Global Market Comments

March 23, 2023

Fiat Lux

Featured Trade:

Trade Alert - (UNG) LEAPS – BUY

(UNG), ($NATGAS), (BOIL)

CLICK HERE to download today's position sheet.

Global Market Comments

March 23, 2023

Fiat Lux

Featured Trade:

Trade Alert - (UNG) LEAPS – BUY

(UNG), ($NATGAS), (BOIL)

CLICK HERE to download today's position sheet.

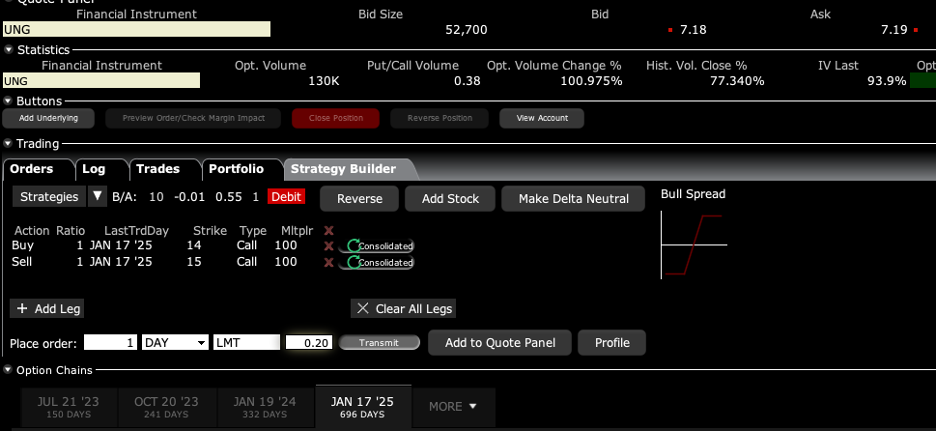

BUY the United States Natural Gas Fund (UNG) January 2025 $14-$15 deep out-of-the-money vertical Bull Call debit spread LEAPS at $0.25 or best

Opening Trade

3-23-2023

expiration date: January 17, 2025

Number of Contracts = 1 contract

Natural gas has just given up its entire recent gain. Forecasts of mild spring weather and recession fears are the reasons. So I am diving back in.

Natural gas at one point fell some 80% since it peaked in June of 2022. It is now down so much that you have to buy it even if you hate it.

The much-predicted nuclear winter in Europe never showed. Instead, the continent enjoyed one of the warmest winters on record, with some ski resorts completely devoid of snow. To save Europe’s bacon, the US government ordered the diversion of dozens of natural gas carriers from China to Europe. The Middle East also ramped up its gas exports.

Now, we have recession fears. Storage in both Europe and the US is near all-time highs.

What happens next is that Covid burns out in China, allowing the economy to recover and sending the demand for natural gas through the roof. The Freeport McMoRan’s export facility in Quintana, TX that blew up a few months ago is coming back on stream.

That screeching sound you hear is natural gas wells being shut down, which happens every time we approach the $2.00 price in gas. That is sowing the seeds of the next shortage. That sets up an easy double for gas from here. While gas may not yet have hit its final bottom, it is close enough to do a trade here.

While the chance of winning a real lottery is something like a million to one, this one is more like 10:1 in your favor. And the payoff is 300% in a little less than two years. That is the probability that (UNG) shares will rise over the next 23 months.

I have been through a half dozen energy cycles in my lifetime, and I can see another one starting up.

I am therefore buying the United States Natural Gas Fund (UNG) January 2025 $14-$15 deep out-of-the-money vertical Bull Call debit spread LEAPS at $0.25 or best.

Don’t pay more than $0.50 or you’ll be chasing on a risk/reward basis.

I think all carbon energy sources eventually go to zero over the next 20 years as they are replaced by alternatives, but we will have several doubles in price on the way there. This is one of those doubles.

But don’t ask me. I only drilled for natural gas in Texas and Colorado for five years in the late 1990s using a revolutionary new technology called “fracking.” I moved on after making a fortune, buying gas for $2 and selling it for $6 or $7.

To learn more about the United States Natural Gas Fund (UNG), please click here.

Please note that these options are illiquid, and it may take some work to get in or out. Executing these trades is more an art than a science.

Let’s say the United States Natural Gas Fund (UNG) January 2025 $14-$15 deep out-of-the-money vertical Bull Call debit spread LEAPS are showing a bid/offer spread of $0.10-$0.90, which is typical.

Enter an order for one contract at $0.10, another for $0.20, another for $0.30 and so on. Eventually, you will enter a price that gets filled immediately. That is the real price. Then enter an order for your full position at that real price.

A lot of people ask me about the appropriate size. Remember, if the (UNG) does NOT rise by 85.9% in 23 months, the value of your investment goes to zero.

If by chance (UNG) rises quickly, which it might, you don’t have to wait the full two years. You can take profits at any time.

The way to play this is to buy LEAPS in ten different companies. If one out of ten increases ten times, you break even. If two of ten work, you double your money, and if only three of ten work you triple your money.

You never should have a position that is so big that you can’t sleep at night, or worse, need to call John Thomas asking if you should sell at a market bottom.

Keep in mind that (UNG) has a substantial “contango” of 35% to overcome. That means the futures one year out are selling at a 35% discount. So, gas has to rise by 35% in a year for you just to break even. The contango covers gas storage charges and the cost of carry for borrowed money.

Notice that the day-to-day volatility of LEAPS prices is miniscule since the time value is so great. This means that the day-to-day moves in your P&L will be small. It also means you can buy your position over the course of a month just entering new orders every day. I know this can be tedious but getting screwed by overpaying for a position is even more tedious.

Look at the math below and you will see that an 85.9% rise in (UNG) shares to $15 will generate a 300% profit with this position, such is the wonder of LEAPS. That gives you an implied leverage of 3.5:1 across the $14-$15 space.

I have done the math here for a single contract. You can adjust your size accordingly.

If you want to get much more aggressive on the natural gas trade, you can buy the ProShares Ultra Natural Gas ETF (BOIL), a 2X long leveraged ETF. Keep in mind that 2X ETFs have much higher costs, wider dealing spreads, and greater tracking errors. This is really designed for short-term or even day trading. (BOIL) is down a staggering 97% from its June high.

Only use a limit order. DO NOT USE MARKET ORDERS UNDER ANY CIRCUMSTANCES. Just enter a limit order and work it.

This is a bet that the (UNG) will not fall below $15 by the January 17, 2025 options expiration in 23 months.

Here are the specific trades you need to execute this position:

Buy 1 January 2025 (UNG) $14 call at…………...……$2.60

Sell short 1 January 2025 (UNG) $15 call at…………$2.35

Net Cost:…………………...……….………..………….….....$0.25

Potential Profit: $1.00 - $0.25 = $0.75

(1 X 100 X $0.75) = $75, or 300% in 23 months.

To see how to enter this trade in your online platform, please look at the order ticket below, which I pulled off of Interactive Brokers.

If you are uncertain on how to execute an options spread, please watch my training video on “How to Execute a Vertical Bull Call Debit Spread” by clicking here.

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep in-the-money spread trades can be enormous.

Don’t execute the legs individually or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

Global Market Comments

October 8, 2021

Fiat Lux

Featured Trade:

(OCTOBER 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(FCX), (TSLA), (BLK), (MS), (JPM), ($NATGAS), (UNG), (BIDU), (MRNA), (COIN), (ROM), ($BTCUSD), (ETHE), (FB), (DAL), (ALK), (LUV) (MSTR), (BLOK), (V), (NVDA), (SLV), (TLT), (TBT)

Below please find subscribers’ Q&A for the October 6 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

Q: When will Freeport McMoRan (FCX) go up?

A: When the China real estate crisis ends, and they start buying copper again to build new apartment buildings.

Q: Do rising interest rates imply trouble for tech?

A: Yes, they do, but only for the short term. Long term, these things all double on a three-year view; and the next rise up in tech stocks will start when interest rates peak out, probably with 10-year yields at 1.76% or 2.00%. The great irony here is that all the big techs profit from higher rates because they have such enormous cash flows and balances. But that is just how markets work.

Q: I know you’ve been promoting Tesla (TSLA) for a very long time. What do you think about it here?

A: We’ve just gone from $550 to over $800. It actually has been one of the best performing stocks in the market for the past four months. Short term, you want to take profits; long term you want to hold it because it could go up 10 times from the current level. They just broke all their sales records and are the fastest growing car company in the US or Europe.

Q: If Blackrock (BLK) is reliant on interest rates, will the rise in interest rates hurt them?

A: No, it’s the opposite. Rising interest rates are positive for Blackrock because it improves the return on their investments, which they get a piece of; so rising interest rates mean more money and more fees. That's why I own it— it is a rising interest rate play, not a falling interest rate play.

Q: What do you think about Baidu (BIDU)?

A: Stay away from all China trades right now, it’s uninvestable. Not only do I not know what the Chinese are going to do next—they seem to be attacking a new industry every week—but the Chinese don’t even seem to know. This is all new to them; they had been embracing the capitalist model for the last 40 years and they now seem to be backtracking. There are better fish to fry, like Morgan Stanley (MS) and JP Morgan (JPM).

Q: Don’t you have a bear put spread on Baidu (BIDU)?

A: We did have a bear put spread on Baidu, but that's only a very short term, front month trade. It does look like it’s going to make money; but keep in mind those are high-risk trades.

Q: Could Natural Gas (UNG) trigger an economic crisis?

A: Not really. In the US, natgas is only a portion of our total energy needs, about 34%, and that’s mostly in the Midwest and California. The US has something like a 200-year supply with fracking. Plus, we’re on a price spike here—we’ve gone from $2 to $20/btu in Europe, entirely manipulated by Russia trying to get more money on their exports and more political control over Europe. So, it’s a short-term deal, and you can bet a lot of pros are out there shorting natgas like crazy right here. The real issue here is that no one wants to invest in carbon-based energy anymore and that is creating bottlenecks in the energy supply chain.

Q: How long will it take to provide EV infrastructure to mass gas station availability?

A: The EV infrastructure has in fact been in progress for 20 years, if you count the first generation of EV in the late 90s, which bombed. Tesla has been building power stations in the US for 10 years. They have 10,000 chargers now in 1,800 stations and their goal is 20,000 charging stations. In fact, most people already have the infrastructure for EV charging—you just charge them at home overnight, like I do. The only time I ever need a charge is when I go to Lake Tahoe. For gasoline engines, on the other hand, it took 20 years to build infrastructure from 1900 to 1920 to replace horses. Believe it or not, gasoline cars were the great environmental advance of the day, because it meant you could get rid of all the horses. New York City used to have 150,000 horses, and the city was constantly struggling through streets of two-foot-deep manure piles. So that was the big improvement. It only took 100 years to take the next step.

Q: The latest commodity with supply constraints I hear about is cotton. Is this all just a temporary thing and can we expect supply capacity to be back to normal next year? Is this just the failing of a just-in-time model that simply doesn’t work in the age of deglobalization?

A: We are losing possibly one third of our current economic growth due to part shortages, labor shortages, supply chain problems—those all go away next year, and that one third of economic growth just gets postponed into 2022 which means that the economic recovery is extended over a longer period of time, and so is the bull market in stocks, how about that! That’s why I’m loading the boat right here. It’s the first time I've been 100% invested since May.

Q: What do you think about the airlines here?

A: High risk, but high return play for the next year. Delta (DAL) is a play on business travel recovery. Alaska Airlines (ALK) and Southwest(LUV) are a play on a vacation travel return flying return, which has already started—we’re back to pre-pandemic TSA clearances at airports.

Q: Is Facebook (FB) a buy now?

A: No, I want to wait for the dust to settle before I go back in. I think it does recover and go to new highs eventually but will go to lower lows first. Regulation is certainly coming but we don’t know what.

Q: When will the chip shortage end?

A: Two years. My prediction is much longer than anybody else's because people are designing chips into new products like crazy. All predictions for the chip shortage to end in only a year don’t take that into account.

Q: When do we go into the (ROM) ProShares Ultra Technology long play?

A: When interest rates peak out sometime early next year. It’s probably a great entry point for tech; until then they go nowhere.

Q: Does the appetite for financials extend to Canada and their banks with higher dividends?

A: Yes, US and Canadian interest rates tend to move fairly closely so that rising rates here should be just as good for banks in Canada, and you might even be able to get them cheaper.

Q: Do you suggest we buy Altcoin?

A: No, not unless you're a Bitcoin professional like a miner, who can differentiate between all the different Altcoins. You can buy up to 100 different Altcoins on the main exchanges like Coinbase (COIN). In the crypto business, there is safety and size; that means Bitcoin ($BTCUSD) and Ethereum (ETHE), which between them account for about three quarters of all the crypto ever issued. A Lot of the smaller ones have a risk of going to zero overnight, and that has already happened many times. So go with the size—they’re less volatile but they’ll still go up in a rising market. And you should subscribe to our bitcoin letter just to get the details on how that market works.

Q: Target for Bitcoin by Christmas?

A: My conservative target is $66,000, but if we really go nuts, we could go as high as $100,000. That’s the “laser eyes” target for a lot of the early investors.

Q: Suggestions for a Crypto ETF?

A: It’s not out yet but will be shortly. I think that Crypto will run like crazy in anticipation of the Bitcoin ETF that we don’t have yet.

Q: Should I buy Moderna (MRNA) on this dip at 320 down from 400, or is this a COVID revenue flash in the pan that won’t come back?

A: It’ll come back because they’re taking their COVID technology and applying it to all other human diseases including cancer, which is why we got in this thing two years ago. But we may have to find a lower low first. So I would wait on all the drug/biotech plays which right now are getting hammered with the demise of the delta virus.

Q: What’s your favorite ETF right now?

A: Probably the (TBT) Double Short Treasury ETF. I’m looking for it to go up another 30% from here to 24 or 25 by sometime next year.

Q: EVs have been hot this year; Lordstown Motors is down to only $5 from $27 and just got downgraded by an analyst to $2. Should I buy, or is this a dangerous strategy?

A: I would say highly dangerous. This company has been signaling that it’s on its way to bankruptcy essentially all year, so don’t confuse “gone down a lot” with being “cheap” because that’s how you buy stuff on the way to zero.

Q: What about Anthony Scaramucci’s ETF?

A: We will have Anthony Scaramucci as a guest in our December summit. And the ETF is a basket of stocks as diverse as MicroStrategy (MSTR), Blok (BLOK), Visa (V), and Nvidia (NVDA), so you will only get a fraction of the Bitcoin volatility. That means if Bitcoin goes up 100% you might get a 40% or 50% move in the actual ETF.

Q: Do you have a Bitcoin book coming out soon?

A: I do, it should be out by the end of this month. That’s The Mad Hedge Guide to Trading Bitcoin, and it will have all the research I’ve accumulated on trading Bitcoin in the past year.

Q: Why have you only issued one trade alert in Bitcoin?

A: You don’t get a lot of entry points for Bitcoin. You buy the periodic bottoms and then you run them. Dollar cost averaging is very useful here because there are no traditional valuation measures to use, like price earnings multiples or price to book. When it comes time to sell, we'll let you know, but there aren’t a lot of Bitcoin plays outside the Bitcoin exchanges.

Q: Thoughts on silver (SLV)?

A: It’s horribly out of favor now and will continue to be so as long as Bitcoin gets the spotlight. Also, there’s a China problem with the precious metals.

Q: There are 8 or 10 good public Bitcoin and Ethereum ETFs in Canada.

A: That’s true, if you’re allowed to trade in Canada.

Q: Can the US ban Bitcoin like China did?

A: No, if they did, it would just move offshore to the Cayman Islands or some other place outside the world of regulation.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log on to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 13, 2020

Fiat Lux

Featured Trade:

(NOVEMBER 11 BIWEEKLY STRATEGY WEBINAR Q&A),

(AMZN), (TSLA), (FB), (AAPL), (ROKU), (UUP), (ITB), (TLT), (TBT), (FXI), (SPY), (BIDU), (TCTZF), ($NATGAS), (DIS) (AMD), (IP), (BIIB), (VRTX)

It looks like I hit the nail on the head once again with a major short position in the United States Natural Gas Fund (UNG).

After my followers bought the July, 2014 $26 puts at $2.16 on Monday, the (UNG) suffered its worst trading day since 2007, the underlying commodity plunging a breathtaking 11%. The puts roared as high as $3.05, a gain of 42% in mere hours. I wish they were all this easy!

If the (UNG) returns to the February low of $22.50 in the near future, you can expect these puts to soar to $5.00. That?s an increase of 130%, and would add 6.53% to our 2014 performance. Please pray for warmer weather, and dance your best weather dance.

It took a perfect storm of technical and fundamental factors to trigger this Armageddon for owners of the troubled CH4 molecule. One of the coldest winters in history produced unprecedented demand for natural gas.

This happened against a backdrop of a long term structural conversion from coal and oil fired electric power plants to gas. Not only is natural gas far cheaper than these traditional carbon based fuels, burning it generates half the carbon dioxide and none of the other toxic pollutants.

The result for traders was one of the boldest short squeezes in history. The incredibly $6.50 Monday opening we saw in natural gas, and the $28 print for the (UNG) was purely the result of distressed margin calls and panic stop loss covering.

At one point, the February natural gas futures, set to expire in just two days, were trading at a 40% premium to the March futures. Extreme anomalies like this are always the father of great trades.

The extent of the industry short position is evident in the cash flows in the underlying exchange traded notes (ETN?s). As prices rose, the long only (UNG) saw $366 million in redemptions, about 36% of its total assets. The Natural Gas Fund (UNL) has lost more than a third of its capital.

On the flip side, the Velocity Shares 3X Inverse Natural Gas Fund (DGAZ) pulled in some $449 million in new investors. Since the rally in natural gas started in November (DGAZ) has cratered from $18 to $2.5. This is why I never recommend 3X leveraged ETF?s.

This all adds currency to my argument that the natural gas revolution is bringing the greatest structural change to the US economy in a century. The industry is evolving so fast that you can expect dislocations and disruptions to continue.

The current infrastructure reflects the state of the market a decade ago and is woefully inadequate, with a severe pipeline shortage evident.? Gas demand is greatest where supplies aren?t. Infrastructure needed to export CH4 abroad is still under construction (see my piece on Chenier Energy (LNG) by clicking here).

The state of North Dakota estimates that it is losing $1 million a day in tax revenue because excess natural gas is being flared at fracking wells for want of transportation precisely when massive short squeezes are occurring in the marketplace. Needless to say, this is all a dream come true for astute and nimble traders, like you.

The question is now what to do about it.

I just called friends around the country, and it appears that a warming trend is in place that could last all the away into March.

It is time to get clever. It would be wise to enter a limit day order to sell your $26 puts right now at the $5.00 price. Since the first visit to these lower numbers usually happens on a big downside spike, the result of stop loss dumping of panic longs accumulated by clueless short term traders this week, you might get lucky and get filled on the first run.

These happen so fast that it will make your head spin, and you won?t be able to type an order in fast enough. If you don?t get filled keep reentering the limit order every day until it does get done, or until we change our strategy.

This has been one of my best trades in years, and it appears that a lot of followers managed to successfully grab the tiger by the tail.

Good for you.

Now We?re Cooking with Gas

Now We?re Cooking with Gas

Now We?re Cooking With Gas (UNG)

Those who followed my advice to buy the United States Natural Gas Fund (UNG) July, 2014 $23 puts at $1.68 yesterday are now in the enviable position of owning a security that is running away to the upside.

At this morning?s high the puts traded at $2.40, a one day gain of an eye popping 43%. I am getting emails from a lucky few that they got in as low as $1.55 after receiving my Trade Alert.

The question is now what to do about it.

I just called friends around the country, and it appears that a warming trend is in place that could last all the away into mid February. It is starting in Florida and Texas and gradually working its away north, although they are still expecting eight inches of snow in Chicago this weekend.

Mad Day Trader Jim Parker is confirming as much with his proprietary trading model chart, which I have included below. He says that we put in an excellent medium term high in the UNG on Thursday at $27. This morning we tested daily support at $23.26 and it held the first time.

But with warmer weather, this is almost certain to break on a future downside push. Then we train out sites on the 18-day moving average at $22.25. After that, $22.07 is in the cards, the top of the gap that we broke through only as recently as January 27, only four days ago.

There, our United States Natural Gas Fund (UNG) July, 2014 $23 puts, with a present delta of 40% (forget this if you don?t speak Greek), should be worth $2.83. You might get more, if implied volatilities for the puts rise on the downside, which they almost always do.

That would be a one-day profit of 68%, adding $3,000 to the value of our notional $100,000 model trading portfolio, or 3% to our performance this year, which I would be inclined to take.

Now it is time to get clever. It would be wise to enter a limit day order to sell your $23 puts right now at the $2.68 price. Since the first visit to these lower numbers usually happens on a big downside spike, the result of stop loss dumping of panic longs accumulated by clueless short term traders this week, you might get lucky and get filled on the first run. If you don?t, keep reentering the limit order every day until it does get done, or until we change our strategy.

This has been one of my best trades in years, and it appears that a lot of followers managed to successfully grab the tiger by the tail.

If there was ever a time to upgrade to Jim Parker?s Mad Day Trader service, it is now. He will see the breakdowns and the reversals with his models faster than I, and get his Trade Alerts out quicker. Why wait for the middleman, who is me? These fast, technically driven markets are where Jim really earns his pay.

If you want to get a pro rata upgrade from your existing newsletter or Global Trading Dispatch subscription to Mad Hedge Fund Trader PRO, which includes Mad Day Trader, just email Nancy in customer support at nmilne@madhedgefundtrader.com.

Do it quick because she is about to get overwhelmed.

Now We?re Cooking with Gas

Time to Sell Natural Gas

I received a crackly, hard to understand call late last night from one of my old natural gas buddies in the Barnet shale in Texas. Chances are that CH4 peaked in price last night with the expiration of the front month contract. It was time to sell.

I spent five years driving a beat up pick up truck on the tortuous, jarring, washboard roads of this forlorn part of the country, buying up mineral rights from old depleted fields for pennies on the dollar.

The sellers thought I was some moron hippie from California, probably high on some illegal drugs. "You want to redrill these fields and throw dynamite down the holes?" It was a crazy idea. Since I was offering hard cash, they couldn't sign the dotted line fast enough.

During the late nineties nobody had ever heard of fracking. Even in the oil industry only a few specialists were aware of it. My old buddy, Boone Pickens, claims he was doing it in the fifties, but then nothing the wily oilman ever does surprises me.

Only a few reckless independent wildcatters were experimenting with the new process. The oil majors wouldn't touch it with a ten-foot pole. It was unproven, dangerous, and could never deliver sufficient volumes to get them interested. With the deep pockets a trial lawyer could only dream about, they couldn't afford the liability risk of polluting a town's drinking water. So it was left to small fry like me to finance this ground-breaking technology.

I ended up developing a couple of fields, riding gas up from $2 to $5 MMBTU, then selling them off to the gas companies. My partners and I made a fortune.

We have remained in touch over the years. Whenever something indecipherable happens in the international capital markets, they call me for an explanation. When something special sets up in the natural gas market, I get the first call.

On Election Day we all go out and get drunk because their conservative vote cancels out my liberal ones, so why bother? We do this at Billy Bob's in Fort Worth, a favorite of former President George W. Bush, where the 24-ounce chicken fried steaks fall over both sides of your plate.

I didn't reenter the gas market until the Amaranth hedge fund blow up took the price up to $17 in 2006, and then down like a stone. I figured out that the United States Natural Gas Fund (ETF) suffered from a peculiar mathematics that was death for long side investors.

The natural gas futures market often trades in a contango. This is when front month contracts trade at a big premium to far month ones, adjusted for the cost of borrowed money. This premium completely disappears at expiration, when the commercial buyers, like electric power plants and chemical companies, take physical delivery of the gas.

What (UNG) does is buy contracts three months out, run them into expiration, and then roll the money into new contracts another three months out. The premium they pay rapidly falls to zero. Then they repeat the process all over again. It is a perfect wealth destruction machine.

The same dilemma besets futures contracts for oil (USO), corn (CORN), wheat (WEAT), and soybeans (SOYB) to a lesser degree, and a lot of traders make their livings from these anomalies.

What (UNG) does is buy contracts three months out, run them into expiration, and then roll the money into new contracts another three months out. The premium they pay rapidly falls to zero. Then they repeat the process all over again. It is a perfect wealth destruction machine.

I have seen a period when natural gas rose 40%, but the (UNG) dove 40%, thanks to the costly effects of the contango. Needless to say, this makes the (UNG) the world's greatest short vehicle in a falling market. It is a fantastic heads I will, tails you lose security.

There is another crucial factor making natural gas such a great natural short that few outside the industry are aware of. You cannot store natural gas to the degree you can semi liquid oil. Unlike Texas tea, natural gas wells can't be capped without damaging their long-term production. It has to flow and be sold at whatever price you can get. If you don't, it goes away. This means that when the price of natural gas falls, it does so with a turbocharger, also making it an ideal short play.

To make a long story short, I made another fortune riding gas down from $17 to $2. I haven't touched it for 2 years. Other hedge fund manager friends of mine made billions on this trade, and then retired to a sedentary life of philanthropy.

At this point, natural gas is up an unbelievable 56% in three months, thanks to Mother Nature's brutal assault on most of the country, except here in balmy California. Demand is at an all time high, prices a 5-year peak, and speculative long positions in the futures market at an eight-year apex. Storage was taken down to a six month low of 1.2 trillion cubic feet with today's 230 billion cubic foot draw down.

Expiration of the front month contract triggered a super spike in the (United States Natural Gas Fund to an astounding $27, while underling natural gas made it all the way up to $5.50, nearly triple the subterranean $1.90 low set in April, 2012.

This is happening in the face of one of the greatest supply onslaughts in history that will hit the market throughout the rest of this year. They're still hiring and drilling like crazy in North Dakota.

The demand spike came hard and so fast that it caught many suppliers by surprise. That has created a bubble in the pipeline, a temporary shortfall in supplies, and triggered an incredible short squeeze in the natural gas market.

Winter can't last forever. Eventually summer comes, and the shortage of natural gas pipeline will get more than made up by thousands of new fracking wells in the US.

If the UNG returns to the November, 2013 $17 low by July 18, the value of the (UNG) July, 2014 $23 put rises from our $1.68 cost to $4.72, a potential gain of 181%. That's a fabulous risk/reward ratio, and we have six months to see it happen.

Keep in mind that liquidity could be an issue here. Yesterday, 1,549 contracts traded against on open interest of 2,297 contracts. The option market spreads here are also humongously wide and the volatility is of biblical proportions, which is endemic to the natural gas market.

Just to get a second opinion, I called Mad Day Trader Jim Parker, as I hadn't been in this market for a while. He said it was warming up in Chicago, and he was venturing outside for a walk for the first time in three days. Out went the Trade Alert!

Below please find a chart for natural gas generated by Jim?s proprietary trading model. The bottom line here is that there is a high probability that we will drop from the current $5.17 down to $4.70, break that, go down to $4.17, break that, and possibly go as low at the November low of $3.40.

They don?t call this market the ?widow maker? for nothing, so expect a lot of heart wrenching volatility before you see a substantial payoff. So it best to enter a spread of small limit orders and hope for the best.

You can best play the short side through the futures market in natural gas. For those without a futures account, you can buy the 2X ProShares Ultra Short DJ-UBS Natural Gas inverse ETF (KOLD) or the 3x Direxion Daily Natural Gas Related Bear 3X Shares inverse ETF (GASX). The more adventurous can sell short the (UNG) outright, if they can find stock to borrow.

Time to Sell Winter Short Billy Bob?s in Forth Worth

Billy Bob?s in Forth Worth

I think that oil peaked last week with the Egyptian Army?s ferocious and bloody attack on the Muslim Brotherhood. I hate to sound cynical here, but count the daily bodies in the street, which has been trending down sharply since Thursday?s, 1,000 plus tally. Fewer bodies mean lower oil prices.

This has most likely broken the back of the fundamentalist opposition movement for at least the time being, which has accounted for the $20 spike in oil prices over the last two months.

This returns us to the longer term fundamental trend for oil, which is sideways at best, and down at worst. The US is flooding the world?s oil markets with energy in all its many forms. The driver here is American fracking technology, which will continue to upend the traditional energy markets for decades to come. It?s just a matter of time before fracking goes mainstream in Europe, especially in the big coal countries of Germany, Poland, and England. Then they can thumb their noses at Russia, a major gas supplier over the last thirty years. China will follow.

In a crucial news item that wasn?t reported nationally, the California legislature voted down a measure to ban hydraulic fracturing in their state. It was defeated in a democratically controlled body. As the Golden State is the most anti energy state in the country, this gives the state a flashing green light to move forward against environmentalist opposition. There is a ton more of new supply coming. This is what the weakness in the price of natural gas is telling you (UNG).

We also received a new negative for oil this month, the collapse of the emerging market currencies, stock markets, and bonds, especially the Indian rupee. This reduces their international purchasing power in US dollar terms, thus raising the cost of oil in local currency terms. You see, oil is priced in dollars. As the emerging markets have seen the largest growth in demand for oil in recent years, this can only be bad for prices.

In terms of my own trading portfolio, I want to have a ?RISK OFF? position, like an oil short, to hedge my two existing ?RISK ON? positions in the Euro (FXE) and the yen (FXY) shorts. US stock markets could be weak into September, and they will take oil down with them.

The energy inventory figures released on Wednesday were another tell. Oil came in line with a 1.5 million barrel weekly draw down. But gasoline showed a precipitous 4 million barrel drop in supplies, meaning that more people are driving to their summer vacations than expected. Texas tea should have rallied at least $1 on the news. Instead it fell $1.50. It is an old trading nostrum that if a contract can?t rally on surprisingly positive developments, you sell the daylights out of it.

Below, you will find another chart that you should wake up and take notice of, the Powershares DB US Dollar Bullish Index Fund (UUP). Commodities traditionally are weak when the dollar is strong. Both the chart and the fundamentals suggest that we are close to a multiyear low for the greenback and are about to enter a prolonged period of dollar strength. This is also grim tidings for oil.

Finally, there is that last resort, the charts. Check out those for the (USO) and oil and it very much looks like we have a triple top in place. That is the straw that breaks the camel?s back. Time to sell.

The only way I am wrong on my oil call is if the Chinese economy is about to take off like a rocket. They are the marginal big swing player in this market. But there is absolutely no sign of that happening in the economic data. If anything, the collapse in emerging markets suggest that conditions in the Middle Kingdom are about to get worse before they get better.

Ouch! That Hurt!

Ouch! That Hurt!

I recently spent an evening with Ambassador Richard Jones, the Deputy Executive Director of the International Energy Agency in Paris, who had some eye opening things to say about the energy space. The IEA was first set up as a counterweight to OPEC during the oil crisis in 1974, and has since evolved into a top-drawer energy research organization.

World GDP will grow an average 3.1%/year through 2030, driving oil demand from the current 84 million barrels/day to 103 million b/d. That means we will have to find the equivalent of six Saudi Arabia?s to fill the gap or prices are going up, possibly a lot. His conservative target has crude at $190 in twenty years. Some 39% of that increase in demand will come from China and 15% from India.

A collapse in investment caused by the financial crisis means that supply can?t recover in time to avoid another price spike. More than 1.5 billion people today don?t have electricity at all, but would love to have it. The best the climate negotiations can hope for is for CO2 to rise until 2020, and then plateau after that, because once this greenhouse gas enters the atmosphere it is very hard to get out.

This will require a massive decarbonization effort reliant on nuclear, hydro, alternatives, and carbon capture and storage. Up to half of the needed carbon reduction can be achieved through simple efficiency measures, like ditching the incandescent light bulb, driving more hybrids, and closing dirty, old coal fired power plants. Natural gas will be a vital bridge, as it is cheap, in abundant supply, and emits only half the carbon of traditional fossil fuels. The total 20-year bill for the rebuilding of our new energy infrastructure will exceed $10 trillion.

Richard, who comes from a long diplomatic career in Kuwait, Kazakhstan, and Israel, certainly didn?t pull any punches. I have been a huge fan of the IEA?s data for 35 years. Better use any weakness in oil prices to accumulate long term positions in crude through the futures, the ETF (USO), the offshore drilling companies like Transocean (RIG), and oil and gas plays like ExxonMobil (XOM)? and Occidental Petroleum (OXY). When oil comes back, it will do so with a vengeance.

I?ll Take Another Six Please

I?ll Take Another Six Please