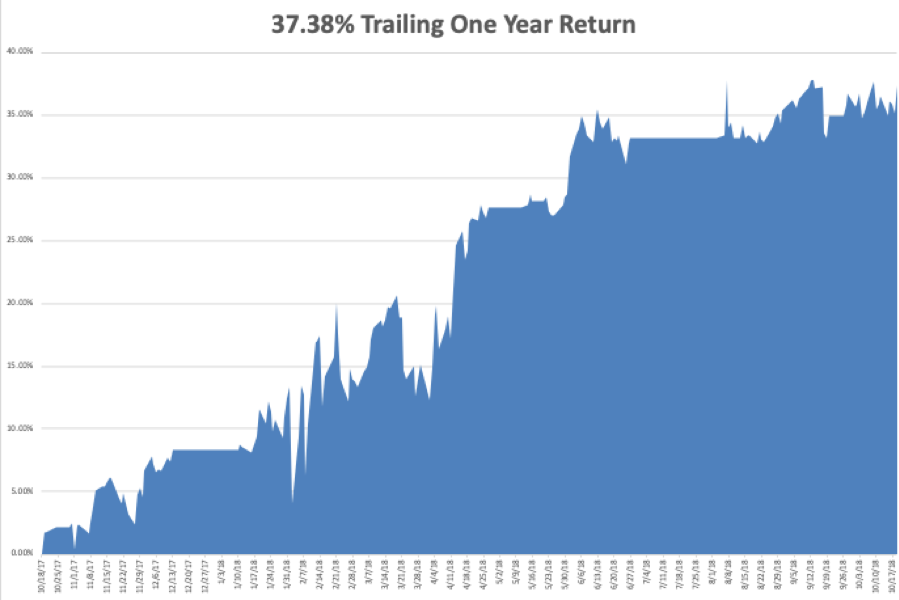

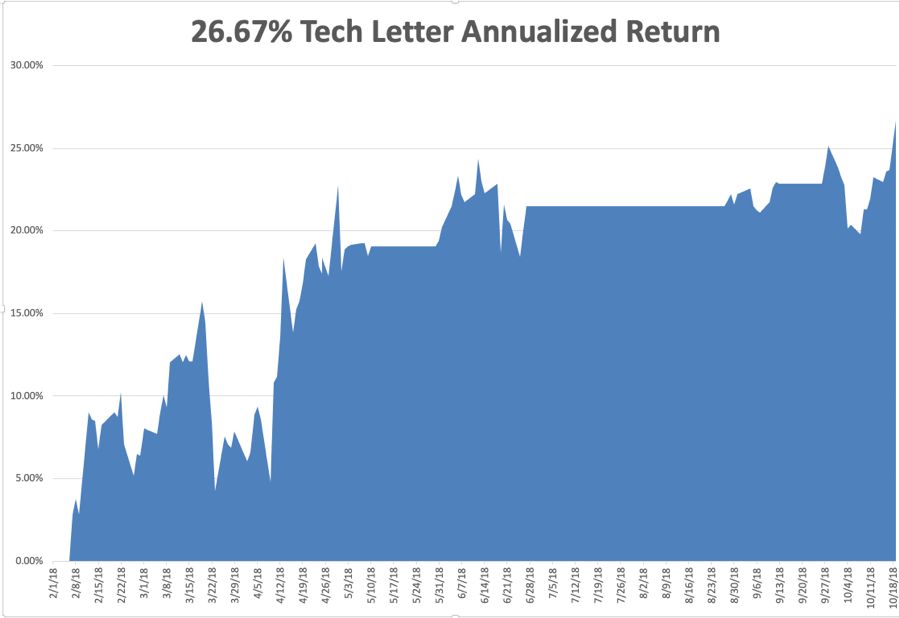

We have been killing it on the trading front. My 2018 year-to-date performance has bounced back to a robust 29.07%, and my trailing one-year return stands at 35.37%. October is up +0.68%, despite a gut-punching, nearly instant NASDAQ swoon of 10.50%. Most people will take that in these horrific conditions.

My single stock positions have been money makers, but my short volatility position (VXX), which I put on early, refuses to go down, eating up much of my profits.

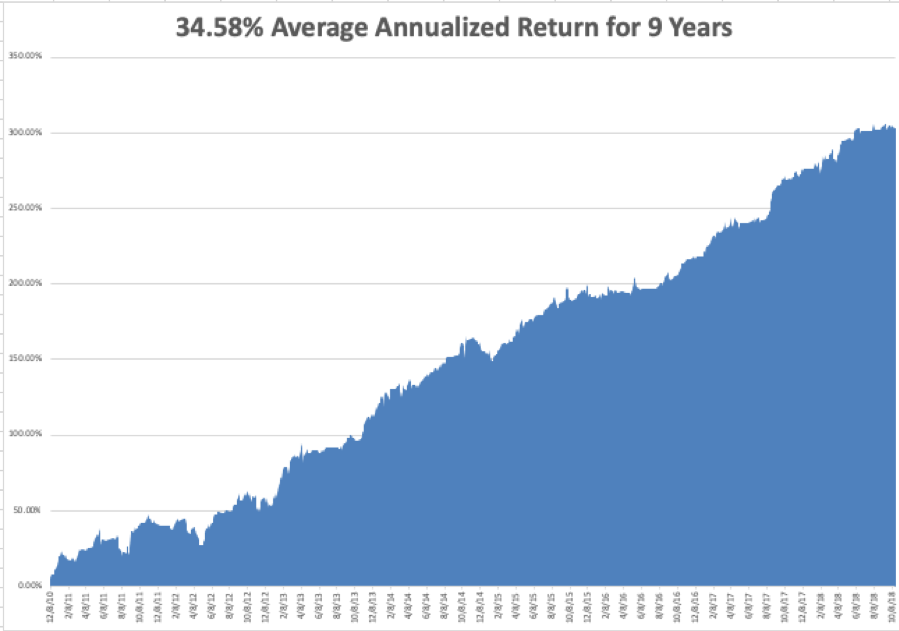

My nine-year return appreciated to 305.54%. The average annualized return stands at 34.58%. Global Trading Dispatch is now only 44 basis points from an all-time high.

The Mad Hedge Technology Letter has done even better, blasting through to a new all-time high at an annualized 26.67%. It almost completely missed the tech meltdown and then went aggressively long our favorite names right at the market bottom.

I’d like to think my 50 years of trading experience is finally paying off, or maybe I’m just lucky. Who knows?

This coming week will be pretty sedentary on the data front, with the Friday Q3 GDP print the big kahuna. Individual company earnings reports will be the main market driver.

Monday, October 22 at 8:30 AM, the Chicago Fed National Activity Index is out. 3M (MMM), and Logitech (LOGI) report.

On Tuesday, October 23 at 10:00 AM, the Richmond Fed Manufacturing Index is published. Juniper Networks (JNPR), Lockheed Martin (LMT), and United Technologies report.

On Wednesday, October 24 at 10:00 AM, September New Home Sales will give another read on entry-level housing. At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report. Advanced Micro Devices (AMD), Ford Motor (F), and Microsoft (MSFT) report.

Thursday, October 25 at 8:30, we get Weekly Jobless Claims. Alphabet (GOOGL) and Intel (INTC) report.

On Friday, October 26, at 8:30 AM, a new read on Q3 GDP is announced.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I am headed up to Lake Tahoe this week to host the Mad Hedge Lake Tahoe Conference. The weather will be perfect, the evening temperatures in the mid-twenties, and there is already a dusting of snow on the high peaks. The Mount Rose Ski Resort is honoring the event by opening this weekend.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 19, 2018

Fiat Lux

Featured Trade:

(LAST CHANCE TO BUY TICKETS NOW FOR THE MAD HEDGE LAKE TAHOE CONFERENCE FOR OCTOBER 26-27)

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT)

Mad Hedge Technology Letter

October 18, 2018

Fiat Lux

Featured Trade:

(UNDERSTANDING THE REAL COMPETITION),

(SPOT), (AAPL), (GOOGL), (MSFT), (HUAWEI)

Microsoft sells computers?

That was the bizarre look I got after telling my friend that Microsoft (MSFT) is in the business of selling laptops, desktop computers, and tablets that convert into laptops from a product line called Microsoft Surface.

This is not your father’s Microsoft.

Things are different now.

Everything changed once they got rid of Steve Ballmer whose inertia prevented Microsoft from taking advantage of the huge influence they culled in the tech sector from being the universal operating system for PCs.

Ballmer’s lack of technical expertise was his own downfall stemming from his terrible decision to buy Nokia’s handset business for $7.6 billion.

The board of directors forced him out and was a blessing in disguise.

Thousands were laid off in the Nokia handset division and a massive write-down was taken.

As big tech spread out their wings and branch off into various businesses they never imagined before, they have reinvented the former images of themselves.

This goes for Microsoft who’s taking their legacy business of Microsoft Office and Windows and leveraging it with the cloud to create a stellar product.

And with the cash hoard, not only are they creating new products by fusing together old products with new technologies, they are overlapping into other big tech companies’ turf.

The overlapping products can be seen in hardware products made by this software behemoth and their neighbors.

The Microsoft Surface division is up 25% YOY speaking volumes to the quality hardware Microsoft produce now even if you didn’t know about it.

Apple (AAPL) has attracted most of the conversation in the "smart" headphones space because of the AirPods.

The sleek white earbuds are becoming ubiquitous with the headphone space trending to a smaller and "true" wireless.

A schism has formed as the AirPods don’t satisfy the entire spectrum of smart headphone fans.

The retro ear-muff shaped headphone with more immersive sound is what I am talking about, and I do recognize that Beats has been in the market for a decade.

Microsoft chose to go this route with their smart headphones and this is their answer to the iconic AirPods and the Google (GOOGL) Pixel Buds.

This smart headphone comes with an embedded digital assistant and integrates noise cancellation.

I tried out the Microsoft's Surface Headphones before they came on the market, and I only had positive things to say about the quality and experience.

They sound impressive, the controls are easy to use, and the modern design is definitely a plus.

The color could use a little reimagination but all in all, I was pleased.

Microsoft Cortana, Microsoft’s digital assistant, for all who don’t know, is also slipped into the experience and a tap on the right earcup will summon Cortana.

It seems that Microsoft still needs a few kinks to work out with Cortana, but voice activation and smart assistants like Siri and Google Assistant can be found in almost every hardware and software product now.

Headphones are city workers’ second most important smart device because of its functionality.

Have you ever been on the New York metro and seen how many people are wearing smart headphones?

Quality headphones shut off the outside world and warm up the insides with the user’s favorites on Spotify (SPOT) or Apple Music.

Stressing out on the commute into work in an Uber is common and calming the frayed nerves before workers enter into the office of dungeons and dragons has a type of value that can never be replicated.

Urban dwellers need high-quality smart headphones and these big tech companies are acutely aware of this.

Google has made an audacious attempt to integrate real-time foreign translation into the Pixel Buds. It only works with Google’s Pixel phones, is hard to operate, and needs the Google Translate app on the phone.

It’s a good first step but the applications using smart headphones are endless.

Smart assistants are the key.

As they become more adept at processing the real world, they streamline and better a human’s life.

Microsoft’s smart headphones have embedded Skype, one of Ballmer’s positive acquisitions during his tenure. And with Cortana integration, it could morph into a natural extension of the Windows 10 experience.

Microsoft’s smart headphones morph into a point of conversion for more of Microsoft’s hardware products as they start to construct an expanding moat.

Headphones used to be more or less the same.

Plug it into the jack and you’re on your merry way.

The headphones of today are looking more different from each other with every iteration.

This was glaringly evident when Apple chose to no longer sell any phones with a 3.5mm headphone jack.

Ironically enough, Google dumped the headphone jack with its Pixel 2 phones a year later even though they bashed Apple for it a few months earlier.

The reason was mainly functional as Google said, “We want the display to go closer and closer to the edge.”

Gradually, smartphones will get rid of everything except a razor-thin screen. All the other clunky business in and around it needs to go. This is the first step and home buttons have been chopped off smartphones as well.

It is fine to get consumed in the battle of smart products between Silicon Valley companies, but there is a larger threat.

Chinese smart products are rapidly catching up to what American companies can produce.

The Middle Kingdom hasn’t surpassed American tech expertise yet but they are debuting devices relative to the competition that could only be dreamed about a few years ago.

Huawei's flagship smartphone Mate 20 and Mate 20 Pro pack a lot of punch and this must be frightening to the FANGs.

The timing of the phone debut is a big victory for American smartphone companies because this phone is good enough to grab market share from existing American companies but aren’t allowed to sell inside America.

Congress putting the kibosh on any sliver of a chance to partner with an American carrier means that there will be no chance of Chinese phones gutting the American smartphone market.

What it does mean is that they will invade and dominate other markets such as South East Asia, Eastern Europe, and Russia.

The same will go for any Chinese smart device.

Huawei has given up trying to circumvent the government blockade.

The Huawei Mate 20 is priced around $800 and the Mate 20 Pro at $1140. They are probably two of the best smartphones ever made and are a direct threat to any American company’s revenue that manufactures smartphones and smart devices.