Featured Trade: (TUESDAY, JUNE 12, 2018, NEW ORLEANS, LA, GLOBAL STRATEGY LUNCHEON), (WHY YOUR FANG STOCKS ARE ABOUT TO DOUBLE IN VALUE), (FB), (AAPL), (NFLX), (GOOGL), (LMT), (ROKU), (HERE IS YOUR TOP-PERFORMING INVESTMENT FOR THE NEXT FIVE YEARS), (ITB), (PHM), (KBH), (DHI), (AVB), (CPS)

The shares of FANGs are all about to double in value in the Silicon Valley if commercial real estate is any indication of the future growth rates.

The group is gobbling up office space at such a prodigious rate that only a vast expansion of their business would justify these massive long-term commitments.

Commercial real estate commitments are one of the most valuable leading indicators of stock performance out there. They show what the companies themselves think are their future prospects.

Apparently, the stock market agrees with me. Technology is virtually the only group of shares moving to new all-time highs in these otherwise dismal trading conditions.

Just this month Facebook (FB) signed a lease for the entire brand new 43-story Park Tower in downtown San Francisco, and that's just to house its Instagram business.

Google (GOOGL) is leasing 39% of the office space in Mountain View, CA. It is currently in negotiations with the nearby city of San Jose to build a skyscraper occupying an entire city block that will house 10,000 tech workers. It also is building another 1 million square feet near an old prewar dirigible landing strip in Moffett Park.

Apple (AAPL) is hogging some 69% of the office space in Cupertino, CA. It is just now moving into its new massive spaceship-inspired headquarters, where 10,000 workers will slave away. The world's largest company is currently on the hunt for a second headquarters location.

Netflix is slowly gobbling up Los Gatos, CA. It was recently joined by the set top device company Roku (ROKU), which is growing by leaps and bounds.

Fruit canning was the original industry of Silicon Valley at the turn of the 20th century, taking advantage of the surrounding peach, plum, and apricot groves. When I was a kid after WWII, defense firms such as Lockheed (LMT) took over, creating thousands of high-paying engineering jobs.

It didn't hurt that Stanford University was spitting distance away, and the University of California was just on the other side of the bay. These two schools supplied the manpower to fuel the hypergrowth ahead.

To say the growth has caused local headaches would be an understatement in the extreme. The San Francisco Bay Area now sports the world's most expensive residential housing. The median San Francisco home price has skyrocketed to $1,334,000 and requires an annual income of $334,000 to support it.

Small businesses such as dry cleaners, nail salons, restaurants, and barber shops have been driven out by soaring rents. It's not uncommon now to go out to dinner only to find a "closed" sign on your favorite nightspot. Your personal assistant now has to travel miles just to get your suits pressed.

As for traffic, forget about it. Rush hour has ceased to exist. Freeways are now jammed a nonstop 12 hours a day in the worst neighborhoods.

Success has its price, and this was never truer than in Silicon Valley.

The New Apple HQ

Where Instagram Now Lives

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/APPLE-HQ-story-2-image-6-e1527804149789.jpg326580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-06-01 01:07:092018-06-01 01:07:09Why Your FANG Stocks are About to Double in Value

The Amazon (AMZN) and Netflix (NFLX) model is not the only technology business model out there.

Micron (MU) has amply proved that.

Bulls were dancing in the streets when Micron announced a blockbuster share buyback of $10 billion starting in September.

This is all from a company that lost $276 million in 2016.

The buyback is an overwhelmingly bullish premonition for the chip sector that should be the lynchpin to any serious portfolio.

The news keeps getting better.

Micron struck a deal with Intel to produce chips used in flash drives and cameras. Every additional contract is a feather in its cap.

The share repurchase adds up to about 16% of its market value and meshes nicely with its choreographed road map to return 50% of free cash flow to shareholders.

Tech's weighting in the S&P has increased 3X in the past 10 years.

To put tech's strength into perspective, I will roll off a few numbers for you.

The whole American technology sector is worth $7.3 trillion, and emerging markets and European stocks are worth $5 trillion each.

Tech is not going away anytime soon and will command a higher percentage of the S&P moving forward and a higher multiple.

The $5 billion in profit Micron earned in 2017 was just the start and sequential earnings beats are part of their secret sauce and a big reason why this name has been one of the cornerstones of the Mad Hedge Technology Letter portfolio since its inception as well as the first recommendation at $41 on February 1.

Did I mention the stock is dirt cheap at a forward PE multiple of just 6 and that is after a 35% rise in the share price so far this year?

What's more, putting ZTE back into business is a de-facto green light for chip companies to continue sales to Chinese tech companies.

China consumed 38% of semiconductor chips in 2017 and is building 19 new semiconductor fabrication plants (FAB) in an attempt to become self-sufficient.

This is part of its 2025 plan to jack up chip production from less than 20% of global share in 2015 to 70% in 2025.

This is unlikely to happen.

If it was up to them, China would dump cheap chips to every corner of the globe, but the problem is the lack of innovation.

This is hugely bullish for Micron, which extracts half of its revenue from China. It is on cruise control as long as China's nascent chip industry trails miles behind them.

At Micron's investor day, CFO David Zinsner elaborated that the mammoth buyback was because the stock price is "attractive" now and further appreciation is imminent.

Apparently, management was in two camps on the capital allocation program.

The two choices were offering shareholders a dividend or buying back shares.

Management chose share repurchases but continued to say dividends will be "phased in."

This is a company that is not short on cash.

The free cash flow generation capabilities will result in a meaningful dividend sooner than later for Micron, which is executing at optimal levels while its end markets are extrapolating by the day.

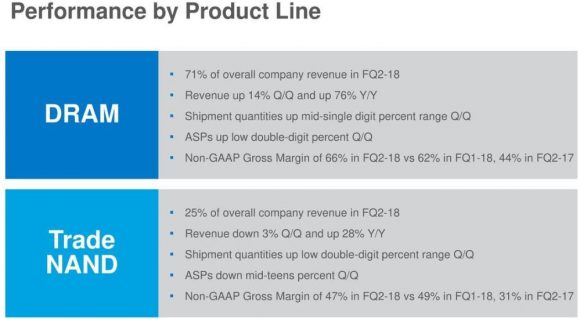

As it stands today, Micron is in the midst of taking its 2017 total revenue of about $20 billion and turning it into a $30 billion business by the end of 2018.

The overall chips market is as healthy as ever and data from IDC shows total revenues should grow 7.7% in 2018 after a torrid 2017, which saw a 24% bump in revenues.

The road map for 2019 is murkier with signs of a slowdown because of the nature of semi-conductor production cycles. However, these marginal prognostications have proved to be red herrings time and time again.

Each red herring has offered a glorious buying opportunity and there will be more to come.

Consolidation has been rampant in the chip industry and shows no signs of abating.

Almost two-thirds of total chip revenue comes from the largest 10 chip companies.

This trend has been inching up from 2015 when the top 10 comprised 53% in 2016 and 56% in 2017.

If your gut can't tell you what to buy, go with the bigger chip company with a diversified revenue stream.

The smaller players simply do not have the cash to splurge on cutting-edge R&D to keep up with the jump in innovation.

The leading innovator in the tech space is Nvidia, which has traded back up to the $250 resistance level and has fierce support at $200.

Nvidia is head and shoulders the most innovative chip company in the world.

The innovation is occurring amid a big push into autonomous vehicle technology.

Some of the new generation products from Nvidia have been worked on diligently for the past 10 years, and billions and billions of dollars have been thrown at it.

Chips used for this technology are forecasted to grow 9.6% per year from 2017-2022.

Another death knell for the legacy computer industry sees chips for computers declining 4% during 2017-2022, which is why investors need to avoid legacy companies like the plague, such as IBM and Oracle because the secular declines will result in nasty headlines down the road.

Half way into 2018, and there is still a dire shortage of DRAM chips.

Micron's DRAM segments make up 71% of its total revenue, and the 76% YOY increase in sales underscores the relentless fascination for DRAM chips.

Another superstar, Advanced Micro Devices (AMD), has been drinking the innovation Kool-Aid with Nvidia (NVDA).

Reviews of its next-generation Epyc and Ryzen technology have been positive; the Epyc processors have been found to outperform Intel's chips.

The enhanced products on offer at AMD are some of the reasons revenue is growing 40% per year.

AMD and Nvidia have happily cornered the GPU market and are led by two game-changing CEOs.

It is smart for investors to focus on the highest quality chip names with the best innovation because this setup is most conducive to winning the most lucrative chip contracts.

Smaller players are more reliant on just a few contracts. Therefore, the threat of losing half of revenue on one announcement exposes smaller chip companies to brutal sell-offs.

The smaller chip companies that supply chips to Apple (AAPL) accept this as a time-honored tradition.

Avoid these companies whose share prices suffer most from poor analyst downgrades of the end product.

Cirrus Logic (CRUS), Skyworks Solutions (SWKS), and Qorvo Inc. (QRVO) are small cap chip companies entirely reliant on Apple come hell or high water.

Let the next guy buy them.

Stick with the tried and tested likes of Nvidia, AMD, and Micron because John Thomas told you so.

"Bitcoin will do to banks what email did to the postal industry." - said Swedish IT entrepreneur and founder of the Swedish Pirate Party Rick Falkvinge.

Capitol Hill unleashed a healthy dose of criticism on Facebook (FB) CEO Mark Zuckerberg and he has mobilized the forces to avoid a repeat shellacking.

Zuckerberg's response has been to reshuffle his cabinet at the Menlo Park, CA, headquarters, and a few tell-tale signs offer a unique glimpse into Facebook's future.

Basically, something needed to change at Facebook.

The company single-handedly took the blame for the entire sector and was not the only company with a liberal stance on personal data.

Zuckerberg would like to eschew public humiliation and avoid being a sitting duck.

The episode in Washington highlights the need for Facebook to decouple itself from ad revenue, which makes up the lion's share of revenue at the firm and find other levers to pull.

Down the road, Facebook's ad business could get crimped by regulators, and a lack of fallback options haunts Facebook investors in their sleep.

Consequently, a whole slew of high-level management rotation is underway at Facebook.

It is the biggest shake-up in the history of Facebook.

The road map starts with one of Zuckerberg's best friends and protege Chris Cox who will manage the new "family of apps" segment.

This collection of projects he will preside over include WhatsApp, Messenger, Instagram, and the Facebook Core App.

The step up in responsibility is warranted for Chris Cox who was credited with creating the Facebook news feed after joining the company in 2005 after ditching his Stanford graduate degree program at the time.

The executive reshuffle coincided with WhatsApp co-founder Jan Koum, one of Silicon Valley's biggest advocates for data privacy, who quit his post as a show of disapproval to Facebook's business model.

Mark Zuckerberg wants to aggressively monetize the WhatsApp messenger service that was acquired for $19 billion in 2014.

Zuckerberg's blueprint involves using the WhatsApp phone numbers as a vehicle to monetize through offering different products.

Facebook would then collect the data from its 1 billion usership and WhatsApp would become Facebook's new advertisement clearing house.

WhatsApp's leadership vehemently refused this U-turn and Koum decided he would rather leave then see his baby ruined.

Facebook consistently refrained in the past from passing WhatsApp to the data mining scientists and was able to prevent full-scale implementations of advertisements onto its platform.

Currently, there are no ads on WhatsApp's interface, and users could be in store for a massive transformation in look and feel.

Facebook investors have been clamoring for Zuckerberg to start the process of making WhatsApp into a material revenue stream.

Time is of the essence as the big data police creep in from the shadows.

Putting Zuckerberg's top guy on the job embarks Facebook down a new path of hyper accelerated profit-making.

Well, that is the goal.

Compounding Facebook's pivot to other businesses is commissioning a new blockchain tech team.

Blockchain technology, the technology that helped unearth bitcoin, has seen a recent slew of endorsements from financial heavy hitters such as Goldman Sachs (GS), which acknowledged the formation of a new business brokering in bitcoin futures.

A year ago, no reputable organization would touch blockchain with a 10-foot pole.

The utilization of blockchain technology would allow trackability and provide more security.

That would help Facebook to understand the provenance of unique problems allowing staff to nip problems in the bud before they snowball.

Blockchain tech fits nicely within the constraints of the model and would enhance the existing Facebook product.

Let's not forget that Facebook has a mountain of cash to fix any problem that crops up.

It is not one of these early stage seed companies burning through heaps of cash waiting for "scalability" down the road.

Facebook is here and now, and it has the money to show for it.

The pillars of blockchain revolve around cryptography. Blockchain would effectively allow individuals to possess more power over their identity decentralizing the stranglehold from Menlo Park.

Thus, Facebook must invest deeply into blockchain to counter the fear that this technology can marginalize the core business.

This epitomizes the tendency for large-cap tech to become preemptive.

None of the powerful FANGs want to miss the next big shift in technology, and the cash hoard allows them to have skin in the game in each revolutionary trend.

The tide has changed at Facebook from the early years where growing the user base was paramount.

Now that user base has matured into a 2.2 billion marketplace.

Facebook's strategy has shifted to extracting more revenue per user and management closely follows this metric.

Mike Schroepfer, the CTO of Facebook, was tabbed as the man leading the charge for Artificial Intelligence (A.I.), Augmented Reality (A.R.), and Virtual Reality (V.R.) technology.

Facebook was able to poach Jerome Pesenti from IBM (IBM), where he was a critical cog in the development of IBM's Watson, to run the Facebook A.I. team. A.I. is routinely implemented into Facebook's core products to enhance performance.

Promoting Chris Cox as the next in line and giving him control over all the powerful products effectively pushes ad tech down the pecking order.

Javier Olivan is the new man at Facebook tasked for managing ads, analytics, and integrity, growth and product management.

Moving forward, the ad division will be laced with a certain level of security to avoid a repeat of Cambridge Analytica.

Zuckerberg must know that there are other Cambridge Analytica's hidden somewhere in the system; another incident would knock down the stock 5% to 10%.

Facebook could look vastly different in a few years if some of these profit drivers prove successful. It only needs one to work.

Disrupt or be disrupted.

At this point, the big tech companies are considering anywhere or anyone to capture accelerated growth. The FANGs are spilling over to other companies' turf.

Crossover is everywhere and this is just the beginning.

Expect Amazon's (AMZN) ad division to grow from the already $2 billion per quarter, gradually challenging the duopoly of Facebook and Alphabet in the digital ad revenue industry.

It is yet to be seen if the new revamp of management will produce better results.

This move could backfire as the management carousel excluded any fresh blood from taking part.

Effectively, Zuckerberg rotated his best friends into different parts of the business without demoting anyone.

Solidifying his close-knit circle of trust is no doubt a defensive reaction to being hounded the past few months, leaving his existing circle as the few people on which he can still count.

Facebook's stock remains healthy and the brouhaha stoked by the data leak gave investors a timely entry point.

I pounded on the table calling the bluff, begging readers to get into Facebook.

The long-term Facebook story is intact but the stock is overbought short-term.

Investors should not sleep on Facebook as it is a profit machine printing money like Apple (AAPL) and the executive revamp is a bullish development for Facebook.

My bet is that Chris Cox goes for the low hanging fruit monetizing WhatsApp, inciting the next leg up in Facebook shares later in the year.

"Simply put: We don't build services to make money; we make money to build better services." - said Facebook CEO Mark Zuckerberg

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Zuckerberg-on-the-Hill-image-2-e1526417830446.jpg343580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-16 01:05:032018-05-16 01:05:03What's Up at Facebook?

Uber has seen a ferocious challenge to its business model of late. It seems everything it touches turns into fool's gold.

It is easy to assign blame to the current CEO, but Dara Khosrowshahi was shoehorned into a difficult situation after previous CEO Travis Kalanick defiantly departed leaving the company in tatters in his wake.

What could go wrong went wrong.

The company was purged of its license to operate in London, which was one of its highest transactional cities.

Uber boasted a ridership of 3.5 million and sub-contracted 40,000 drivers in London that singlehandedly wiped out the Cockney black cab industry.

The land of fish and chips has not exactly been kind to Uber with the British seaside resort city Brighton the next location to excommunicate Uber from its sandy shores.

Uber's massive data breach of 2016, which took Uber a full year to publicly disclose, of 25.6 million names, 22.1 million mobile phone numbers, and 607,000 driver's license numbers was cited as one of the reasons Uber's license in Brighton was discontinued.

Is there a way back for CEO Dara Khosrowshahi?

The future looks turbulent at best.

Khosrowshahi has left no stone unturned carrying out his search for a new CFO. Uber has not had a CFO since 2015, and a CFO is required to shepherd the company through the IPO process.

Prospective candidates will not touch this position with a 10-foot pole.

Several high-profile hopefuls have already rebuffed offers.

It was painfully obvious to onlookers last week at Uber's Elevate conference in Los Angles that Alphabet (GOOGL) is dominating every potential business that Uber desires to penetrate.

Waymo, Alphabet's autonomous driving technology arm, is miles ahead of Uber after developing in secret for many years.

Waymo's self-driving testing began in 2009 while Uber's first test was carried out in September 2016 in Pittsburgh, conceding a seven-year head start to bitter rivals.

Even worse, Uber's trials have been sidelined as of late because of a casualty in the Phoenix program. Arizona is on the verge of removing Uber from possible future tests along with California making Pittsburgh the last place left to consolidate operations.

At the Elevate conference, Khosrowshahi elucidated Uber's roadmap to industry professionals, and his synopsis was largely underwhelming.

Khosrowshahi broke down the future into three easy-to-understand stages.

In the next two to three years, stage one consists of focusing on improving existing algorithms, enhancing ride share transactions, and expanding to different locations widening the companies ride-share footprint.

Stage 1.5 detailed refining its Uber Eats segment seizing further market share from Grubhub (GRUB) and Amazon (AMZN), the two biggest rivals.

In two to five years from now, stage two entails ramping up the e-bike segment through recently acquired e-bike firm Jump.

Lastly, stage three was proposed to happen in five to 10 years and encompass growing a newly minted air-taxi division called Elevate.

Up until today, Uber's core business has been an unmitigated failure of massive proportions.

In the fourth quarter of 2016, Uber hemorrhaged $2.8 billion then followed up the fourth quarter in 2017 with a $4.5 billion loss, a stark reminder that profits are hard to come by in the tech world.

If losses are what investors want, Uber gives it to you in spades.

If it cannot successfully monetize the core business using cars, the e-biking future is dead on arrival.

Stage 1.5 is all designer chocolates and fancy roses now because growth and margins remain healthy. However, this industry is fraught with booby traps that I chronicled in the recently published story about Grubhub (GRUB).

Stage three was a division that Khosrowshahi reviewed several times after he took the top job and it made the cut after deep contemplation.

Uber plans to start conducting trials in 2020 in Dallas or Los Angeles with the hope of commercial operations starting in 2023.

This timeline is wishful thinking because regulators would never grant operational authority to Uber in a mere five years when it cannot even succeed on asphalt with its self-driving technology.

Lamentably, Alphabet's co-founder Larry Page has an ace up his sleeve.

Since last October, stealth flight trials have been carried out in New Zealand by firm Kitty Hawk led by Sebastian Thrun one of the creators of Waymo, which is developing autonomous flying taxis.

Kitty Hawk was developed for years in secret and personally backed by Larry Page's personal wealth.

He has already poured more than $100 million of his own money into this venture.

To further develop its business, Kitty Hawk was forced to decamp to New Zealand as the Federal Aviation Administration (FAA) in America lacks a path to certification and commercialization.

New Zealand has embraced the revolutionary start-up, and New Zealand is the first country poised to develop a functional robo air-taxi network.

Kitty Hawk's hopes and dreams rely on the aircraft Cora. Please click here to visit its website for more information.

Cora is an all-electric affair powered by batteries with a 36-foot wingspan.

This meshes perfectly with New Zealand's hope to be carbon free by 2050.

Cora has been manufactured with capabilities of flying at heights up to 2,950 feet and a range of 62 miles.

New Zealand has bet the ranch on aerospace technology allowing even marginal start-ups within its borders such as Martin Jetpack, the first commercially sold jetpack, operating with a flight ceiling of 2,500 feet and sold at a starting price of $150,000.

It is ironic that Uber chose to host an aerial-taxi conference considering it is not the company building the flying taxis.

This is the crux of the problem in which Uber finds itself.

It does not produce anything unique.

The biggest winners that take home the lion's share of the spoils are the firms that create a proprietary product that cannot be replicated easily such as Netflix's original content or Google's advanced search engine.

The heavy lifters gain control and can dictate the path toward monetization.

Page's Kitty Hawk is in the driver's seat with the best technology and Uber's Khosrowshahi recently met with Thrun pitching his idea of partnering up.

Expectedly, Kitty Hawk declined to become buddies because nothing can be gained by collaborating with Uber.

Kitty Hawk stated that it plans to develop an app for its own robo-flights, which could crush Uber's dream of being the end all be all of transportation apps.

At the end of the day, Uber is just an app matching drivers and passengers, and creating this app is highly replicable.

It takes billions upon billions of dollars to build an autonomous aerial taxi from scratch. Uber's inability to produce aircraft gives it little negotiating power down the line.

On that note, Uber announced a partnership with NASA to build an air traffic control system, which would logically be used to construct landing ports similar to a helipad for aircraft to land.

By carving out a sliver of the industry mastering port construction, it gives Uber a narrow entranceway into the future of aero-taxi industry albeit a weaker strategic position than Page's Kitty Hawk.

Another day and another loss to Alphabet. Wave the white flag.

Each loss leads to the need for more funding.

More funding has brought on more losses for Uber in a vicious cycle that has seen Uber's valuation slip at the last round of financing.

In the next five years, onlookers can expect much of the same from Uber - underperformance in the form of accelerated losses from its core ride-sharing business.

Capital is disappearing into a black hole and the monetization of Uber Eats and Jump is nothing about which to boast.

These are side businesses at best.

The road map is wishy-washy at best. Uber's Elevate division could turn out to be lipstick on a pig hyping up the company for its 2019 IPO to attract more dollars - the same reason it needs to recruit a new CFO.

The IPO road show will give Uber a platform to explain how it plans to curtail losses. A miracle is required for Uber to finally turn into a profitable business by the time it goes public.

To visit Uber's Elevate division to watch a video of its version of the future of aerial taxis, please click here.

"A computer once beat me at chess, but it was no match for me at kickboxing." - said American comedian Emo Philips.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Uber-image-1-e1526328288895.jpg324580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-15 01:05:442018-05-15 01:05:44Hard Times at Uber

No, I'm not making this recommendation because they let you park your RV in their parking lots at night for free.

And no, I'm not smoking California's biggest cash crop either (it's not grapes).

I predicted as much in my recent research piece, "Who Will Be the Next FANG?" by clicking here.

It is the dawn of a new era with the world absorbing yet another FANG to add to the list of Facebook (FB), Alphabet (GOOGL), Amazon (AMZN), and Netflix (NFLX).

As the tech world powers on to new heights, nothing can slow down these juggernauts.

Let's face it - companies are more lucrative when technical expertise is ramped up and infused into the business model.

Ground zero of the tech movement - Silicon Valley - has helped supercharge the economy and prodigious earnings' results support this thesis.

New innovations will fuel the next level up in the tech arm's race but more crucially, so will new geographical locations.

Instead of throwing a dart at a world map, the locations are a no-brainer because tech scavenger hunts orbit around one idiosyncrasy and that is scale.

Scalability is a sacred word in the tech world.

If a start-up cannot scale up, investors can't imagine future profits, entrepreneurs can't imagine growth, and funding dries up.

End of story.

For instance, Amazon's business model does not mesh kindly with pint-sized Iceland.

Not because Amazon discriminates against Iceland's culinary delicacy of sheep testicles but because the population is only around 330,000 people.

Scale equals success.

Indisputably, every country with an Amazon-esque business is being bid up because big tech firms know how to digitally monetize, effectively out-sourcing an incredibly profitable business model that has worked unabated for the developed world for the past decade or two.

The heightened awareness of existential survival is pitting foreign money against each other in far-flung places jostling for the same digital assets after a decade of cheap financing enriching tech companies.

Remember that first mover advantage leads to dominance in the datasphere because the volume of data is directly correlated to the bottom line.

Examples are rife around the world, for instance Amazon's $580 million purchase of Souq.com, described as the Amazon of the Middle East headquartered in Dubai and the biggest e-commerce site in the Arab world.

E-commerce commands a paltry 2% of sales in the region. That number is poised to explode as digital-savvy, tech Millennials reach peak consuming age and the migration to mobile erupts.

A preemptive strike is usually the most compelling strategy for large cap tech as it pushes out the smaller players, which lack the resources to compete.

Even the corporate offices of Walmart (WMT) in Bentonville, Arkansas, would wholeheartedly agree with me after doling out for its new toy.

Yes, Walmart acquired a 77% share in the Amazon of India, Flipkart, for $16 billion after the real Amazon failed to cut a deal with the most famous e-commerce unicorn in India.

This new development is a game changer.

India is a country that tech executives pinpoint as the future because of its massive population, economic growth, and economic potential foreign investors hope to tap up.

The International Monetary Fund (IMF) has anointed India as the fastest growing economy in 2018, and the 7.4% growth this year will follow with an even sturdier 7.8% in 2019.

Amazon has been well aware of India's ascent. Its CEO Jeff Bezos pledged to invest more than $5 billion in India and Amazon began its e-commerce operation in 2013.

Amazon's early entrance into the Indian e-commerce industry has paid off grabbing 31% of market share putting it in second place behind Flipkart's 40%, according to big data firms.

The Indian e-commerce space was $20 billion in 2017, and by 2019, expect that number to grow to $35 billion.

Walmart CEO Doug McMillon noted that by 2026, the Indian e-commerce industry will surpass $200 billion. When it comes to clothing and fashion, Flipkart has a 70% share in India.

Even more valuable than the economic growth is the new pipeline of tech talent that will help Walmart compete with Amazon.

The Trump administration's crackdown on H-1B visas that Silicon Valley utilizes to bring developers to American shores has forced American tech companies to implement a work-around.

Essentially, the only difference now will be that the past recipients of H-1B visas will be sitting in an air-conditioned office in Bengaluru, India, until the visa documents come through.

Flipkart has a deep pipeline into the best engineering schools in India and the staff of more than 30,000 employees work on Indian wage levels.

This deal is one of the biggest talent grabs of tech developers the world has ever seen. And this group has the know-how of building an Amazon-style digital marketplace platform from zero.

The Flipkart investment comes after Walmart's purchase of Jet.com, an e-commerce company based in Hoboken, New Jersey.

The $3.3 billion purchase of Jet.com in 2016 was the beginning of Walmart's digital strategy, and it has come a long way in a very short time.

Walmart is now a vaunted member of the FANG group and has a new army of developers to back up this claim.

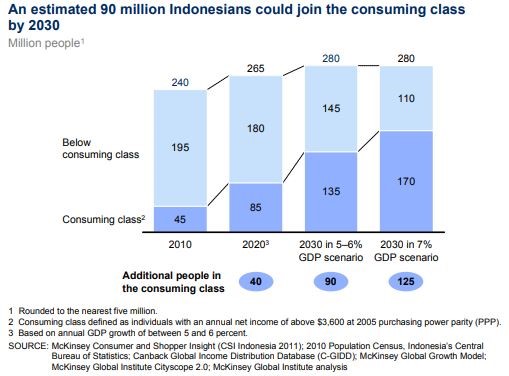

Glancing at the opportunities to scale, Indonesia is clearly the runner-up behind India.

Indonesia has been tagged as a tech new battleground with a population of 260 million in 2016 and growing.

The country has a medium age of 28, meaning this young population could turn into a reliable source of new tech developers who traditionally are young and digital natives.

Economic prosperity has been welcomed with open arms to this tropical island nation. It is poised to become the seventh largest economy by 2030, up from its rank of No. 16 today, creating a burgeoning middle class with newfangled discretionary spending.

The rural migration to urban environments will add another 90 million people living in Indonesian cities by 2030, while Internet access is growing by 20% each year in Indonesia.

Goldman Sachs recently issued a note to investors citing Indonesia's unbridled potential.

Capital is pouring into Indonesia at a breakneck speed with Alibaba investing $1.1 billion into Tokopedia, the Amazon of Indonesia.

Companies are coming to the stark realization that the domestic low hanging fruits have been picked, and aging developed countries are turning to undeveloped regions of growth to advance business objectives.

This is why South East Asia has been bombarded with an onslaught of Japanese, Korean, and Chinese investments and not only in the tech sector.

The Far East powerhouse countries are battling each other in Southeast Asia for consumer goods, infrastructure, high speed trains, and of course technology.

Uber just sold its Southeast Asian ride-sharing asset Grab to China's DiDi Chuxing and SoftBank for $2 billion.

The Southeast Asian region is one of the hottest places to make a deal because of a lack of FANG occupancy.

Walmart sold off on the Flipkart news because of the potential impairment to margins, but this move is a long-term positive for Walmart shareholders.

Flipkart does not turn a profit and Walmart is still solely judged by earnings. Unfortunately, it does not receive the same license to focus on growth like Tesla, Amazon, and Netflix.

However, I have a hunch that down the road, investors will agree this move by Walmart's McMillon was as shrewd as can be.

Like the colonial powers of yore, India and Southeast Asia are likely to be divvied up.

American companies already own more than 70% of market share in India e-commerce.

India is the biggest democracy in Asia and a staunch ally of the United States.

India's frosty relationship with China due to border spats and communist origins will stunt China's ability to take over and expand in India.

However, Southeast Asian countries are more likely to go the way of Cambodia, which is reliant on Chinese money to fund new initiatives, hamstrung by Chinese debt up to its eyeballs, and acquiesced political capital to the Mandarins.

Chinese investment's path of least resistance is Southeast Asia. This progression will be facilitated by the sizable Chinese expat population that resides in Indonesia, Vietnam, Thailand, Philippines, Myanmar, Laos and Cambodia.

Long-term shareholders of Amazon and Walmart will be rewarded. However, expect a few more Indians walking around Bentonville, Seattle, and Hoboken.

"My life is now a constant assessment of whether what's happening in real life is more entertaining than what's happening on my phone." - said television host Damien Fahey.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Flipkart-image-4-e1526071908849.jpg263509MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-14 01:05:032018-05-14 01:05:03Meet the New FANG

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.